Andreas Park PRO

Professor of Finance at UofT

Instructors: Andreas Park & Zissis Poulos

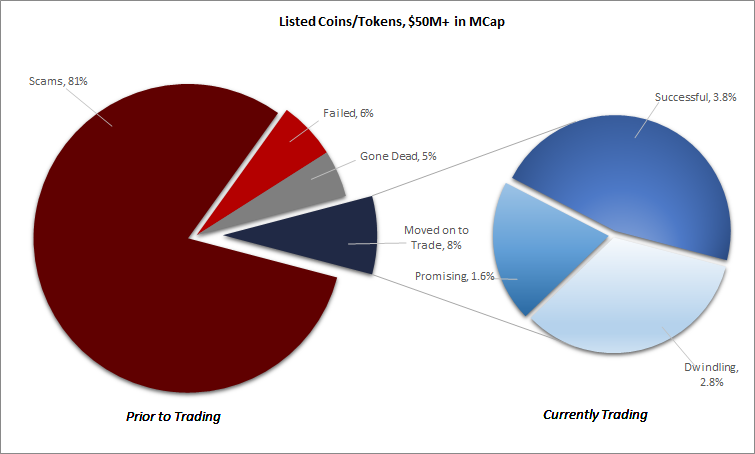

Source: Satis Group LLC

Data: coinschedule

Around 1B in token sales so far

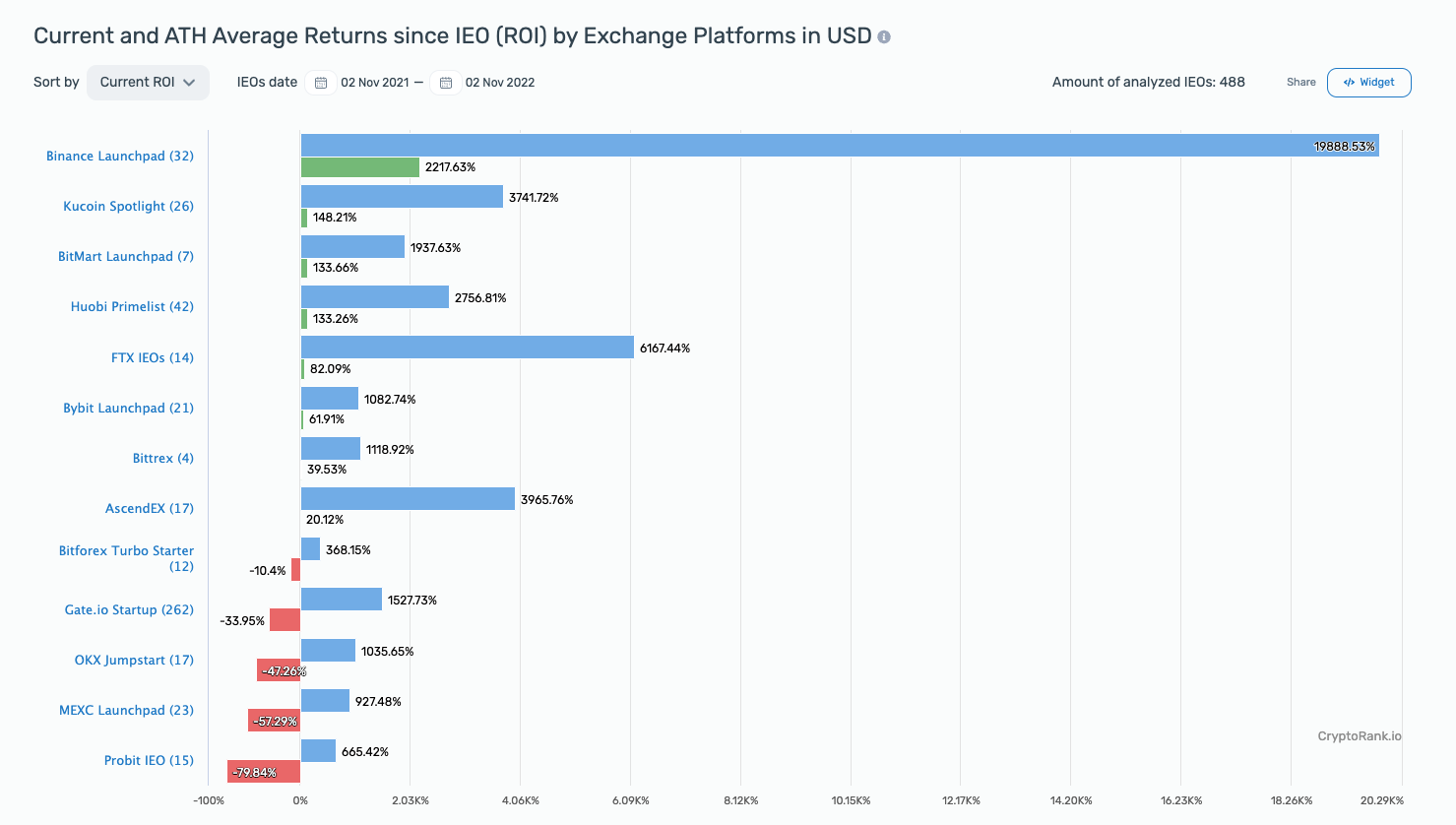

https://cryptorank.io/

IEO Data for 2022

https://cryptorank.io/

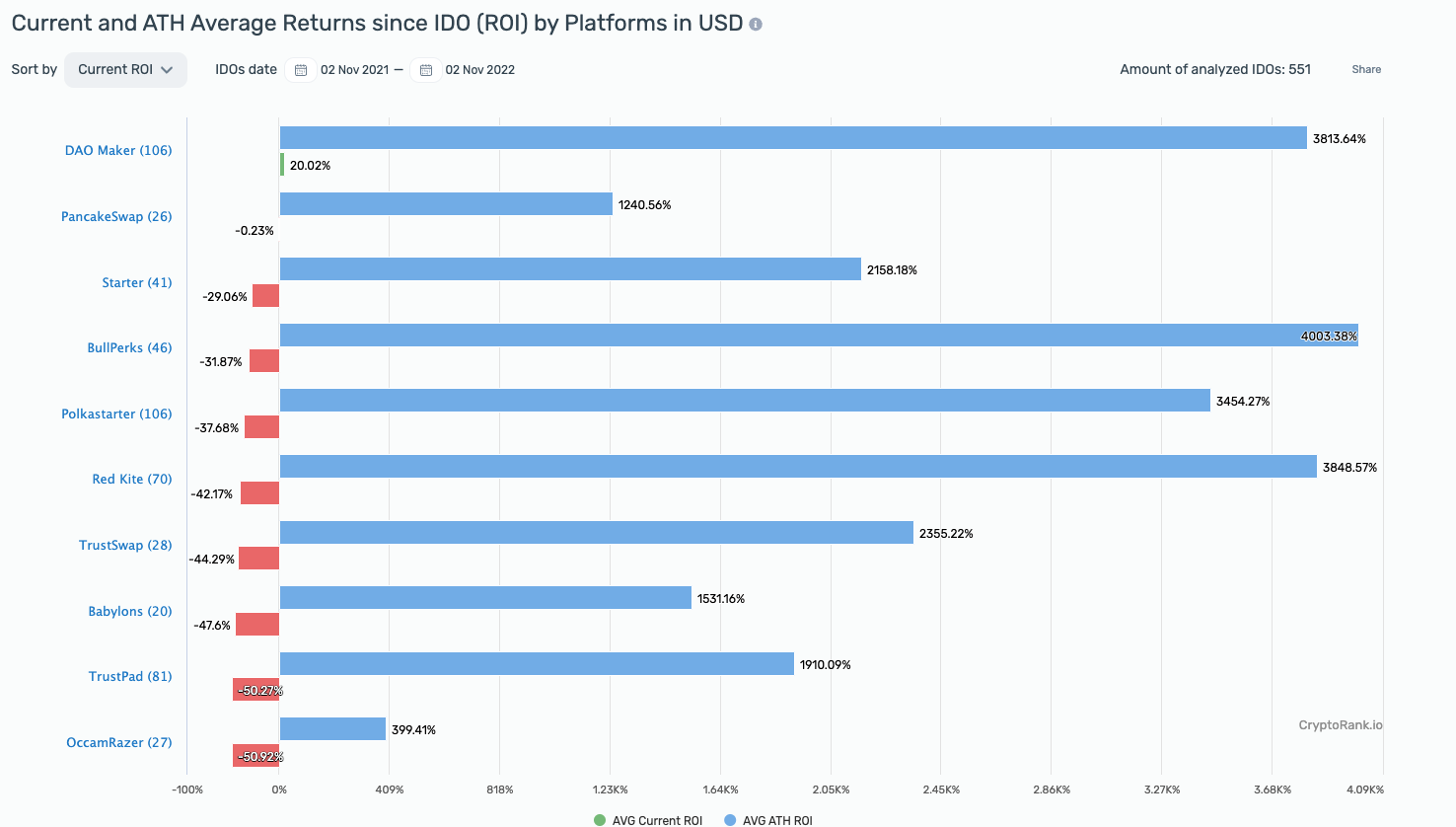

IDO Data for 2022

| count | Total Raised (M) | Mean Raised (M) | Mean ROI | Mean ATH ROI | |

|---|---|---|---|---|---|

| IEO | 324 | 266 | 1.8 | 28x | 47x |

| IDO | 779 | 35 | 0.25 | 10x | 30x |

Smaller projects opt for IDO

https://cryptorank.io/

Data for 2021

Sidebar: “crypto asset” means a digital representation of value or contractual rights, which may be transferred and stored electronically, using distributed ledger or similar technology;

Sidebar: Designation orders (CMA Section 127) (paraphrased)

Key takeaway: many investment contracts can be deemed securities

Payment

Asset

Utility

Source: Harbour (a tech firm)

Recently permitted by the SEC in the US and the CSA in Canada; restrictions (among others)

Limits for investors (per firm and total portfolio value)

Must used registered platform

CTPs have recently been informed to limit new investments to $50K

What's a crypto-token and what's special about it?

payments:

utility

stablecoins

governance

asset

derivatives

Disclaimer: this list in non-exhaustive, new ideas come up every day!

“I believe every ICO I’ve seen is a security. … ICOs that are securities offerings, we should regulate them like we regulate securities offerings. End of story.”

Jay Clayton, Chairman, U.S. Securities and Exchange Commission, testimony before the United States Senate, February 6, 2018

“I have asked the SEC’s Division of Enforcement to continue to police this area vigorously and recommend enforcement actions against those that conduct initial coin offerings in violation of the federal securities laws”

tokens enter the public market and become accessible to the general public => huge implications on transparency and disclosure requirements

in pre-financing and pre-sale phases of an ICO, tokens that confer claims to acquire tokens in the future

treated as securities

Payment

Asset

Utility

if additionally or only has an investment purpose at the point of issue:

=> treated as security

Example: ML/TF laws

Source: Satis Group LLC

Data from early 2018

total gain: 230,000%

Lower commissions with cryptocurrencies (no intermediaries to feed).

Can be pre-programmed to carry out the company’s incentive payouts — or returns — as set out in White Papers and Investor Prospectuses.

Contingent fundraising.

Milestone automation.

Venture financing open to everyone

Small minimum investment amounts

Global investor base

Tokens are immediately tradable

Classification (Source: Satis Group LLC)

Source: Satis Group LLC

Payment

Asset

Utility

Lessons?

Traditional economy

Decentralized economy

Traditional "centralized" economy

Chod and Lyandres (MS 2021):

Davydiuk, Gupta, and Rosen (2018)

Lee and Parlour (RFS 2022)

Malinova and Park (2018)

Shakhnov and Zaccaria (2022)

price

demand

marginal cost

marginal revenue

general idea: sell future output

two approaches for token sales

sell a fraction of future revenue

sell units of future output

price

demand

marginal cost

marginal revenue

Entrepreneur does not internalize the effect of an extra output unit on the token value for the tokenholders!

Result: overproduction

price

demand

marginal cost

marginal revenue

Result: underproduction

\(\Rightarrow\) shifts marginal revenue for entrepreneuer left because get only fraction of revenue

revenue sharing: underproduction

output presale: overproduction

\(c\)

\(MR\)

"does not internalize" = externality

address externality: TAX!

here: tax future token income

incremental token income gets shared

\(\Rightarrow\) combine the two to get the monopoly quantity!

Idea:

entrepreneur can influence expected demand

with effort

without effort

assume \[\textit{NPV}(\text{effort})>0>\textit{NPV}(\text{no effort})\]

Investors (equity or token holders) only finance the project if the entrepreneur undertakes the effort

Solve for the optimal funding conditional on the entrepreneur taking the effort

Derive conditions such that the entrepreneur undertakes effort

1.

2.

Key insight: a token contract incentivizes effort better than equity (similarly to canonical debt vs. equity insights)

Optimal token contract has debt features:

all projects that can be financed by equity can be financed by the optimal token contract but

some projects that can be financed by optimal tokens contracts cannot be financed by equity.

Simple model of revenue-based ICO vs equity financing from the standard corporate finance + IO toolbox

Theorem 1: Without frictions, an optimal token contract finances the same projects as equity

Theorem 2: With entrepreneurial moral hazard,

By Andreas Park

This set of slides describes tokens as a form of financing of operations.