Andreas Park PRO

Professor of Finance at UofT

Discussion of "Stablecoin Runs and the Centralization of Arbitrage"

Paper by Ma, Zeng, and Zhang

Discussion by: Andreas Park

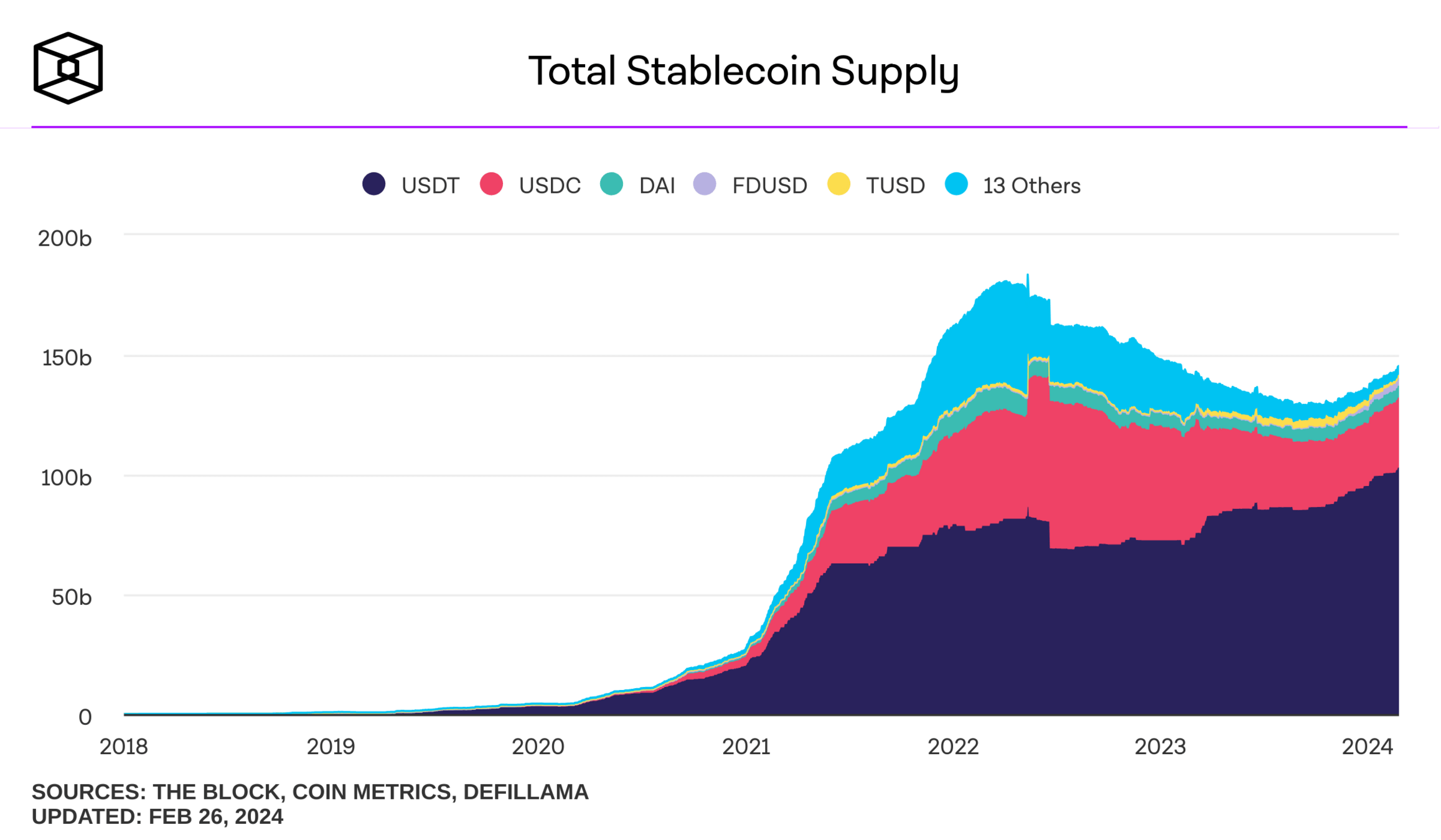

What is a stablecoin?

digital representation of a unit of a fiat currency on a blockchain

pulled from Nick Carter's talk on "Will stablecoins serve or subvert U.S. interests?"

stablecoins are crypto's/blockchain's first "killer" use case

JPM coin

USDC

USDT

UST, Basis, Neutrino

DAI, FEI

Collateral Backed Stablecoins: USDT & USDC

\(\Rightarrow\) 5% over-collateralized

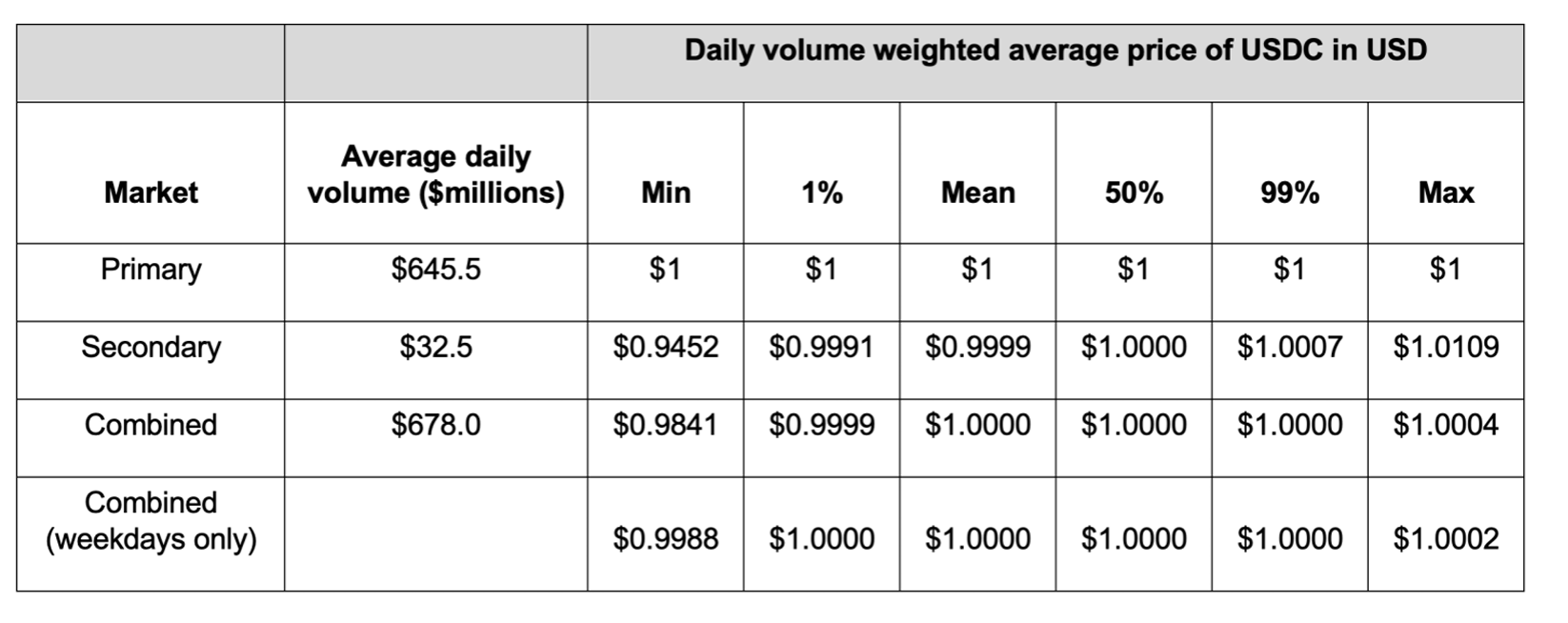

primary market acces: 6 entities only

Collateral Backed Stablecoins: USDT & USDC

primary market acces: 560+ entities

What makes a Stablecoin stable?

USD-USDT (6 months)

\(\Rightarrow\) need a primary/reference market mechanism to allow for forces of arbitrage to align prices

Arbitrage when price(stablecoin)>$1

arbitrageur

issuer/ primary market

secondary market

What makes a Stablecoin stable?

Arbitrage when price(stablecoin)<$1

arbitrageur

issuer/ primary market

secondary market

This paper: Runs!

Key Model Ingredients and what they do

1. stablecoin with primary and secondary market

2. liquidity transformation by stablecoin issuer \(\to\) Diamond-Dybvig bank run model

3. Morris-Shin-style global game

What's the Key Tension

to exchange stablecoins for USD at parity issuer needs to

find cash or

sell illiquid assets

Issues in the Secondary Market

Issues in the Primary Market

What's the Key Tension

What's the Key Mechanism

key implication:

less liquid backing \(\to\) more run risk

to exchange stablecoins for USD at parity issuer needs to

find cash or

sell illiquid assets

Issues in the Secondary Market

Issues in the Primary Market

key implication:

more liquidity \(\to\) more run risk

Intuition for Key Result

key implication:

more liquidity \(\to\) less price impact

less price impact \(\to\) more run risk

more abitrageurs \(\to\) more secondary market liquidity

Model Implications

Comments

Comment 0: all OK with the theory?

Comment 1: What brings prices back to parity?

1. primary market arbitrage

2. secondary market arbitrage

Arbitrage when price(stablecoin)<$1

arbitrageur

issuer/ primary market

secondary market

arbitrageur

issuer/ primary market

secondary market

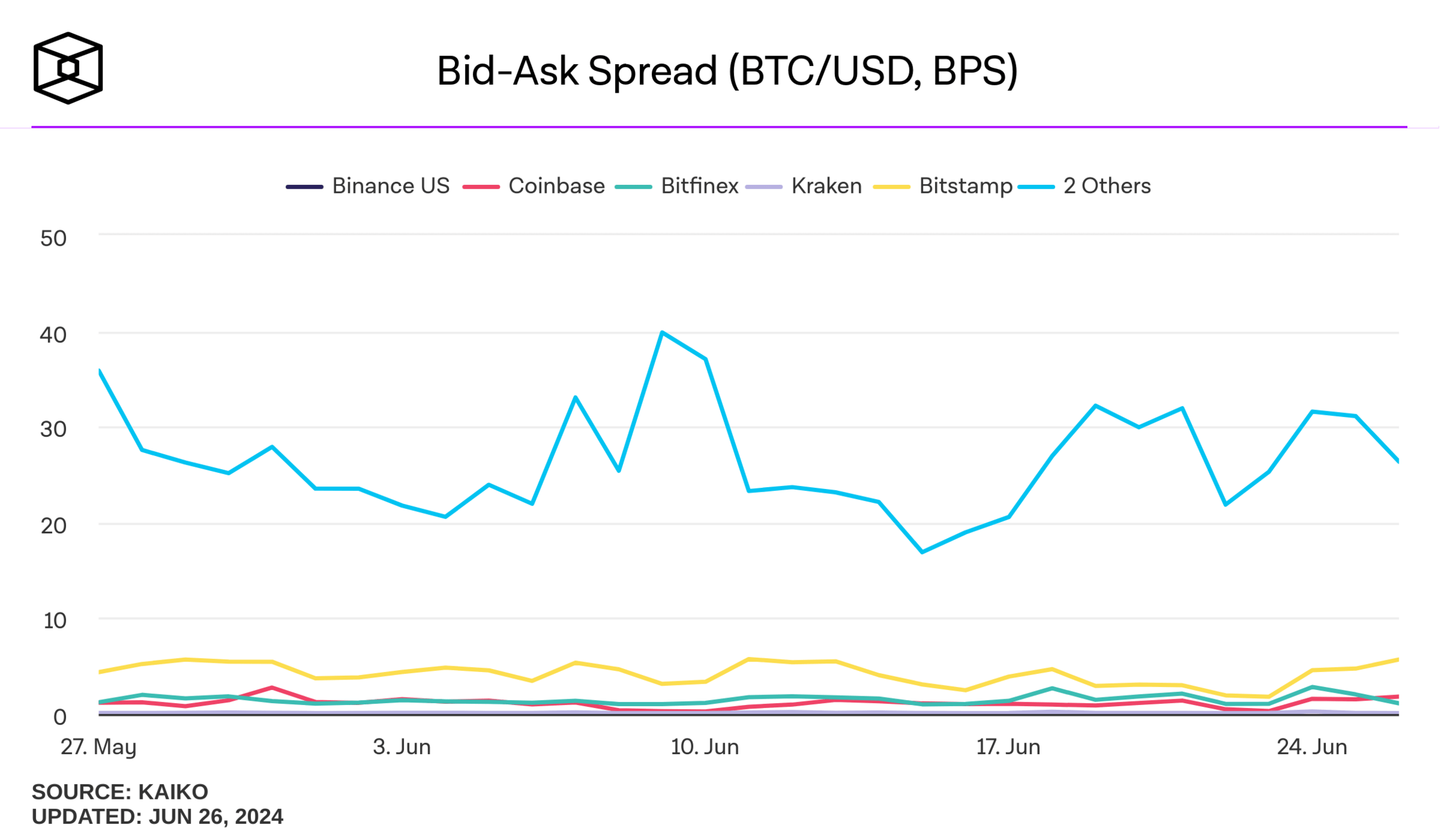

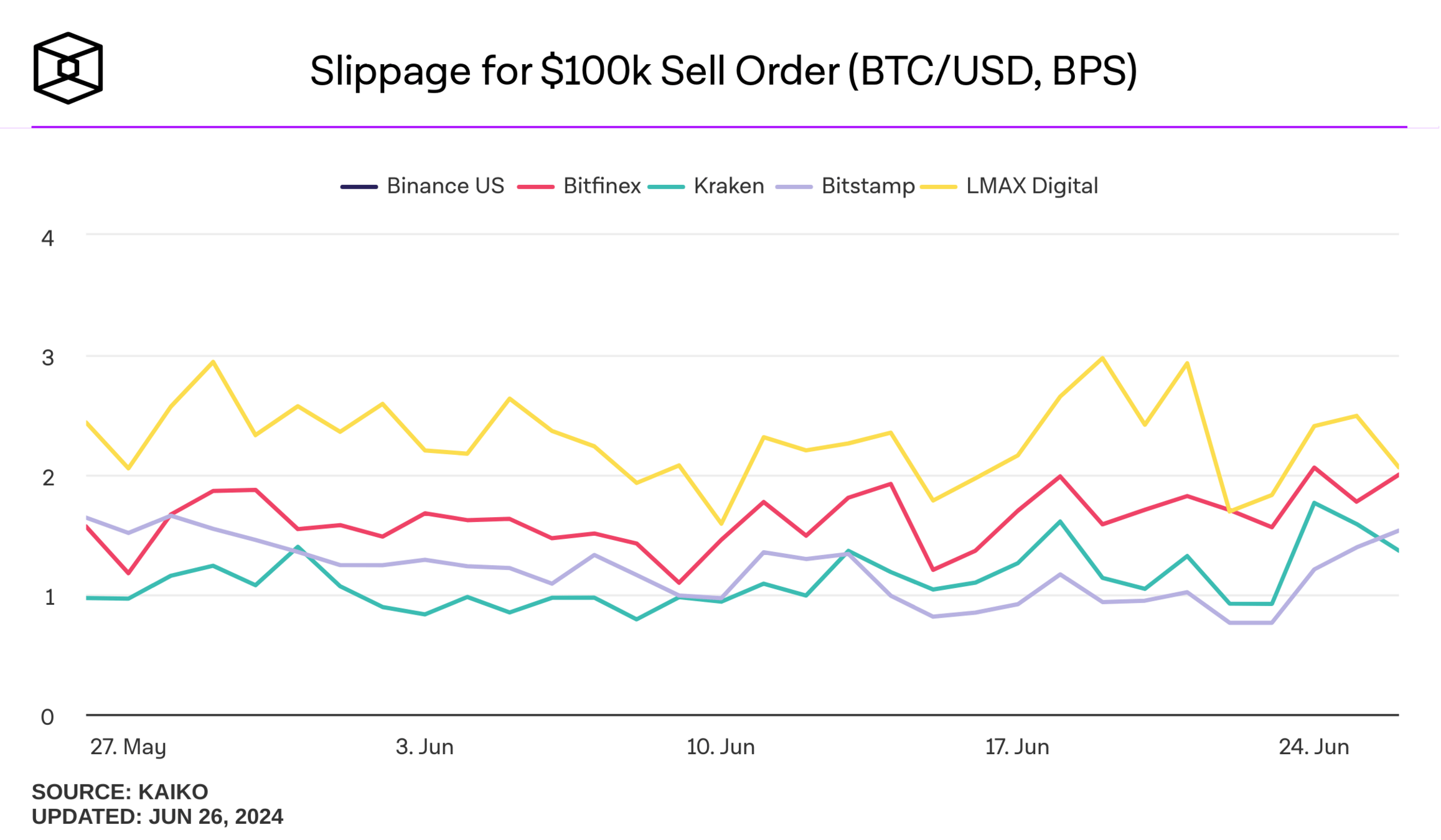

Cost on Kraken: .1 bps

Source: Liao (2023) "How to preserve the singleness of money for tokenised forms of money? "

Does secondary market activity justify primary market flows?

Comment 2: Price impact argument for infinitesimal investors

Comment 3: cranky referee #2

censored ;-)

Comment 4: issuers optimize over #of arbitrageurs?

Comments 5: odds and ends

Comment 3: cranky referee #2

Proposition 2: "The run threshold, that is, run risk, is increasing in \(\phi\) if and only if \(g(\phi) > K\), where \(g(\phi)\) is continuous and strictly decreasing in \(\phi\) , and satisfies \(\lim_{\phi \to 0} g(\phi)>0\)."

By Andreas Park