Katya Malinova PRO

I am an Associate Professor, Mackenzie Investments Chair in Evidence-Based Investment Management at the DeGroote School of Business, McMaster University, Canada.

Technology

Legal/Regulation

Economic functions

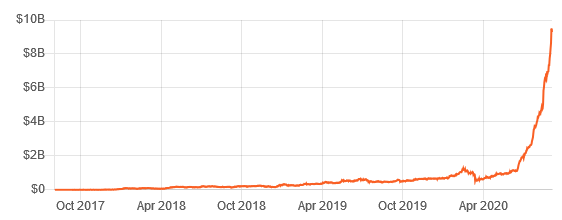

Total value locked in DeFi applications

Is there economic merit to tokens?

Do tokens solve an economic problem?

Financing mechaniPlatforms

Sockin and Xiong (2018)

Li and Mann (2020)

Bakos and Halaburda (2019)

Cong, Li, and Wang (2018)

Canidio (2020)

Chod, Trichakis, Yang (2019)

Catalini and Gans (2019)

Chod and Lyandres (2020)

Davydiuk, Gupta, and Rosen (2019)

Lee and Parlour (2019)

Garratt and van Oordt (2019)

Financing mechanism

Platforms

entrepreneur wants to produce a good or service

Setup cost for production \(C_0\)

Marginal cost of producing \(c\)

Demand is uncertain: revealed after the setup cost has been paid but before production.

Inverse demand \(p(q)=x-q\)

\( x\) is uniform on \([0,\theta]\).

\(x_i\)

\(x_j\)

\(x_k\)

\(c\)

price

If financing with own funds

\(\Rightarrow\) entrepreneur

maximizes monopoly profits

\(\Rightarrow\) produces

monopoly quantity

demand

marginal cost

marginal revenue

Equity financing

\(\Rightarrow\) max \((1-\alpha)\)(monopoly profits)

=> no distortion

\(q^m=(x-c)/2\)

\(MR=x-2q\)

\(p(q)=x-q\)

general idea: sell future output

two approaches for token sales

sell a fraction of future revenue

sell units of future output

price

demand

marginal cost

marginal revenue

Entrepreneur does not internalize the effect of an extra output unit on the token value for the tokenholders!

Result: overproduction

entrepreneur issues \(t\) tokens

for \(x\le t\): earns zero

for \(x>t\): solves \[\max_q q (x-q-t)-cq.\]

effectively solves

\(\max_q\) s.t. \(MR(q)+t=c\)

price

demand

marginal cost

marginal revenue

\(\Rightarrow\) "tilts" marginal revenue for

entrepreneuer left because

get only fraction of revenue

\(\Rightarrow\) solves \((1-\alpha)\)MR(q) = c

Result: underproduction

NB: Similar to underinvestment in Chod and Lyandres (2020)

revenue sharing: underproduction

output presale: overproduction

\(c\)

\(MR\)

"does not internalize" = externality

address externality: TAX!

here: tax future token income

incremental token income gets shared

\(\Rightarrow\) combine the two to get the monopoly quantity!

Presell \(t\) tokens.

As with equity, the entrepreneur receives the full NPV.

The entrepreneuer produces optimally at \(q^t=q^m\)

If \(q<t\) \(\Rightarrow\) redeem at rate \(t/q\) and tokenholders receive refund of \(c(t-q)\).

If quantity produced \(q>t\), then share \(\alpha_t\) of revenue from incremental \(q-t\) tokens with tokenholders

Idea:

entrepreneur can influence expected demand

with effort

without effort

common topic in corporate finance

very relevant in "decentralized" world where developers are scattered around the globe

also applicable to, e.g. established firms that do something new

assume \[\textit{NPV}(\text{effort})>0>\textit{NPV}(\text{no effort})\]

Investors (equity or token holders) only finance the project if the entrepreneur undertakes the effort

Solve for the optimal funding conditional on the entrepreneur taking the effort

Derive conditions such that the entrepreneur undertakes effort

1.

2.

Key insight: a token contract incentivizes effort better than equity (similarly to canonical debt vs. equity insights)

Optimal token contract has debt features:

get nothing if demand is low (only original

tokenholders get anything)

benefit if demand is high

all projects that can be financed by equity can be financed by the optimal token contract but

some projects that can be financed by optimal tokens contracts cannot be financed by equity.

Simple model of revenue-based ICO vs equity financing from the standard corporate finance + IO toolbox

Theorem 1: Without frictions, an optimal token contract finances the same

projects as equity

Theorem 2: With entrepreneurial moral hazard,

any equity-financeable project can be financed by an optimal token

some token-financeable projects cannot be financed by equity

\(\Rightarrow\) There is economic and conceptual merit to token financing

@katyamalinova

malinovk@mcmaster.ca

slides.com/kmalinova

sites.google.com/site/katyamalinova/

By Katya Malinova

This deck is arranged as a 2x2 matrix, to be viewed column by column.