Andreas Park PRO

Professor of Finance at UofT

Andreas Park

Traditional Markets

What is Market Microstructure?

Broker

Exchange

Internalizer

Wholeseller

Darkpool

Venue

Settlement

Traditional Institutions

Investors

Trading Arrangements

central limit order book

complexity

price impact of trades

anonymity

price discovery

centralized auction

bilateral

negotiation

Request

for Quote

open

outcry

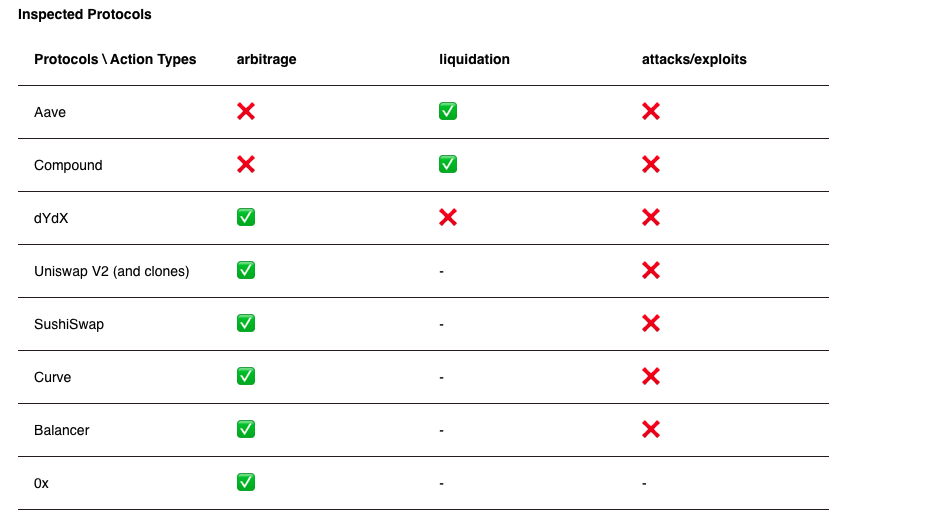

Who trades?

Key question for liquidity provision

Seminal papers

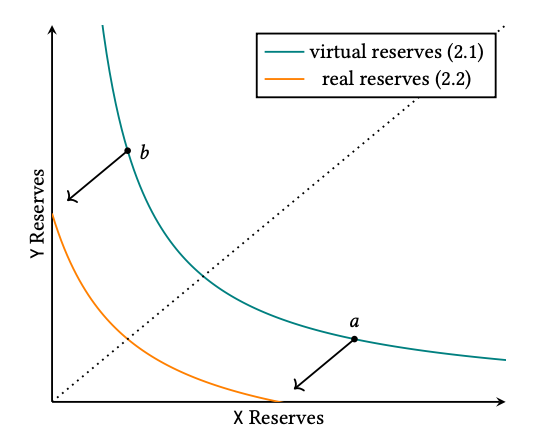

What's there first? Orders or Liquidity?

Seminal papers

Basics of liquidity provision under value uncertainty

Questions:

every model has some form of structure like

\[\text{trading income (fees, spreads, etc)} +\underbrace{\text{what I sold it for}-\text{value of net position}}_{\text{positional gain/loss}} \ge \text{outside option} \]

Example 1: Grossman/Miller

Example 2: Kyle or Glosten-Milgrom

Example 3: Limit order market (a la Glosten 1994)

Crypto vs TradFi Markets

Key Differences Defi vs TradiFi

Broker

Exchange

Internalizer

Wholeseller

Darkpool

Venue

Settlement

Investor

Centralized Trading

BTC/USD

ask: 7,600

bid: 7,550

BTC/USD

ask: 7,500

bid: 7,450

buy BTC

sell BTC

move BTC to Kraken

Crypto Wash Trading, Lin William Cong, Xi Li, Ke Tang, Yang Yang

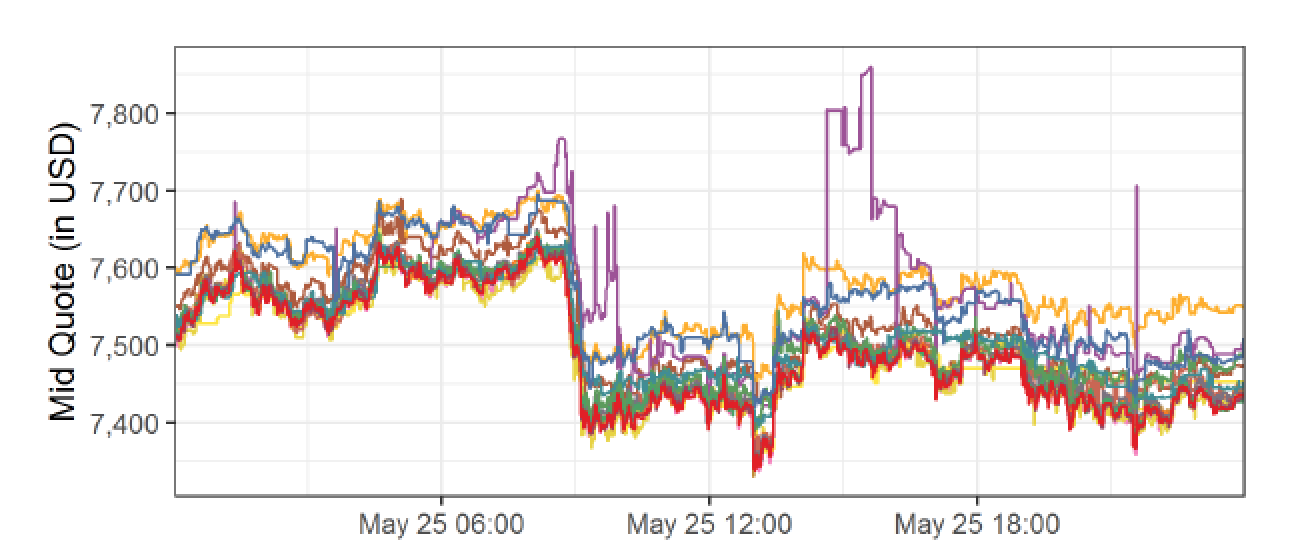

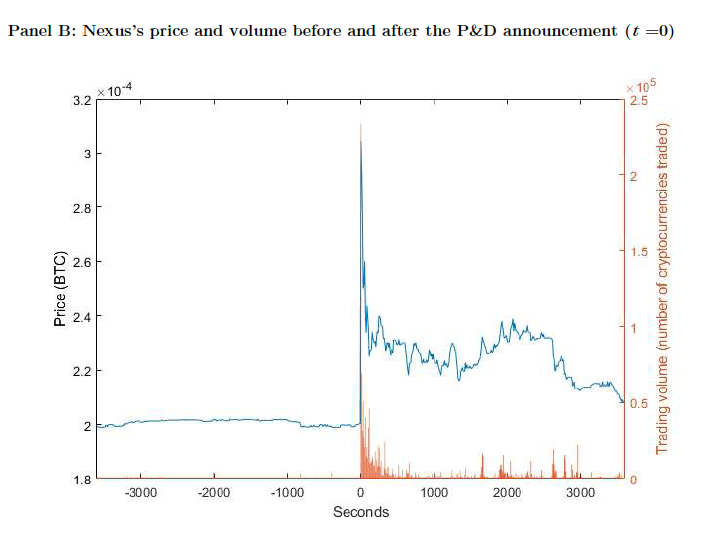

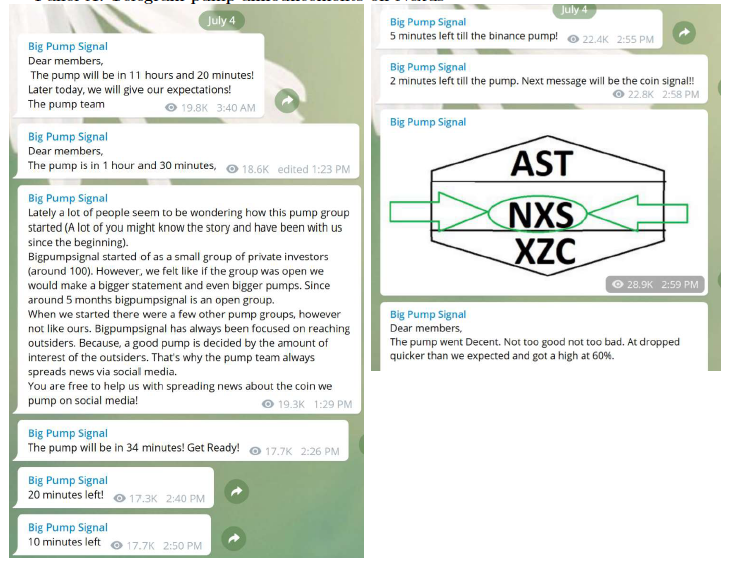

What is pump and dump?

arranged via Telegram Channels

August 2016

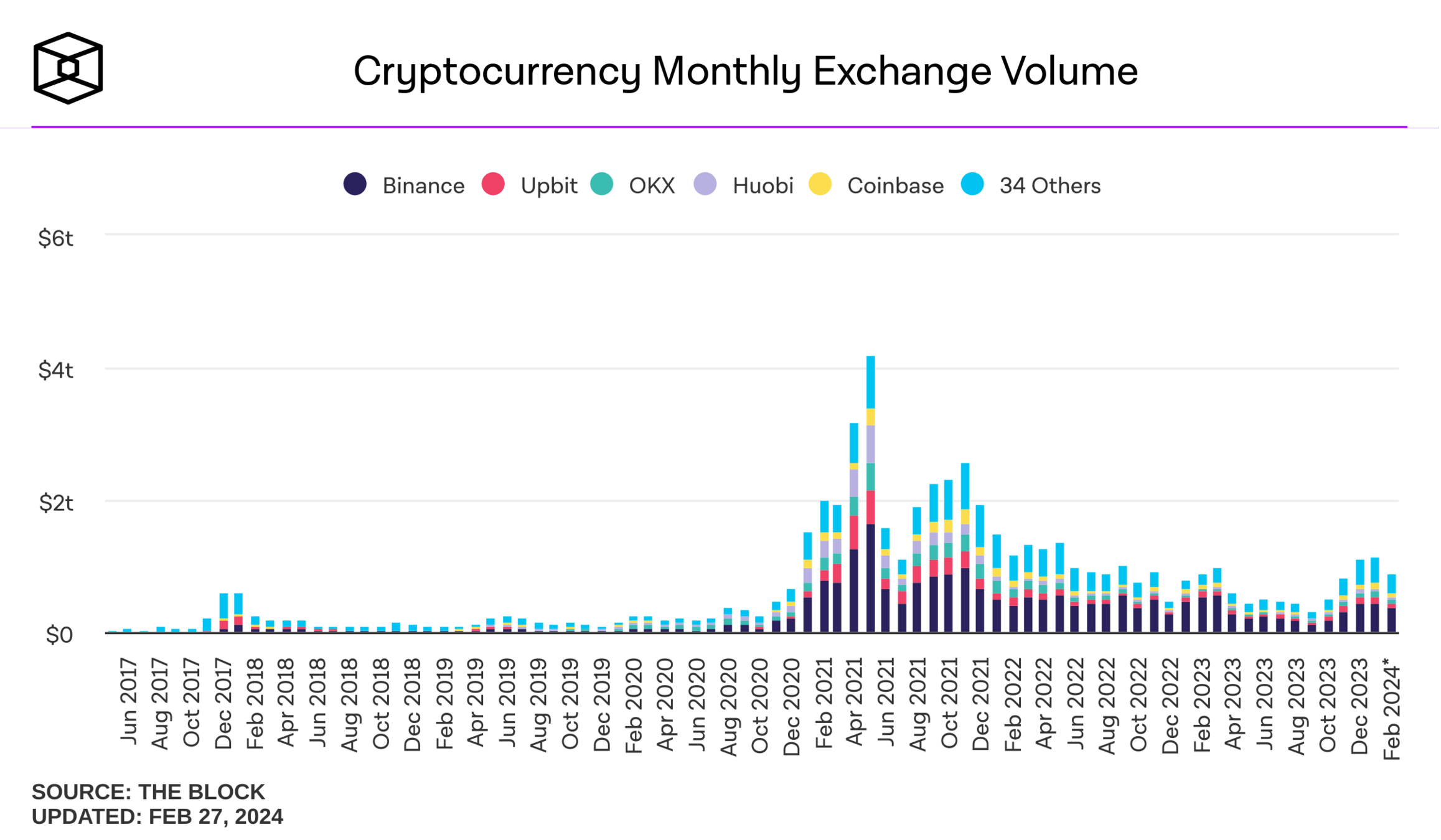

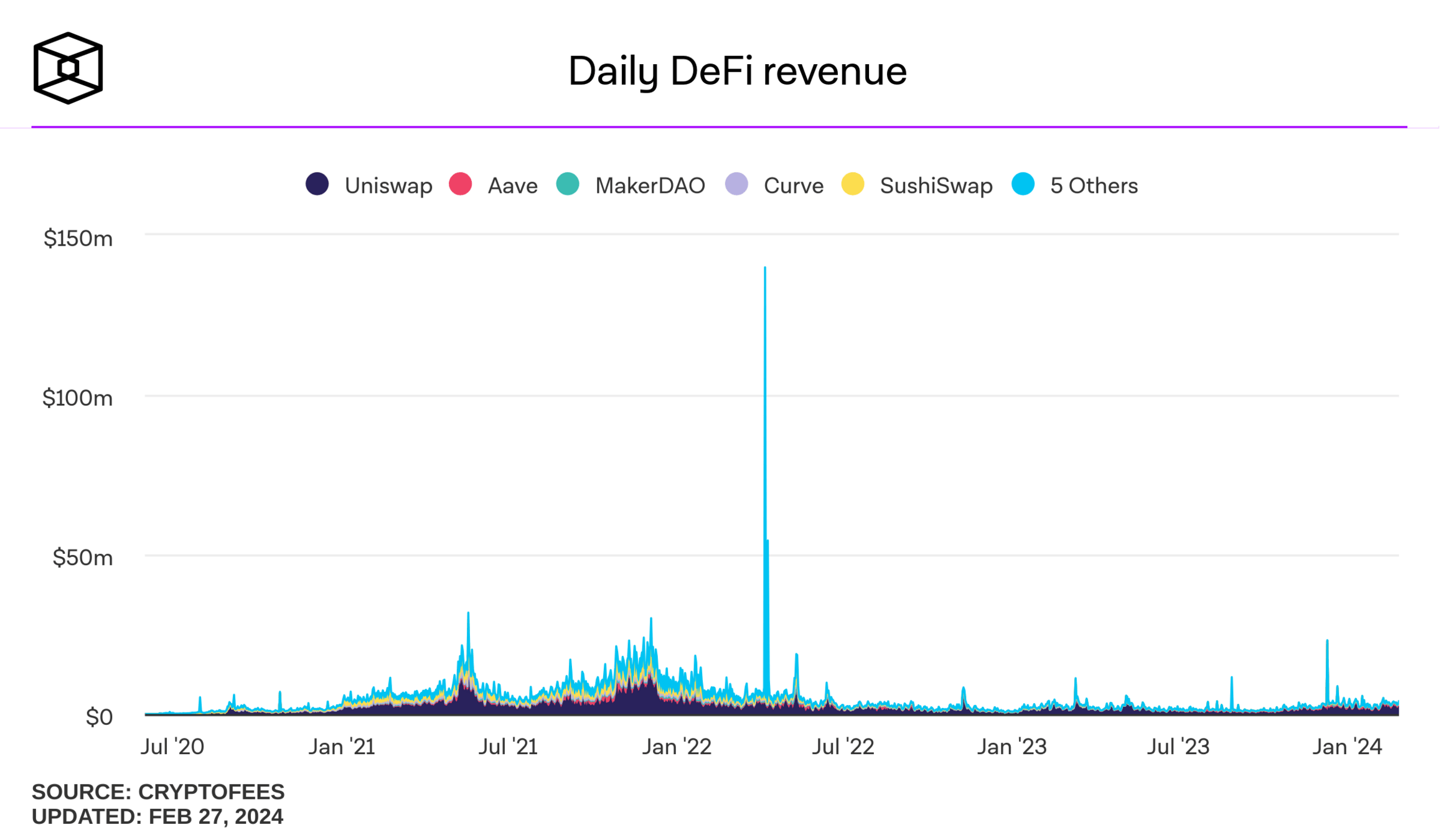

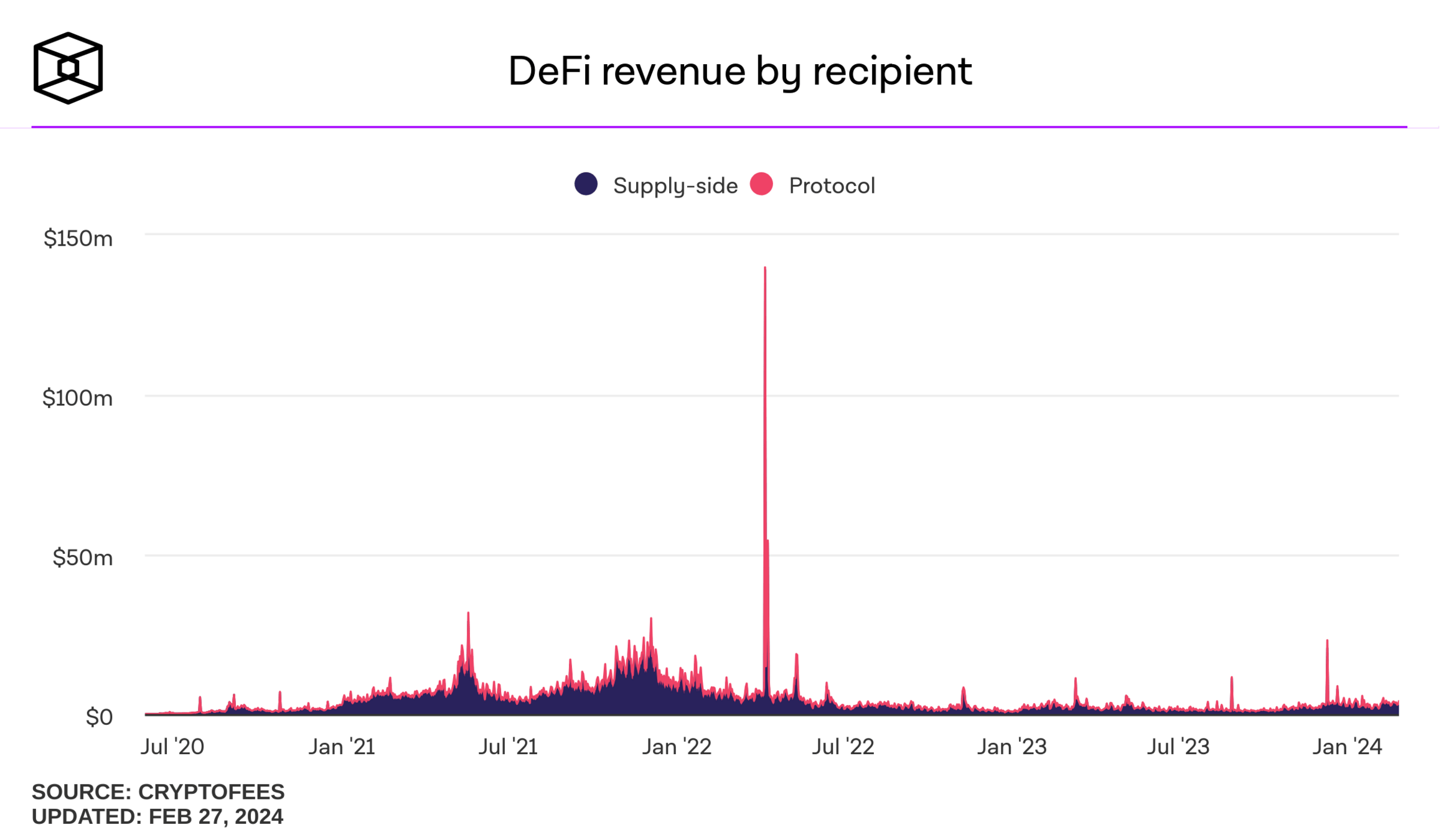

Decentralized Trading

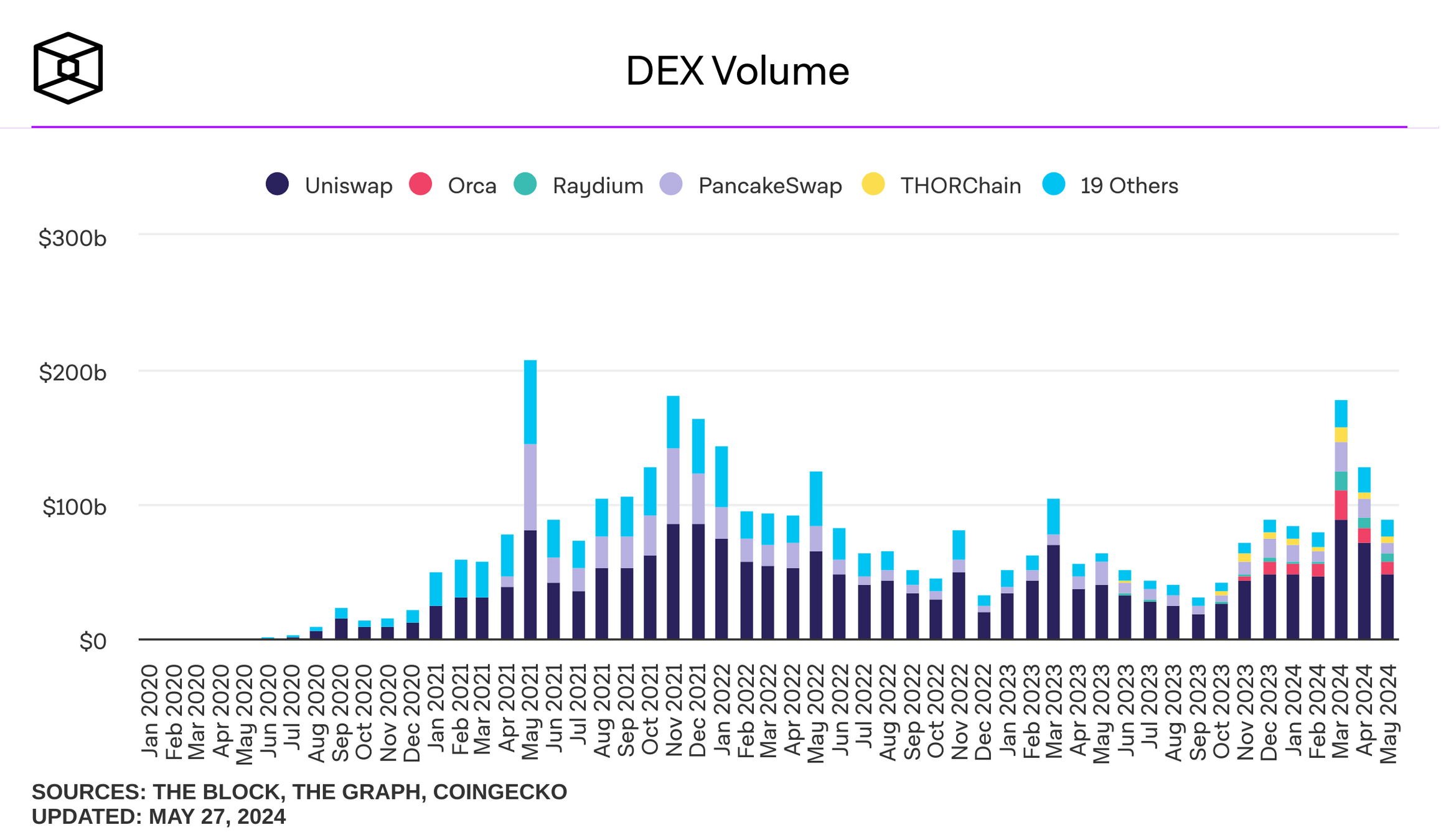

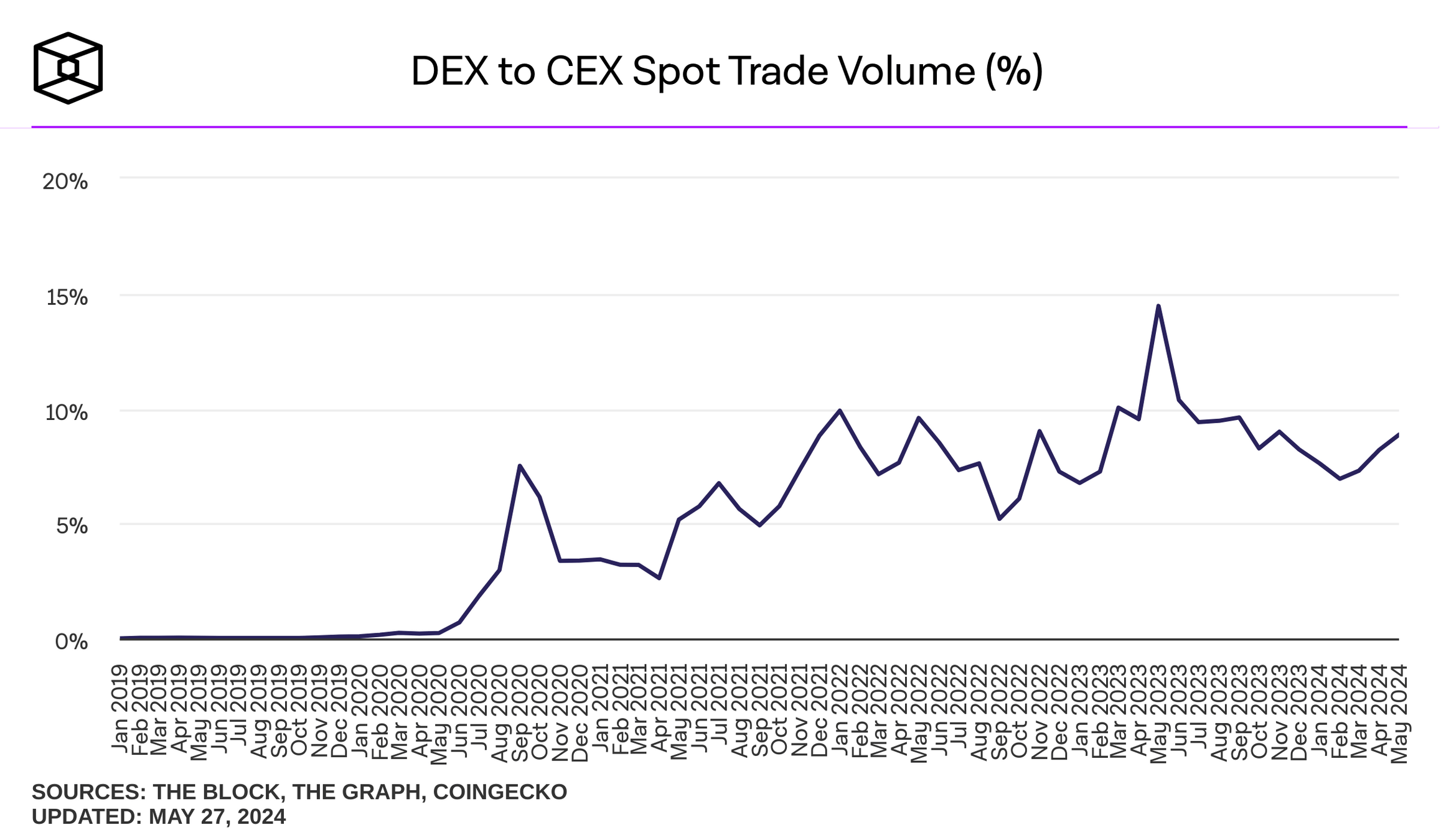

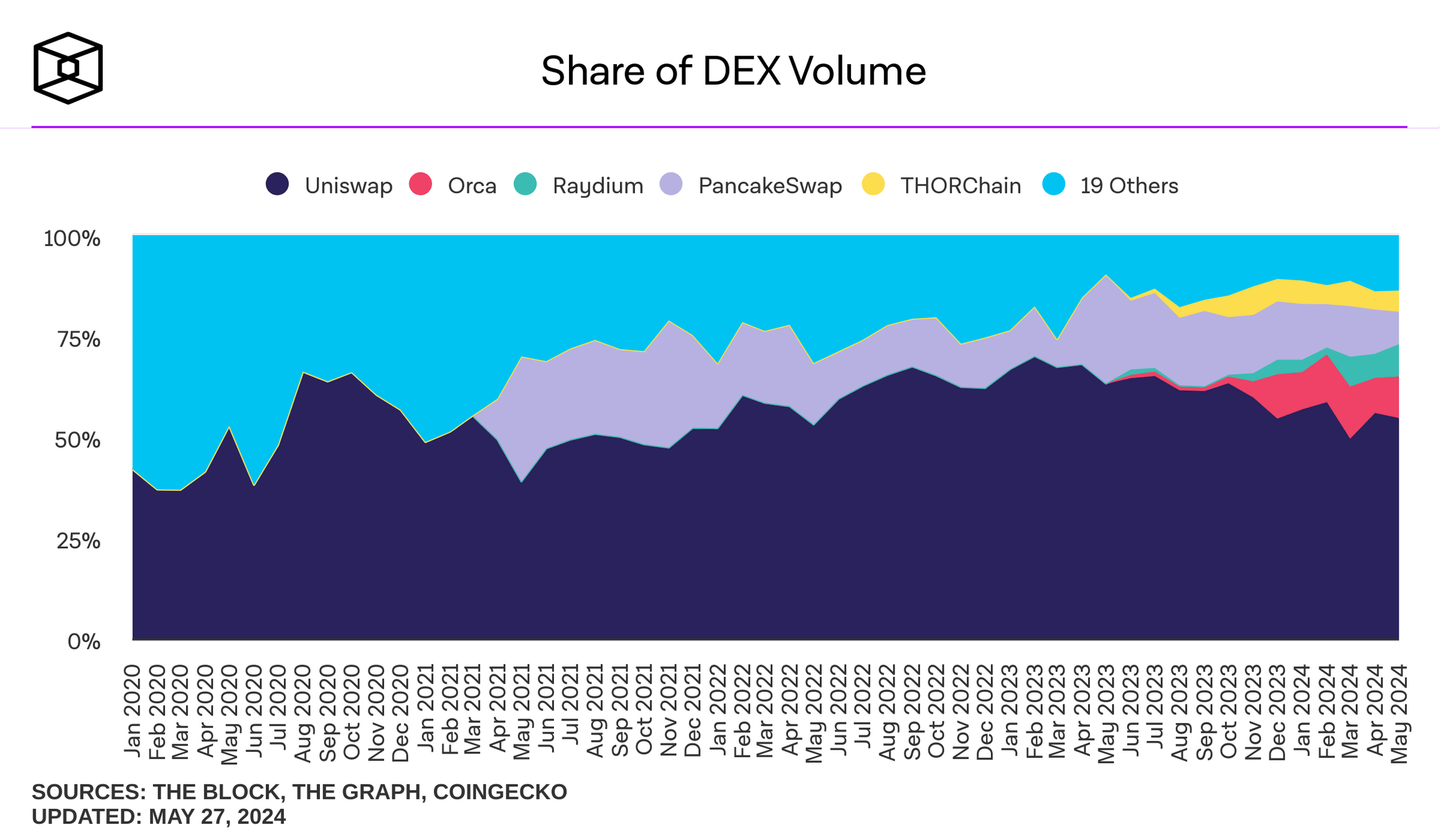

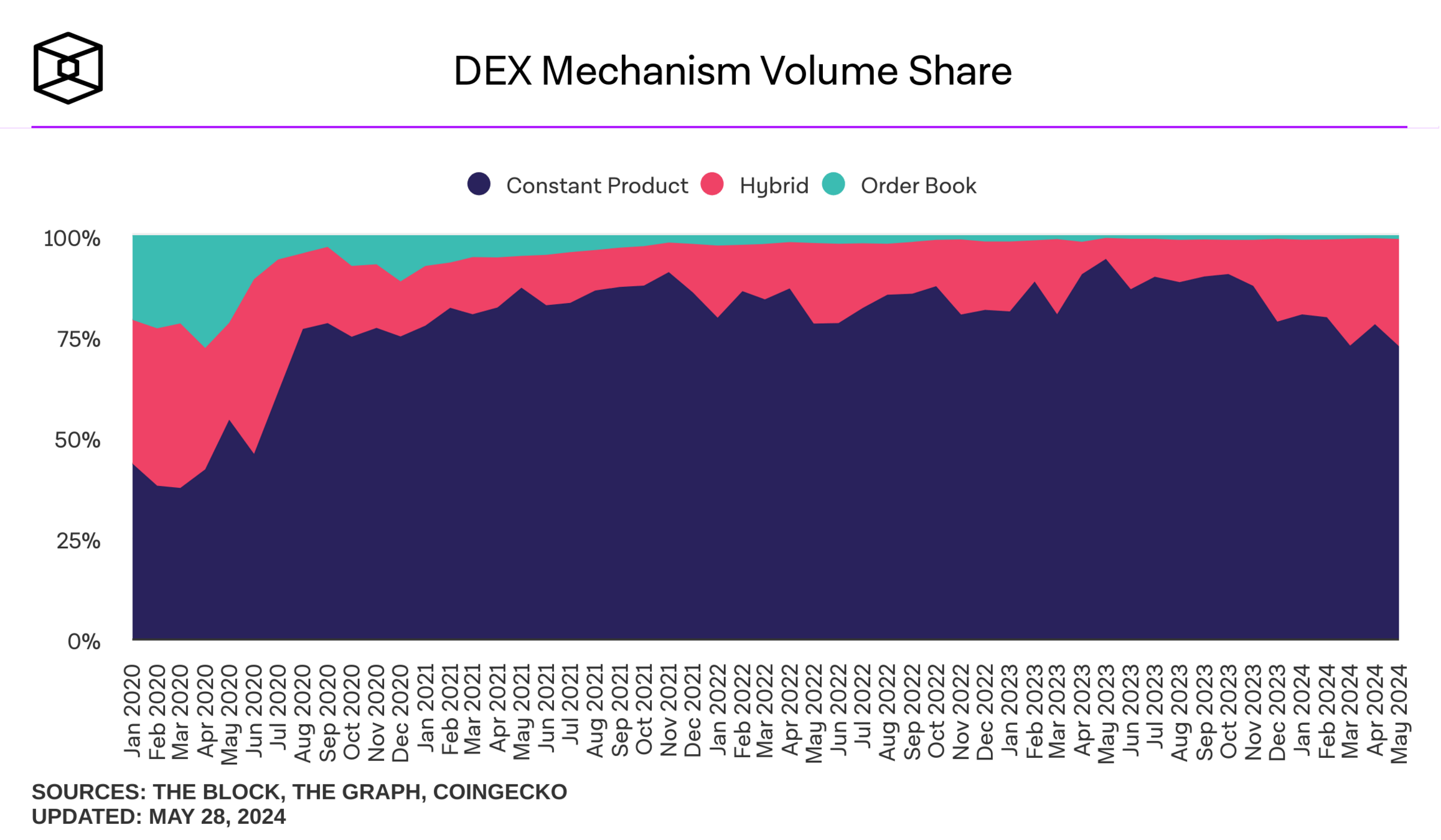

where do I find these plots? theblock.co/data/

Liquidity providers

Liquidity demander

Liquidity Pool

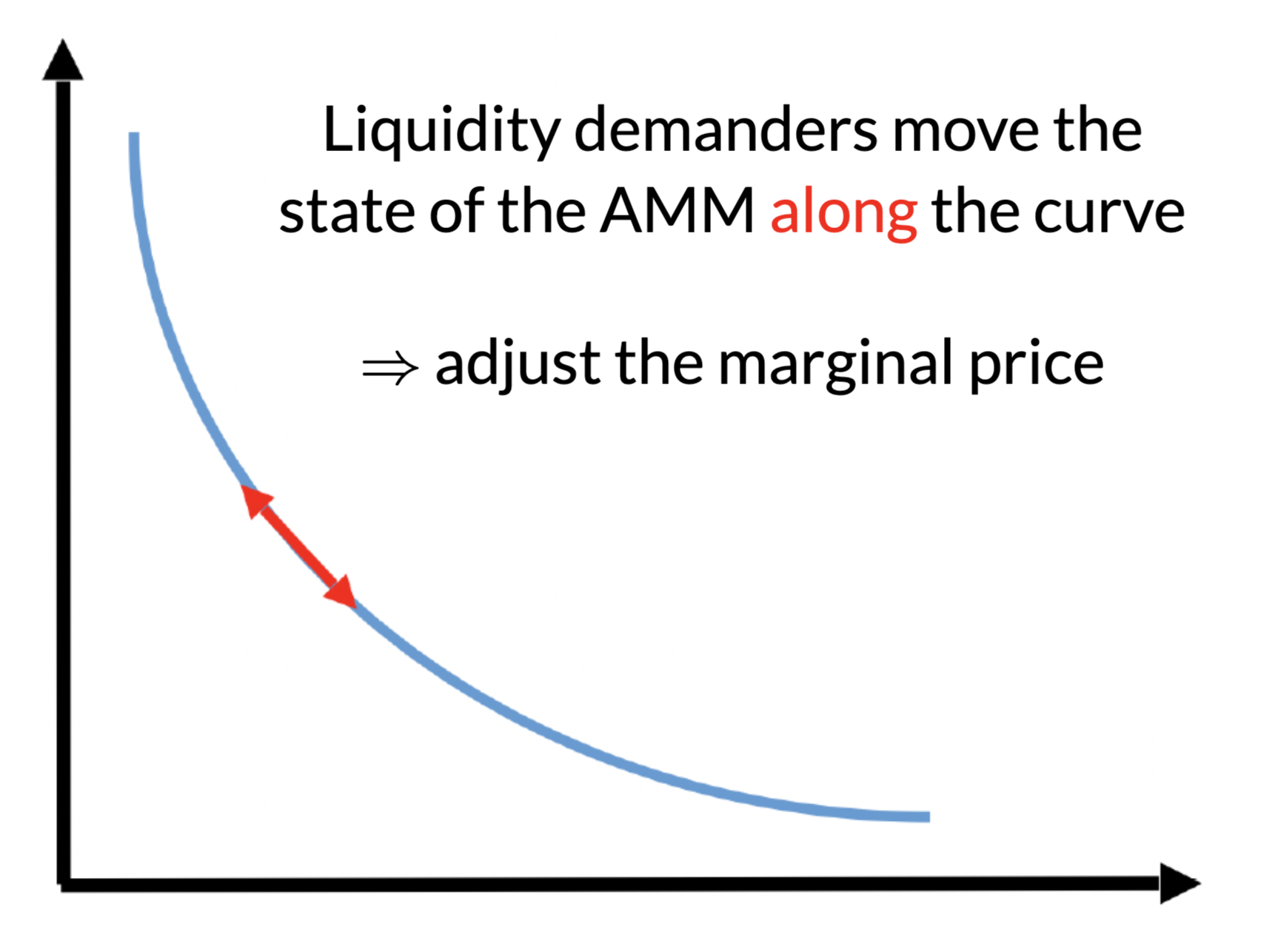

AMM pricing is mechanical:

No effect on the marginal price

| limit order book | periodic auctions | AMM | |

|---|---|---|---|

| continuous trading |

|||

| price discovery with orders | |||

| risk sharing |

|||

| passive liquidity provision | |||

| price continuity |

|||

| continuous liquidity | |||

| sniping prevented |

AMM Theory: The Price Function

Basic Requirements

What does an AMM need?

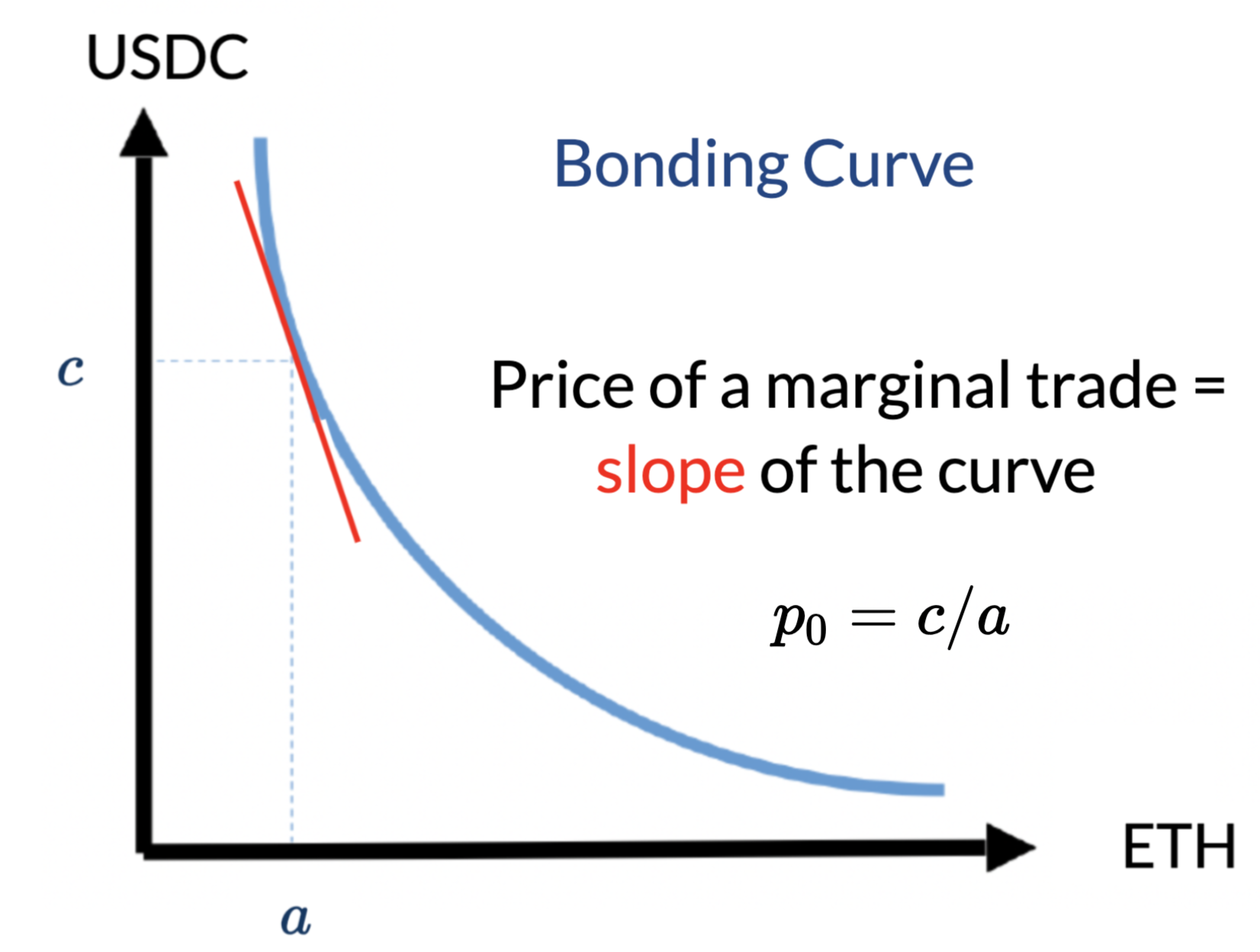

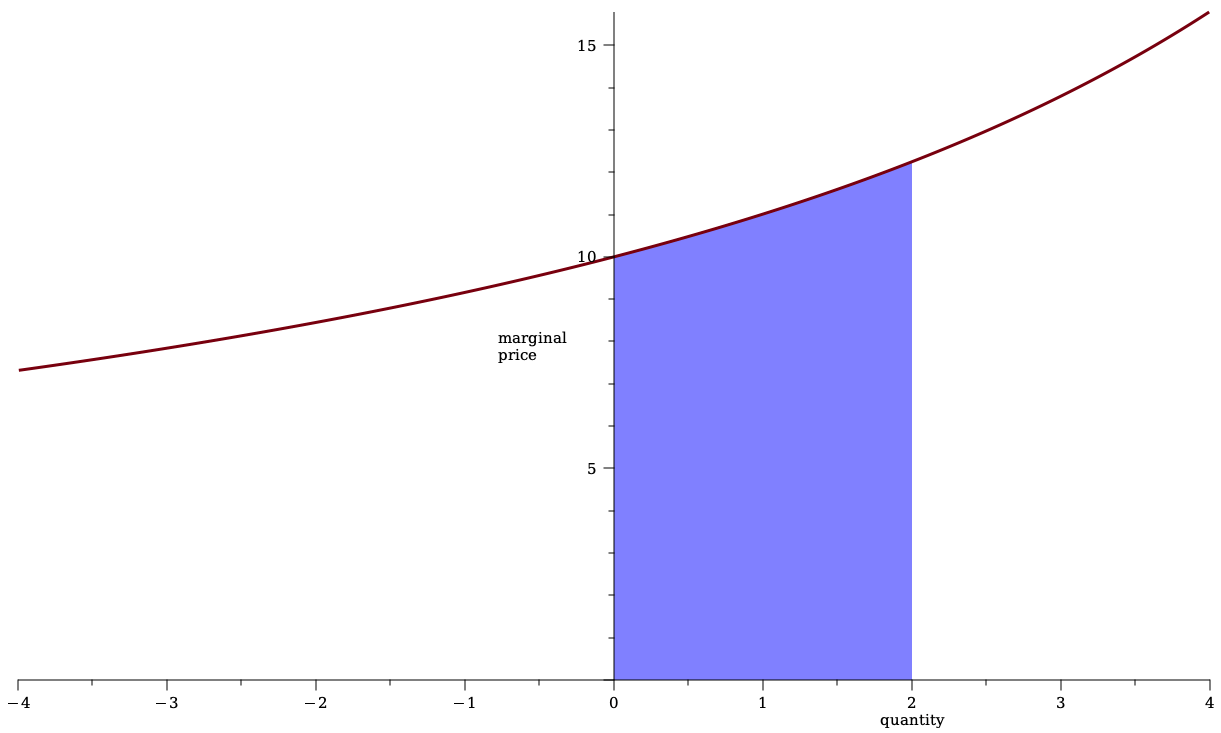

quantity

price

\(q\)

\(p^m(q)\)

\(\Delta c(q)(Q)=p(q)^m\times q\)

Traditional pricing: auctions/open outcry/RFQ: uniform price

idea: cost of \(q=\) price\(\times\) quantity

Some Pricing Rules from Traditional Markets: Uniform Price

\(q=2\)

\(\Delta c(q)= q\times p^m(q)=2\times 15.5\)

Main pricing rule in stock exchanges: limit order book

quantity

price

\(q\)

\(p^m(q)\)

\(\Delta c(q)=\int_0^qp^m(s)~ds\)

Some Pricing Rules from Traditional Markets: Limit Order Book

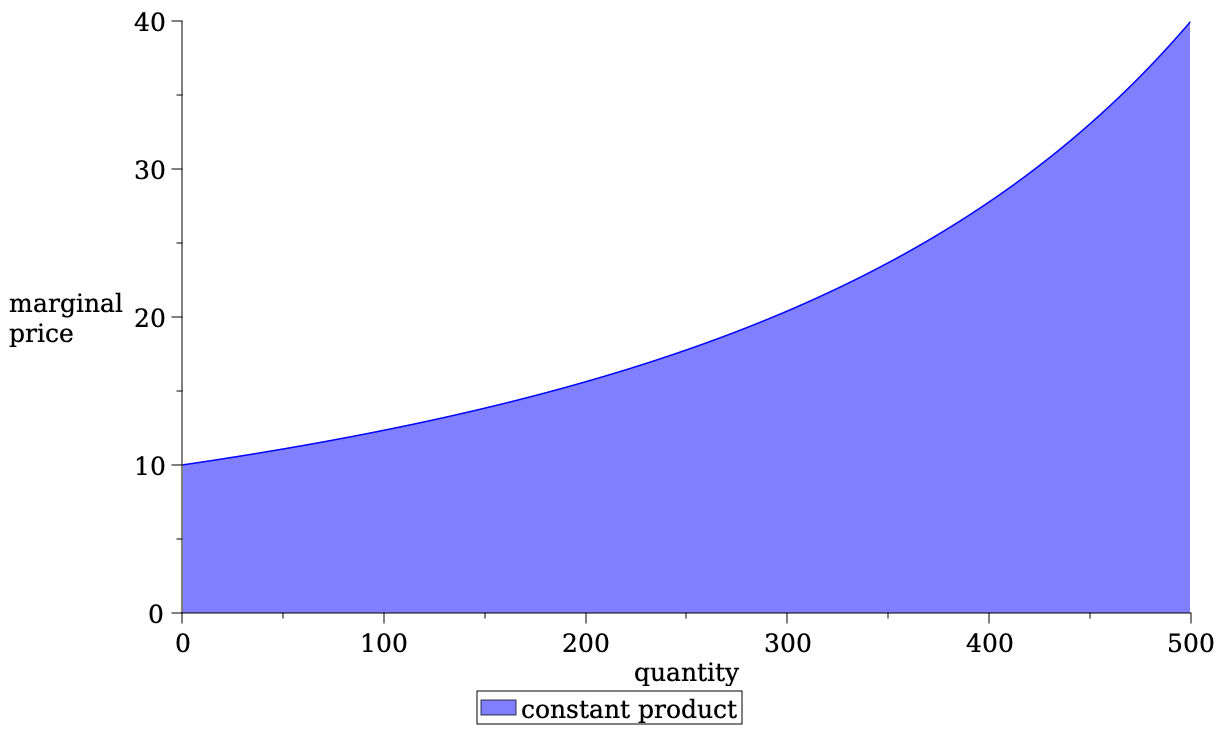

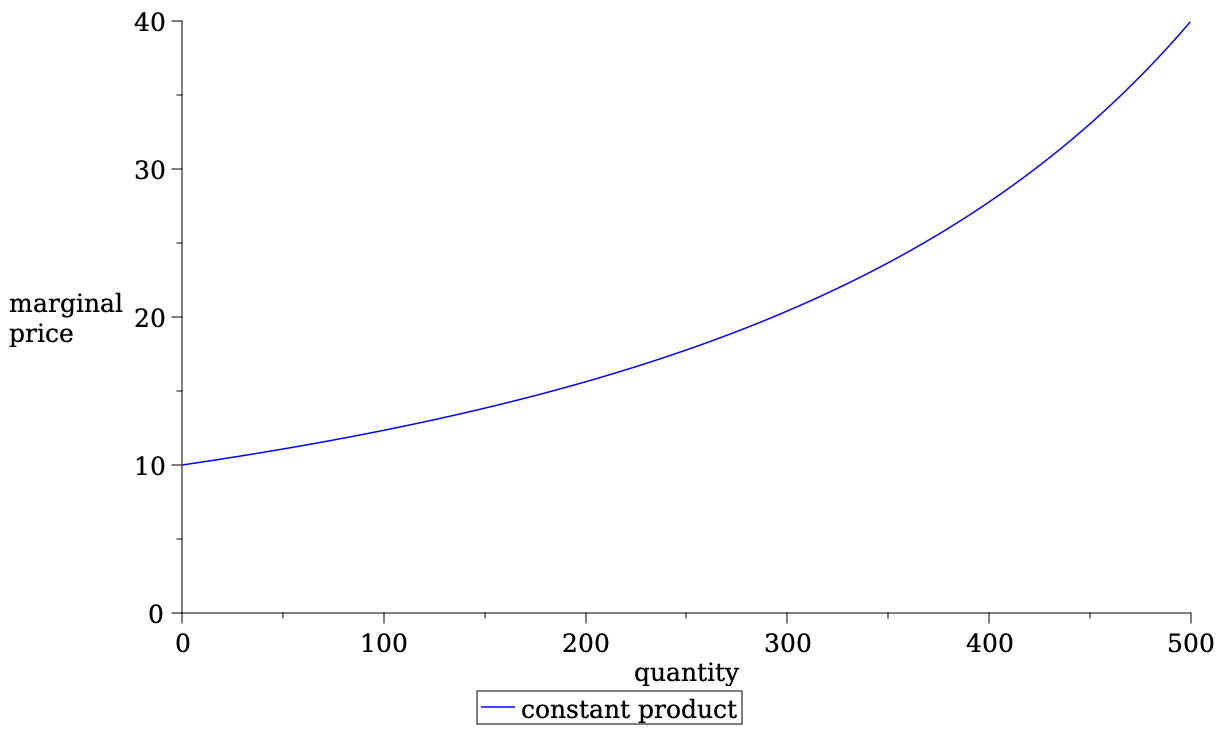

Most Common Pricing Rule in DeFi: Constant Product

Most Common Pricing Rule in DeFi: Constant Product

Insight: AMM pricing function is the same as a limit order book when we require

Some insights on pricing functions

The Pricing Function

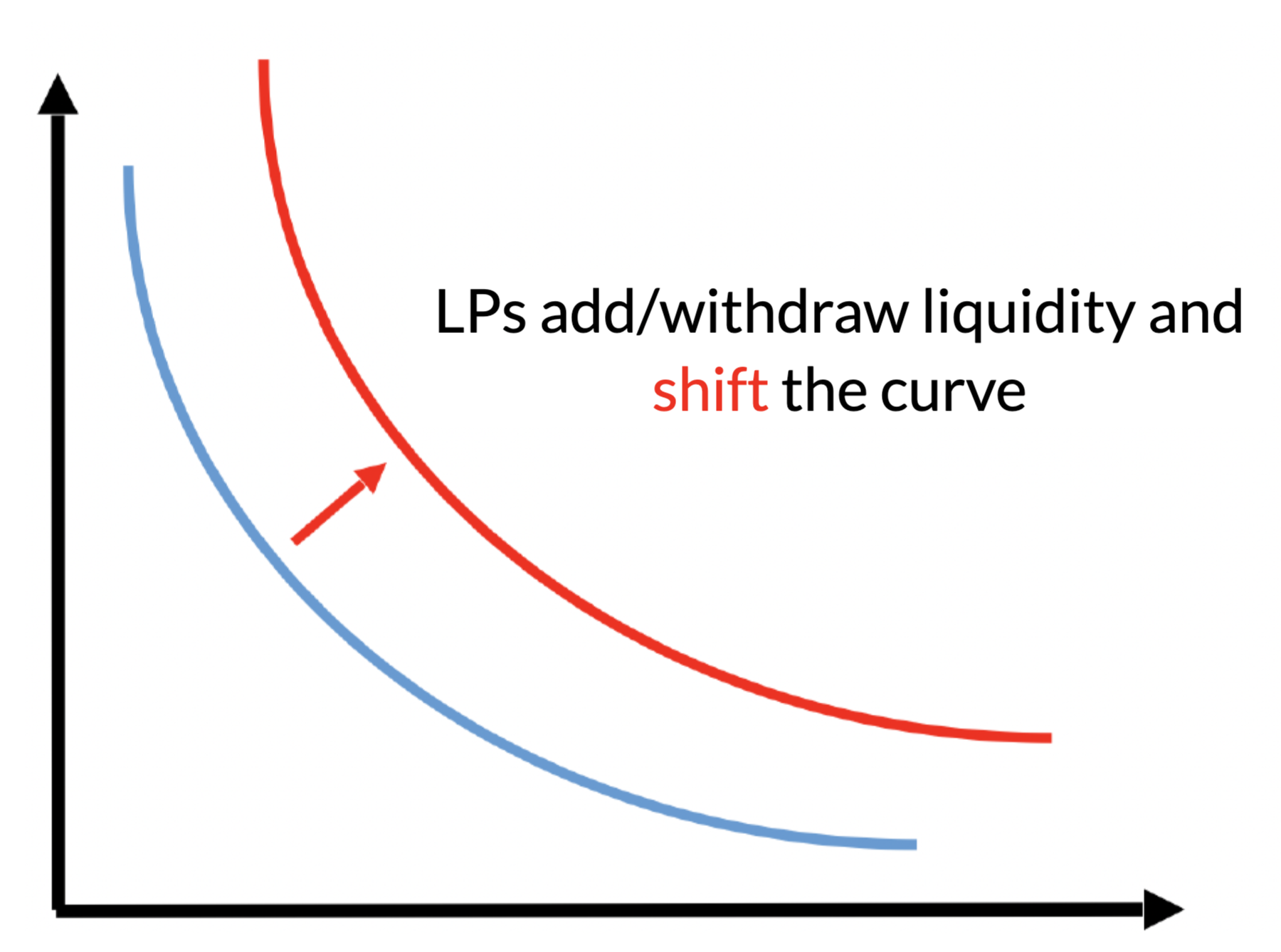

Liquidity Supply and Demand in an Automated Market Maker

Liquidity providers: positional losses

Buy and hold

Provided liquidity

in the pool

Two views

Basics of Liquidity Provision

\[\underbrace{F \int DV \mu(DV) }_{\text{fees earned on}\atop \text{balanced flow}}+\int_0^\infty\underbrace{(\Delta c(q^*)-q^*p_t(R)}_{\text{adverse selection loss} \atop \text{when the return is {\it R}}} +\underbrace{F \cdot \Delta c(q^*))}_{\text{fees earned}\atop \text{from arbitrageurs}}~\phi(R)dR \ge 0.\]

\(q^* \) is what arbitrageurs trade to move the price to reflect \(R\)

Basic idea of liquidity provision: earn more on balanced flow than what you lose on price movement

\[\text{fee income} +\underbrace{\text{what I sold it for}-\text{value of net position}}_{\text{adverse selection loss}} \ge \text{cost of capital} \]

in AMMs:

protocol fee

in tradFi: bid-ask spread

Theory Literature on AMM

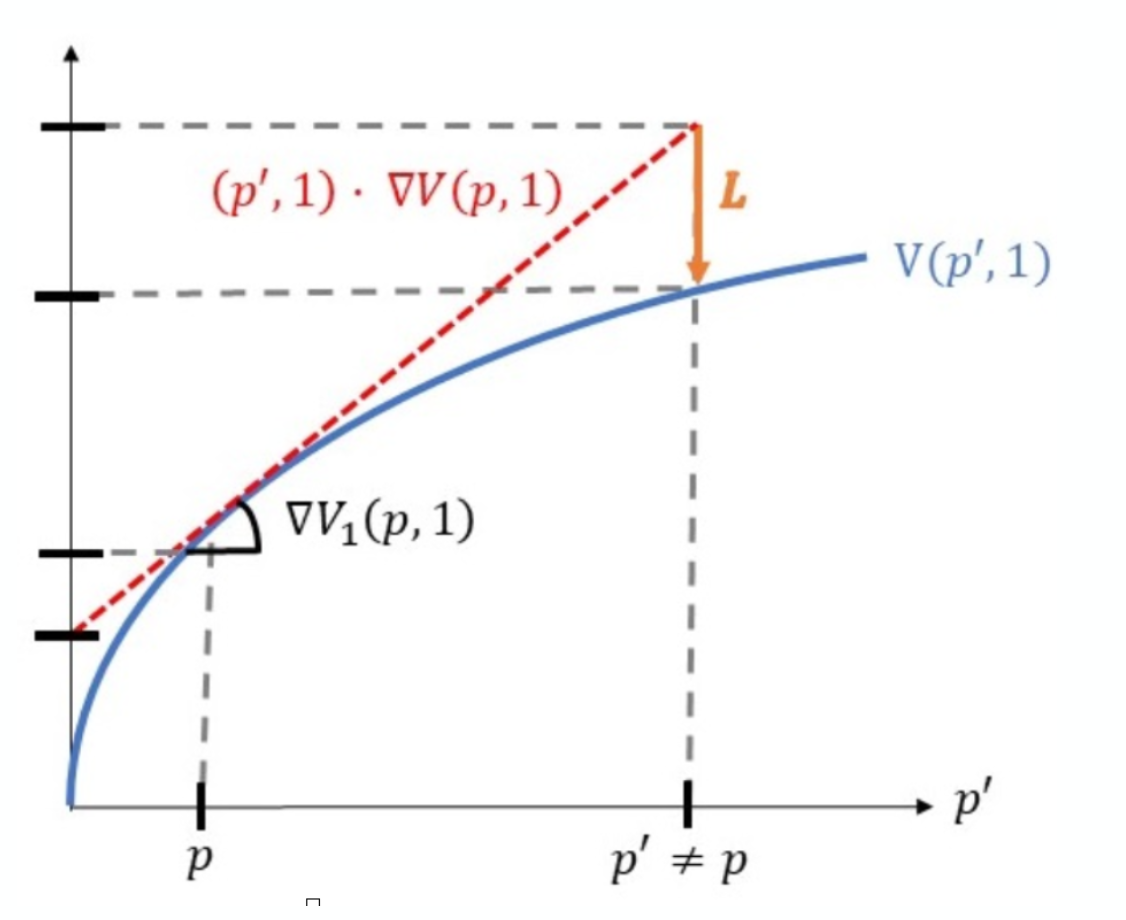

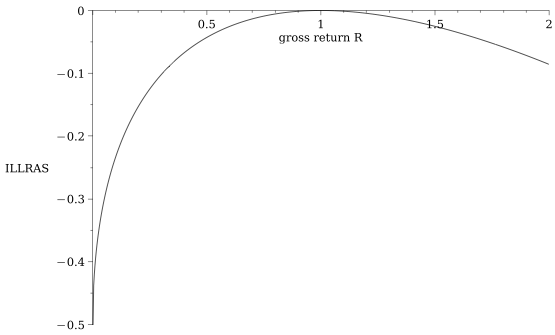

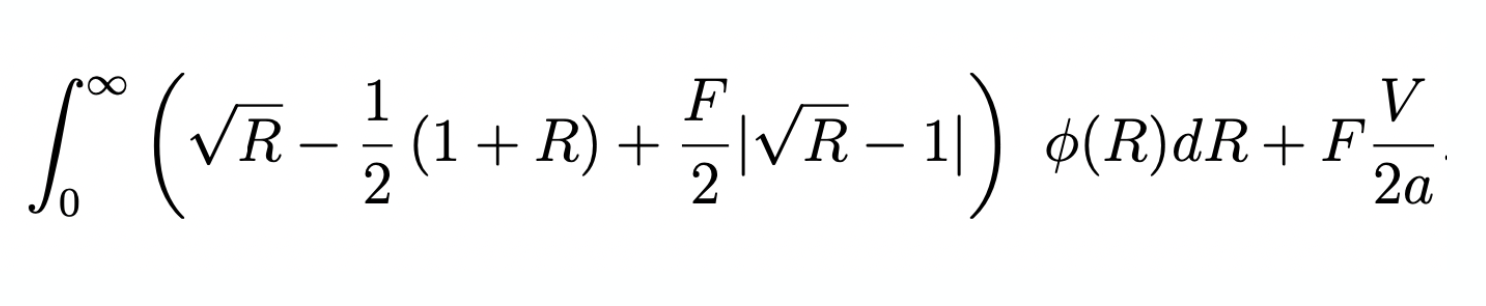

Sidebar: we can quantify how much a PASSIVE LP loses when the price moves by \(R\)

for orientation:

\[\frac{\text{adverse selection loss when the return is \(R\)}}{\text{initial deposit}}=\sqrt{R}-\frac{1}{2}(R+1)\]

see Barbon & Ranaldo (2022)

Liquidity Demander's Decision & (optimal) AMM Fees

Result:

competitive liq provision\(\to\) there exists an optimal (min trading costs) fee \(>0\)

Similar to Lehar&Parlour (2023) and Hasbrouck, Riviera, Saleh (2023)

\[F^\pi=\frac{1}{E[|\sqrt{R}-1|/2]+V}\left(-2q\ E[\text{position loss}]+ \sqrt{-2qV\ E[\text{position loss}]}\right).\]

assume: liquidity providers add liquidity until they break even in expectation

Empirical Work

Lehar and Parlour (2021)

Barbon & Ranaldo (2023)

Other notables:

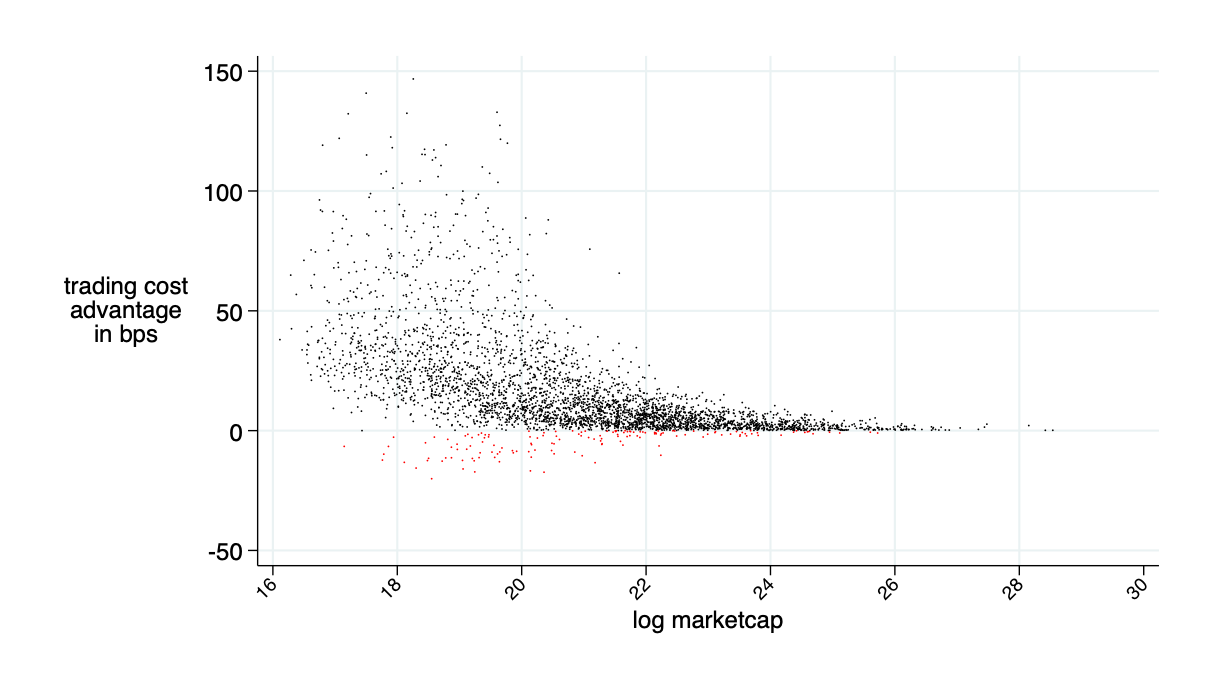

Malinova & Park (2023): AMM applied to equities would reduce trading costs by 30%

UniSwap v3

UniSwap v3 has "concentrated liquidity provision"

Just a little more institutional details

users submit liquidity positions \((u,d,p_u,p_d)\) and receive an ERC-721 (=NFT) token as a receipt

the code segments liquidity into discrete exponential intervals \([p_k,p_{k+1}]\) with \[p_k=(1+\delta)^k. ~~~(\text{numerically: }p(k)=1.0001^k)\]

it aggregates liquidity over these intervals

the pricing curve for each interval is determined by the constant product rule

intervals may be "empty"

How the price is determined

How the price is determined

\(p_d\)

\(p_u\)

\(p_0\)

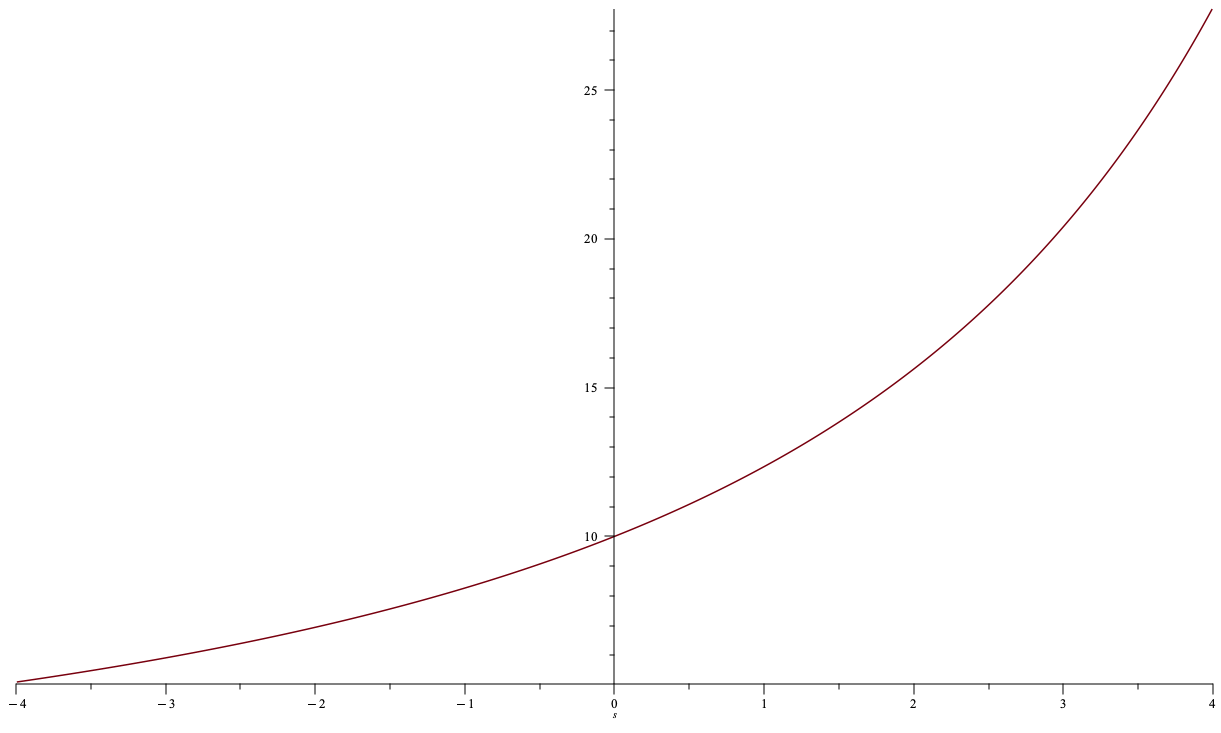

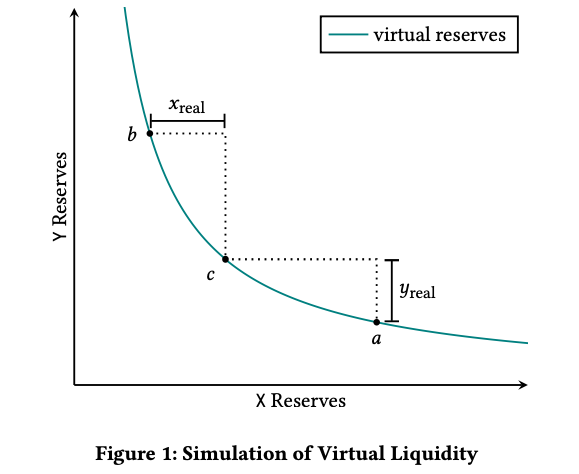

we know this curve has functional form \[p^m(q)=\frac{\tilde{a}c}{(\tilde{a}-c)^2}\]

where \(\tilde{a}\) is the virtual liquidity

quick disclaimer: what follows is not how UniSwap is explained on its website etc. But the resulting maths are the same

More on UniSwap v3

marginal "limit order book" price

\[\gamma(s)=\frac{ac}{(a-s)^2}\]

\(p_u=15\)

\(p_d=7\)

\(u=2\)

\(p_0=10\) (that's exogenous, not a choice)

Finding virtual liquidity factor \(\tilde{a}\)

marginal "limit order book" price

\[\gamma(s)=\frac{ac}{(a-s)^2}\]

\(p_u=15\)

\(p_d=7\)

\(u=2\)

\(p_0=10\) (that's exogenous, not a choice)

= find the right curve

= find the right "\(\tilde{a}\)"

Finding the fourth parameter \(\Delta c(d)\)

marginal "limit order book" price

\[\gamma(s)=\frac{ac}{(a-s)^2}\]

\(p_u=15\)

\(p_d=7\)

\(u=2\)

\(d=?\)

required cash deposit \(\Delta c(d)=\) the amount that I pay for \(d\)

Solutions

Numerical example

Want to read more?

Concerns around Automated Market Makers

a

b

c

d

e

f

g

Problem 1: Public Mempools allow sandwich (MEV) attacks

related paper: “Maximal Extractable Value and Allocative Inefficiencies in Public Blockchains”. A. Capponi, R. Jia, and Y. Wang (2023)

Problem 2: Just-In-Time Liquidity (single trade cream skimming)

X-Router

Liquidity pool

OTC

Problem 2: Just-In-Time Liquidity (at the MEV level)

X-Router

Liquidity pool

searcher/builder

balanced orders

add as much liquidity as possible

withdraw liquidity

unbalanced orders

related paper: Capponi, Jia, and Zhu (2024) "The Paradox of Just-in-Time Liquidity in Decentralized Exchanges: More Providers Can Lead to Less Liquidity"

From Vitalik Buterin's post on the topic:

https://ethresear.ch/t/improving-front-running-resistance-of-x-y-k-market-makers/1281

Theorem (Park 2023):

Hypothetical example

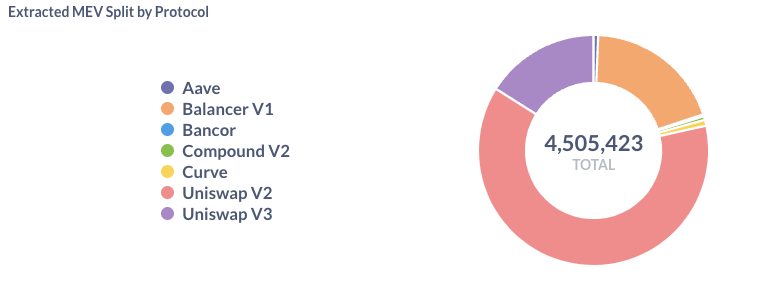

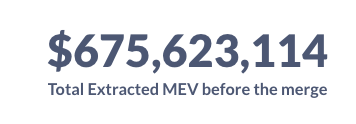

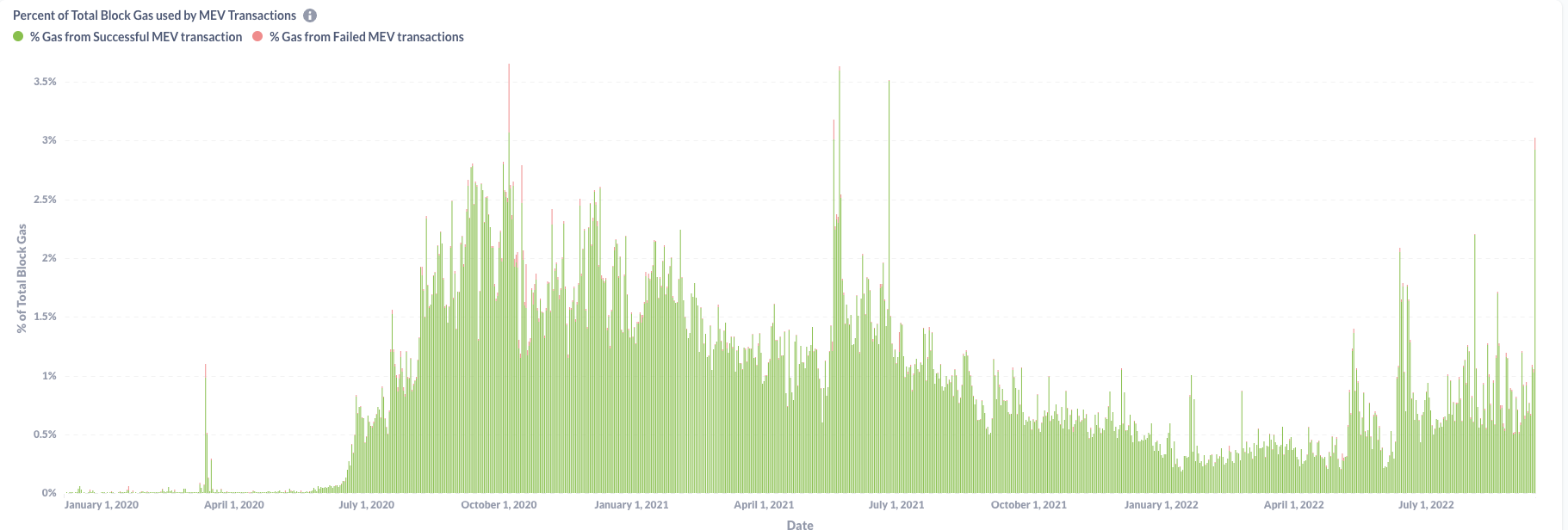

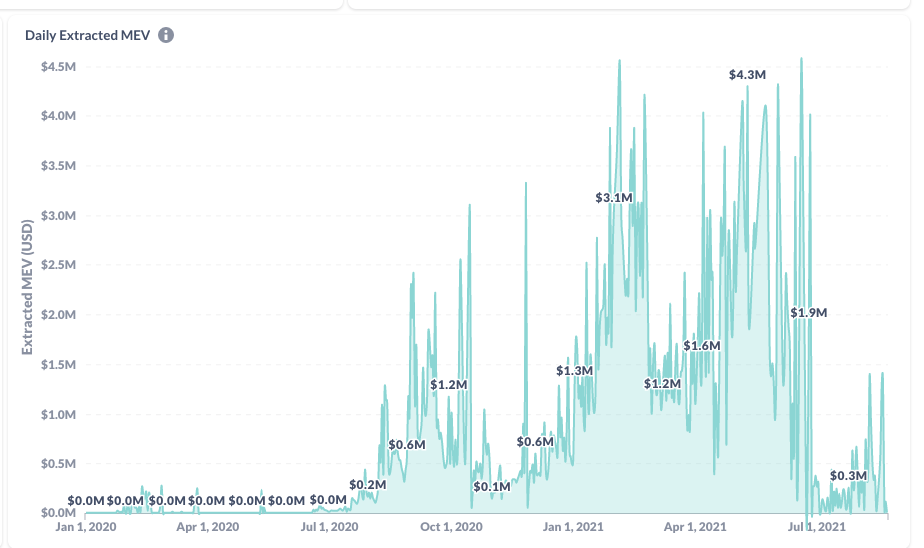

The Bigger Picture: MEV Extraction

read more at: "Battle of the Bots: Flash Loans, Miner Extractable Value and Efficient Settlement", Lehar & Parlour, 2023

The Bigger Picture and Last Words

Last Words

@financeUTM

andreas.park@rotman.utoronto.ca

slides.com/ap248

sites.google.com/site/parkandreas/

youtube.com/user/andreaspark2812/

Literature

AMM Literature: a booming field

Lehar and Parlour (2021): for many parametric configurations, investors prefer AMMs over the limit order market.

Aoyagi and Ito (2021): co-existence of a centralized exchange and an automated market maker; informed traders react non-monotonically to changes in the risky asset’s volatility

Capponi and Jia (2021): price volatility \(\to\) welfare of AMM LPs; conditions for a breakdown of liquidity supply in the automated system; more convex pricing \(\to\) lower arbitrage rents & less trading.

Capponi, Jia, and Wang (2022): decision problems of validators, traders, and MEV bots under the Flashbots protocol.

Park (2021): properties and conceptual challenges for AMM pricing functions

Milionis, Moallemi, Roughgarden, and Zhang (2022): dynamic impermanent loss analysis for under constant product pricing.

Hasbrouck, Rivera, and Saleh (2022): higher fee \(\Rightarrow\) higher volume

Empirics:

Lehar and Parlour (2021): price discovery better on AMMs

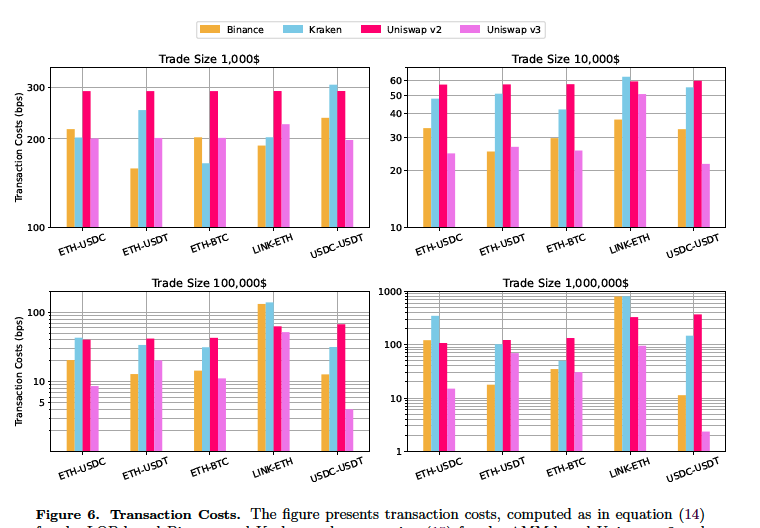

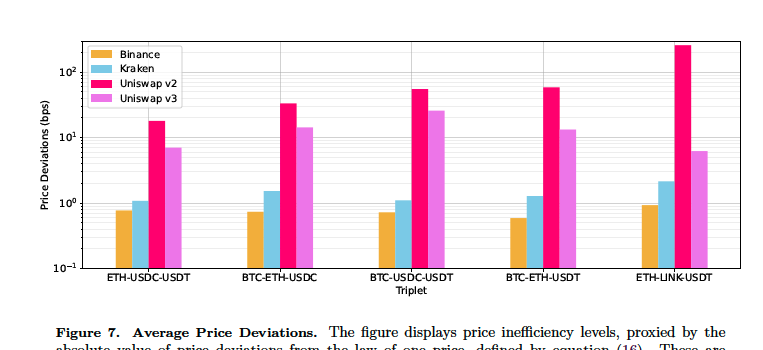

Barbon and Ranaldo (2022): compare the liquidity CEX and DEX; argue that DEX prices are less efficient.

payments network

Stock Exchange

Clearing House

custodian

custodian

beneficial ownership record

seller

buyer

Broker

Broker

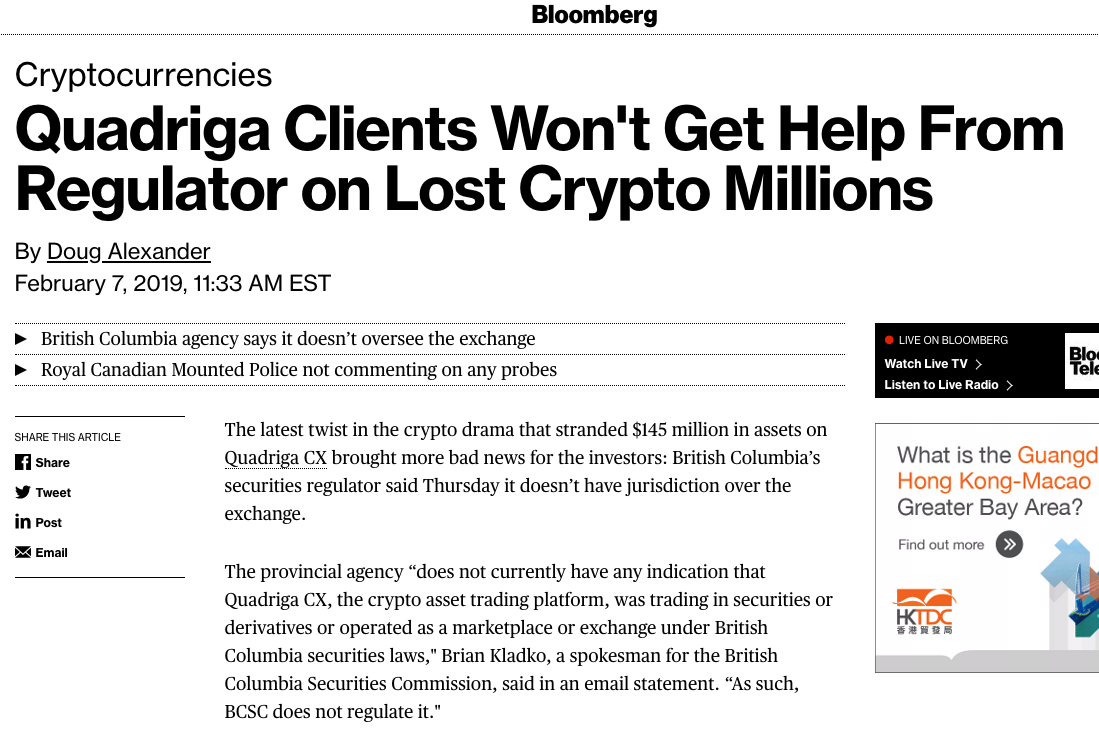

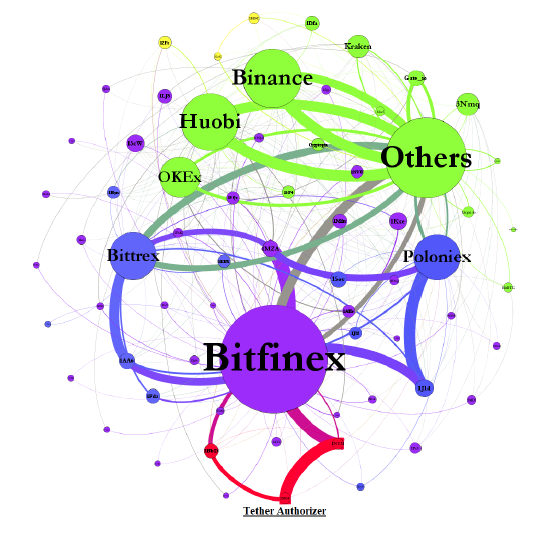

IS BITCOIN REALLY UN-TETHERED? JOHN M. GRIFFIN and AMIN SHAMS

Journal of Finance 2020

Figure 1. Aggregate Flow of Tether between Major Addresses

marginal pricing function

quantity \(q\)

price \(p^m(q)\)

Illustration of pricing

Some Pricing Rules from Traditional Markets: Limit Order Book

\[\Delta c(q)=\int_0^q\rho(s) ds.\]

Returns to Liquidity Provision

For fixed balanced volume \(V\) and fee \(F\)

Competitive liquidity provision

Basics of Liquidity Provision

\[\text{LP payoff}=\text{what I sold it for}-\text{value of net position}+\text{fee income}\]

see Lehar and Parlour (2023), Barbon & Ranaldo (2022).

(incremental) adverse selection loss when the return is \(R\)

fees earned

on informed

fees earned

on balanced flow

for reference:

positional loss

Basics of Liquidity Provision

\[\frac{1}{\text{initial deposit}}\int_0^\infty(\Delta c(q^*)-q^*p_t(R)+F \cdot \Delta c(q^*))~\phi(R)dR +\frac{F p_0 V}{\text{initial deposit}}\ge 0\]

\[\int_0^\infty\left(\frac{\Delta c(q^*)-q^*p_t(R)}{\text{initial deposit}} +F \cdot \frac{\Delta c(q^*)}{\text{initial deposit}}\right)~\phi(R)dR +\frac{F p_0 V}{\text{initial deposit}}\ge 0\]

closed form functions of \(R\) only

(see Barbon & Ranaldo (2022))

\[\underbrace{F \int DV \mu(DV) }_{\text{fees earned on}\atop \text{balanced flow}}+\int_0^\infty\underbrace{(\Delta c(q^*)-q^*p_t(R)}_{\text{adverse selection loss} \atop \text{when the return is {\it R}}} +\underbrace{F \cdot \Delta c(q^*))}_{\text{fees earned}\atop \text{from arbitrageurs}}~\phi(R)dR \ge 0.\]

Basics of Liquidity Provision

\(\Rightarrow\) \(\Delta c(q^*)-q^*p_t(R)\) is also referred to as the "impermanent loss" or "divergence loss"

\(\Delta c(q^*)-q^*p_t(R)=\underbrace{p_t(R)\times(a-q^*) +c+\Delta c(q^*)}_{\text{value of liquidity deposit}}-\underbrace{(p_t(R)a+c)}_{\text{value of buy-} \atop \text{and-hold position}}\)

see Milionis, Moallemi, Roughgarden, and Zhang (2022) for a dynamic analysis of impermanent loss

Basics of Liquidity Provision

Liquidity provision measured as "collective" deposit \(\alpha\) of token's market cap as function of

\[E[\text{DL}(R)]+F\cdot E[\text{another function of }R]+F\cdot \frac{\text{E[dollar volume]}}{\text{initial deposit}}\ge 0.\]

\[\text{what I sold it for}-\text{value of net position}+\text{fee income} \ge 0 \]

The Decision of the Liquidity Demander

\[F^\pi=\frac{1}{E[|\sqrt{R}-1|/2]+E[DV]}\left(-2q\ E[\text{DL}]+ \sqrt{-2qE[DV]\ E[\text{DL}]}\right).\]

this is from Malinova and Park (2023); similar result is in Hasbrouk, Riviera, Saleh (2023)

Model Summary

The Pricing Function

Liquidity Deposit \(\Rightarrow\) slope of the price curve

The Pricing Function (just a little more)

The Pricing Function (almost done, just one more thing)

AMMs continue to evolve: UniSwap v3

Basic idea:

Source:" Uniswap v3 Core," Adams, Zinsmeister, Salem, Keefer, Robinson (2021)

Some UniSwap v3 maths (Barbon & Ranaldo 2023)

Source: Elsts (2021) "Liquidity Math in UniSwap v3"

\(X\)

\(Y\)

normal trade: sell \(x\) \(\to\) get \(y'\)

\(Y-y'\)

\(X+x\)

front-running:

\(Y-y'-y''\)

\(X+2x\)

\(y'>y''~\Rightarrow\)

front-running is intrinsically profitable

Disclaimer:

Problems:

lesser problem because

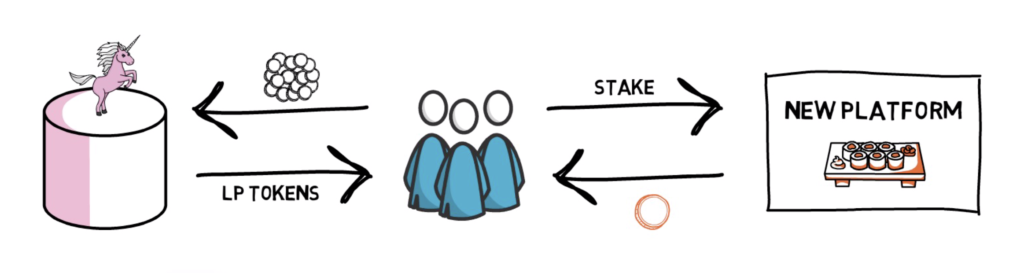

Common solution: create a reward token! Here's how this works

Step 4: users receive a reward token based on the time that they lock up the "receipt" token

Step 3: users lock up the "receipt" token in a smart contract

Step 2: users contribute liquidity and get a "receipt" token

Step 1: create reward tokens and deposit into a smart contract

borrow

provide collateral

Application: Pool-based borrowing and lending

Same problems as with trading:

But: in contrast to trading, here you need both!

liquidity \(\nearrow\)

volume \(\nearrow\)

protocol fees \(\nearrow\)

token value \(\nearrow\)

Platform economics is tricky:

Without intermediaries:

platform economics!

incentives for both?

What value do these tokens have?

Vampire Attacks and Other Shenanigans

Source: https://finematics.com/vampire-attack-sushiswap-explained/

another common trick:

By Andreas Park

Presentation for CBER-DFI Crypto-Economics Summer School 2024