Patrick Power

Economics PhD @ Boston University

This is an augmented presentation of the original paper where I add both my own thoughts and ideas from other articles in addition to the paper under discussion. For a clear understanding of the original paper, please see the original paper.

Financial Distress

Financial Distress

Non-financial Distress

Landlord

Homeowner

Renter

Impact of Foreclosure

"Our most intriguing finding from the credit report data is that foreclosure causes additional financial distress."

Let's Discuss

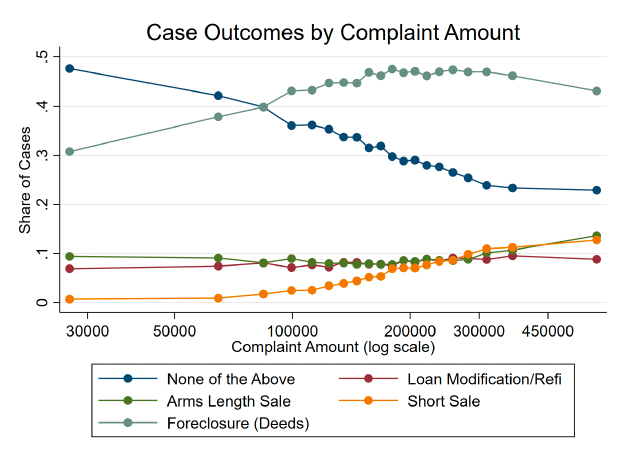

Which Foreclosure Is More Important?

"It turns out that foreclosure in the administrative judicial records and foreclosure in the credit report data are only loosely correlated."

"This may be because while payments and debt amounts are automatically filled from lenders computer systems into credit reports, foreclosures require manual entry on the part of lenders and thus may have more error. This is why many papers that use credit report data to study foreclosure use delinquency measures rather than the foreclosure flag."

Delinquency

Bank Foreclosure

Judge's Decision to Foreclose

Possible Setups

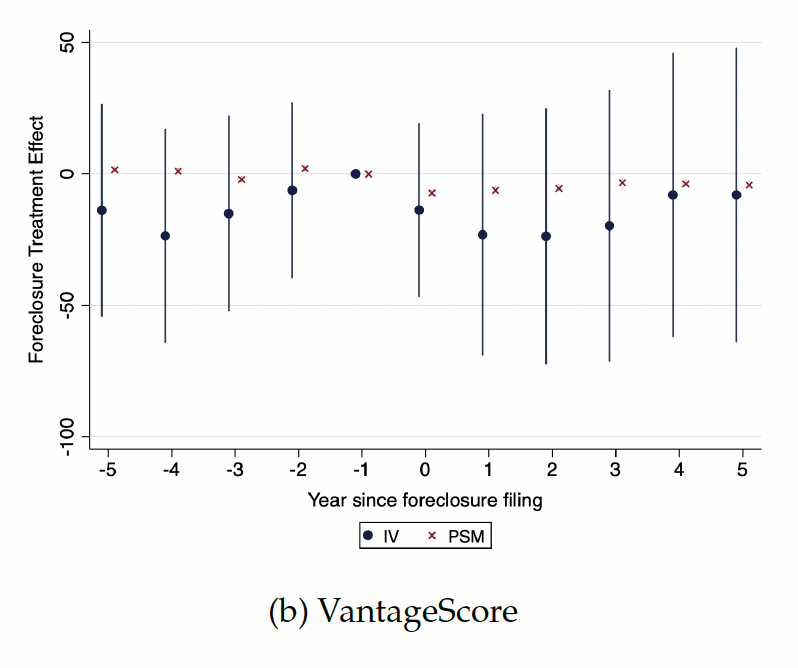

Impact of Judicial Foreclosure on Credit Score

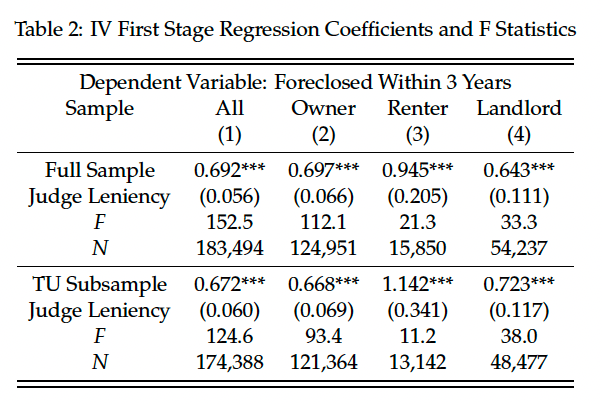

Instrumental Variables

Selection-on-Observables

Judge-IV

Concerns

Judges

Immediate

Outcomes

Downstream

Outcomes

Household

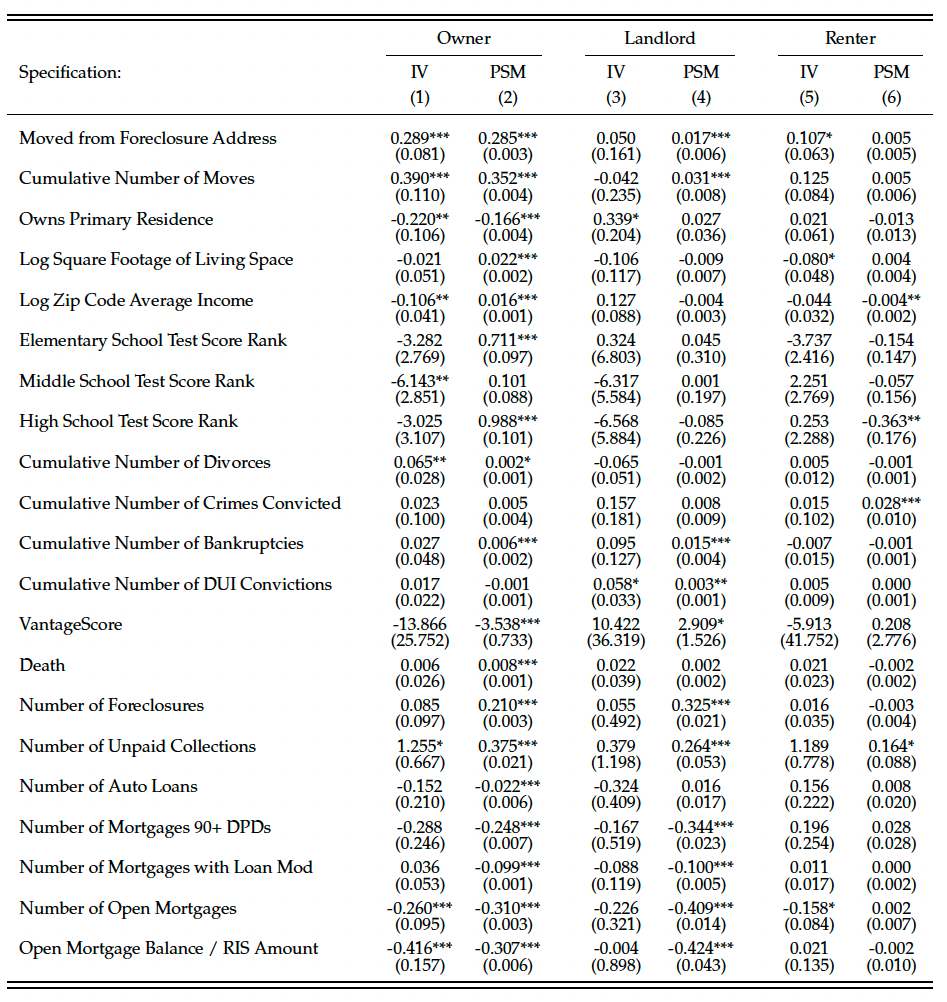

IV v.s. PSM

Context

Proposal

Why this is a bad idea

Does Judge-IV Capture the relevant population in this setting?

"The average foreclosure, however, is in a worse neighborhood and does not have far to fall on the neighborhood quality ladder – and in fact may actually improve neighborhoods after moving out due to regression to the mean."

Let's Discuss

Yes ... but there's an uncertainty that the standard errors of the estimator don't capture

"We next turn to the landlords, for whom we mainly use PSM because of wide confidence intervals for IV."

"The confidence intervals in the reader's mind are generally larger than those reported under the coefficient in a regression table" - Anonymous*

Further Discussion

Re-read the interpretation - What do you think?

These are intended to be helpful to students reading the paper

"We ask whether existing estimates of the social costs of foreclosure are incomplete because they neglect significant non-pecuniary costs."

Comment

Suggestion

"Second, our findings about treatment effect heterogeneity and the significant gaps between marginal and average households implies that different policies may have different implications."

Comment

Suggestion

"For all owners, foreclosure causes housing instability, reduced homeownership, and financial distress including increased delinquency on other debts."

Comment

Suggestion

"The identifying assumption of the PSM approach is that (1) conditional on the propensity score fixed effects, the treatment and control groups have parallel trends"

Comment

"The main disadvantage of the PSM approach is that it assumes selection on the observables"

"In the judge IV context, montonicity is a concern if, for instance, minority judges are more lenient for minority defendants and non-minority judges are more lenient for non-minority defendants. We evaluate the monotonicity assumption extensively in Appendix B.2 and find no evidence of a violation of monotonicity."

Comment

By Patrick Power