Andreas Park PRO

Professor of Finance at UofT

February 6, 2020

Andreas Park

Associate Professor of Finance, University of Toronto

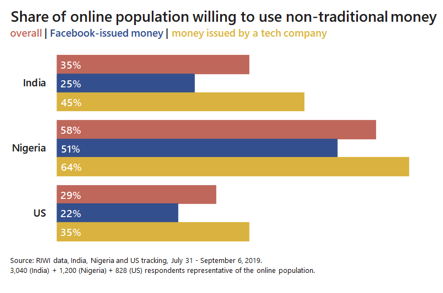

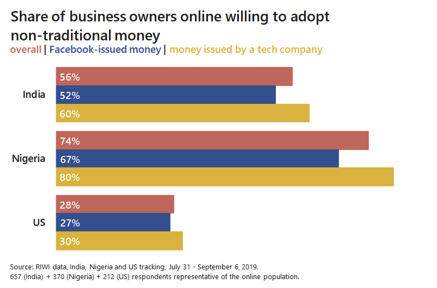

Source: Will Libra Succeed? Results of a Global Randomized Survey Experiment; by Danielle Goldfarb and yours truly

Basic idea of competitive equilibrium

aggregate mining cost = aggregate reward

Double spending attack

condition that prevents it

(Chiu & Koeppl RFS 2018)

| transactions per second | T per 12 hours (business day) | |

|---|---|---|

| Bitcoin | 7 | 302,400 |

| Ethereum | 30 | 1,296,000 |

| Algorand | 2000 | 86,400,000 |

| Conflux | 3500 | 151,200,000 |

| Athereum | 5000 | 216,000,000 |

| Payments Canada retail | 648 | 28,000,000 |

| US retail | 7639 | 330,000,000 |

| Canada number of equity trades | 46 | 2,000,000 |

| Orders on Canadian equity markets | 3588 | 155,000,000 |

Lessons?

Is there economic merit to token-finance?

Do financing tokens solve an economic problem?

Traditional economy

Decentralized economy

Traditional "centralized" economy

Chod and Lyandres (2018):

Davydiuk, Gupta, and Rosen (2018)

Lee and Parlour (2018)

Malinova and Park (2018)

What is the economic impact of "tokenizing everything"?

How will it affect investments and investment banking?

Which business opportunities will it enable?

What do tokens and "alternative money" mean for payments?

blockchain is a transformative technology, but won't be used in practice overnight

many conceptual and technological challenges remain, but there are already various areas of application

legal, regulatory, and competitive changes are needed and then the opportunities are endless ...

it will open up the banking world further, foster international competition, and change how we pay and exchange value

My view: business development will happen in private/semi-public space; strong increase in recent activity; no more testing but re-engineering of processes.

@financeUTM

andreas.park@rotman.utoronto.ca

slides.com/ap248

sites.google.com/site/parkandreas/

youtube.com/user/andreaspark2812/

price

demand

marginal cost

marginal revenue

general idea: sell future output

two approaches for token sales

sell a fraction of future revenue

sell units of future output

price

demand

marginal cost

marginal revenue

Entrepreneur does not internalize the effect of an extra output unit on the token value for the tokenholders!

Result: overproduction

price

demand

marginal cost

marginal revenue

Result: underproduction

NB: Similar to Chod and Lyandres (2018)

\(\Rightarrow\) shifts marginal revenue for entrepreneuer left because get only fraction of revenue

revenue sharing: underproduction

output presale: overproduction

\(c\)

\(MR\)

"does not internalize" = externality

address externality: TAX!

here: tax future token income

incremental token income gets shared

\(\Rightarrow\) combine the two to get the monopoly quantity!

Idea:

entrepreneur can influence expected demand

with effort

without effort

common topic in corporate finance

very relevant in "decentralized" world where developers are scattered around the globe

also applicable to, e.g. established firms that do something new

assume \[\textit{NPV}(\text{effort})>0>\textit{NPV}(\text{no effort})\]

Investors (equity or token holders) only finance the project if the entrepreneur undertakes the effort

Solve for the optimal funding conditional on the entrepreneur taking the effort

Derive conditions such that the entrepreneur undertakes effort

1.

2.

Key insight: a token contract incentivizes effort better than equity (similarly to canonical debt vs. equity insights)

Optimal token contract has debt features:

get nothing if demand is low (only original

tokenholders get anything)

benefit if demand is high

all projects that can be financed by equity can be financed by the optimal token contract but

some projects that can be financed by optimal tokens contracts cannot be financed by equity.

Simple model of revenue-based ICO vs equity financing from the standard corporate finance + IO toolbox

Theorem 1: Without frictions, an optimal token contract finances the same

projects as equity

Theorem 2: With entrepreneurial moral hazard,

any equity-financeable project can be financed by an optimal token

some token-financeable projects cannot be financed by equity

\(\Rightarrow\) There is economic and conceptual merit to token financing

By Andreas Park