Marius Zoican PRO

I am an Associate Professor of Finance and Canada Research Chair in Financial Technology at the University of Calgary’s Haskayne School of Business. My research sits at the intersection of technology and finance.

Charles Martineau and Marius Zoican

Bank of Lithuania October 16, 2020

How does investor attention impact analyst coverage choices?

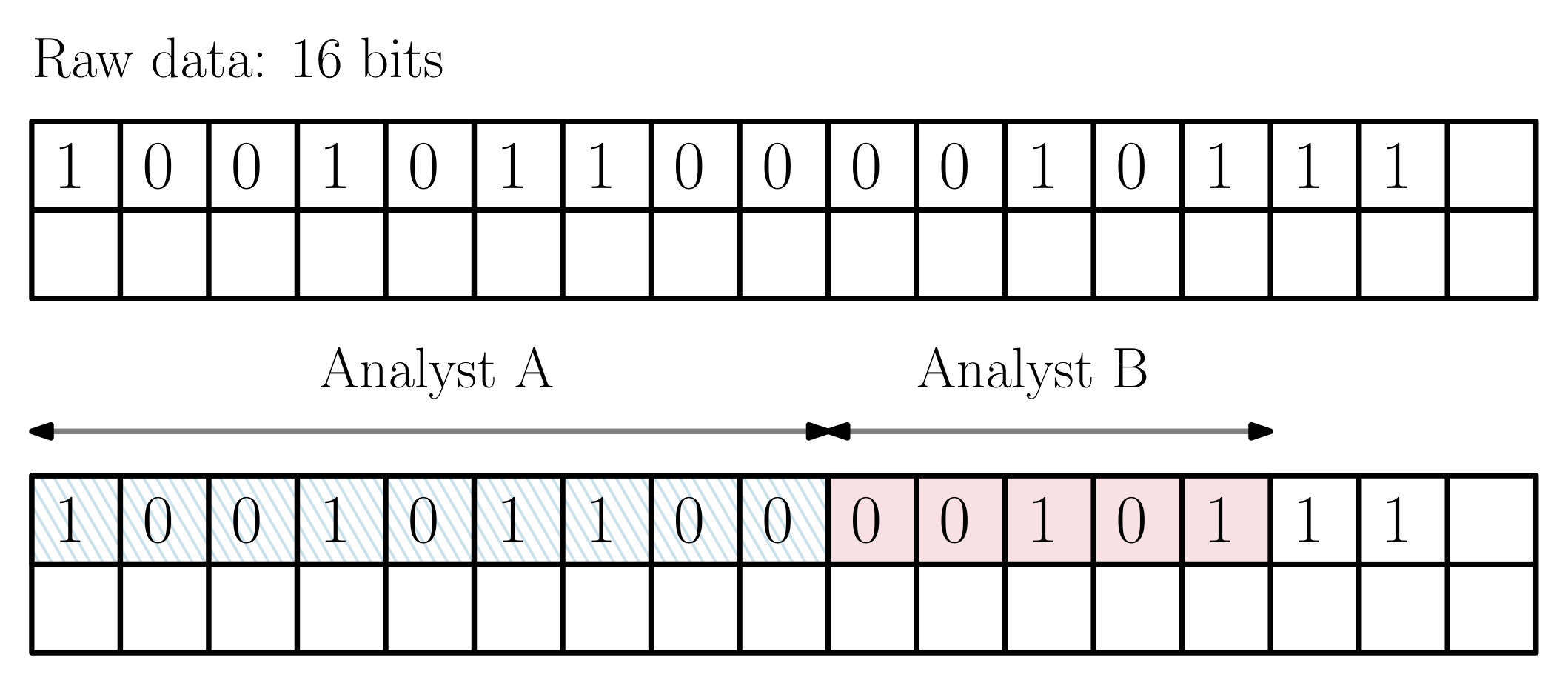

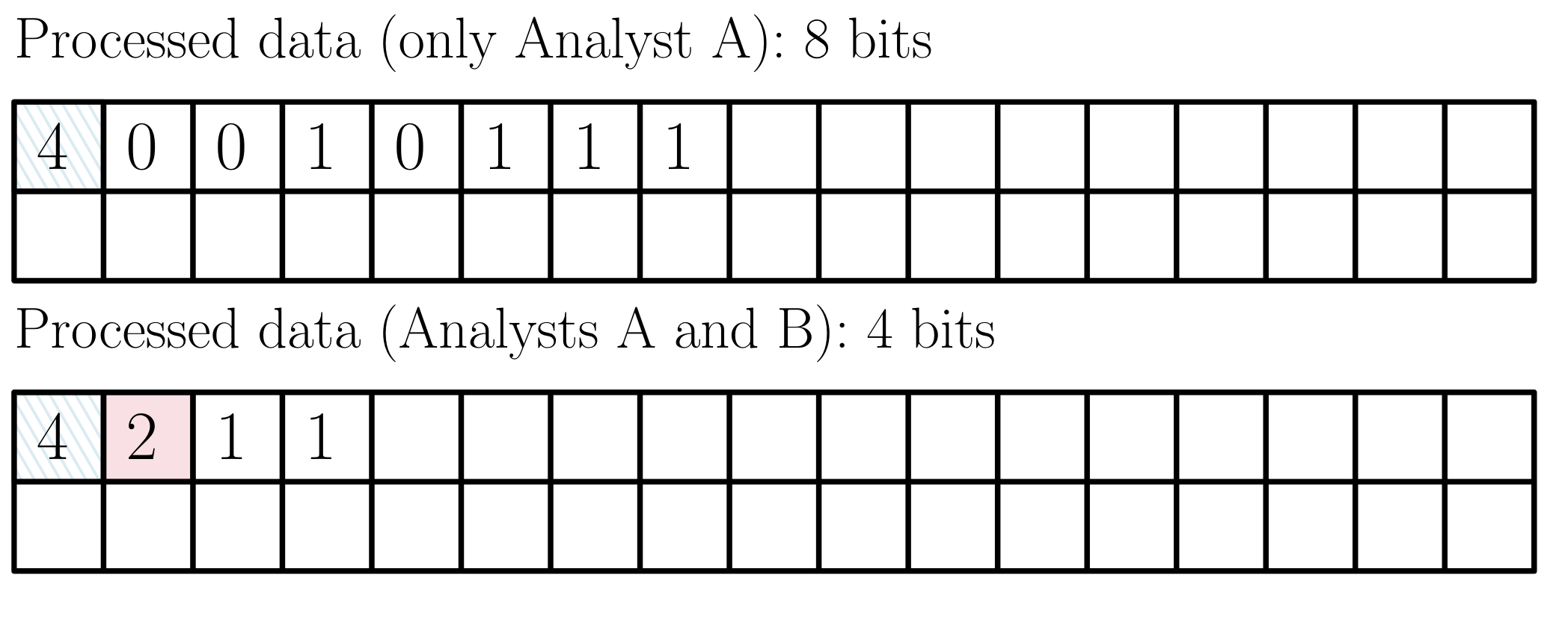

Analyst objective

Maximize trading volume & revenue for brokerage house.

(Groysberg, Healy, and Maber, 2011)

Research question

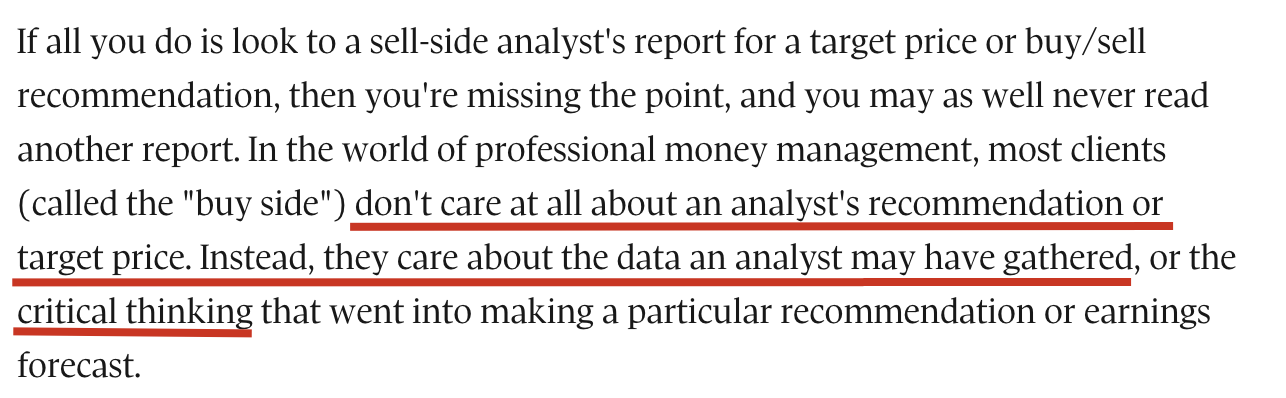

Contributions

Results

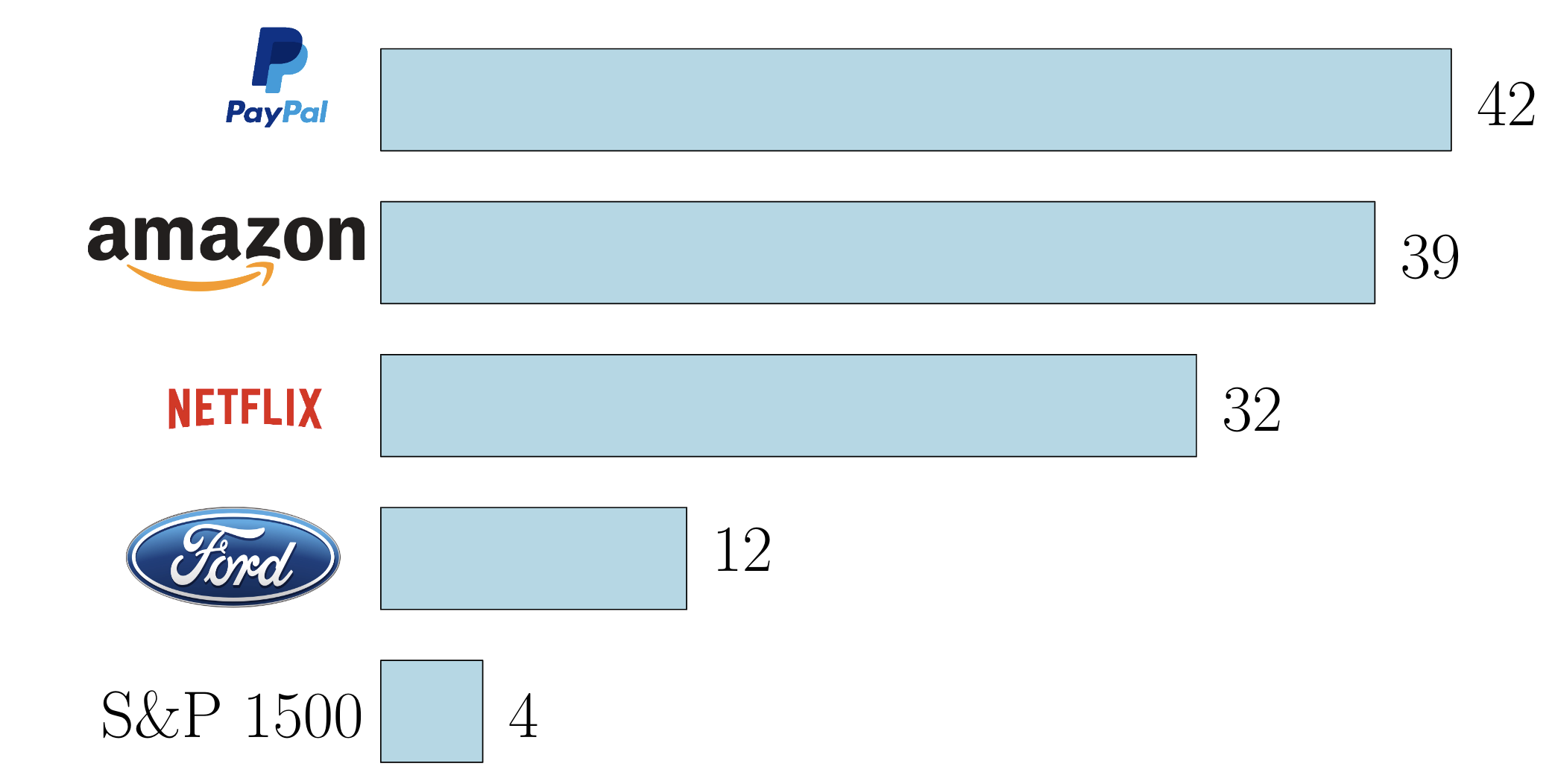

A growing literature shows that investor attention plays an important role in asset pricing at determining, e.g.,:

However, we know little on how investor attention influence information supply in financial markets.

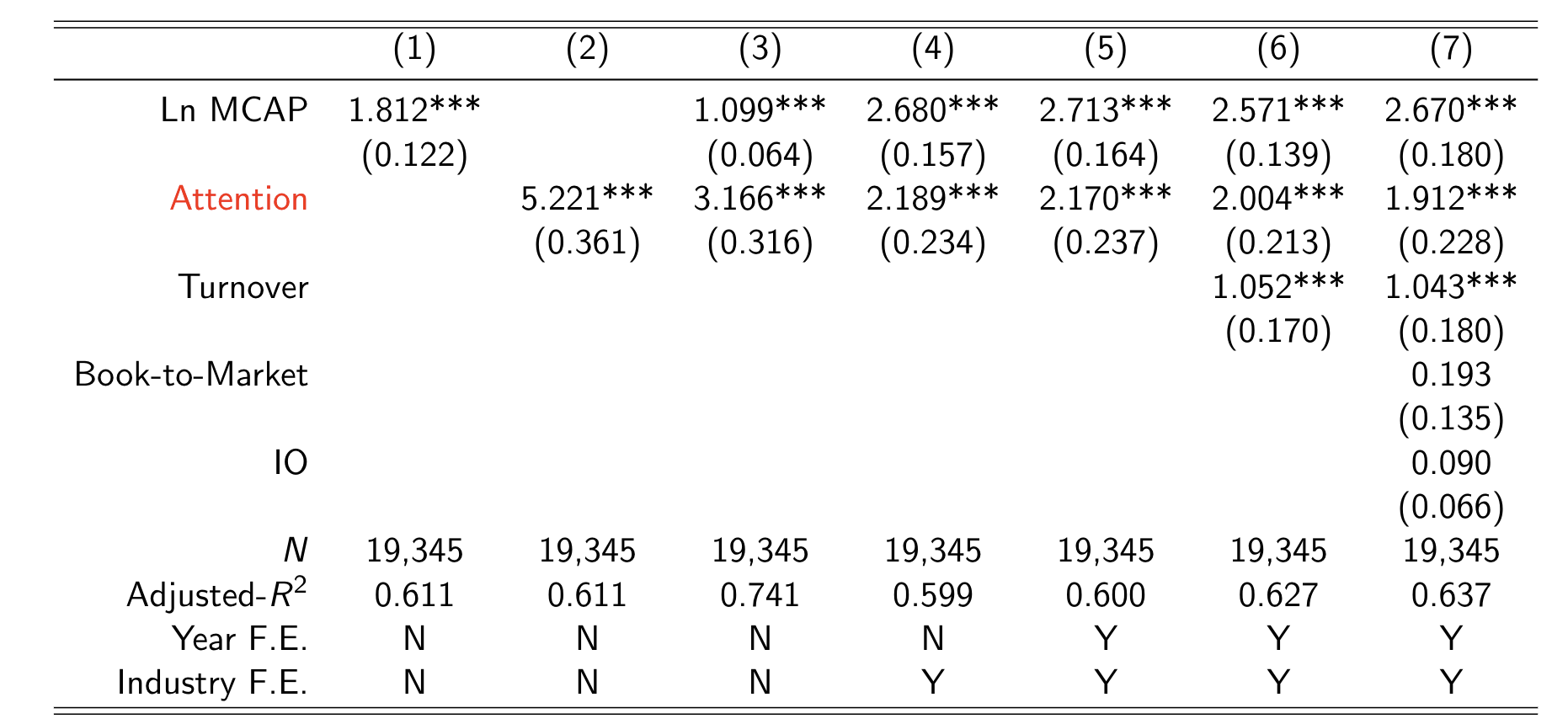

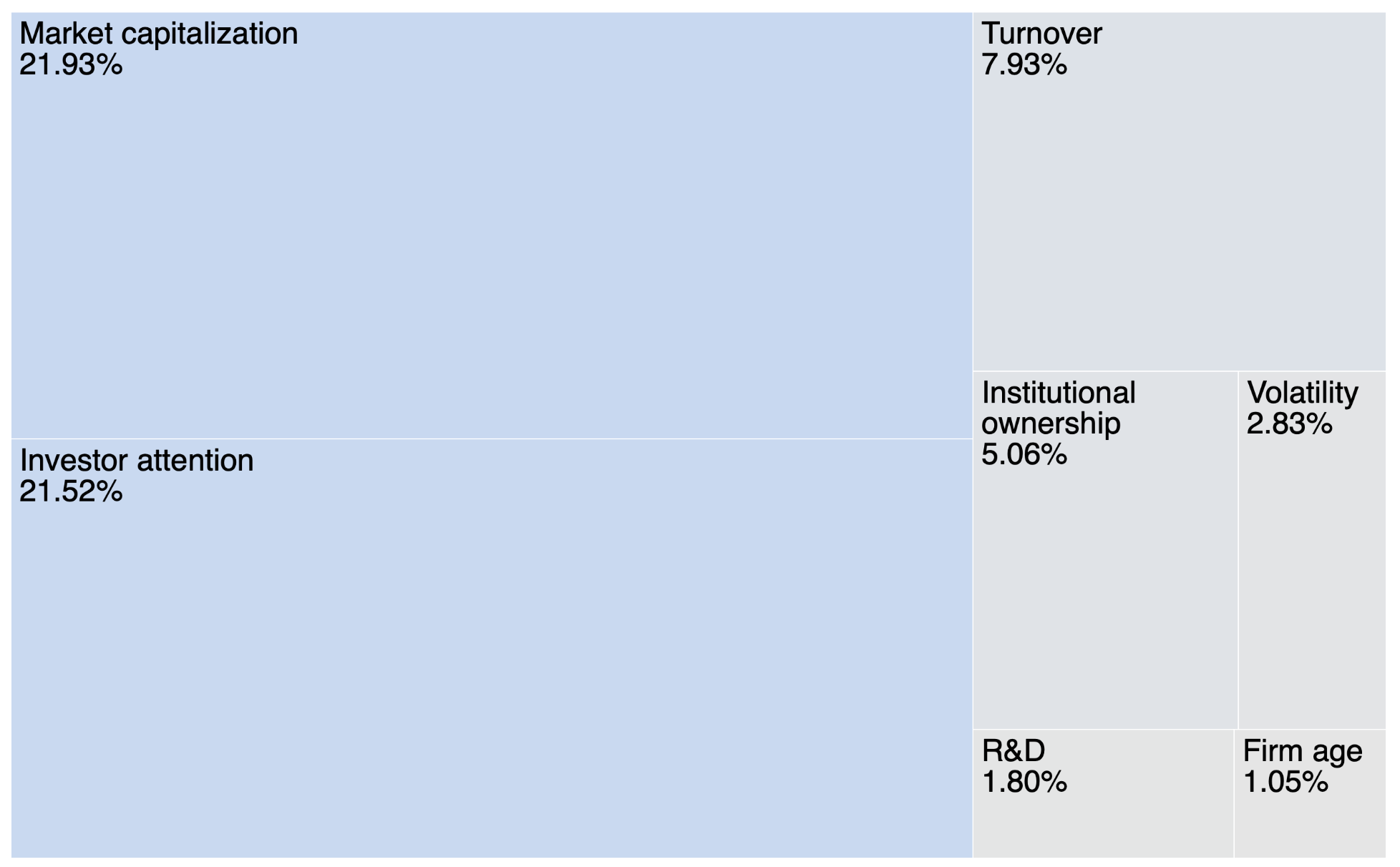

*using Shapley-Owen decomposition

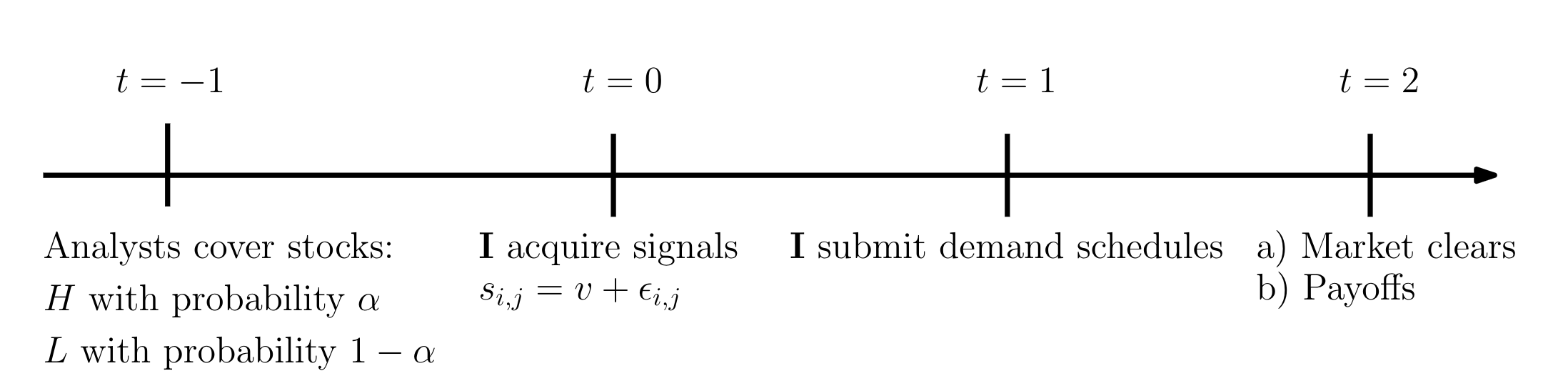

Assets

Two risky-assets in zero net supply, paying off at t=2

1. A high-precision asset H:

2. A low-precision asset L:

Agents

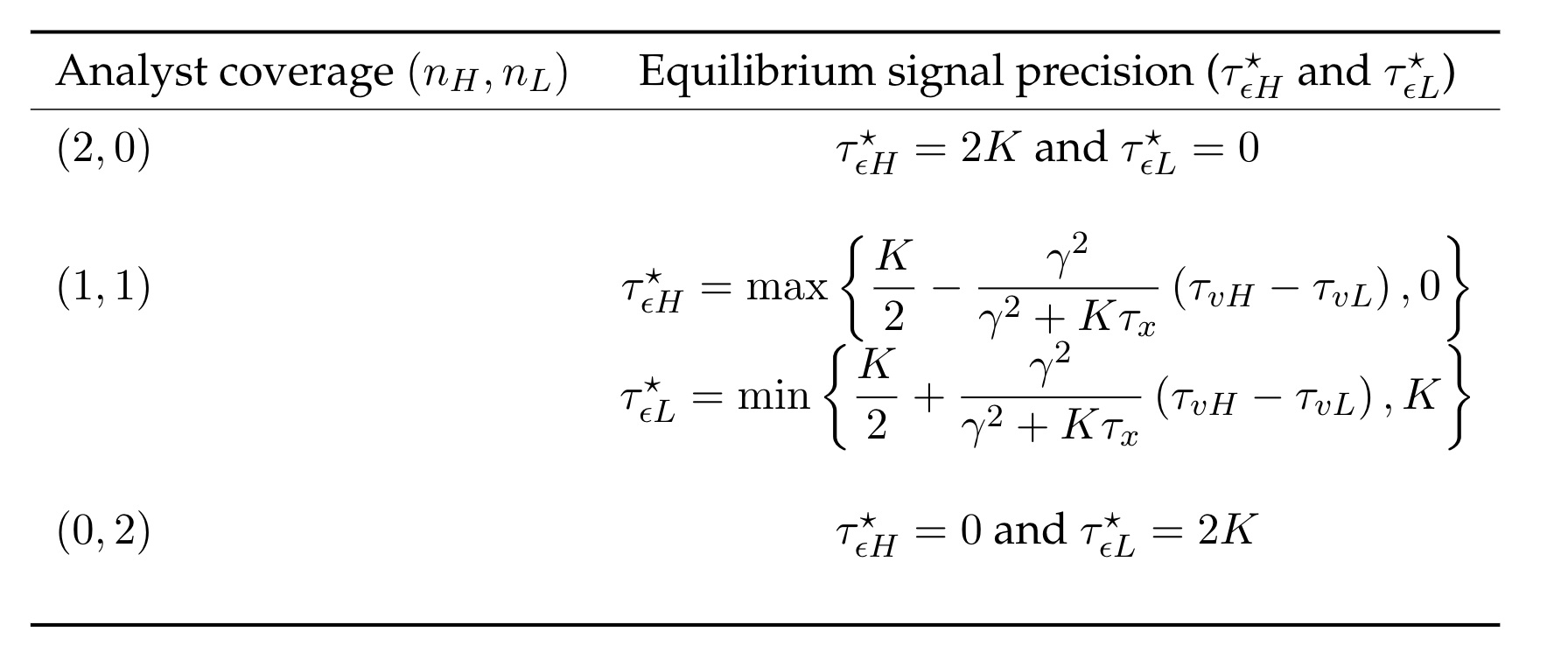

Each investor j can acquire unbiased signals about stock i:

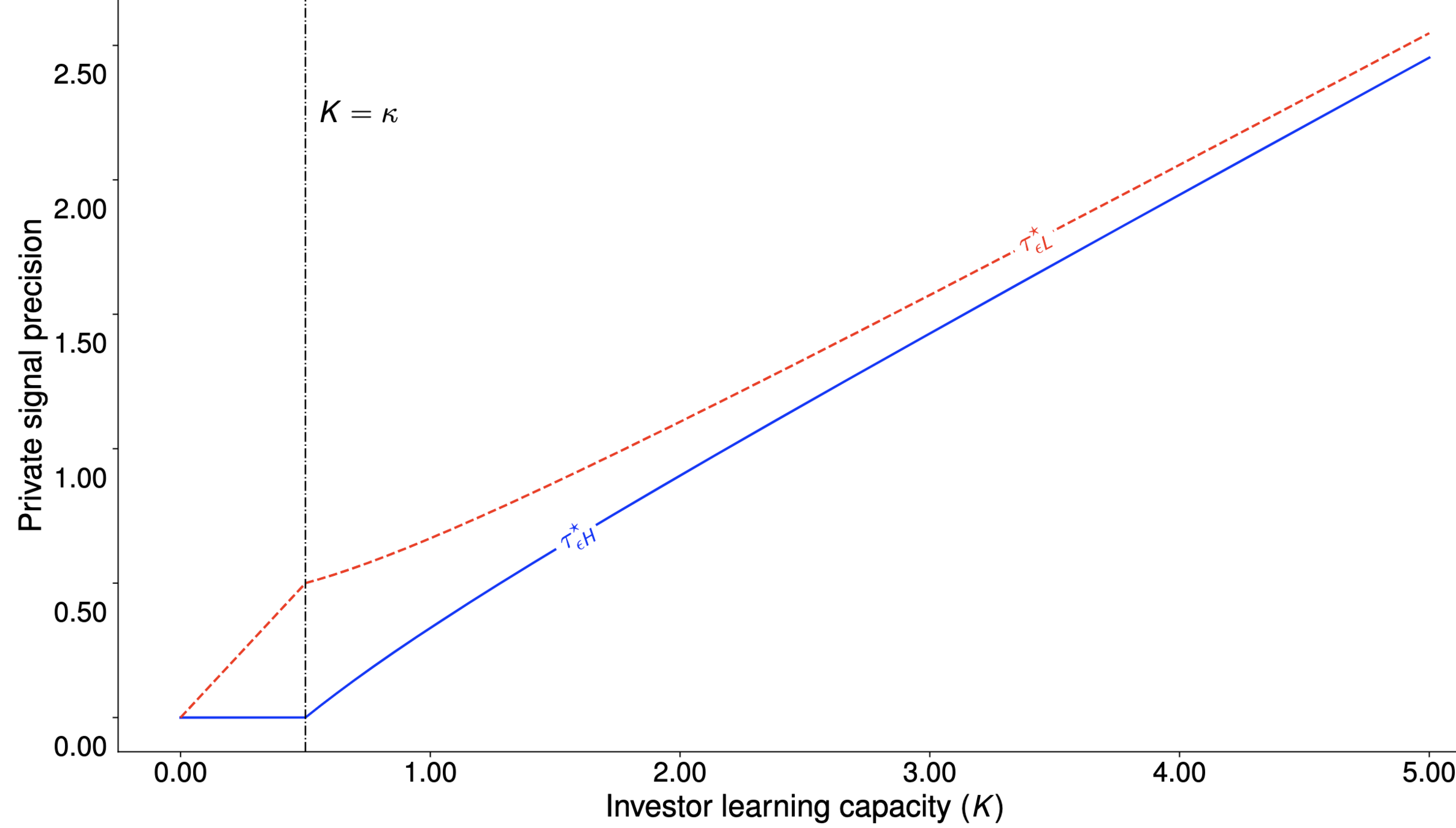

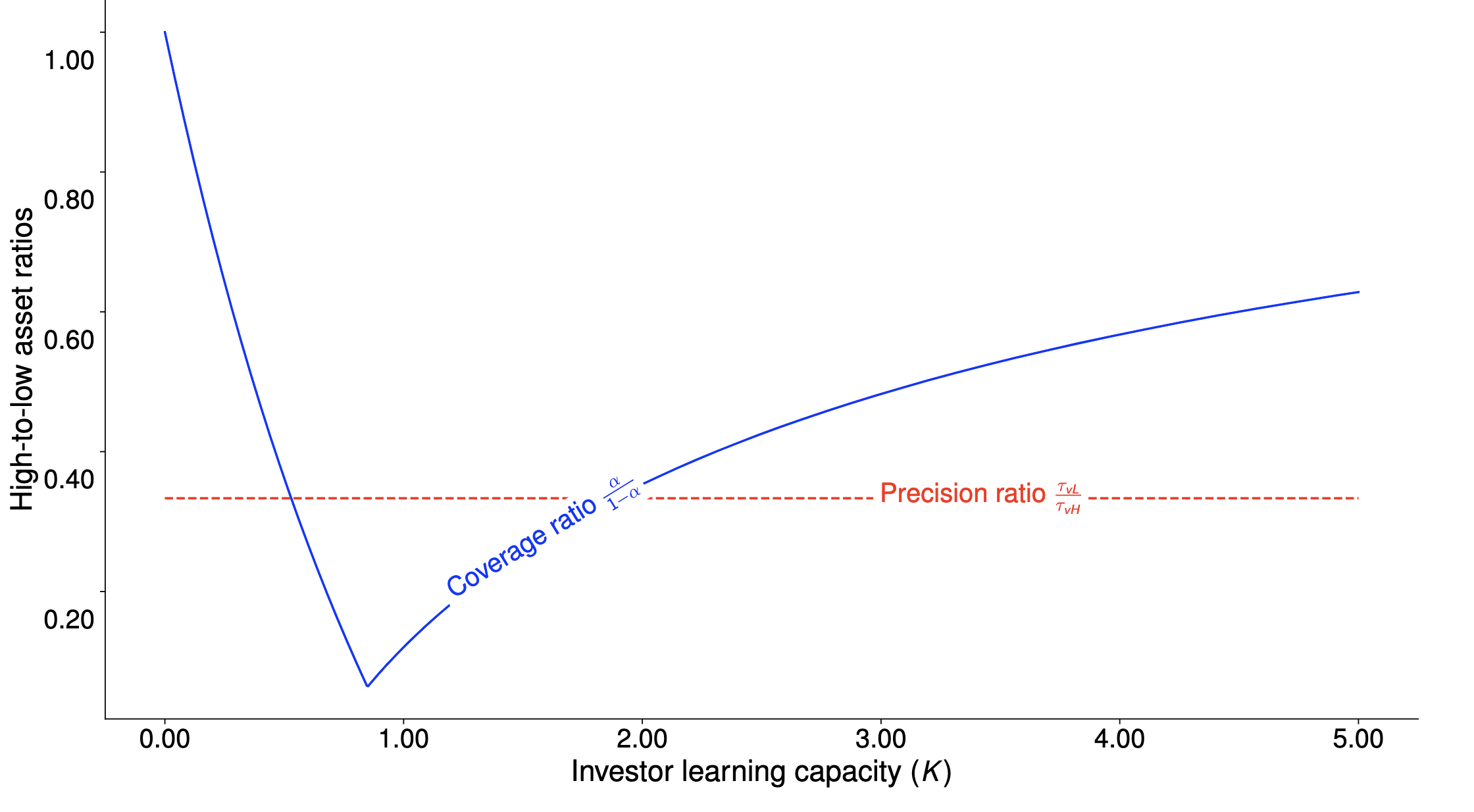

Investors choose the signal precision, but have finite learning (attention) capacity K:

Learning cost is lower if more analysts cover stock i

(through a "familiarity" argument):

(note decreasing returns to scale)

(i) Conjecture linear price:

(ii) Optimal demand from investor j, conditional on signal:

(iii) Market clearing condition:

(iv) Clearing price:

Following Verrecchia (1982), problem boils down to:

Posterior precision

A measure of price impact

Investors have zero mass so take price as given.

Problem becomes:

Text

Attention constraint

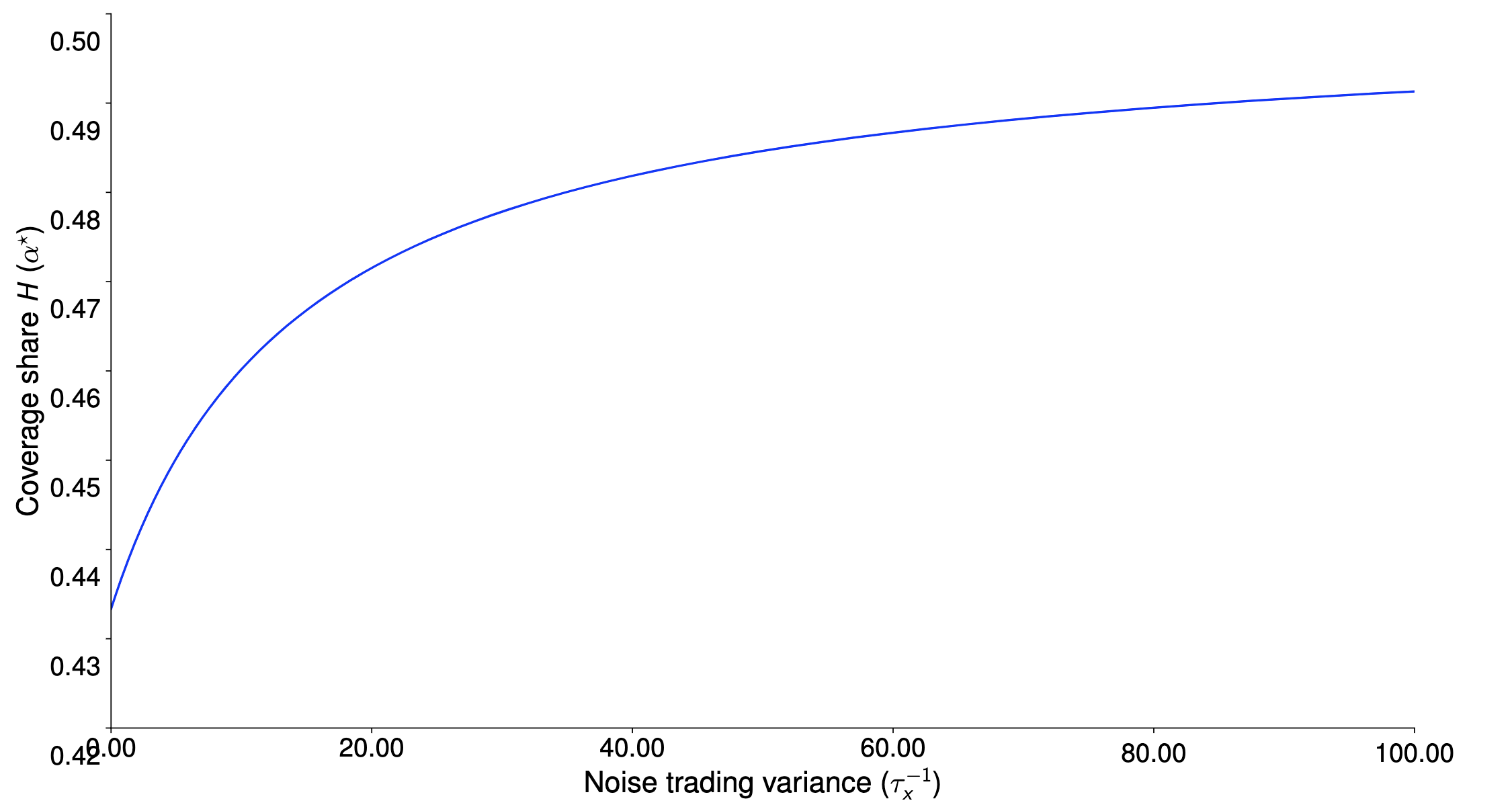

The expected volume in a given stock i is:

Mechanism

If analyst j covers stock H, her utility is:

If analyst j covers stock H, her utility is:

If analyst j covers stock L, her utility is:

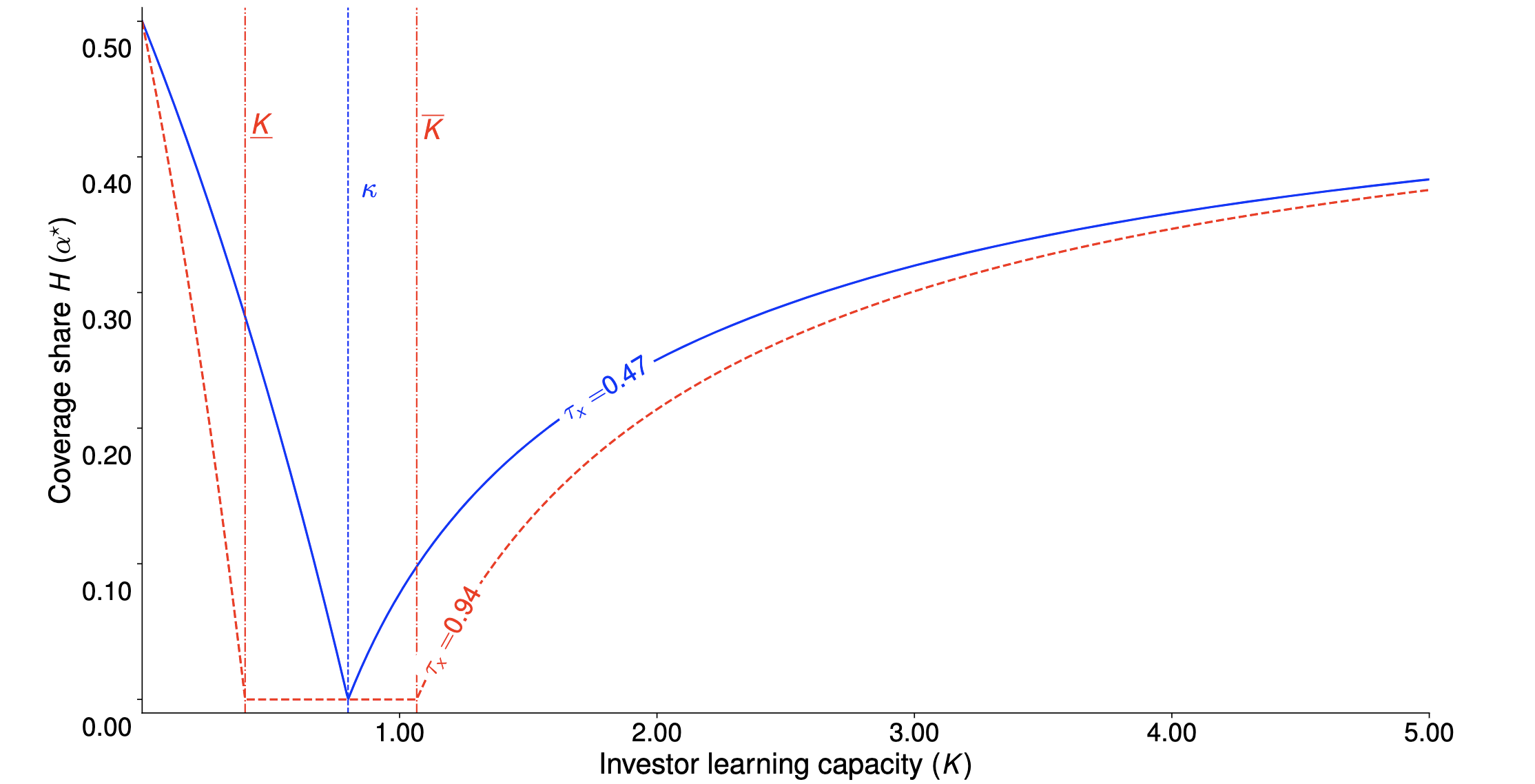

The equilibrium probability to cover stock H is:

Example: If stock L has a payoff variance 3x that of stock $H$, it can have up to 10x more analyst coverage in expectation

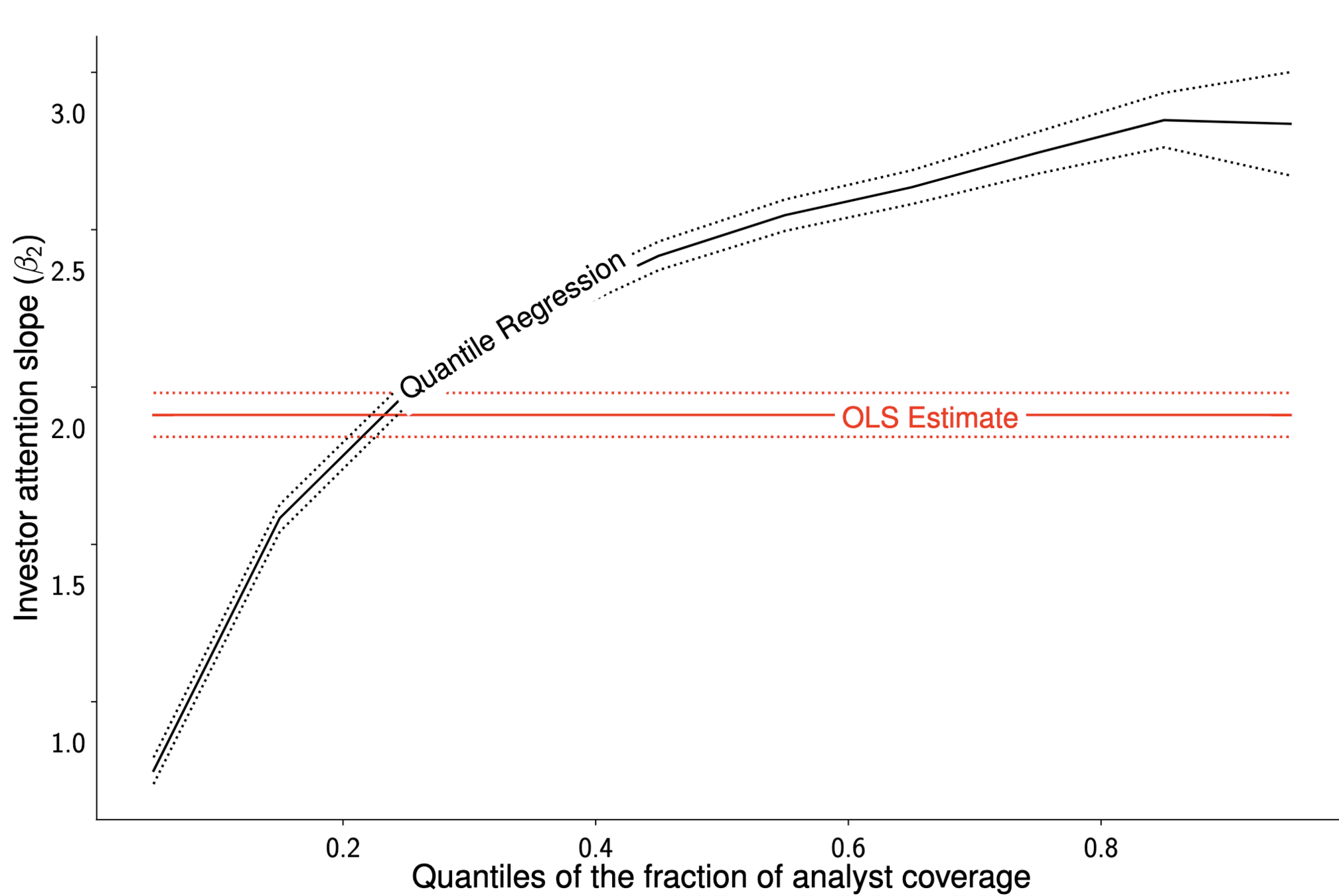

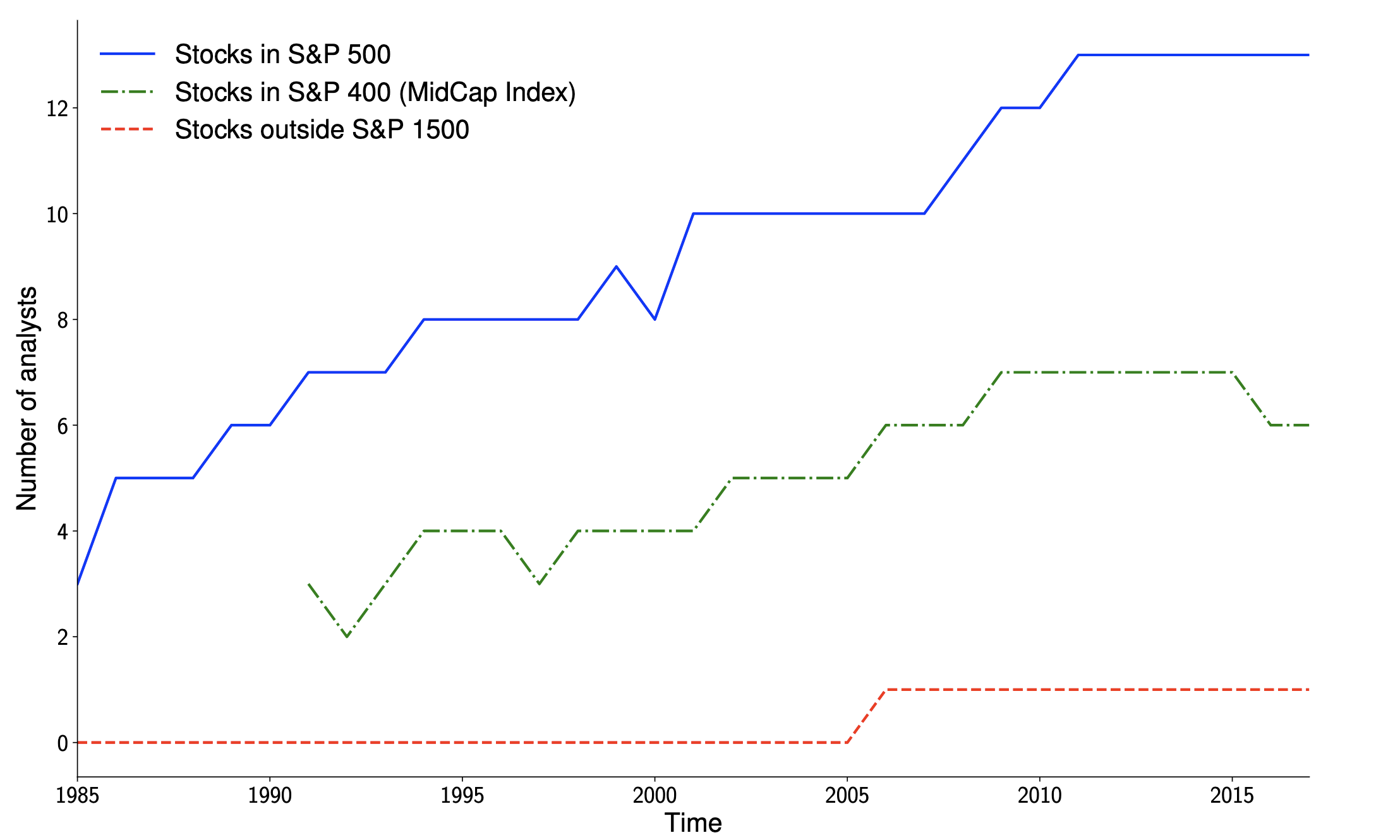

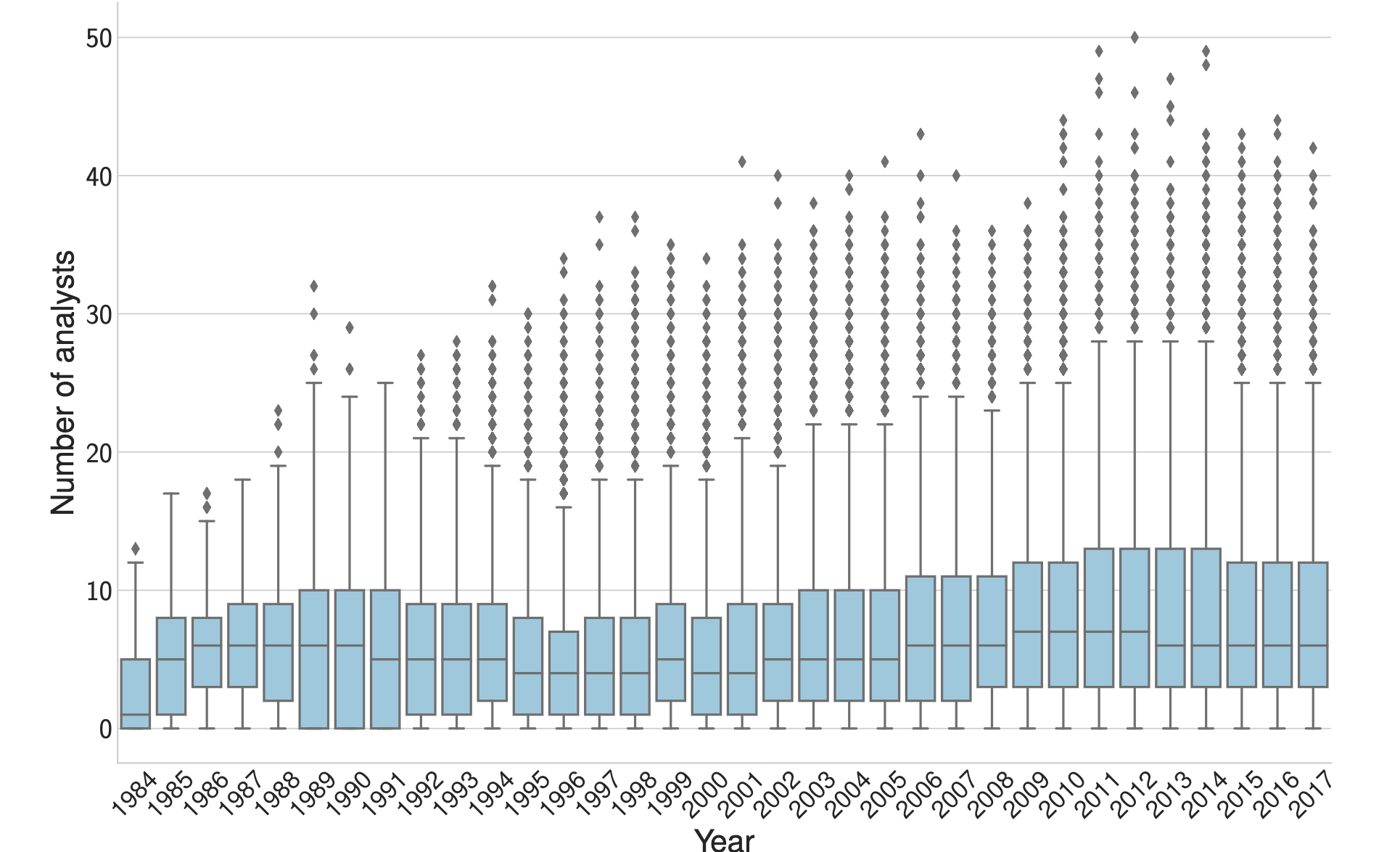

The implications of our model match empirical patterns: the significant analyst coverage clustering in U.S. equities.

By Marius Zoican

Seminar presentation at the Bank of Lithuania on October 16, 2020.