Temporal Relational Ranking for Stock Prediction

Feng et al.

Motivation

- Most methods are either time series or cross-sectional

- Most optimized for classification or regression

Objective

- Tailor deep learning models for stock ranking

- Capture stock relations in a time-sensitive manner

Results

- New component: Temporal Graph Convolution (TGC)

-

Novel architecture: Relational Stock Ranking (RSR)

- Combine LSTM with TGC

- Jointly models temporal evolution and relation network of stocks

- Back-testing on NASDAQ and NYSE

- Beats benchmarks and SFM model

Background

Ranking as a Target

- Classification and regression may be suboptimal

- Ranking selects stocks with highest expected revenue

Ranking as a Target

- Method 2: \(\downarrow\) MSE, \(\downarrow\) profit

- Method 1: picked the biggest change,

\(\uparrow\) MSE, \(\uparrow\) profit

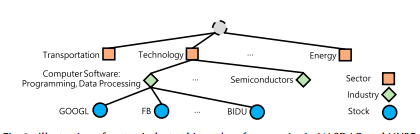

Stock Relations

- Three types of relations:

- Industry

- First Order

- Second Order

- Relations are stated as (subject; predicate; object)

Stock Relations

- Industry:

- NASDAQ and NYSE classify each stock into a sector and industry

- (GOOGL; Computer Software: Programming, Data Processing; FB)

Stock Relations

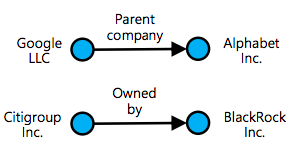

- First and Second Order:

- Data from Wikidata

- Tens of millions of objects

- Hundreds of millions of statements

- (Alphabet, Inc.; founded by; Larry Page)

Stock Relations

- First Order:

- Company \(i\) has a first order relation with \(j\) if there is a statement with \(i\) as the subject and \(j\) as the object

- (Citigroup Inc.; owned by; BlackRock Inc.)

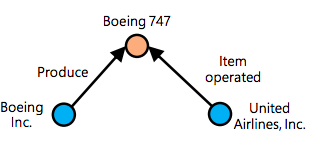

Stock Relations

- Second Order:

- Company \(i\) has a second order relation with \(j\) if they have statements sharing the same object

Stock Relations

Previous/Component Models

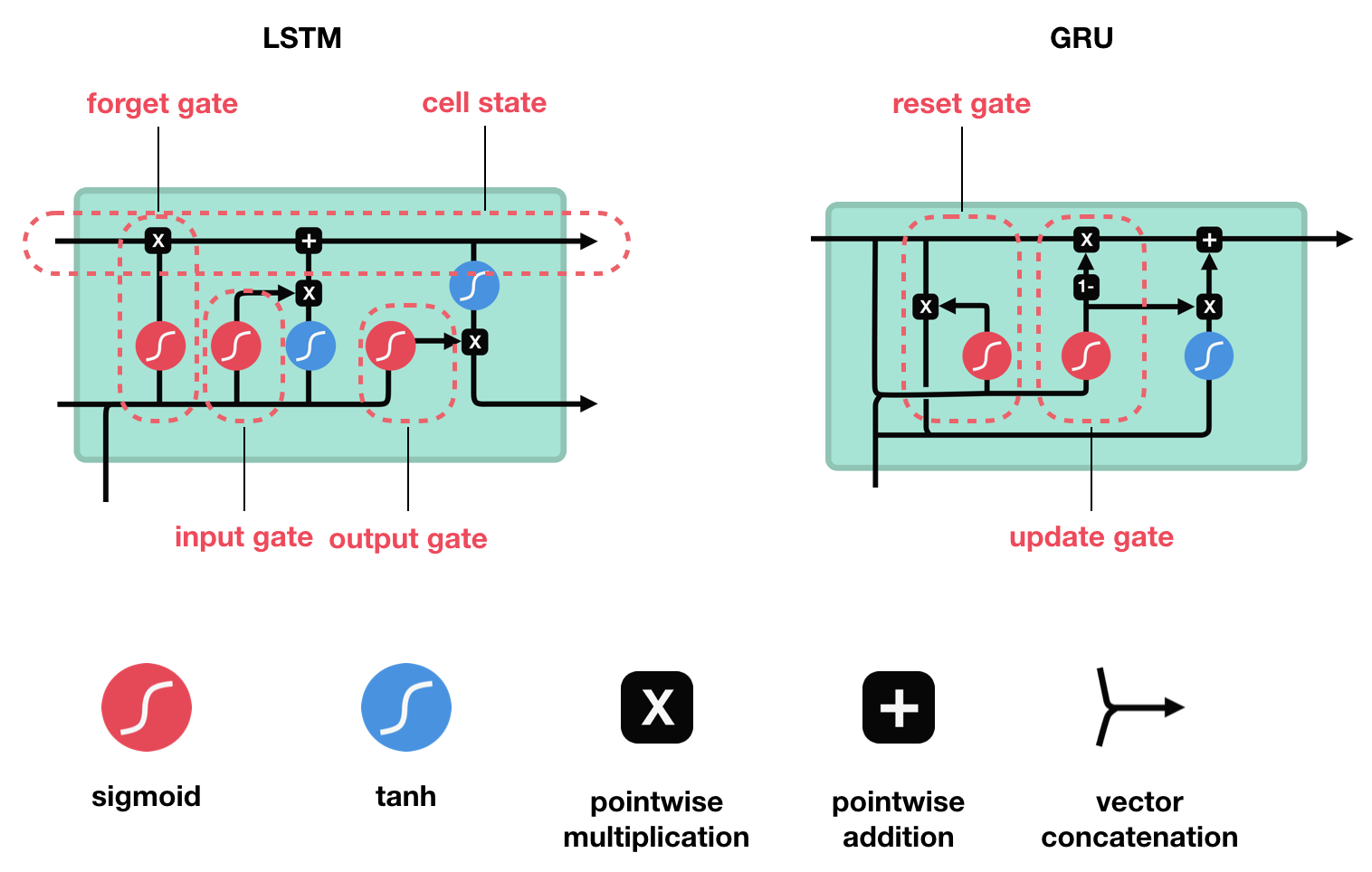

Long Short Term Memory

(LSTM)

Graph-based Learning

- Minimize objective function \(\Gamma=\Omega+\lambda\Phi\)

- \(\Omega\): task specific loss

- \(\Phi\): graph regularization term; smooths prediction over graph

\[\Phi=\sum_{i=1}^N\sum_{j=1}^N \text{strength of smoothness}_{ij}\cdot \text{smoothness}_{ij}\]

Graph-based Learning

\[\Phi=\sum_{i=1}^N\sum_{j=1}^N \text{strength of smoothness}_{ij}\cdot \text{smoothness}_{ij}\]

- Strength of smoothness= \(g(x_i,x_j)\) = similarity between feature vectors

- i.e., edge weight

Graph-based Learning

\[\Phi=\sum_{i=1}^N\sum_{j=1}^N \text{strength of smoothness}_{ij}\cdot \text{smoothness}_{ij}\]

- smoothness=\(||\frac{f(x_i)}{\sqrt{D_{ii}}} - \frac{f(x_j)}{\sqrt{D_{jj}}}||^2\)

- \(D_{ii}\): degree of node \(i\)

- Enforces that similar nodes have similar predictions

Graph Convolutional Networks

- Combine smoothness assumption with CNNs

- Cannot directly apply convolution onto adjacency matrix

- Solution: Use spectral convolutions

Graph Convolutional Networks

\[f(F,X)=UFU^TX\]

- \(f\): filtering operation of convolution

- \(F\): diagonal matrix parameterizing convolution

- \(U\): eigenvector matrix of graph Laplacian matrix \(L\)

- \(L=U\Lambda U^T=D^{-1/2}(D-A)D^{-1/2}\)

Graph Convolutional Networks

\[f(F,X)=UFU^TX\]

- Approximate equation with Chebyshev polynomials of order \(k=1\) (proven sufficient in previous work)

- Reduces to \(f(F,X)=AX\)

- Elements of A: \(A_{ij}=g(x_i,x_j)\)

- Inject convolution into a fully connected layer as \(A(XW+b)\)

New Model

Relational Stock Ranking

- Input:

- \(X^t=[x^{t-S+1},\dots,x^t]^T\in \R^{S\times D}\)

- sequential input features of a specific stock

- sequence length \(S\); \(D\) features

- \(\mathcal X^t\in \R^{N\times S\times D}\)

- collected sequential features of all \(N\) stocks

- Target: \(\hat r^{t+1}=f(\mathcal X^t)\)

- ranking-aware 1-day return

Relational Stock Ranking

- Relations of two stocks:

- \(K\) types of relations

- Encode pairwise relation between two stocks as a multi-hot binary vector \(a_{ij}\in \R^k\)

- Relation of all stocks:

- \(\mathcal A \in \R^{N\times N\times K}\)

- \(i\)-th row, \(j\)-th column is \(a_{ij}\)

Relational Stock Ranking

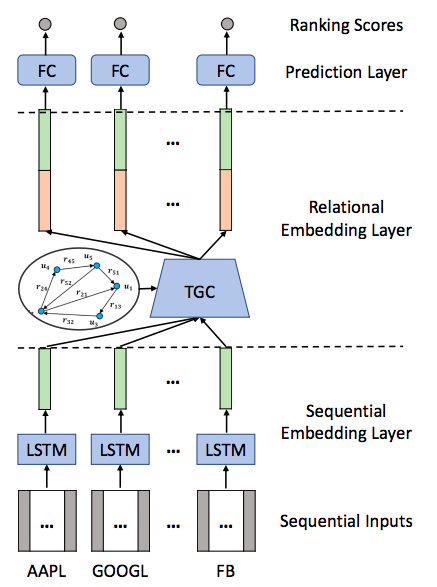

- Three Layers:

- Sequential Embedding Layer

- Relational Embedding Layer

- Prediction Layer

Relational Stock Ranking

Sequential Embedding Layer

- Intuitive to first regard the historical status of a stock

- First apply a sequential embedding layer

- Choose LSTM since captures long-term dependency

- ex: interest rates

Sequential Embedding Layer

- Take last hidden state \(h_i^t\)

- Set it as sequential embedding \(e_i^t=h_i^t\)

- \(E^t=LSTM(\mathcal X^t)=[e_1^t,\dots,e_N^t]^T\in \R^{N\times U}\)

- \(U\): number of hidden units in LSTM

Relational Embedding Layer

- New component of neural network modeling: Temporal Graph Convolution

- Generates relational embeddings \(\bar E^t\in \R^{N\times U}\)

- These are time-sensitive (dynamic)

- Key technical contribution of this work

- We will build up the model intuitively

Relational Embedding Layer

- Uniform Embedding Propagation

- From link analysis

\[\overline{e_i^t} = \sum_{\{j|sum(a_ji)>0\}} \frac{1}{d_j}e_j^t\]

- Only stocks that have at least one relation are used

- \(d_j\): number of stocks satisfying the condition

Relational Embedding Layer

2. Weighted Embedding Propagation

- Different relations may have different impacts

\[\overline{e_i^t} = \sum_{\{j|sum(a_ji)>0\}} \frac{g(a_{ji})}{d_j}e_j^t\]

- g: Relation-strength function

- Aims to learn impact strength of relations in \(a_{ji}\)

Relational Embedding Layer

3. Time-aware Embedding Propagation

- Relation-strength may evolve over time

\[\overline{e_i^t} = \sum_{\{j|sum(a_ji)>0\}} \frac{g(a_{ji},e_i^t,e_j^t)}{d_j}e_j^t\]

- Includes temporal and stock information

Relational Embedding Layer

- Two designs of \(g\):

- Explicit modeling

- Implicit modeling

Relational Embedding Layer

- Explicit modeling:

g(a_{ji},e_i^t,e_j^t)=e_i^{t^T}e_j^t\times \phi(w^Ta_{ji}+b)

similarity

relation importance

- \(w\in\R^K,b\): model parameters to be learned

- \(\phi\): leaky rectifier activation function

Relational Embedding Layer

- Implicit modeling:

g(a_{ji},e_i^t,e_j^t)=\phi(w^T[e_i^{t^T},e_j^{t^T},a_{ji}^T]^T+b)

- \(w\in\R^{2U+K},b\): learned

- Learn both similarity and relation importance

- \(g\) is then normalized through a softmax function

Relational Embedding Layer

- Connection with graph-based learning:

- Embedding propagation equivalent to GCN at time \(t\)

- Proof omitted

- GCN must have fixed adjacency matrix

Prediction Layer

- Feed both sequential embeddings and revised relational embeddings into a fully connected layer to predict rank-aware returns

Prediction Layer

- Proposed objective function:

l(\hat r^{t+1},r^{t+1})=||\hat r^{t+1}-r^{t+1}||^2+\alpha \sum_{i=0}^N\sum_{j=0}^N \max\{0,-(\hat r_i^{t+1}-\hat r_j^{t+1})(r_i^{t+1}-r_j^{t+1})\}

- First term: SSE

- punishes difference between ground-truth and prediction

- Second term: pair-wise max-margin loss

- Encourages predicted ranking scores of stock pair to have the same relative order as ground-truth

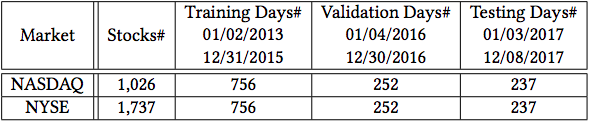

Data

Sequential Data

- Source: Google Finance

- Historical price data from NASDAQ and NYSE

- NASDAQ more volatile, NYSE more stable

- Filter stocks:

- Traded on at least 98% of days

- Never been traded less than $5.00

Historical Price Data

Historical Price Data

- \(p_i^t\): closing price of stock \(i\) on day \(t\)

- Normalized by max price of stock \(i\)

- Ground truth: \(r_i^{t+1}=(p_i^{t+1}-p_i^t)/p_i^t\)

- Calculate 5, 10, 20, 30 day moving averages of returns

Stock Relation Data

- Sector-industry relations: NASDAQ and NYSE

- Company-based relations: Wikidata

Experiment

Three Metrics:

- Mean Squared Error (MSE)

- Want smaller value of MSE (\(\geq 0\))

- Mean Reciprocal Rank (MRR)

- Take average of reciprocal rank of selected stock

- Want larger value of MRR (\([0,1]\))

- Cumulative Investment Return Ratio (IRR)

- Want larger value of IRR

Experimental Setting

- Market close on day \(t\): predict a ranking list and buy the highest ranked stock

- Market close on day \(t+1\): sell the stock

Experimental Setting

Assumptions:

- Same amount of money spent every day

- Market liquid enough to buy stock at the closing price on day \(t\)

- Liquid enough to sell at closing price on day \(t+1\)

- Transaction costs ignored

Methods

- SFM: Fourier signal deep learning

- LSTM: regression target

- Rank_LSTM: rank target

- GBR: add graph regularization term to Rank_LSTM

- GCN: static graph convolution

- RSR_E: explicitly modeled RSR

- RSR_I: implicitly modeled RSR

Methods

- Grid search validation

- Adam optimizer, learning rate 0.001

Three Research Questions

- How does ranking compare to classification or regression? Can RSR outperform SOTA solutions?

- Do stock relations enhance the neural network-based solution? Does TGC outperform GBR or GCN?

- How does our proposed RSR solution perform under different back testing strategies?

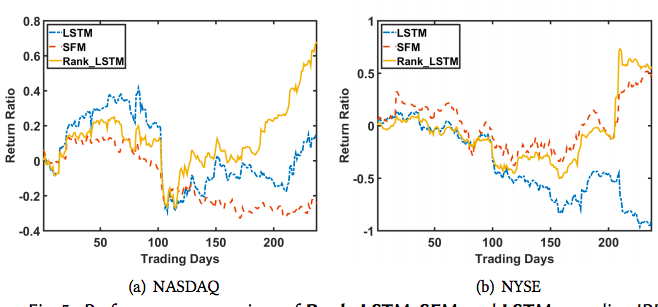

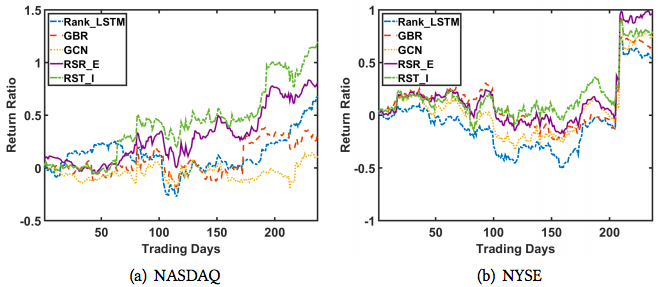

Q1: Rank

- Rank_LSTM outperforms SFM and LSTM in IRR

- Fails to beat in all metrics

- Could be because there is a tradeoff between accurately predicting value and order

- High variance

- Picking one stock volatile

-

LSTM performs unexpectedly bad on the NYSE

- Can do better with different parameters (snooping)

Q1: Rank

Q1: Rank

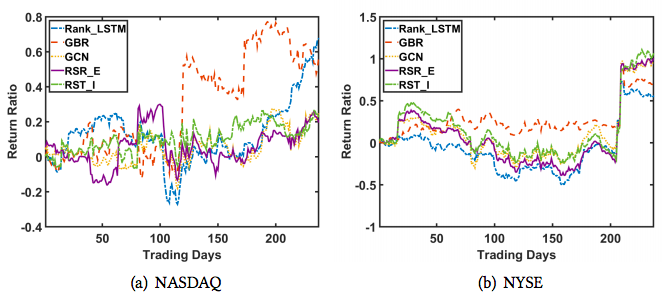

Q2: Relations: Industry

- Industry relations more valuable on NYSE than NASDAQ

- NYSE less volatile, industry relations are long-term

- On NYSE, all relational methods outperform Rank_LSTM

- On NYSE, RSR_E and RSR_I are top two methods

- Performance across metrics again inconsistent

- On NYSE, much of gains achieved on days 206 and 209

- Importance of accurately doing rank and size

Q2: Relations: Industry

Q2: Relations: Industry

Q2: Relations: Wiki

-

RSR_E and RSR_I achieve best IRR performance

- Especially on NYSE

Q2: Relations: Wiki

Q2: Relations: Wiki

Q2: Relations: Sector-wise

- Is the performance sensitive to sectors?

- Back-tested each sector separately on NASDAQ

- Only technology produced an acceptable IRR

Q2: Relations: Types of Wiki

- Compared performance when a type of relation was removed

- Top 5 factors:

- Product or material produced

- Member of

- Industry

- Part of

- Product or material produced; Industry

Q2: Relations: Types of Wiki

Q2: Brief Conclusion

- Considering stock relations helpful for stock ranking, especially on stable markets

- Proposed TGC is promising model for stock relations

- Important to consider appropriate relations suitable for the target market

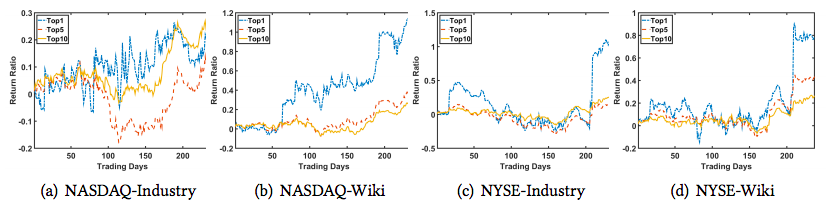

Q3: Strategy

- Three strategies: Top1, Top5, Top10

- Equally split budget among stocks

-

Top1>Top5>Top10

- If ranking algorithm good, then should put all money on stock with highest expected return

- RSR_I continues to do poorly in NASDAQ-Industry

Q3: Strategy

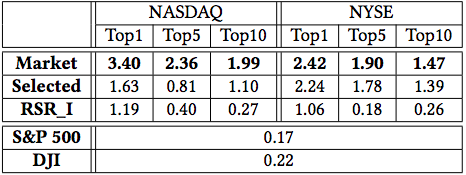

Q3: Strategy: Comparison to Benchmarks

- Compare strategy to S&P 500 and DJIA

- Also formulate two ideal versions of strategies:

- Market: select stocks with highest return ratio from the whole market

- Selected: select stocks with highest return ratio from the set of stocks traded by RSR_I

Q3: Strategy: Comparison to Benchmarks

Conclusion

- Demonstrated potential of learning-to-rank methods

- Proposed RSR framework with novel TGC component

- Outperforms indicies and SOTA methods

Future Work

- Explore more advanced learning-to-rank techniques

- Integrate risk management

- Investigate other strategies

- buy-hold-sell (long)

- borrow-sell-buy (short)

- Integrate alternative data

- News/social media

- Explore TGC in other fields

Analysis

- Trading strategy seems unlikely

- No reports on statistical significance

- Not sure why prices were normalized if in return space

- Would like to see sector relations as well

- Would like to see all types of relations at once

- Everything available on github

Temporal Relational Ranking

By Connor Chapin

Temporal Relational Ranking

Presentation on "Efficient Estimation of Word Representations in Vector Space"