Marius Zoican PRO

I am an Associate Professor of Finance and Canada Research Chair in Financial Technology at the University of Calgary’s Haskayne School of Business. My research sits at the intersection of technology and finance.

Bergman, Kadan, Michaely, and Moulton

Discussion by Marius Zoican

Main findings

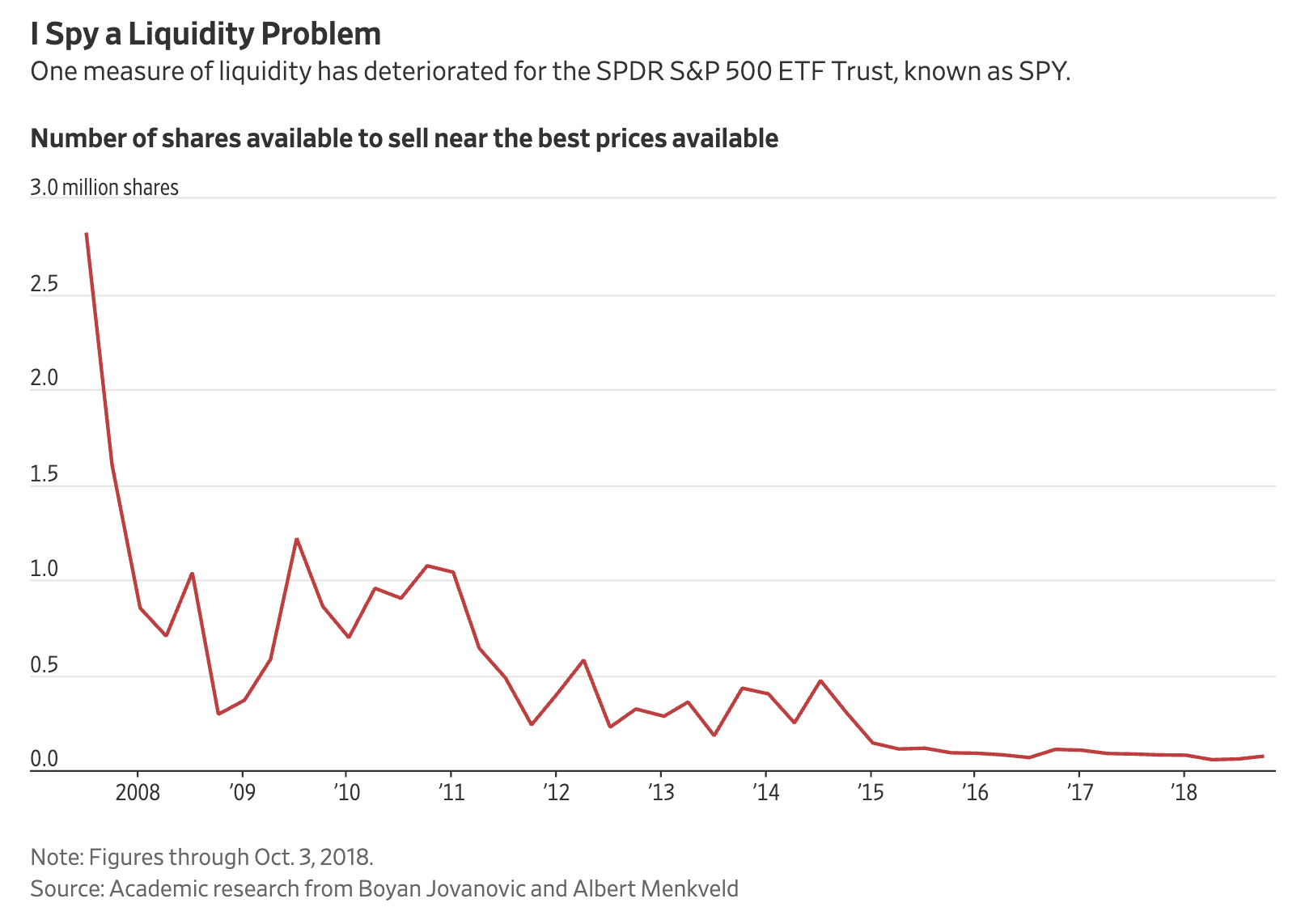

Source: Jovanovic and Menkveld (2020)

we show that the illiquidity of stressed bonds has increased after the Volcker Rule. Dealers regulated by the rule have curtailed their market-making activities and non-Volcker-affected dealers have not offset the decreased activities of Volcker-affected dealers.

(I would like to see more on the implications)

| Price decomposition | Order book data |

|---|---|

| Kalman filter: decompose price in permanent (martingale ) and transitory component (AR process : |

Build an intra-day measure of order book imbalance (e.g., top 5 levels) |

| Do prop traders trade against the sign of ? | Do prop traders buy when there is sell (buy) pressure at the ask (bid)? |

Intermediary Capital Risk Factor and Liquidity

Results on negative returns

Is prop trading activity relatively stable over time?

If yes, wouldn't lagged stock liquidity/volatility be endogenous to prop trader presence? (25% of trading for most stocks)

By Marius Zoican

Discussion of "Do Proprietary Traders Provide Liquidity" by Bergman, Kadan, Michaely, and Moulton