Andreas Park PRO

Professor of Finance at UofT

Stablecoins, Tokenization, and CBDCs

Instructor: Andreas Park

What is money?

store of value

unit of account

method of exchange

What's the relationship of payments and monetary policy?

A

B

\(-\)

0

+

A

B

0

+

\(-\)

Option 1: borrow from BoC

lending rate:

deposit rate:

target rate

target rate\(+\)25bps

target rate\(-\)25bps

A

B

0

+

\(-\)

Option 2: borrow from another bank

target rate

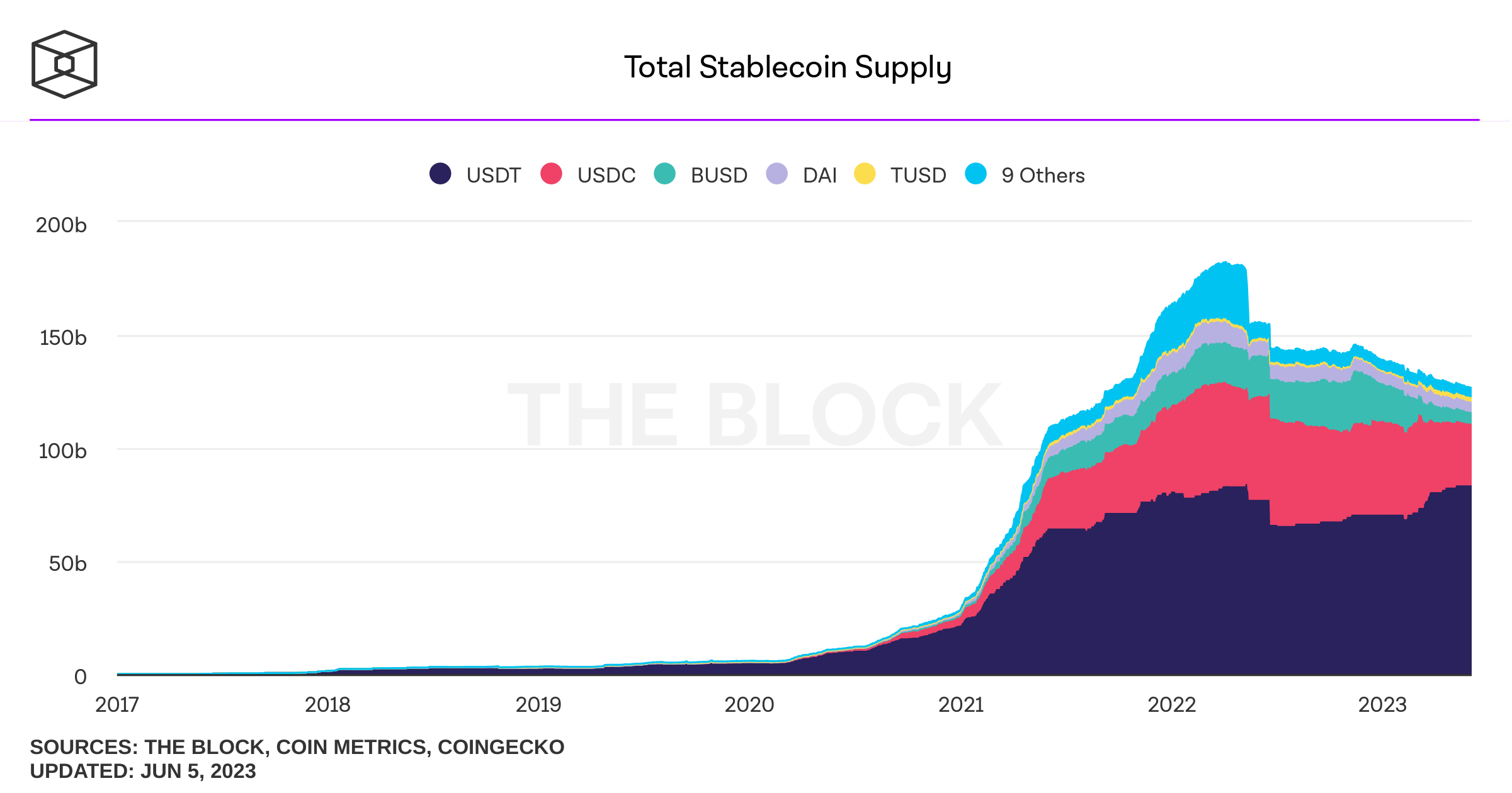

Stablecoins

pulled from Nick Carter's talk on "Will stablecoins serve or subvert U.S. interests?"

JPM coin

USDC

USDT

TUSD

DAI, FEI

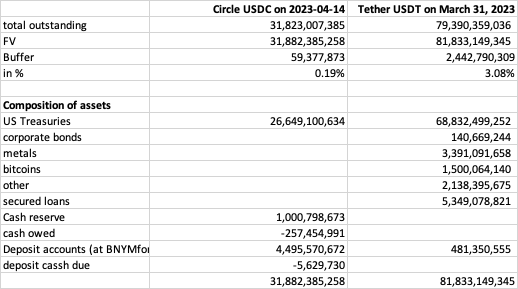

Collateral Backed Stablecoins: USDT & USDC

\(\Rightarrow\) 5% over-collateralized

primary market acces: 6 entities only

Collateral Backed Stablecoins: USDT & USDC

primary market acces: 560+ entities

What makes a Stablecoin stable?

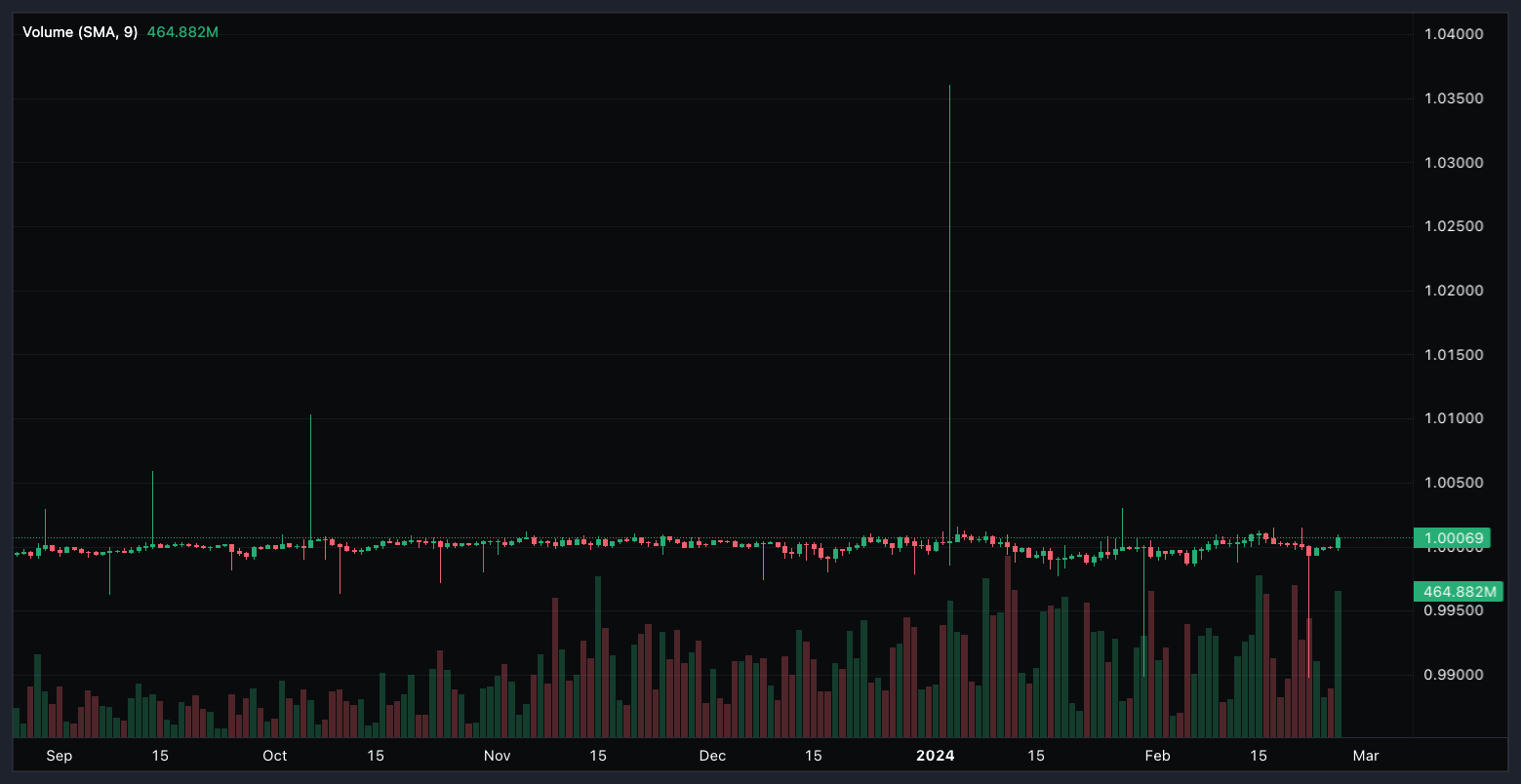

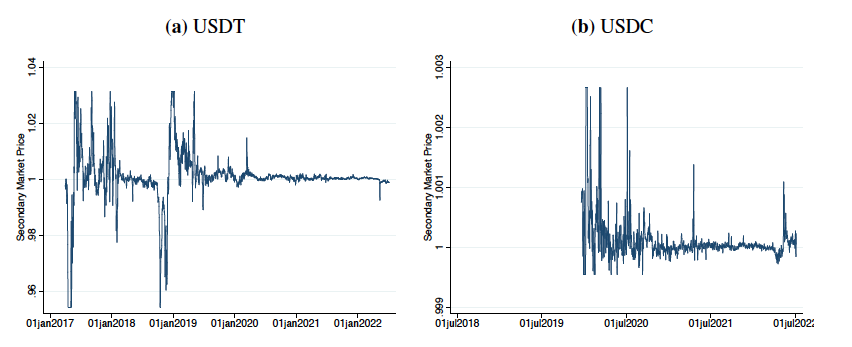

USD-USDT (6 months)

\(\Rightarrow\) need a primary/reference market mechanism to allow for forces of arbitrage to align prices

Arbitrage when price(stablecoin)>$1

collateralized stablecoin

arbitrageur

issuer/ primary market

secondary market

collateralized stablecoin

arbitrageur

Arbitrage when price(stablecoin)<$1

issuer/ primary market

secondary market

What makes a Stablecoin stable?

What makes a Stablecoin stable?

in crypto:

fully collateralized

issuer

under-collateralized

smart contract

Case 1: price(1 SC) \(>\) 1 FU \(\to\) SC expensive

collateralized stablecoin

arbitrageur

issuer

market

Case 2: price(1 SC) \(<\) 1 FU \(\to\) SC cheap

collateralized stablecoin

arbitrageur

issuer

market

A thought experiment for a stablecoin

Option 1a (existing cash):

Option 1b (convert cash to digital):

Option 2 (overcollateralized):

Option 3 (exotic):

What are Apple's options?

Thought experiment: Apple Inc. wants to issue a stablecoin

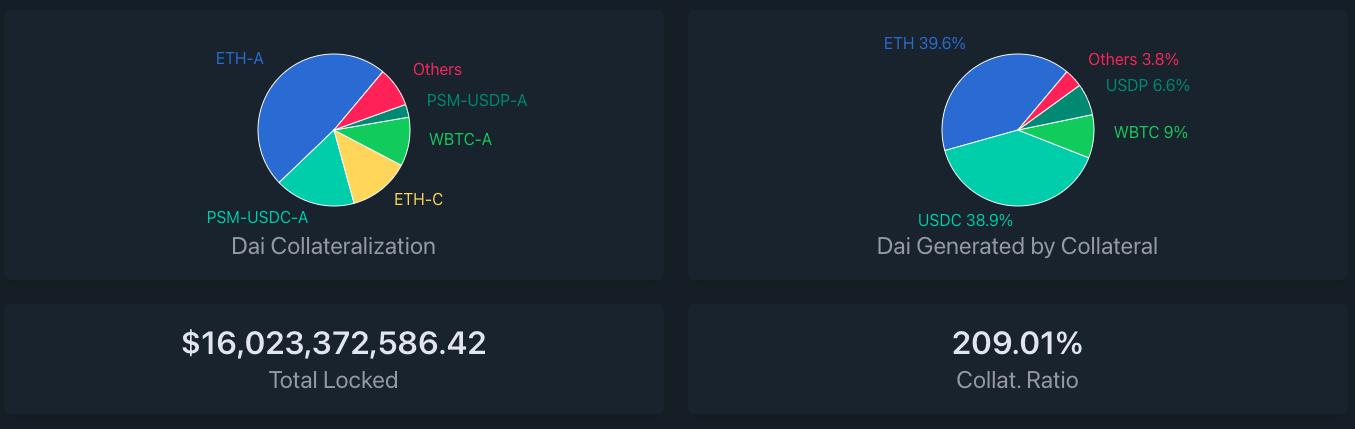

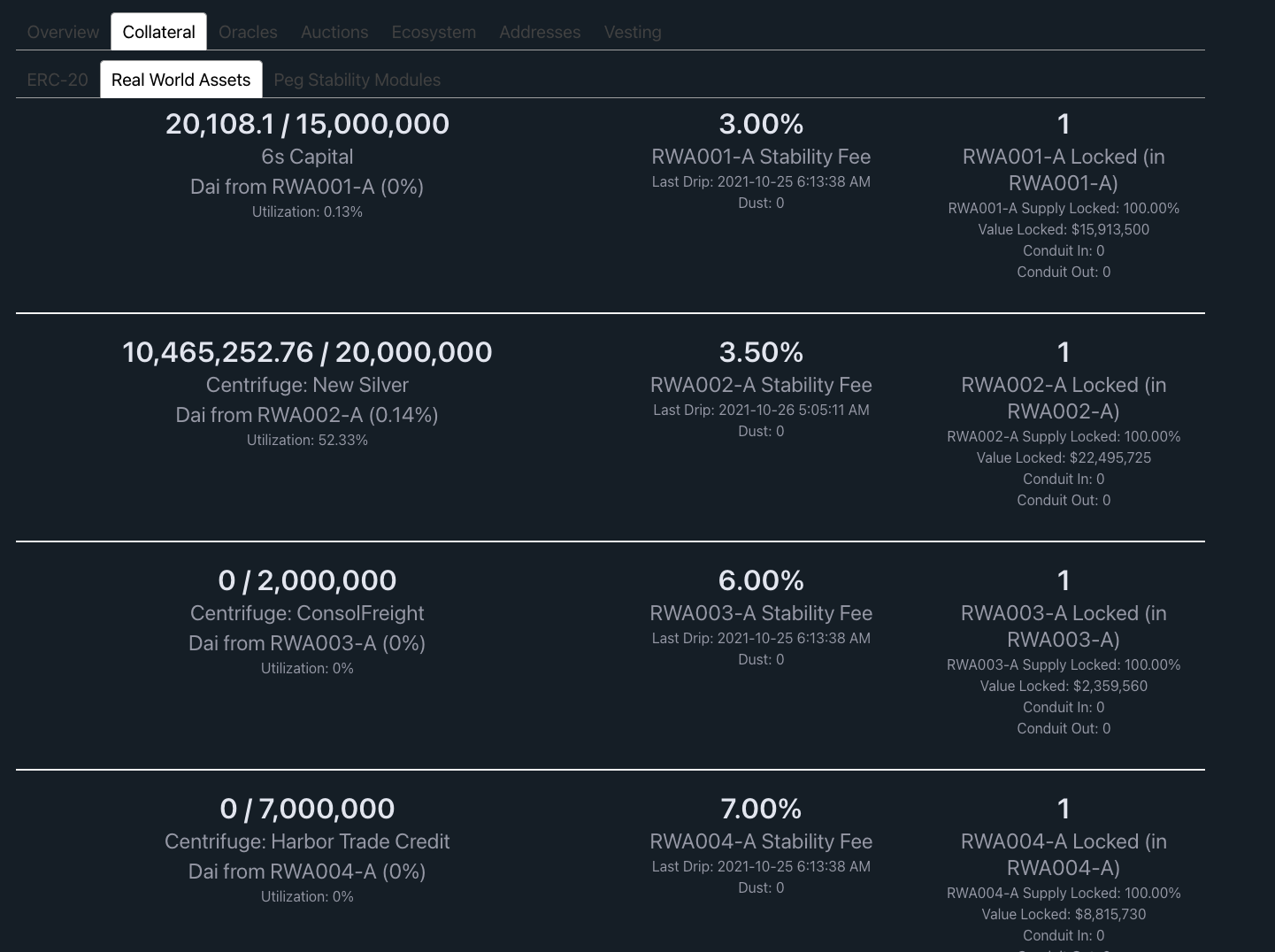

MakerDAO's DAI

(or: Apple's Option 2)

4 ETH

(1 ETH = $375)

(Oct 15, 2020)

\(\approx\) $1,500

\(\vdots\)

1,500 DAI

(1 DAI = $1)

formally: this smart contract is a collateralized debt position (CDP)

fractional collateral \(\to\) collateralization factor \(=\) 150%

total collateral = $1,500

maximum loan = $1000

overcollateralization = $500

actual loan (example) = $500

buffer = $500

ETH \(\nearrow\) $500

value of ETH collateral = $2,000

maximum loan = $2,000/150%=$1,333

total collateral = $2,000

maximum loan = $1,333

overcollateralization = $667

actual loan (example) = $500

buffer = $500

overcollateralization = $667

new loan capacity= $333

ETH \(\searrow\) $187.5

value of ETH collateral = $750

maximum loan = $750/150%=$500

total collateral = $750

maximum loan = $500

overcollateralization = $250

actual loan (example) = $500

buffer = $0

for reference: former value of collateral

ETH \(\searrow\) $150

value of ETH collateral = $600

maximum loan = $600/150%=$400

total collateral = $600

maximum loan = $400

required overcollateralization = $200

actual loan (example) = $500

buffer = -$100

for reference: former value of collateral

\(\Rightarrow\) triggering of liquidation auction by "keeper"

sell 3.33 ETH=$500=500 DAI

repay $500=500 DAI loan

retain incentive

return remainding ETH to vault owner

borrowers of DAI need to pay interest \(\to\) stability fee

DSR paid on "locked" DAI

total amount of debt (or DAI) outstanding is limited

Sidebar: how is this decided?

\(\to\) special "governance" token MKR

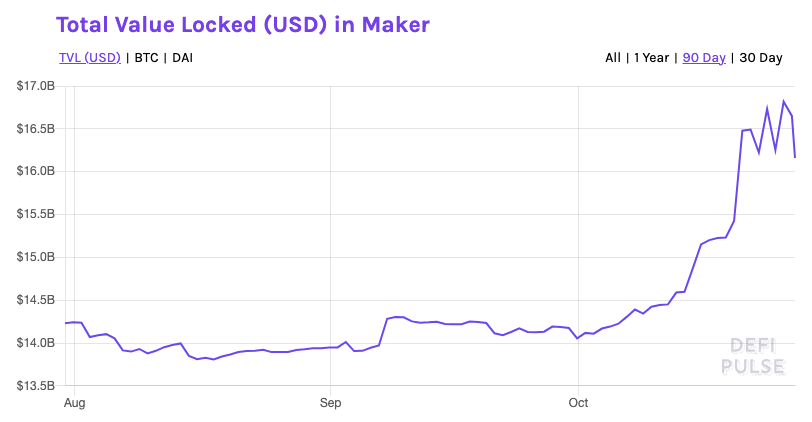

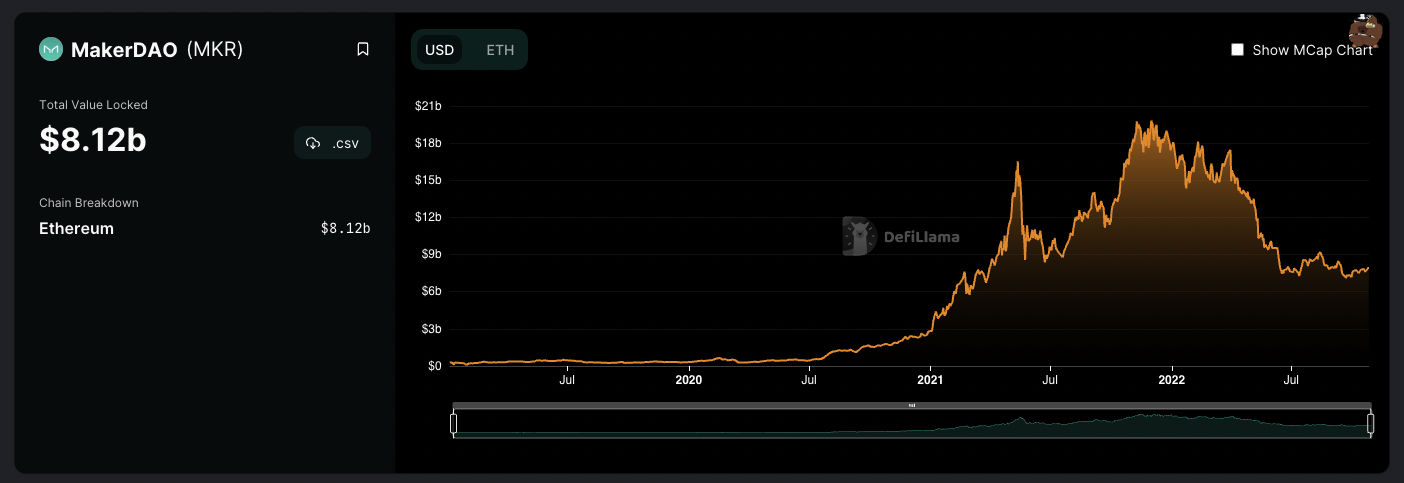

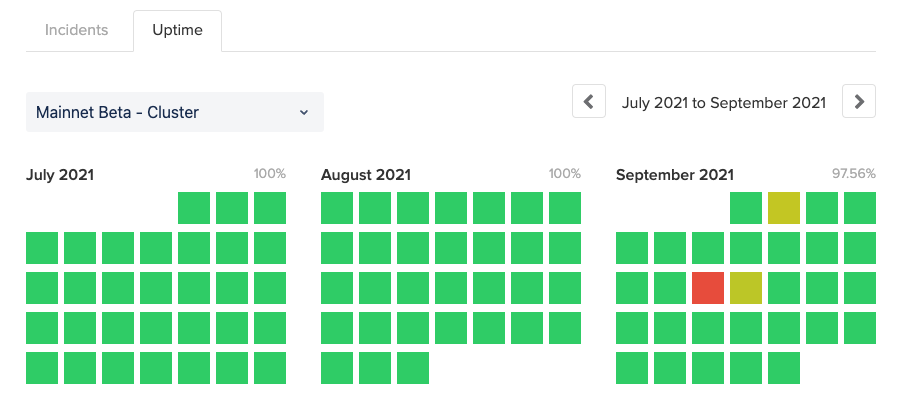

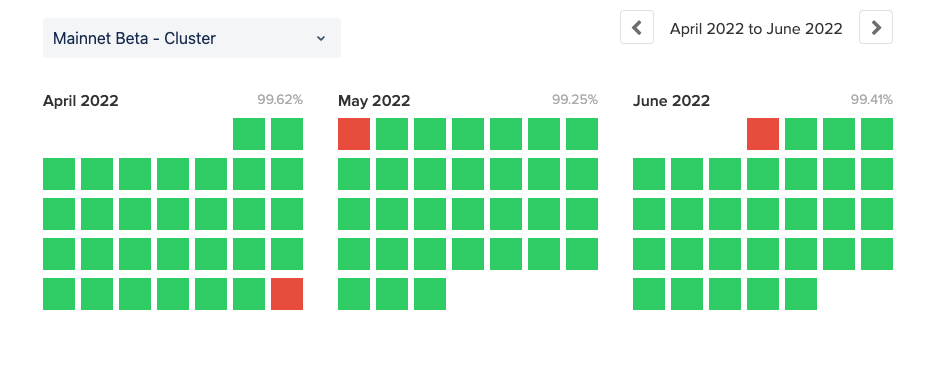

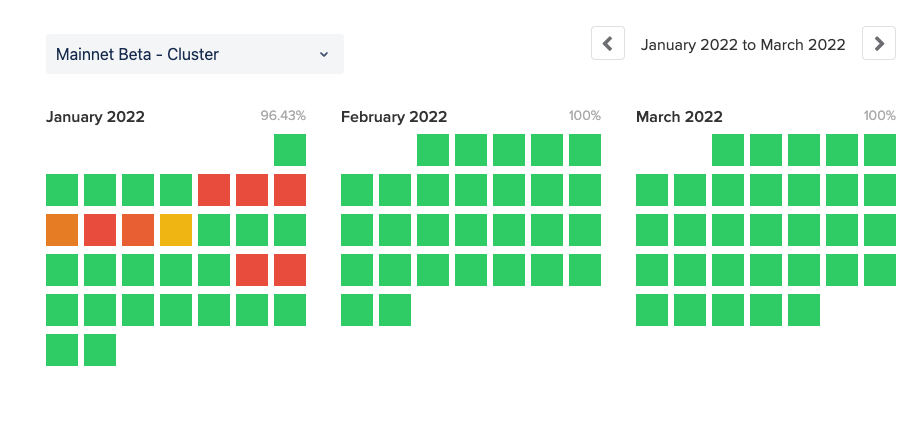

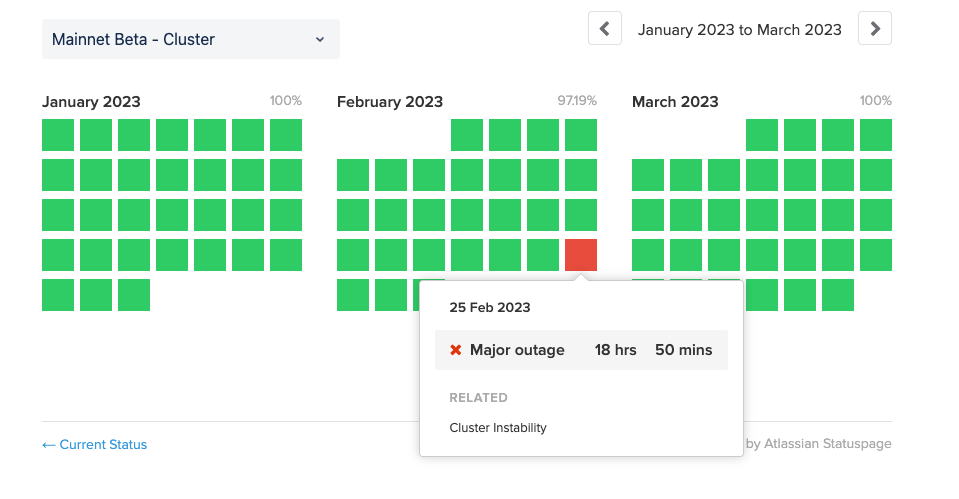

Source: daistats.com (Oct 27, 2021)

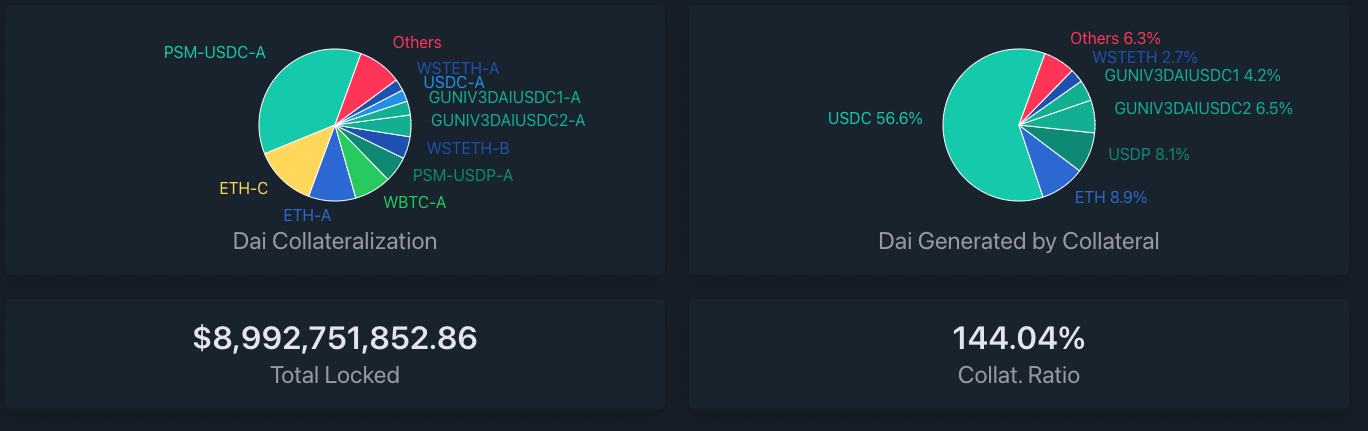

Source: daistats.com (Oct 26, 2022)

The Problem:

The Solution:

Note: In May 2021, ETH prices dropped again by >30% but no drama in DAI

Algorithmic Stablecoin: UST on Terra

(or: Apple's Option 3)

Case 2: price(1 SC) \(<\) 1 FU \(\to\) SC cheap

under-collateralized stablecoin

arbitrageur

issuer

market

Case 1: price(1 SC) \(>\) 1 FU \(\to\) SC cheap

arbitrageur

issuer

The Case of Luna-Terra

exchange LUNA for newly minted UST tokens at the prevailing $ market rate

market

LUNA market

Case 2: price(1 SC) \(<\) 1 FU \(\to\) SC cheap

arbitrageur

issuer

The Case of Luna-Terra

exchange SC for newly minted LUNA tokens at the prevailing $ market rate

market

LUNA market

Case 2: price(1 SC) \(<\) 1 FU \(\to\) SC cheap

DISCUSSION

POTENTIAL PROBLEMS

Case 2: price(1 SC) \(<\) 1 FU \(\to\) SC cheap

Case 2: price(1 SC) \(<\) 1 FU \(\to\) SC cheap

Case 2: price(1 SC) \(<\) 1 FU \(\to\) SC cheap

Case 2: price(1 SC) \(<\) 1 FU \(\to\) SC cheap

Case 2: price(1 SC) \(<\) 1 FU \(\to\) SC cheap

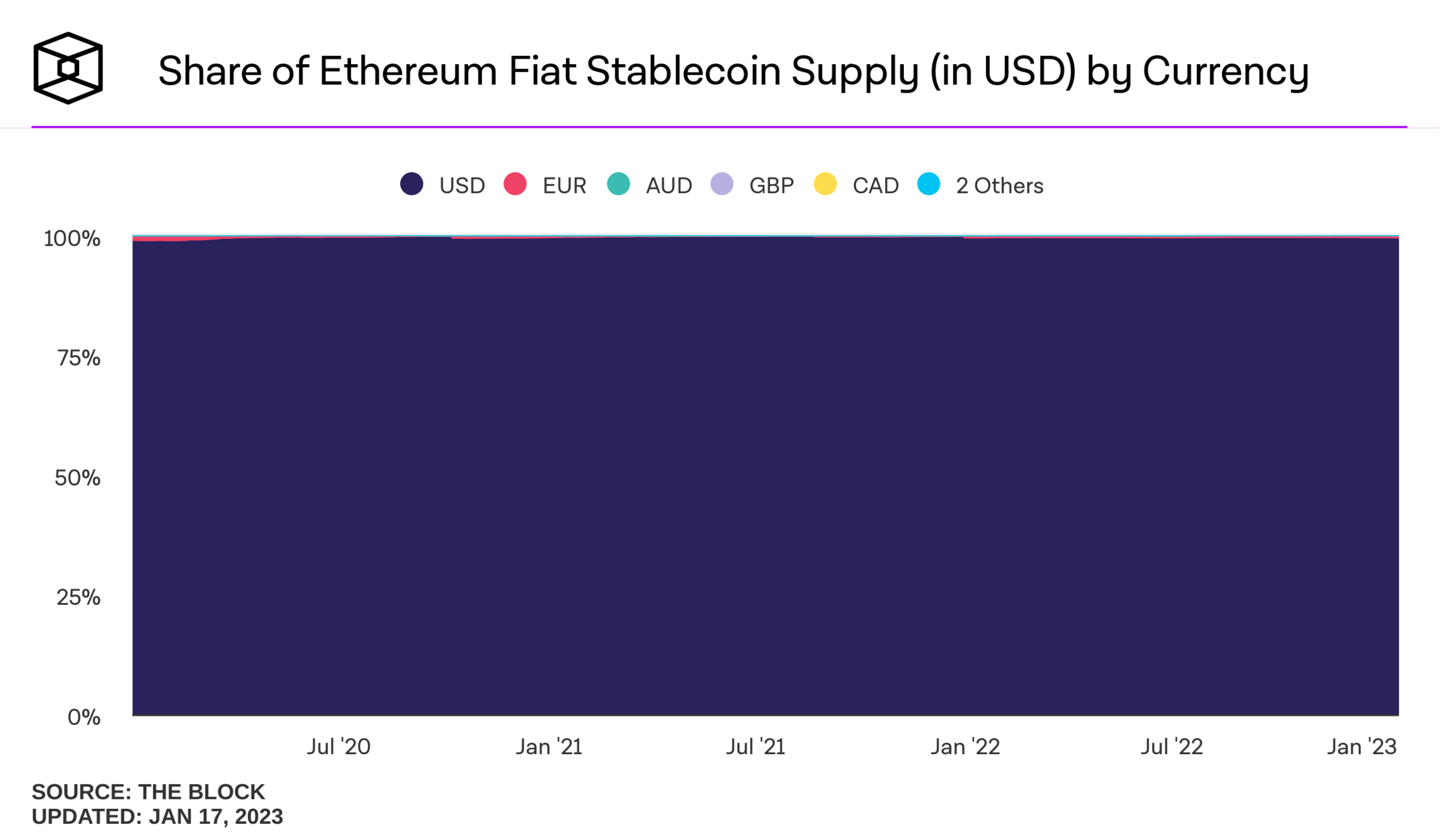

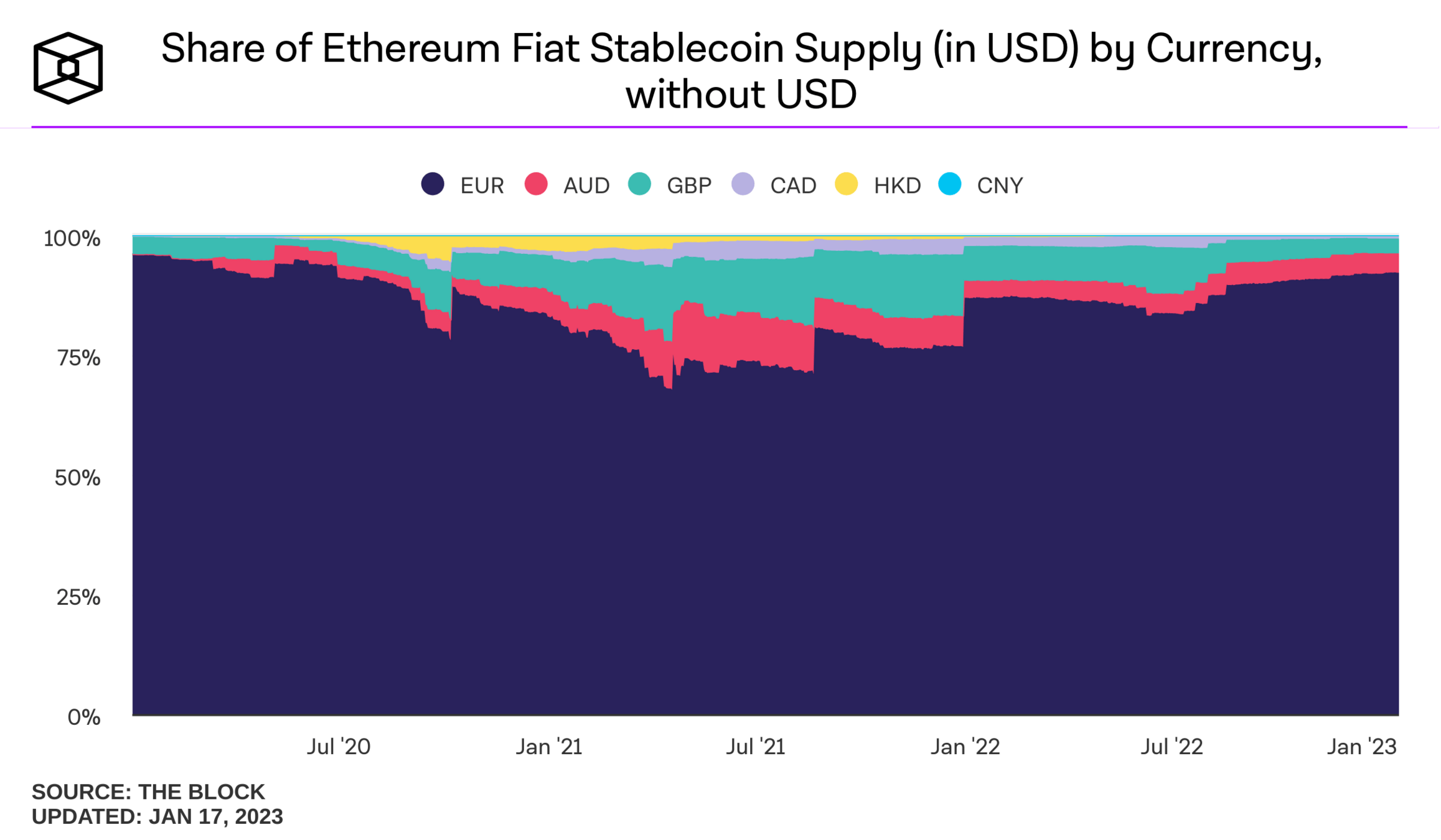

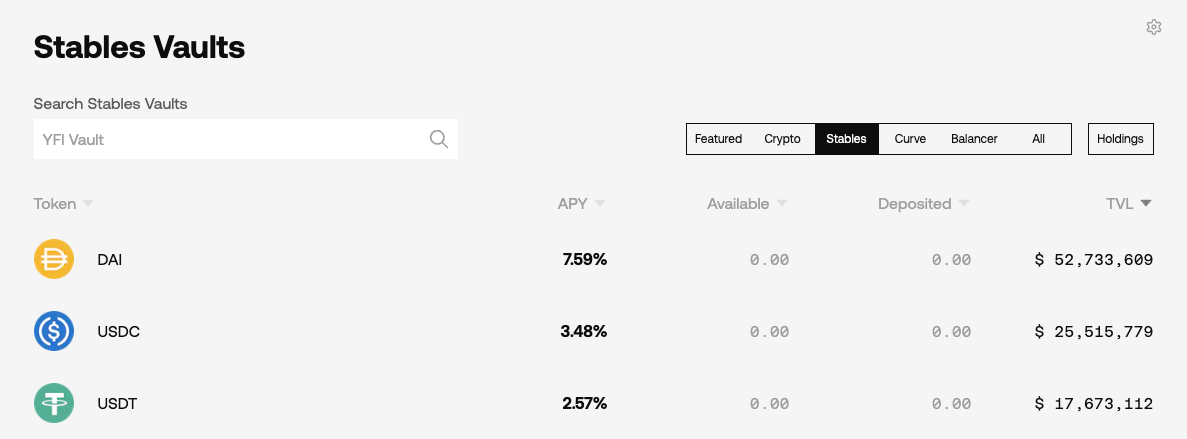

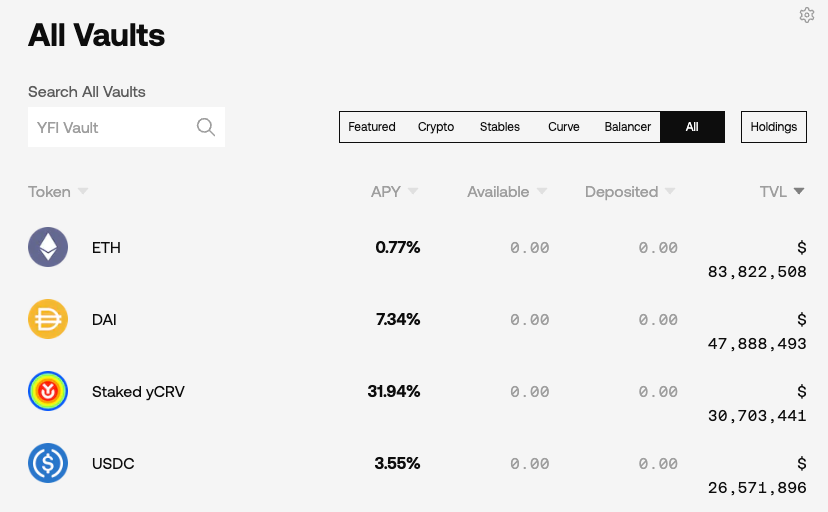

Stablecoin use cases

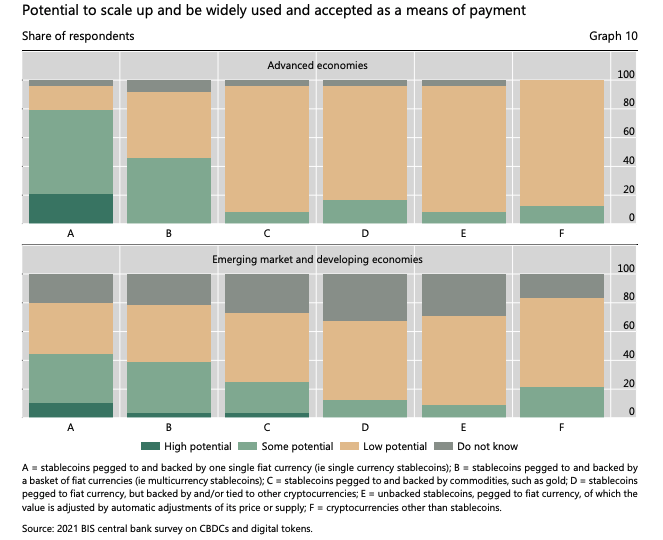

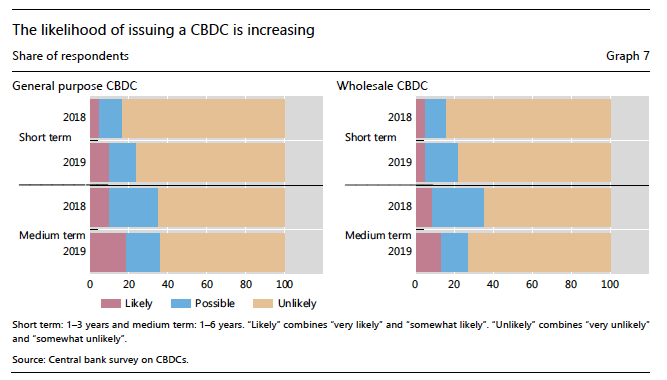

What do central bankers think about stablecoins?

BIS Survey of Central Banks:

What do central bankers think about stablecoins?

Stablecoin use cases

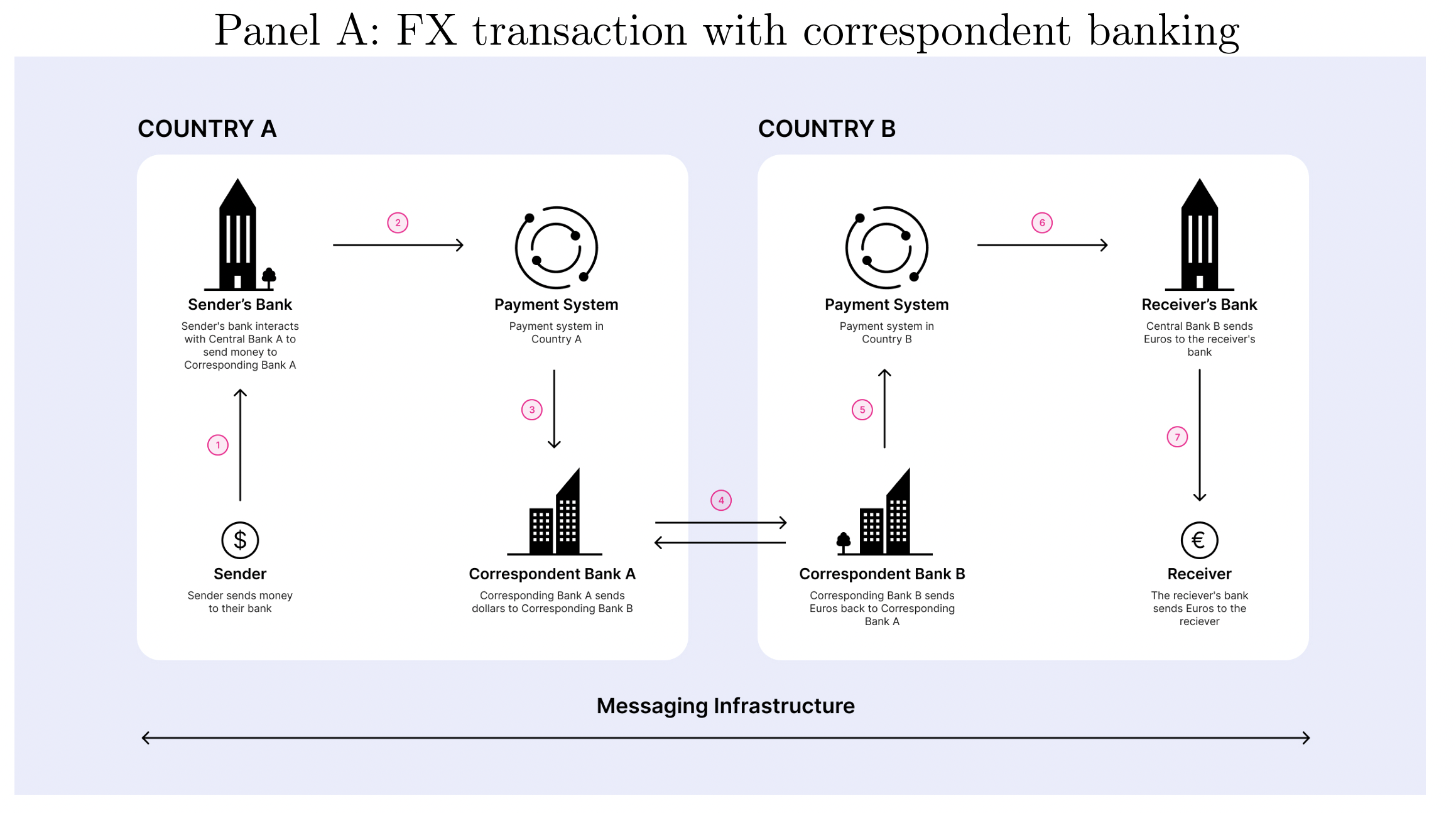

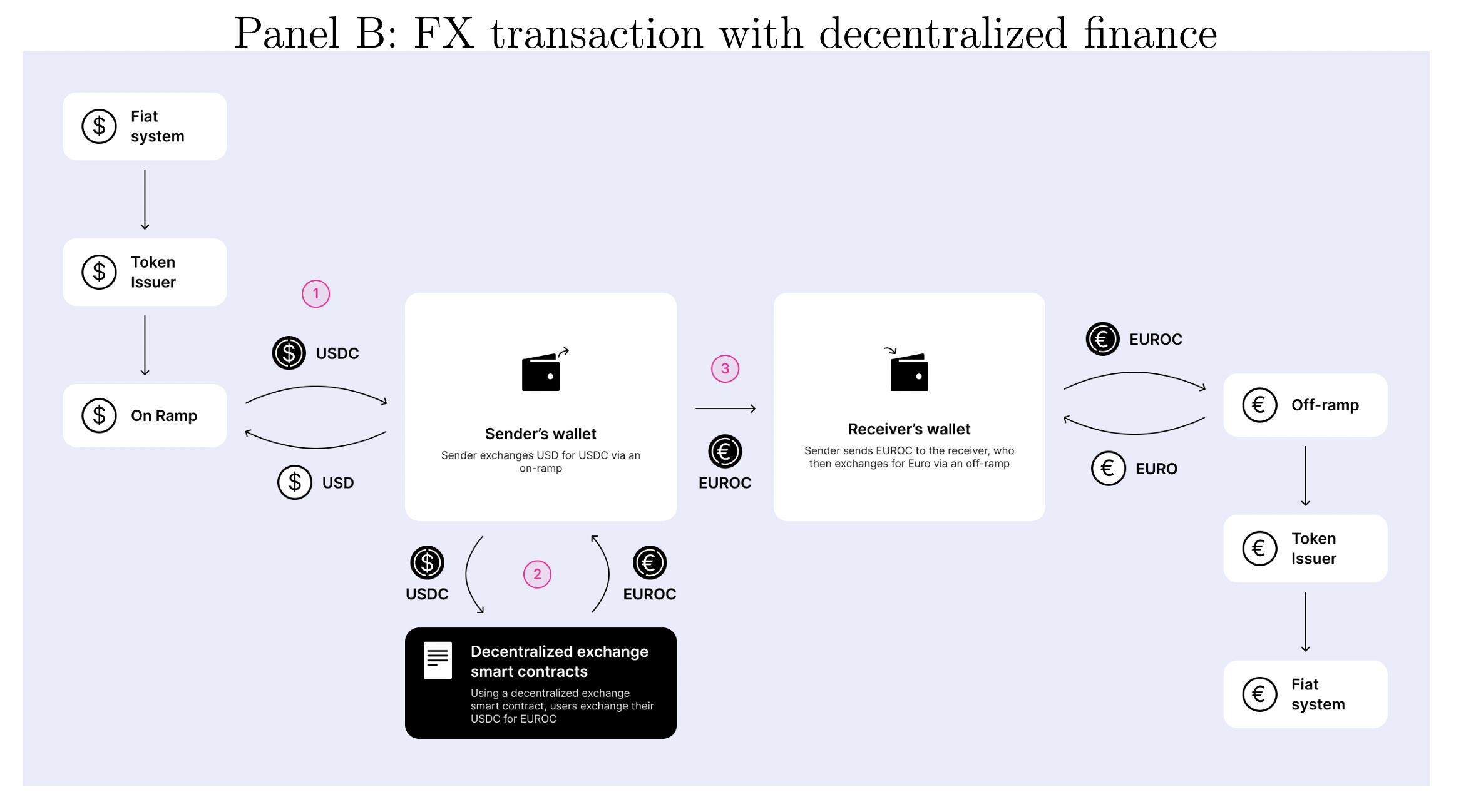

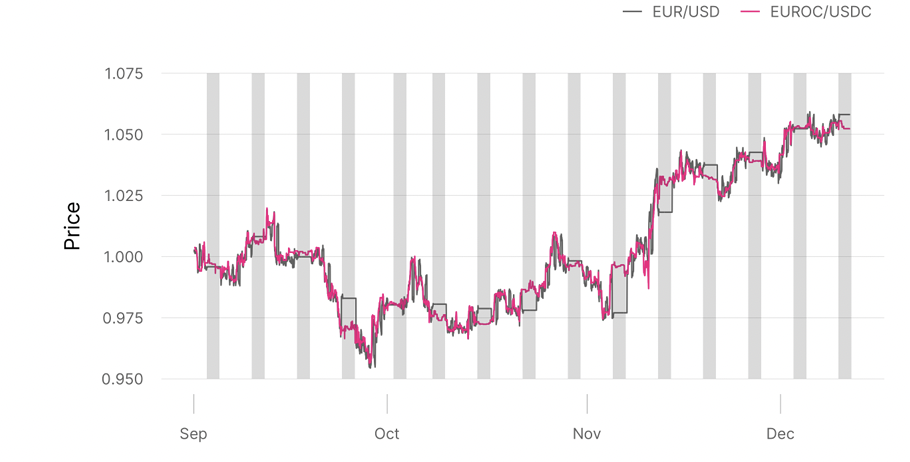

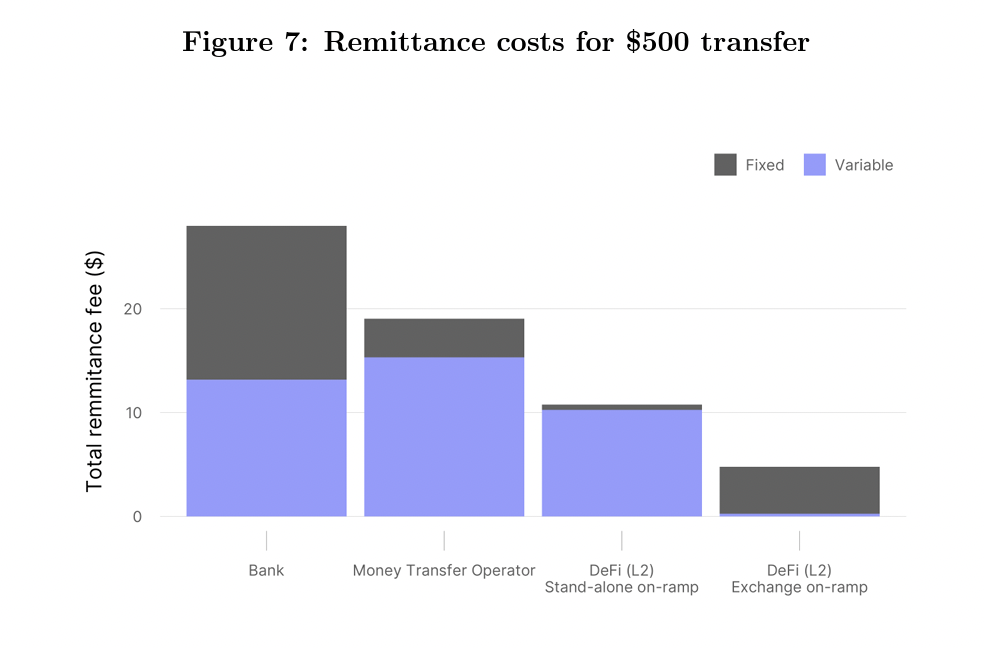

Source: On-chain Foreign Exchange and Cross-border Payments by Austin Adams, Mary-Catherine Lader, Gordon Liao, David Puth, Xin Wan (2023) [team from UniSwap Labs]

DeFi fees:

Risks to Financial Stability

Broad Blockchain Risks to Financial Stability

Lending capacity & Monetary transmission

Deposit mobility

AML/CFT/Sanction evasion

Dollarization

Failures/runs

New cyber-risks

Stablecoin Run Risks

Stablecoin Run Risks

Stablecoin Run Risks

Source: "Stablecoin Runs and the Centralization of Arbitrage," by Ma, Zeng, Zhang, 2023

Stablecoin Run Risks (2)

Source: "Stablecoin Runs and the Centralization of Arbitrage," by Ma, Zeng, Zhang, 2023

Result: lower concentration can have higher run risk

volatility (USDT)\(>>\)volatility (USDC)

stylized facts reg arbitrageurs

USDT \(\approx 4\%\)

USDC \(<1\%\)

"haircuts proxy for the discount incurred when illiquid assets are converted into cash at short notice"

Empirical calibration of run risk (dates/months signify important changes in reserve assets):

USDT in March 2022: 3.45%

USDC October 2021: 0.14%

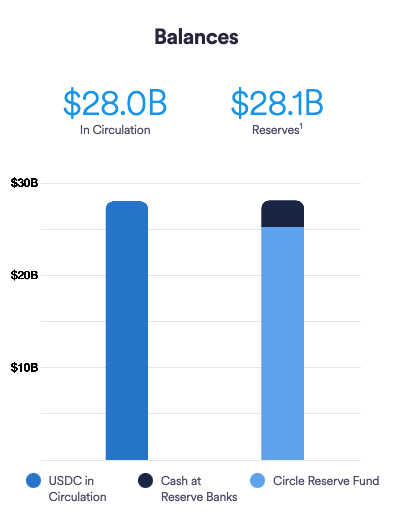

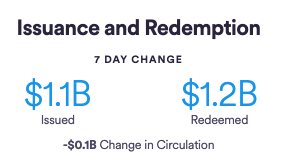

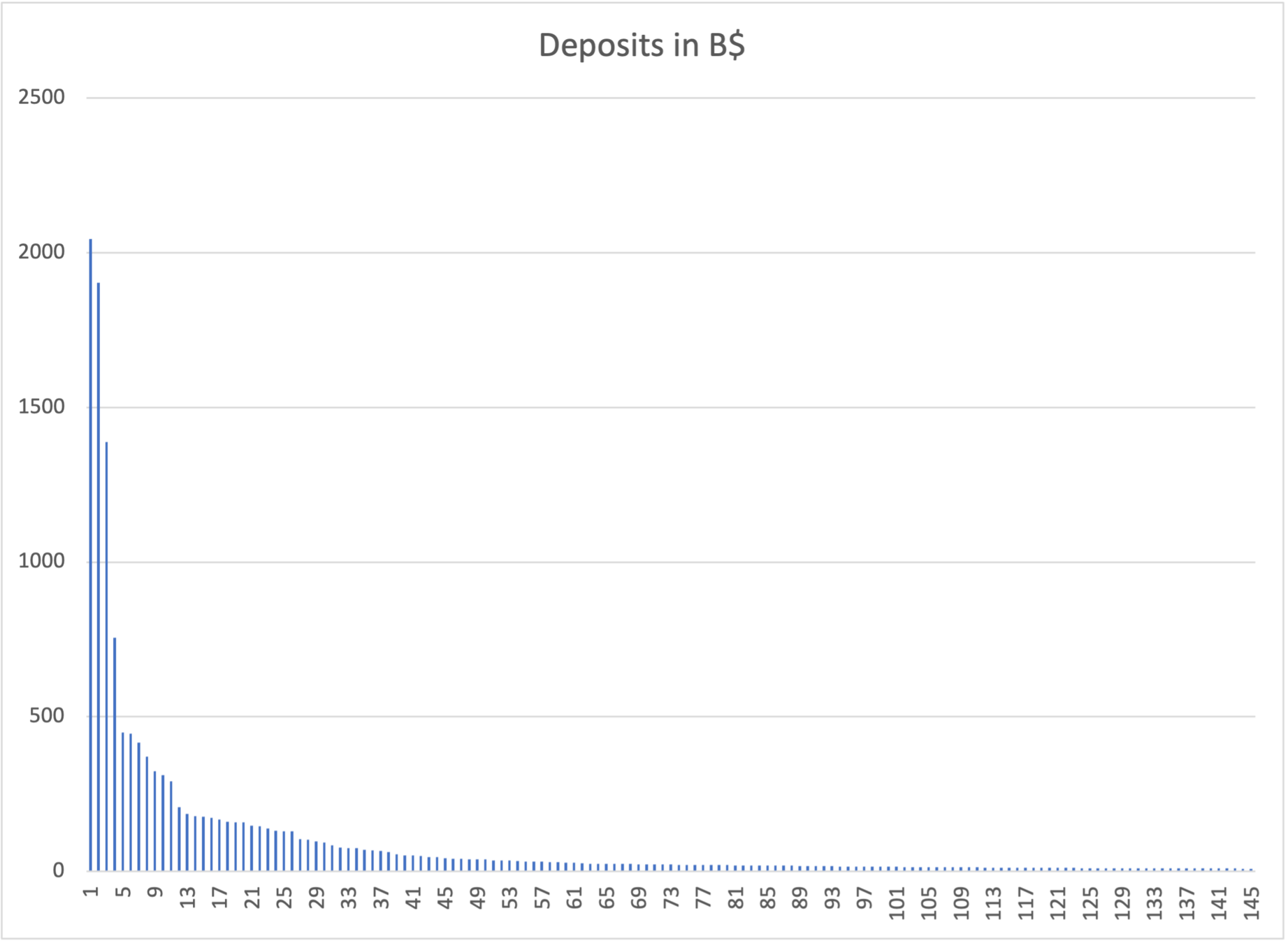

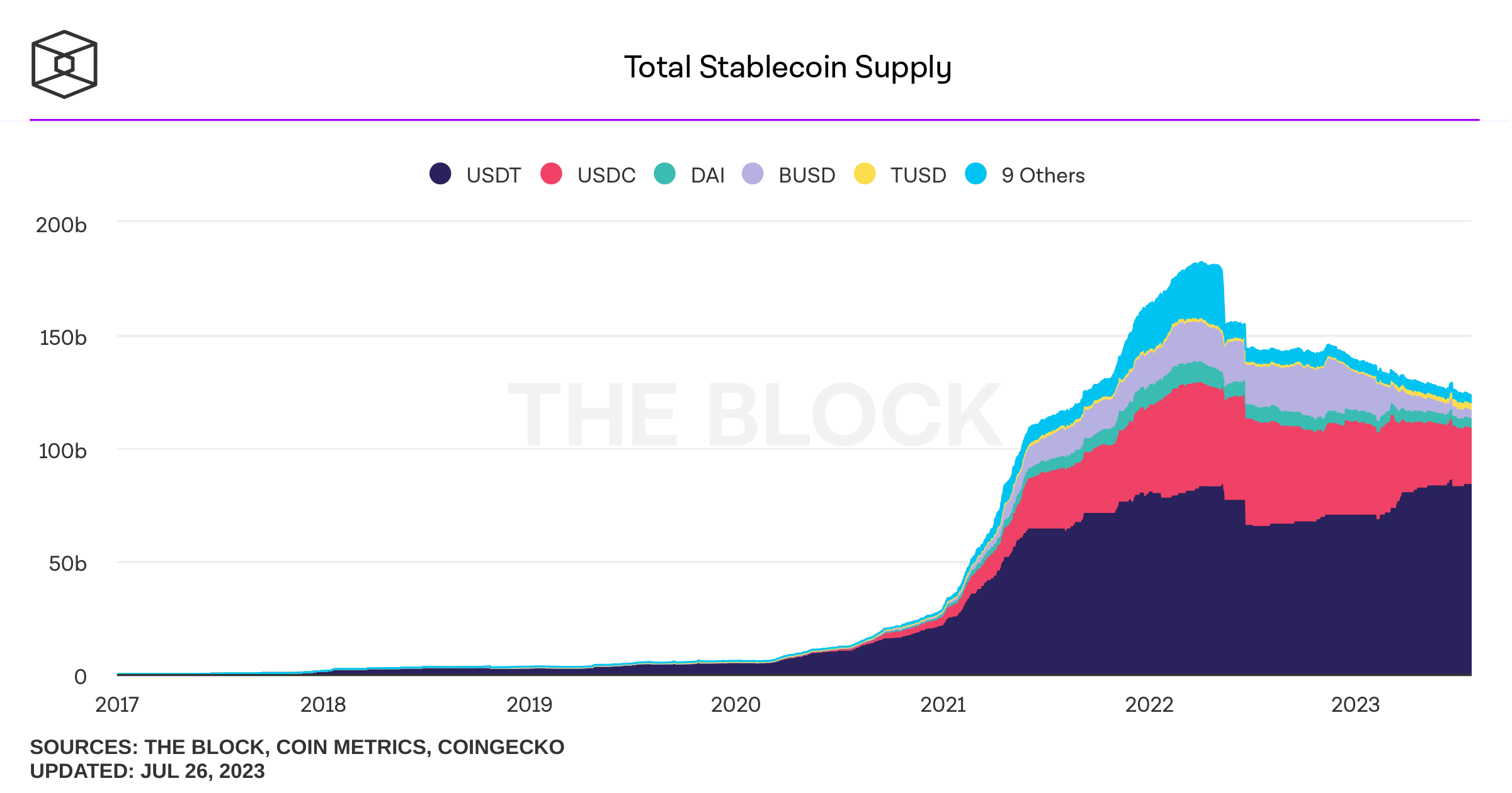

Stablecoins and Deposit Markets

Stablecoins and Deposits

Source: Jeremy Allaire testimony to the U.S. Congress , June 14, 2023 https://www.circle.com/executiveinsights/payment-stablecoins-support-the-dollar-and-u.s.-economic-competitiveness

Collapse of Anchor (as part of the TERRA-Luna debacle)

max TVL:

top 20

max lending:

top 50

current lending:

top 100

Crypto-assets incl. Stablecoins and Deposits

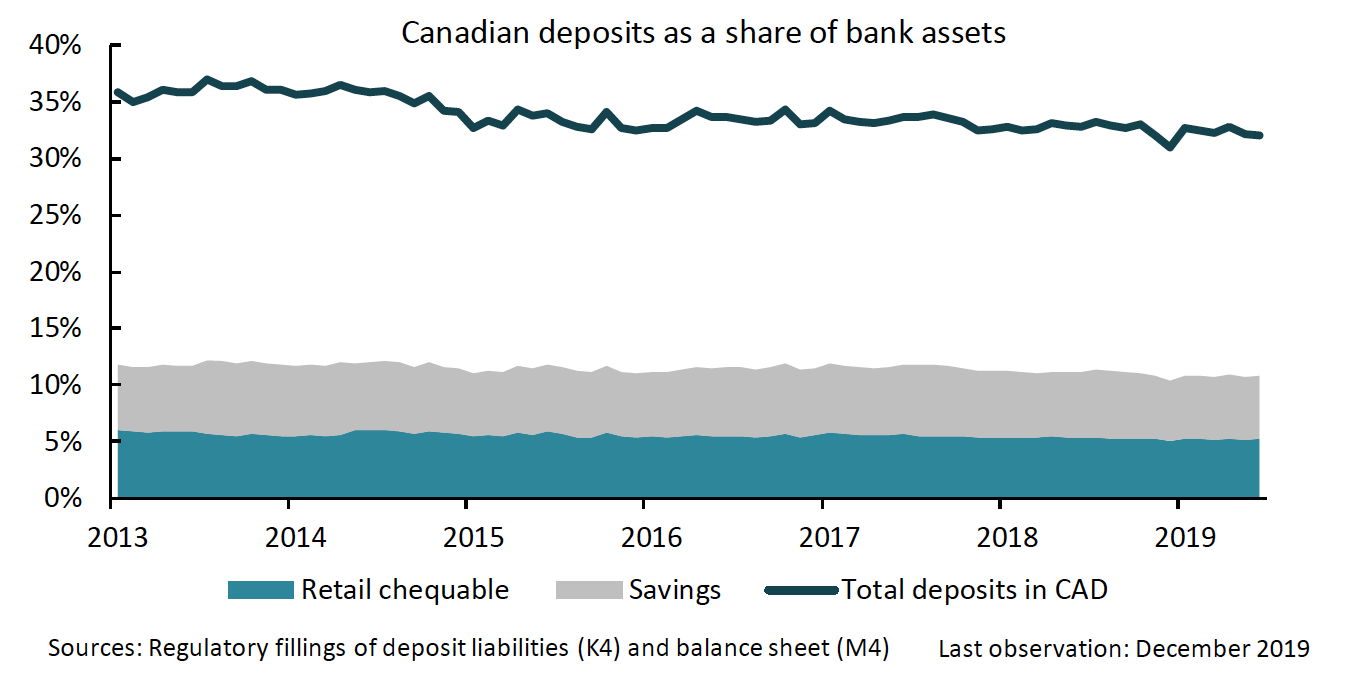

Canadian Banks' Financing with Retail Deposits

BoC analysis (August 2020):

Stablecoins and Deposits

Source of savings:

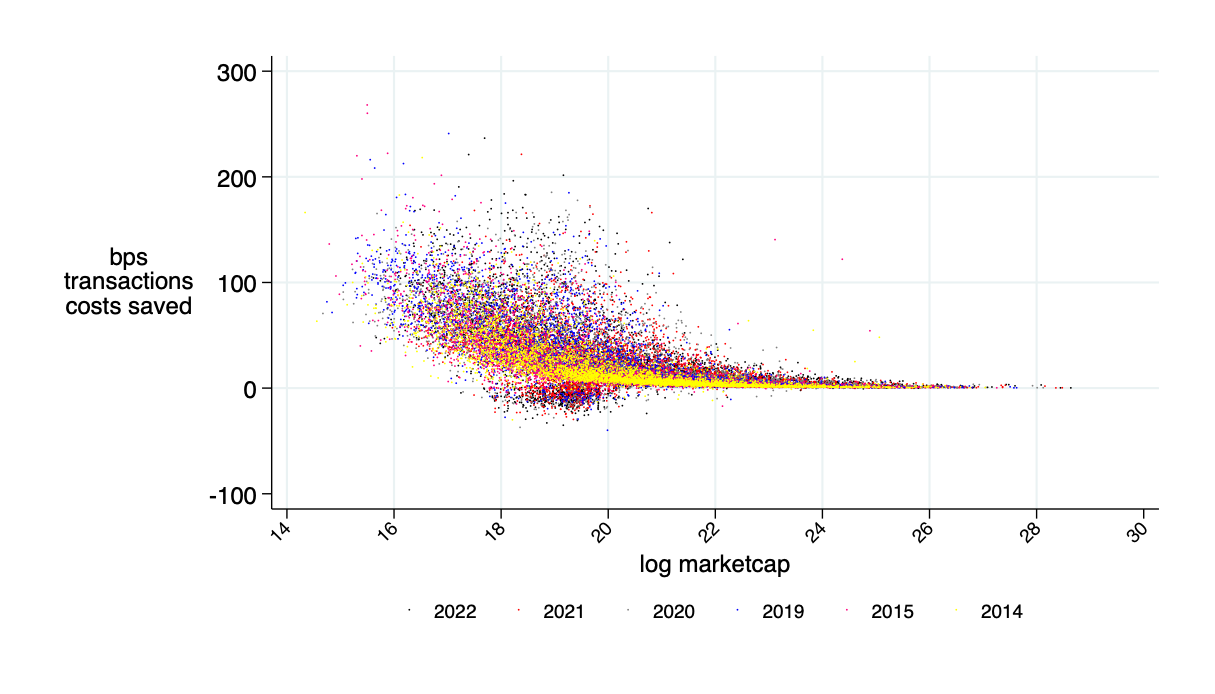

AMMs applied to equity trading could save \(\approx\) 30% of transaction costs

Source: "Learning from DeFi: Would Automated Market Makers Improve Equity Trading?" working paper, Malinova & Park 2023

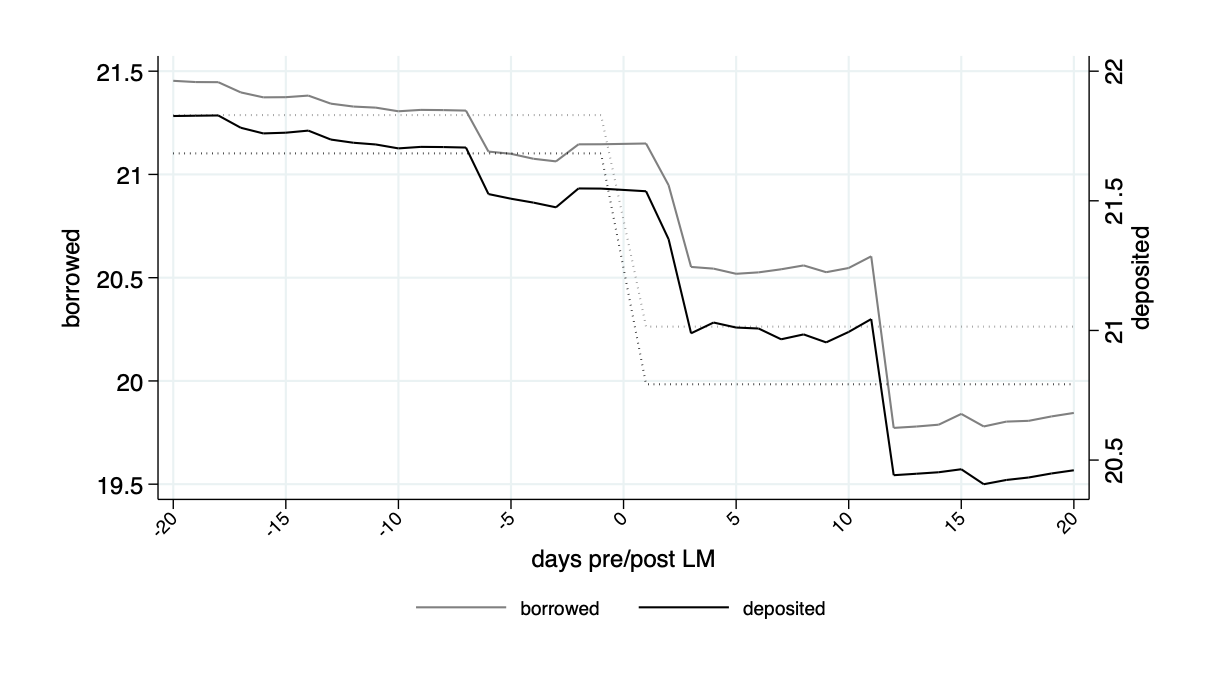

Automate Investment Strategies for Lending Pool Deposits

"yield aggregator:" push capital where rate of return is highest

Yield Aggregators create very mobile liquidity

Source: "Phantom Liquidity in DeFi Lending", Park and Stinner (2023) working paper

A Consequence of Liquidity Mining: Yield Aggregators

Idea:

Stablecoins and Deposits

huge demand for continuously available "high quality" money

Small Open Economy Risks

Currency Competition

Source: "The Coming Battle of Digital Currencies," Will Cong and Simon Mayer, 2022

Findings

Source: "Decrypting new age international capital flows", C. Graf von Luckner, Carmen M. Reinhart, Kenneth Rogoff, JME 2023

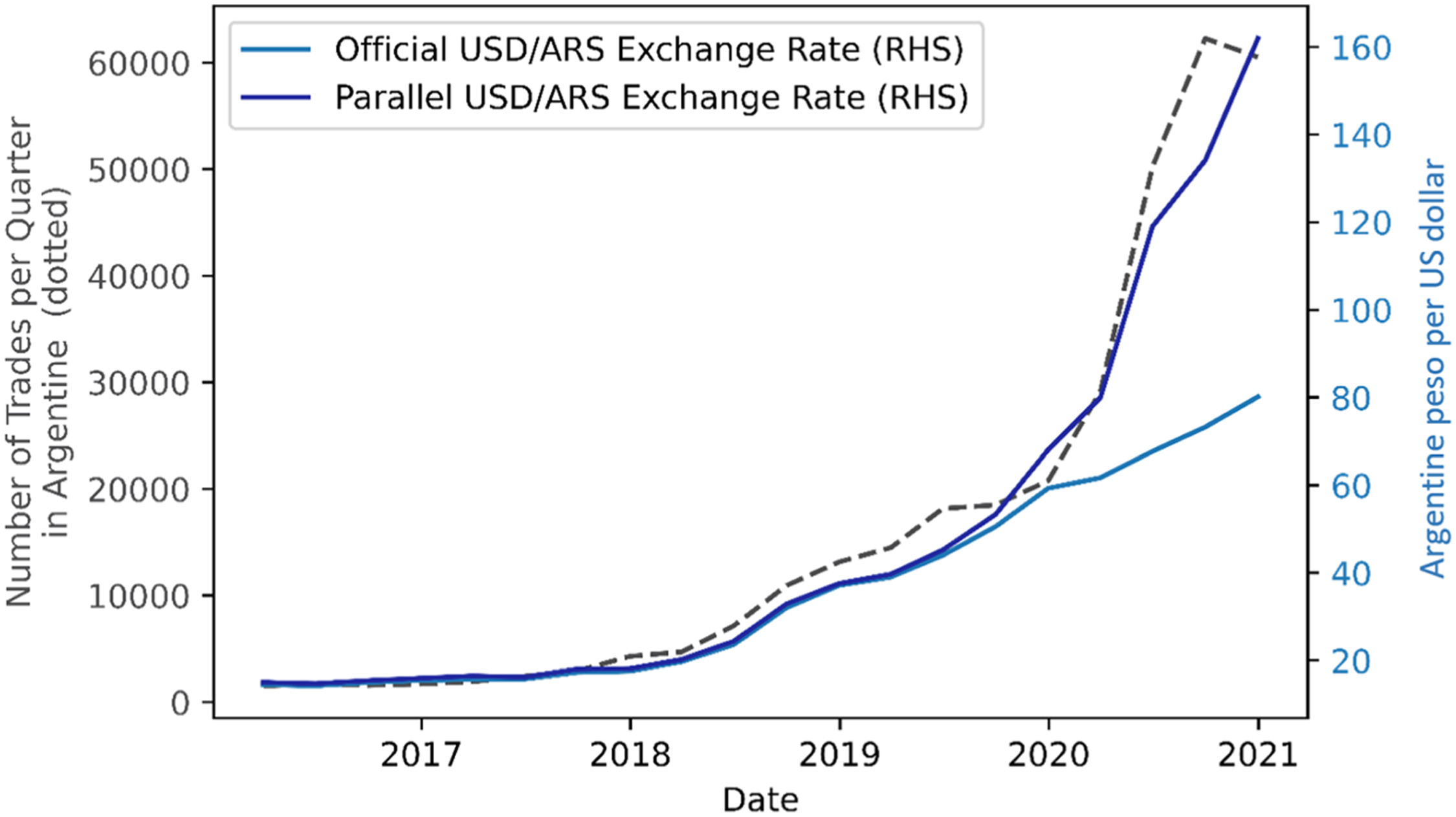

"there is already a growing market for using crypto as vehicle currency for transactions in developing economies and emerging markets, especially for international capital flight and evading exchange controls."

Idea:

Weak Fiat vs. Crypto: Some Empirical Evidence

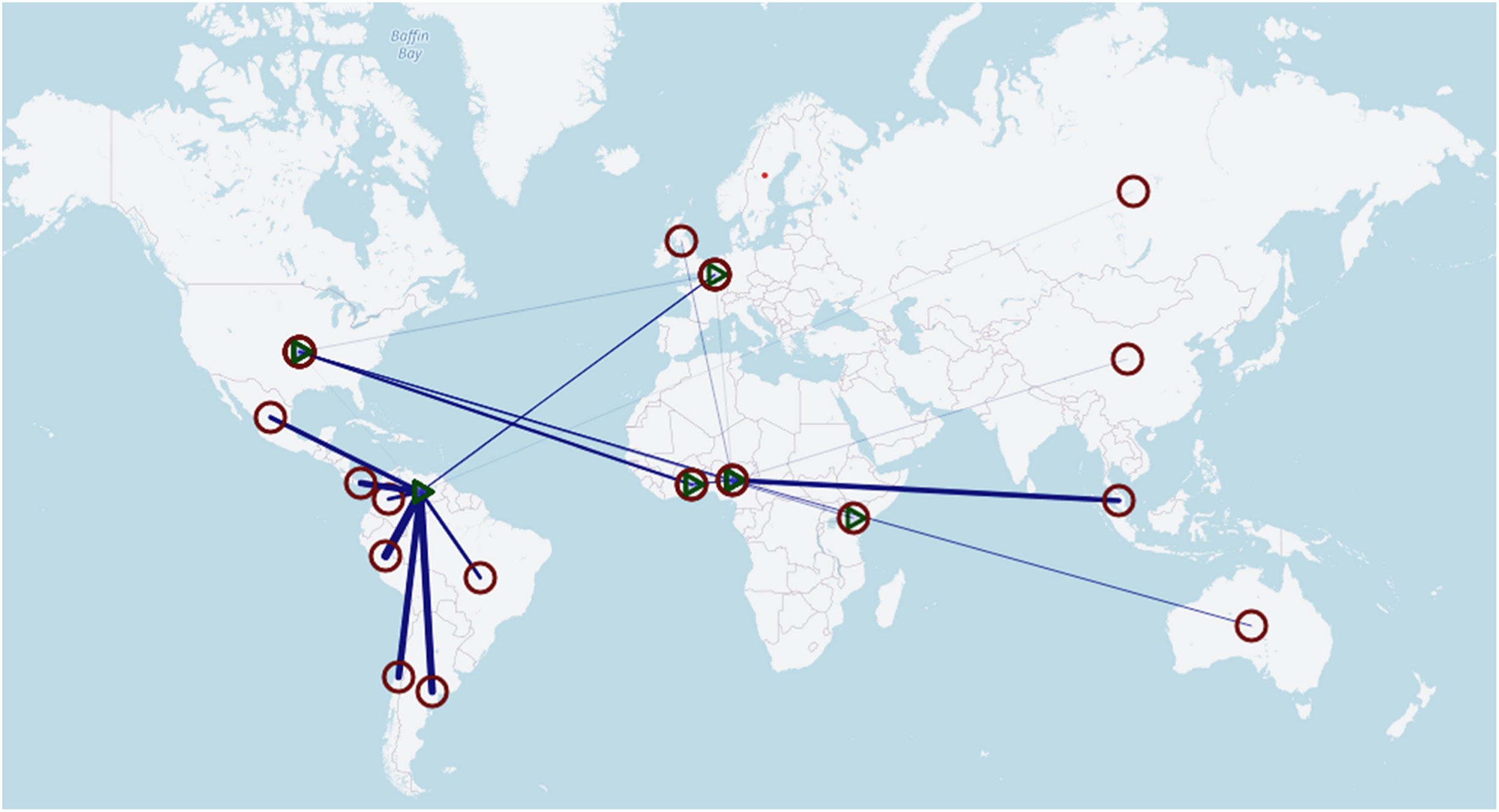

Fig. 5. Example of Bitcoin market expansion coinciding with capital controls in Argentina Source: LocalBitcoins.com API, BlueDollar.net, Authors’ Calculations.

Fig. 2. The World's 25 biggest Crypto Vehicle Channels. Circles: Origin, Triangles: Destination. Line-width: Channel volume as share identified trade volume in Origin Currency Sources: LocalBitcoins.com API, Paxful.com API, Authors’ Calculations.

Cracking the Code: How the US Government Tracks Bitcoin Transactions By YoonJae Chung Seoul International School (2019)

no fungible tokens allowed, but NFTs OK.

Cyberattacks and Hacks

Risk is in every layer of the tech stack!

Cyberattacks and DeFi-Thefts

run by Jump Trading a very sophisticated, tech-savvy HFT firm

\(\Rightarrow\) many threat vectors

Wallet Hacks

Hacker remotely stole validator private keys

Bridge attack

Hacker minted WETH out of thin air on Solana's contract

Signatures were not verified! Bridge attack....hmmm

Tech Overload: Solana

PS: Bitcoin has never been down, but Ethereum had some major slowdowns

Special Use Case: New Forms of Prudential Regulation without Regulators?

Fundamental Problem for centralized exchanges

New trend: data providers check assets

Assets: cash in bank accounts and crypto assets in exchange wallets

Liabilities: customers' crypto and cash deposits

Proof of crypto assets

publish all exchange wallets

proof of control: shift assets from one address to another at a pre-determined time

Proof of crypto liabilities

public customer balances - customer can check

own holding

sum of all

Problem: privacy (adequate solutions exist)

Proof of Assets & Liabilities

Might be a model for bank stability?

Money Laundering and Crime

Basic FINTRAC Rules for Money Services Businesses

\(\Rightarrow\) the rules are "tight"

Big Picture Concern

criminals don't use USDC - why are we so worried?

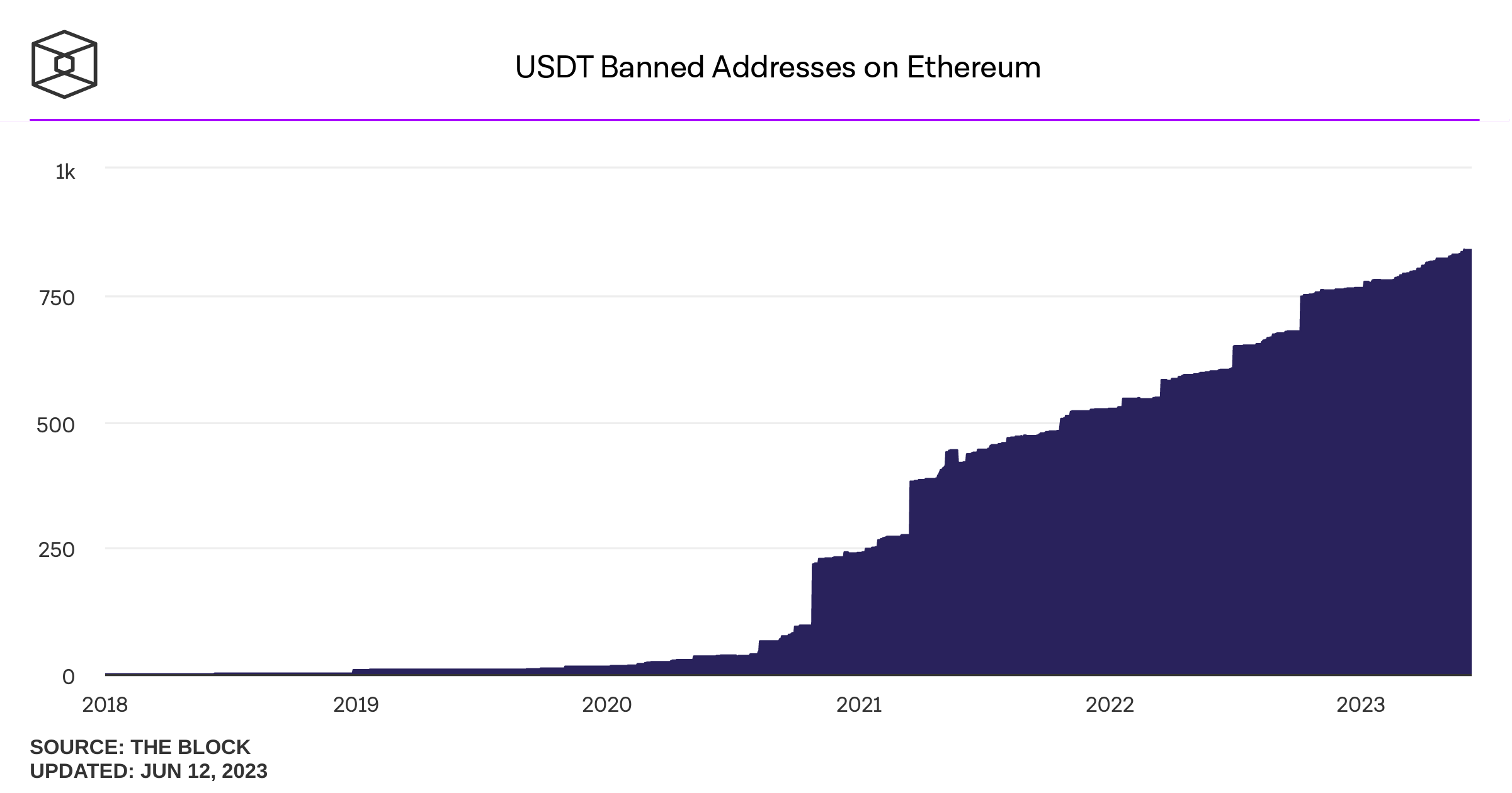

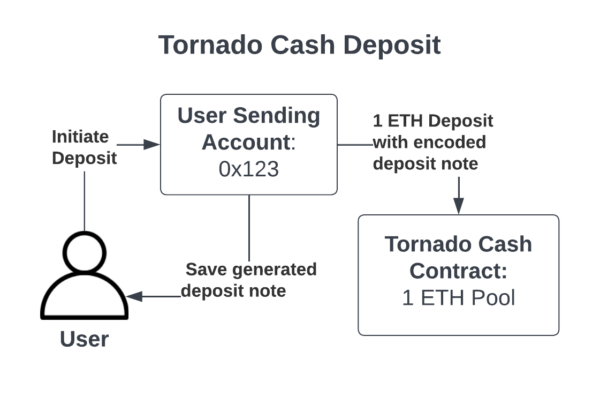

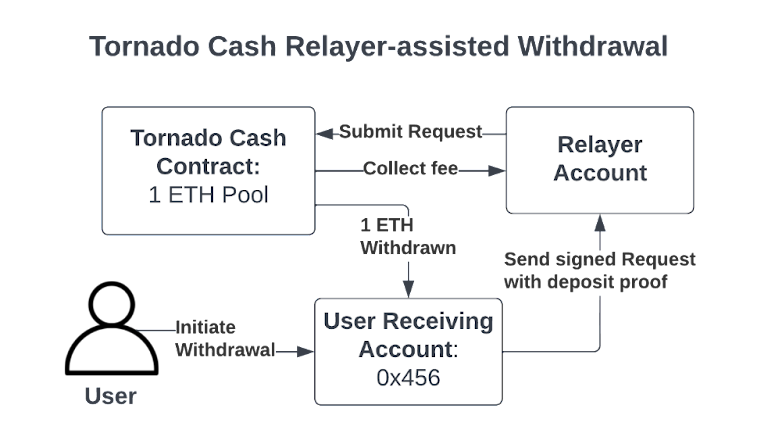

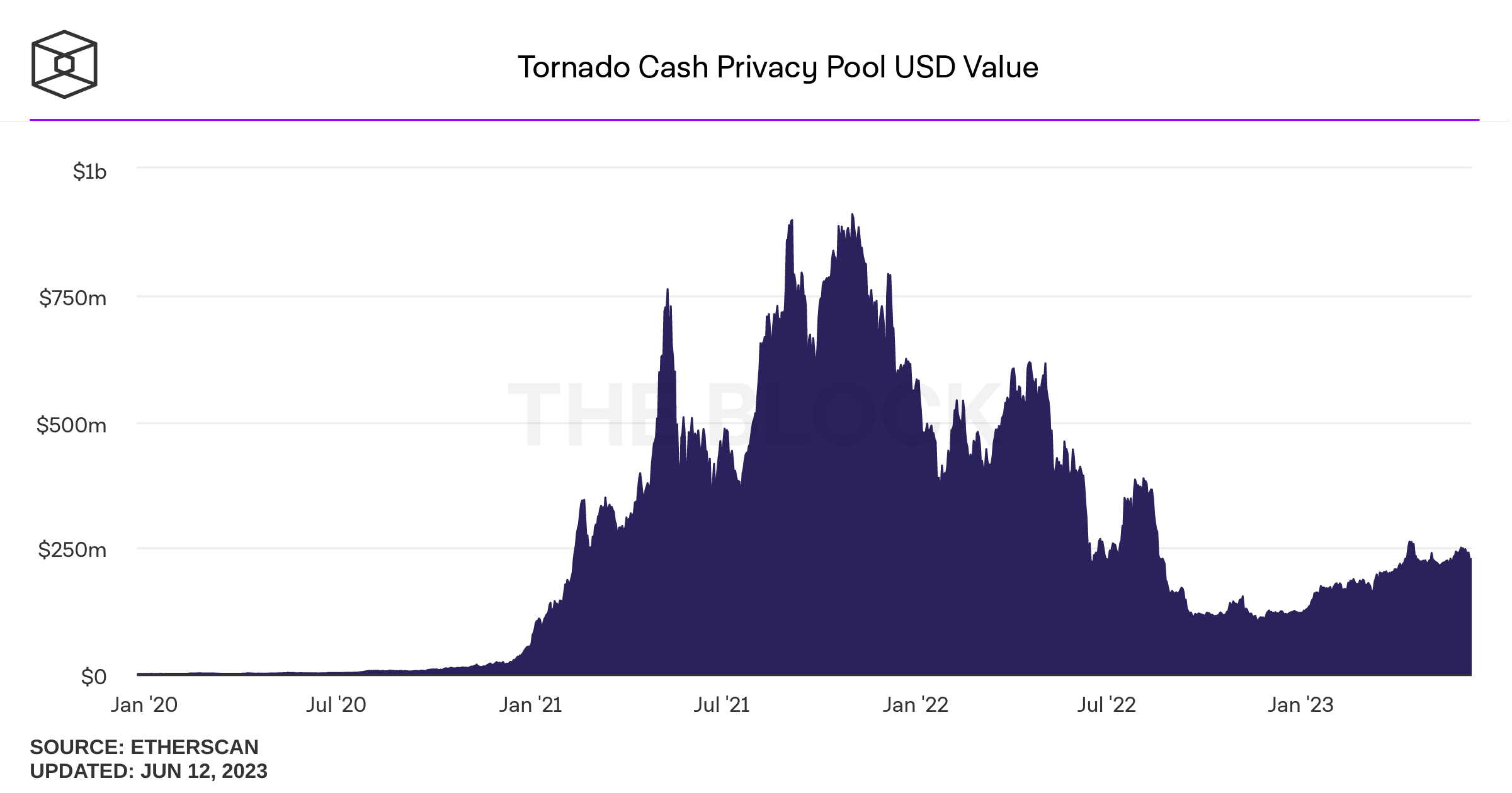

August 8, 2022: OFAC sanctions Tornado Cash

extra info:

Summary on Concerns regarding Stablecoins

back to Nick Carter's talk on "Will stablecoins serve or subvert U.S. interests?"

Asset Tokenization

Key Institutional Features of Equities

Institutional Differences: Crypto Asset Ownership, Accounts, Wallets, and Self Custody

Smart contract accounts

Externally owned accounts

controlled by private keys

private

key

public

key

(seed phrase)

public

address

wallet = software to keep and use private keys

Blockchain Ownership Attribution

Institutional Differences: The Investment Process

issuers

investors

services

needed & provided

A general purpose value management infrastructure:

intermediaries

separate institutions

The blockchain reality:

new institutions

will emerge

Asset Tokenization or

"The Creation of Asset-Linked Tokens"

Tokenization of stocks is nothing new: American Depository Receipts

foreign investor/

issuer

domestic bank with foreign representation

ADR issuing bank handles

Is this a workable model for blockchain- tokenization of existing assets?

foreign representation of domestic bank/ its custodian

domestic depository bank

S.E.C.

registration with form F-4

domestic broker

issues and cancels ADRs

domestic investor

lets investors own and trade ADRs

domestic

market

deposits shares

Blockchain Tokenization has many options

existing investor/

issuer

token issuance platform

investor

wallet

instruct to create tokens

deposits shares

custodian bank

deposits shares

creates tokens and sells to investors

centralized or decentralized

market

S.E.C.

registration

Token Standards

Some basic facts

Fact 1: Ownership of tokenized asset can be

Fact 2: By default issuers do not know who owns their tokens

Fact 3: Investors who hold tokens in DeFi smart contracts have fluctuating holdings.

Fact 4: General ownership restrictions are almost impossible to enforce, and transfer restriction would negate advantages of tokenization

Problems that require solving

ADR issuing bank handles

How are these functions performed with crypto-assets?

Fact 2: By default issuers do not know who owns their tokens

Some remedies for communication and dividends

All this needs a legal framework that adapts to a decentralized, digital world

Problems that require solving

ADR issuing bank handles

Remaining FIs handle

Fact 4: General ownership restrictions are almost impossible to enforce, and transfer restriction would negate advantages of tokenization

Legal and regulatory frameworks currently rely on intermediaries and are not prepared for self-custody

Broader Implications for the Financial Industry and the Financial System

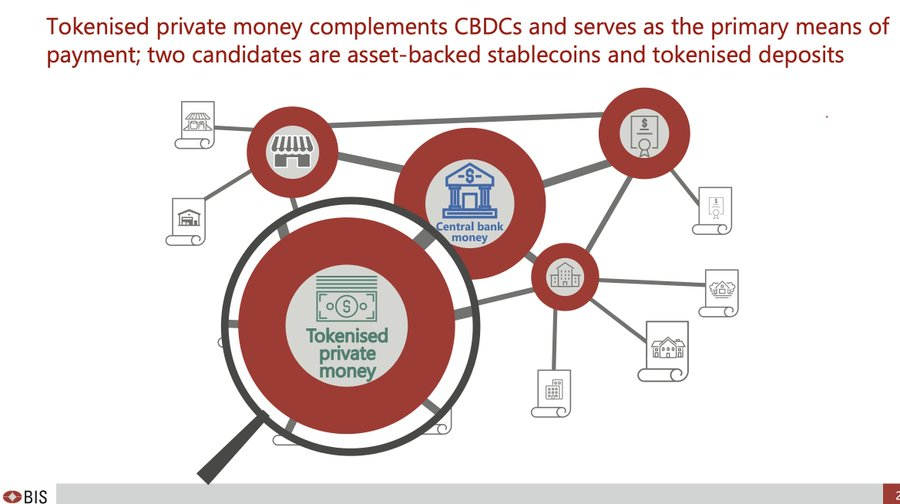

Asset tokenization would likely create a massive expansion in demand for stablecoins

Business risk for existing FI: super-easy entry

idea: create new mutual fund like asset

Business Risk to FIs: Customers choose what's best for them

"yield aggregator:" push capital where rate of return is highest

Yield Aggregators are very mobile liquidity

Source: "Phantom Liquidity in DeFi Lending", Park and Stinner (2023) working paper

Effects on the IO of Financial Services

Last Words

Summary

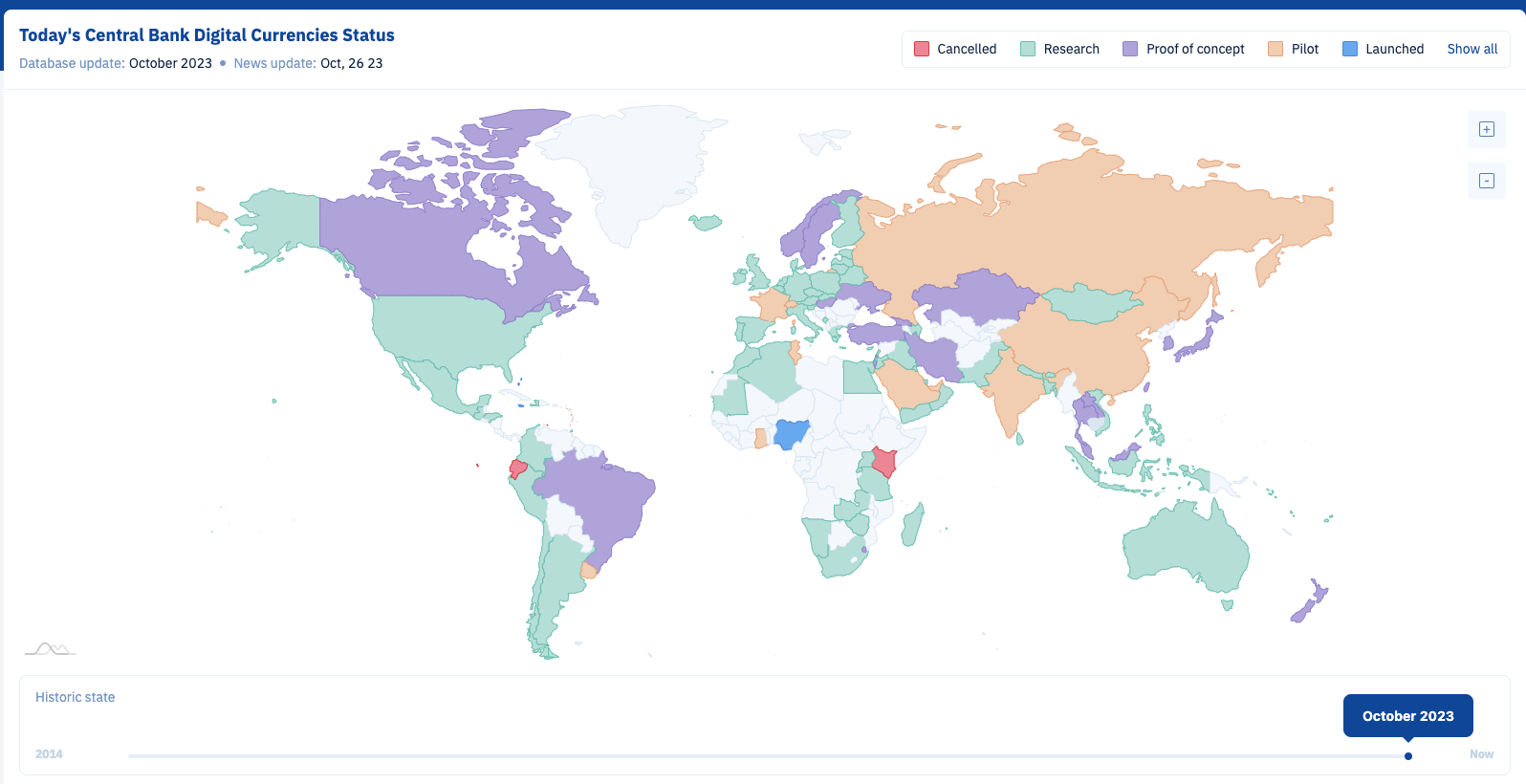

Central Bank-Issued Digital Currencies

Evolution

2008

2014/5

2019

2020

Source: CBDCtracker.org

Source: BIS Quarterly Review, March 2020

The Year is 2008: what the Toronto a la cart program teaches us about CBDCs

Cautionary tales for central bank innovation

what people want

what we got

Features of Digital Money

fast money

CBDC run by

Central Bank

CBDC on new communually run system

bank-issued stablecoin on public blockchain

|

What? |

||||

|---|---|---|---|---|

| 24/7 instantaneous | ||||

| borderless | ||||

| programmable | ||||

| privacy | ||||

| p2p | ||||

| no commercial 3rd party | ||||

| nominal fee |

Evolution

The State strikes back: CBDCs

China: kinda-sorta running; provinces prep own initiatives

U.S.: has bigger problems and is always a last mover

UK: preparing

Canada: contingency planning (it'll happen within two years)

EMU: It's coming (Christine Legarde)

Would a CBDC improve the efficiency of its currency function?

Would CBDC improve the efficiency and safety of both retail and large-value payment systems?

Is CBDC an appropriate policy response to payment innovations such as privately issued e-money and digital currency to achieve its monetary policy goals and to implement policies promoting financial stability?

"Central Bank Digital Currencies: A Framework for Assessing Why and How " Fung and Hallaburda 2016, BoC Working Paper

Contingency Planning for a Central Bank Digital Currency (BoC website)

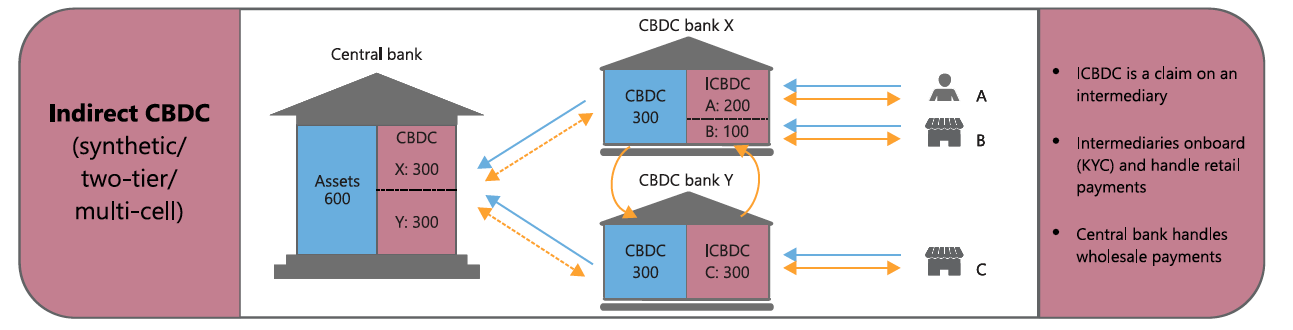

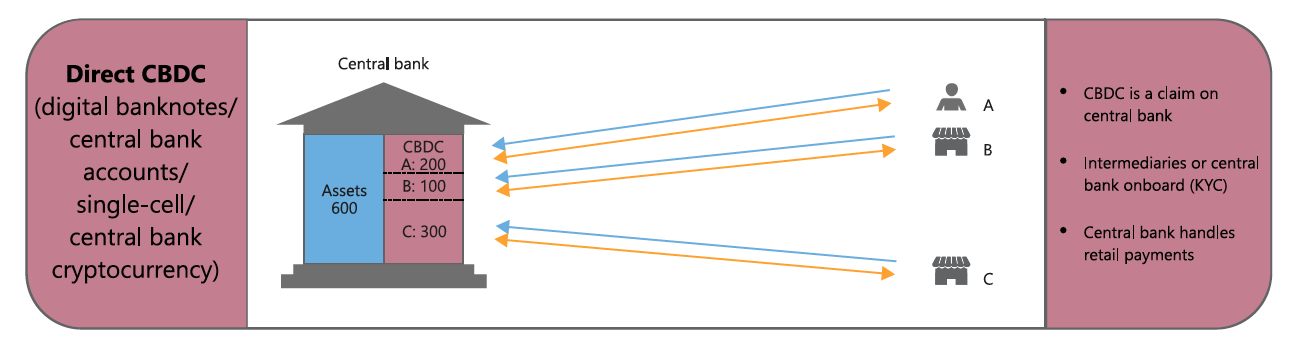

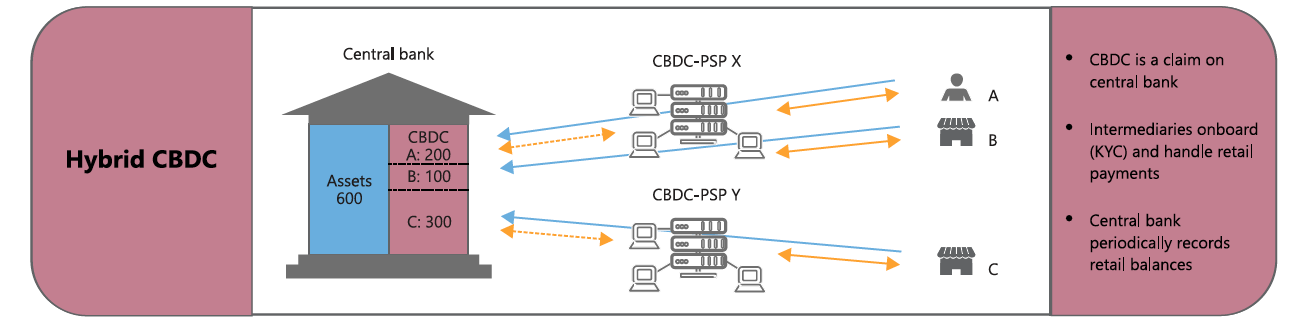

CBDC: Token vs Accounts

identification of the object being transferred as a means of payment

identification of the individual whose account is being debited

example: cash

example: ETH

Should the central bank issue e-money? Kahn, Rivadeneyra, Wong, Bank of Canada working paper 2019

BoC analysis (August 2020):

Are CBDCs desirable?

Discussion Points

Discussion Points: how will you introduce and run it? Concerns

go alone

and do self

partner with banks \(=\)

use them for distribution and operation

The Year is 2008: what the Toronto a la cart program teaches us about CBDCs

Cautionary tales for central bank innovation

what people want

what we got

Chrystia Freeland Justin Trudeau

of all things crypto and digital in Canada

from the Budget 2022

UK Government: "wider plans to make Britain a global hub for cryptoasset technology and investment."

highest incentive to launch CBDC to gain tech advantage

nip crypto stablecoin in the bud

adopt crypto (likely stablecoin relating to dominant country)

Cong & Meyer 2022: The Coming Battle of Digital Currencies

fast money

real time rails run by chartered banks

CBDC

run by

chartered banks

run by

Bank of Canada

new communually run system

Stablecoin

private firm (e.g. Facebook)

CBDC on public blockchain

chartered bank-issued on public blockchain

fast money

CBDC run by

Bank of Canada

CBDC on new communually run system

bank-issued stablecoin on public blockchain

|

What? |

||||

|---|---|---|---|---|

| 24/7 instantaneous | ||||

| borderless | ||||

| programmable | ||||

| privacy | ||||

| p2p | ||||

| no commercial 3rd party | ||||

| nominal fee |

Components

Features

very bad policies

governments with good intentions

the stuff of distopian nightmares: tools that bad governments can use to turn on its citizens

Where do CBDCs fall in and under what conditions?

And then there's the economics

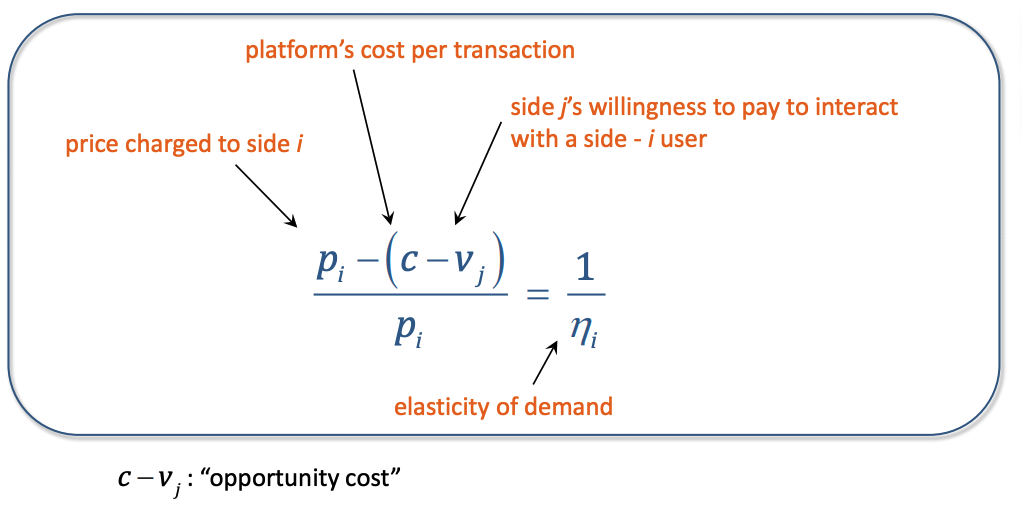

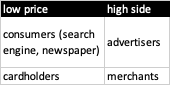

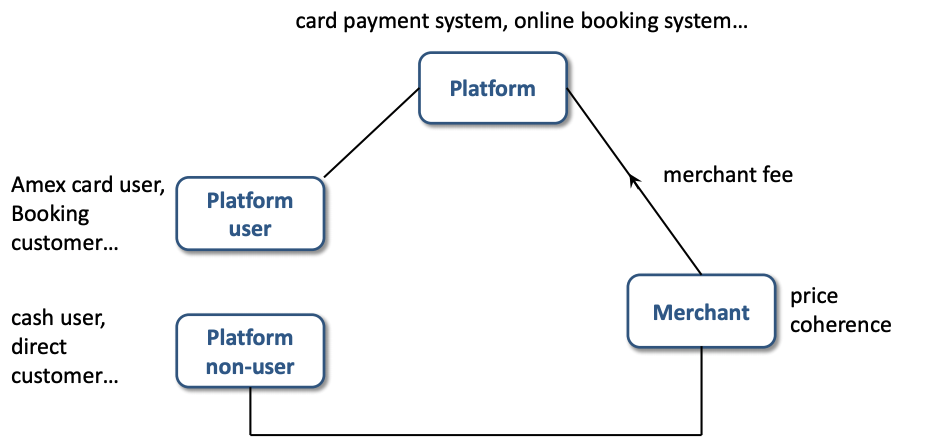

Source: "Regulating Competing Payment Networks", Lulu Wang, Northwestern Kellogg

Quick background:

normal payments infrastructure

And then there's the economics

Source: "Regulating Competing Payment Networks", LuluWang, Northwestern Kellogg

simplified version

here: one-sided market

but the market is two-sided!

Source: "Regulating Competing Payment Networks", LuluWang, Northwestern Kellogg

but the market is two-sided!

Source: "Regulating Competing Payment Networks", LuluWang, Northwestern Kellogg

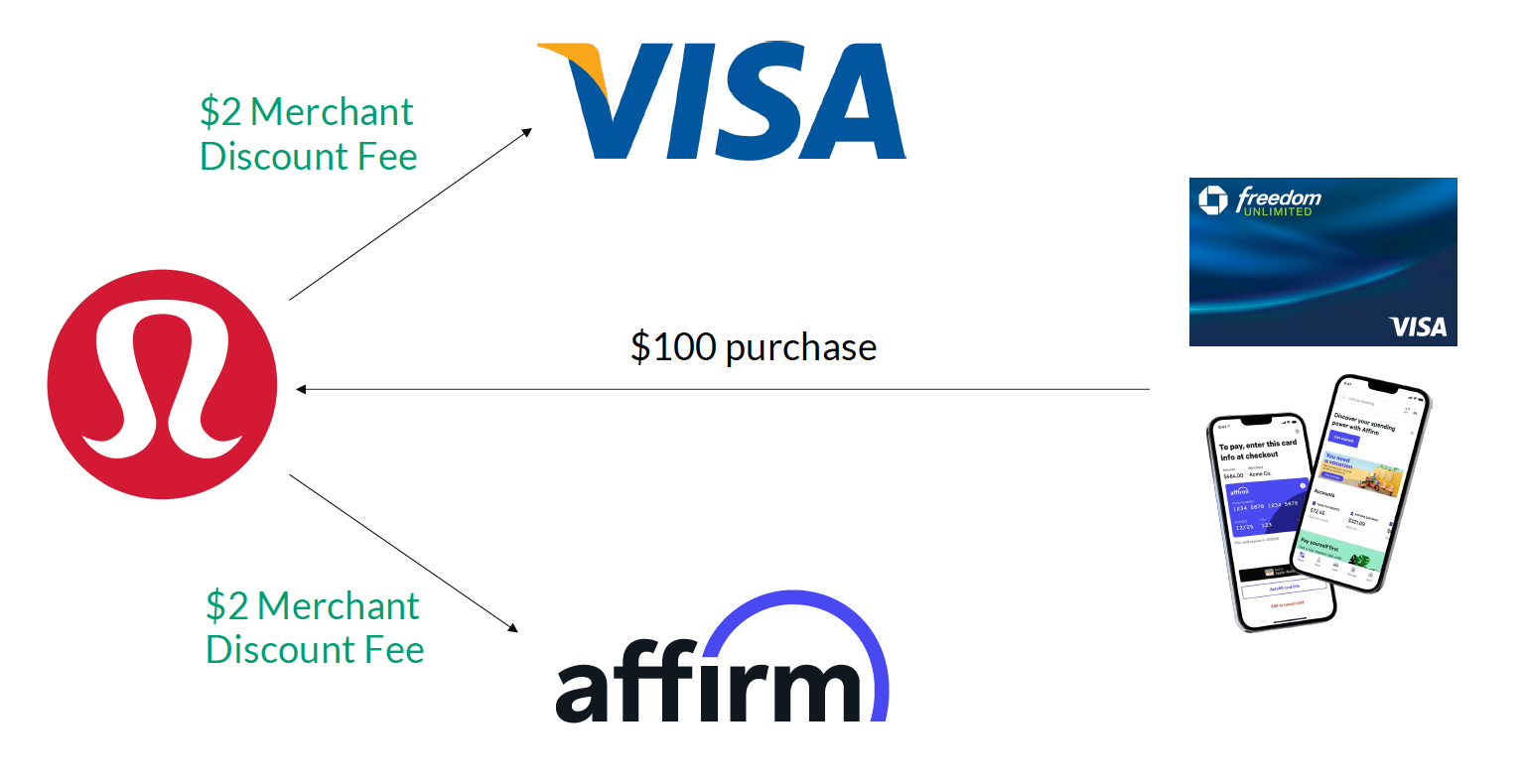

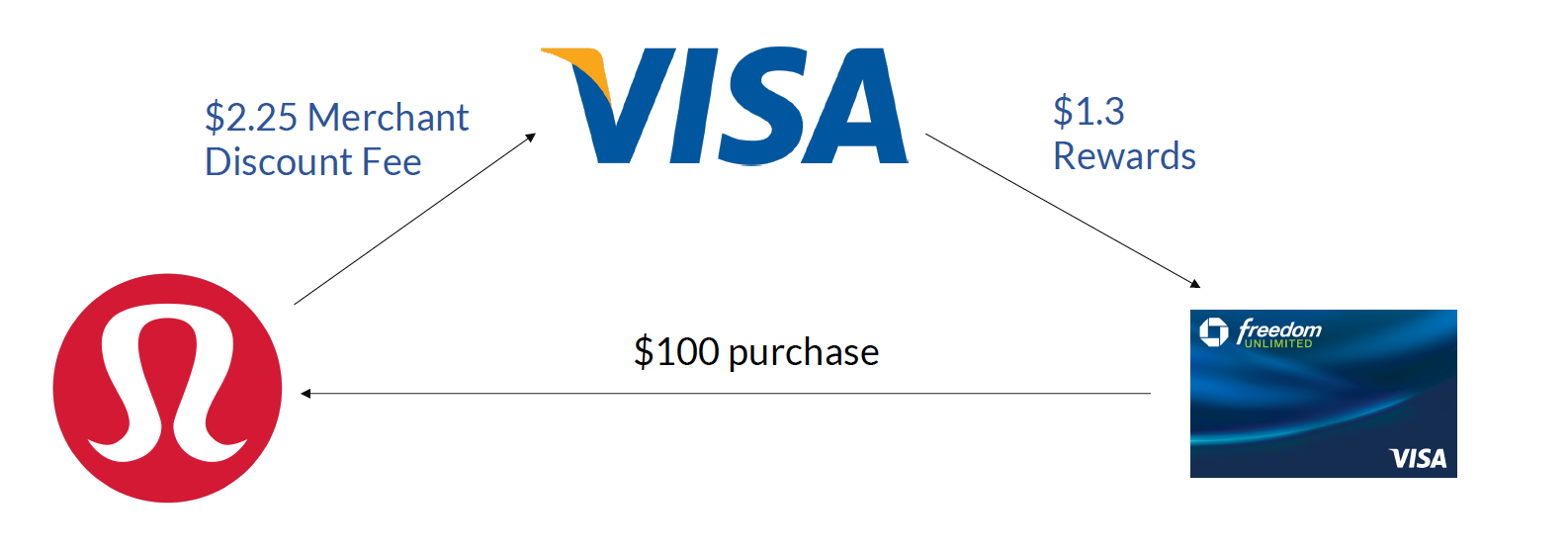

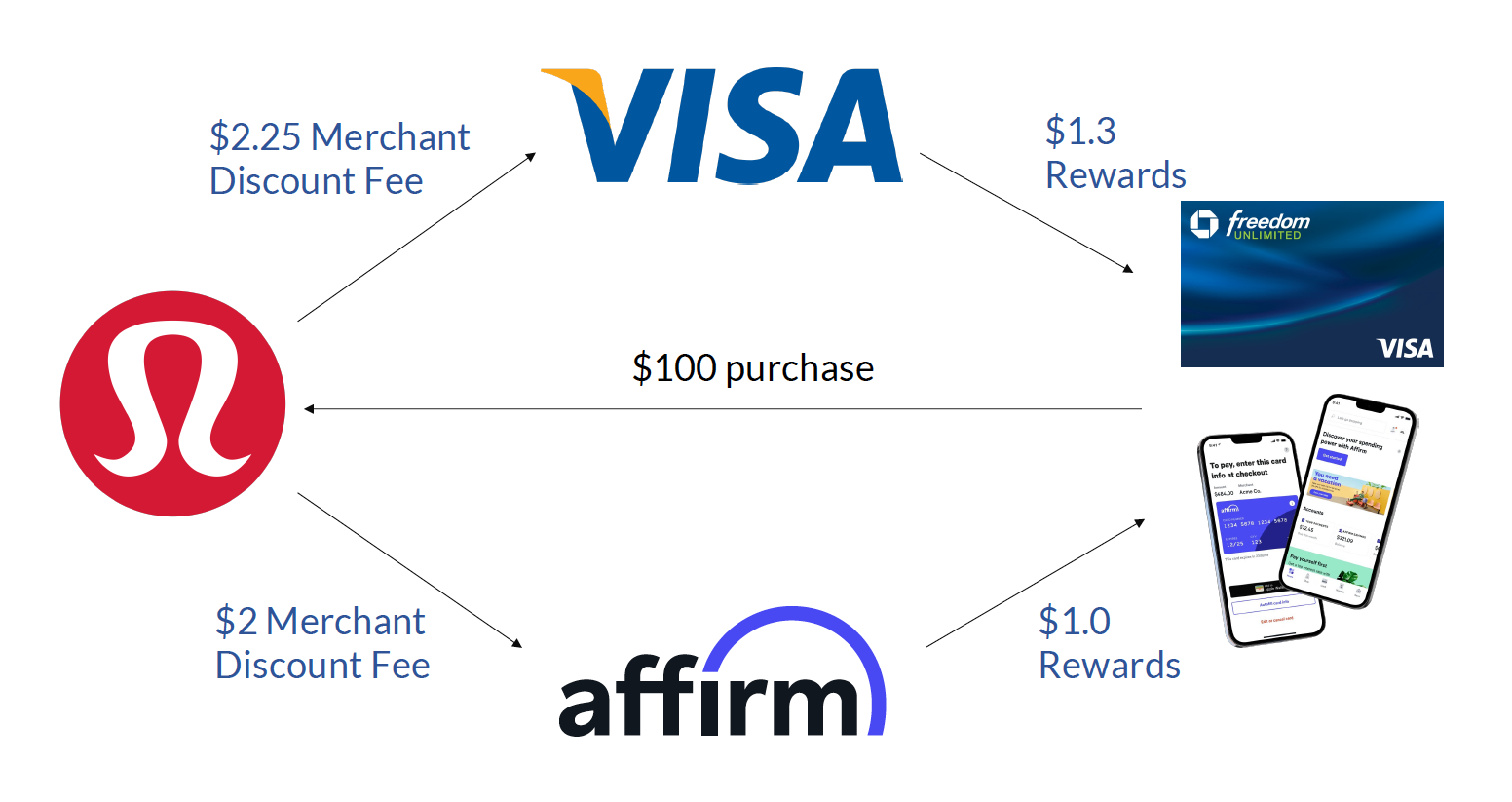

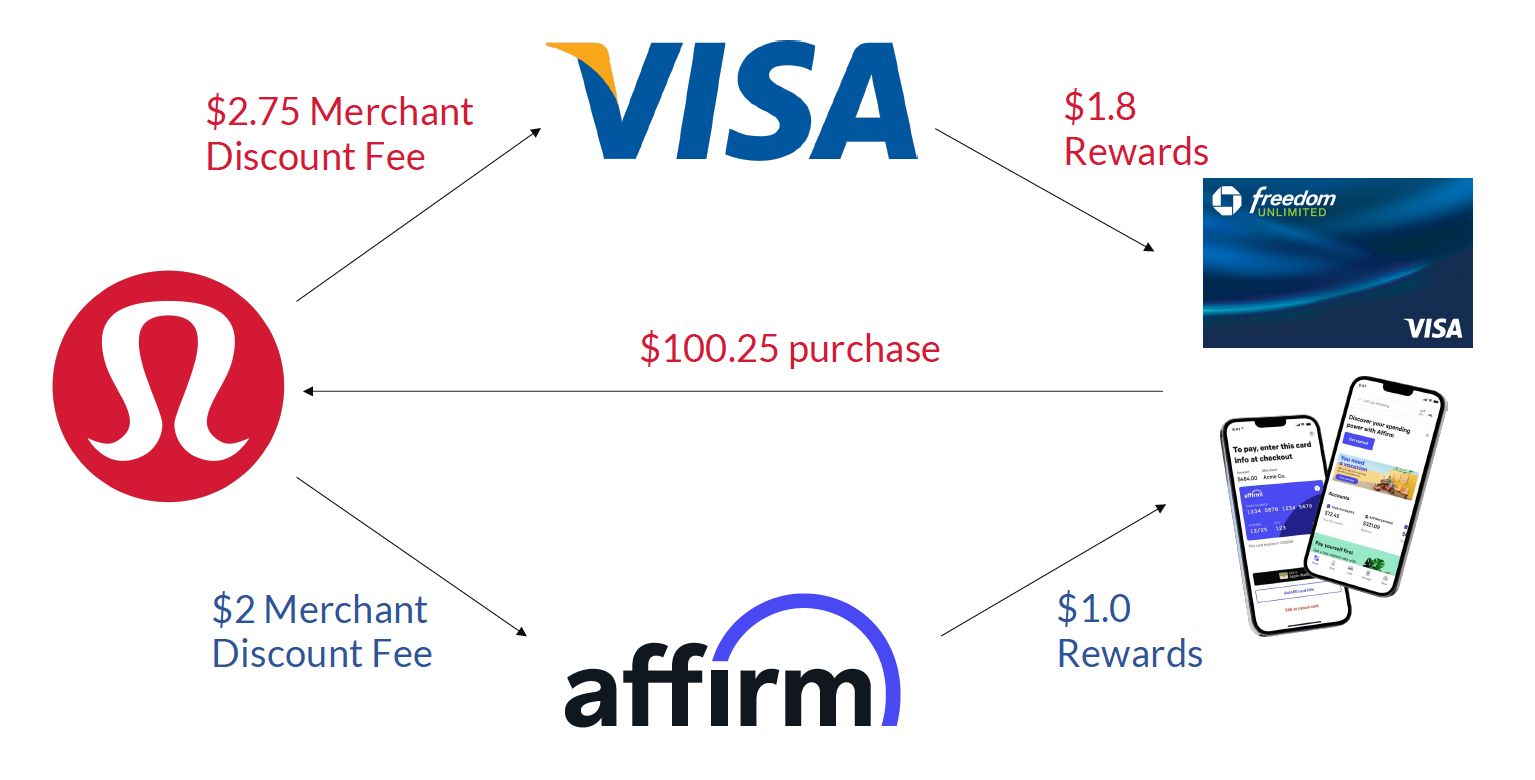

VISA cranks up the rewards

merchant raises prices - for everyone!

benefit of a CBDC as a competing payments tool is unclear

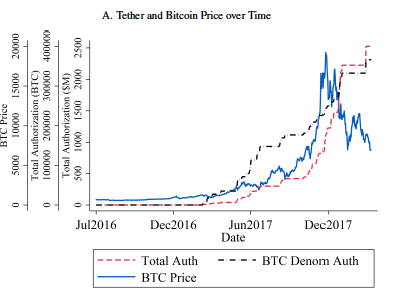

Why should we worry about private money? The Case of Tether

Historically: “Tether Platform currencies are 100% backed by actual fiat currency

assets in our reserve account.”

Text

Today: "The Tether Platform is fully reserved when the sum of all tethers in circulation is less than or equal to the value of our reserves."

IS BITCOIN REALLY UN-TETHERED?

JOHN M. GRIFFIN and AMIN SHAMS

Journal of Finance 2020

Text

IS BITCOIN REALLY UN-TETHERED?

JOHN M. GRIFFIN and AMIN SHAMS

Journal of Finance 2020

Text

IS BITCOIN REALLY UN-TETHERED?

JOHN M. GRIFFIN and AMIN SHAMS

Journal of Finance 2020

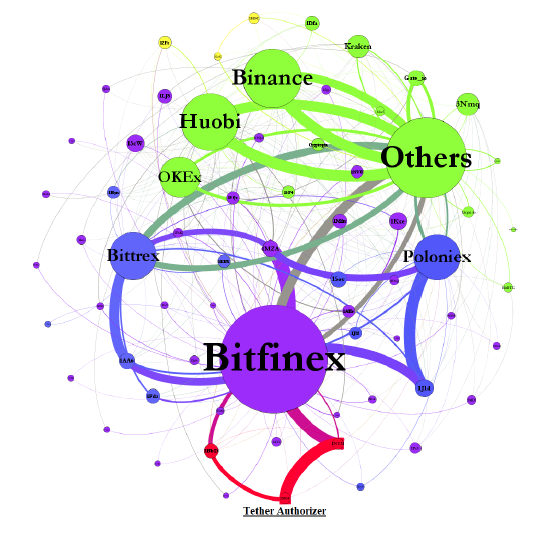

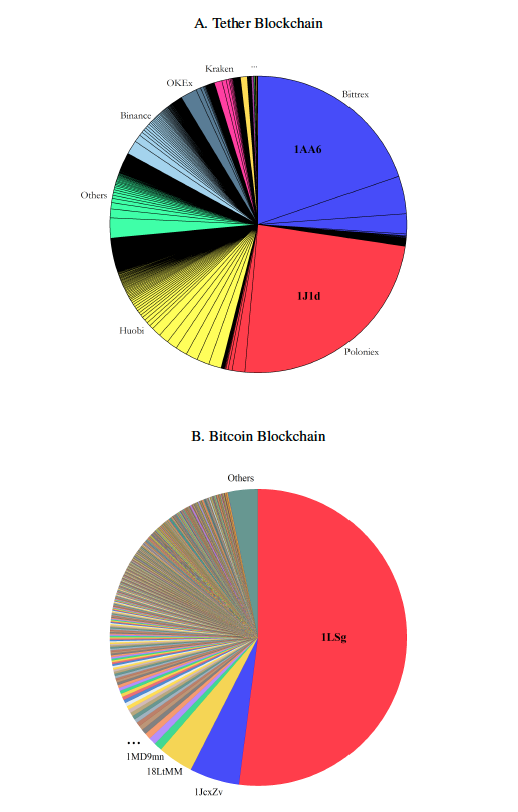

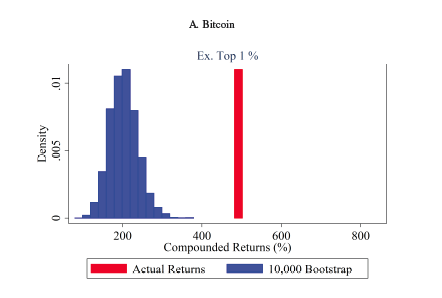

Figure 1. Aggregate Flow of Tether between Major Addresses

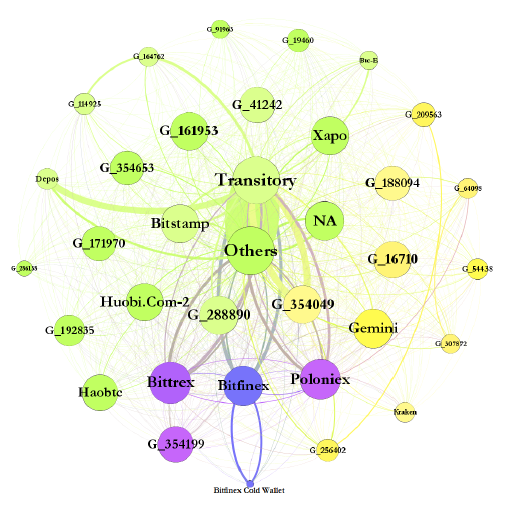

Figure 3. Aggregate Flow of Bitcoin between Major Addresses.

Top Accounts Associated with the Flow of Tether from and Bitcoin to Bitfinex

the 1% of hours with the strongest lagged Tether flow are associated with 58.8% of the Bitcoin buy-and-hold return over the period.

the "normal-times" returns

CBDC: Token vs Accounts

A Taxonomy

Bech and Garratt (2017)

Prevailing view: account-based central bank e-money system is unlikely to be the preferred choice of policymakers

Tokens or Accounts?

Prevailing view: account-based central bank e-money system is unlikely to be the preferred choice of policymakers

Why not?

Some history on private money

CBDC: Impact of "Global" Money

CBDC: Impact of "Global" Money

Cryptocurrencies, Currency Competition and the Impossible Trinity

Benigno, Schilling, Uhlig (2020)

Old: impossible trinity

New: with free capital and global currency, equalization of national policy interest rates

\(\to\) less of a point of national currency

Platform Economics

Examples of platform markets

gamers

users

“eyeballs”

cardholders

videogame platform

operating system

portals, newspapers, TV

debit & credit cards

game developers

application developers

advertisers

merchants

buyer

platform

seller

Platform pricing

Source: Jean Tirole's Nobel Lecture

Implications for the platform business model

Source: Jean Tirole's Nobel Lecture

Simple Example: heterosexual clubbing

assumption: people go clubbing to meet the opposite gender

common problem: imbalance of people from each gender

common solution: differential pricing (including free entry) for one side of the market

Regulation?

Question: is it a must-use arrangement or do people have alternatives?

By Andreas Park