Katya Malinova PRO

I am an Associate Professor, Mackenzie Investments Chair in Evidence-Based Investment Management at the DeGroote School of Business, McMaster University, Canada.

WFA 2024

Honolulu, June 28-30, 2024

| McMaster University |

University of Toronto |

|---|

Preliminaries

Liquidity providers

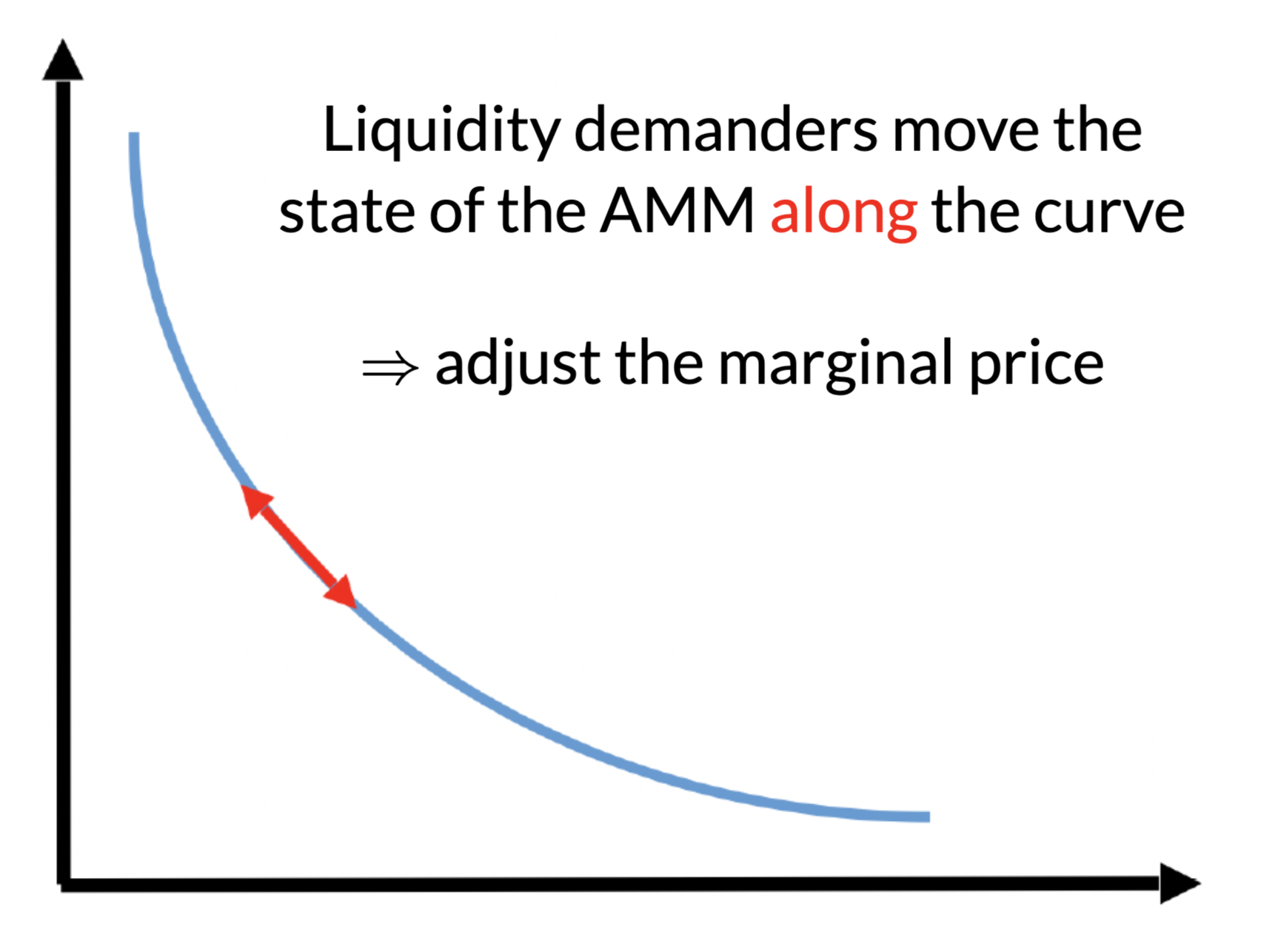

Liquidity demander

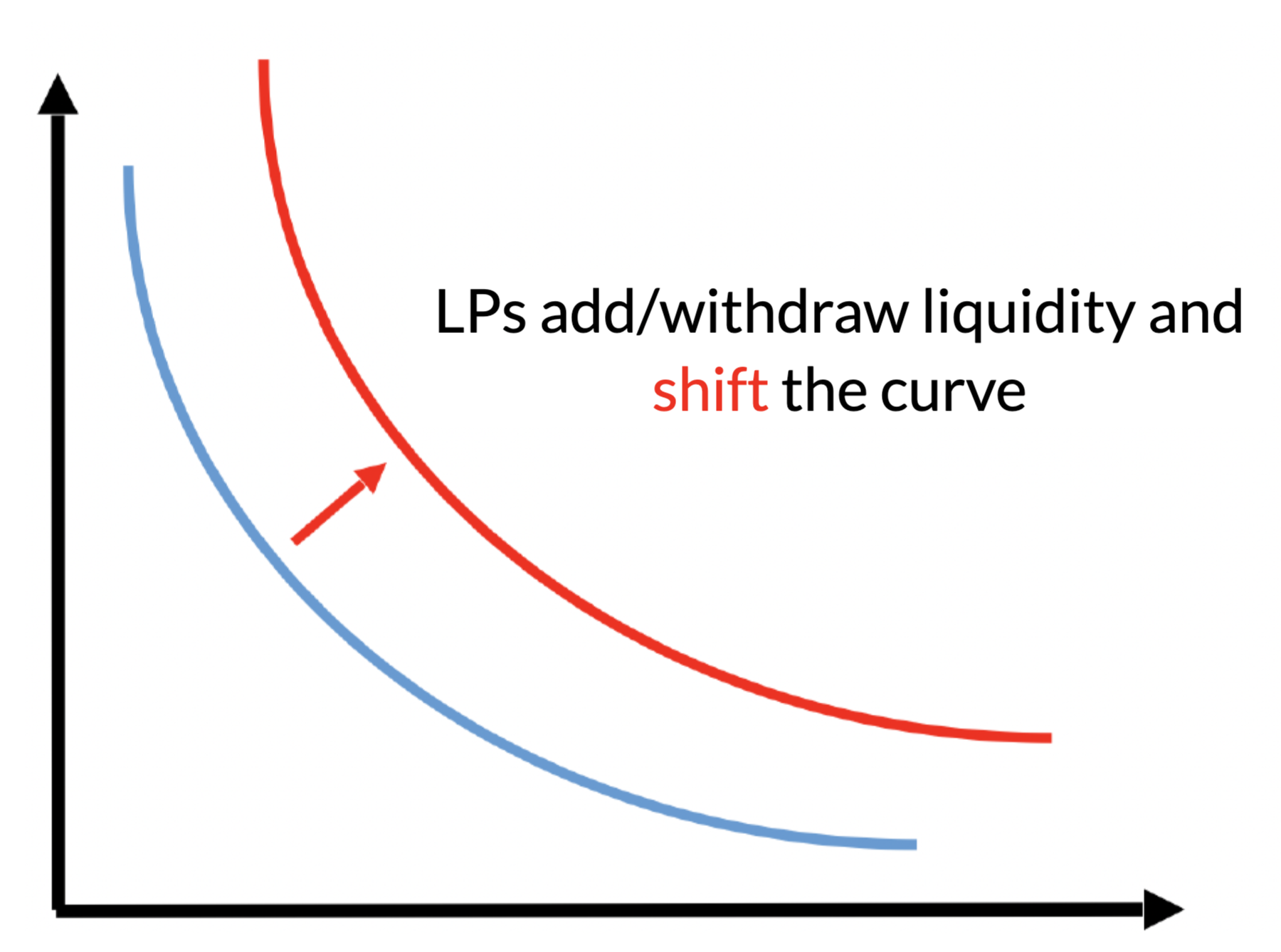

Liquidity Pool

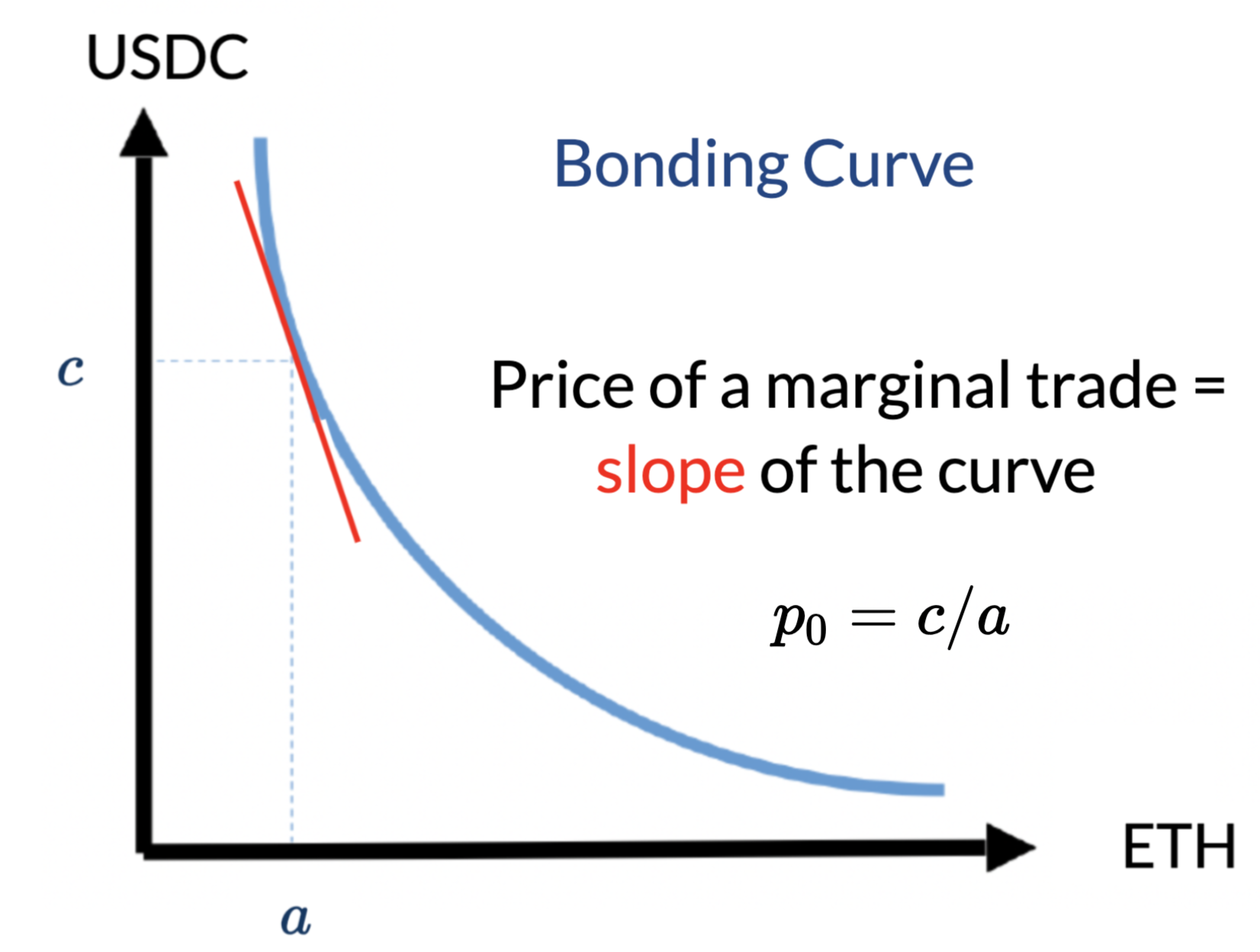

AMM pricing is mechanical:

No effect on the marginal price

Key Components

Existing asset holders, not market makers, do not aim for zero inventory!

Modelling Calibrate-able Liquidity Supply and Demand in an Automated Market Maker

Liquidity providers

Buy and hold

Provided liquidity

in the pool

Expected returns to liquidity providers over the "deposit period"

Similar to Lehar and Parlour (2023), Barbon & Ranaldo (2022).

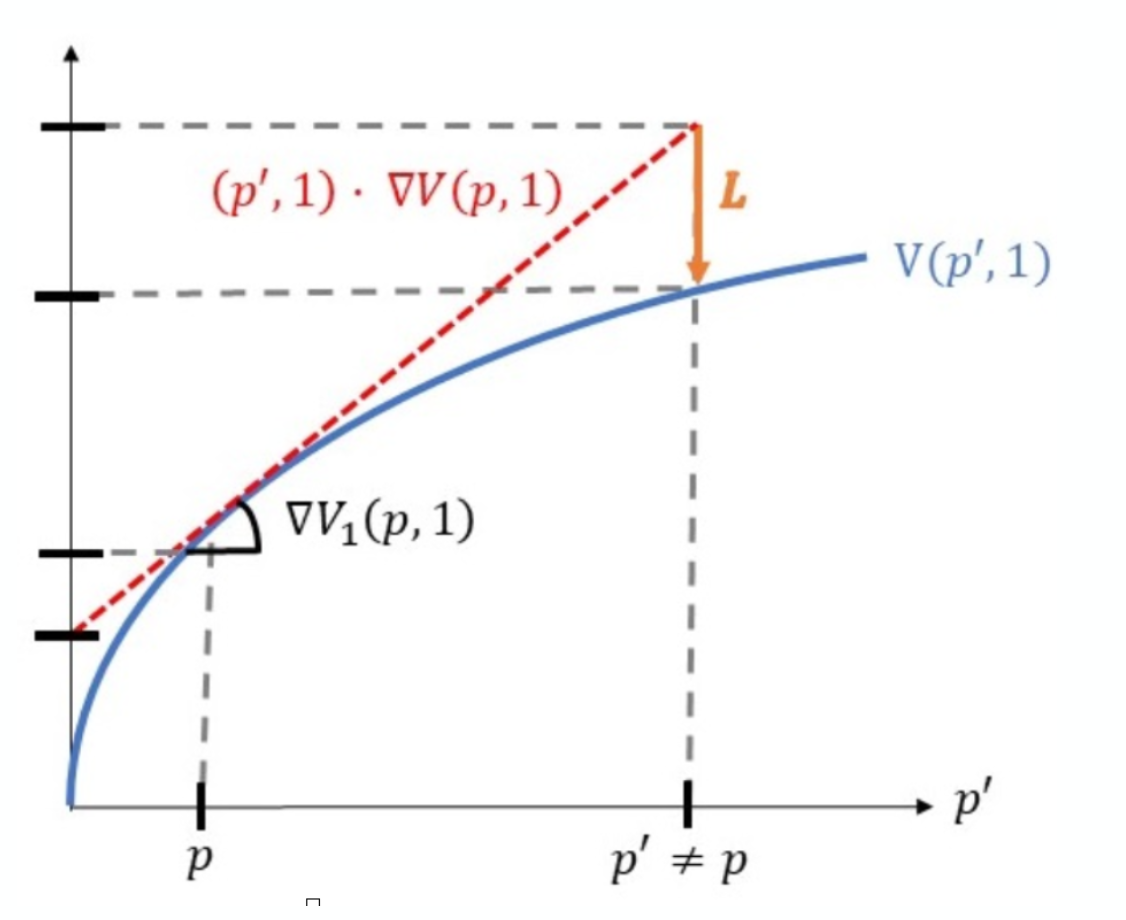

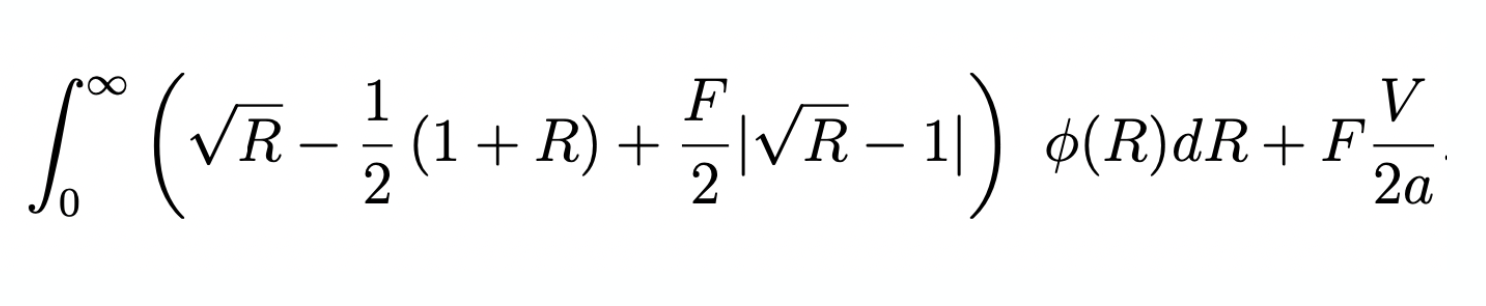

(incremental) adverse selection loss \(L\) when the asset return is \(R=p'/p\)

fees earned

on informed

fees earned

on balanced flow

for reference:

For fixed balanced volume \(V\) & fee \(F\):

\(=\) 0

Liquidity Demander's Decision & (optimal) AMM Fees

Result:

competitive liq provision\(\to\) there exists an optimal (min trading costs) fee \(F >0\)

Similar to Lehar&Parlour (2023) and Hasbrouck, Riviera, Saleh (2023)

What's next?

Approach: daily AMM deposits

Background on Data

some volume may be intermediated

AMMs based on historical returns

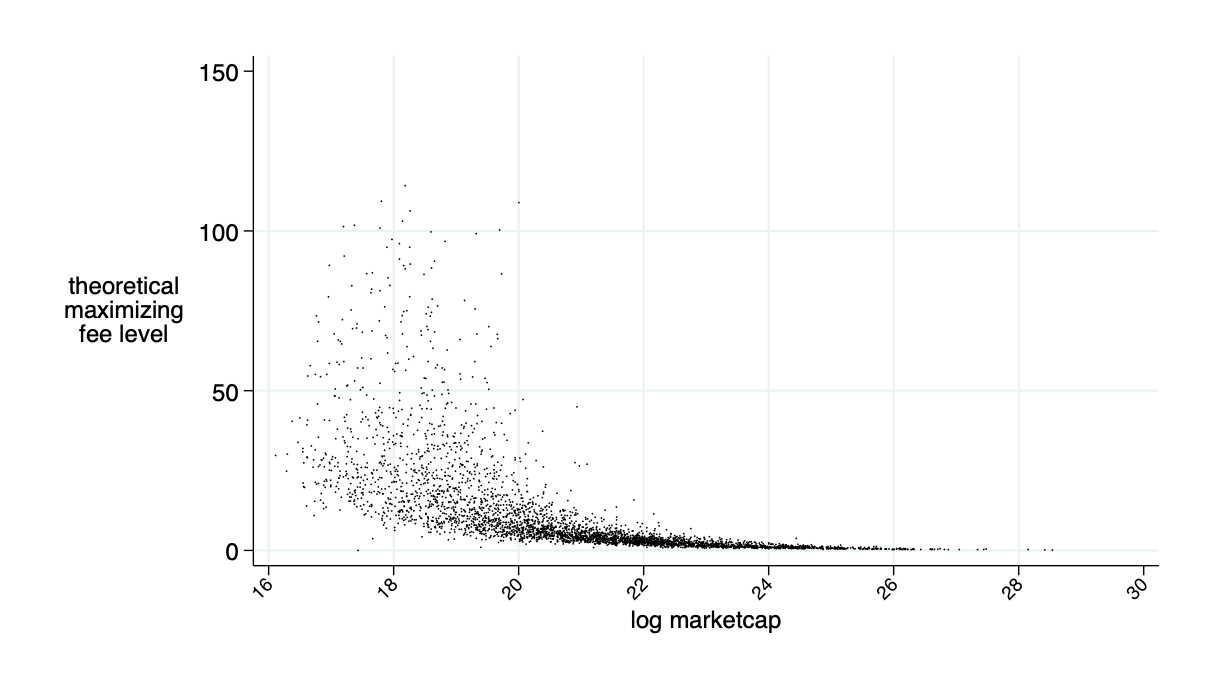

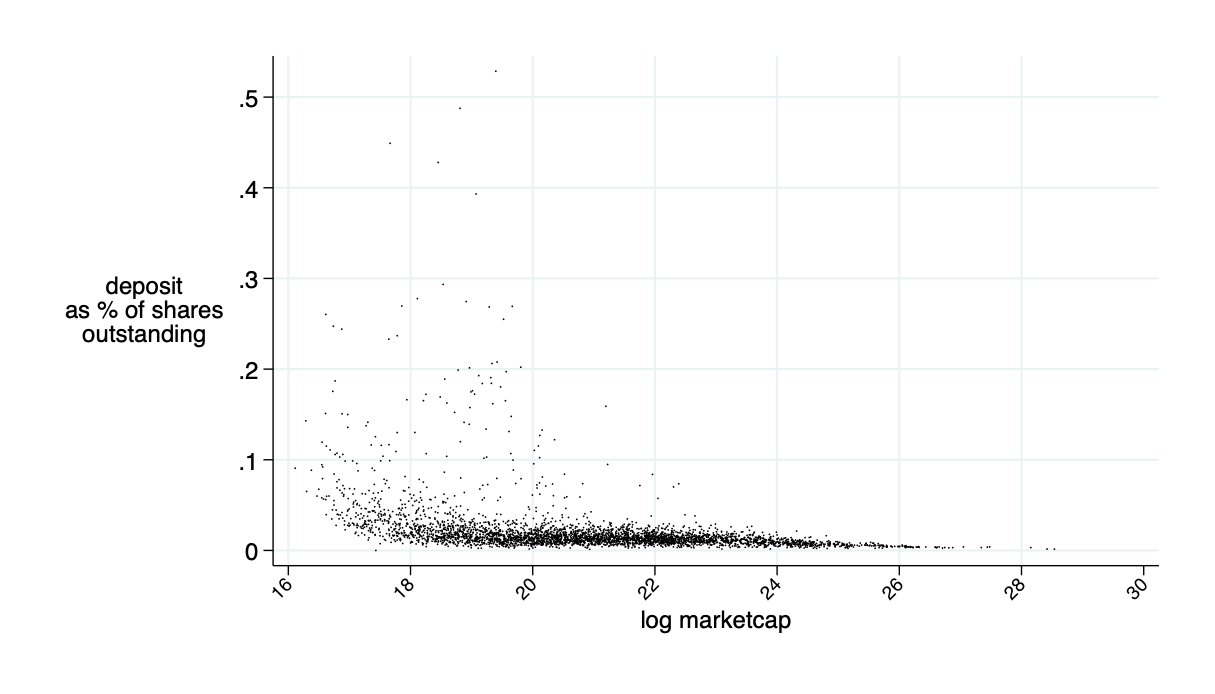

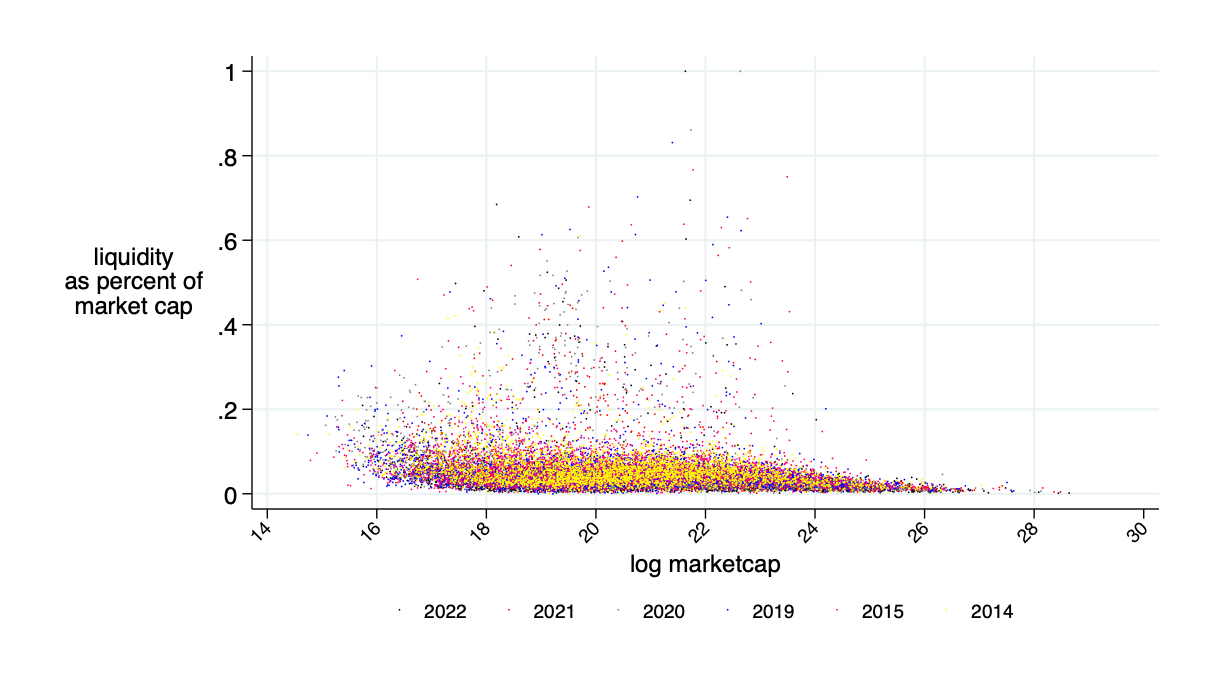

Average of the market cap to be deposited for competitive liquidity provision: \(\bar{\alpha}\approx 2\%\)

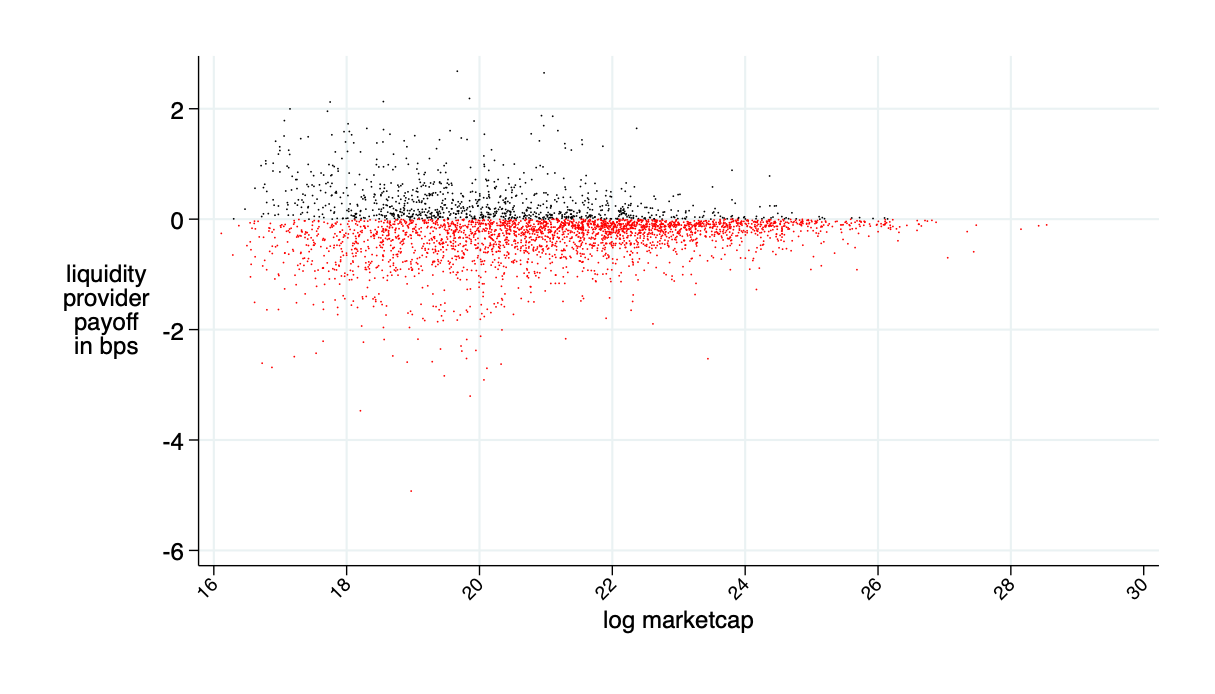

almost break even on average (average loss 0.2bps \(\approx0\))

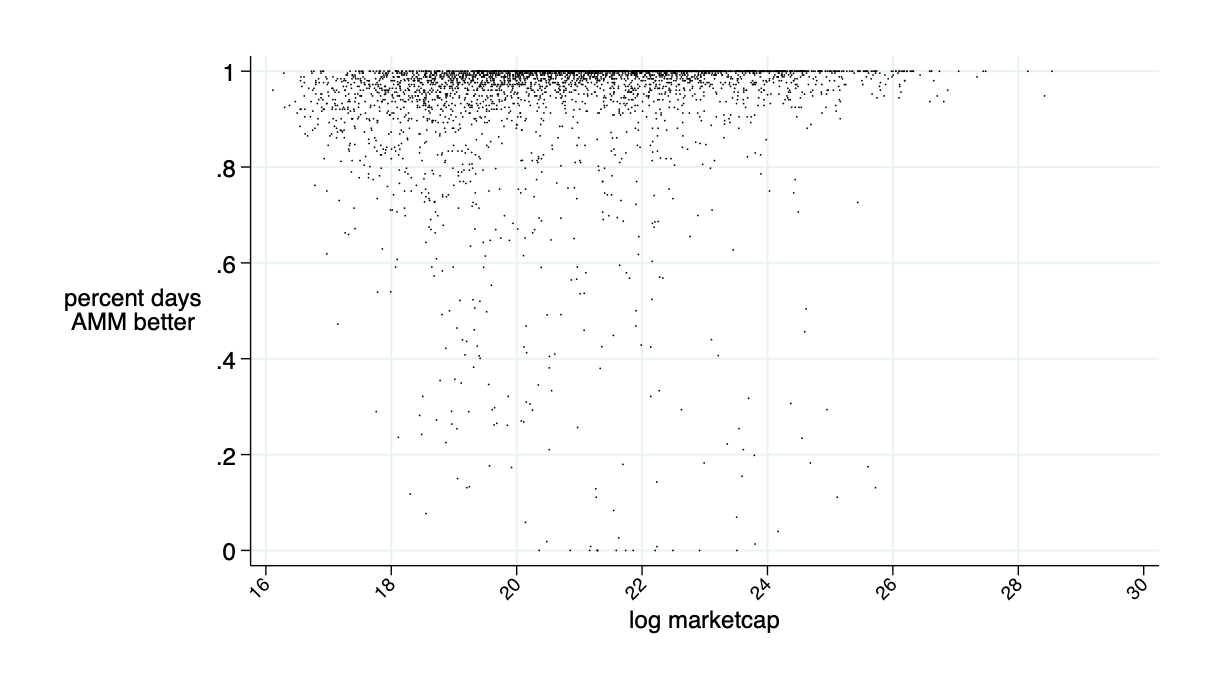

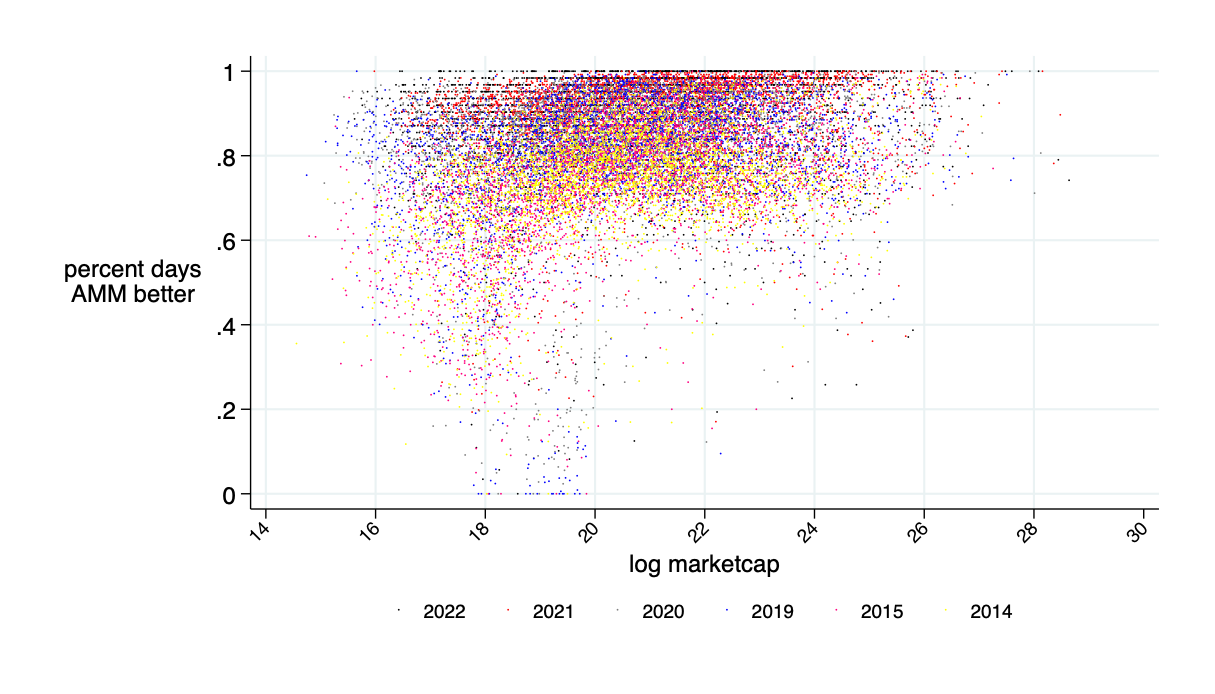

average: 94% of days AMM is cheaper than LOB for liq demanders

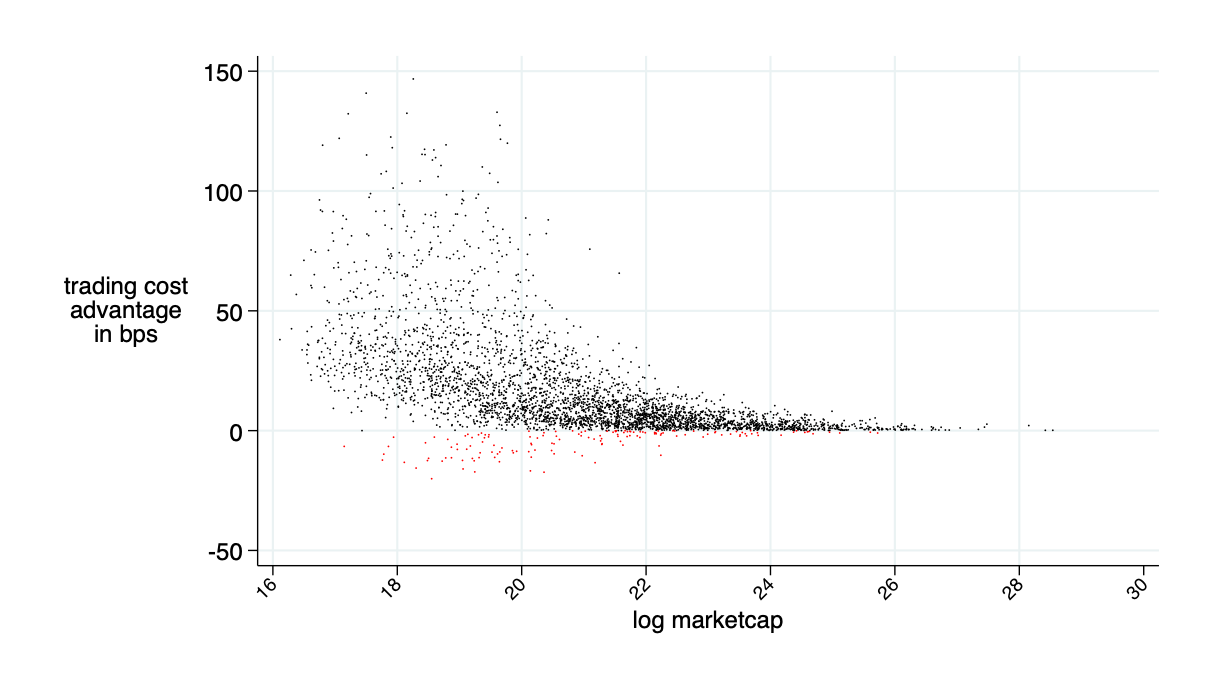

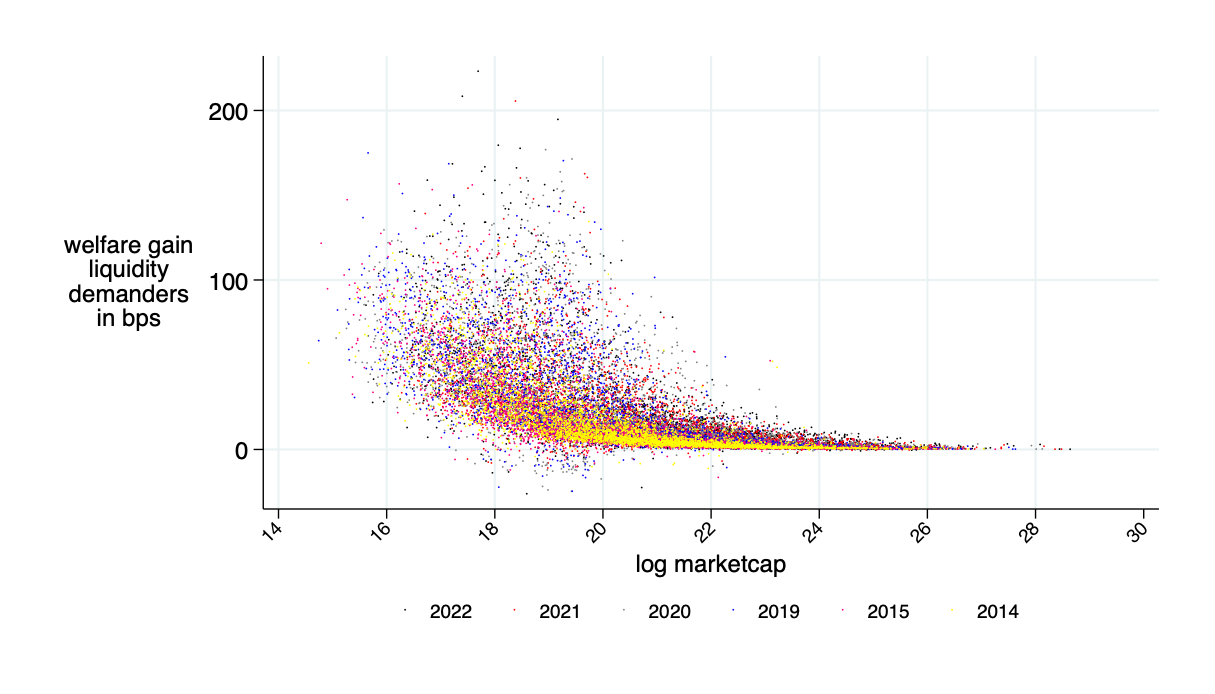

average savings: 16 bps

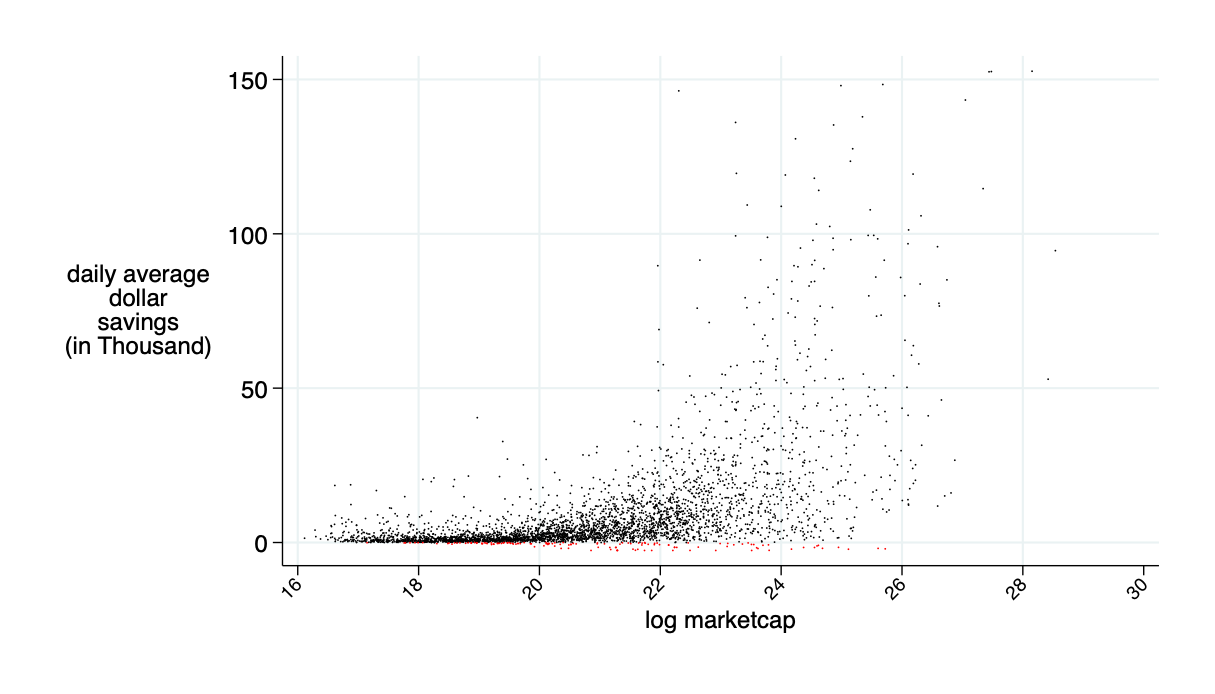

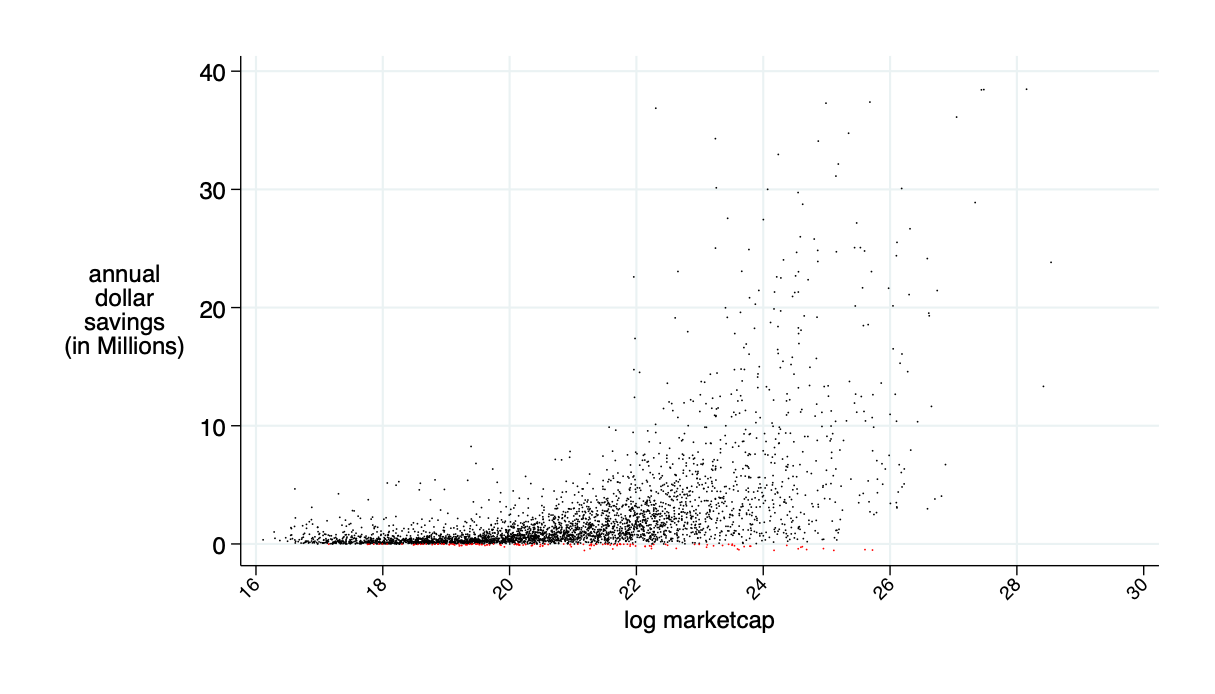

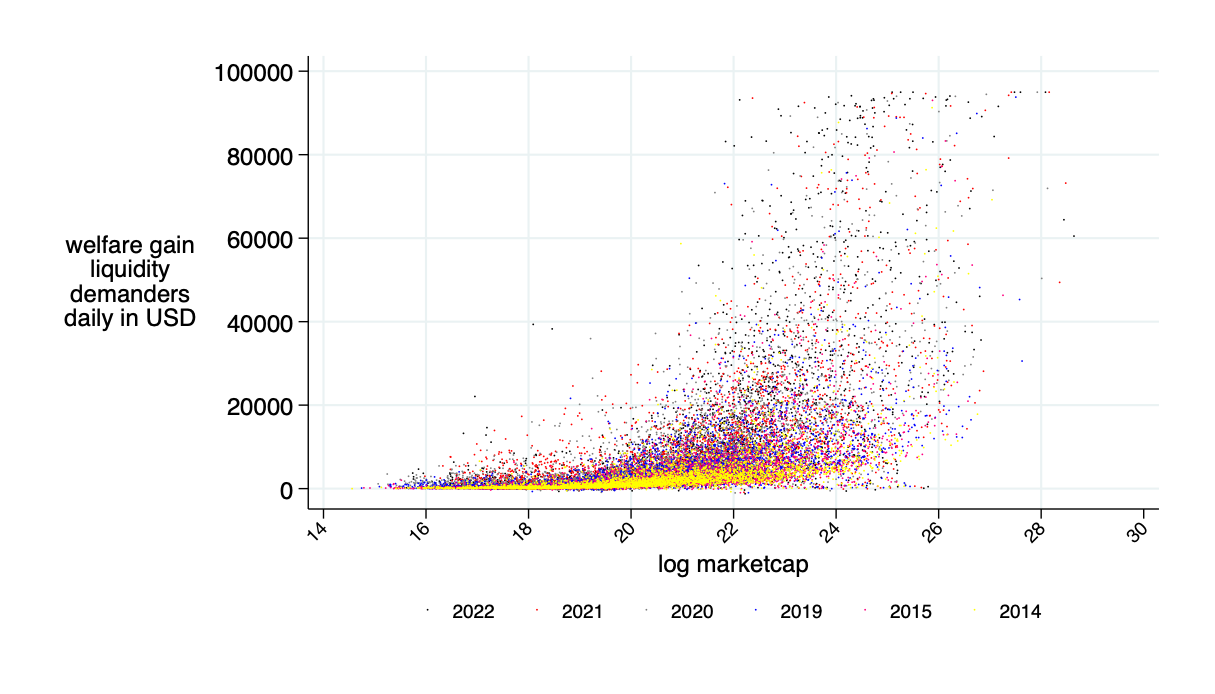

average daily: $9.5K

average annual saving: $2.4 million

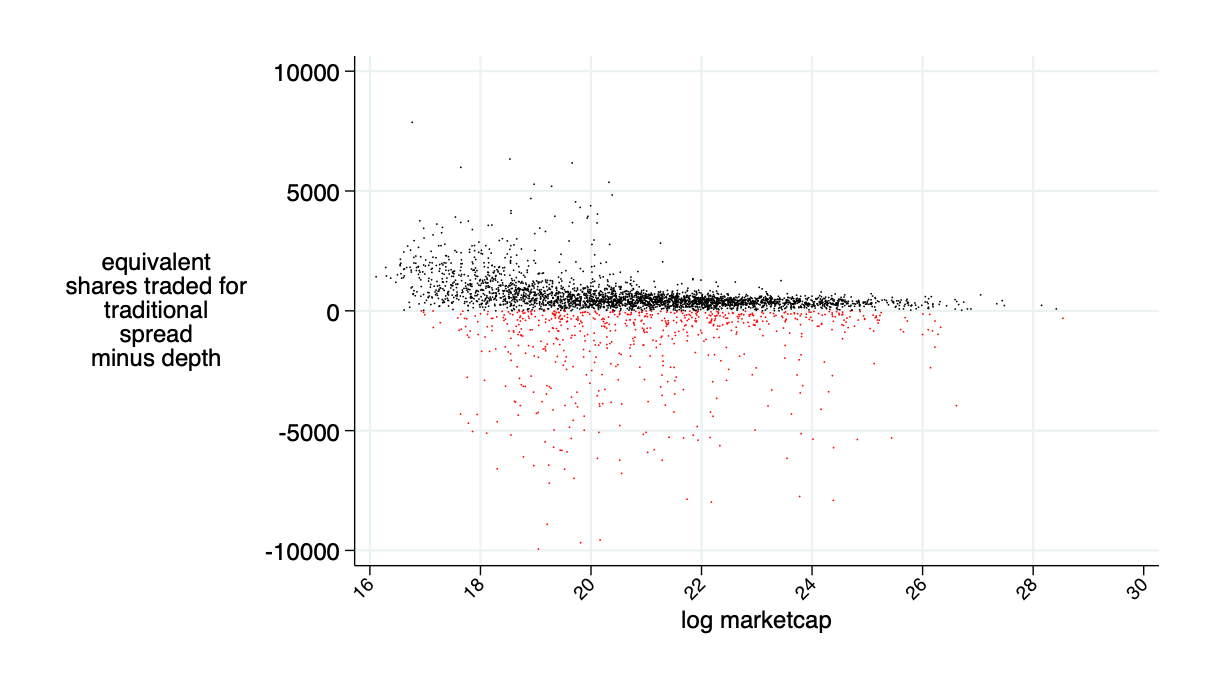

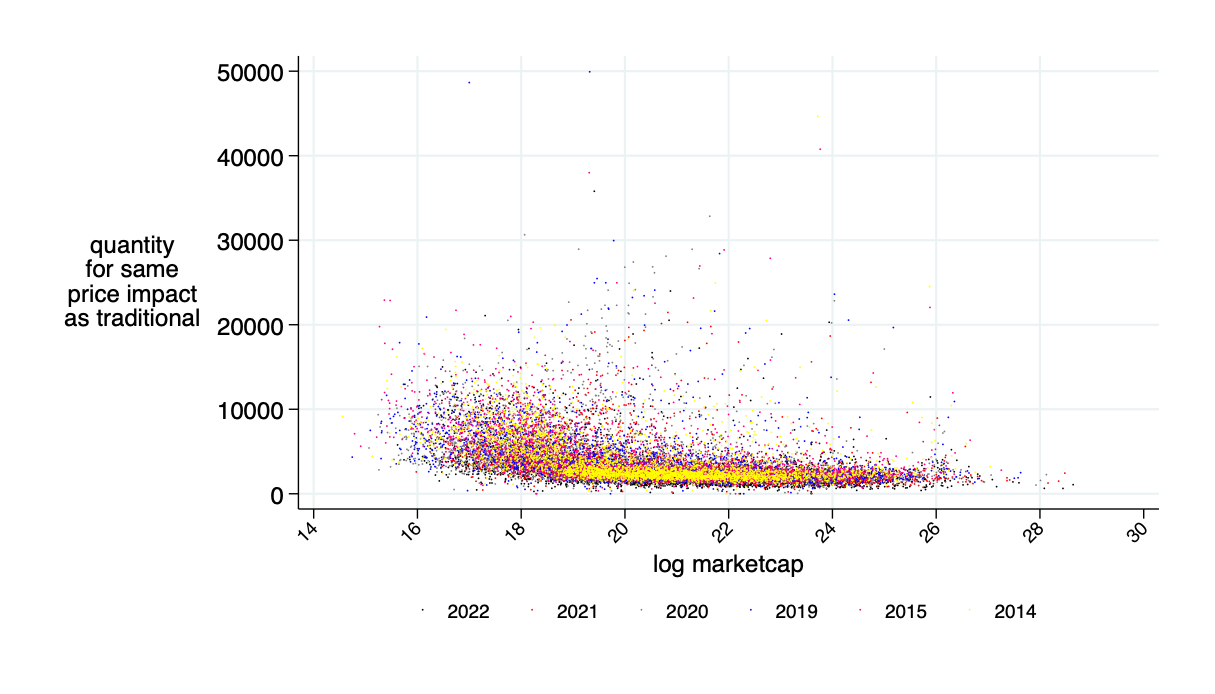

implied "excess depth" on AMM relative to the traditional market

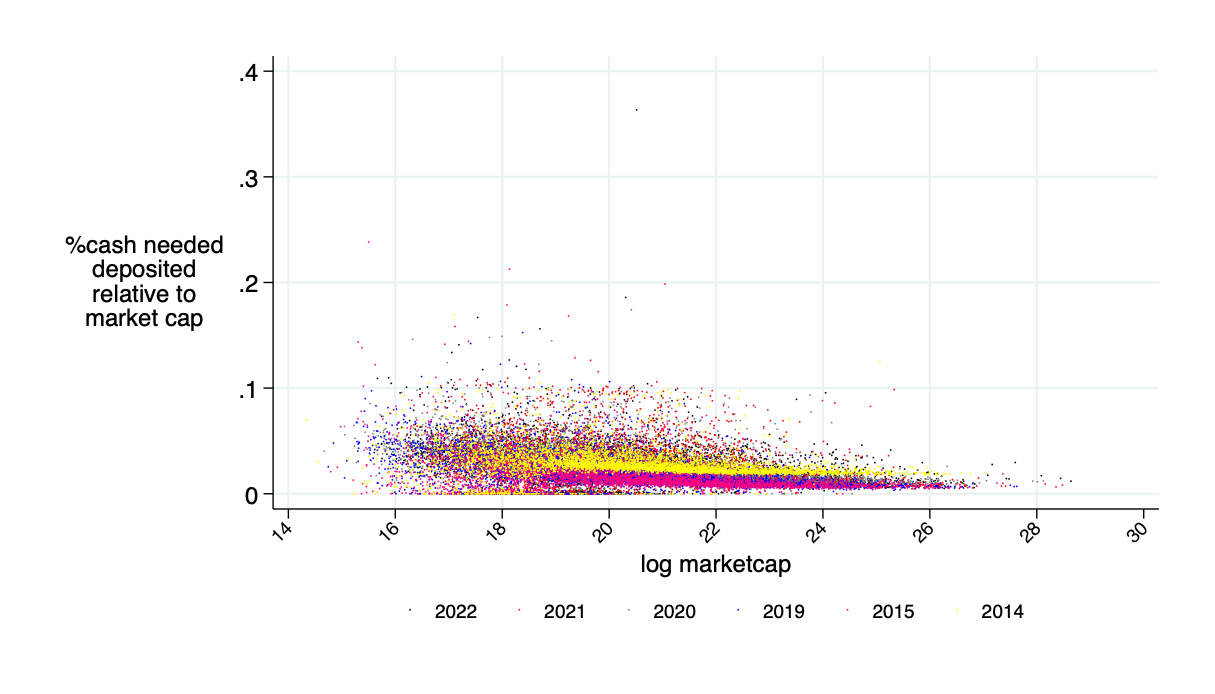

Sidebar: Cash deposit requirements

\(\Rightarrow \) Need about 5% of the value of the shares deposited -- not 100% -- to cover up to a 10% return decline

Summary

@katyamalinova

malinovk@mcmaster.ca

slides.com/kmalinova

https://sites.google.com/site/katyamalinova/

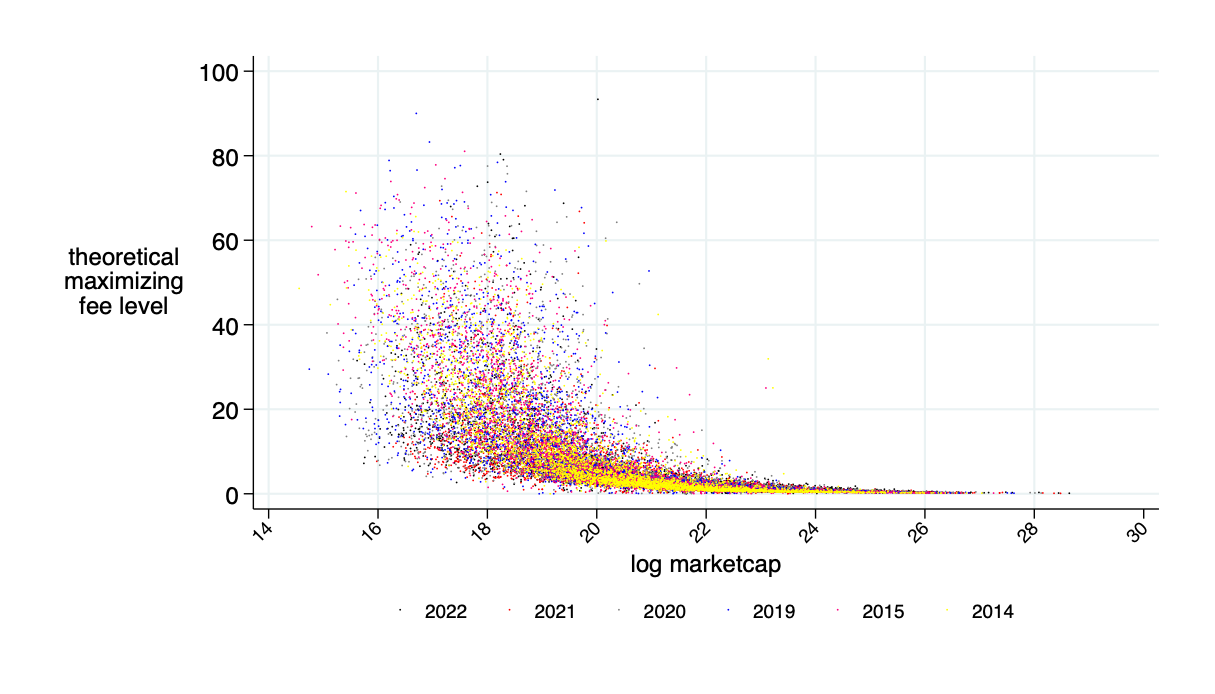

Optimal fee \(F^\pi\)

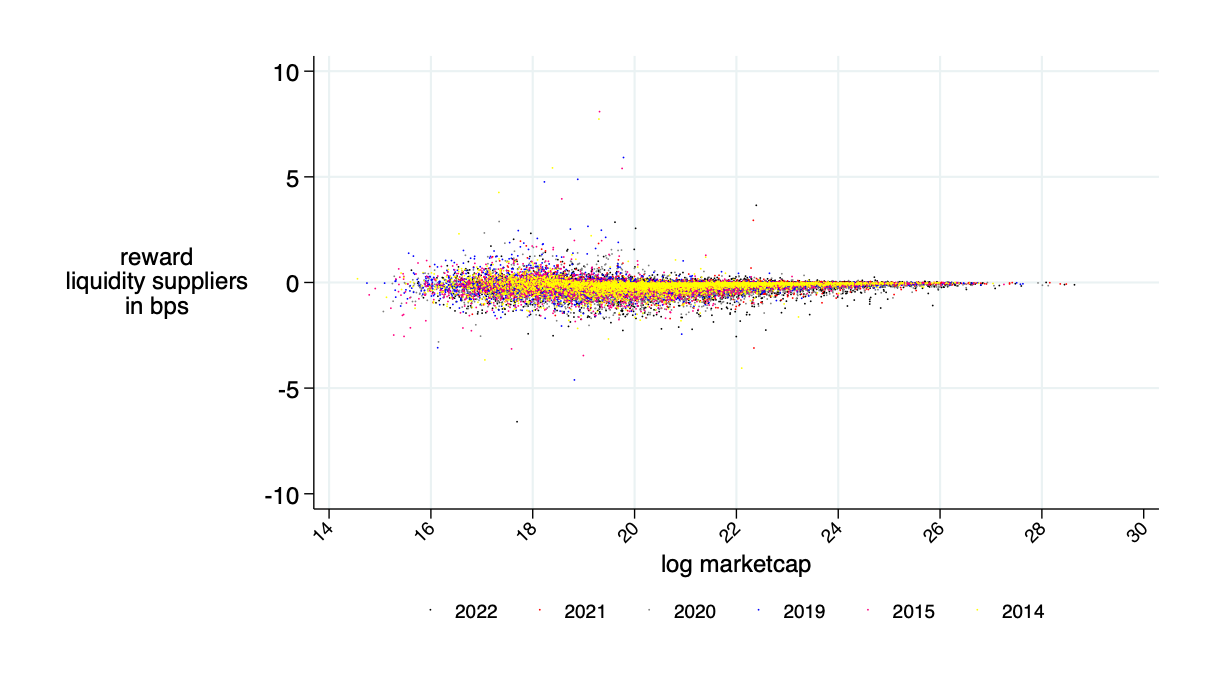

average benefits liquidity provider in bps (average=0)

Insight: Theory is OK - LP's about break even

\(\overline{\alpha}\) for \(F=F^\pi\)

Need about 10% of market cap in liquidity deposits to make this work

actually needed cash as fraction of "headline" amount

Only need about 5% of the 10% marketcap amount in cash

AMMs are better on about 85% of trading days

quoted spread minus AMM price impact minus AMM fee (all measured in bps)

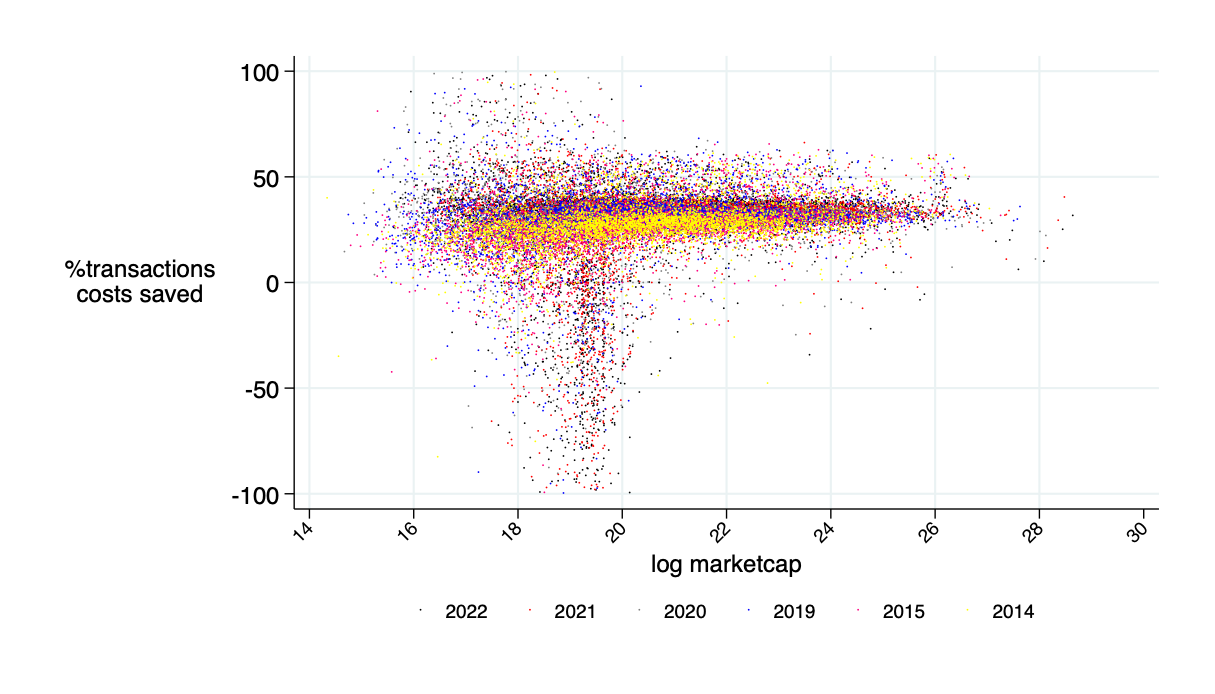

relative savings: what fraction of transactions costs would an AMM save? \(\to\) about 30%

theoretical annual savings in transactions costs is about $15B

By Katya Malinova

WFA Presentation 2024