Content ITV PRO

This is Itvedant Content department

Learning Outcome

5

Analyse which bond is suitable for different investors.

4

Understand the role of credit ratings and regulations.

3

Compare bonds based on risk, return, and liquidity.

2

Identify the key features of both types of bonds.

1

Understand the meaning of government and corporate bonds.

What is a Government Bond?

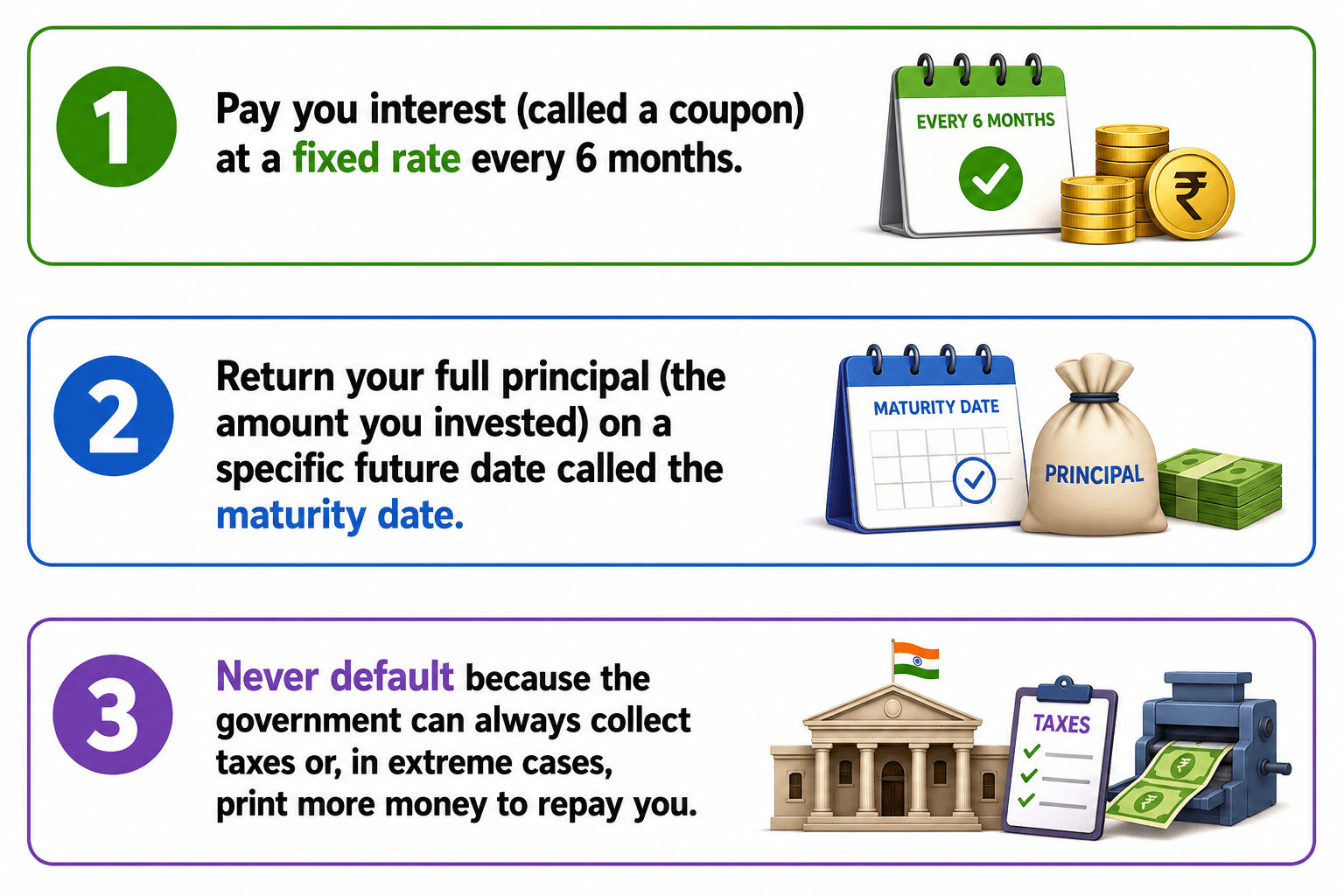

A Government Bond is a loan you give to the Government of India (or a state government). In exchange, the government promises to:

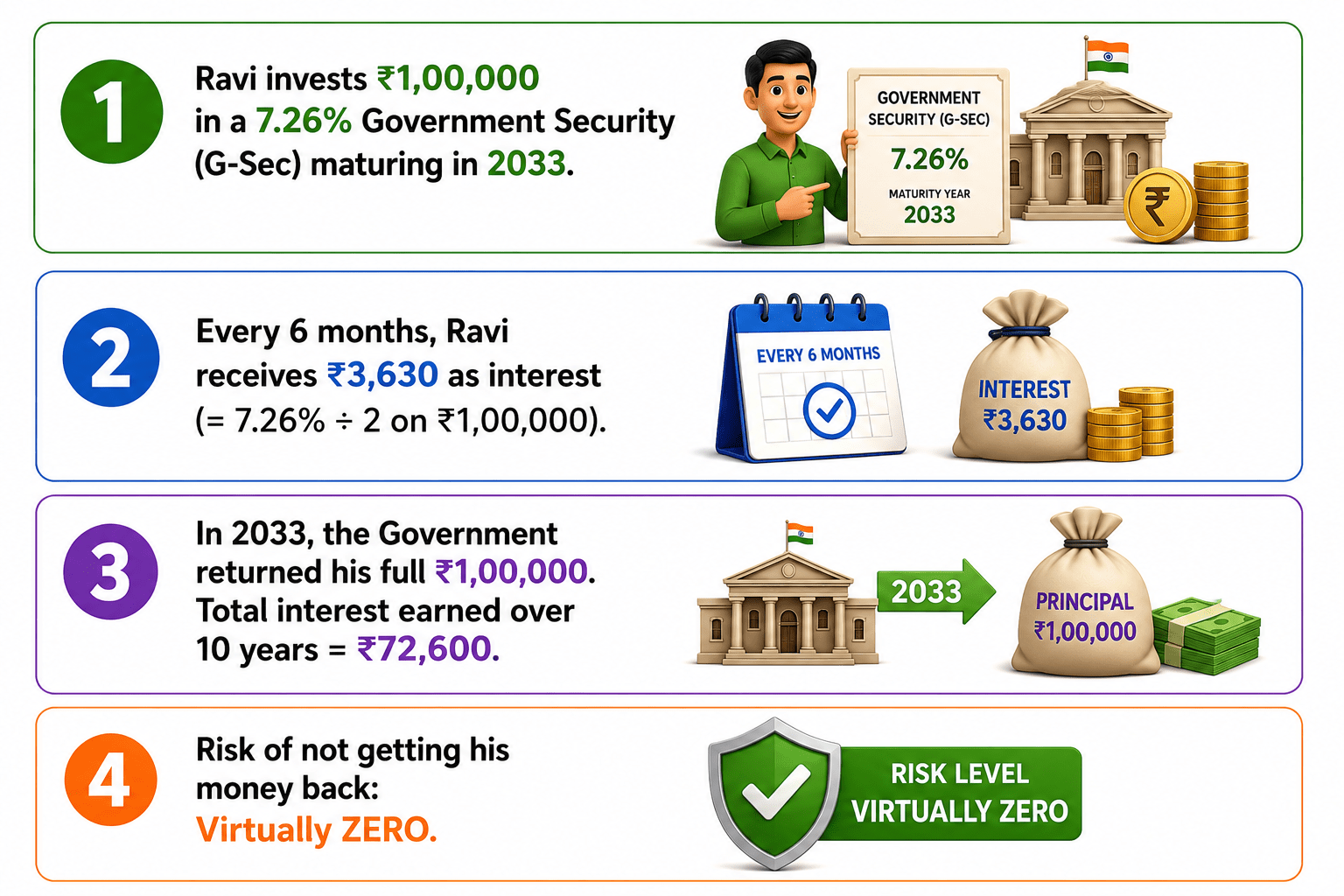

Eg- Ravi invests ₹1,00,000 in a 7.26% Government Security (G-Sec) maturing in 2033.

Every 6 months, Ravi receives ₹3,630 as interest

(= 7.26% ÷ 2 on ₹1,00,000).

In 2033, the Government returned his full ₹1,00,000. Total interest earned over 10 years = ₹72,600.

Risk of not getting his money back: Virtually ZERO.

Types of Government Bonds in India

1. G-Secs (Government Securities)- Long-term bonds issued by the Central Government. The most common type. Maturities from 5 to 40 years. Pays interest twice a year.

2. T-Bills (Treasury Bills)- Short-term borrowing by the government. Lasts only 91, 182, or 364 days. No interest payments — you buy at a discount and get full face value back. Example: Buy at ₹97,000, get ₹1,00,000 back in 91 days.

3. State Dev. Loans (SDLs) - Same as G-Secs but issued by state governments (Maharashtra, Gujarat, etc.) instead of the Central Government. Slightly higher interest than G-Secs.

4. Inflation-Linked Bonds- Special bonds where your interest and principal grow with inflation. Protects your purchasing power. Ideal for long-term investors worried about rising prices.

5. RBI Floating Rate Bonds- Interest rate changes every 6 months based on small savings rates. Good when interest rates are rising.

6. Sovereign Green Bonds- Government bonds where money is used only for green/environment projects like solar energy or clean water. Launched in India in 2023.

What is a Corporate Bond?

A Corporate Bond is a loan you give to a company. In exchange, the company promises to:

Pay you interest (coupon) at a fixed rate usually higher than a government bond.

Return your principal at the maturity date.

But here’s the key difference, the company may fail. If it goes bankrupt, you may lose some or all of your money.

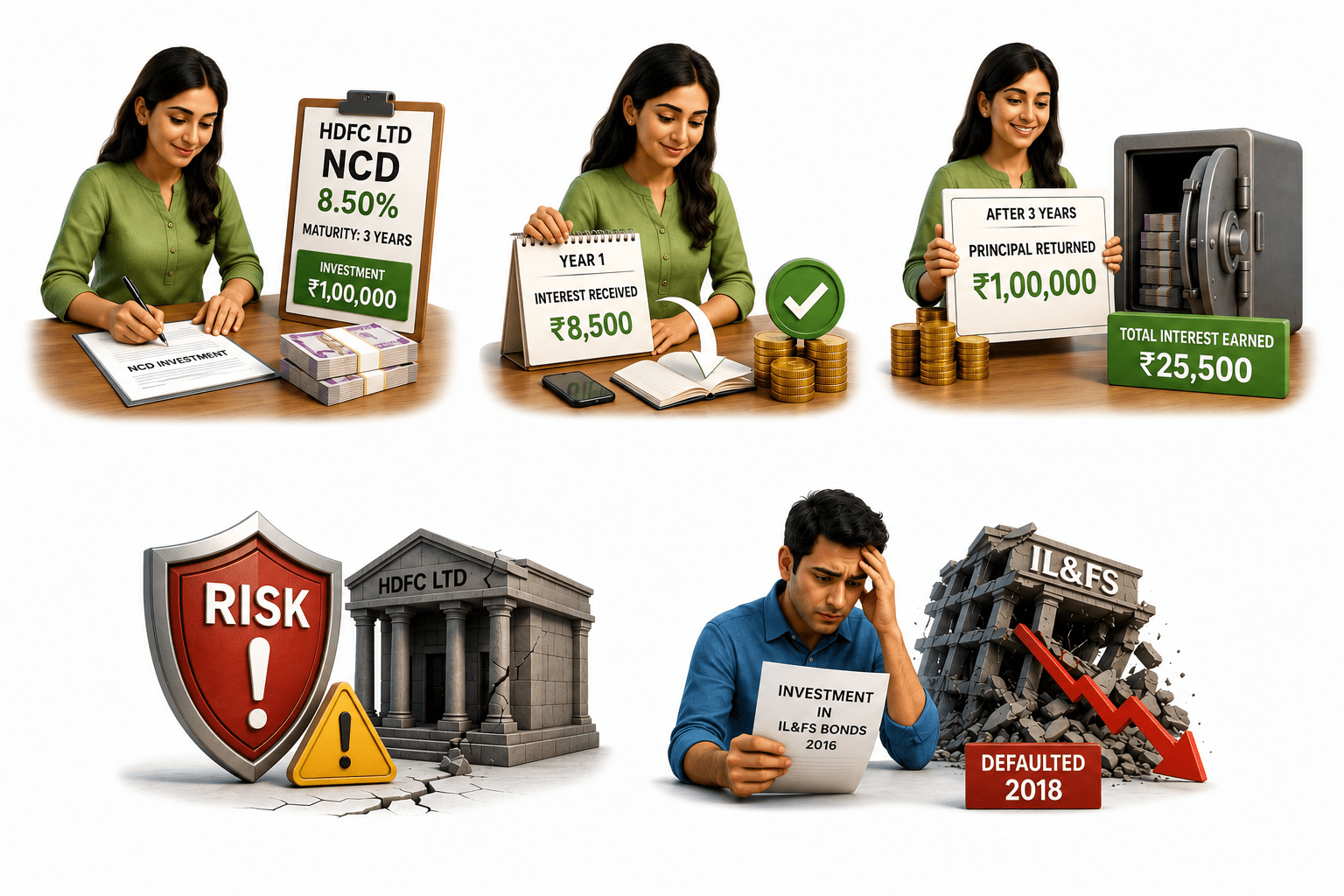

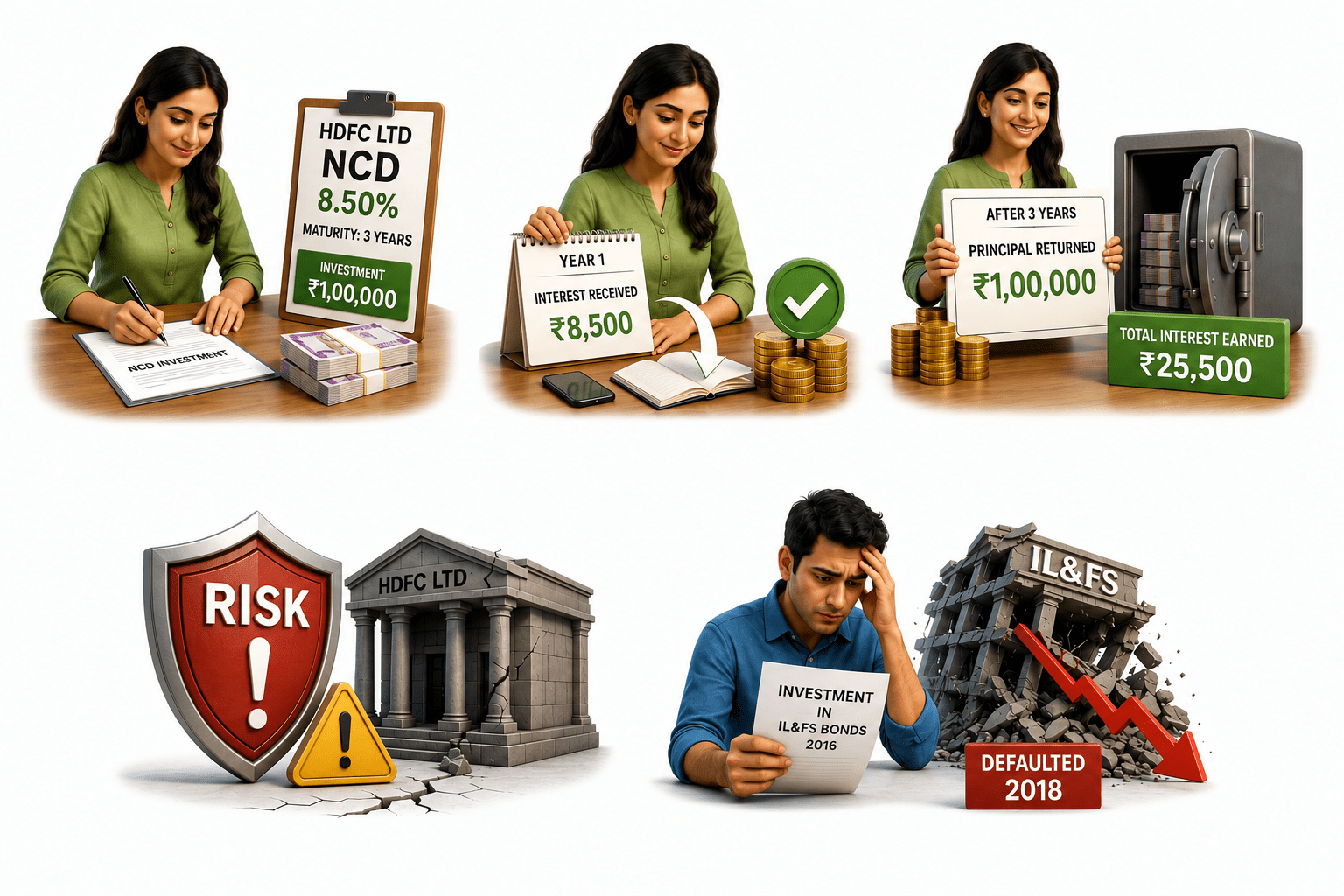

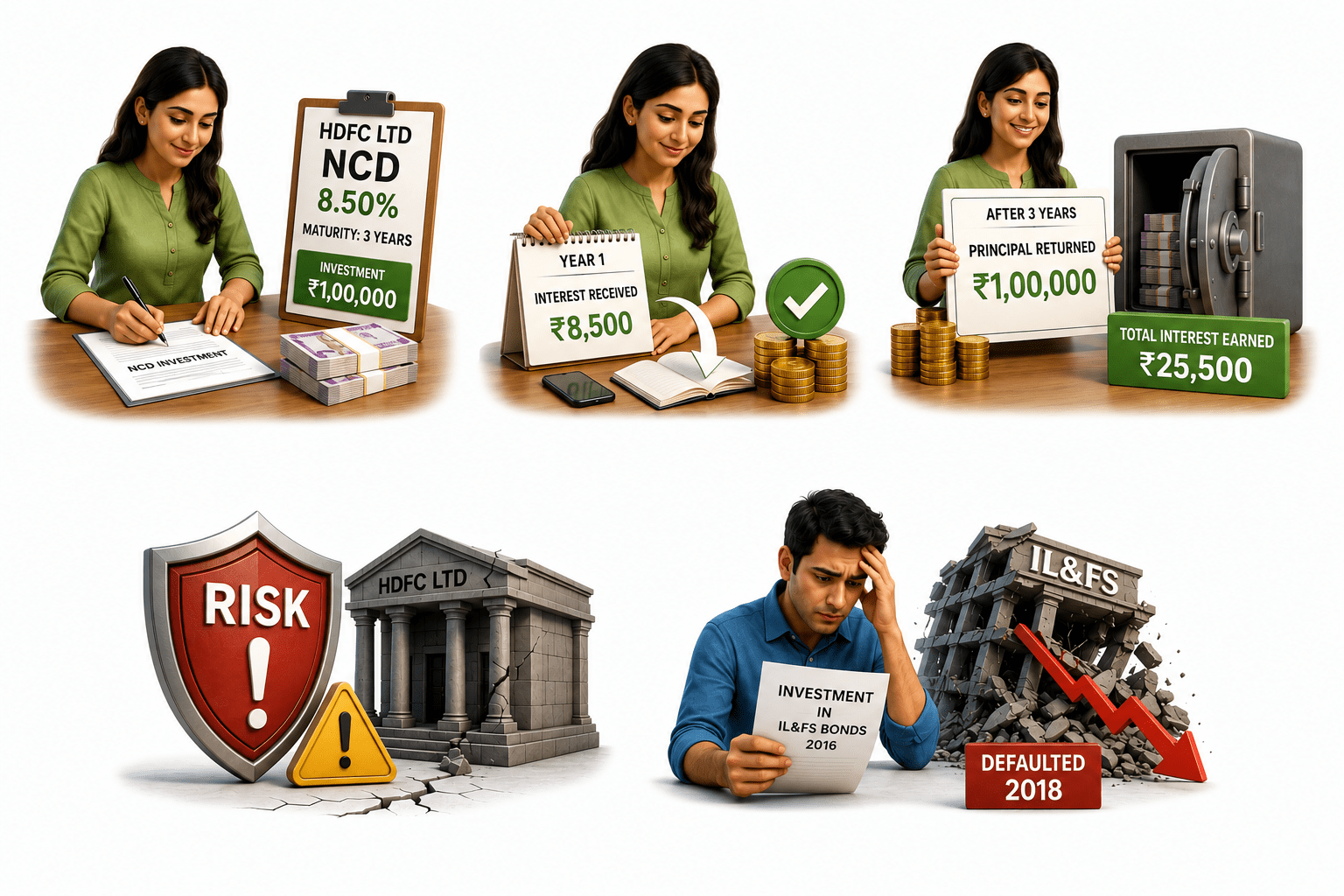

Example: Priya invests ₹1,00,000 in an HDFC Ltd NCD (Non-Convertible Debenture) at 8.50%, maturing in 3 years.

Every year, Priya receives ₹8,500 as interest.

By 2018, IL&FS defaulted and Amit lost a significant portion of his investment.

A reminder that even AA-rated corporate bonds can fail.

Risk: If HDFC Ltd faces financial trouble (very unlikely for AAA-rated), her principal could be at risk.

Counter-Example: Amit invests in IL&FS bonds rated AA in 2016.

In 3 years, HDFC Ltd returns her full ₹1,00,000.

Total interest earned = ₹25,500.

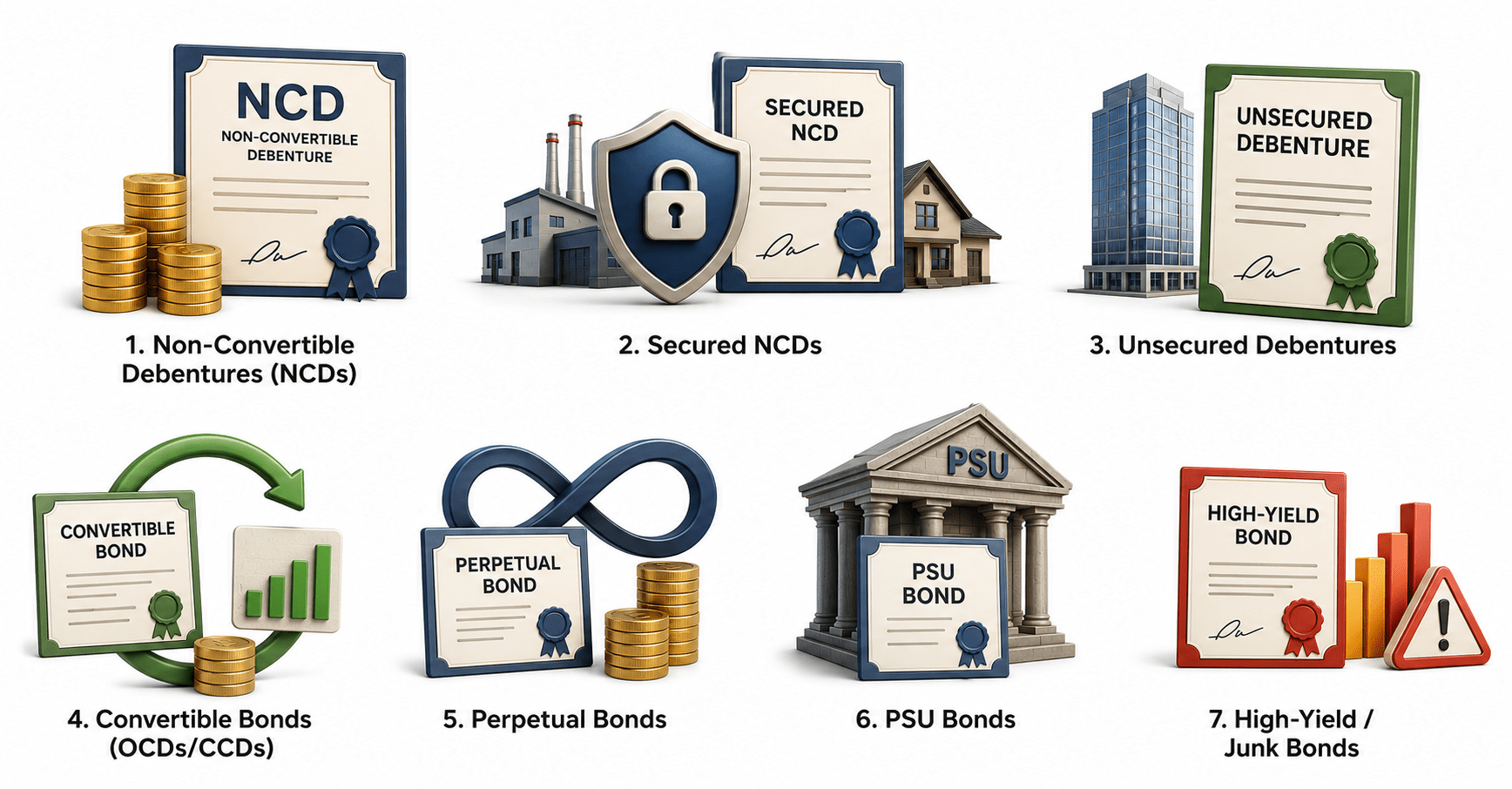

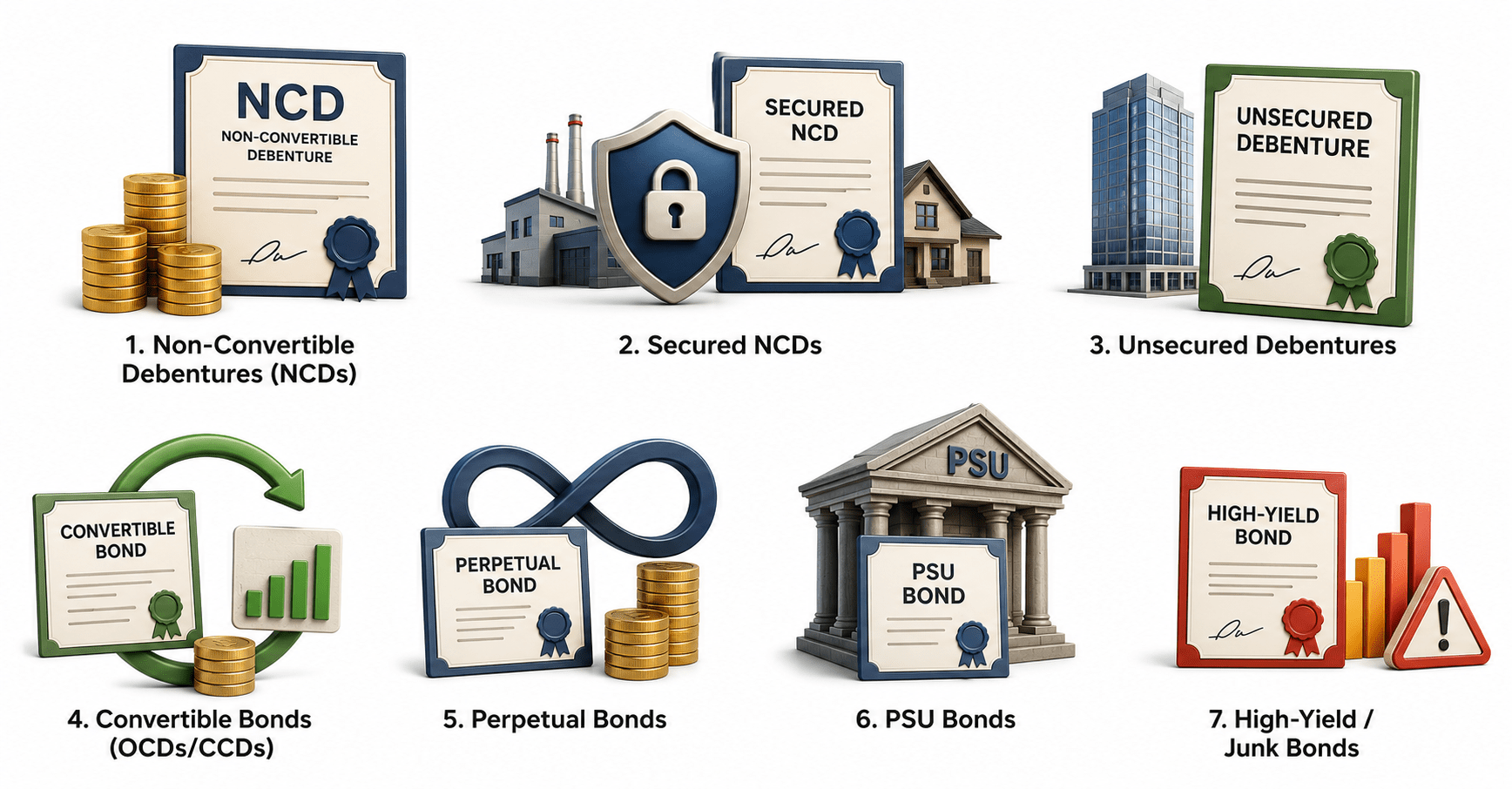

Types of Corporate Bonds

1. Non-Convertible Debentures (NCDs)- The most common corporate bond in India. Simply put — you lend to a company, it pays interest, returns your money. Cannot be converted to shares. Can be secured (backed by assets) or unsecured.

2. Secured NCDs- The company pledges specific assets (property, plant) as collateral. If it defaults, these assets are sold to repay you first. Safer than unsecured.

3. Unsecured Debentures- No collateral. You rely purely on the company’s ability to repay. Higher yield to compensate for higher risk.

Types of Corporate Bonds

7. High-Yield / Junk Bonds- Issued by companies with low credit ratings (BB or below). Very high interest (12–16%+) but very high risk of default. Not for ordinary investors.

6. PSU Bonds- Bonds issued by government-owned companies like NTPC, IRFC, NHAI. Safer than private corporate bonds because the government is the ultimate owner.

5. Perpetual Bonds- Issued by banks. No fixed maturity — the bank pays you interest forever (in theory). Very high risk — can be written to zero if the bank faces a crisis. Eg: Yes Bank AT1 bonds written down in 2020.

4. Convertible Bonds (OCDs/CCDs)- These bonds can be converted into equity shares later. You start as a lender and may become a shareholder. Attractive in growing companies.

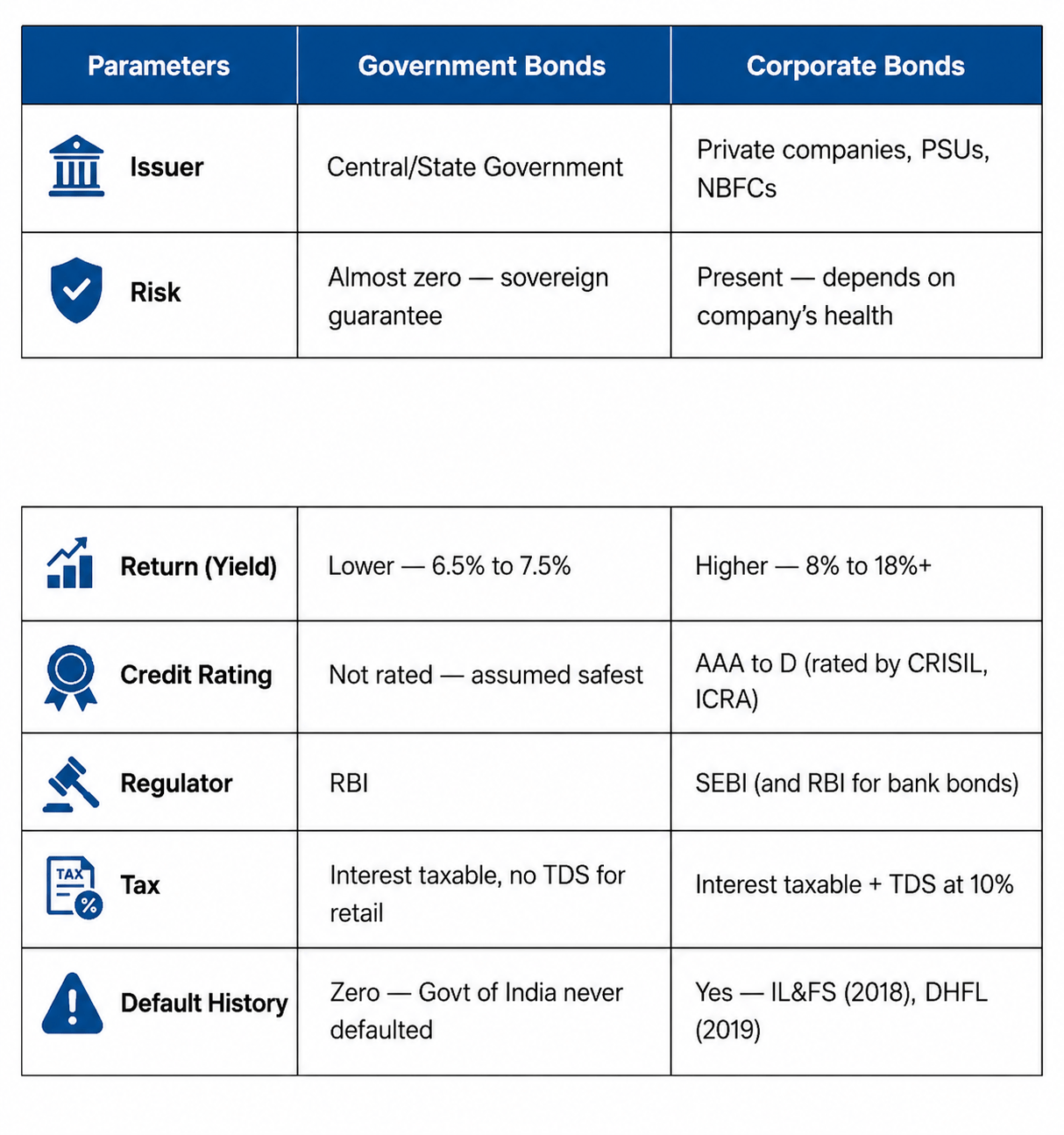

Government Bonds vs. Corporate Bonds

Summary

5

Bonds help in risk diversification.

4

Different bonds serve different investment needs.

3

Government bonds are safer than corporate bonds.

2

Bond prices and interest rates move inversely.

1

Bonds are fixed-income instruments representing loans.

Quiz

Which bond is generally safer?

A. Corporate Bond

B. Government Bond

C. Debenture

D. Commercial Paper

Quiz-Answer

Which bond is generally safer?

A. Corporate Bond

B. Government Bond

C. Debenture

D. Commercial Paper

By Content ITV