Andreas Park PRO

Professor of Finance at UofT

Katya Malinova and Andreas Park

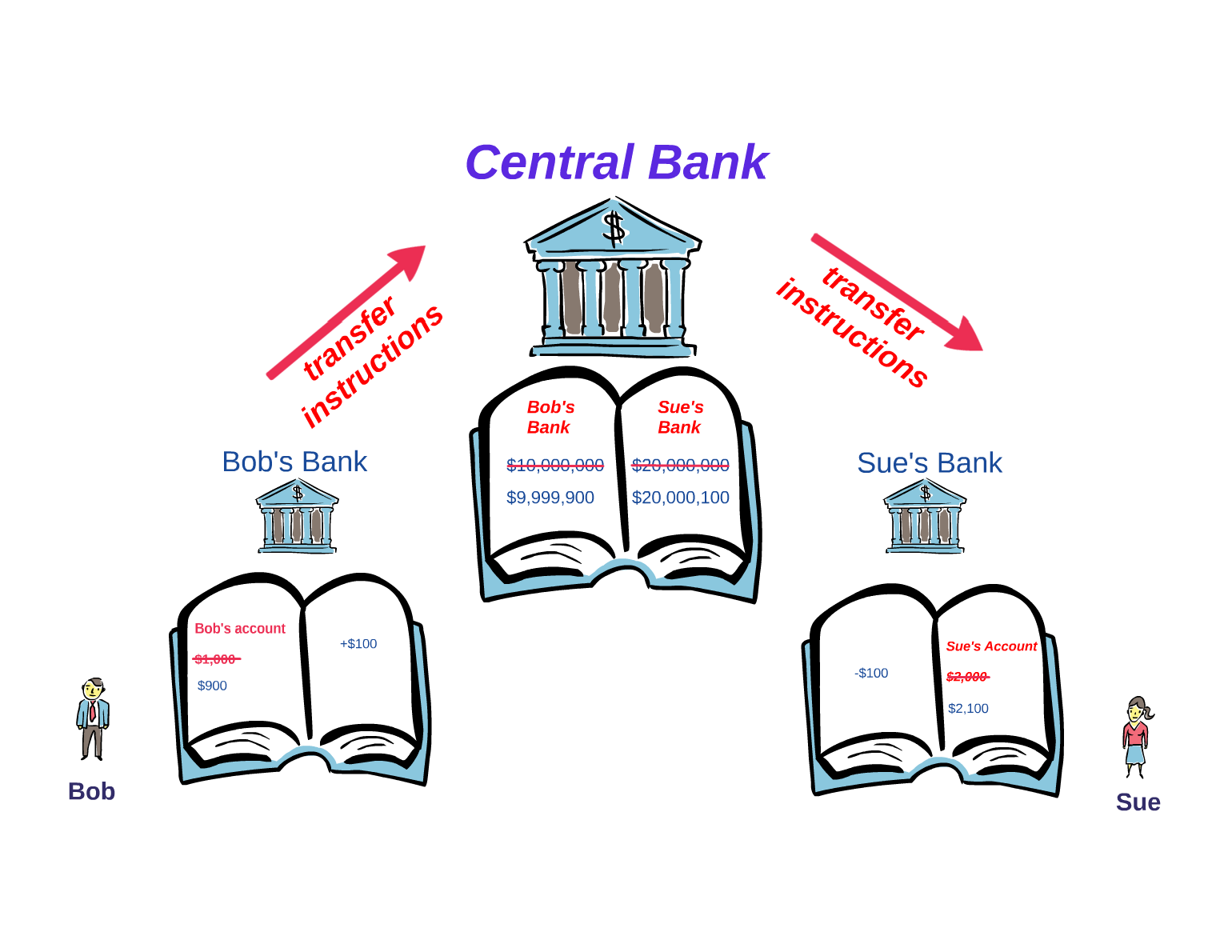

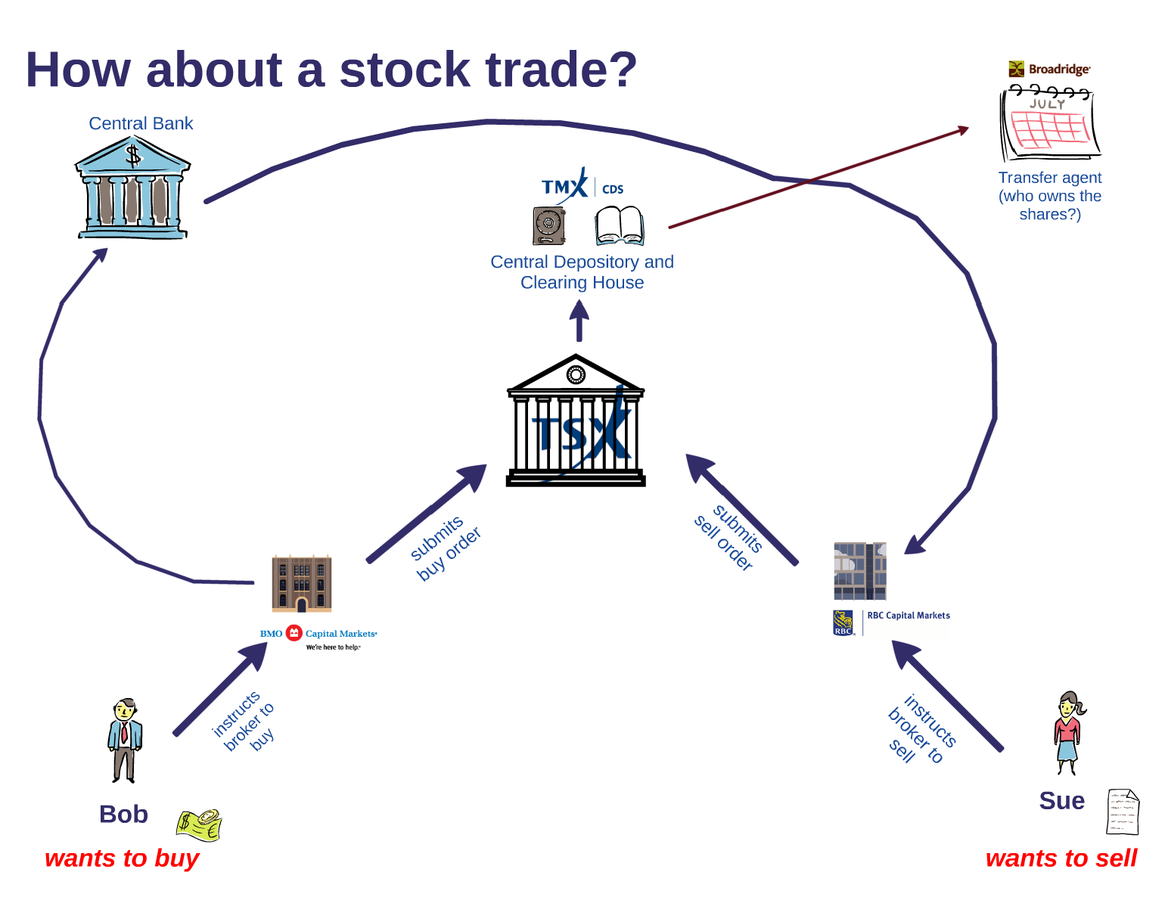

frictionless electronic transfer of information

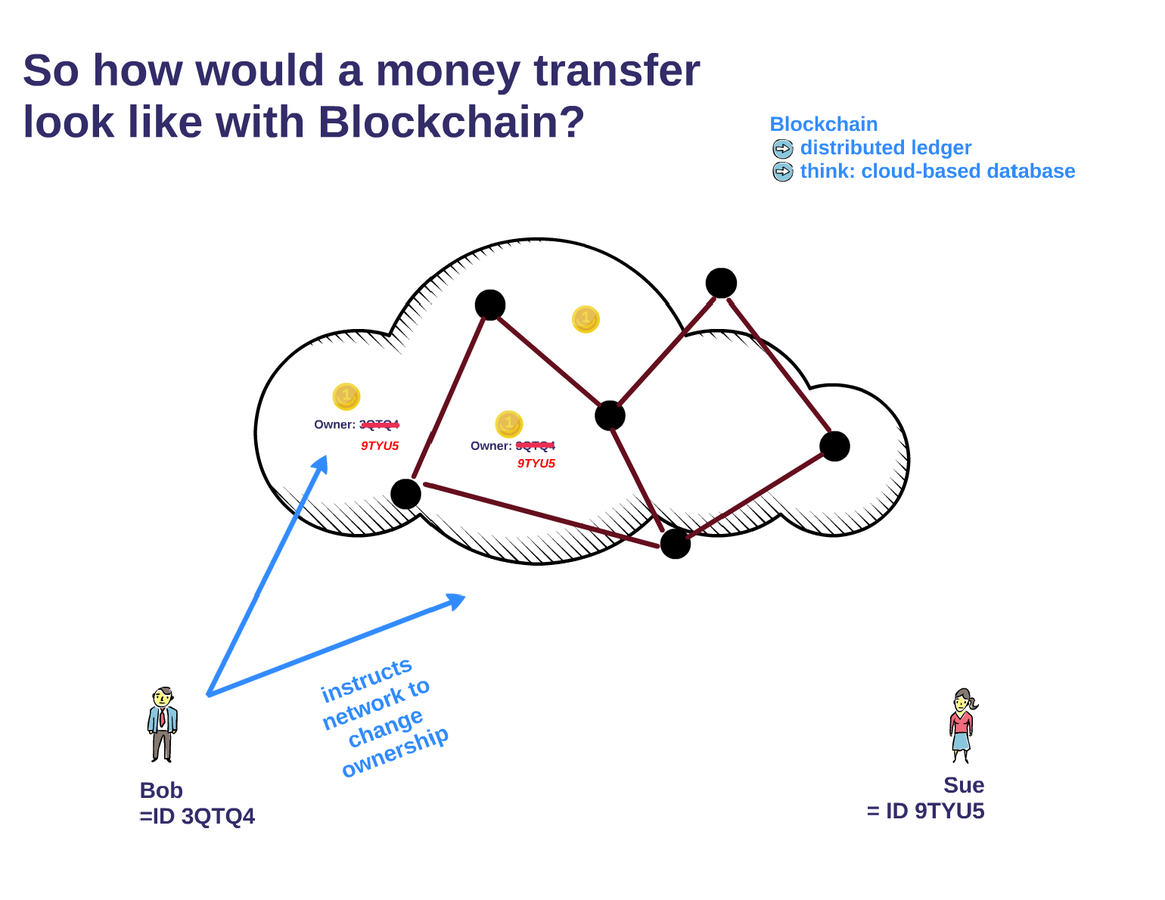

Blockchain:

frictionless electronic transfer of value

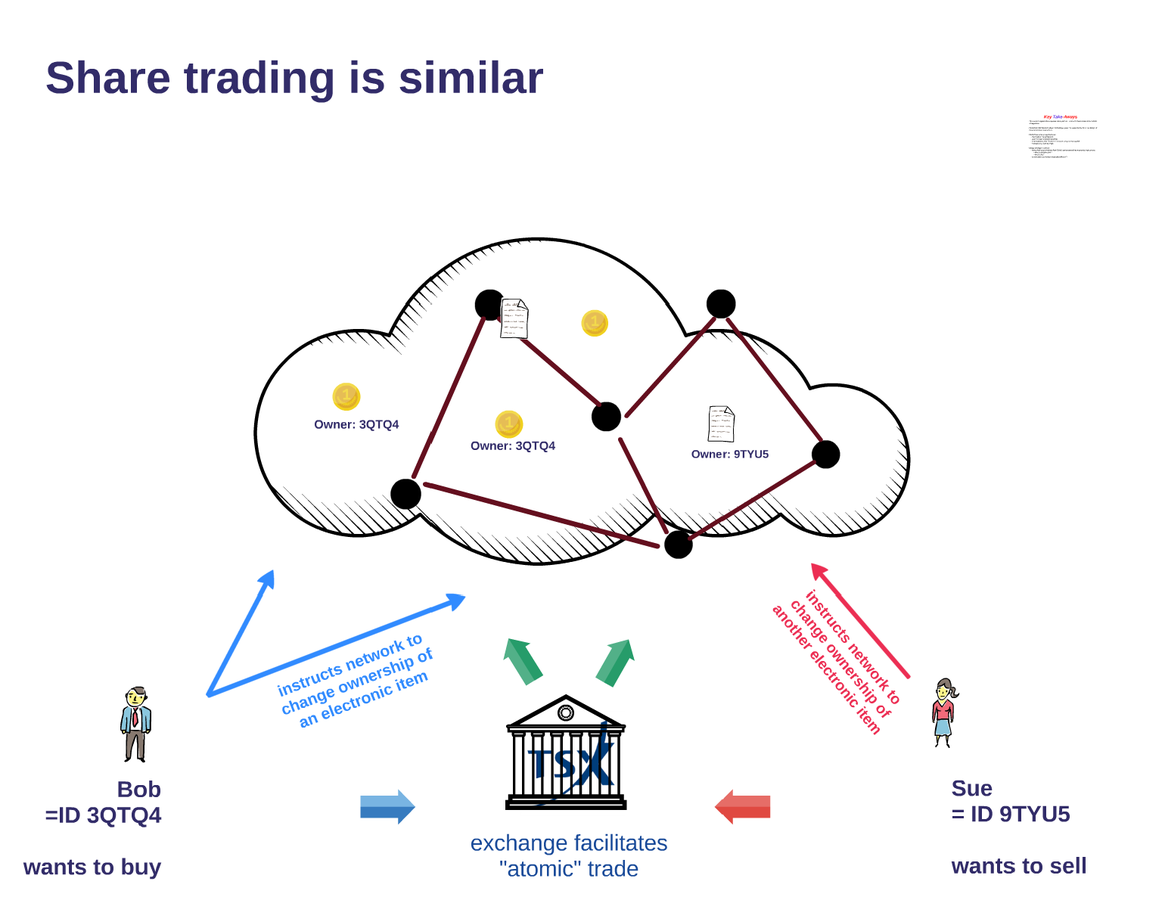

A version with an exchange

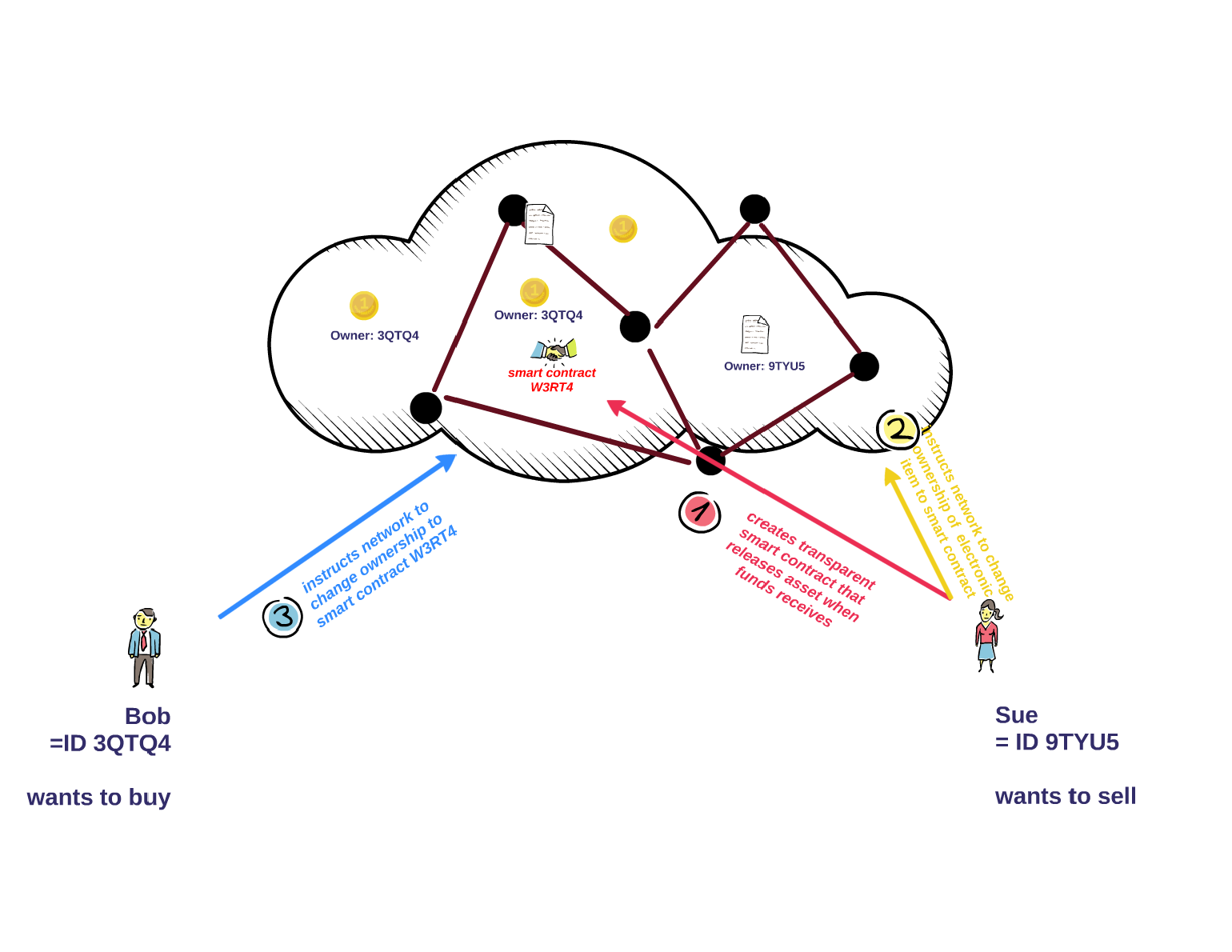

A version without an exchange but with smart contracts

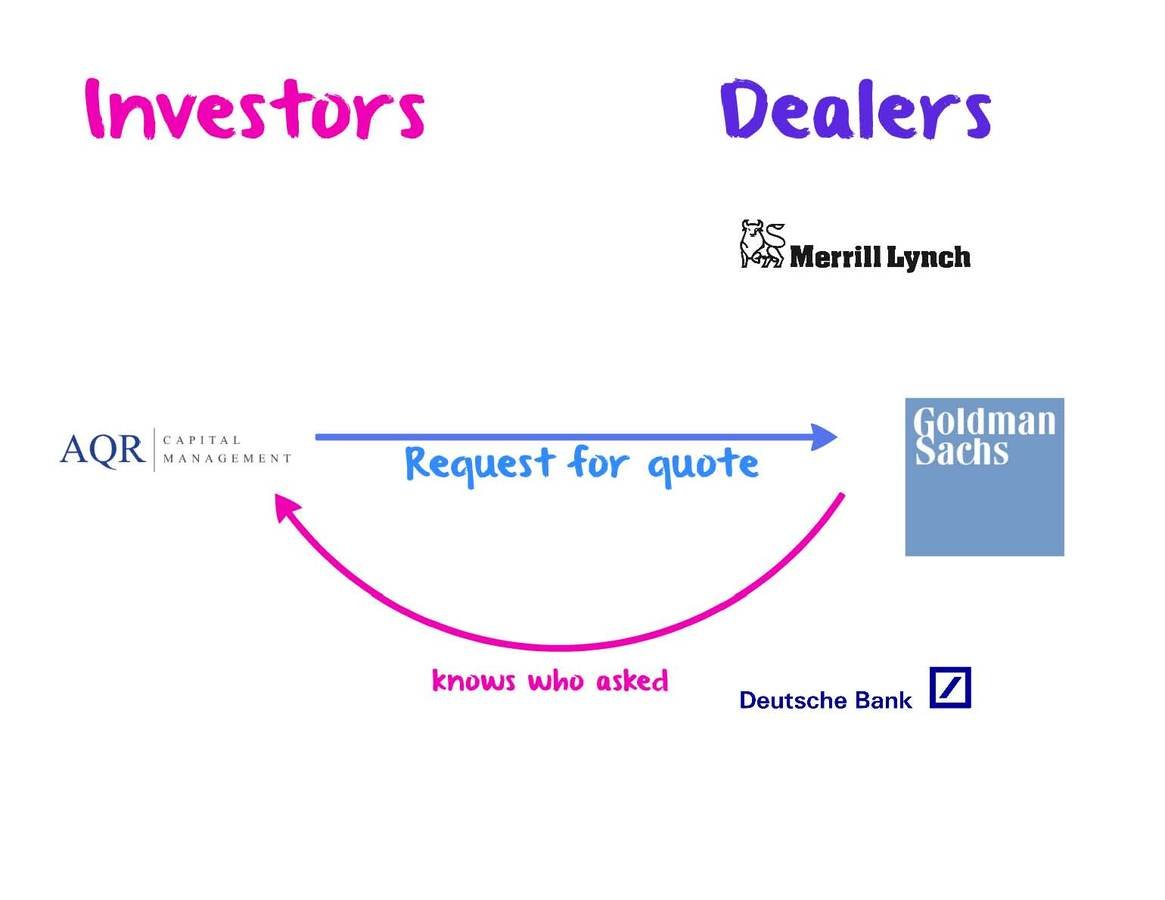

Anton Golub, Lykke Chief Scientific Officer: "[T]he public ledger becomes a valuable source of trading data.

While it is not possible to identify the traders [by name],

any observer can deduct [...] detailed position data - by tracking tick-by-tick transaction data from the blockchain.[...]"

For this paper

Also interesting

Who benefits and loses under which regime?

Each period one is hit with size Q=1 liquidity shock.

Other can absorb the shock at zero cost.

Disclaimer:

Disclaimer:

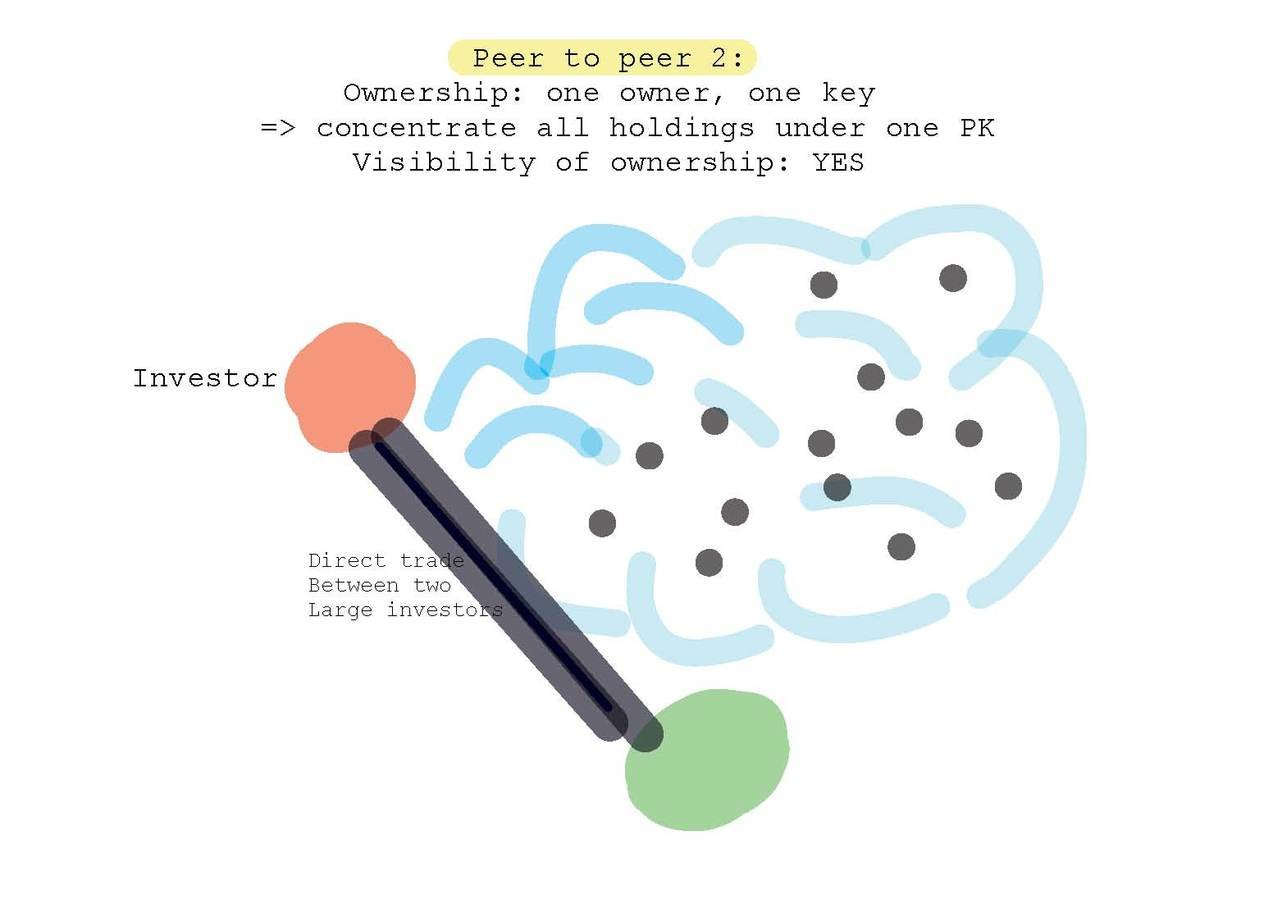

Requires a system design choice:

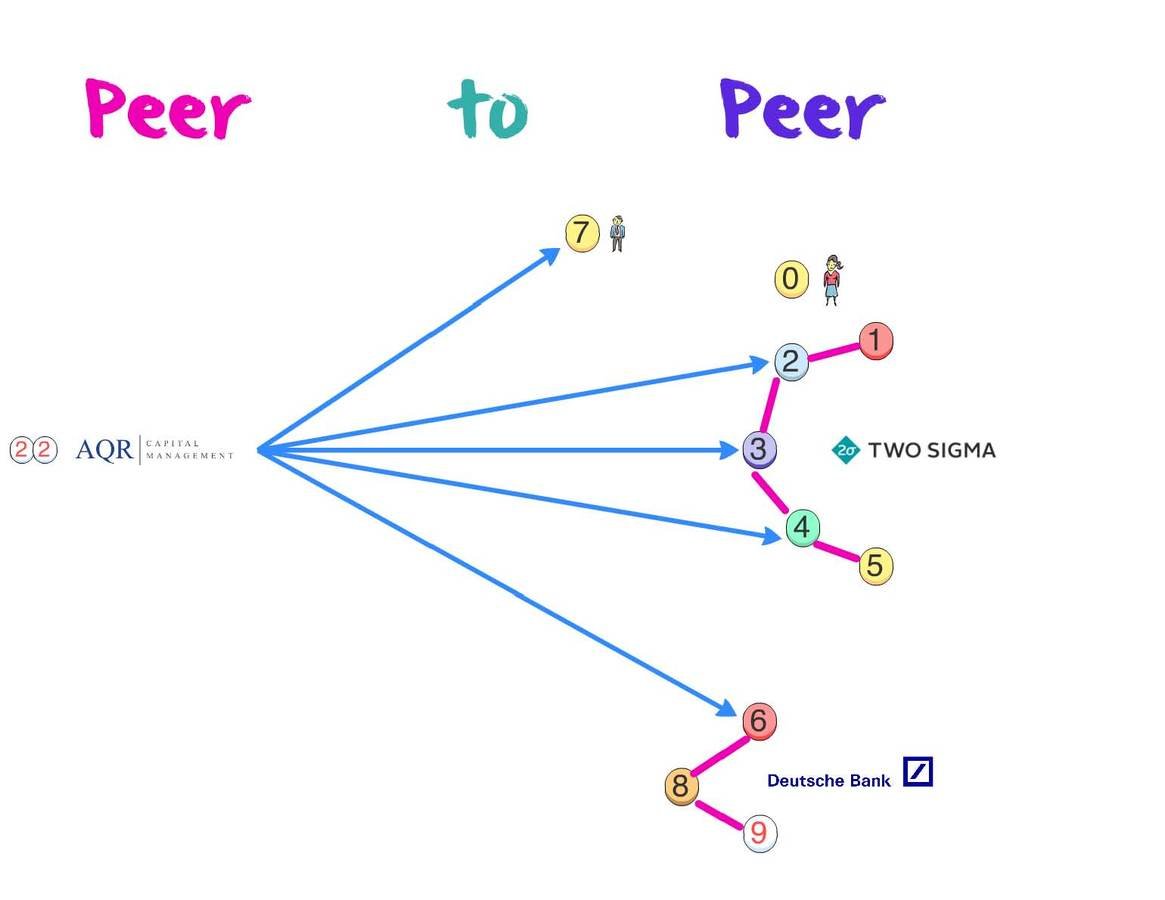

Large trader LT may:

Trade with small investors,

the intermediary.

Approach the other large trader LP.

data cost

current market price paid to small

costly trading with intermediary

validation cost

escape complexity and validation costs,

avoid price impact of trade with risk-averse intermediaries.

Closest and native to "public" blockchains:

small traders

large trader

small traders

large trader

small traders

large trader

filled

unfilled

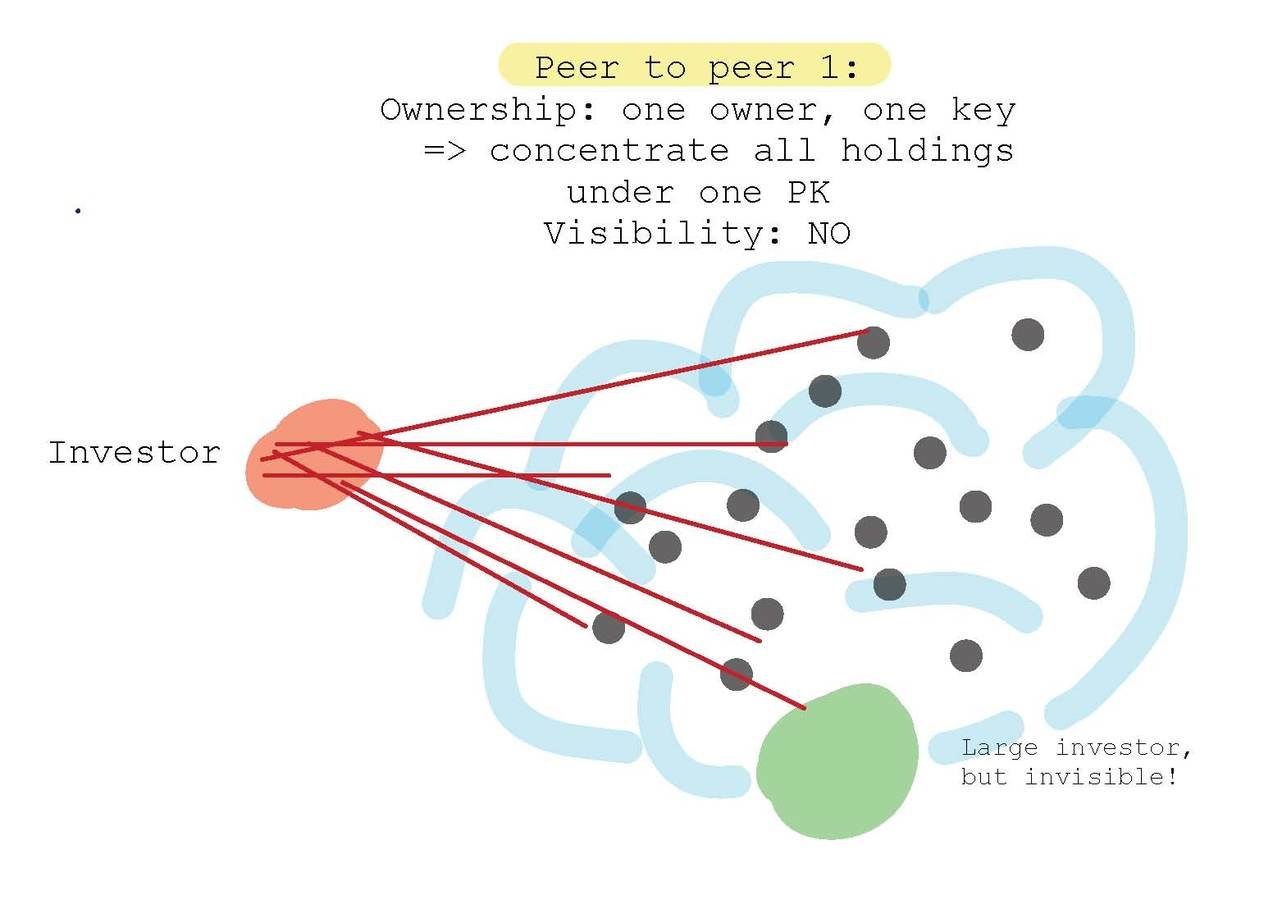

Setting I:

non-transparent, single IDs

Setting III: large accept

Setting III: large reject

continuum & large accepts

setting I: non-transparent

continuum & large rejects

"over-trade" with the intermediary

Trigger Strategy:

accept offer

submit large amount to continuum

submit large amount to continuum

front run

Result 1: There exists an equilibrium with no front-running where

provided

Result 2 (numerical): For small discount (=infrequent interaction) factors, the equilibrium with no front-running where LP accept does not exist. Then:

=> over-trading with intermediary

Payoffs with transparent, concentrated ownership are highest.

Observations

Finding 3:

The following relations hold for the average equilibrium stage payoffs of large traders.

Finding 4: (Numerical)

There exist parametric configurations such that large traders trade with each other at p > 0 in the multi-ID ownership setting, but their average equilibrium payoff in the opaque single-ID setting is higher.

For dispersed ownership, there exist parametric configurations s.t.

small increase in validation cost => increase in aggregate payoff

Idea: Switch from

Anton Golub, Lykke Chief Scientific Officer:

=> Let’s start talking about market design with blockchain technology!

By Andreas Park

This is a set of slides that I used for the presentation of my paper with Katya Malinova on our paper "Market Design with Blockchain Technology". This iteration was presented at a conference at the Cambridge Centre for Alternative Finance, Judge School of Business, Cambridge University, June 2017. This deck of slides is designed for a 30 minute presentation.