Andreas Park PRO

Professor of Finance at UofT

Katya Malinova and Andreas Park

How did these guys put it ...?

source:

1. Multiple trading protocols are possible

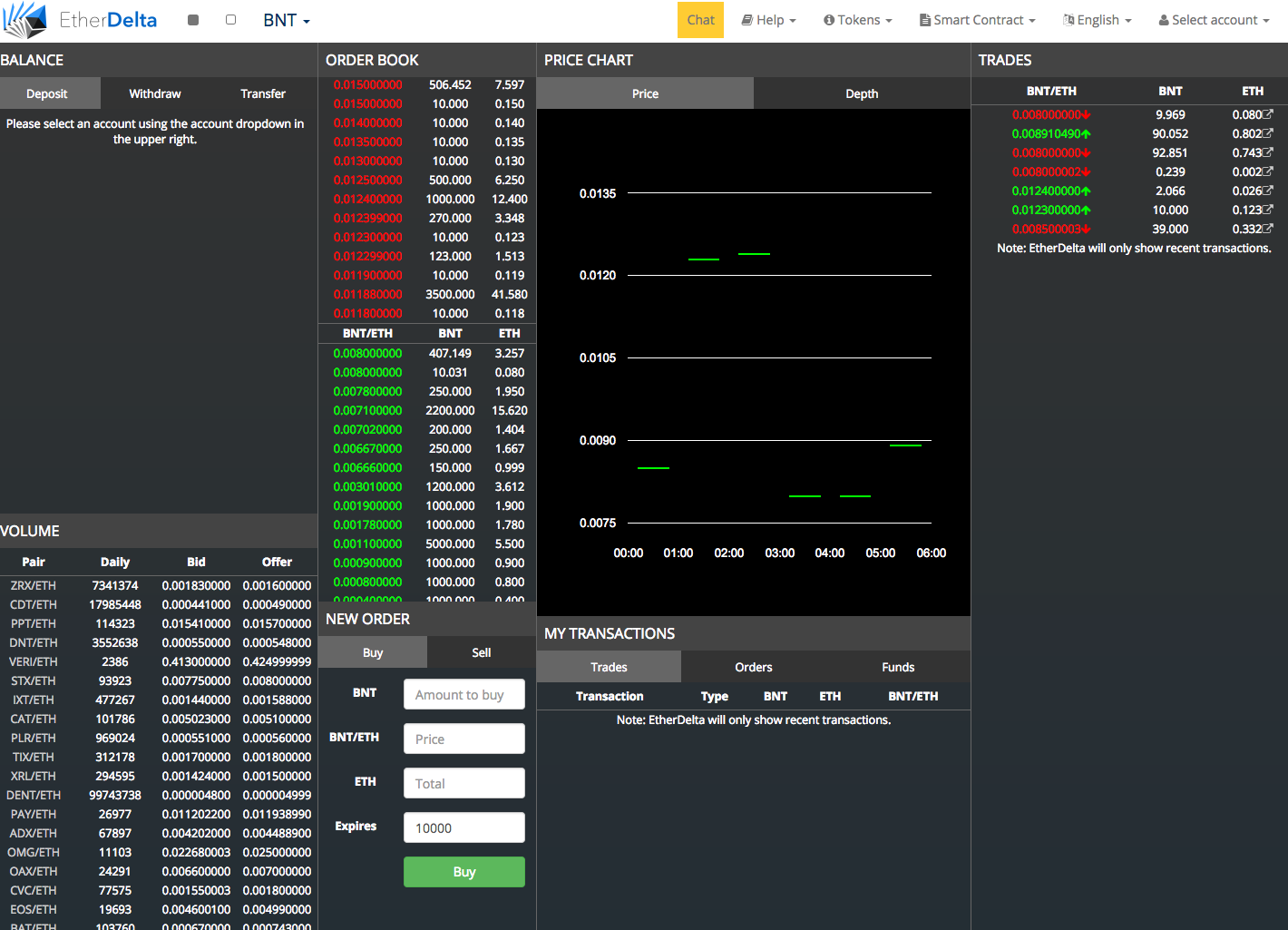

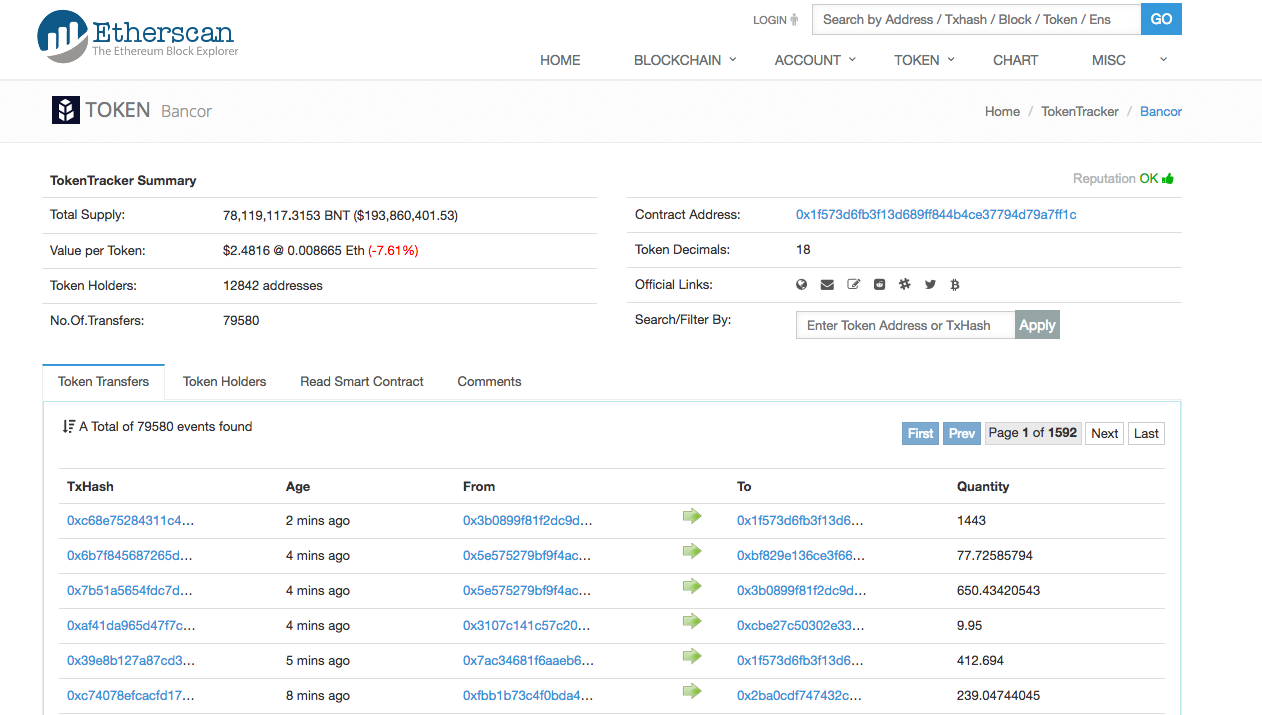

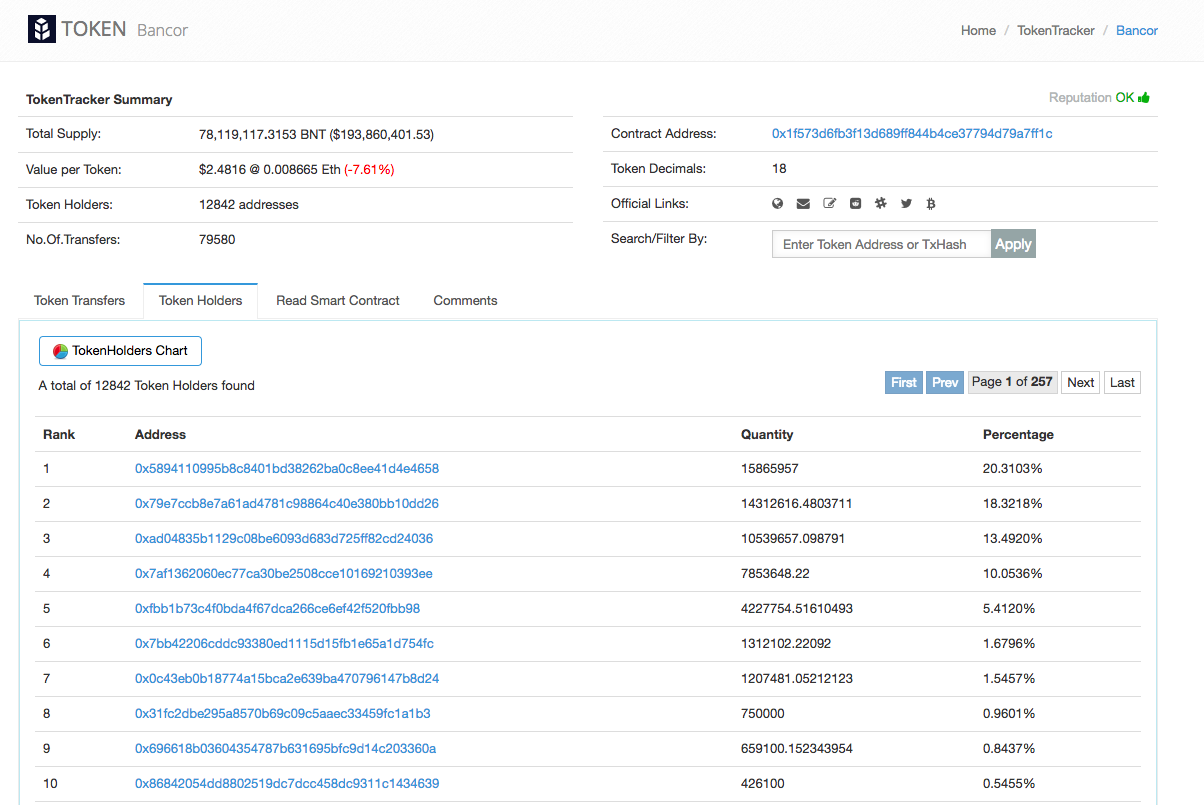

User-facing exchange mask

Fully Decentralized, "OTC",

Peer-to-Peer Exchange

2. High Level of Transparency

See transactions between "addresses" (="IDs")

3. You can tell who owns what

Key: wallets/addresses = IDs but NOT = traders

Who benefits and loses under which regime?

Each period one is hit with size Q=1 liquidity shock.

Other can absorb the shock at zero cost.

Disclaimer:

Idea:

Requires a system design choice:

Repeated setting:

Front-running is punished by “grim trigger” & trade forever with small and intermediary.

Single shot:

LP always extracts all surplus (or would front-run).

Closest and native to "public" blockchains:

small traders

large trader

small traders

large trader

small traders

large trader

filled

unfilled

Opaque Single ID

Opaque Multi-ID: LP accepts

Opaque Multi-ID: LP rejects

accept offer

"target" small investors only

"target" IDs of both: large and small

front run

Result 1: There exists an equilibrium with no front-running where

provided

Result 2 (numerical): For small discount (=infrequent interaction) factors, the equilibrium with no front-running where LP accept does not exist. Then:

=> "over-trading" with intermediary

Observations

Finding 3:

For the average equilibrium stage payoffs of large traders.

Finding 4: (Numerical)

There exist parametric configurations such that large traders trade with each other at p > 0 in the multi-ID ownership setting, but their average equilibrium payoff in the opaque single-ID setting is higher.

By Andreas Park

I used this set of slides for a microstructure workshop at Machester Business School in September 2018. The deck has been designed for a 25 minute presentation.