Andreas Park PRO

Professor of Finance at UofT

Instructor: Andreas Park

Rotman School of Management & FinHub, Rotman's Financial Innovation Lab

Date: June 2023

Business of Payments Executive Ed

A quick survey, before we even start

please navigate to

Topic: Innovations in payments: Why and how?

Goal: Convey solutions and competitive developments to payments-related challenges of consumers & businesses

HOW Part 1: Innovation WITHIN the current institutional arrangements

HOW Part 2: Innovation OUTSIDE the current institutional arrangements

sending money peer-to-peer

help with budgeting

mortgage

loans for car

payment card

Recent in-class discussion assignment (50 students)

What do you need a bank for? (in this order)

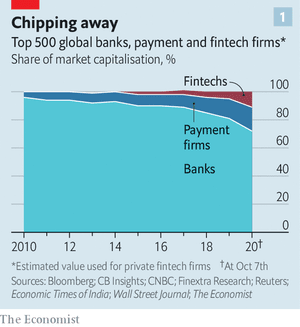

in many countries, this space is FinTech

Source: CNBC Jan 15, 2021, https://www.cnbc.com/2021/01/15/jamie-dimon-says-jpmorgan-chase-should-absolutely-be-scared-s-less-about-fintech-threat.html

"Payments is the hill for banks to die on"

"JPM should absolutely be scared s**tless about the FinTech threat"

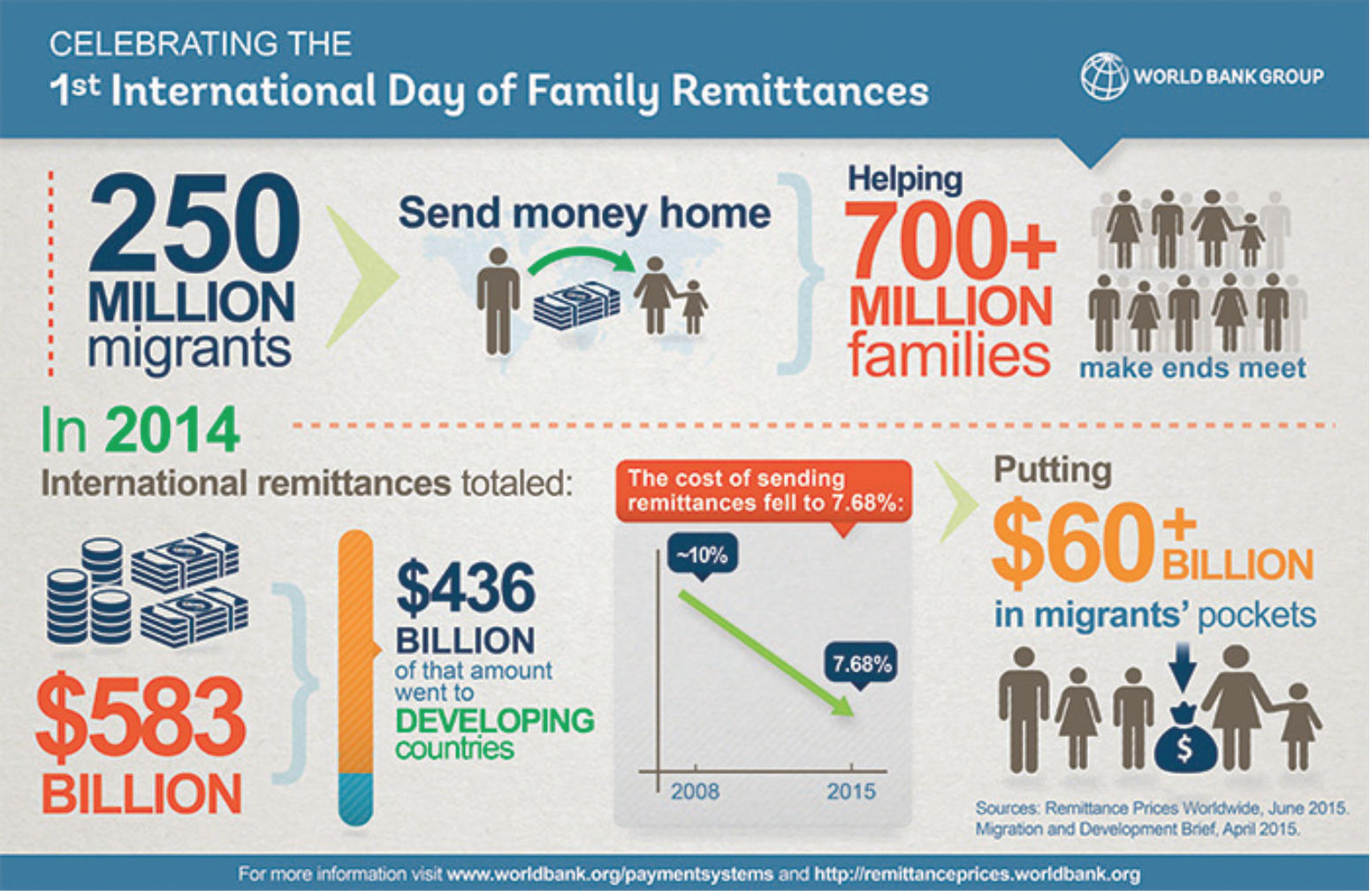

payments is a profitable line of business

payments data is very valuable

payments \(=\) clunky and full of frictions

payments is the entry level drug to all things FinTech

Giancarlo Bruno, Senior Director, Head of Financial Services Industry, World Economic Forum

payments matter a lot more to people than we might think

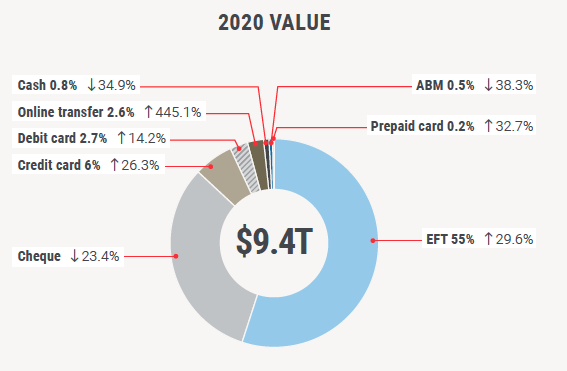

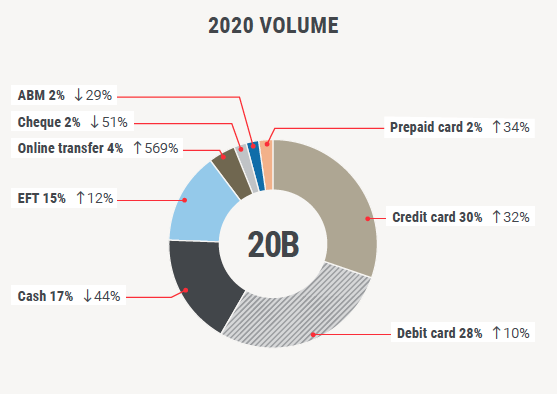

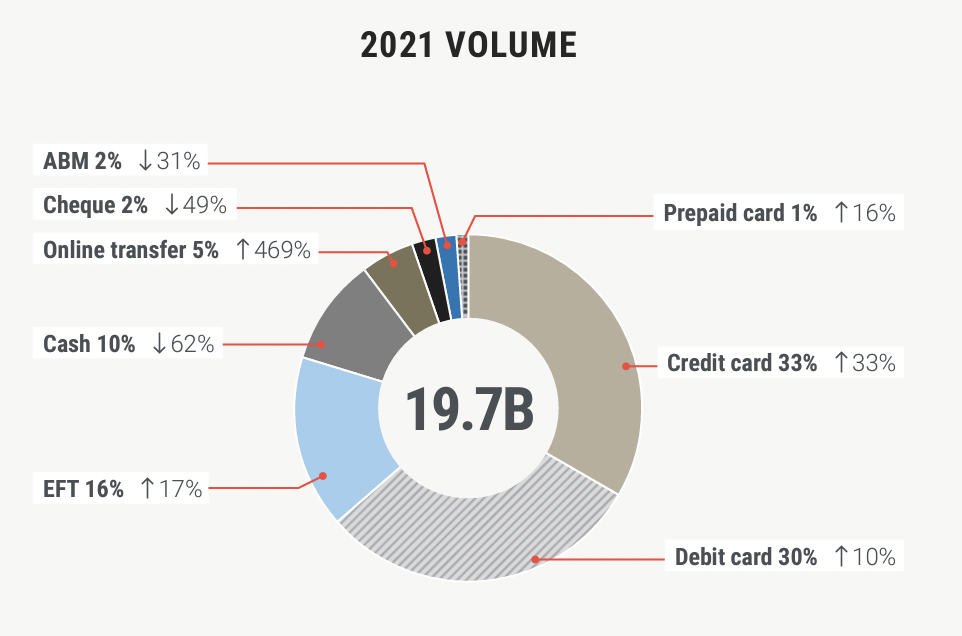

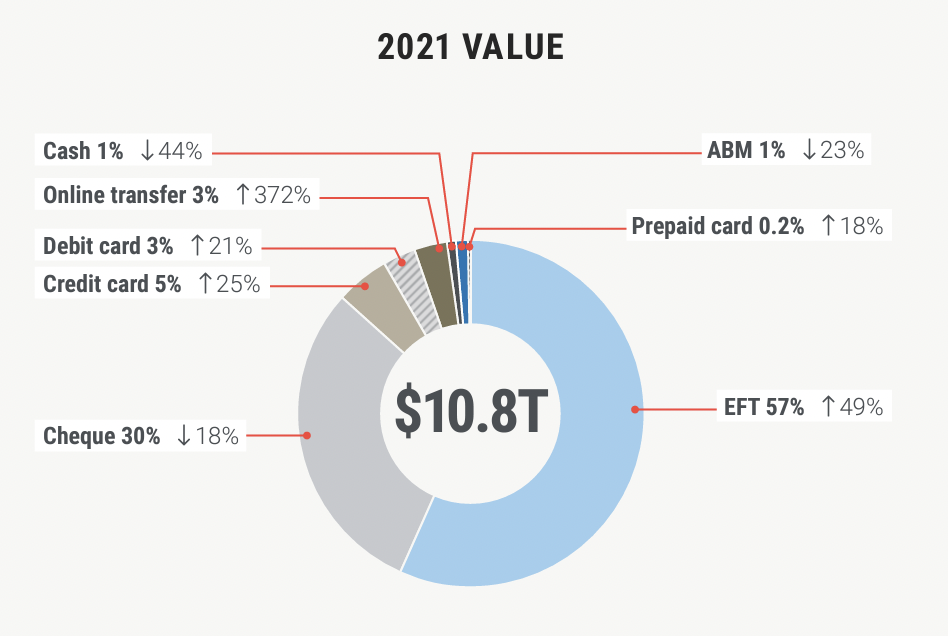

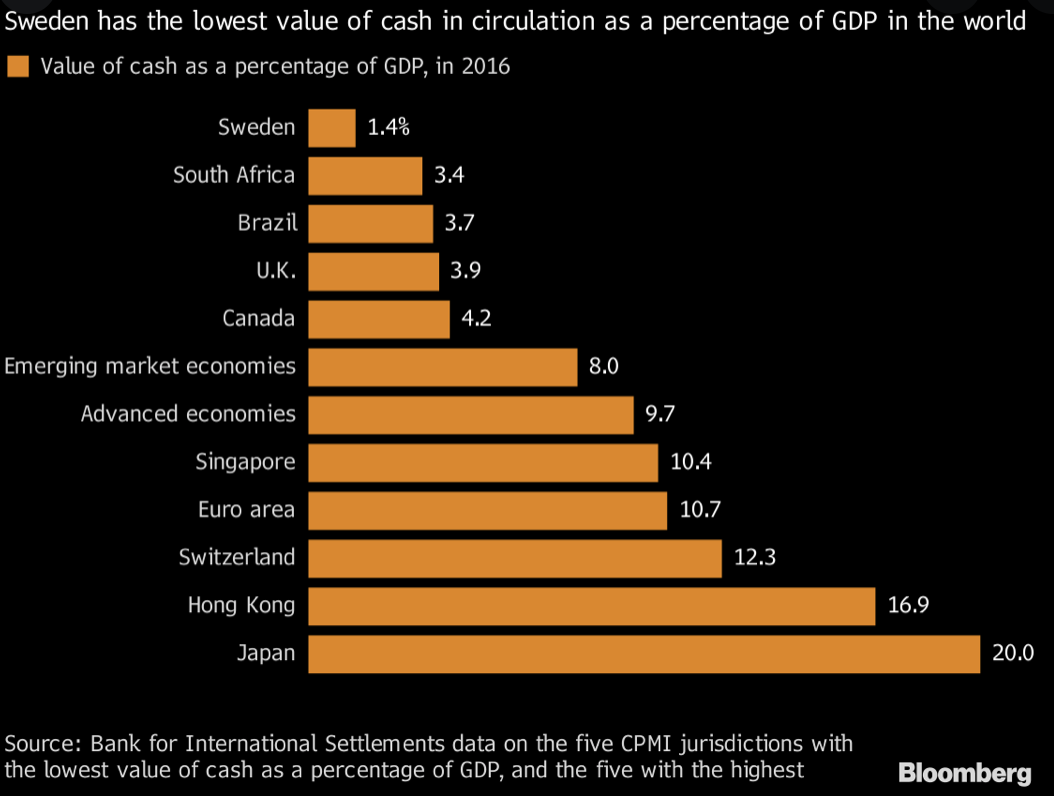

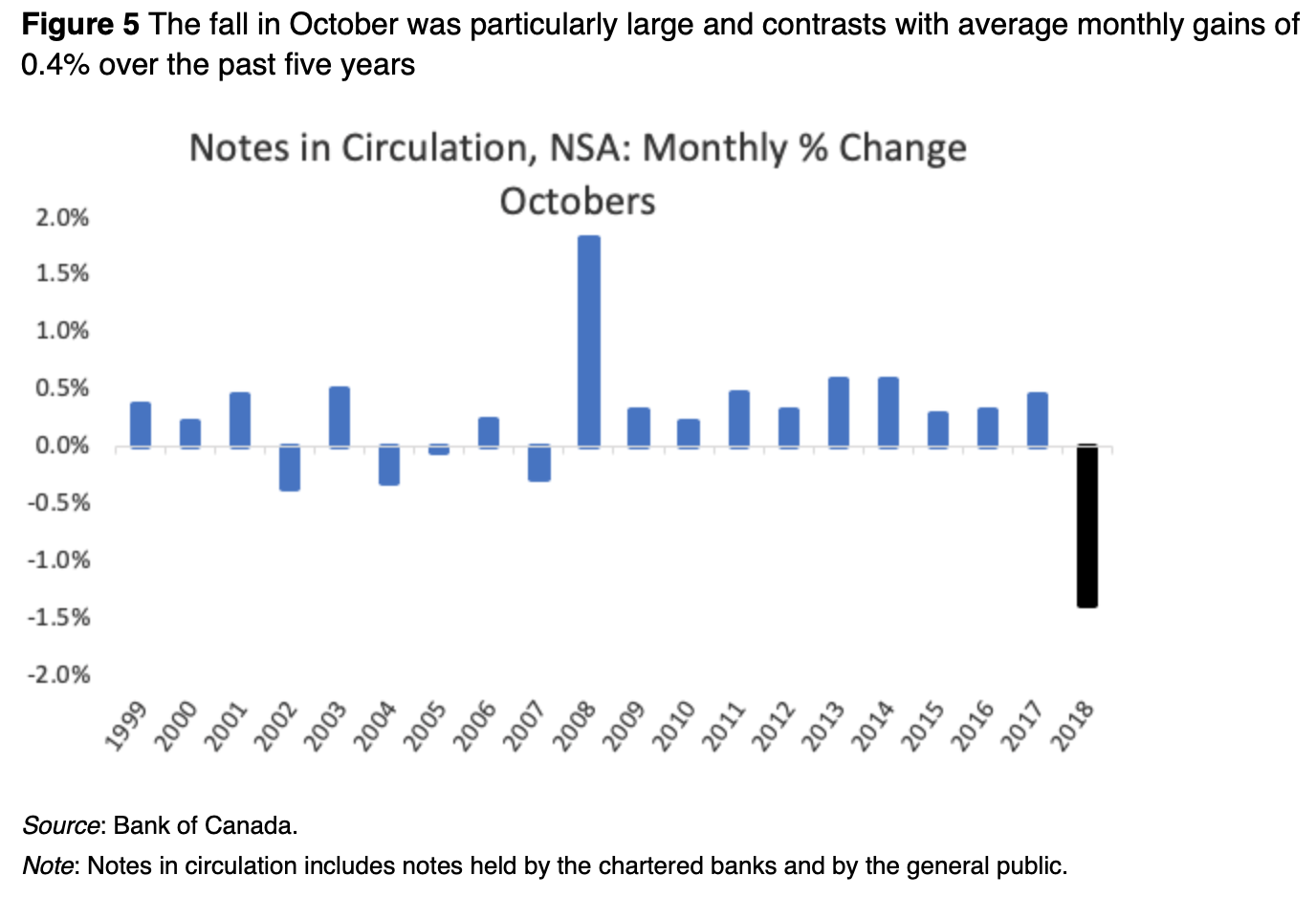

Who pays with dead trees and why?

Not who you think:

%change is for past 5 years

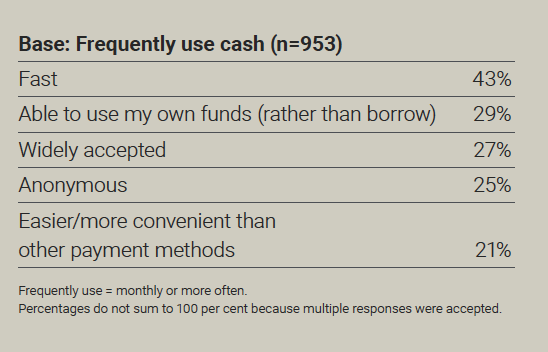

Why do people use cash?

Fun Fact: cash is probably the only day-to-day item that you have to get in-person

2020 Survey

2021 Survey

... it's just 9 steps away!

?

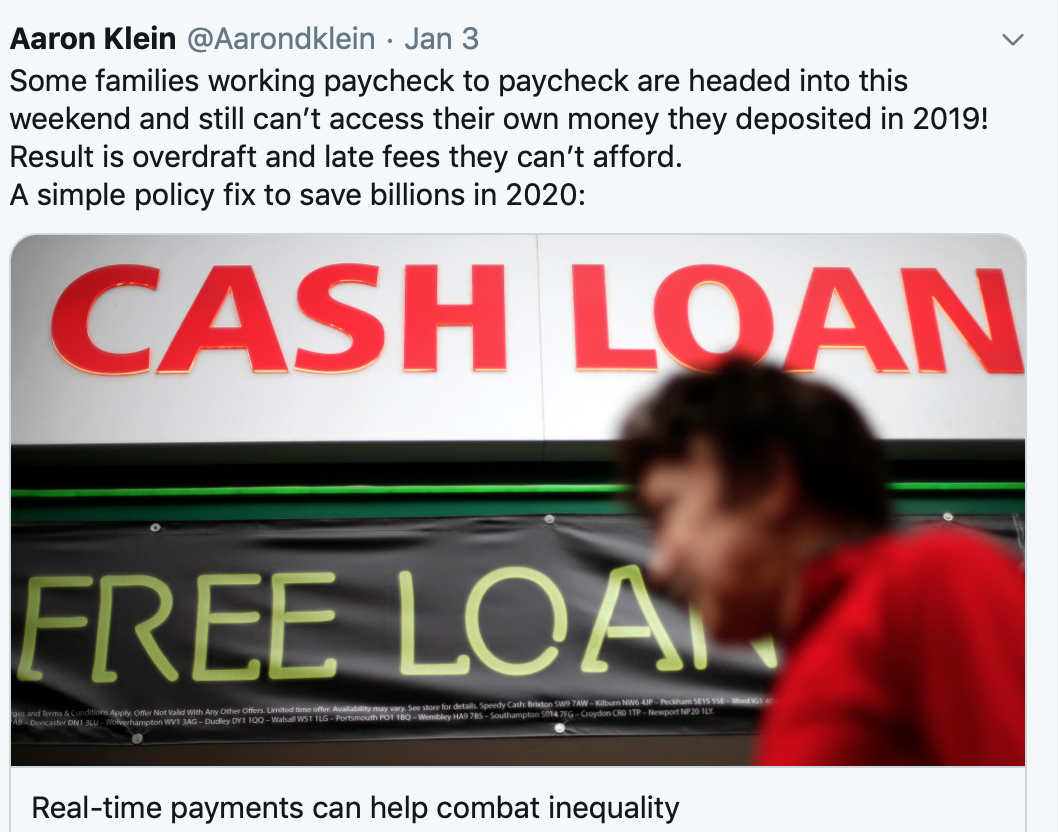

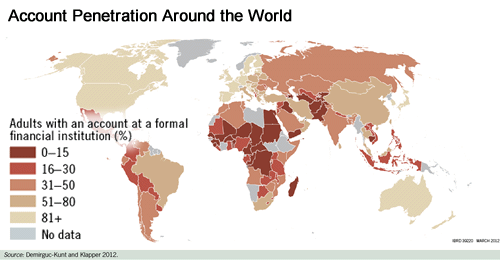

https://www.brookings.edu/opinions/real-time-payments-can-help-combat-inequality/

https://www.brookings.edu/opinions/real-time-payments-can-help-combat-inequality/

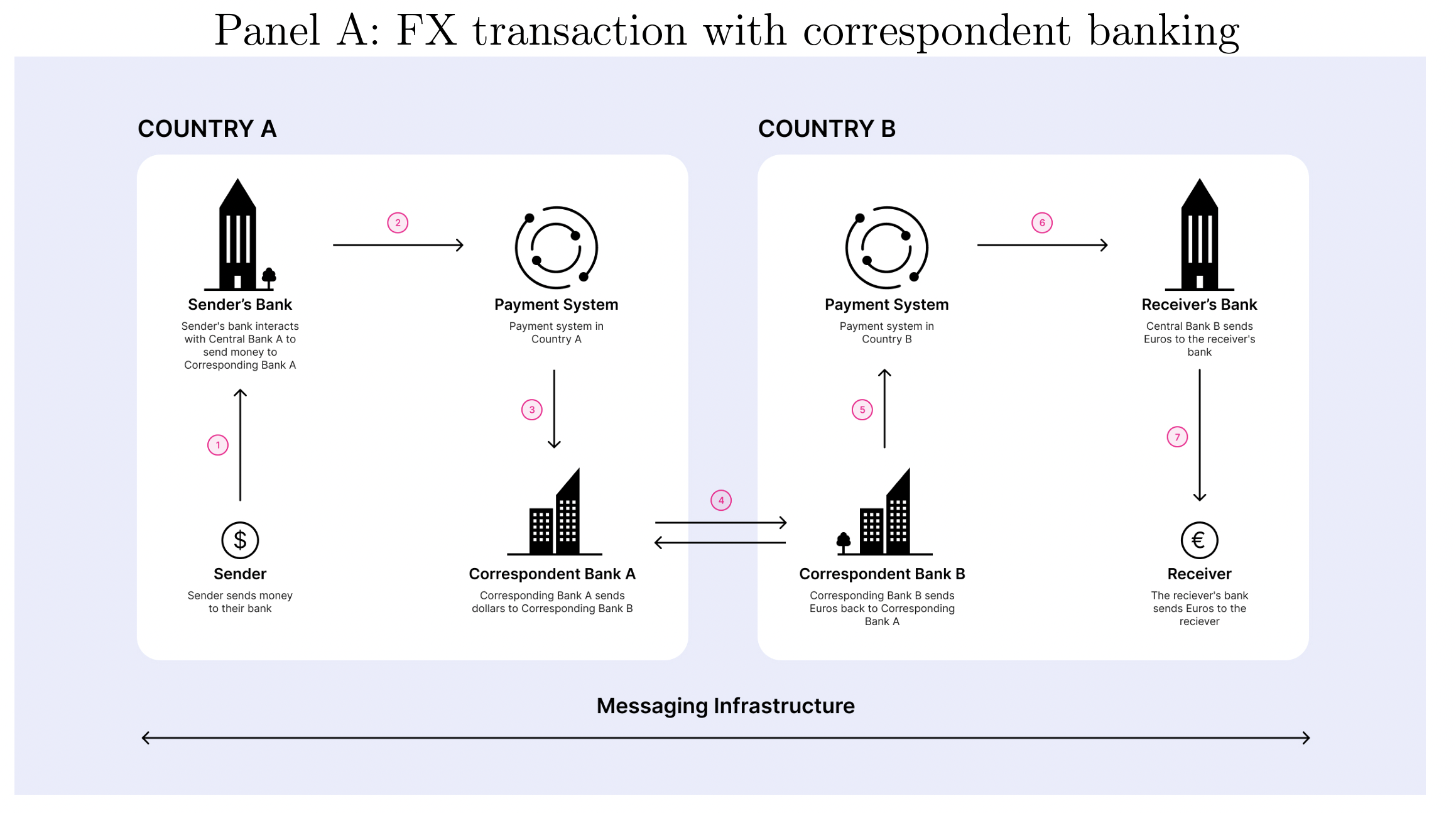

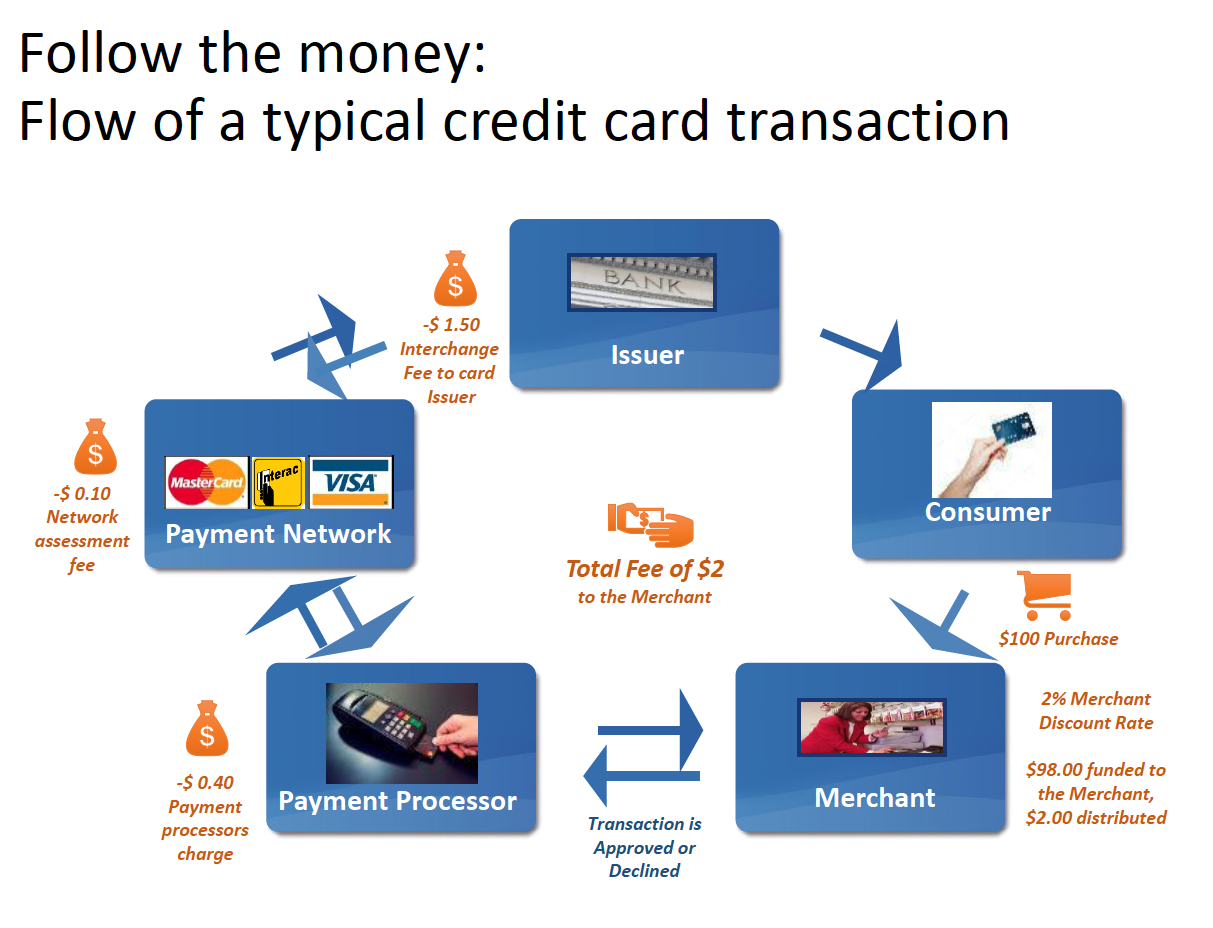

How is it that Amazon delivers same day but merchants receive their payment two days later?

Source: Schmall & Wolkowitz (2016), Center for Financial Services Innovation (2016) "Financially Underserved Market Size Study"

Pull

Push

Source: How can payments modernization benefit Canadian businesses? Evaluating the cost of payments processing; EY and Payments Canada, 2018

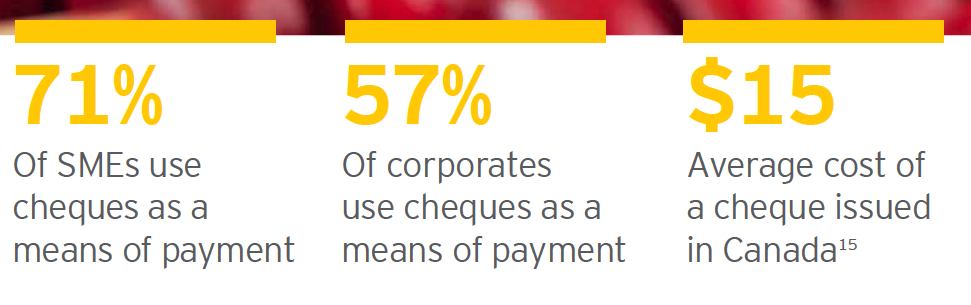

From Wendy Rotenberg: 734 Million Cheques for $4 Trillion

Source: How can payments modernization benefit Canadian businesses? Evaluating the cost of payments processing; EY and Payments Canada, 2018

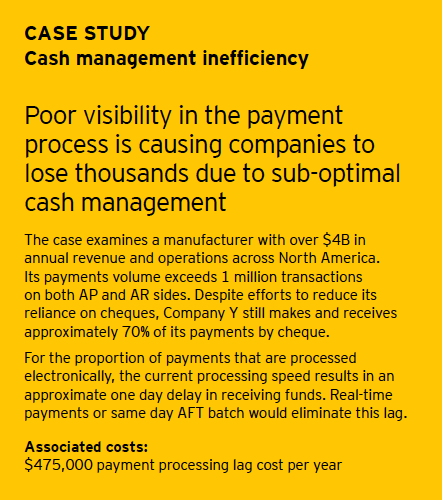

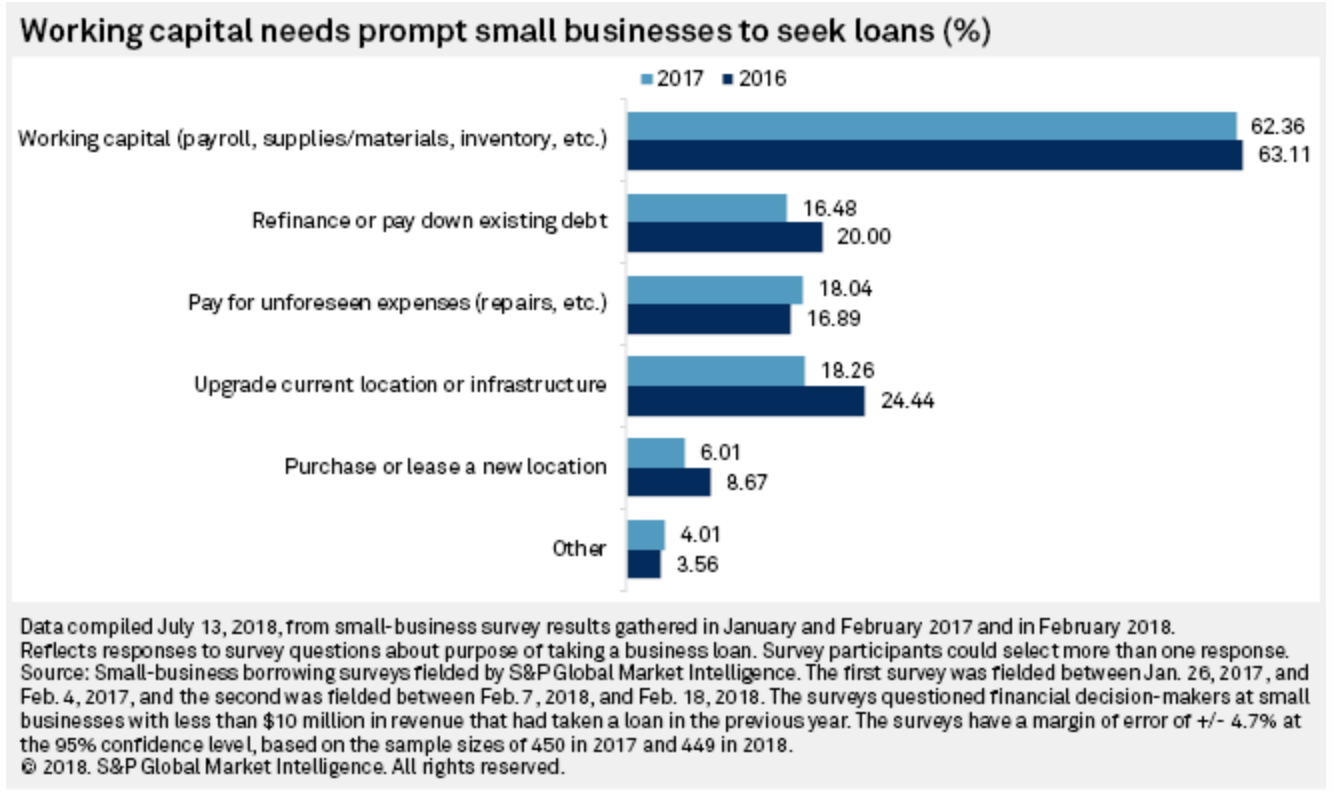

SME: why do they need the money?

Source: How can payments modernization benefit Canadian businesses? Evaluating the cost of payments processing; EY and Payments Canada, 2018

Can we get there with FinTech and PayTech?

gig economy instant pay

fast vendor payment and B2B & inter-company real time payments

Innovations in Non-physical Payments around the world

Cash-In

agent

Cash-Out

agent

and almost every other 905 tourist mall

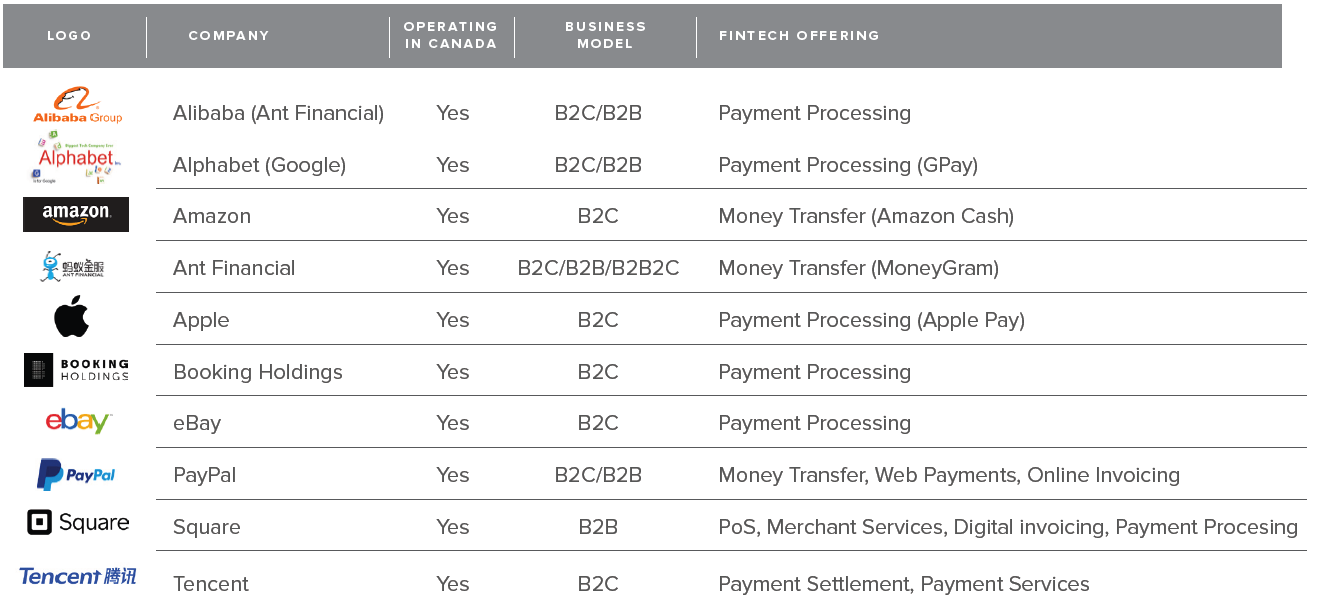

The Threat of Big Tech

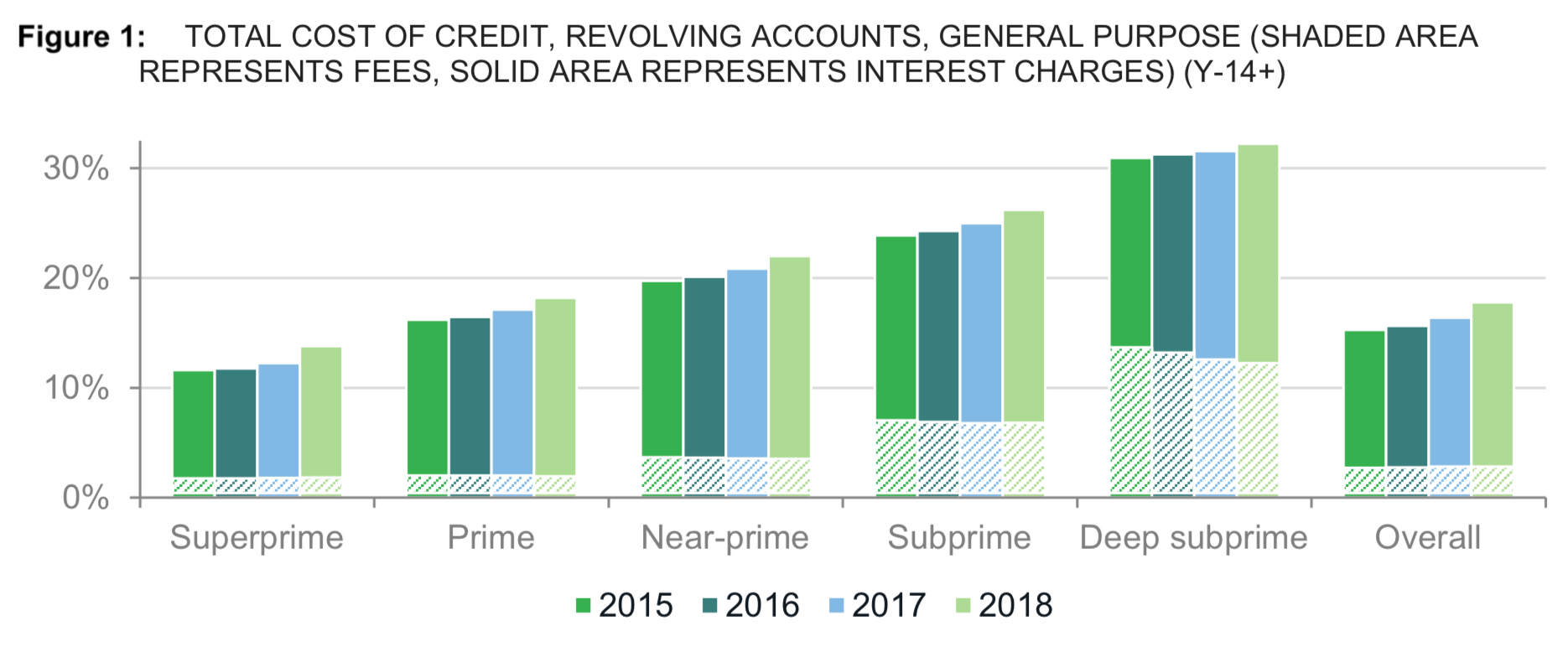

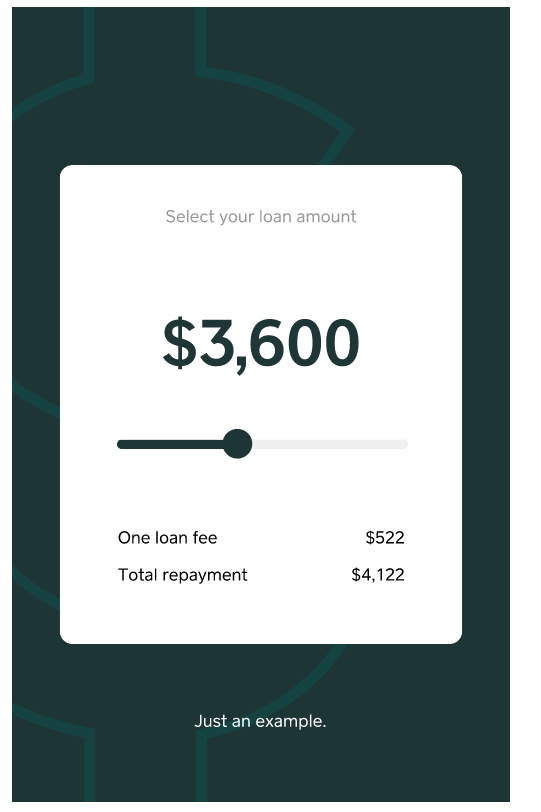

New frontier: revenue-based lending

14.5% interest - over what horizon?

Government Intervention

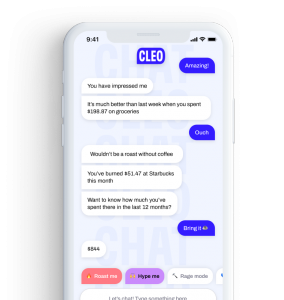

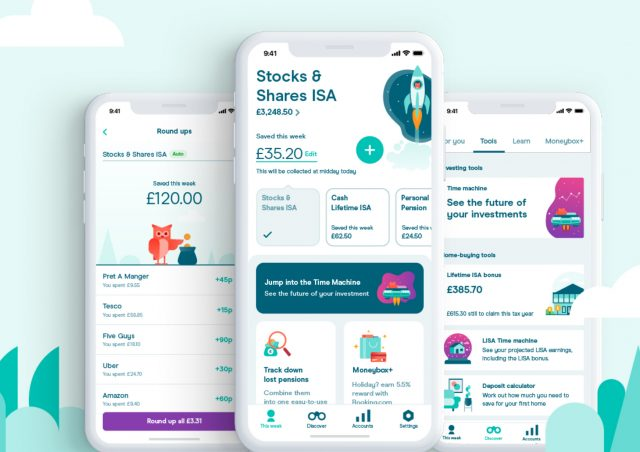

AI chatbot that chides you if you overspend and that advises you if an expense fits your budget

allows you to redesign your salary pay structure (make monthly weekly etc)

get alerts for suspicious transactions of elderly parents

Moneybox

aggregates all your banking related services

Source: Accenture Consulting Open Banking in Canada: Opportunity Knocks

End of Part 1 survey

please navigate again to

End of Part 1 debate

Setup: Random sorting into TWO groups

Format

Your task for the next 10 minutes

Outside Force #1: Decentralized Finance

What is a Cryptocurrency?

Conceptually: What is a Blockchain?

payments

stocks, bonds, and options

swaps, CDS, MBS, CDOs

insurance contracts

A blockchain is a

What makes DeFi different from TradFi

decentralized finance =

provision of financial service functionality without the necessary involvement of a traditional financial intermediary like a bank or broker-dealer*

digital media =

provision of information service functionality without the necessary involvement of a traditional information intermediary like a publisher, library, or newagency

*my take: applies to only commoditizable services

payments network

Stock Exchange

Clearing House

custodian

custodian

beneficial ownership record

seller

buyer

Broker

Broker

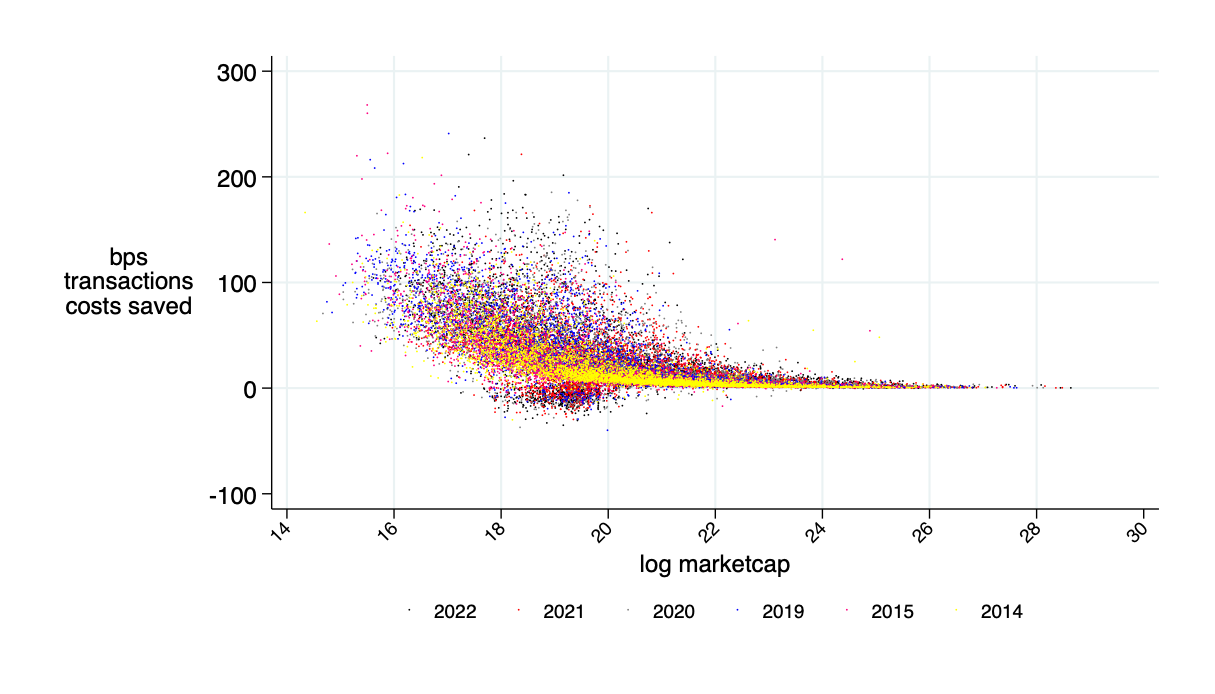

Source of savings:

Possible transaction cost savings: \(\approx\) 30%

Source: "Learning from DeFi: Would Automated Market Makers Improve Equity Trading?" working paper, Malinova & Park 2023

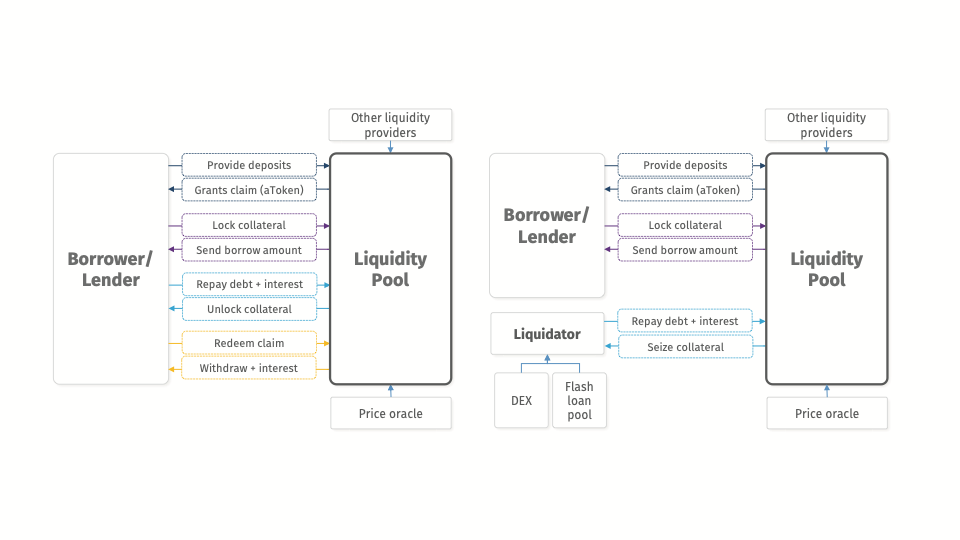

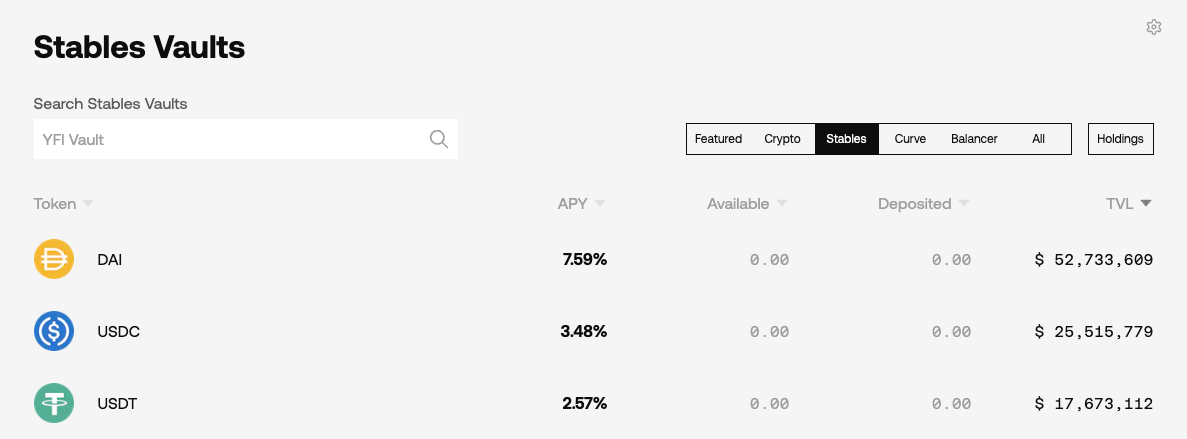

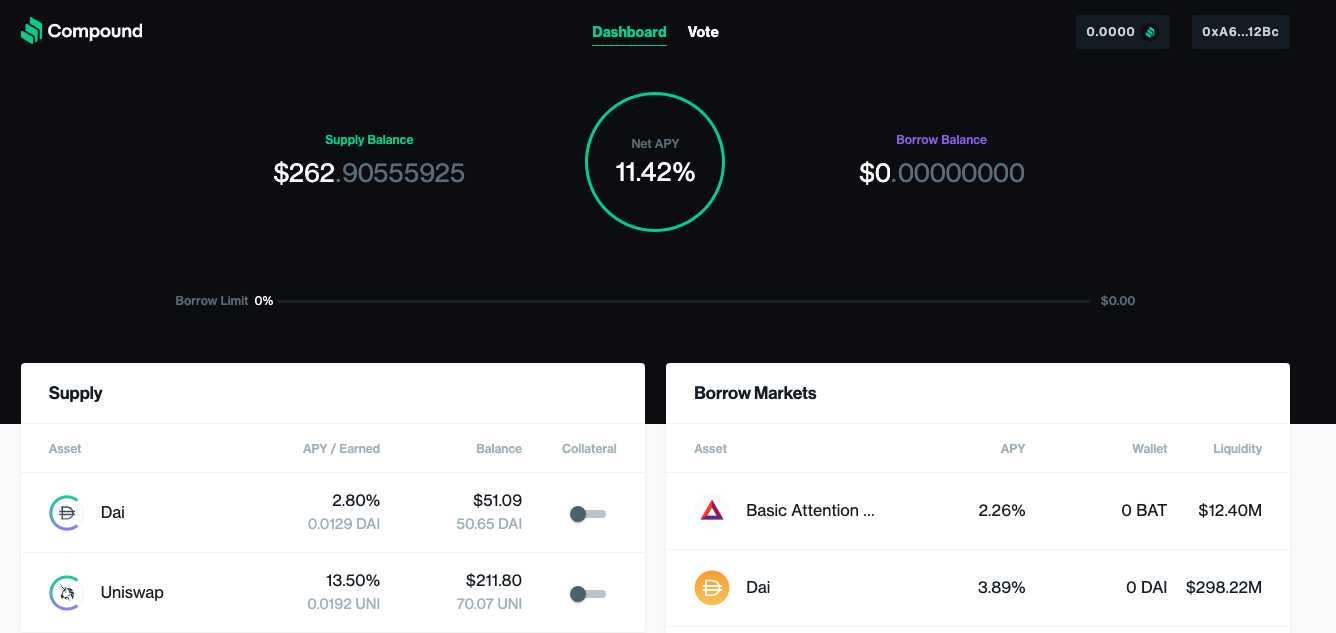

Application: Decentralized Borrowing & Lending

borrow

provide collateral

The Flow of Event: Normal Times

The Flow of Event: Collateral Liquidation

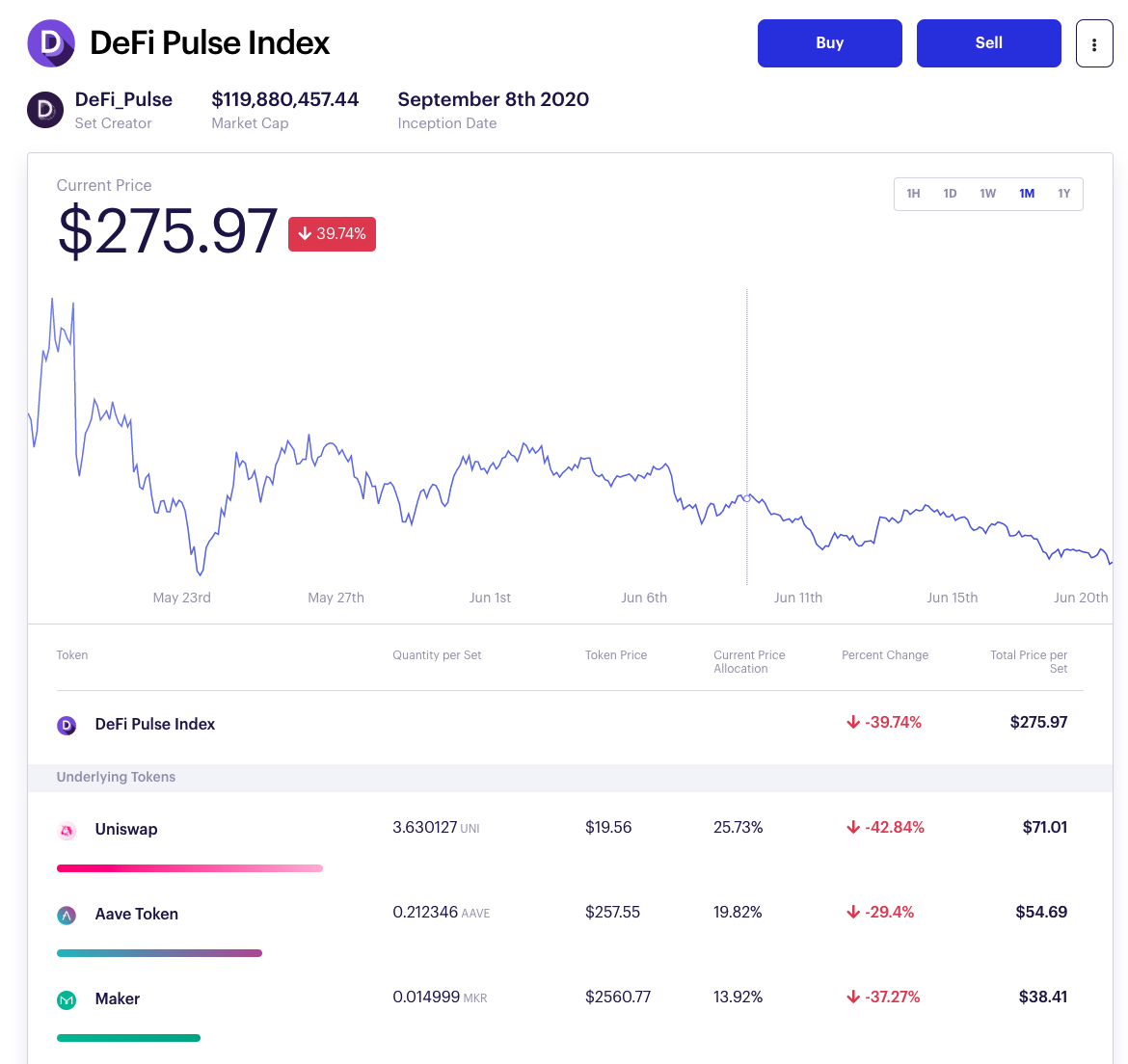

Obvious Smart Contract Application: Automate Investment Strategies

idea: create new mutual fund like asset

"yield aggregator:" push capital where rate of return is highest

Peer-to-peer \(\Rightarrow\) Platforms

liquidity \(\nearrow\)

volume \(\nearrow\)

protocol fees \(\nearrow\)

token value \(\nearrow\)

Platform economics is tricky:

it works!

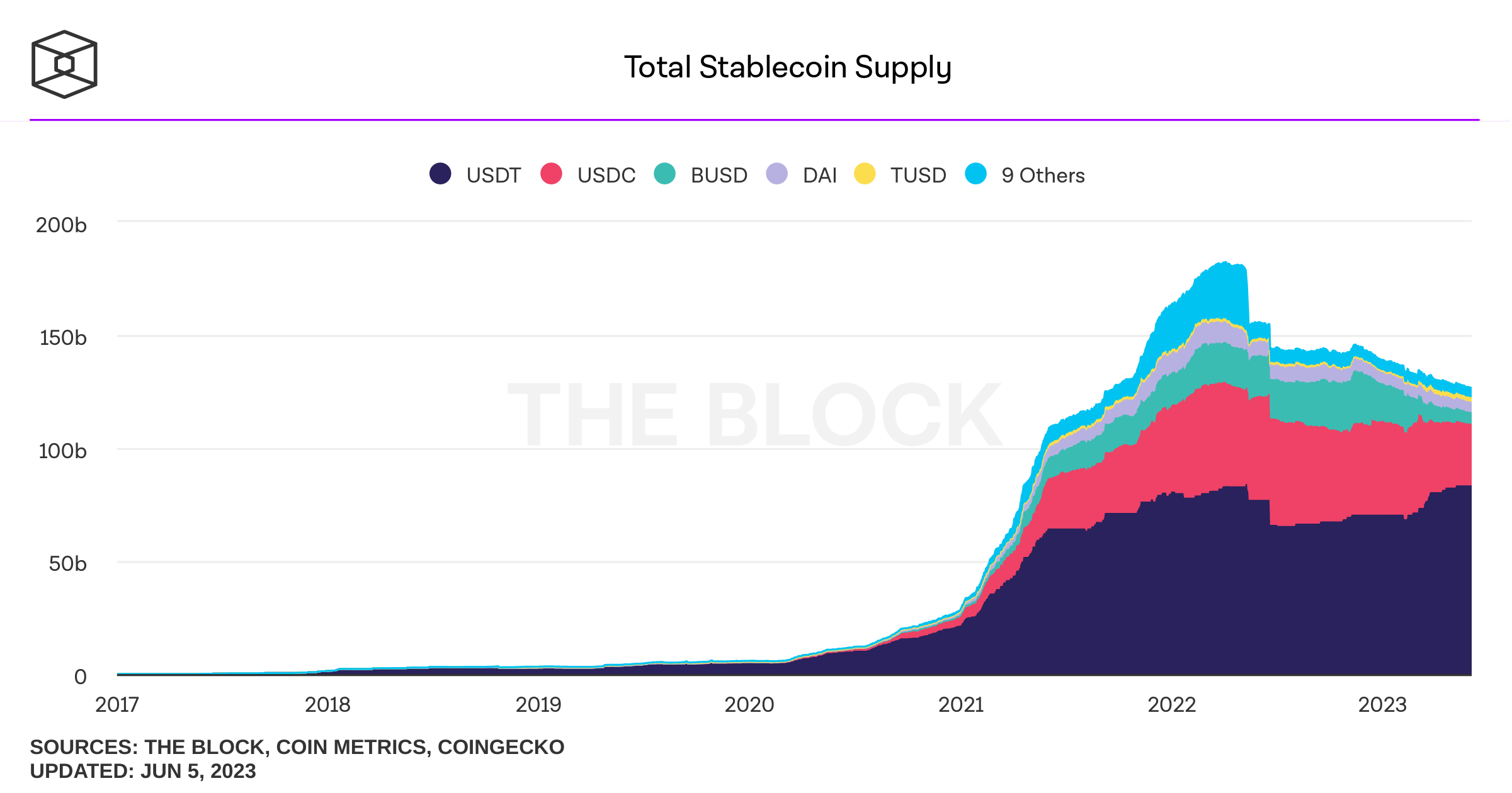

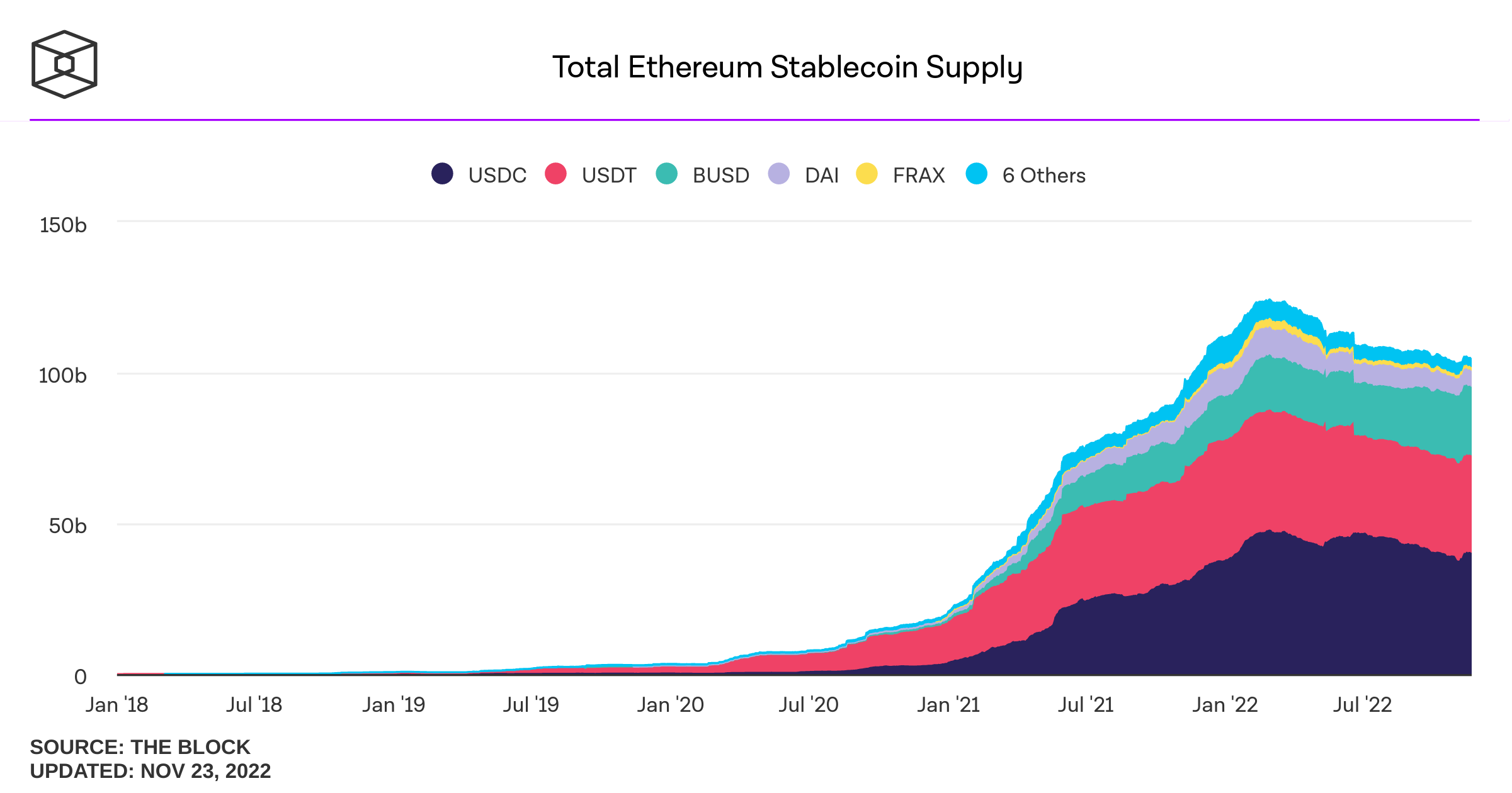

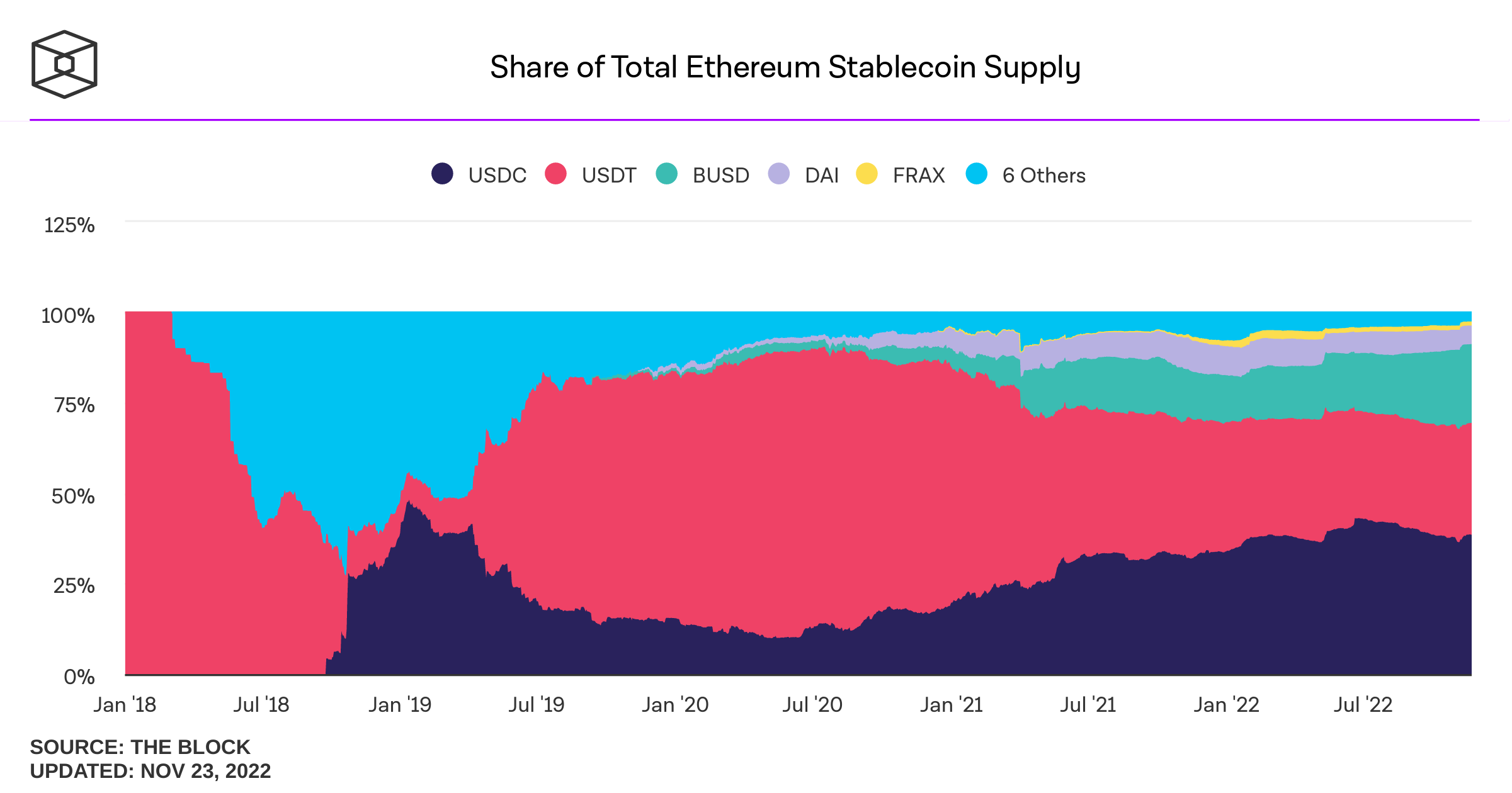

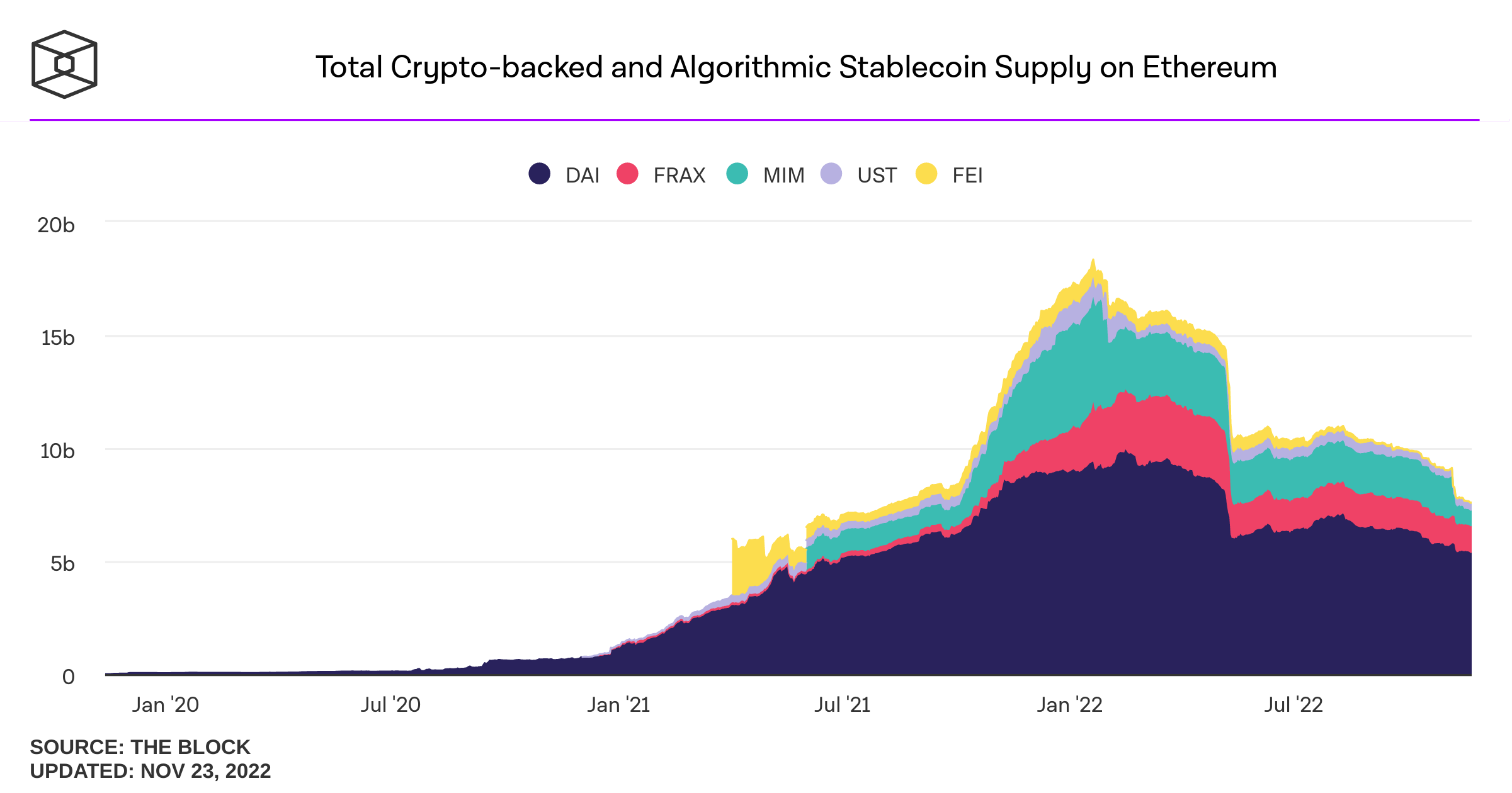

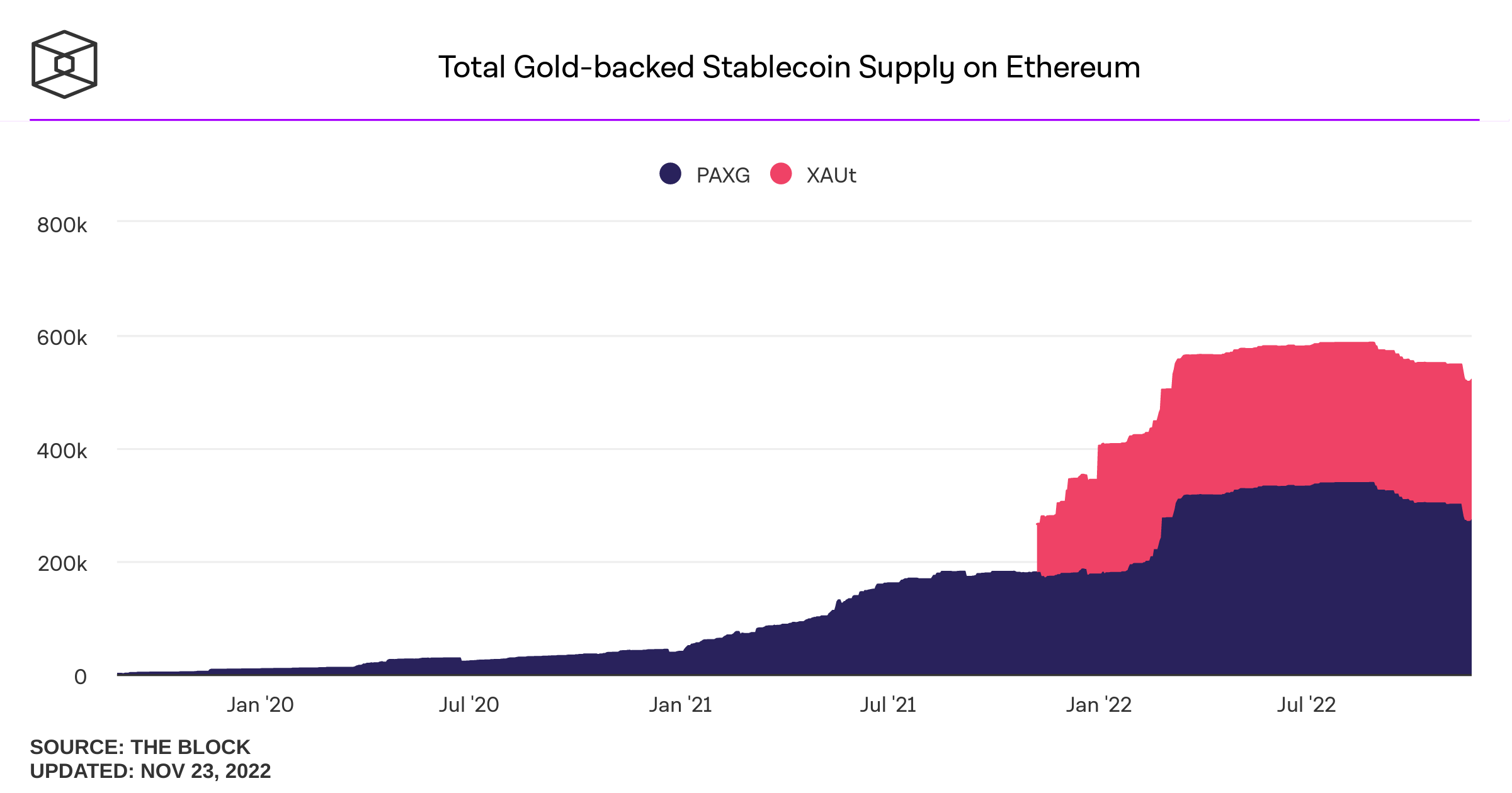

Stablecoins

Stablecoins: Digital Representations of the USD

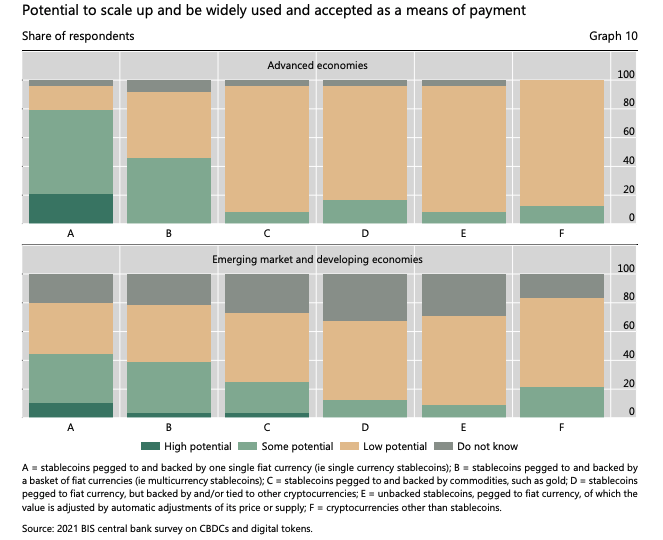

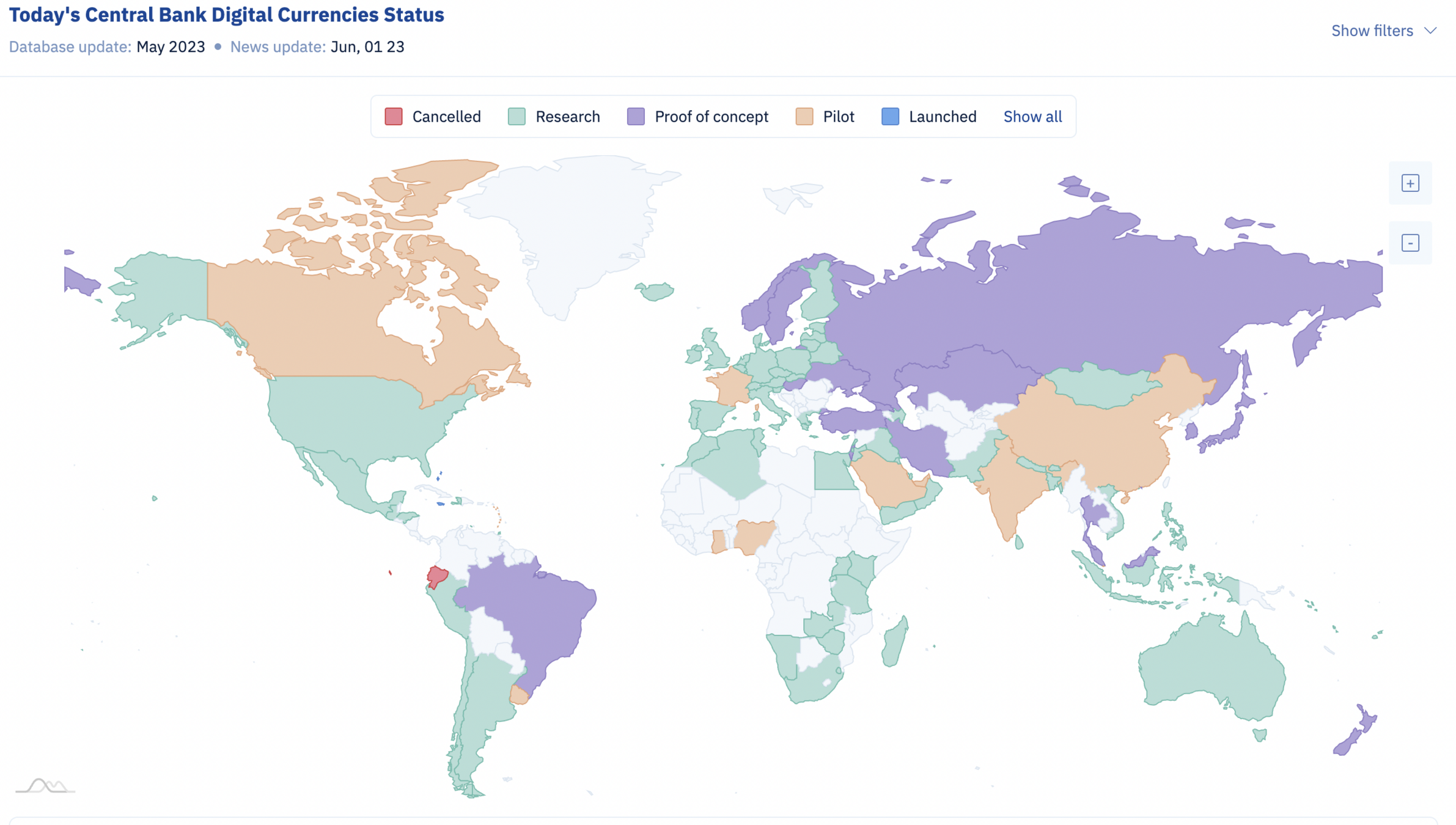

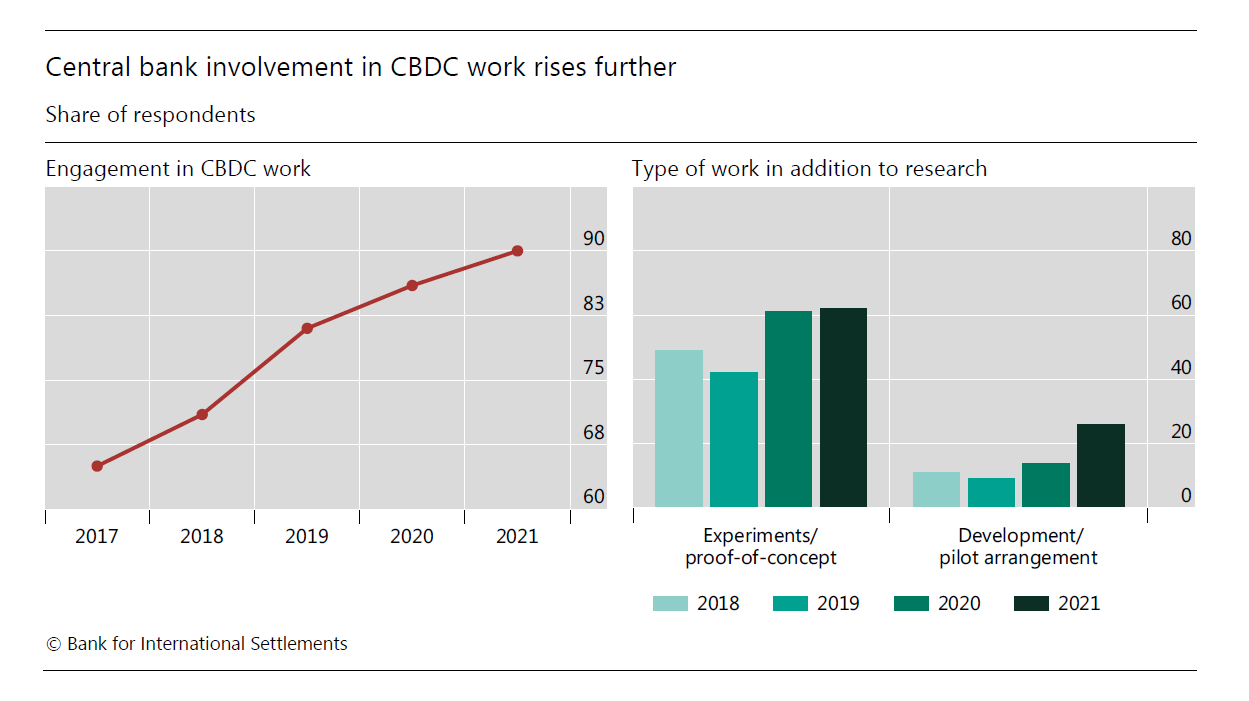

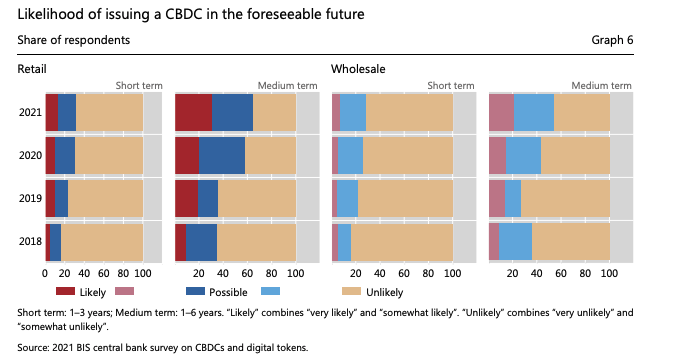

BIS Survey of Central Banks:

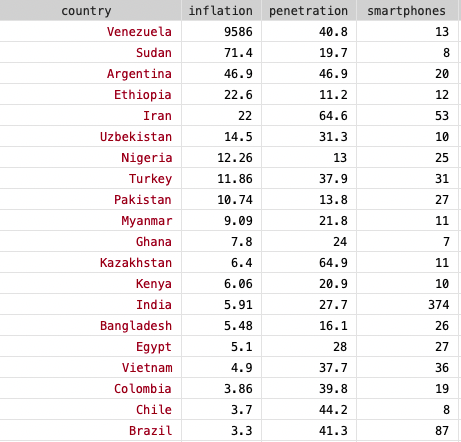

cellphone data from 2018 (NewZoo), inflation from 2020 (World Population Review)

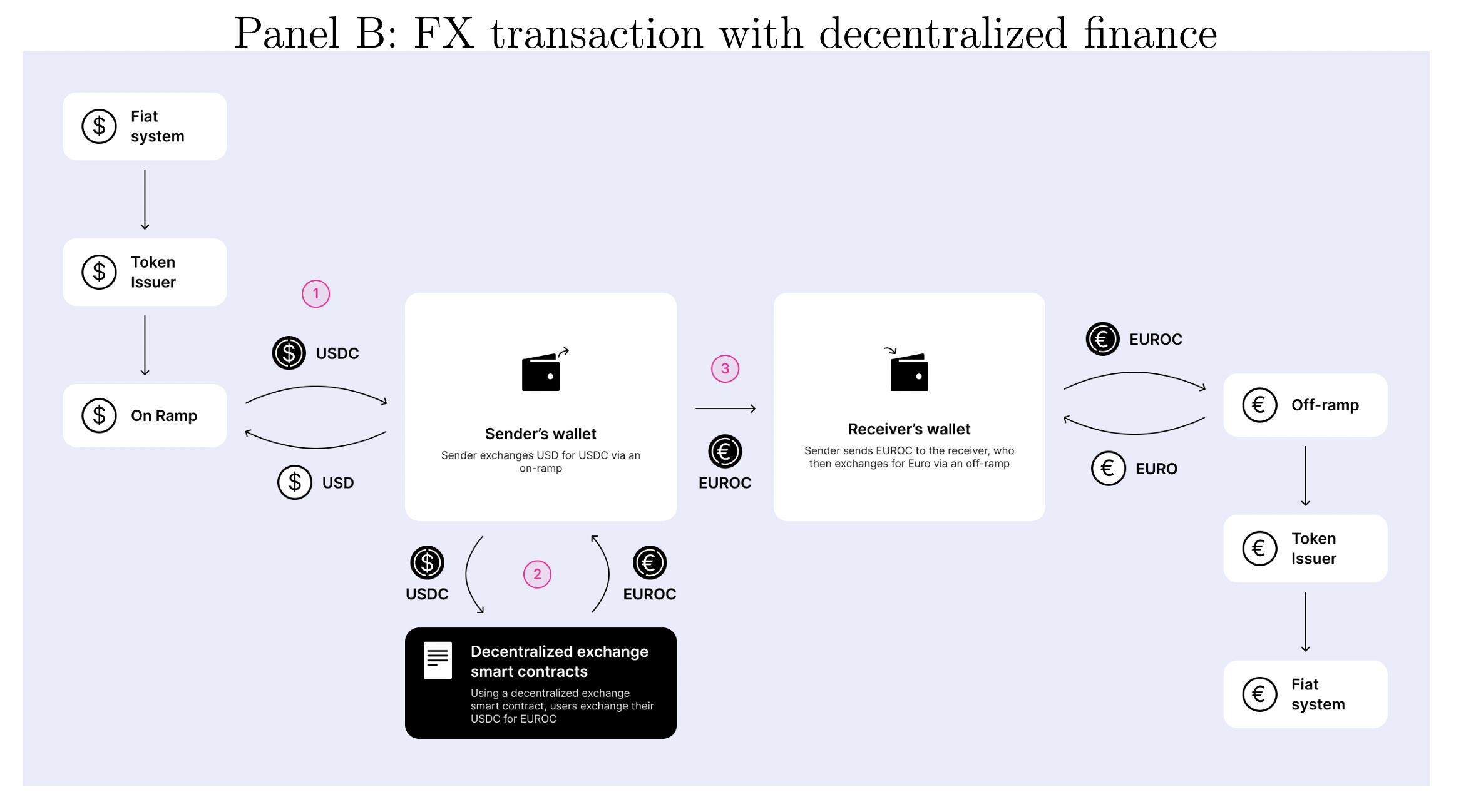

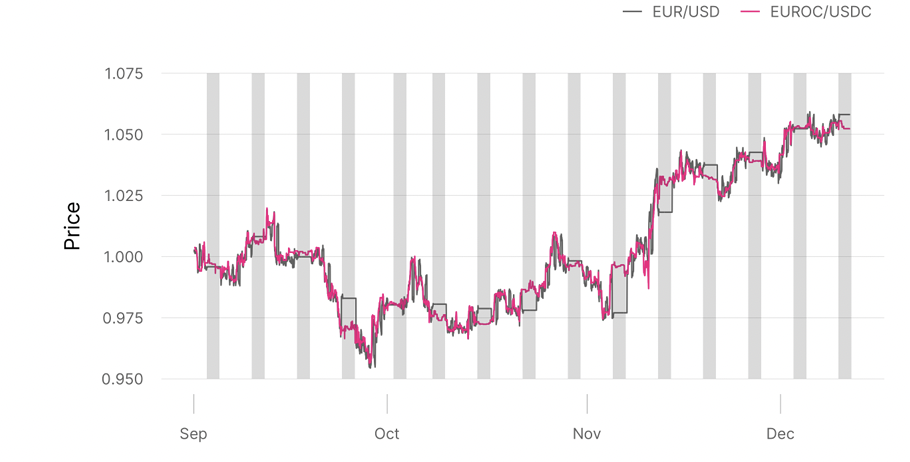

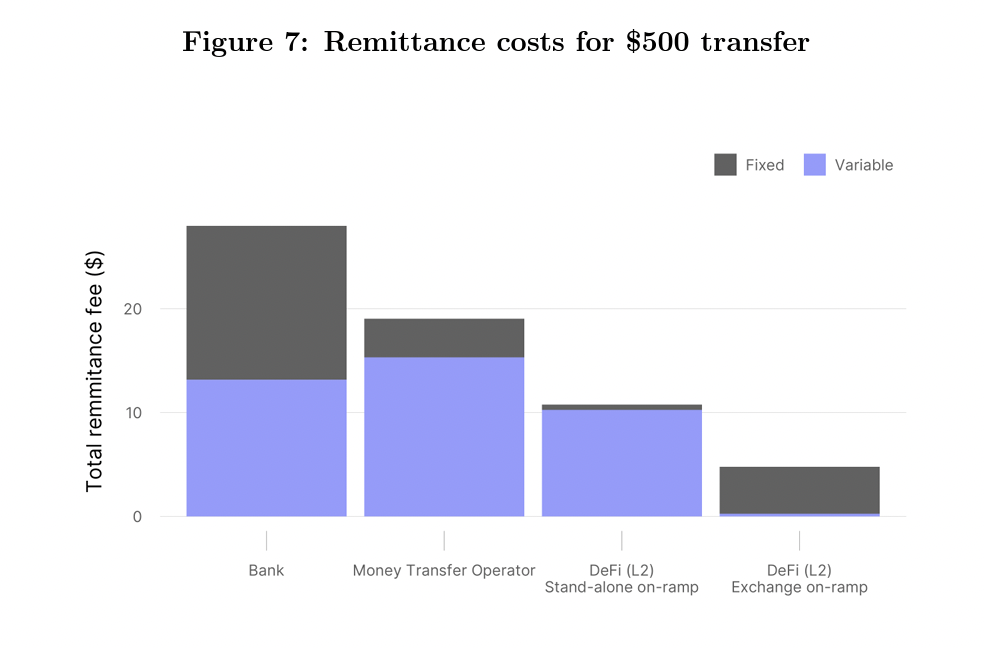

Source: On-chain Foreign Exchange and Cross-border Payments by Austin Adams, Mary-Catherine Lader, Gordon Liao, David Puth, Xin Wan (2023) [team from UniSwap Labs]

DeFi fees:

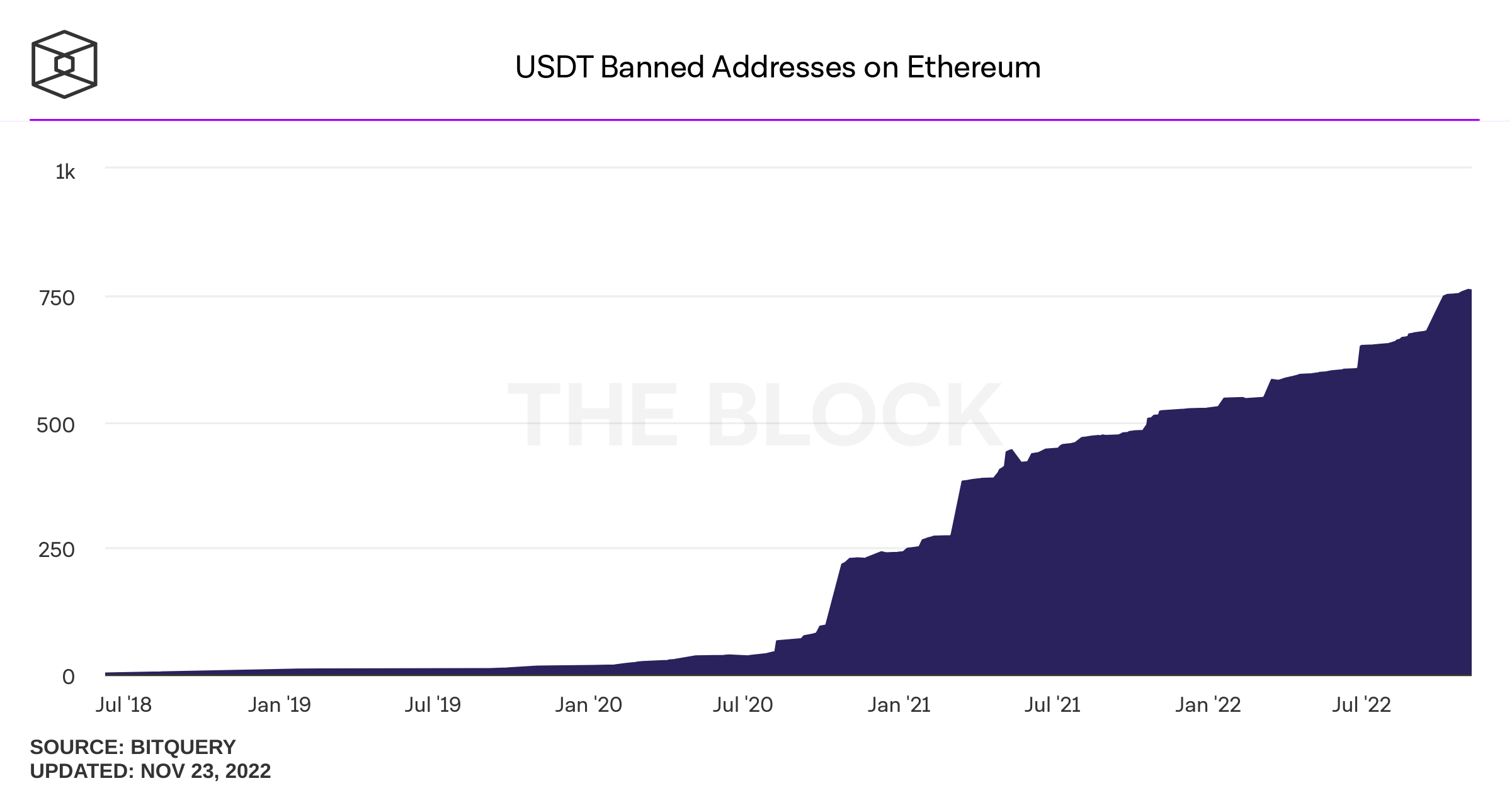

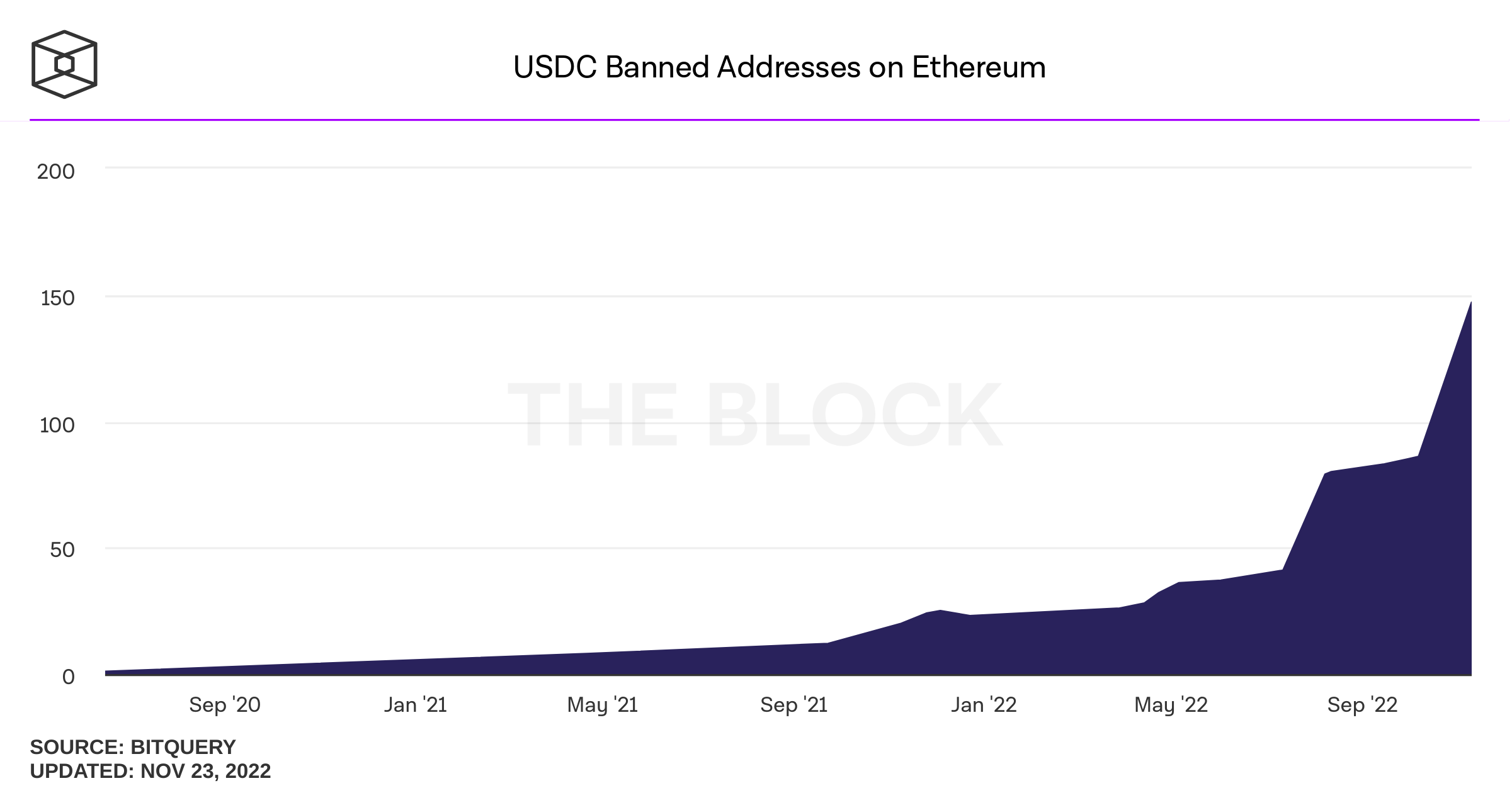

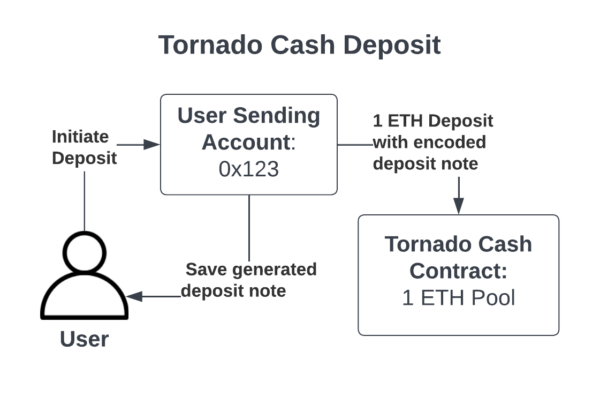

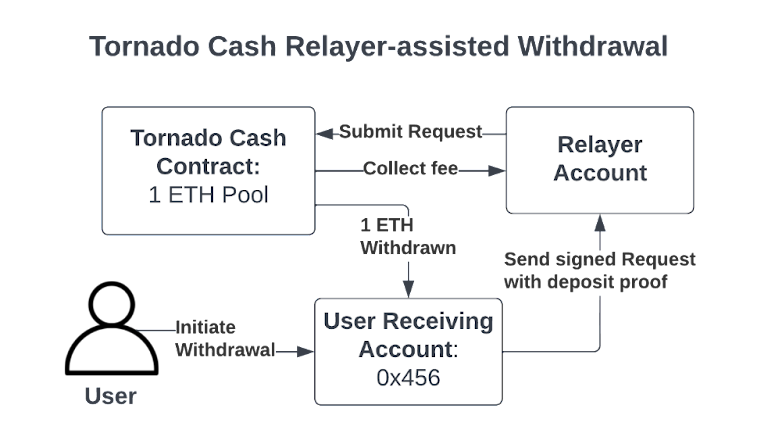

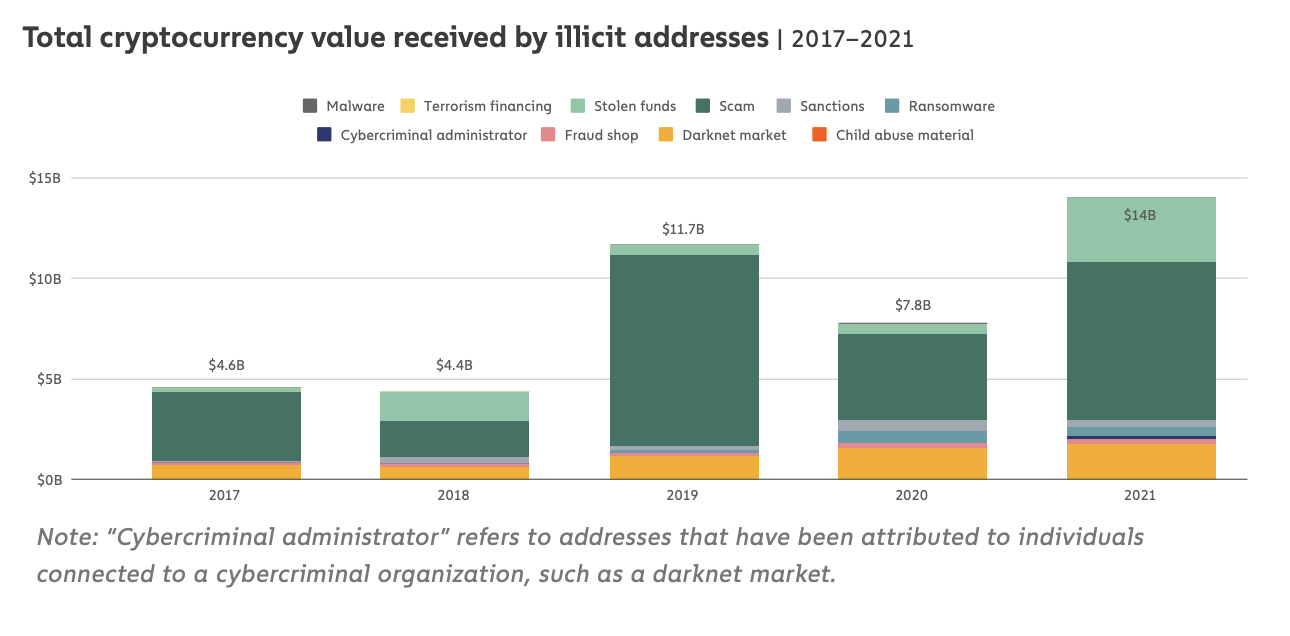

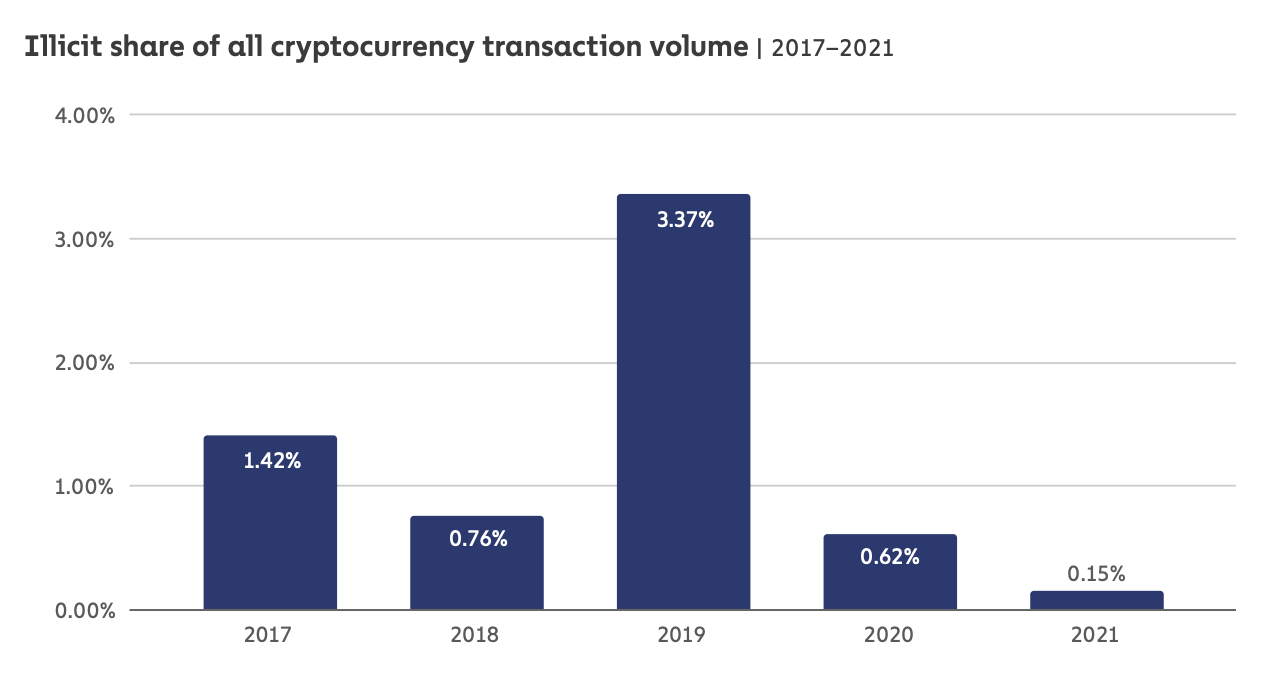

Money Laundering and Crime

extra info:

Outside Force #2:

Central Bank-Issued Digital Currencies

Evolution

(now defunct)

CBDCs are on their way

Chrystia Freeland Justin Trudeau

of all things crypto and digital in Canada

fast money

real time rails run by chartered banks

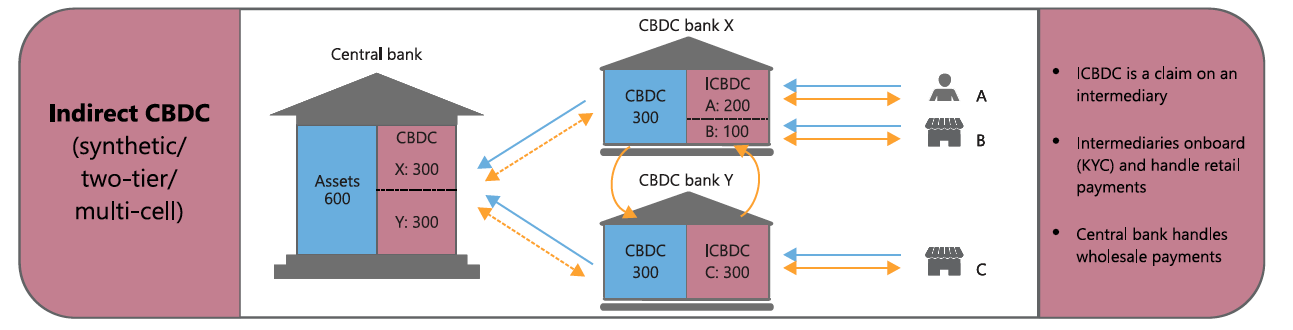

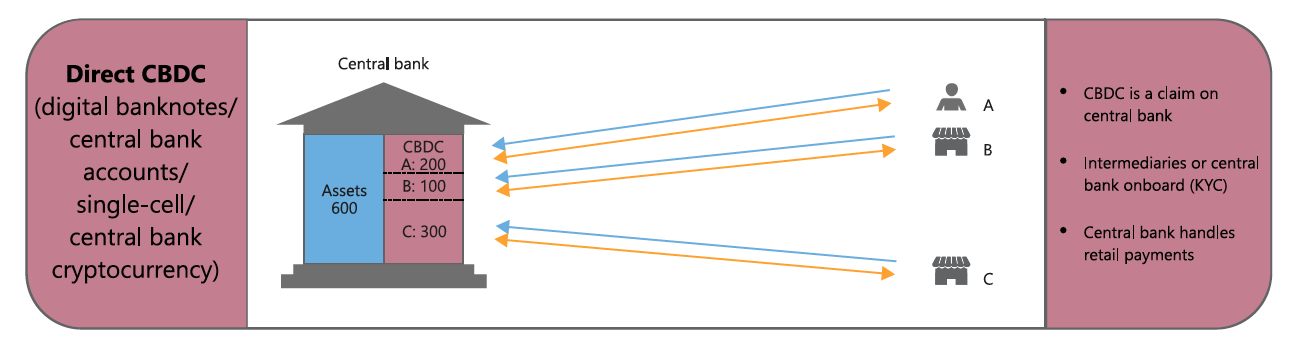

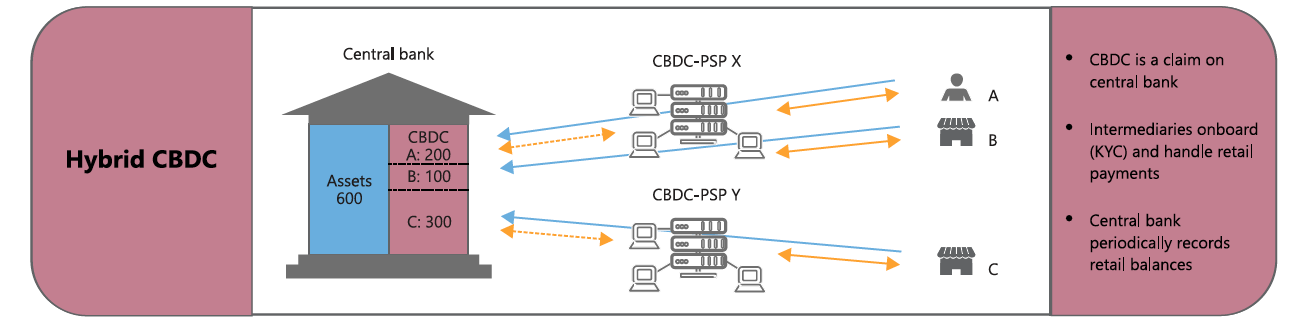

CBDC

run by

chartered banks

run by

Bank of Canada

new communually run system

Stablecoin

private firm (e.g. Facebook)

CBDC on public blockchain

chartered bank-issued on public blockchain

The Bank of Canada's Contingency Plan (Feb 2020):

Consider Issuing CBDC if:

Will they?

Veneris, Park, Long, Puri (2021): BoC is in a legal position to issue a CDBC and there are several legal paths to do so

Can they?

What's Next?

CBDCs

End of Part 2 survey

please navigate again to

End of Part 2 debate

Setup: Random sorting into TWO groups

Format

Your task for the next 10 minutes

@financeUTM

andreas.park@rotman.utoronto.ca

slides.com/ap248

sites.google.com/site/parkandreas/

youtube.com/user/andreaspark2812/

banking and payments activity require a banking license

need approval of the Finance Minister and the Office of the Superintendent of Financial Institutions (OSFI)

providing any financial service

acting as a financial agent

providing investment counselling or portfolio management services

issuing payment, credit, or charge cards,

operating a payment, credit, or charge card plan in co-operation with others (including other financial institutions)

granting of bank license has extensive list of regulatory criteria (subject to political interpretation)

takes 2 to 5 years to successfully acquire a banking license in Canada

Rogers applied in 2011 and was granted a Schedule I bank license in 2013

most FinTechs and PayTechs do not have the time or money to acquire a banking license

PayTech demonstrated use and purpose of prepaid card to regulator

OSFI rep had never seen one, not had any experience in dealing with the regulatory implications of this product.

OSFI and others do not have Fintechs and PayTechs in scope (not yet threat to the safety and soundness of the financial system).

EXAMPLE #1

regulatory compliance = lawyers

lawyers = second line of defence teams at FI

\(\Rightarrow\) decision makers have very little access to clients and the frontline.

EXAMPLE #2

good at general service and infrastructure

banks have very rigid ways of engaging with their clients, “they push information, they don’t take it”

\(\Rightarrow\) poor at customization and customer service

Banks' Modus Operandi

Premise of FinTech

start with customer needs and then build platforms

Source: Seizing The Opportunity: Building The Toronto Region Into A Global Fintech Leader; TFI/Deloitte/McMillian 2019

Source: Seizing The Opportunity: Building The Toronto Region Into A Global Fintech Leader; TFI/Deloitte/McMillian 2019

loyalty

Payment financing

mobile payment integration

mobile payments + rewards

connect advertising directly with immediate mobile purchasing option

personal payment management app

Payment financing + loyalty

Overall idea: increase visibility of payments across the supply chain and across internal business operations

property management and rent payments

B2B & inter-company real time payments

gig economy instant pay

fast vendor payment

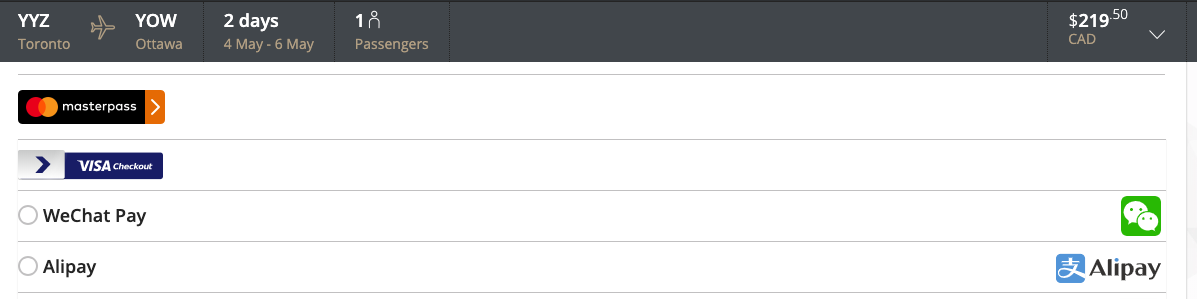

North American merchants connect to Chinese consumers who use WeChat & Alipay

https://www.youtube.com/embed/g1IqjY88YuM?enablejsapi=1

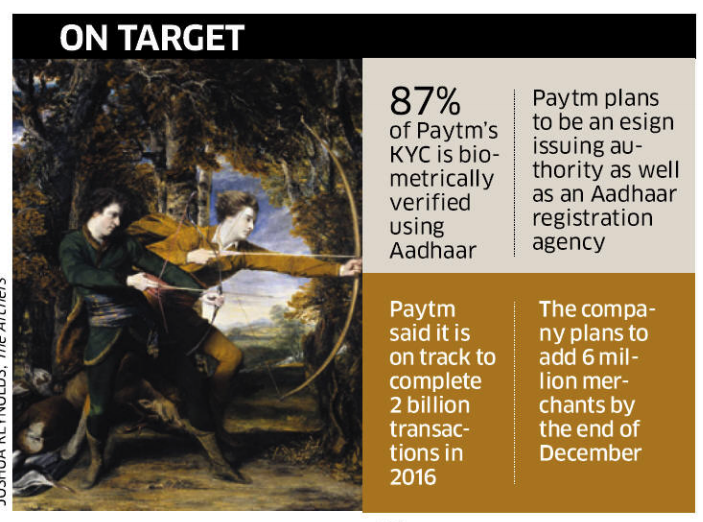

"To empower residents of India with a unique identity and a digital platform to authenticate anytime, anywhere."

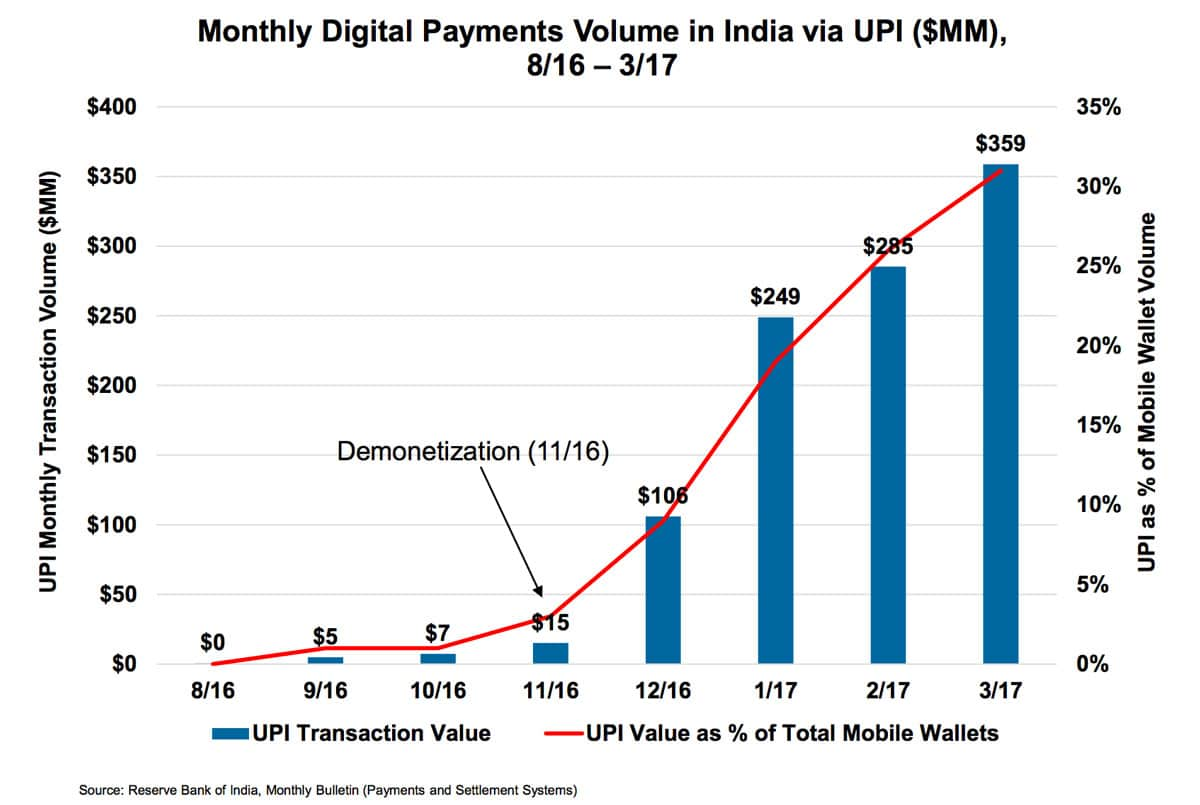

UPI puts multiple bank accounts into a single mobile application (of any participating bank), merging several banking features, seamless fund routing & merchant payments under one hood.

Why we should be skeptical of untethered AI

\(\vdots\)

Smart Contract Derivatives with Synthetix

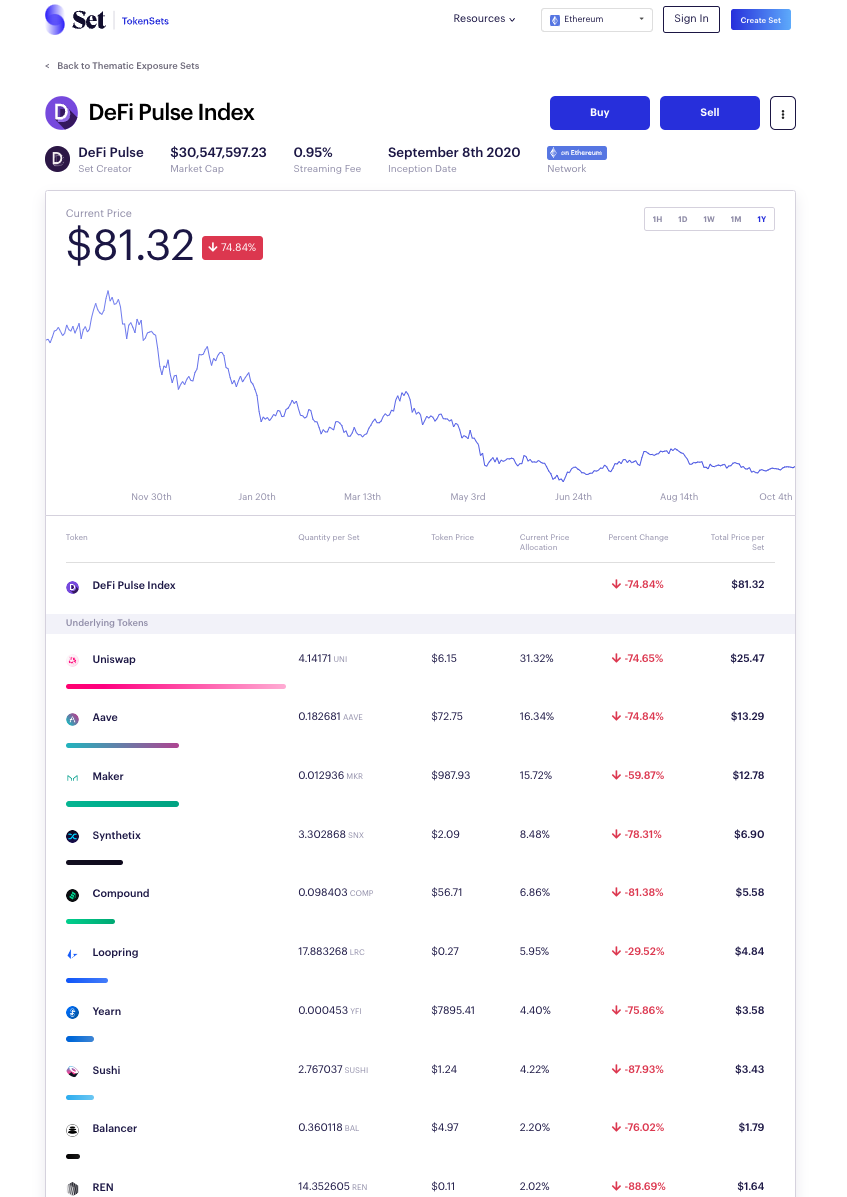

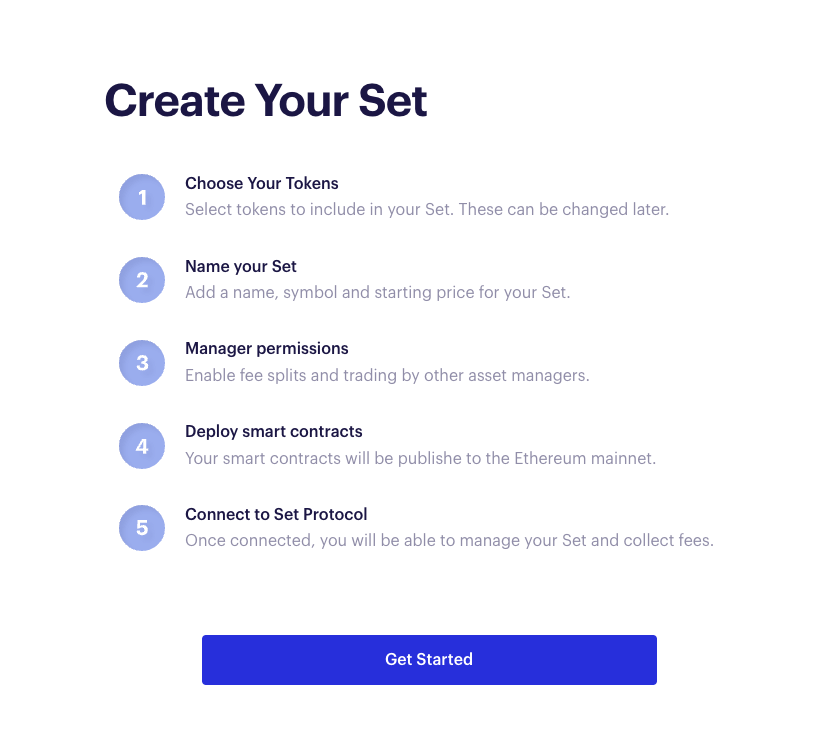

Securities Creation: Tokensets

idea: create new mutual fund like asset

Risks and open problems

Partnerships

"new financial infrastructure"

When it goes live, it will come with extensive "layer two" functionality

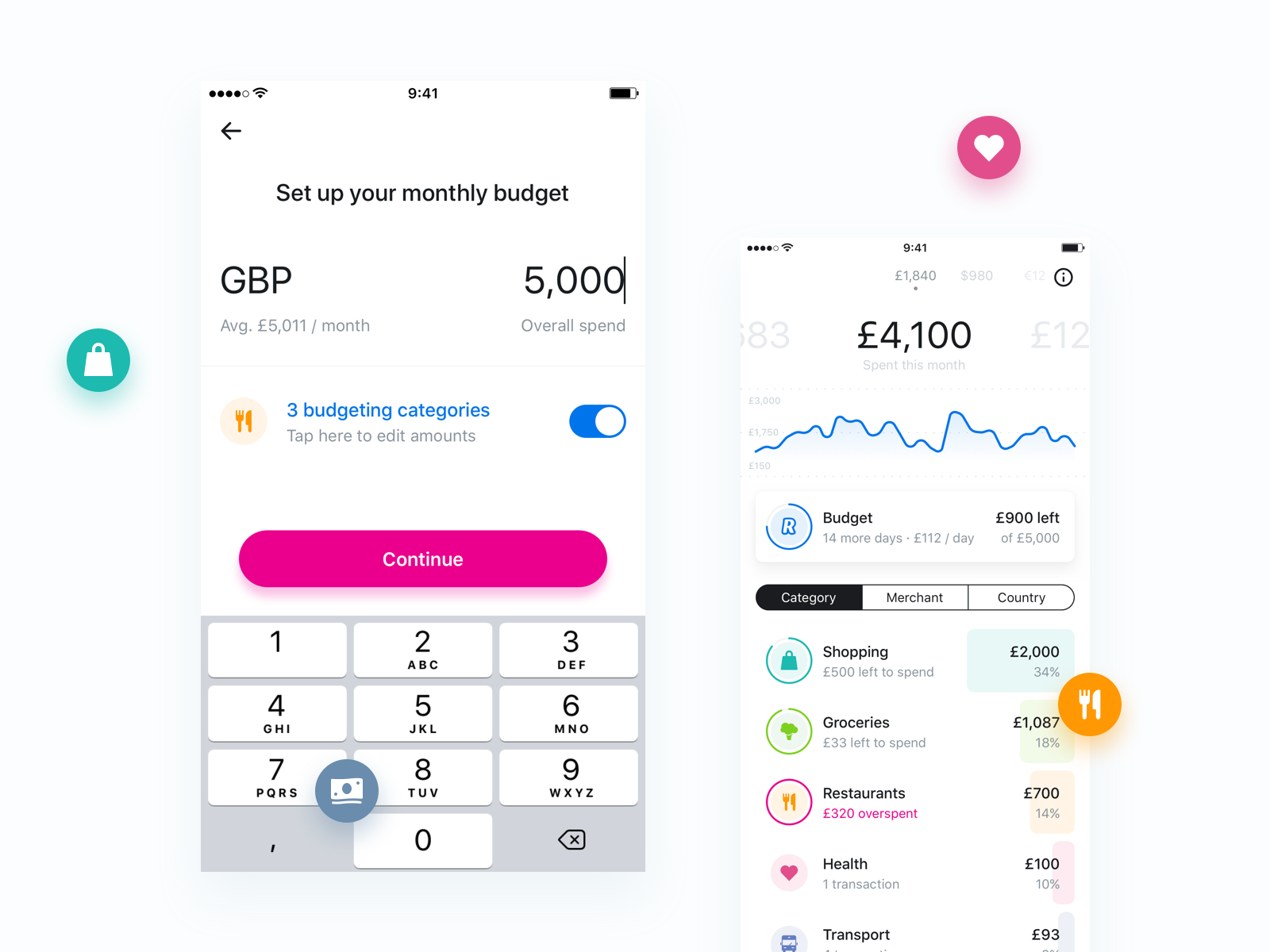

How much money is coming into and out of the account each month

Spending habits: what you spend money on and where you spend it

Payment habits: Are you paying bills way ahead of deadline or tardy?

Source: BIS Quarterly Review, March 2020

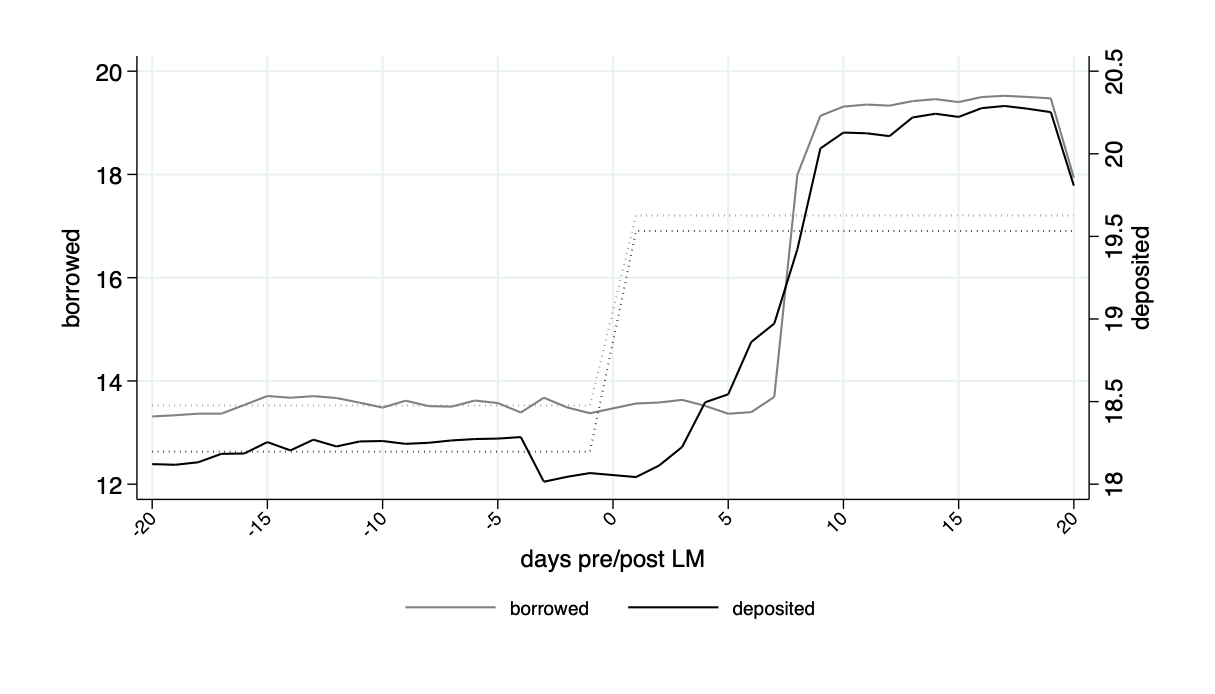

BoC analysis (August 2020):

By Andreas Park