Economic Data Sciences PRO

Understandable A.I.

Understandable Artificial Intelligence

Evaluating Existing Fund

©2018 Economic Data Sciences

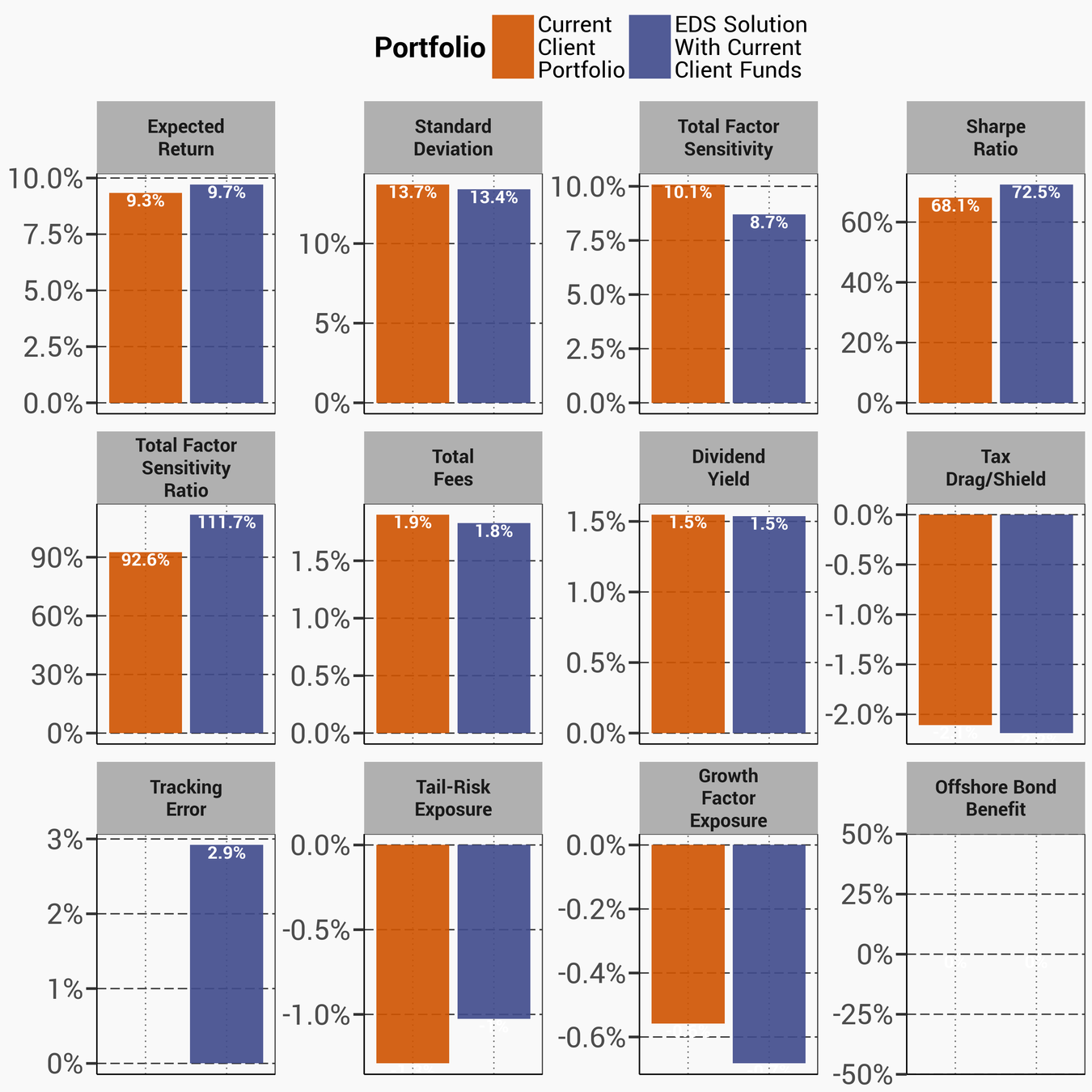

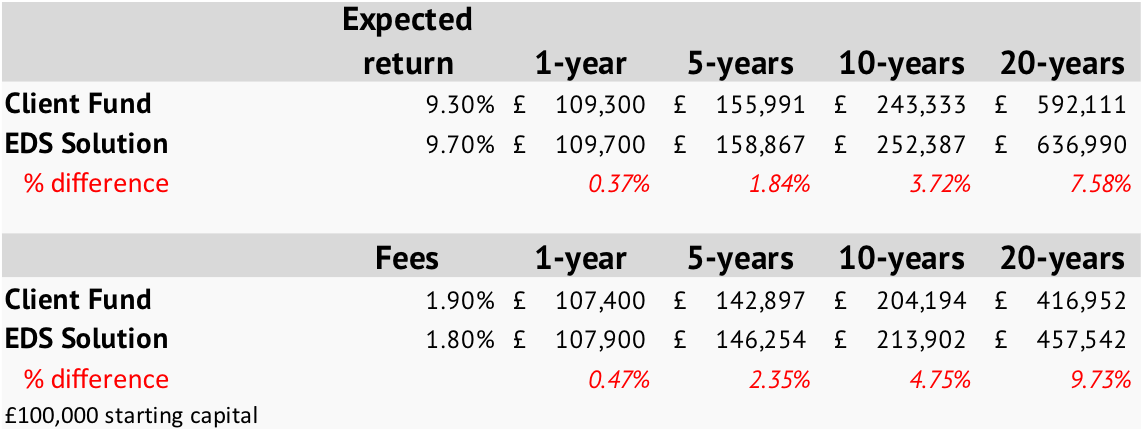

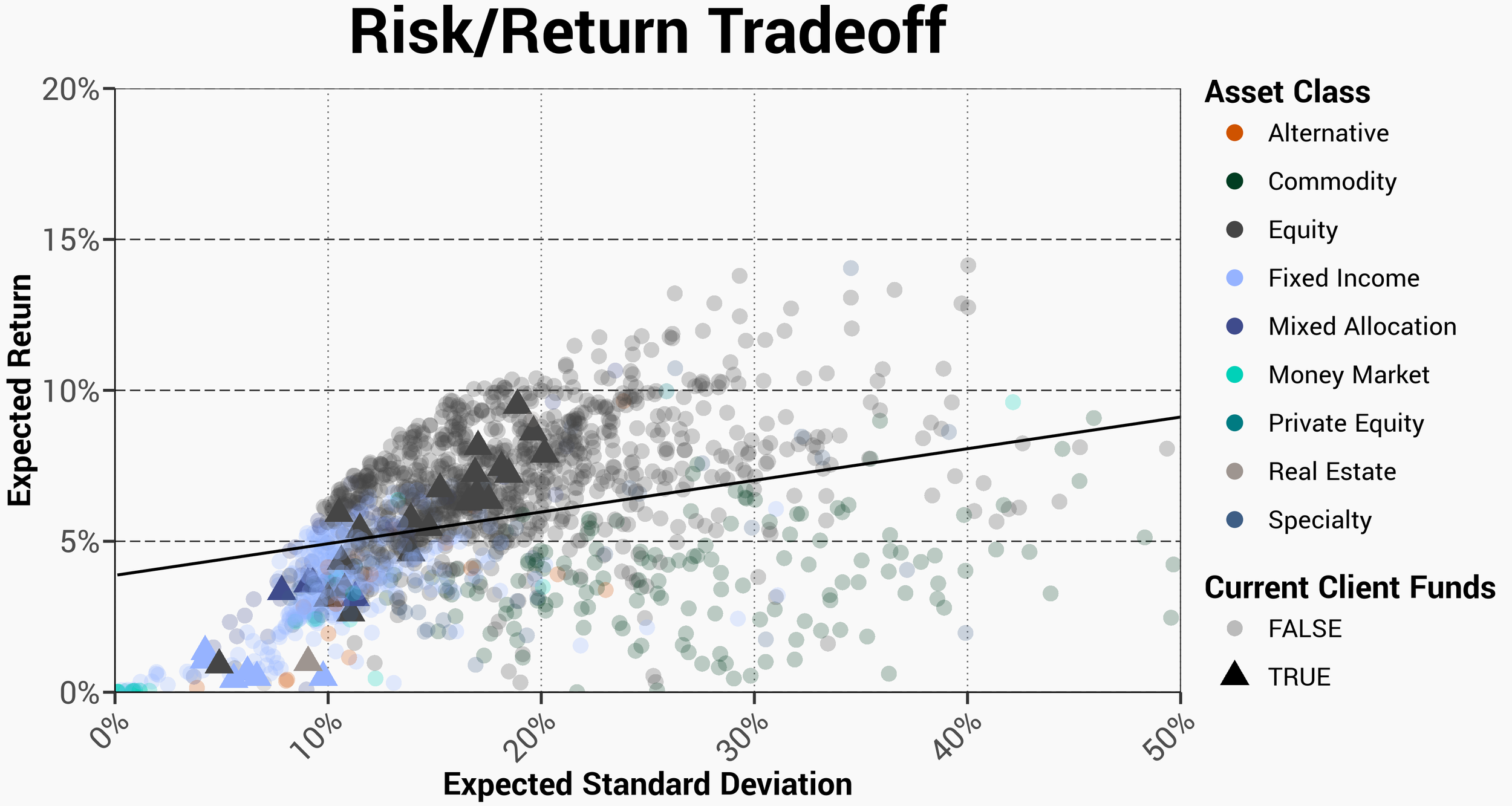

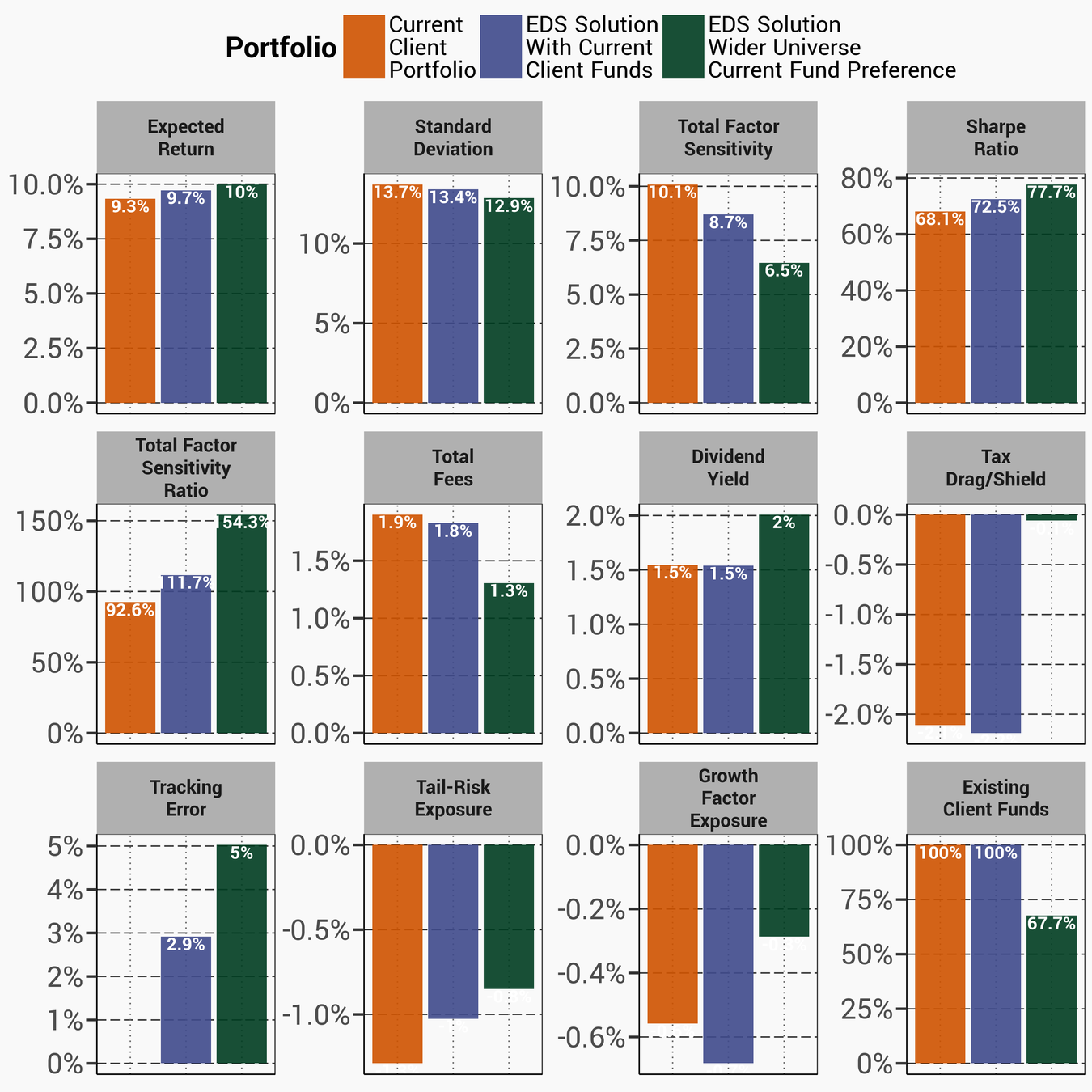

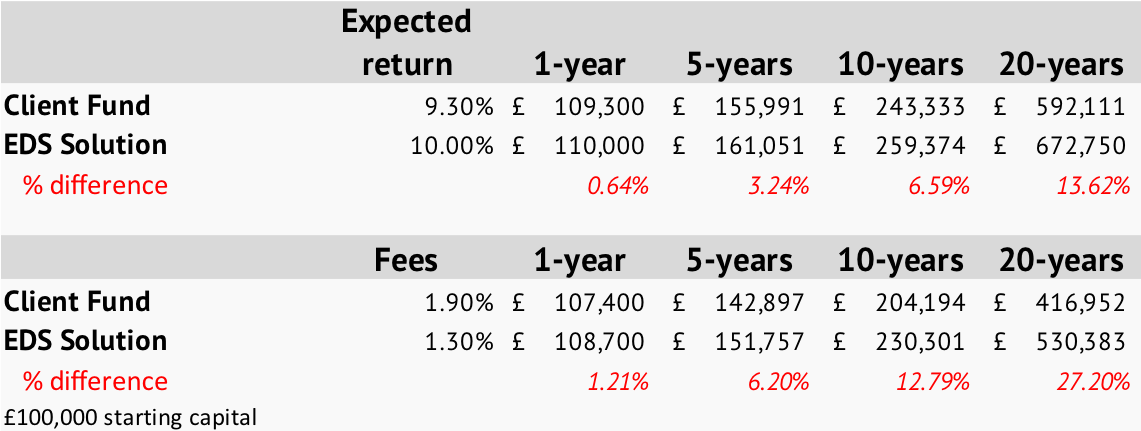

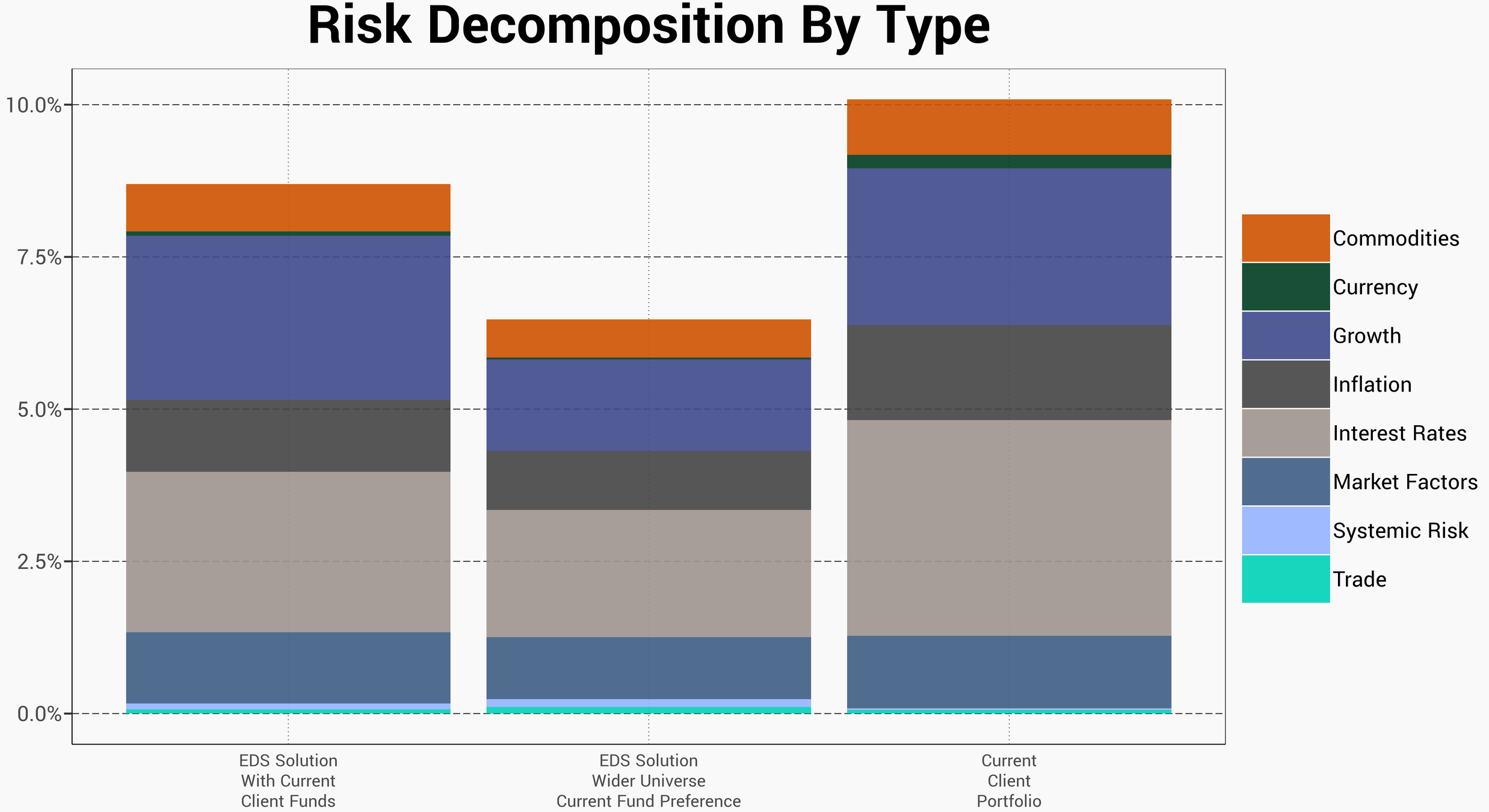

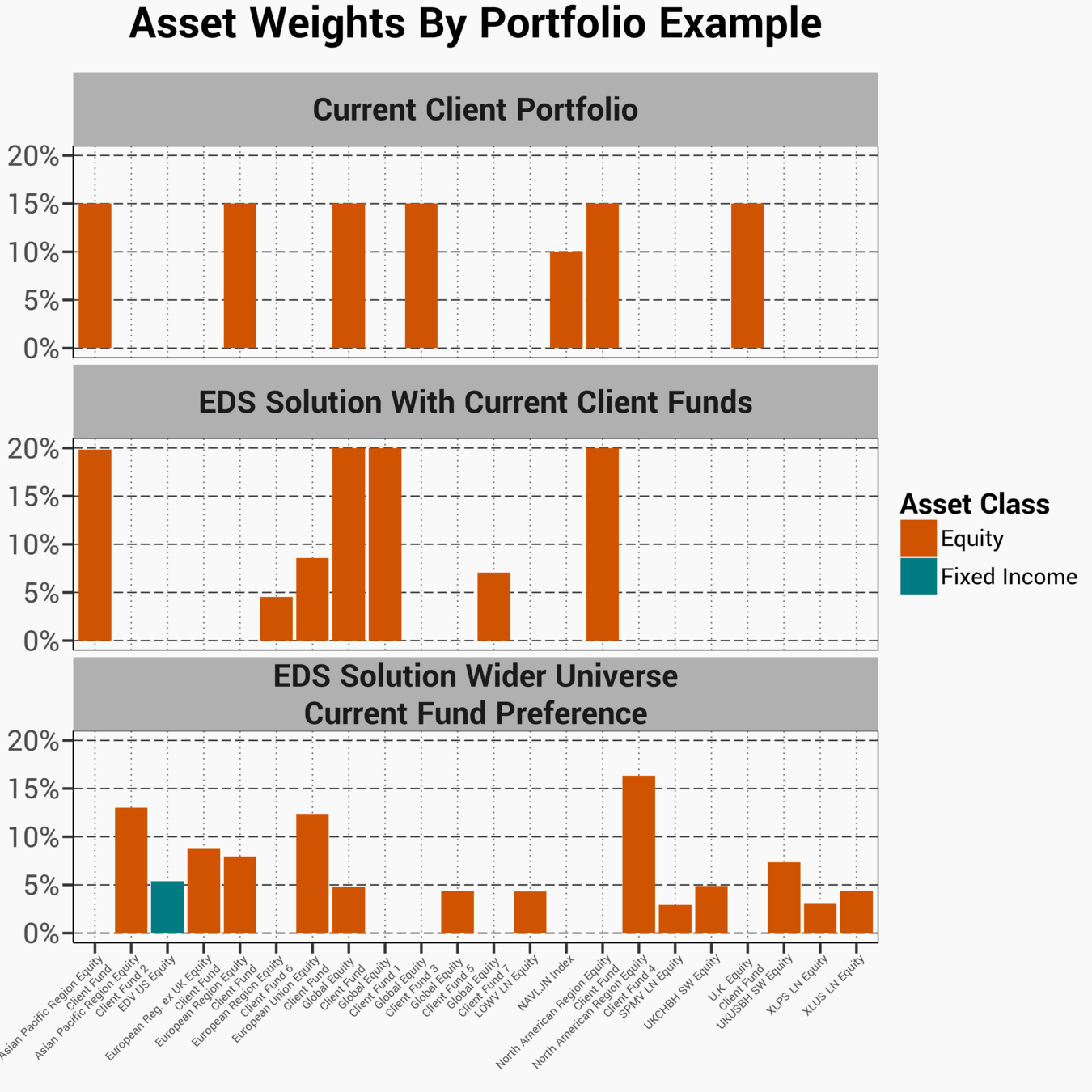

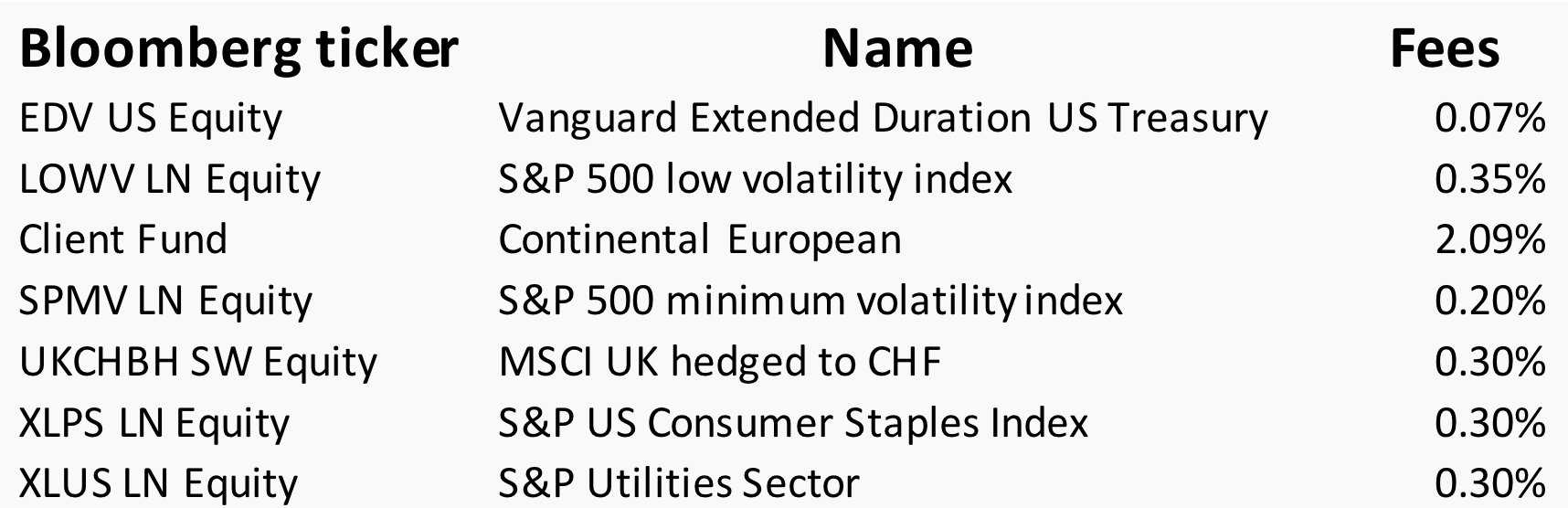

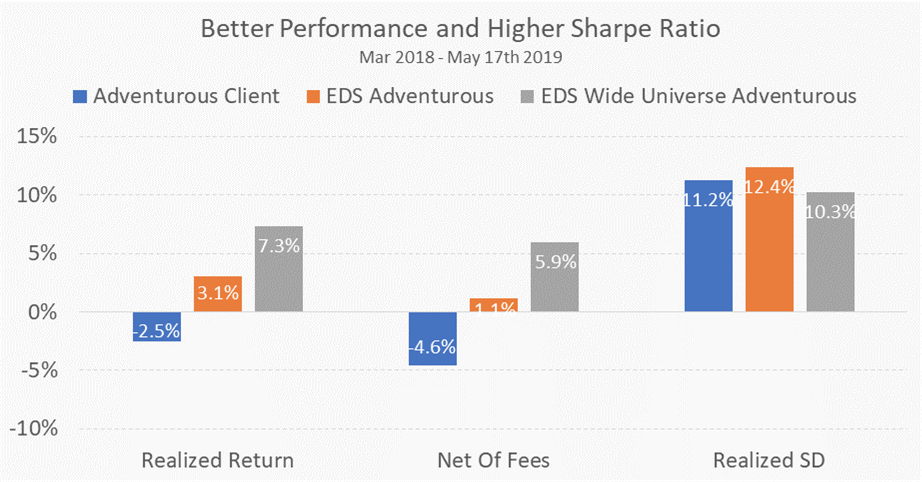

EDS was given a sample portfolio by a UK pension fund. Since only the asset weights were known, EDS tool deducted the investors' preferences and proceeded to analyze the holdings

The analysis was split into 3 stages:

©2018 Economic Data Sciences

*Data from EDS, St. James's Place, & Bloomberg, courtesy of London Business School

©2018 Economic Data Sciences

©2018 Economic Data Sciences

*Data from EDS, St. James's Place, & Bloomberg, courtesy of London Business School

©2018 Economic Data Sciences

©2018 Economic Data Sciences

*Data from EDS, & Bloomberg, courtesy of London Business School

©2018 Economic Data Sciences

©2018 Economic Data Sciences

©2018 Economic Data Sciences

©2018 Economic Data Sciences

*Data from EDS, St. James's Place, & Bloomberg, courtesy of London Business School

©2018 Economic Data Sciences

*Data from EDS, St. James's Place, & Bloomberg, courtesy of London Business School

©2018 Economic Data Sciences

*Data from EDS, St. James's Place, & Bloomberg, courtesy of London Business School

©2018 Economic Data Sciences

©2018 Economic Data Sciences

©2018 Economic Data Sciences

info@EconomicDataSciences.com

©2018 Economic Data Sciences

©2018 Economic Data Sciences

©2018 Economic Data Sciences

©2018 Economic Data Sciences

info@EconomicDataSciences.com

info@EconomicDataSciences.com

By Economic Data Sciences