Andreas Park PRO

Professor of Finance at UofT

Tokenization of Traditional Assets

and their trading

Katya Malinova and Andreas Park

Background and Overview of this Policy Paper

Idea: Think through the process and implications of tokenizing common shares on the Ethereum (or similar) public blockchain

My perspective: an economist, not a lawyer!

Source: "Relevance of on-chain asset tokenization in ‘crypto winter’"

By Sumit Kumar, Rajaram Suresh, Darius Liu, Bernhard Kronfellner and Aaditya Kaul, Sept 2022

(South-East Asian countries)

Key Institutional Differences

Key Institutional Features of Equities

Institutional Differences: Crypto Asset Ownership, Accounts, Wallets, and Self Custody

Smart contract accounts

Externally owned accounts

controlled by private keys

private

key

public

key

(seed phrase)

public

address

wallet = software to keep and use private keys

Blockchain Ownership Attribution

Institutional Differences: Asset Creation

Institutional Differences: The Investment Process

issuers

investors

services

needed & provided

A general purpose value management infrastructure:

intermediaries

separate institutions

The blockchain reality:

new institutions

will emerge

Institutional Differences: Trading and Asset Registries

payments network

Broker

Broker

Stock Exchange

Clearing House

custodian

custodian

seller

buyer

beneficiary ownership record

Institutional Differences: Trading and Asset Registries

seller

buyer

Application: Decentralized Borrowing & Lending

borrow

provide collateral

UniSwap Lab supports development

a website app accesses the code

token holders control contact features

don't own the code

operation = decentral

control = decentral

anyone can use the baseline code

core code runs on the blockchain

tokens used as rewards

Institutional Differences: Blockchain Project Operation

Asset Tokenization or

"The Creation of Asset-Linked Tokens"

Tokenization of stocks is nothing new: American Depository Receipts

foreign investor/

issuer

domestic bank with foreign representation

ADR issuing bank handles

Is this a workable model for blockchain- tokenization of existing assets?

foreign representation of domestic bank/ its custodian

domestic depository bank

S.E.C.

registration with form F-4

domestic broker

issues and cancels ADRs

domestic investor

lets investors own and trade ADRs

domestic

market

deposits shares

foreign investor/

issuer

domestic bank with foreign representation

foreign representation of domestic bank/ its custodian

domestic depository bank

S.E.C.

registration with form F-4

domestic broker

issues and cancels ADRs

domestic investor

lets investors own and trade ADRs

domestic

market

deposits shares

Blockchain Tokenization has many options

existing investor/

issuer

token issuance platform

investor

wallet

instruct to create tokens

deposits shares

custodian bank

deposits shares

creates tokens and sells to investors

centralized or decentralized

market

S.E.C.

registration

existing investor/

issuer

investor

wallet

centralized or decentralized

market

S.E.C.

existing investor/

issuer

token issuance platform

investor

wallet

instruct to create tokens

deposits shares

custodian bank

deposits shares

creates tokens and sells to investors

centralized or decentralized

market

S.E.C.

registration

Token Standards

Some basic facts

Fact 1: Ownership of tokenized asset can be

Fact 2: By default issuers do not know who owns their tokens

Fact 3: Investors who hold tokens in DeFi smart contracts have fluctuating holdings.

Fact 4: General ownership restrictions are almost impossible to enforce, and transfer restriction would negate advantages of tokenization

Problems that require solving

ADR issuing bank handles

How are these functions performed with crypto-assets?

Fact 2: By default issuers do not know who owns their tokens

Some remedies for communication and dividends

All this needs a legal framework that adapts to a decentralized, digital world

Problems that require solving

ADR issuing bank handles

Remaining FIs handle

Fact 4: General ownership restrictions are almost impossible to enforce, and transfer restriction would negate advantages of tokenization

Legal and regulatory frameworks currently rely on intermediaries and are not prepared for self-custody

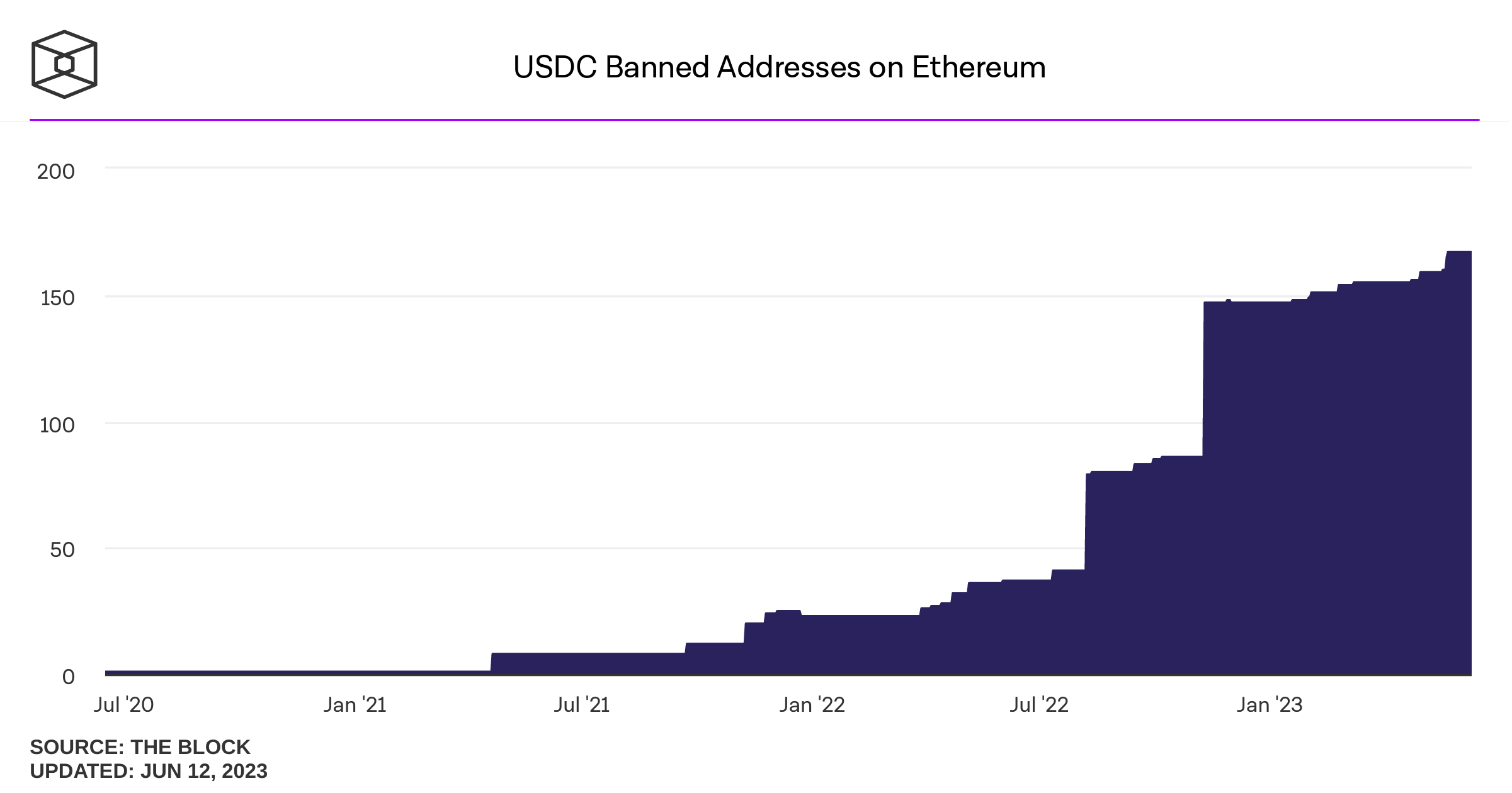

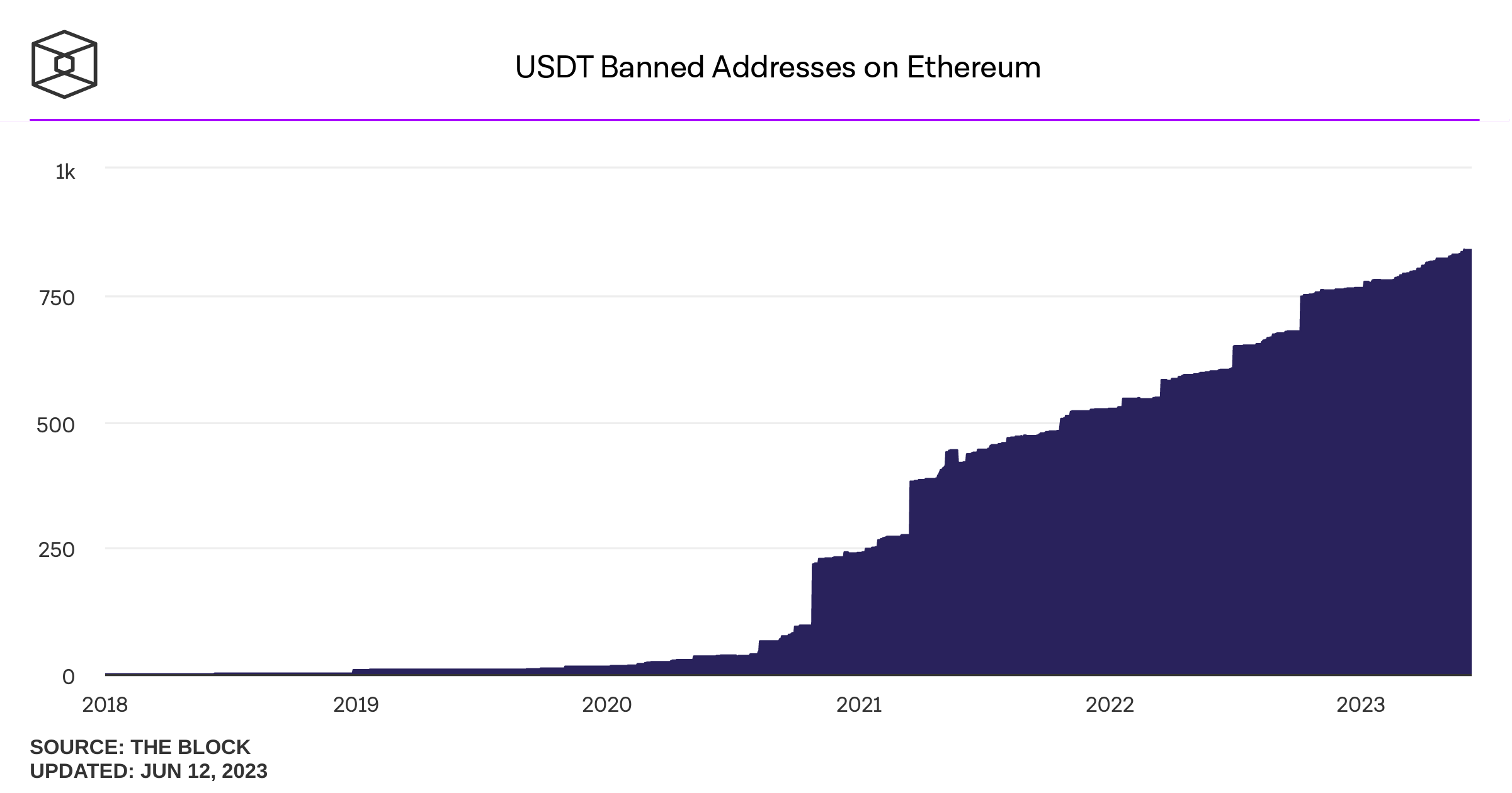

criminals don't use USDC - why are we so worried?

Broader Implications for the Financial Industry and the Financial System

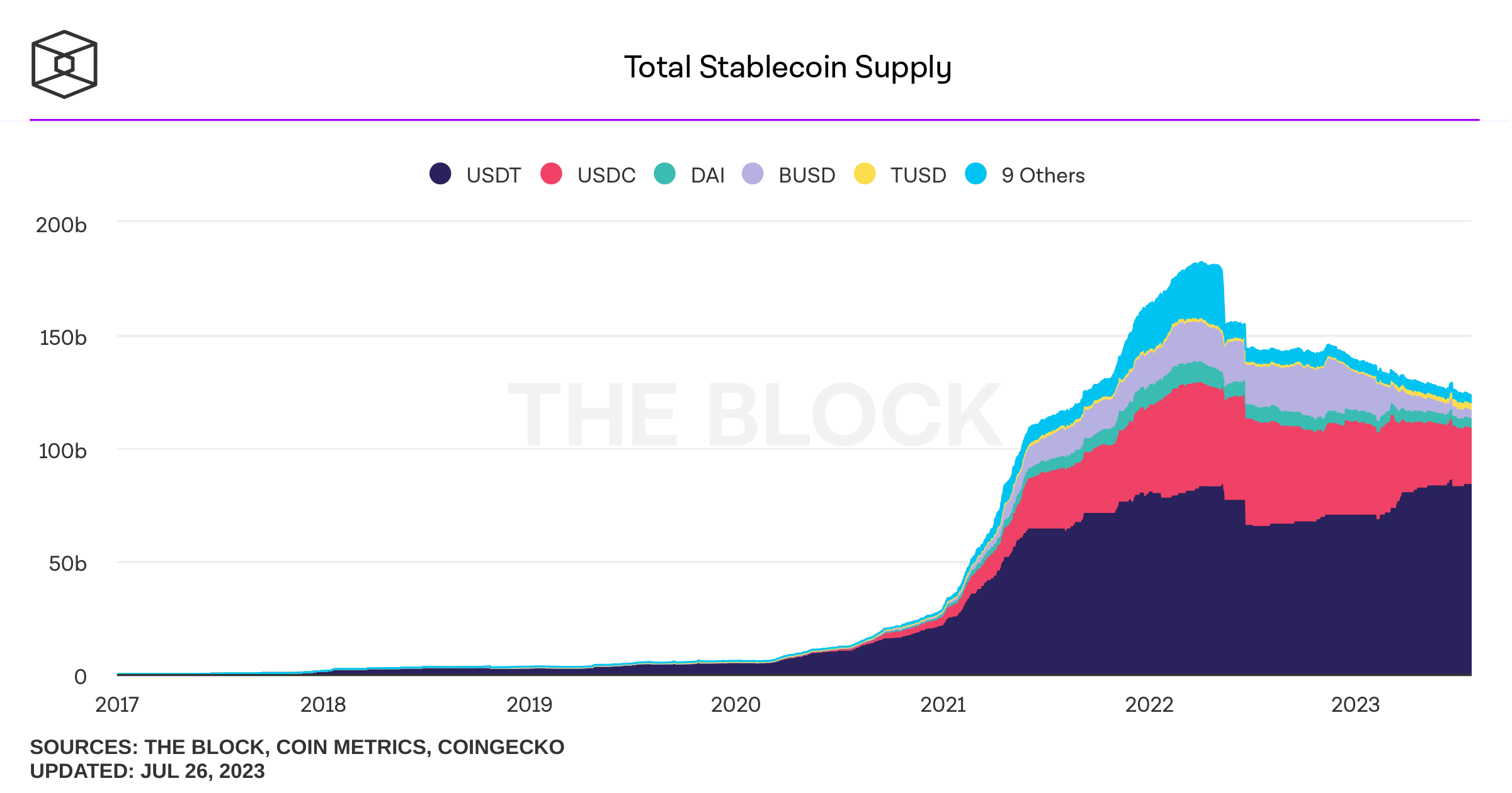

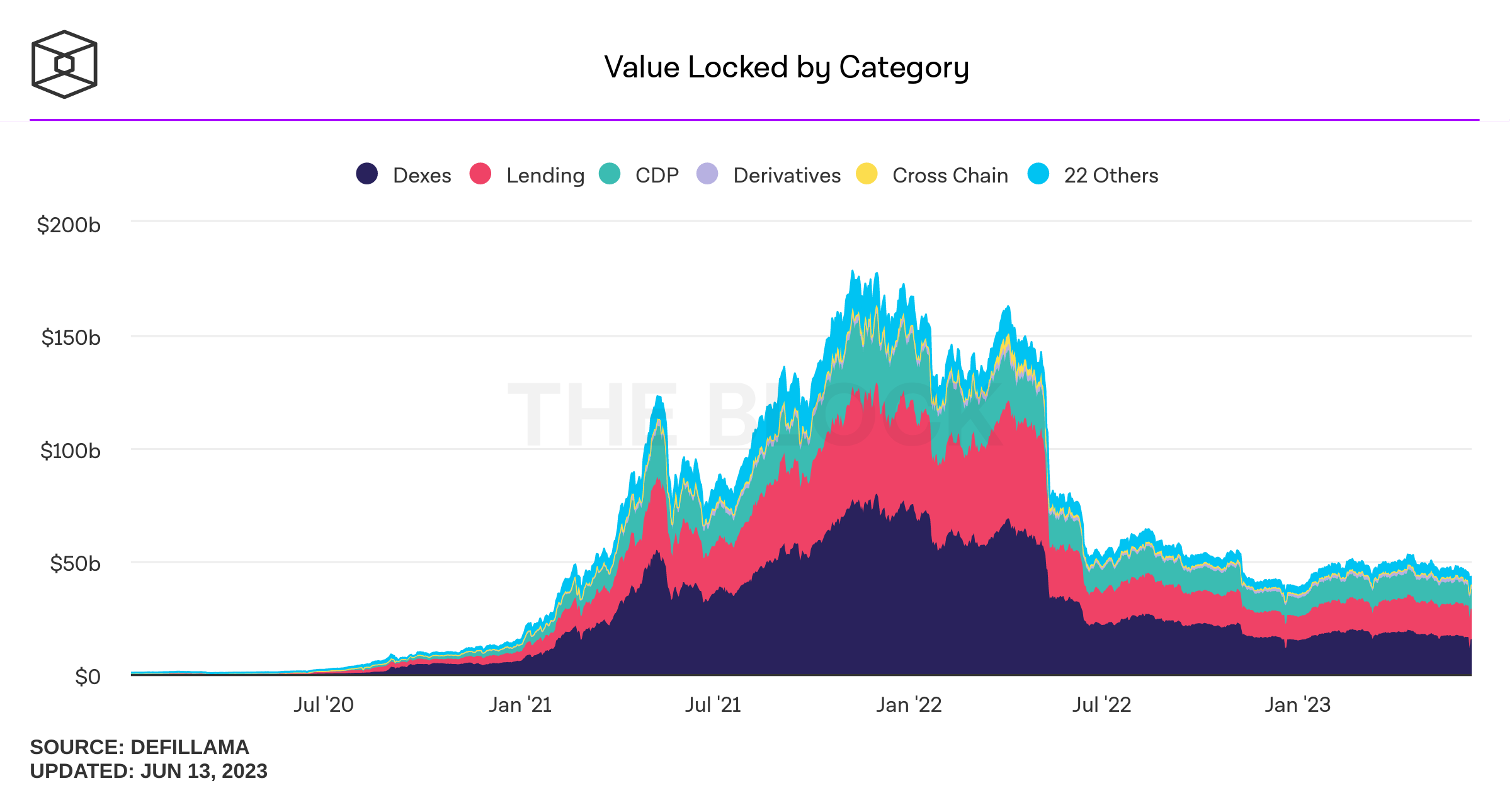

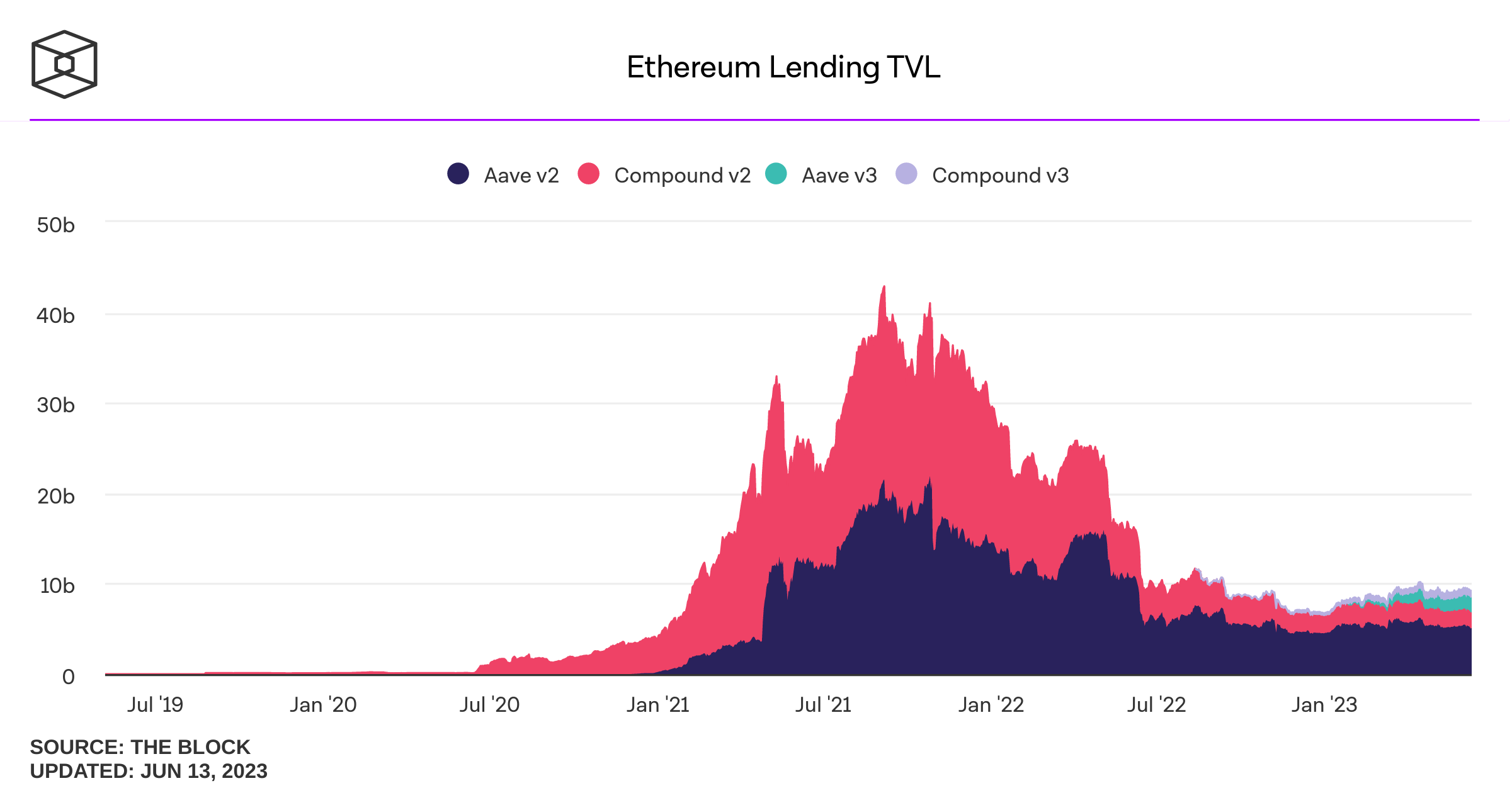

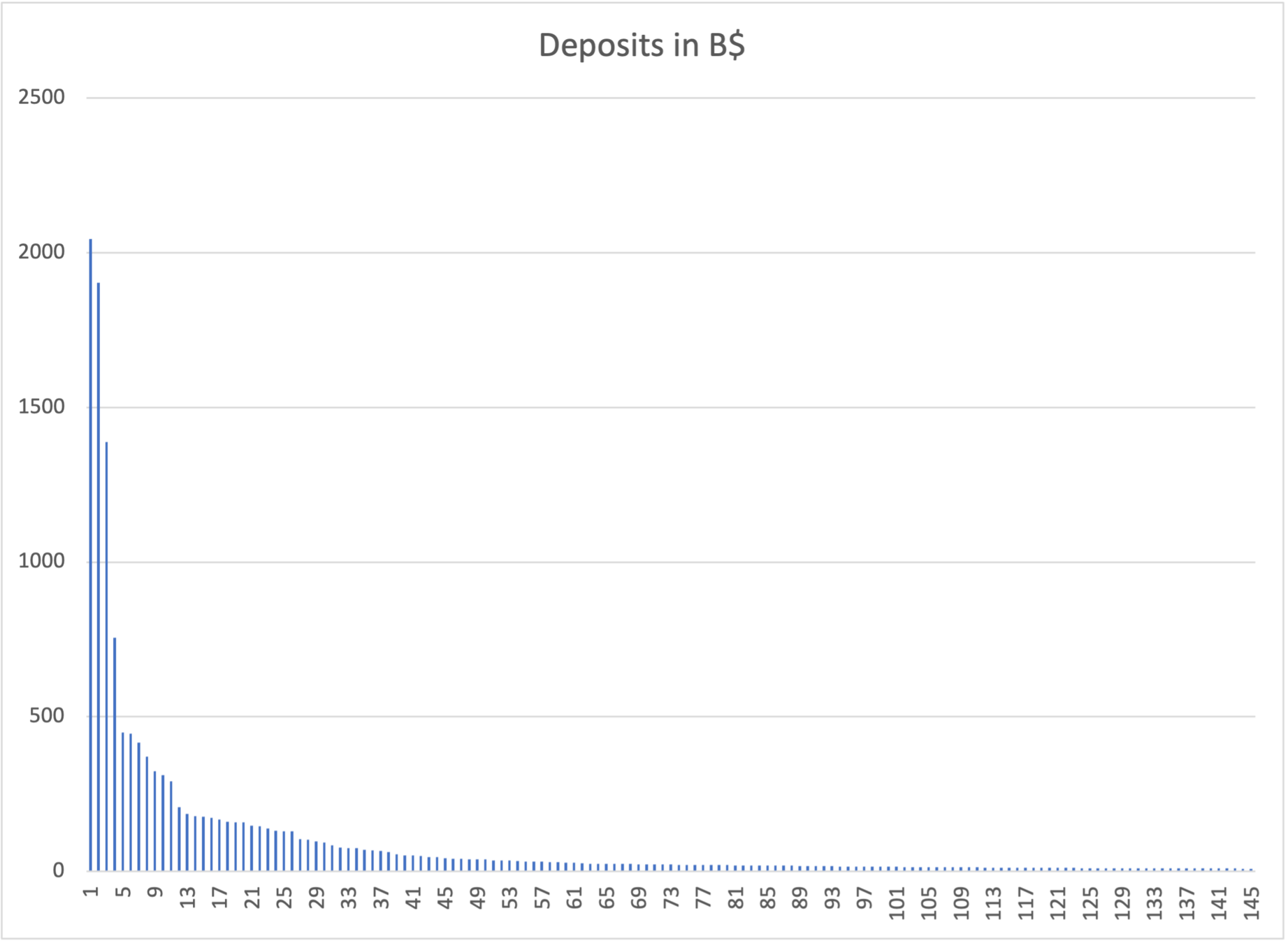

Asset tokenization would likely create a massive expansion in demand for stablecoins

max TVL:

top 20

max lending:

top 50

current lending:

top 100

Asset tokenization would likely create a massive expansion in demand for stablecoins

Stablecoins and Deposits

huge demand for continuously available "high quality" money

Broad Blockchain Risks to Financial Stability

Lending capacity & Monetary transmission

Deposit mobility

AML/CFT/Sanction evasion

Dollarization

Failures/runs

New cyber-risks

Broad Blockchain Risks to Financial Stability

Stablecoins require deposits that are invested only in HQLAs

stablecoin deposits \(\not=\) sticky

Crypto-assets facilitate sanction evasion, money laundering, ransonware attacks, terrorist financing

USD stablecoins

Stablecoin failure/runs could lead to

a host of unknown, highly scalable attack vectors

Lending capacity & Monetary transmission

Deposit mobility

AML/CFT/Sanction evasion

Dollarization

Failures/runs

New cyber-risks

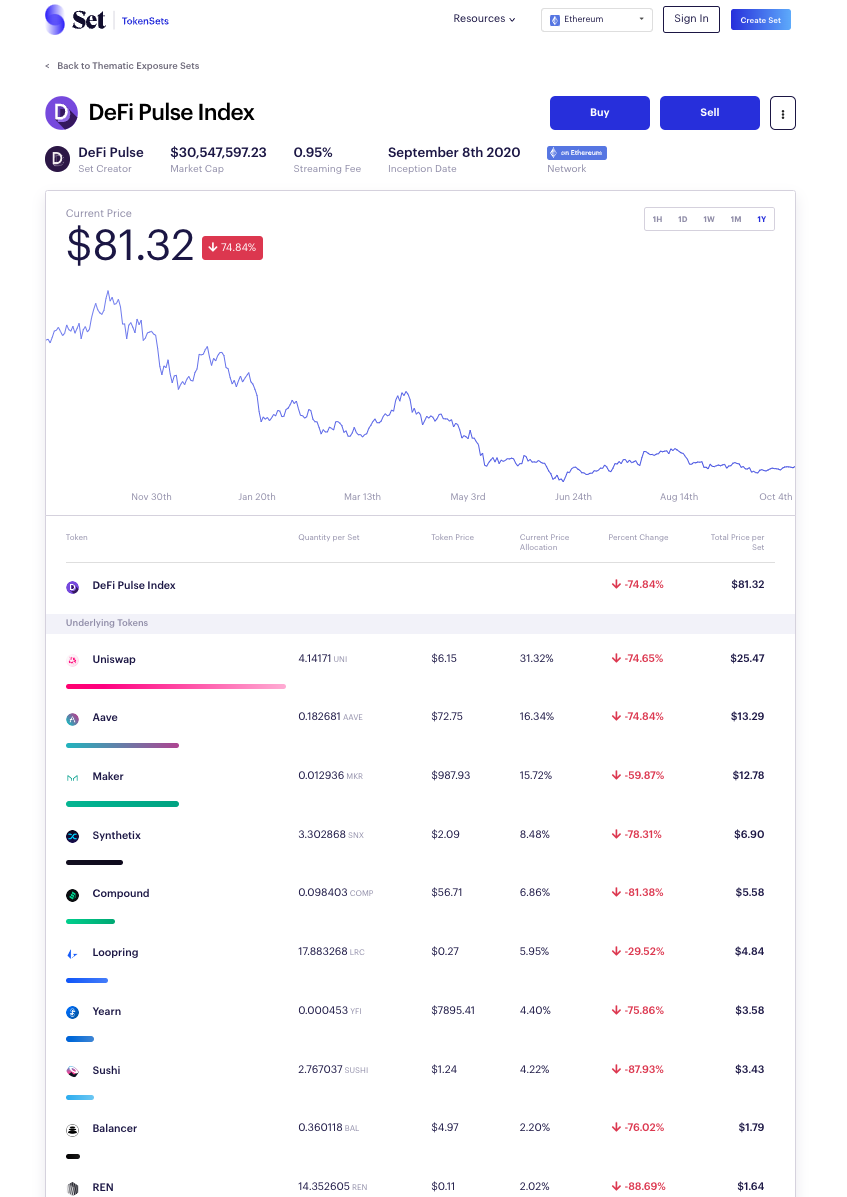

Business risk for existing FI: super-easy entry

idea: create new mutual fund like asset

Business Risk to FIs: Customers choose what's best for them

"yield aggregator:" push capital where rate of return is highest

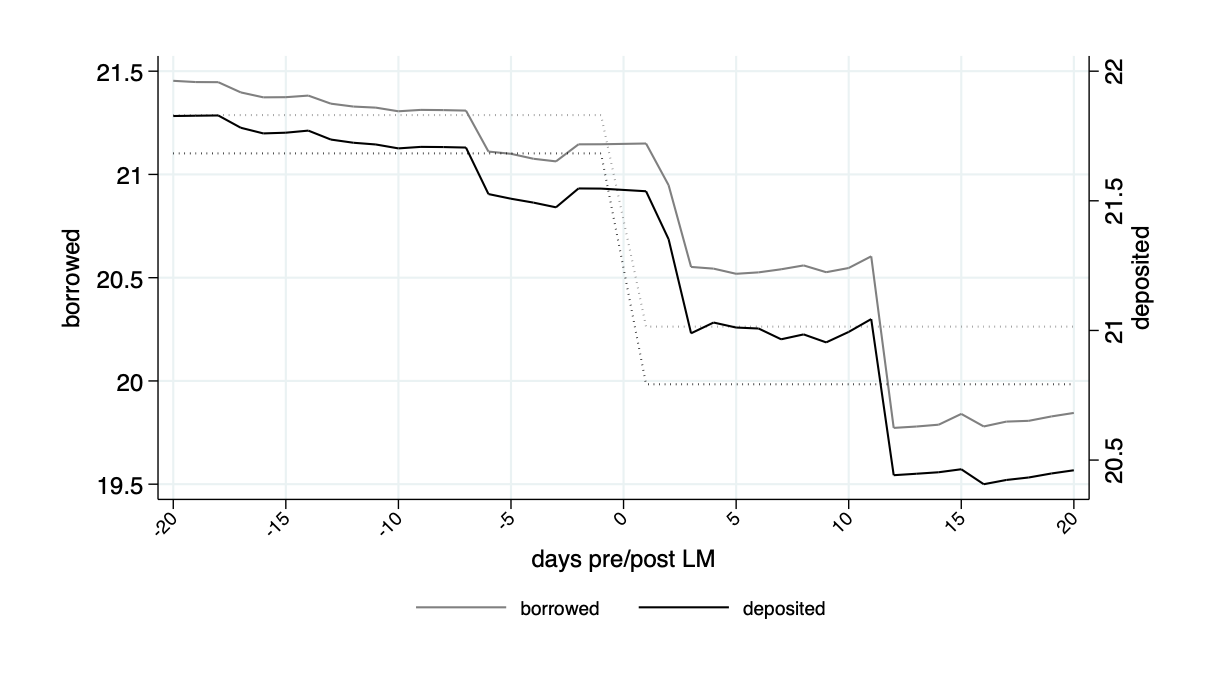

Yield Aggregators are very mobile liquidity

Source: "Phantom Liquidity in DeFi Lending", Park and Stinner (2023) working paper

Effects on the IO of Financial Services

Last Words

Summary

@financeUTM

andreas.park@rotman.utoronto.ca

slides.com/ap248

sites.google.com/site/parkandreas/

youtube.com/user/andreaspark2812/

By Andreas Park