Patrick Power

Economics PhD @ Boston University

Based Largely on Chapter Three of Alex F. Schwartz "Housing Policy in the United States"

"Economics has long chafed at its association with “soft” fields such as philosophy and history and thus spent most of the 20th century trying to imitate the hard sciences by becoming more mathematically rigorous. But this attempt didn’t work, because trying to explain the world via mathematical models is still fundamentally interpretive, requiring crucial assumptions about which factors belong in one’s formula at all. The shift instead plunged economics even deeper into esoteric theorizing and insider jargon."

Incentive

Net Effect

Assets

Libabilities

Bank

Mortgages

Deposits

Liquidity Risk:

Interest Rate Risk:

Key Risks

Maturity Transformation Problem

Home Loan Bank System (1932)

Home Owners Loan Corporation (1933)

Federal Housing Administration (1934)

The Federal National Mortgage Association (1938)

FHA Insured Mortgages

Fannie Mae

Investors

Mortgages

$

Bonds

$

Loans

Securities

Thrifts

Homeowner

Home Loan Bank

Homeowner

Mortgage Company

FHA

FANNIE MAE

Mortgages Prior to 1980

Community Reinvestment Act (1977)

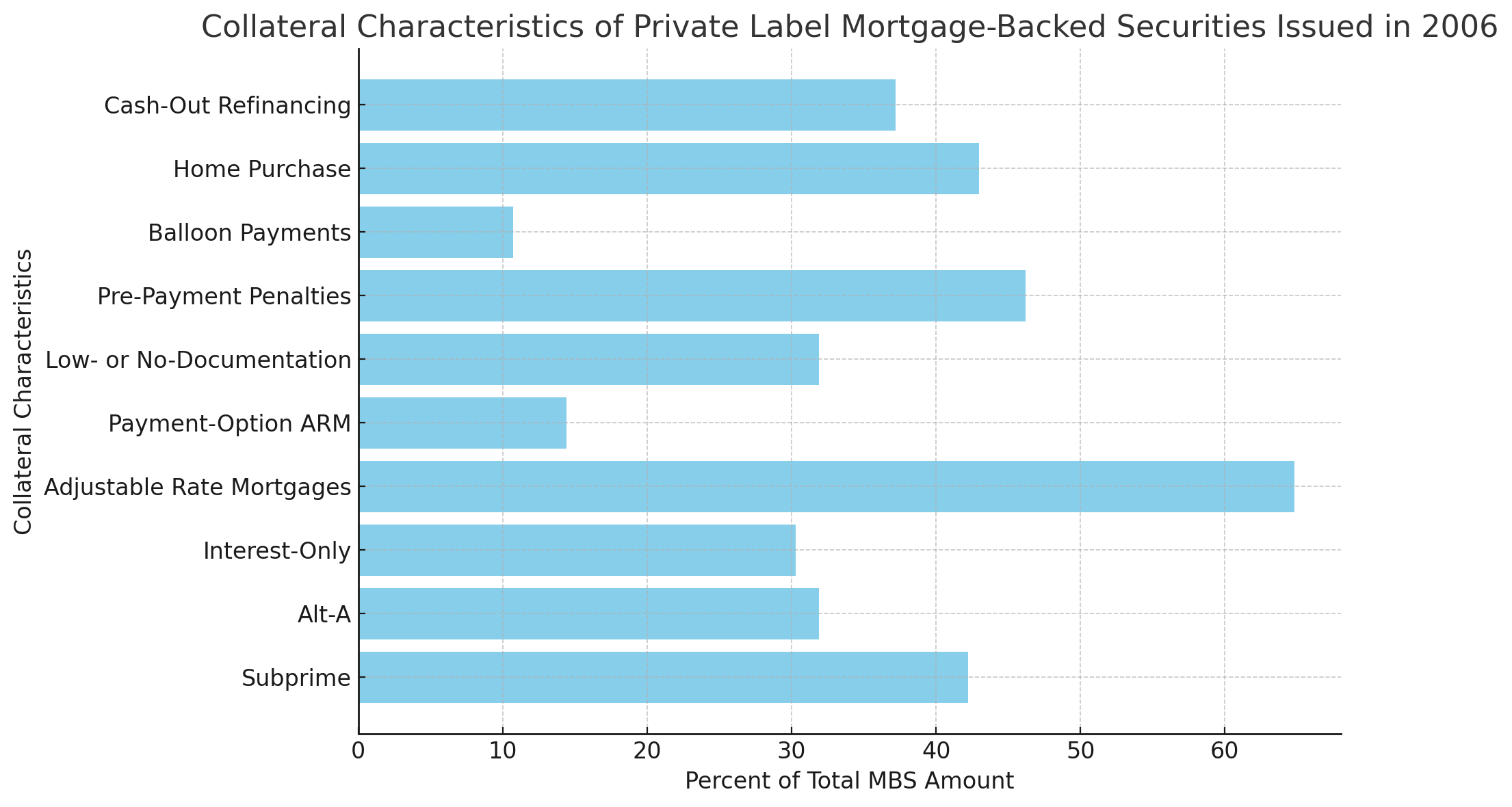

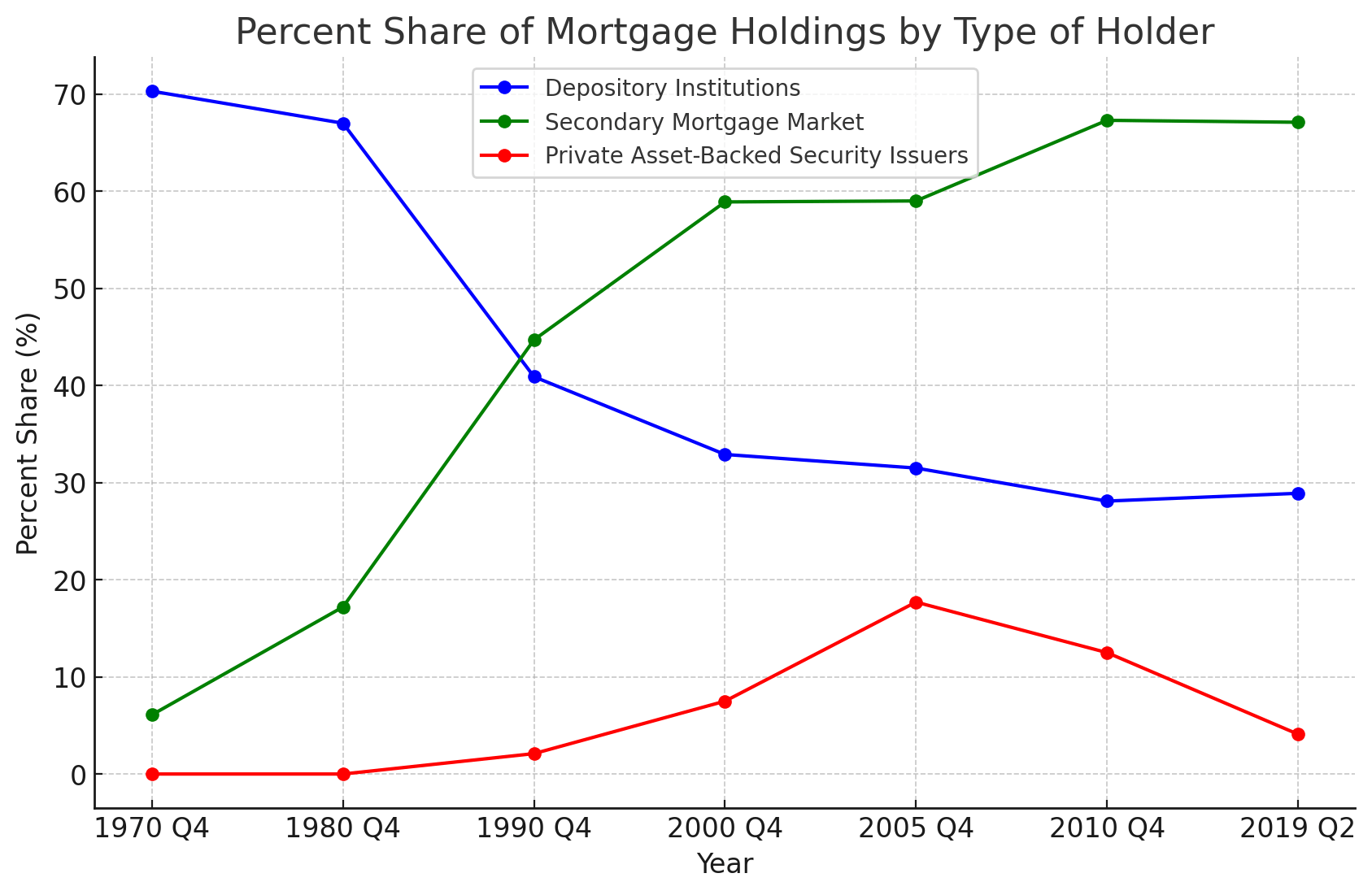

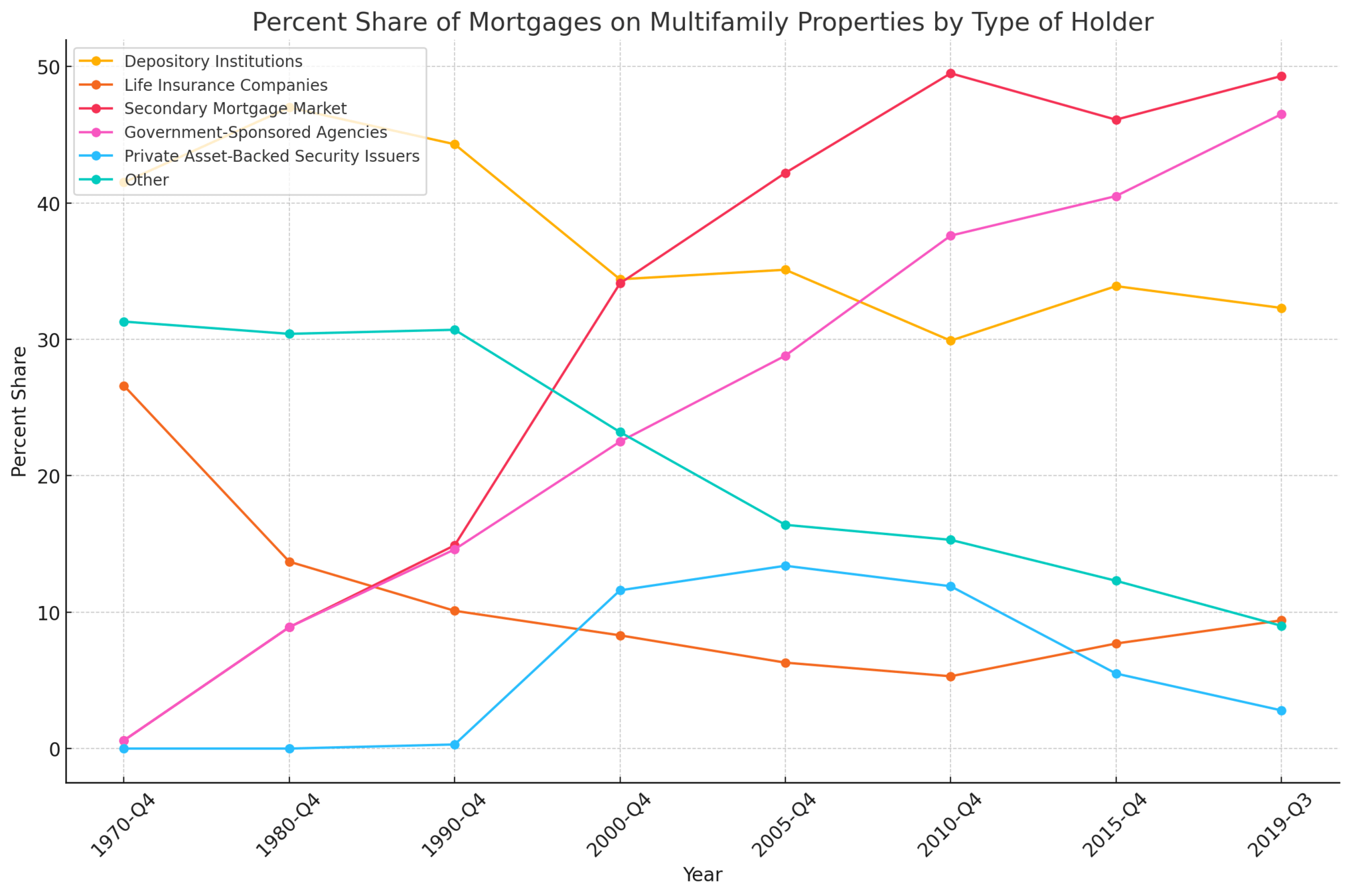

Residential Mortgage Backed Securities

RMBS

Senior Tranche

Mezzanine Tranche

Equity Tranche

Lower Tranches

Subprime Loan

Alt-A Mortgages

Prime Loan

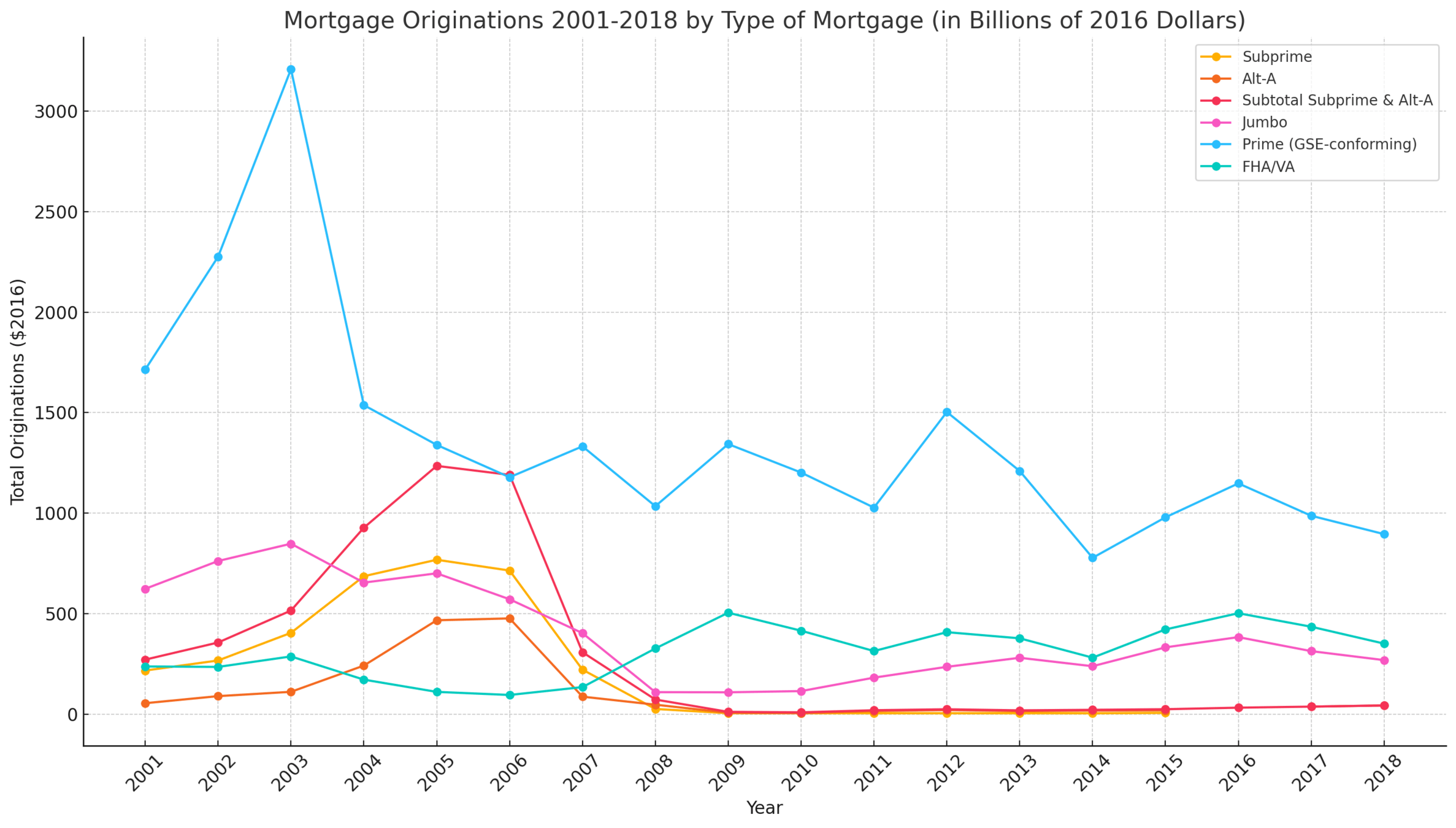

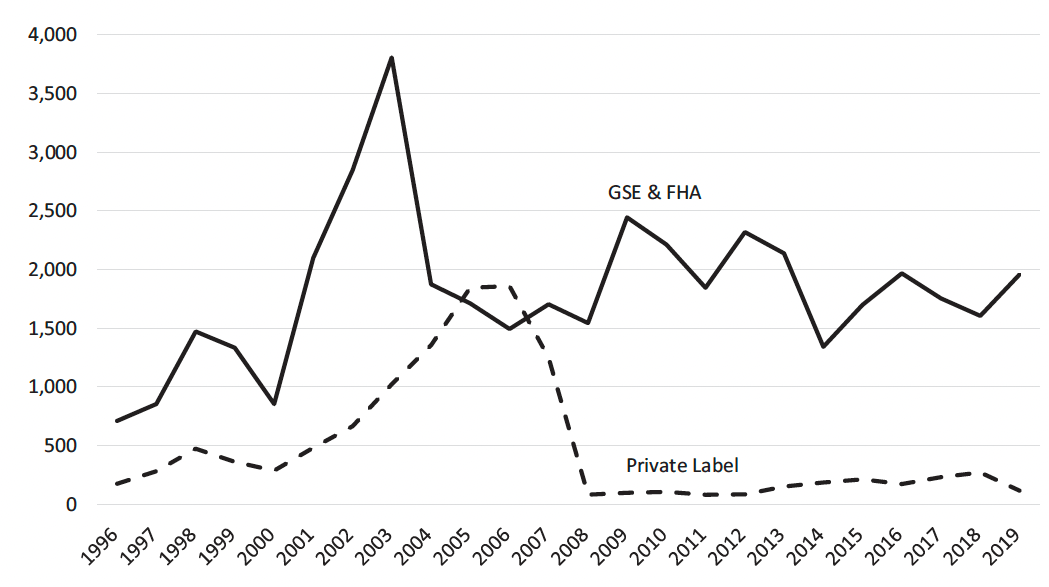

Issuance of mortgage- backed securities, by type, in billions of 2018 dollars

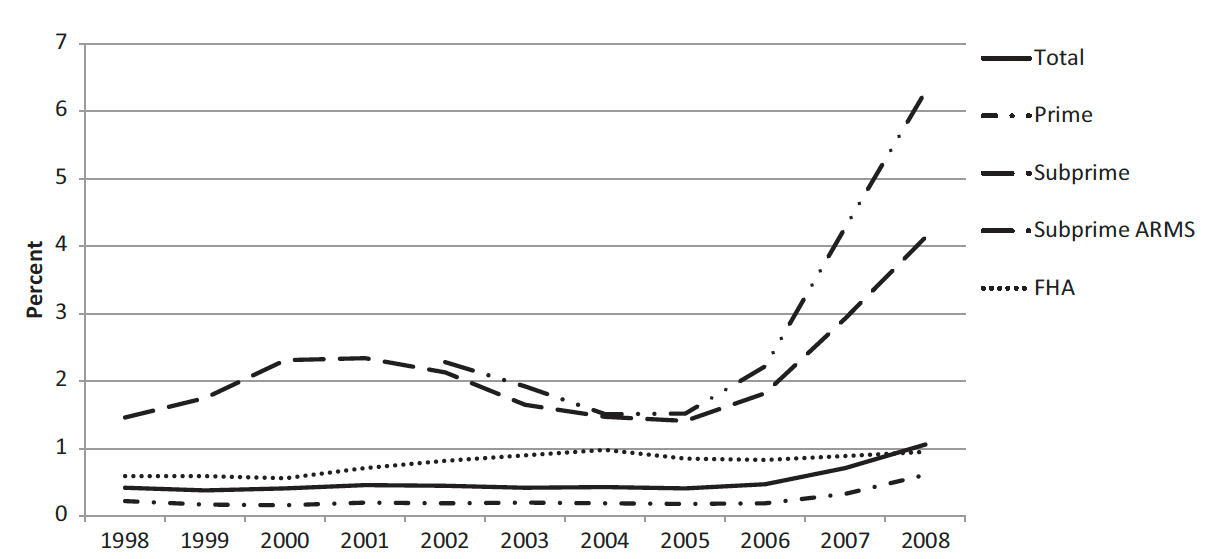

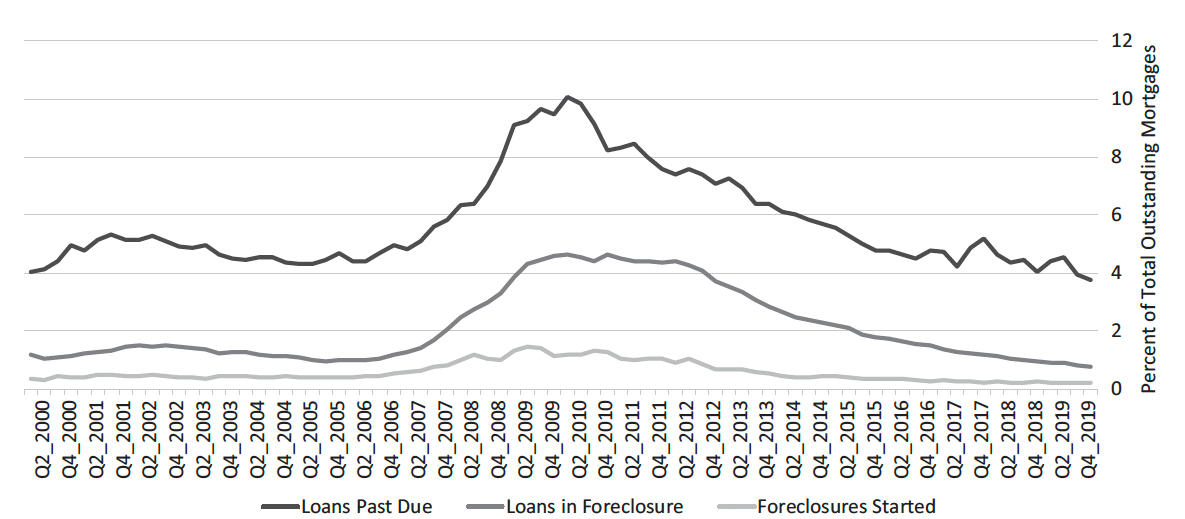

Percent of home mortgages starting foreclosure

Bear Stearns

JPMorgan Chase

Lehman Brothers

Bankruptcy

Merril Lynch

Bank of America

Fannie Mae & Freddie Mac

Conservatorship

Qualified Mortgages (Consumer Financial Protection Bureau)

"Senior tranches received the highest ratings, mezzanine tranches lower ratings, and the equity tranches were not rated at all"

"While mortgages on second homes and investment properties can be restructured in bankruptcy court, mortgages on one’s primary residence cannot"

By Patrick Power