Katya Malinova PRO

I am an Associate Professor, Mackenzie Investments Chair in Evidence-Based Investment Management at the DeGroote School of Business, McMaster University, Canada.

DeGroote School of Business

McMaster University

Future Perspectives of Blockchains

Lucerne, April 18, 2024

Preliminaries & Some Motivation

Nokia's market shares for devices:

What happened and can it happen to banks?

What did they pay for?

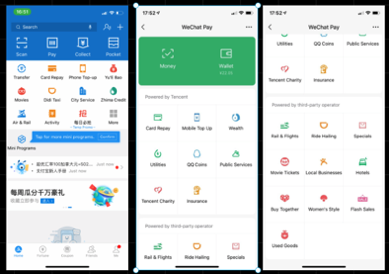

What do people value?

If banks move all data into "the cloud," why do we need banks?

Financial Infrastructure

payments

stocks, bonds, and options

swaps, CDS, MBS, CDOs

insurance contracts

payments

stocks, bonds, and options

swaps, CDS, MBS, CDOs

insurance contracts

Siloed banks

Cloud computing and cloud storage

Open banking and open data

The past (and the present?)

The present and near future

3-5 years in the future

5-10 years in the future

Platforms?

Banks?

Tech firms?

The Business of Trading in a Decentralized World

payments network

Stock Exchange

Clearing House

custodian

custodian

beneficial ownership record

seller

buyer

Broker

Broker

Text

Liquidity providers

Liquidity demander

Liquidity Pool

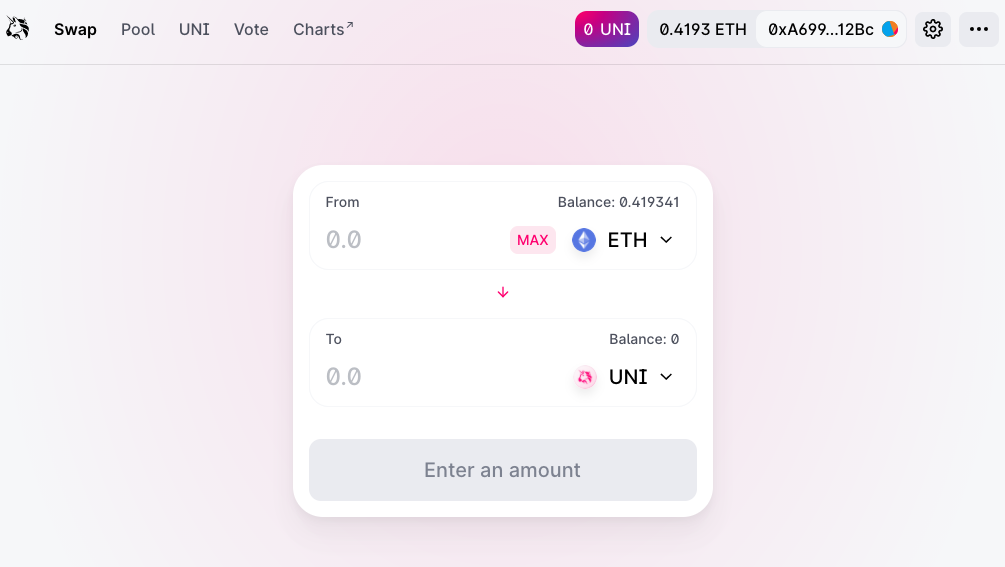

\(\to\) simply connect with MetaMask (or similar wallet)

How does this look in practice?

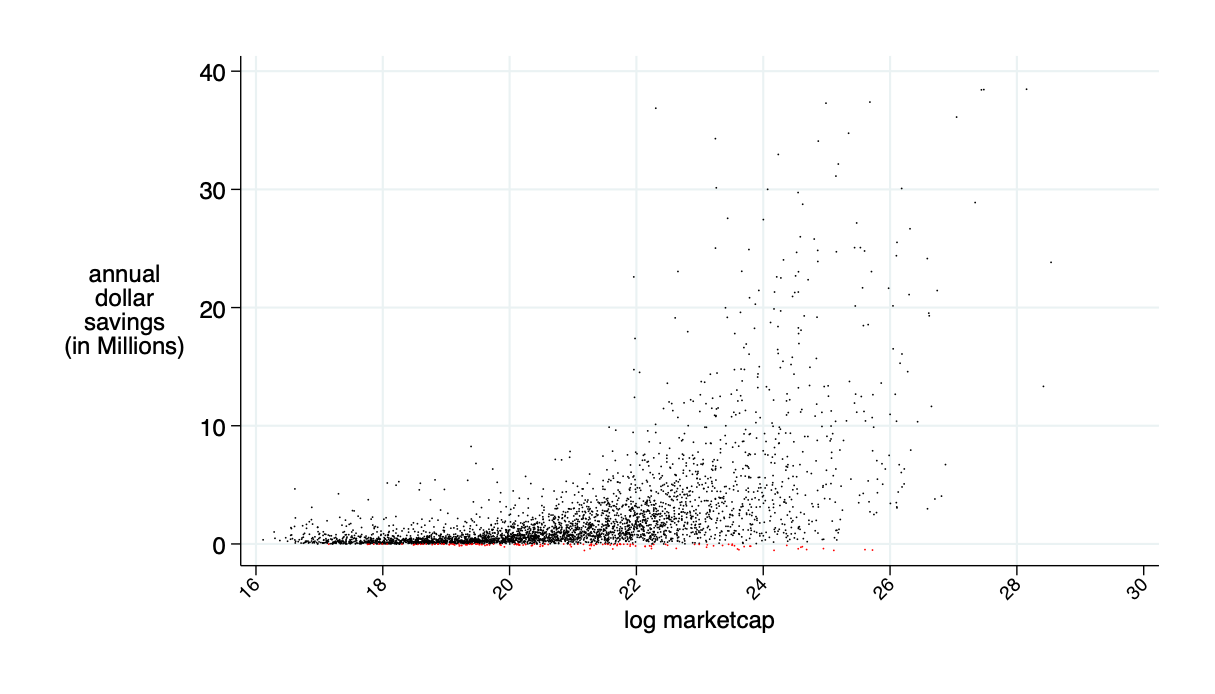

average annual saving: $2.4 million

Source: "Learning from DeFi: Would Automated Market Makers Improve Equity Trading?" working paper, Malinova & Park 2023

Possible transaction cost savings if AMM applied to equity trading: \(\approx\) 30%

Source of savings:

UniSwap Lab supports development

a website app accesses the code

token holders control contact features

don't own the code

operation = decentral

control = decentral

anyone can use the baseline code

core code runs on the blockchain

tokens used as rewards

Blockchain-based Businesses?

liquidity \(\nearrow\)

volume \(\nearrow\)

protocol fees \(\nearrow\)

token value \(\nearrow\)

Platform economics is tricky:

Business Challenges

Additional common infrastructure challenges?

What value do these tokens have?

Economics of financing instruments

Lots of academic research on tokens!

Tokens as financing tools:

tokens as revenue claims lead to under-investment relative to equity

token retention by the entrepreneur as a tool to signal quality

developer incentives for continuous development

importance of future monetary policy

Chod and Lyandres (2021), Gan, Tsoukalas, and Netessine (2021a), Davydiuk, Gupta, and Rosen (2023), Canidio (2018), Catalini and Gans (2018)

Lots of academic research on tokens!

Tokens for platforms:

network effects, overcome coordination failures, accelerate adoption

transfer of governance rights from platform to users

speculators early on, users later

pre-sale allows for more surplus extraction for the entrepreneur, more projects to be financed

Li and Mann (2018), Bakos and Halaburda (2019), Sockin and Xiong (2023), Cong, Li, and Wang (2021) and Cong, Li, and Wang (2022) (asset-pricing based), Prat, Danos, and Marcassa (2023), Chod, Trichakis, and Yang (2022), Shakhnov and Zaccaria (2021),

Lee and Parlour (2022), Goldstein, Gupta, and Sverchkov (2022).

Tokens: summing up

evolving use: when do they stop being investment contracts?

Bringing TradFi to DeFi:

Asset Tokenization or

"The Creation of Asset-Linked Tokens"

Tokenization of stocks is nothing new: American Depository Receipts

foreign investor/

issuer

domestic bank with foreign representation

ADR issuing bank handles

Is this a workable model for blockchain- tokenization of existing assets?

foreign representation of domestic bank/ its custodian

domestic depository bank

S.E.C.

registration with form F-4

domestic broker

issues and cancels ADRs

domestic investor

lets investors own and trade ADRs

domestic

market

deposits shares

detailed review: Malinova and Park (2023) "Tokenized Stocks for Trading and Capital Raising" available on SSRN https://papers.ssrn.com/abstract=4365241

Blockchain Tokenization has many options

existing investor/

issuer

token issuance platform

investor

wallet

instruct to create tokens

deposits shares

custodian bank

deposits shares

creates tokens and sells to investors

centralized or decentralized

market

S.E.C.

registration

Use Case #1 for Tokenized Assets: Stablecoins

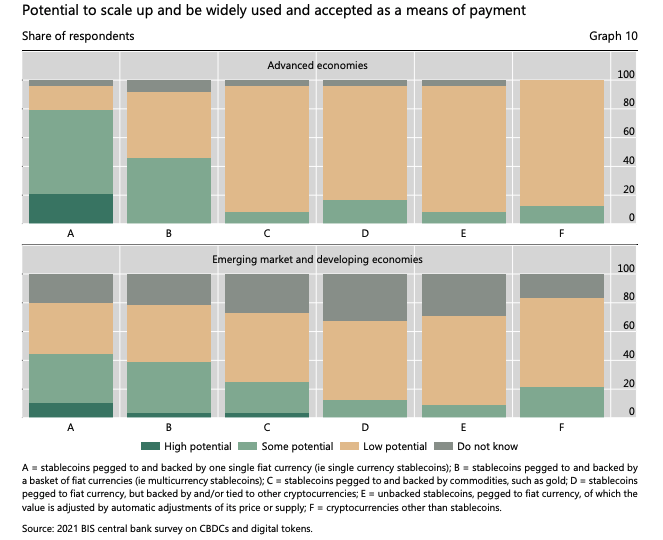

What do central bankers think about stablecoins?

BIS Survey of Central Banks (2021):

Advanced economies:

80%+: high potential or some potential for single-currency backed

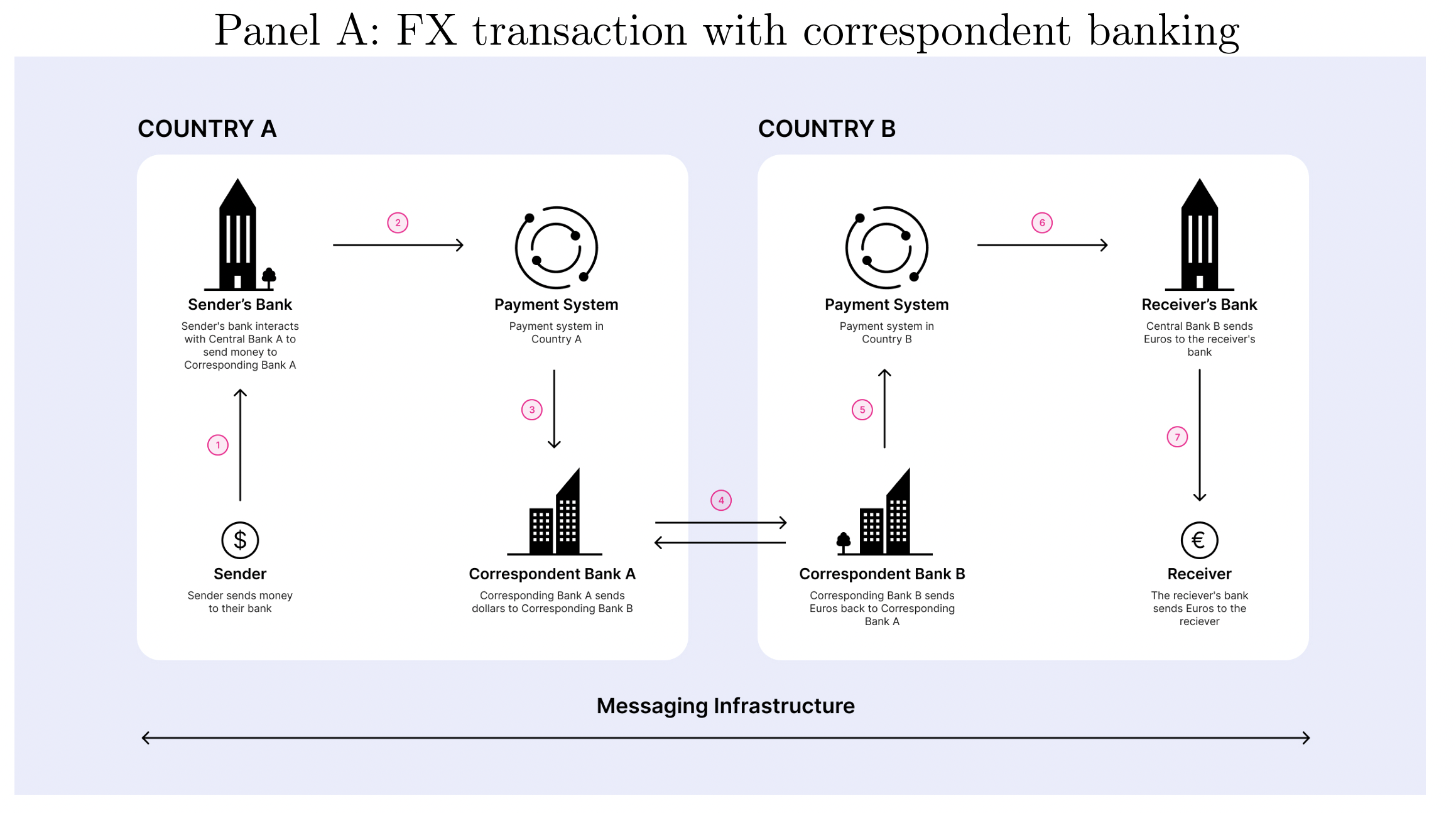

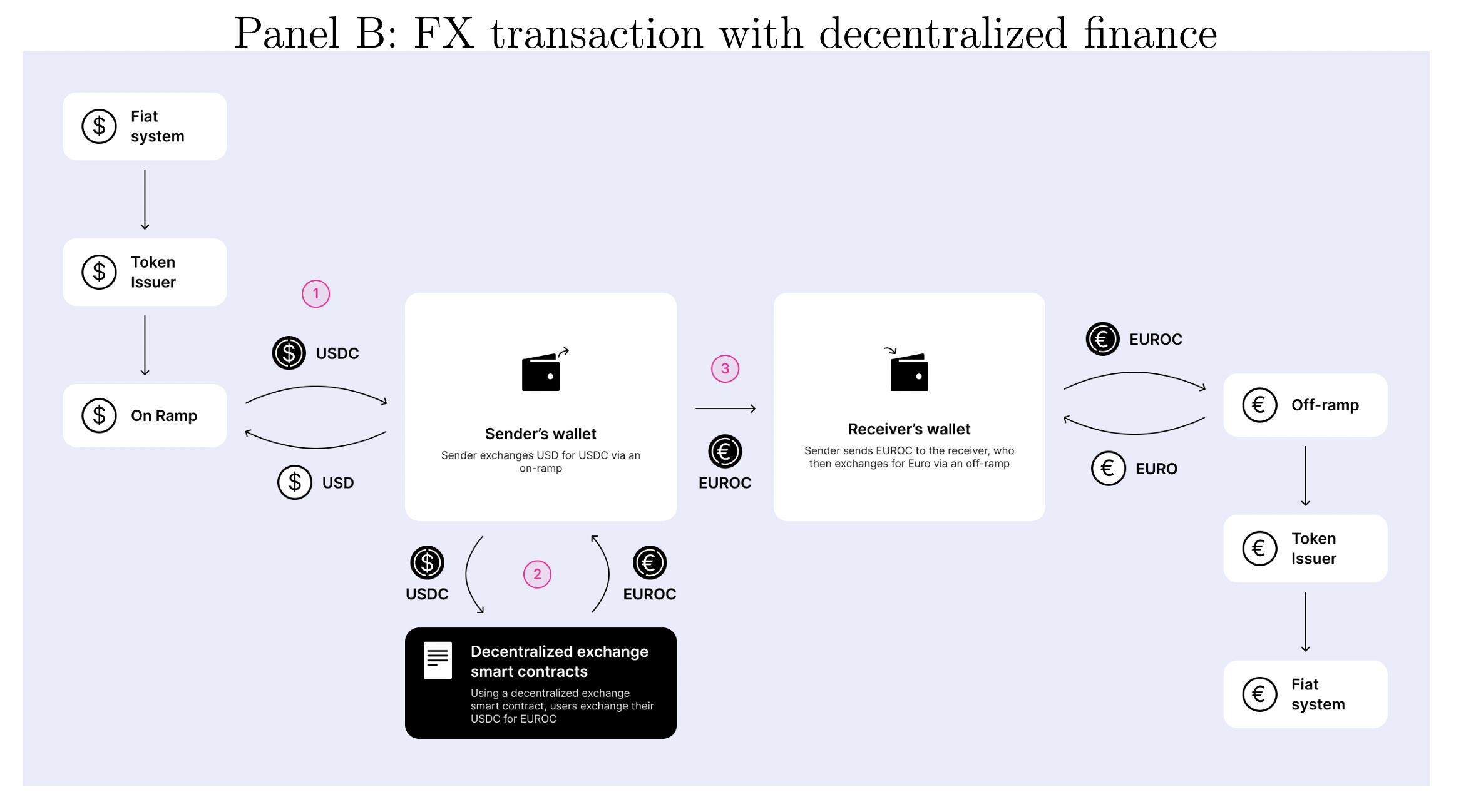

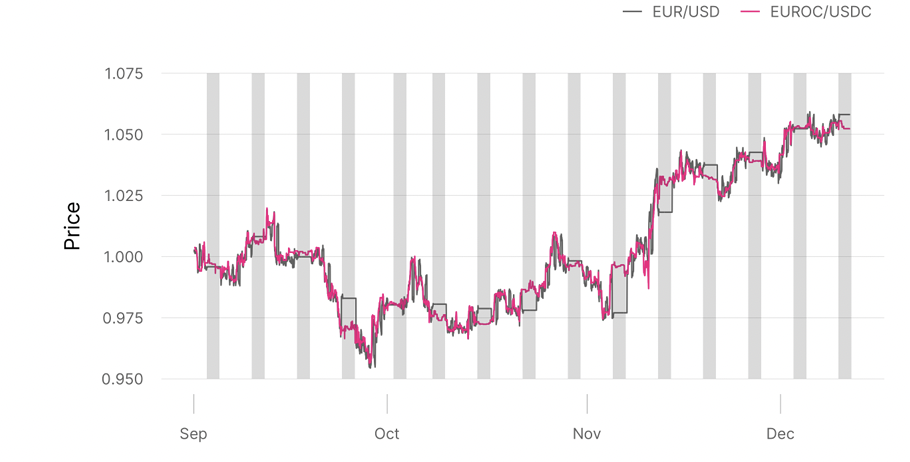

Source: On-chain Foreign Exchange and Cross-border Payments by Austin Adams, Mary-Catherine Lader, Gordon Liao, David Puth, Xin Wan (2023) [team from UniSwap Labs]

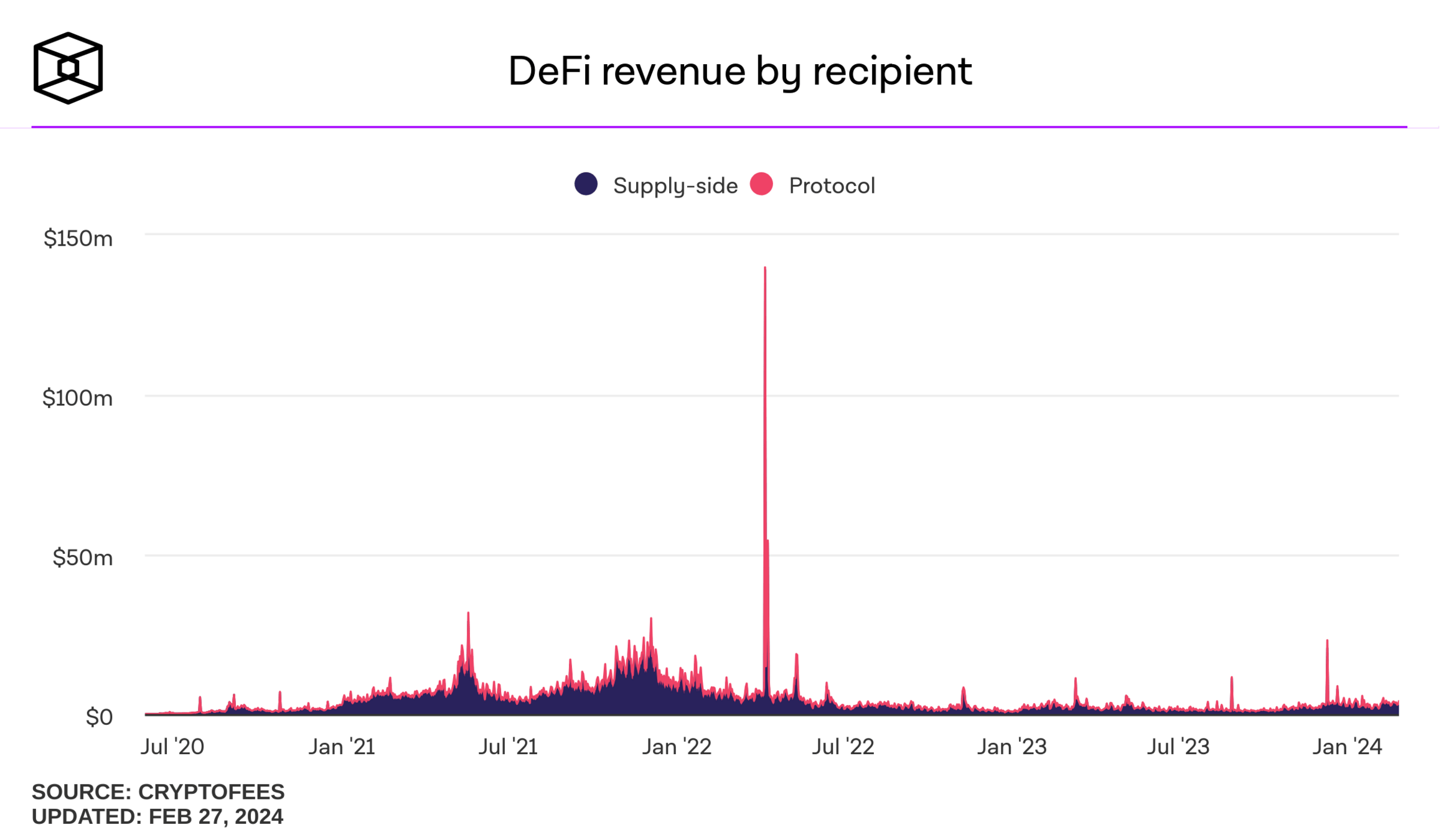

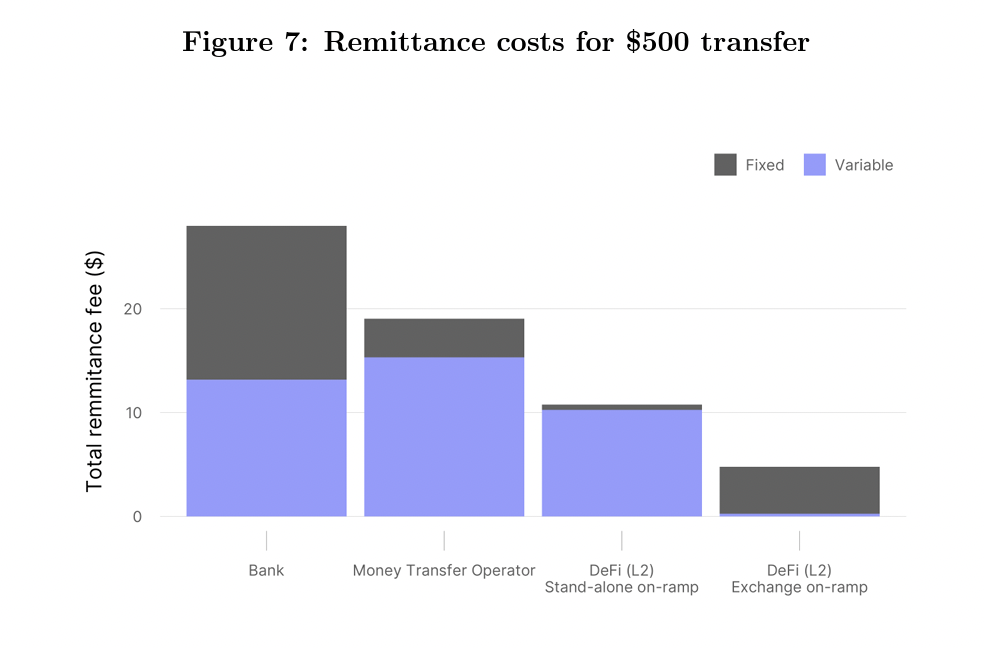

DeFi fees:

Further Thoughts

The Development is Ongoing

@katyamalinova

malinovk@mcmaster.ca

slides.com/kmalinova

https://sites.google.com/site/katyamalinova/

By Katya Malinova

Presentation at Future Perspectives of Blockchains – Legal, Economic, Political and Technical Challenges and Prospects