Katya Malinova PRO

I am an Associate Professor, Mackenzie Investments Chair in Evidence-Based Investment Management at the DeGroote School of Business, McMaster University, Canada.

Systematic volume spikes and intraday liquidity patterns:

Fingerprints of HFT activity?

Discussion by Katya Malinova

Will J. Armstrong, Laura Cardella, and Nasim Sabah

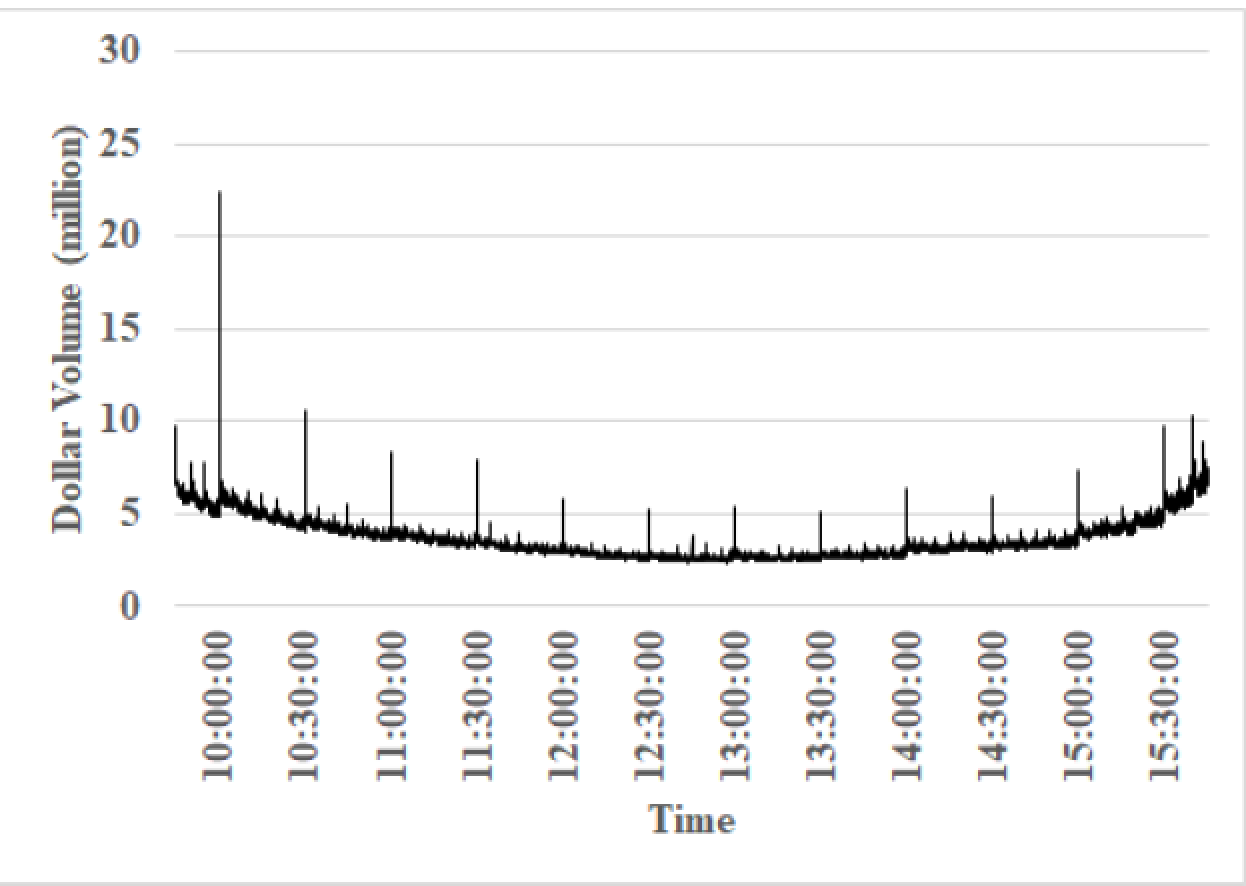

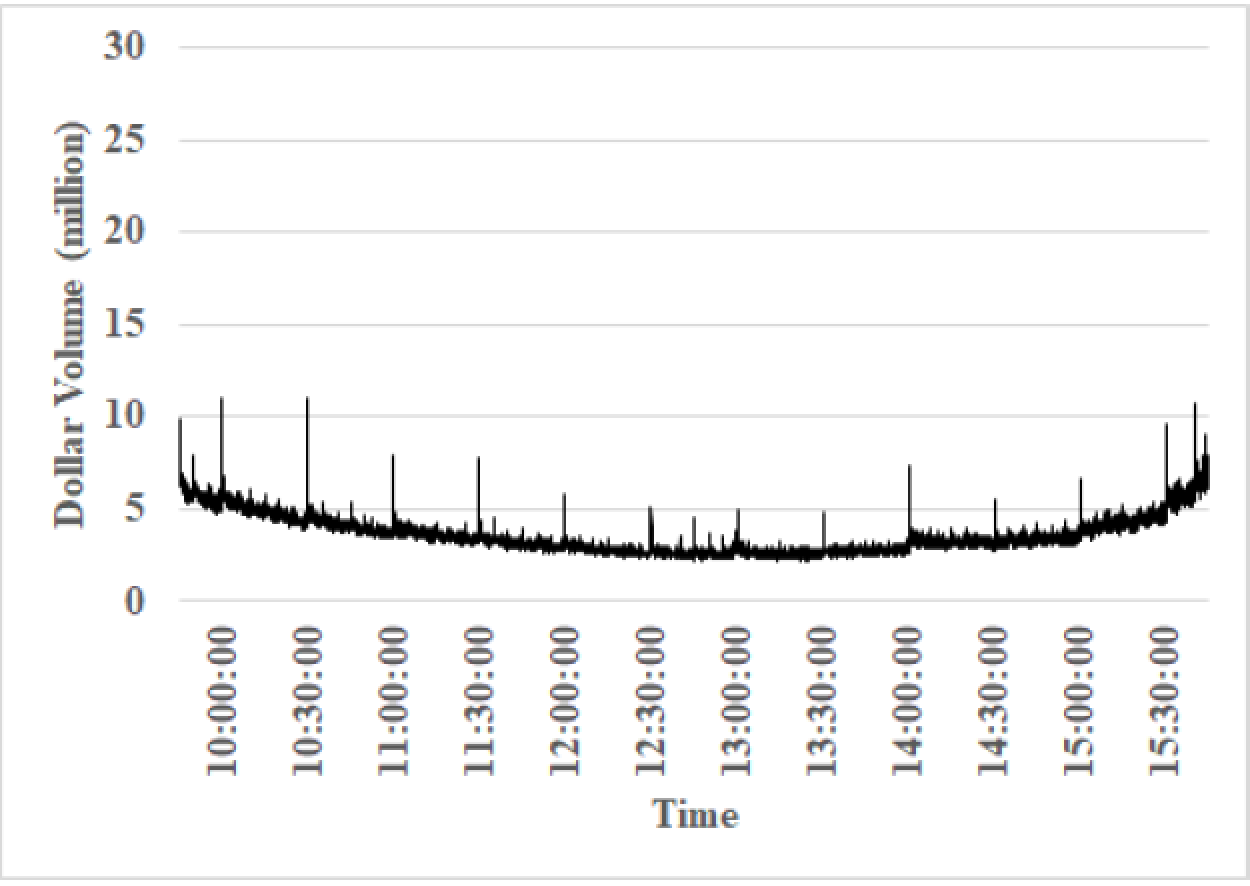

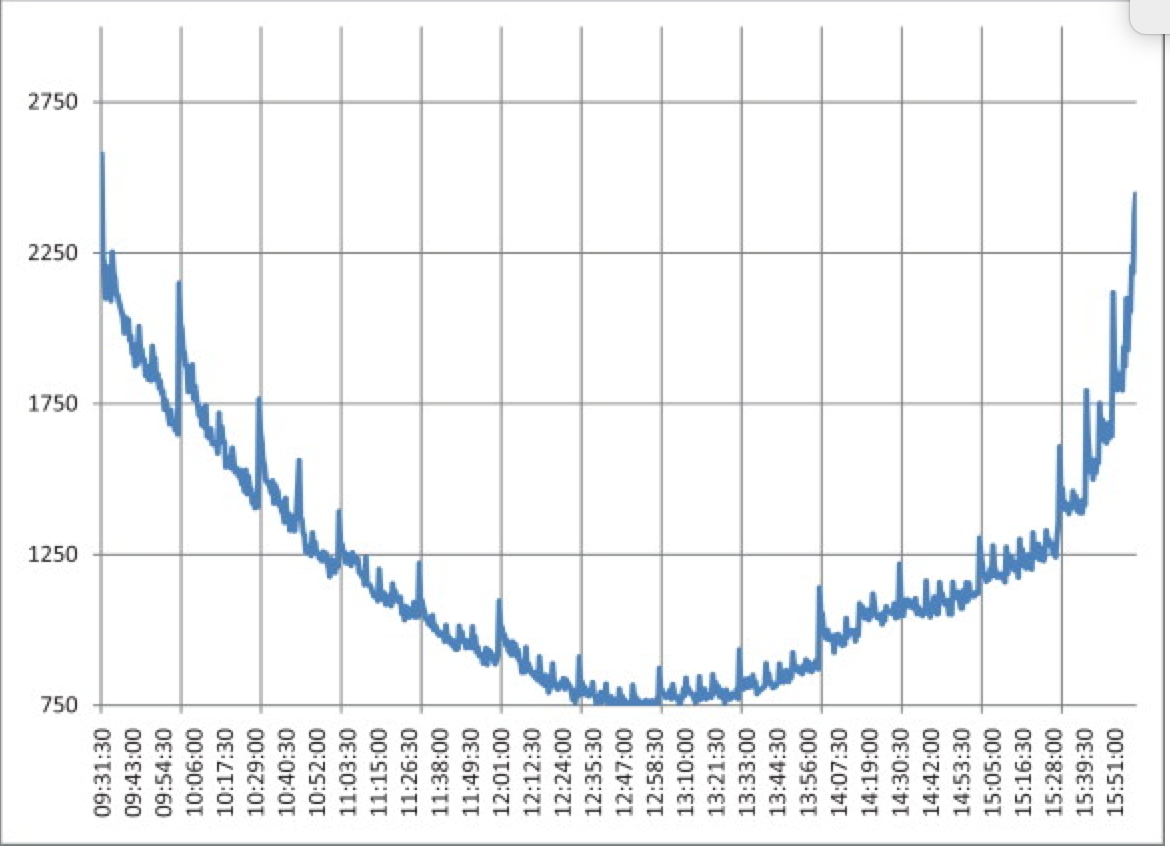

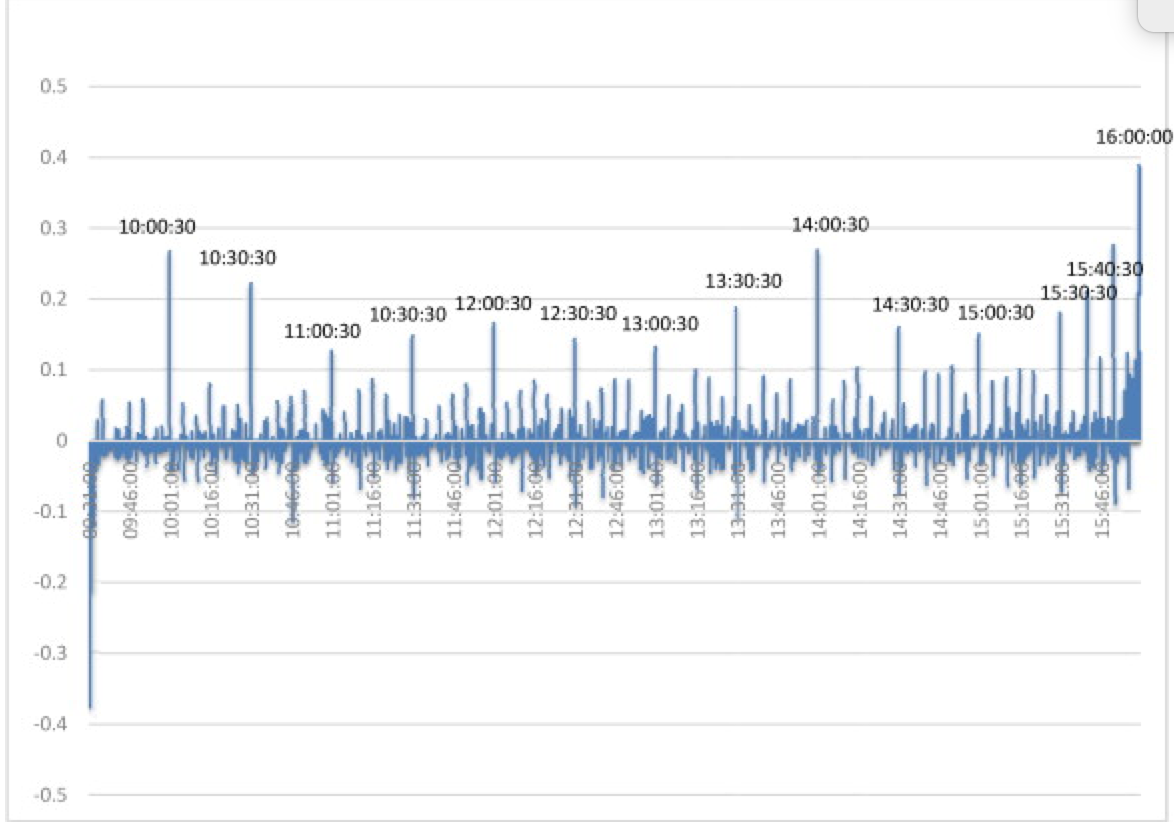

Volume "clusters" at discrete time nodes

Only partially explained by news anouncements

No such thing as "steady trade/order flow

\(\Rightarrow\) Caution is needed when interpreting traditional (esp. time-weighted) measures

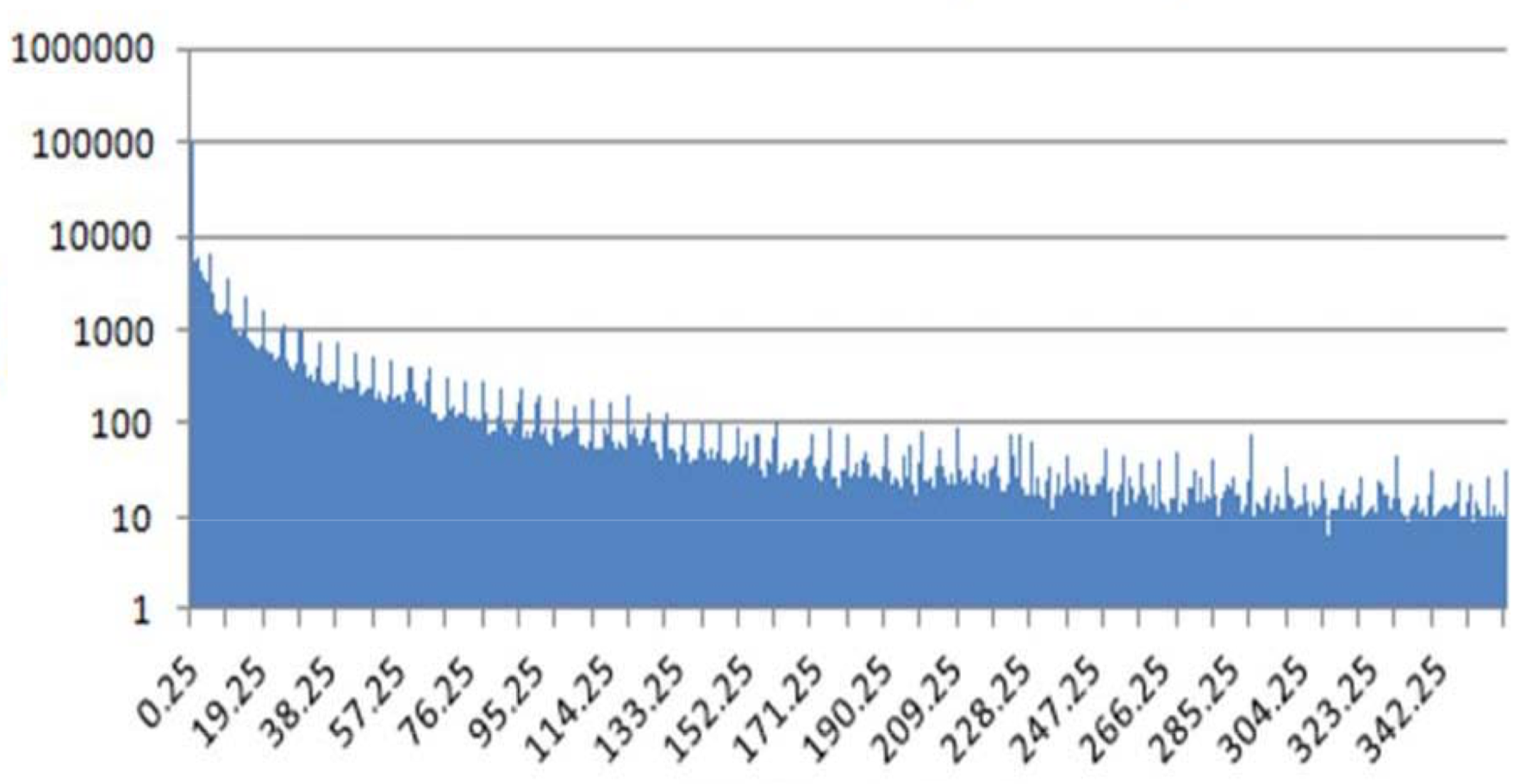

Trades Cluster at Discrete Nodes

Volume is (predictably?) higher at 10:00, 10:30, 11:00, 11:30,...

The authors:

Alternate explanations?

Broussard and Nikiforov (2014):

Source: Doug Clark (ITG Canada); TSX Data on November 30 2011

Likely "machine based" -- but need not be HFT

Suppose buy-side algos trade at discrete nodes:

Can we identify/disentangle cause and consequence?

\(\Rightarrow\) improvements in the spreads possible in either of these

Other features may also match the authors' findings, e.g. more prominent/easier to detect in small stocks

What about the costs?

If HFTs respond to predictable buy-side trading:

If HFTs "front-run" predictable, say, buy orders

Spreads can be higher but what about price changes?

Filtering the announcements:

@katyamalinova

malinovk@mcmaster.ca

slides.com/kmalinova

https://sites.google.com/site/katyamalinova/

By Katya Malinova

This is a discussion that I gave at the Women in Microstructure Meeting June 2019. The slides are arranged in a "2x2 table" and meant to be viewed " column-by-column".