Lecture 10: Markov Decision Processes

Shen Shen

April 18, 2025

11am, Room 10-250

Intro to Machine Learning

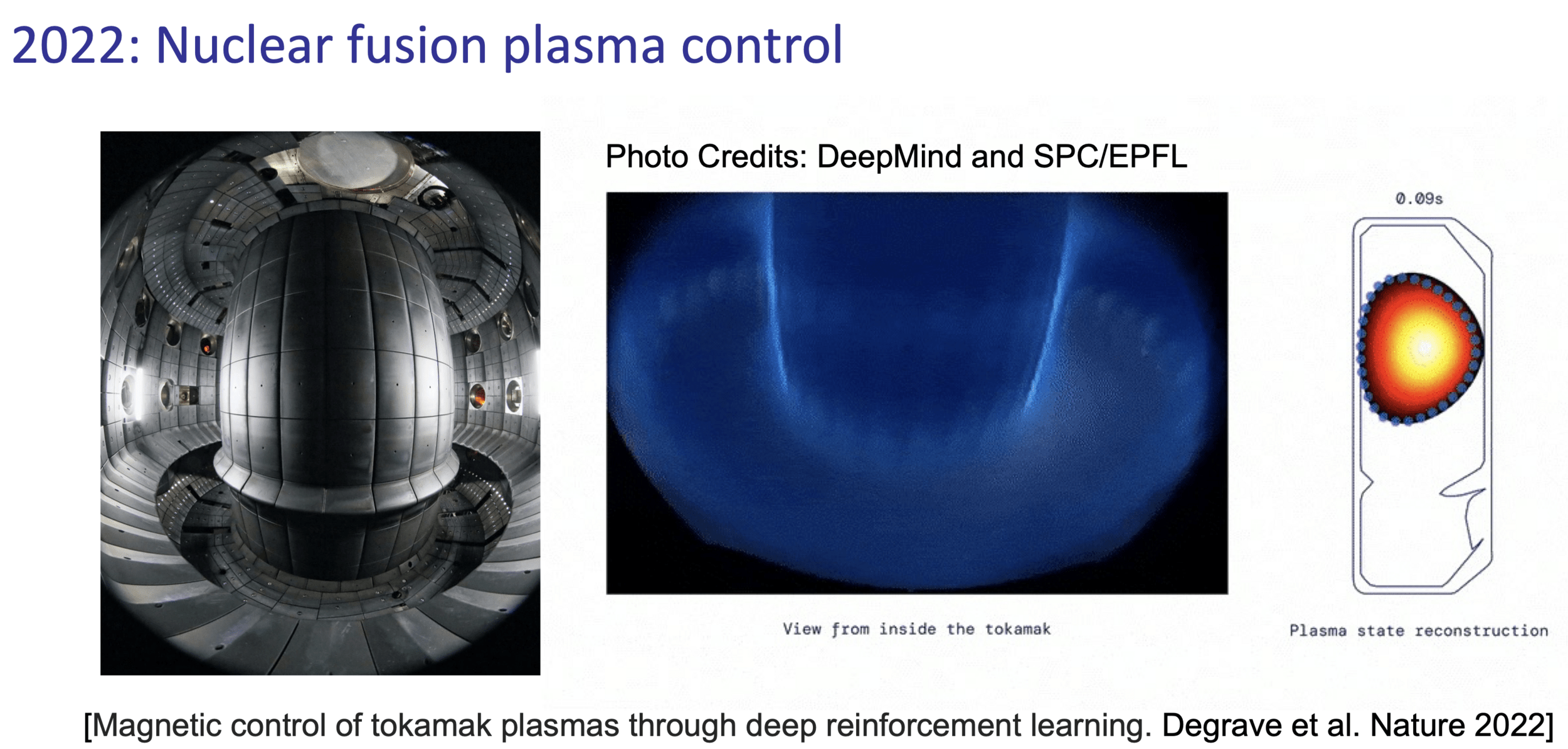

Toddler demo, Russ Tedrake thesis, 2004

(Uses vanilla policy gradient (actor-critic))

Reinforcement Learning with Human Feedback

Outline

- Markov Decision Processes Definition, terminologies, and policy

-

Policy Evaluation

-

State Value Functions \(\mathrm{V}^{\pi}\)

-

Bellman recursions and Bellman equations

-

-

Policy Optimization

-

Optimal policies \(\pi^*\)

-

Optimal action value functions: \(\mathrm{Q}^*\)

-

Value iteration

-

Outline

- Markov Decision Processes Definition, terminologies, and policy

-

Policy Evaluation

-

State Value Functions \(\mathrm{V}^{\pi}\)

-

Bellman recursions and Bellman equations

-

-

Policy Optimization

-

Optimal policies \(\pi^*\)

-

Optimal action value functions: \(\mathrm{Q}^*\)

-

Value iteration

-

Markov Decision Processes

-

Research area initiated in the 50s by Bellman, known under various names:

-

Stochastic optimal control (Control theory)

-

Stochastic shortest path (Operations research)

-

Sequential decision making under uncertainty (Economics)

-

Reinforcement learning (Artificial intelligence, Machine learning)

-

-

A rich variety of accessible and elegant theory, math, algorithms, and applications. But also, considerable variation in notations.

-

We will use the most RL-flavored notations.

- (state, action) results in a transition \(\mathrm{T}\) into a next state:

-

Normally, we get to the “intended” state;

-

E.g., in state (7), action “↑” gets to state (4)

-

-

If an action would take Mario out of the grid world, stay put;

-

E.g., in state (9), “→” gets back to state (9)

-

-

In state (6), action “↑” leads to two possibilities:

-

20% chance to (2)

-

80% chance to (3).

-

-

80\%

20\%

Running example: Mario in a grid-world

- 9 possible states \(s\)

- 4 possible actions \(a\): {Up ↑, Down ↓, Left ←, Right →}

1

1

1

1

-10

-10

-10

-10

reward of (3, \(\downarrow\))

reward of \((3,\uparrow\))

reward of \((6, \downarrow\))

reward of \((6,\rightarrow\))

- (state, action) pairs give rewards:

- in state 3, any action gives reward 1

- in state 6, any action gives reward -10

- any other (state, action) pair gives reward 0

-

discount factor: a scalar that reduces the "worth" of rewards, depending on the timing Mario gets the rewards.

- e.g., say this factor is 0.9. then, for (3, \(\leftarrow\)) pair, Mario gets a reward of 1 at the start of the game; at the 2nd time step, a discounted reward of 0.9; at the 3rd time step, it is further discounted to \((0.9)^2\), and so on.

Mario in a grid-world, cont'd

- \(\mathcal{S}\) : state space, contains all possible states \(s\).

- \(\mathcal{A}\) : action space, contains all possible actions \(a\).

Markov Decision Processes - Definition and terminologies

In 6.390,

- \(\mathcal{S}\) and \(\mathcal{A}\) are small discrete sets, unless otherwise specified.

- \(\mathcal{S}\) : state space, contains all possible states \(s\).

- \(\mathcal{A}\) : action space, contains all possible actions \(a\).

- \(\mathrm{T}\left(s, a, s^{\prime}\right)\) : the probability of transition from state \(s\) to \(s^{\prime}\) when action \(a\) is taken.

Markov Decision Processes - Definition and terminologies

80\%

20\%

\(\mathrm{T}\left(7, \uparrow, 4\right) = 1\)

\(\mathrm{T}\left(9, \rightarrow, 9\right) = 1\)

\(\mathrm{T}\left(6, \uparrow, 3\right) = 0.8\)

\(\mathrm{T}\left(6, \uparrow, 2\right) = 0.2\)

In 6.390,

- \(\mathcal{S}\) and \(\mathcal{A}\) are small discrete sets, unless otherwise specified.

- \(s^{\prime}\) and \(a^{\prime}\) are short-hand for the next-timestep

- \(\mathcal{S}\) : state space, contains all possible states \(s\).

- \(\mathcal{A}\) : action space, contains all possible actions \(a\).

- \(\mathrm{T}\left(s, a, s^{\prime}\right)\) : the probability of transition from state \(s\) to \(s^{\prime}\) when action \(a\) is taken.

- \(\mathrm{R}(s, a)\) : reward, takes in a (state, action) pair and returns a reward.

Markov Decision Processes - Definition and terminologies

reward of \((3,\uparrow\))

reward of \((6,\rightarrow\))

\(\mathrm{R}\left(3, \uparrow \right) = 1\)

\(\mathrm{R}\left(6, \rightarrow \right) = -10\)

In 6.390,

- \(\mathcal{S}\) and \(\mathcal{A}\) are small discrete sets, unless otherwise specified.

- \(s^{\prime}\) and \(a^{\prime}\) are short-hand for the next-timestep

- \(\mathrm{R}(s, a)\) is deterministic and bounded.

- \(\mathcal{S}\) : state space, contains all possible states \(s\).

- \(\mathcal{A}\) : action space, contains all possible actions \(a\).

- \(\mathrm{T}\left(s, a, s^{\prime}\right)\) : the probability of transition from state \(s\) to \(s^{\prime}\) when action \(a\) is taken.

- \(\mathrm{R}(s, a)\) : reward, takes in a (state, action) pair and returns a reward.

- \(\gamma \in [0,1]\): discount factor, a scalar.

- \(\pi{(s)}\) : policy, takes in a state and returns an action.

The goal of an MDP is to find a "good" policy.

Markov Decision Processes - Definition and terminologies

In 6.390,

- \(\mathcal{S}\) and \(\mathcal{A}\) are small discrete sets, unless otherwise specified.

- \(s^{\prime}\) and \(a^{\prime}\) are short-hand for the next-timestep

- \(\mathrm{R}(s, a)\) is deterministic and bounded.

- \(\pi(s)\) is deterministic.

- \(a_t = \pi(s_t)\)

- \(r_t = \mathrm{R}(s_t,a_t)\)

Policy \(\pi(s)\)

Transition \(\mathrm{T}\left(s, a, s^{\prime}\right)\)

Reward \(\mathrm{R}(s, a)\)

time

a trajectory (aka, an experience, or a rollout), of horizon \(h\)

\(\quad \tau=\left(s_0, a_0, r_0, s_1, a_1, r_1, \ldots s_{h-1}, a_{h-1}, r_{h-1}\right)\)

\underbrace{\hspace{4cm}}

initial state

all depends on \(\pi\)

\dots

s_2

s_3

s_4

s_5

a_2

a_3

a_4

r_2

r_3

r_4

s_0

s_1

a_0

a_1

r_0

r_1

s_{h-2}

a_{h-2}

r_{h-2}

s_{h-1}

a_{h-1}

r_{h-1}

- \(\operatorname{Pr}\left(s_t=s^{\prime} \mid s_{t-1}=s, a_{t-1}=a\right)=\mathrm{T}\left(s, a, s^{\prime}\right)\)

Policy \(\pi(s)\)

Transition \(\mathrm{T}\left(s, a, s^{\prime}\right)\)

Reward \(\mathrm{R}(s, a)\)

time

\dots

s_2

s_3

s_4

s_5

a_2

a_3

a_4

r_2

r_3

r_4

s_0

s_1

a_0

a_1

r_0

r_1

s_{h-2}

a_{h-2}

r_{h-2}

s_{h-1}

a_{h-1}

r_{h-1}

Starting in a given \(s_0\), how "good" is it to follow a policy \(\pi\) for \(h\) time steps?

\mathrm{R}(s_0, a_0)

\gamma \mathrm{R}(s_1, a_1)

\gamma^3\mathrm{R}(s_3, a_3)

\gamma^2 \mathrm{R}(s_2, a_2)

\dots

+

+

+

+

\gamma^{h-1}\mathrm{R}(s_{h-1}, a_{h-1})

+

One idea:

Policy \(\pi(s)\)

Transition \(\mathrm{T}\left(s, a, s^{\prime}\right)\)

Reward \(\mathrm{R}(s, a)\)

time

\dots

s_2

s_3

s_4

s_5

a_2

a_3

a_4

r_2

r_3

r_4

s_0

s_1

a_0

a_1

r_0

r_1

s_{h-2}

a_{h-2}

r_{h-2}

s_{h-1}

a_{h-1}

r_{h-1}

Starting in a given \(s_0\), how "good" is it to follow a policy \(\pi\) for \(h\) time steps?

But in

Mario game:

80\%

20\%

??

\mathrm{R}(s_0, a_0)

\gamma \mathrm{R}(s_1, a_1)

\gamma^3\mathrm{R}(s_3, a_3)

\gamma^2 \mathrm{R}(s_2, a_2)

\dots

+

+

+

+

\gamma^{h-1}\mathrm{R}(s_{h-1}, a_{h-1})

+

One idea:

-10

\uparrow

6

if start at \(s_0=6\) and policy \(\pi(s) =\uparrow, \forall s\), i.e., always up

\mathrm{R}(s_0, a_0)

\gamma \mathrm{R}(s_1, a_1)

\gamma^3\mathrm{R}(s_3, a_3)

\gamma^2 \mathrm{R}(s_2, a_2)

\dots

+

+

+

+

\gamma^{h-1}\mathrm{R}(s_{h-1}, a_{h-1})

+

\mathbb{E}[

]

in 390, this expectation is only w.r.t. the transition probabilities \(\mathrm{T}\left(s, a, s^{\prime}\right)\)

\( h\) terms

\underbrace{\hspace{7.6cm}}

Policy \(\pi(s)\)

Transition \(\mathrm{T}\left(s, a, s^{\prime}\right)\)

Reward \(\mathrm{R}(s, a)\)

time

\dots

s_2

s_3

s_4

s_5

a_2

a_3

a_4

r_2

r_3

r_4

s_0

s_1

a_0

a_1

r_0

r_1

s_{h-2}

a_{h-2}

r_{h-2}

s_{h-1}

a_{h-1}

r_{h-1}

Starting in a given \(s_0\), how "good" is it to follow a policy \(\pi\) for \(h\) time steps?

Outline

- Markov Decision Processes Definition, terminologies, and policy

-

Policy Evaluation

-

State Value Functions \(\mathrm{V}^{\pi}\)

-

Bellman recursions and Bellman equations

-

-

Policy Optimization

-

Optimal policies \(\pi^*\)

-

Optimal action value functions: \(\mathrm{Q}^*\)

-

Value iteration

-

Definition: For a given policy \(\pi(s),\) the state value functions

\(\mathrm{V}_h^\pi(s):=\mathbb{E}\left[\sum_{t=0}^{h-1} \gamma^t \mathrm{R}\left(s_t, \pi\left(s_t\right)\right) \mid s_0=s, \pi\right], \forall s, h\)

- value functions \(\mathrm{V}_h^\pi(s)\): the expected sum of discounted rewards, starting in state \(s,\) and follow policy \(\pi\) for \(h\) steps.

- horizon-0 values defined as 0.

- value is long-term, reward is short-term (one-time).

\mathrm{R}(s_0, a_0)

\gamma \mathrm{R}(s_1, a_1)

\gamma^3\mathrm{R}(s_3, a_3)

\gamma^2 \mathrm{R}(s_2, a_2)

\dots

+

+

+

+

\gamma^{h-1}\mathrm{R}(s_{h-1}, a_{h-1})

+

\mathbb{E}[

]

expanded form

\mathbb{E}[

]

\( h\) terms

\underbrace{\hspace{4cm}}

evaluate the "\(\pi(s) = \uparrow\), for all \(s,\) i.e. the always \(\uparrow\)" policy

\mathrm{R}(s_0, a_0)

\gamma \mathrm{R}(s_1, a_1)

\gamma^2 \mathrm{R}(s_2, a_2)

\dots

+

+

+

horizon \(h\) = 0: no step left

\mathrm{V}^{\uparrow}_0(s) = 0

horizon \(h\) = 1: receive the rewards

\mathrm{V}^{\uparrow}_1(s) = \mathrm{R}(s, \uparrow)

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

1

-10

states and

one special transition:

rewards

- \(\pi(s) = ``\uparrow",\ \forall s\)

- \(\gamma = 0.9\)

80\%

20\%

0

0

\mathrm{R}(1, \uparrow) + \gamma \mathrm{R}(1, \uparrow)

0

\mathrm{R}(2, \uparrow) + \gamma \mathrm{R}(2, \uparrow)

1.9

\mathrm{R}(3, \uparrow) + \gamma \mathrm{R}(3, \uparrow)

0

\mathrm{R}(4, \uparrow) + \gamma \mathrm{R}(1, \uparrow)

= 1 + 0.9 *(1) = 1.9

\mathrm{R}(5, \uparrow) + \gamma \mathrm{R}(2, \uparrow)

\mathrm{V}^{\uparrow}_2(s) =

horizon \(h = 2:\)

\mathbb{E}[

]

\mathrm{R}(s_0, a_0)

\gamma\mathrm{R}(s_1, a_1)

+

\( 2\) terms inside

states and

one special transition:

rewards

- \(\pi(s) = ``\uparrow",\ \forall s\)

- \(\gamma = 0.9\)

80\%

20\%

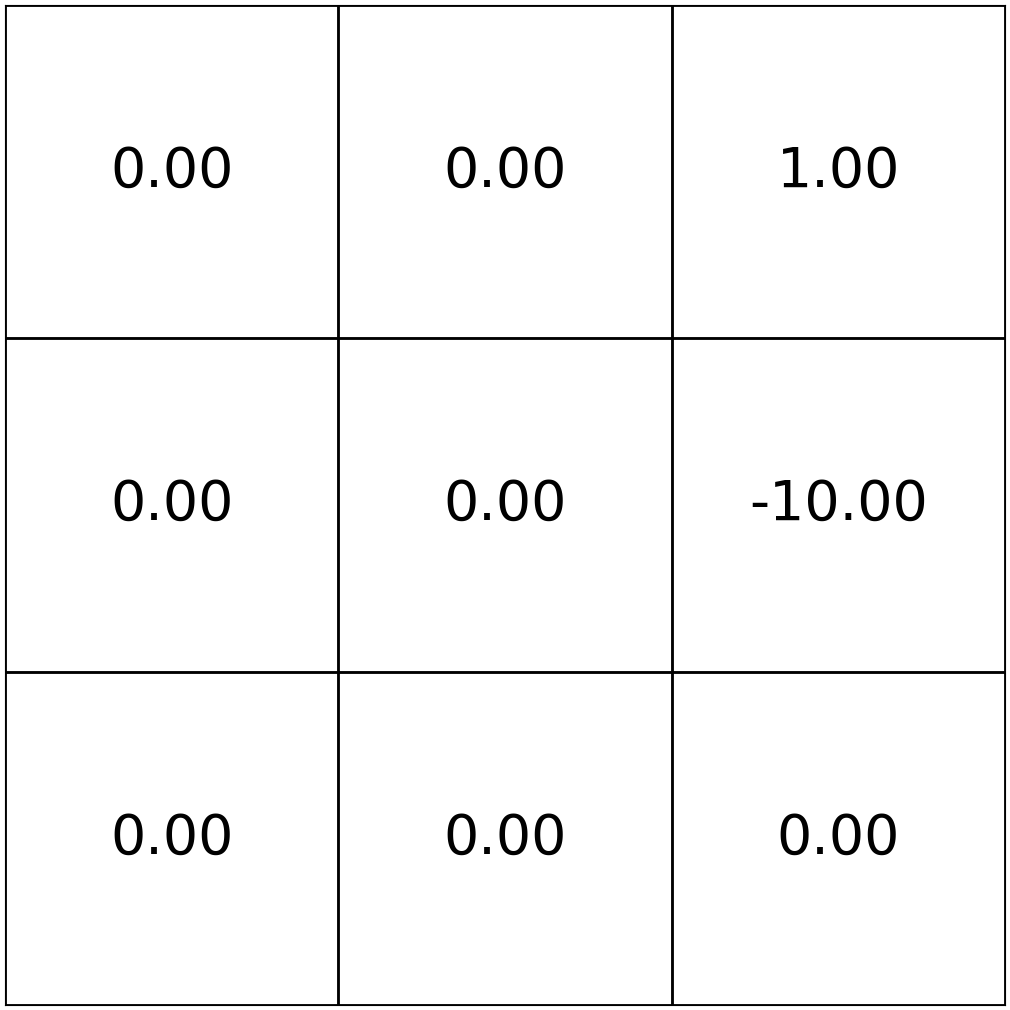

-9

0

0

-9.28

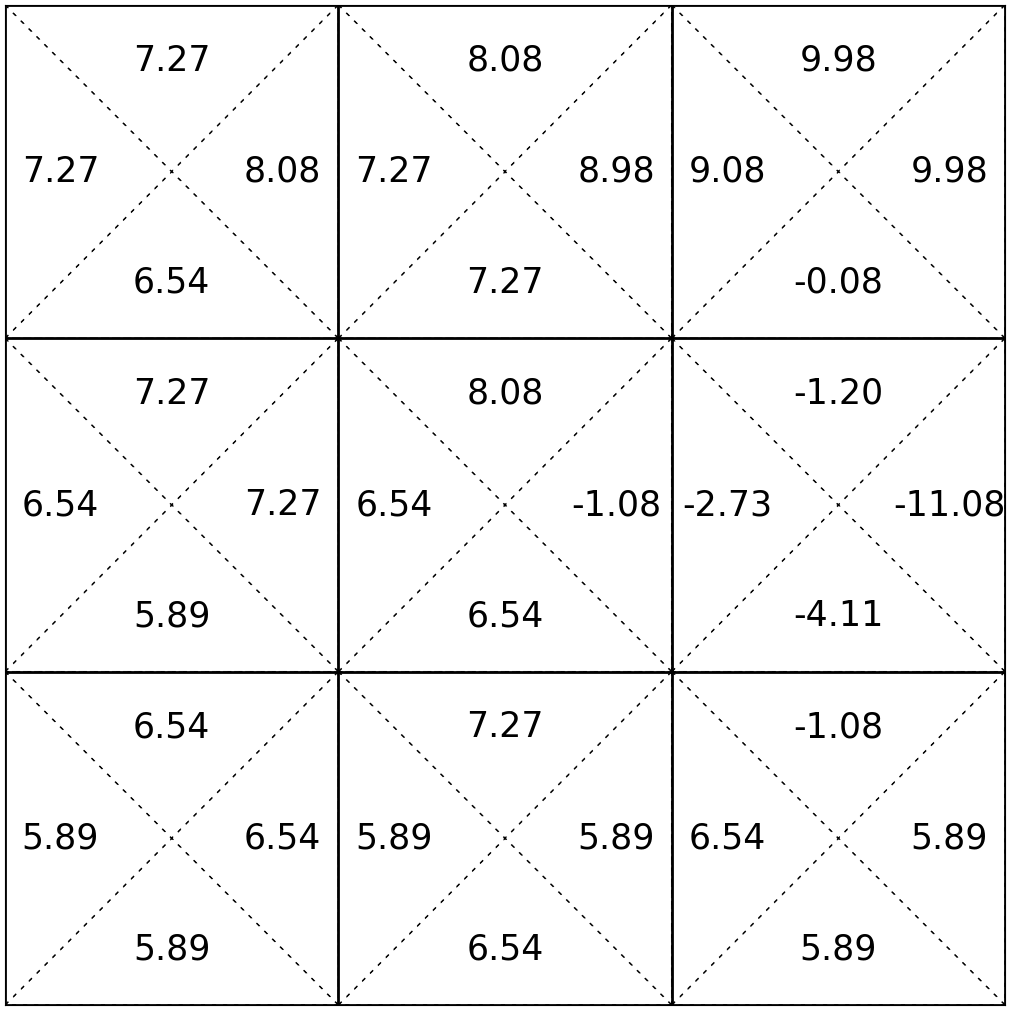

\mathrm{R}(6, \uparrow) + \gamma [.2 \mathrm{R}(2, \uparrow) + .8 \mathrm{R}(3, \uparrow)]

\mathrm{R}(8, \uparrow) + \gamma \mathrm{R}(5, \uparrow)

\mathrm{R}(7, \uparrow) + \gamma \mathrm{R}(4, \uparrow)

\mathrm{R}(9, \uparrow) + \gamma \mathrm{R}(6, \uparrow)

= -10 + 0.9*(0.2*0+0.8*1)

= -9.28

?

= 0 + 0.9*(-10)

action \(\uparrow\)

\mathrm{R}(6, \uparrow)

20\%

80\%

action \(\uparrow\)

\mathrm{R}(2, \uparrow)

\gamma

action \(\uparrow\)

\mathrm{R}(3, \uparrow)

\gamma

\mathbb{E}[

]

\mathrm{R}(s_0, a_0)

\gamma\mathrm{R}(s_1, a_1)

+

\( 2\) terms inside

\mathrm{V}^{\uparrow}_2(s) =

0

0

1.9

0

0

horizon \(h = 2:\)

states and

one special transition:

rewards

- \(\pi(s) = ``\uparrow",\ \forall s\)

- \(\gamma = 0.9\)

80\%

20\%

V^{\uparrow}_3(6)

action \(\uparrow\)

action \(\uparrow\)

action \(\uparrow\)

action \(\uparrow\)

action \(\uparrow\)

20\%

80\%

80\%

\mathrm{R}(6, \uparrow)

\gamma \mathrm{R}(2, \uparrow)

20\%

+

+

\gamma \mathrm{R}(2, \uparrow)

\gamma^2 \mathrm{R}(2, \uparrow)

\gamma \mathrm{R}(3, \uparrow)

\mathrm{R}(s_0, a_0)

\gamma \mathrm{R}(s_1, a_1)

+

\mathbb{E}[

]

\gamma^2 \mathrm{R}(s_2, a_2)

+

\mathrm{R}(6, \uparrow)

\gamma^2\mathrm{R}(3, \uparrow)

\gamma^2 \mathrm{R}(2, \uparrow)

\gamma \mathrm{R}(3, \uparrow)

20\%

+

80\%

\gamma^2\mathrm{R}(3, \uparrow)

+

=

horizon \(h = 3:\)

states and

one special transition:

rewards

- \(\pi(s) = ``\uparrow",\ \forall s\)

- \(\gamma = 0.9\)

80\%

20\%

\mathrm{R}(6, \uparrow)

\gamma \mathrm{R}(2, \uparrow)

20\%

+

+

\gamma^2 \mathrm{R}(2, \uparrow)

\gamma \mathrm{R}(3, \uparrow)

80\%

+

\gamma^2\mathrm{R}(3, \uparrow)

=

+

[

]

]

[

=

+

\left[\mathrm{R}(3, \uparrow) + \gamma \mathrm{R}(3, \uparrow)\right]

\gamma

+

80\%

\mathrm{R}(6, \uparrow)

\left[\mathrm{R}(2, \uparrow) + \gamma \mathrm{R}(2, \uparrow)\right]

\gamma

20\%

=

80\%

\gamma

20\%

+

V^{\uparrow}_2(2)

\gamma

+

\mathrm{R}(6, \uparrow)

\mathrm{V}^{\uparrow}_2(3)

\mathrm{V}_h^\pi(s)=\mathrm{R}\left(s, \pi(s)\right)+\gamma \sum_{s^{\prime}} \mathrm{T}\left(s, \pi(s), s^{\prime}\right) \mathrm{V}_{h-1}^\pi\left(s^{\prime}\right)

the immediate reward for taking the policy-prescribed action \(\pi(s)\) in state \(s\).

horizon-\(h\) value in state \(s\): the expected sum of discounted rewards, starting in state \(s\) and following policy \(\pi\) for \(h\) steps.

\mathrm{V}^{\uparrow}_3(6)

=

80\%

\gamma

20\%

+

\mathrm{V}^{\uparrow}_2(2)

\gamma

+

\mathrm{R}(6, \uparrow)

\mathrm{V}^{\uparrow}_2(3)

\((h-1)\) horizon future values at a next state \(s^{\prime}\)

sum up future values weighted by the probability of getting to that next state \(s^{\prime}\)

discounted by \(\gamma\)

\mathrm{V}_h^\pi(s)=\mathrm{R}\left(s, \pi(s)\right)+\gamma \sum_{s^{\prime}} \mathrm{T}\left(s, \pi(s), s^{\prime}\right) \mathrm{V}_{h-1}^\pi\left(s^{\prime}\right), \forall s

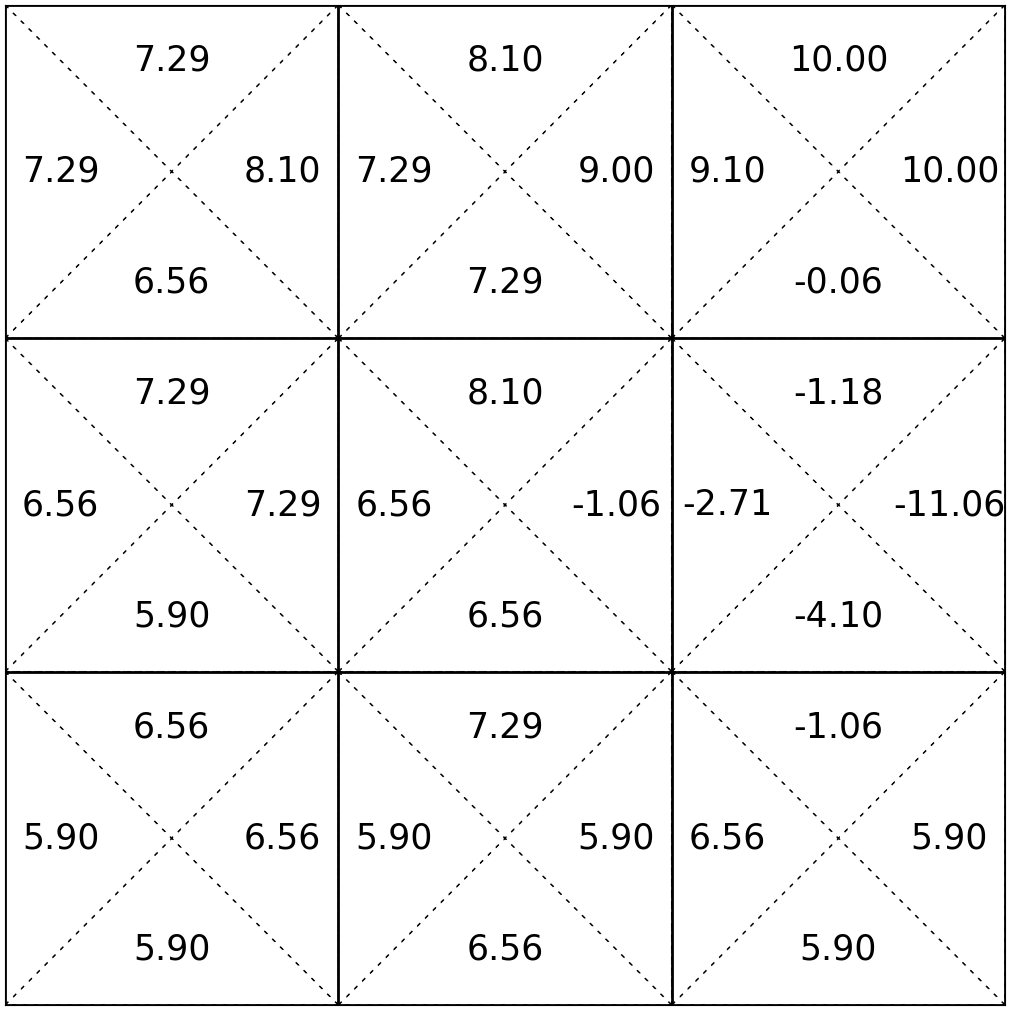

Bellman Recursion

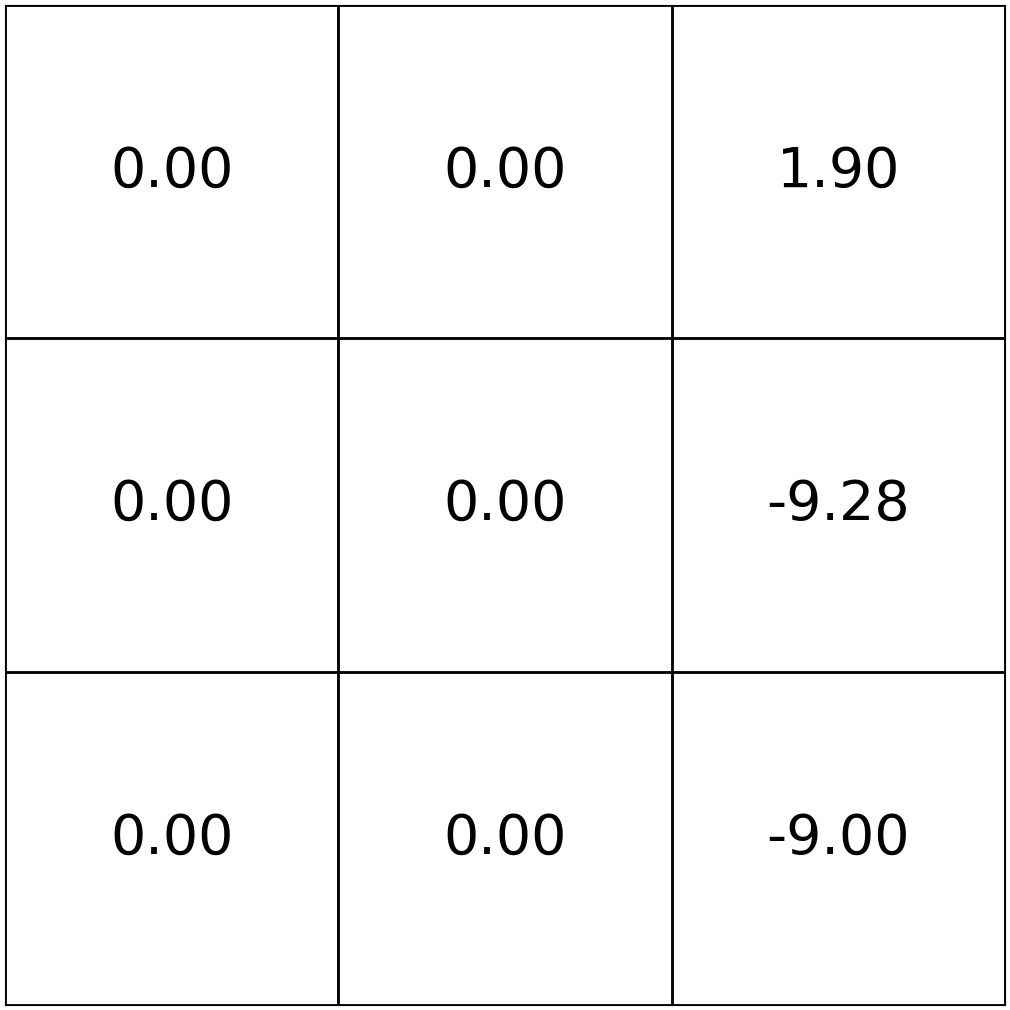

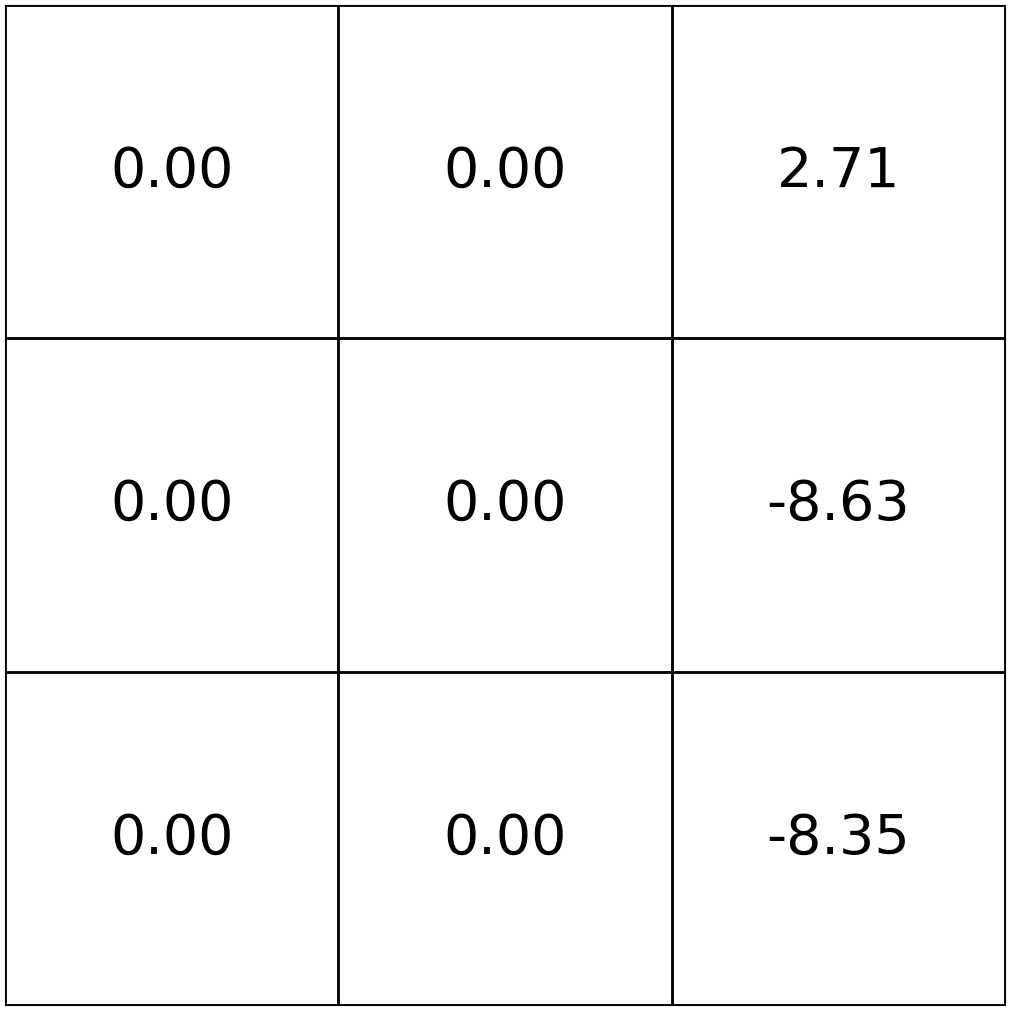

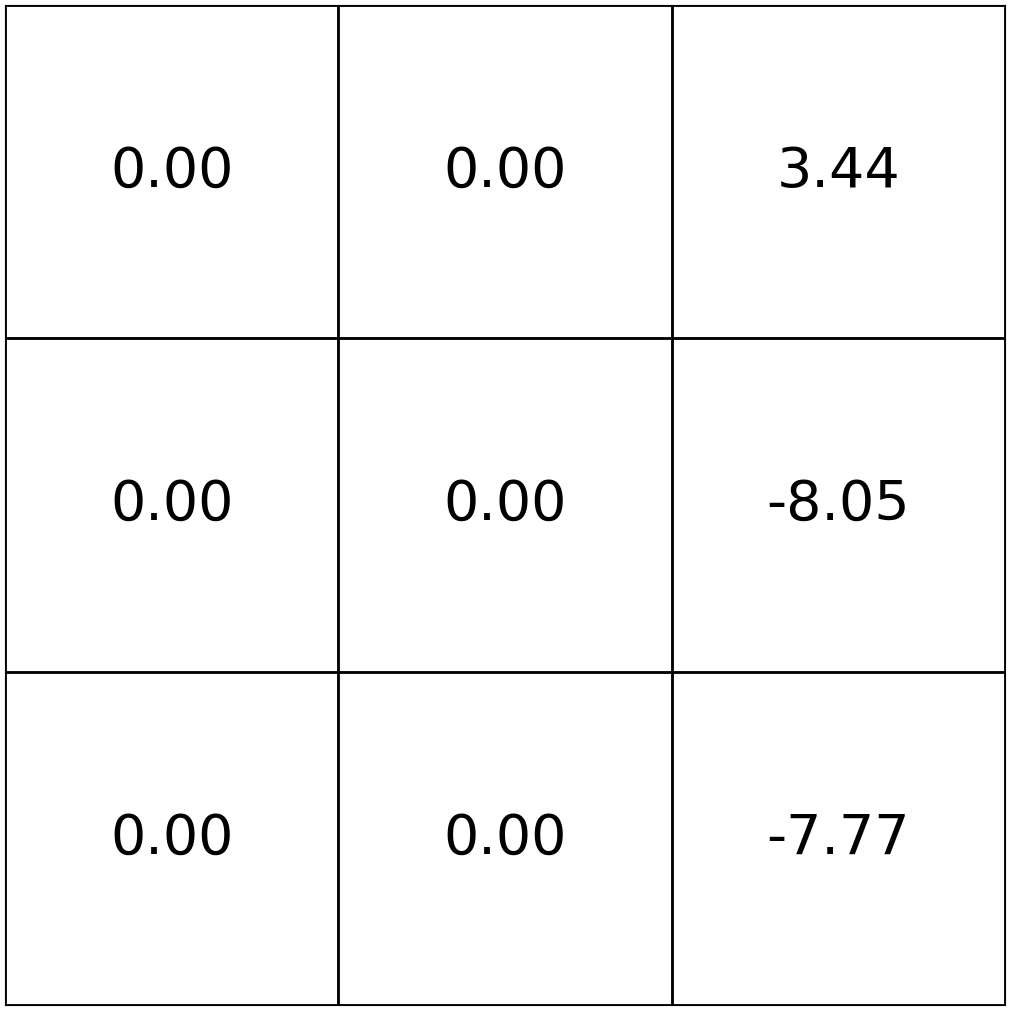

\mathrm{V}^{\uparrow}_2(s)

\mathrm{V}^{\uparrow}_3(s)

\mathrm{V}^{\uparrow}_4(s)

\mathrm{V}^{\uparrow}_5(s)

\mathrm{V}^{\uparrow}_6(s)

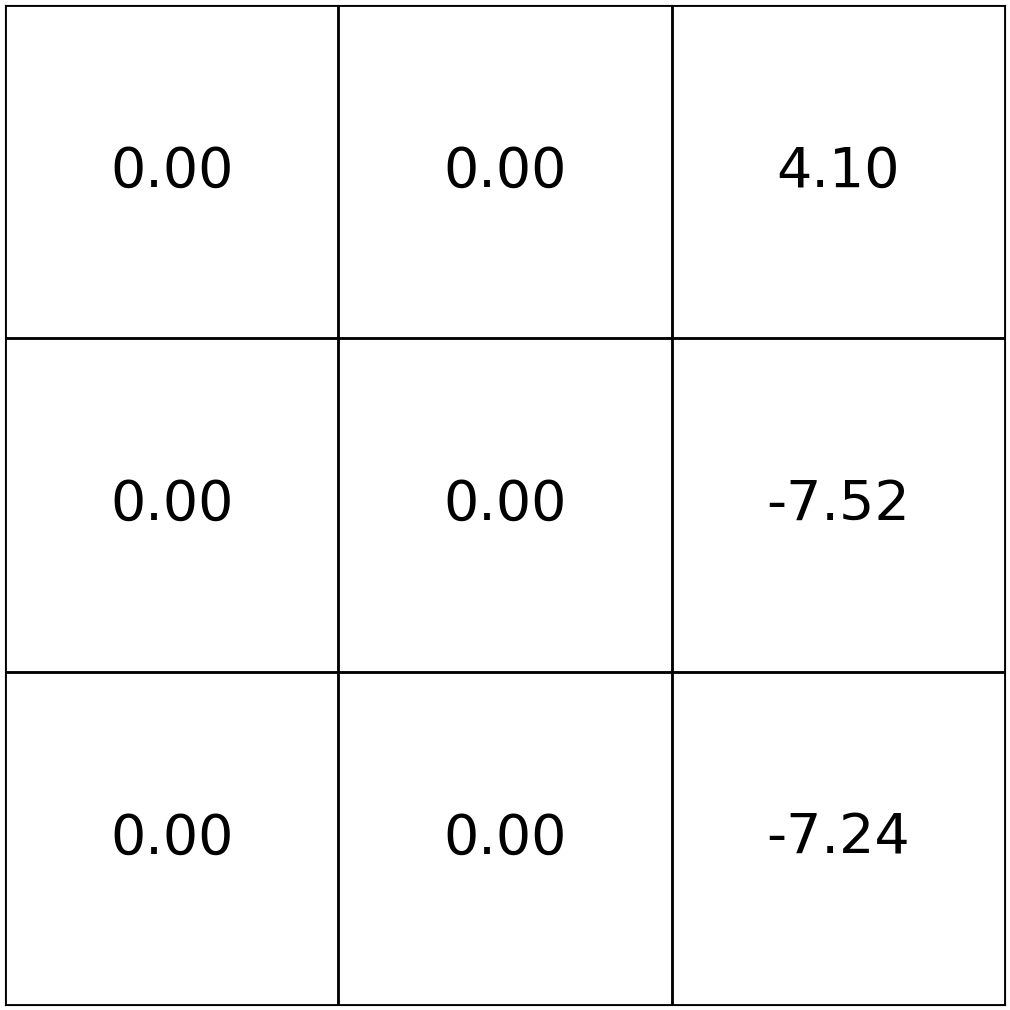

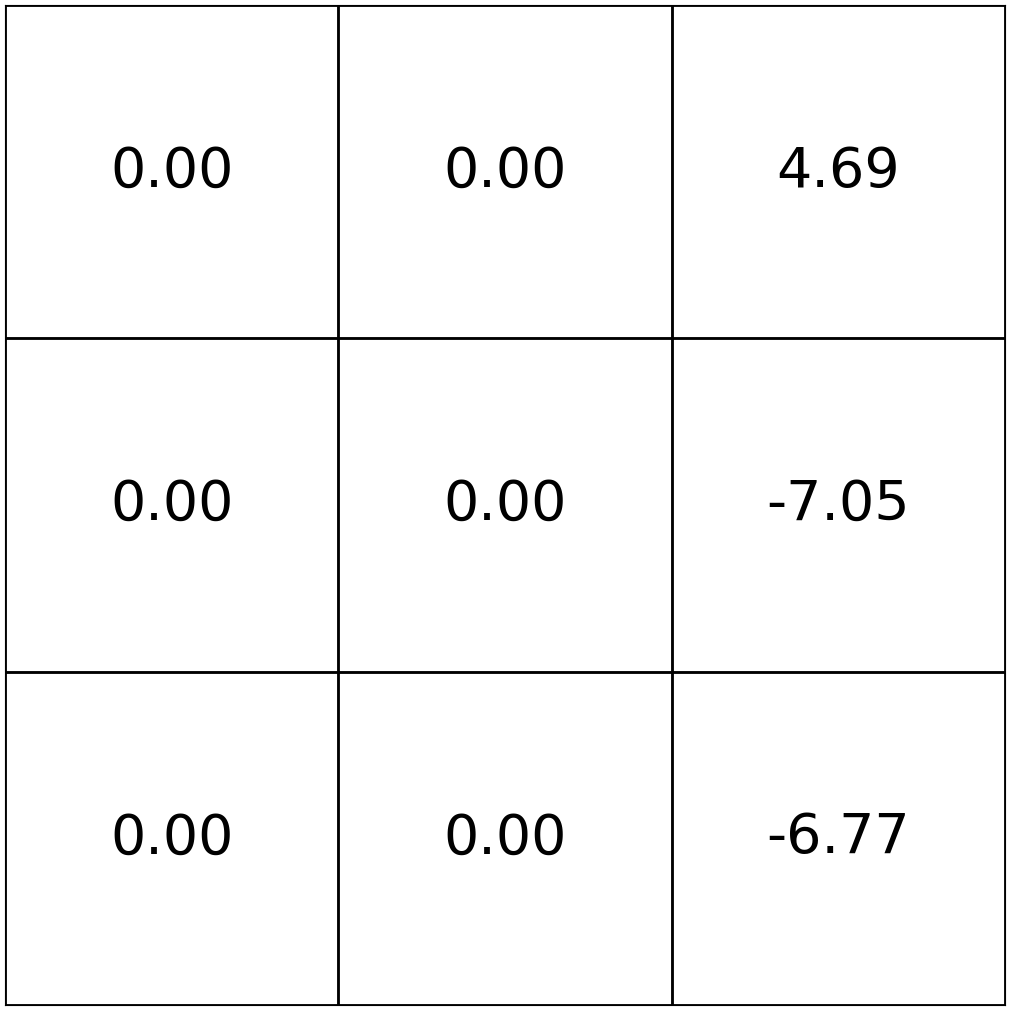

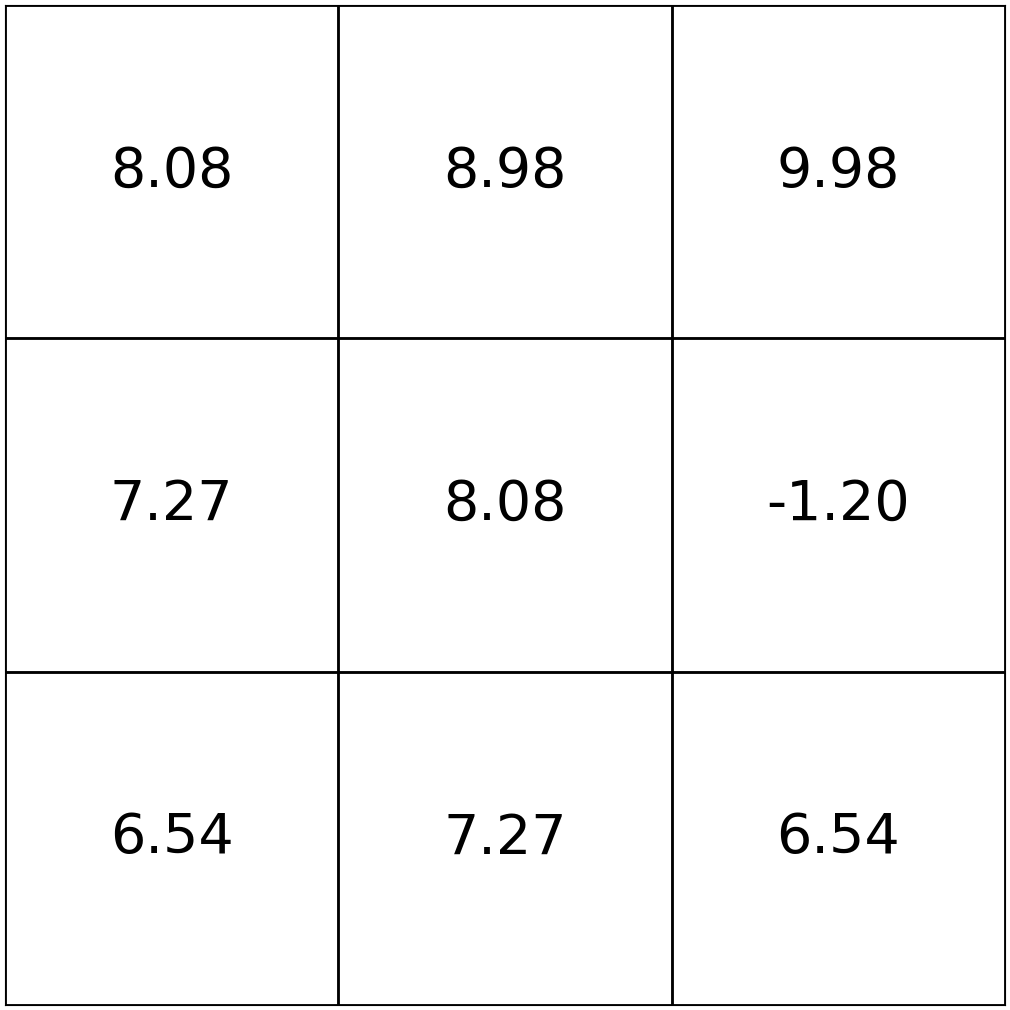

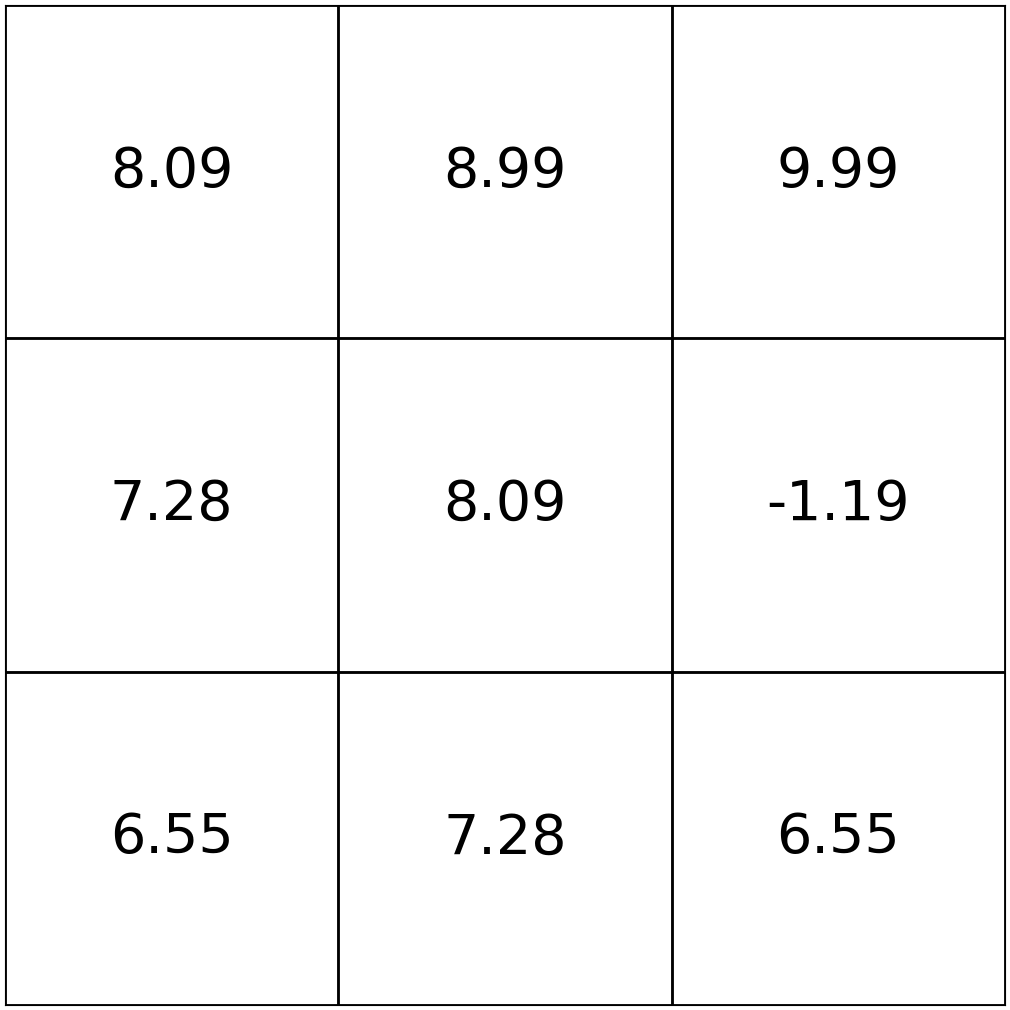

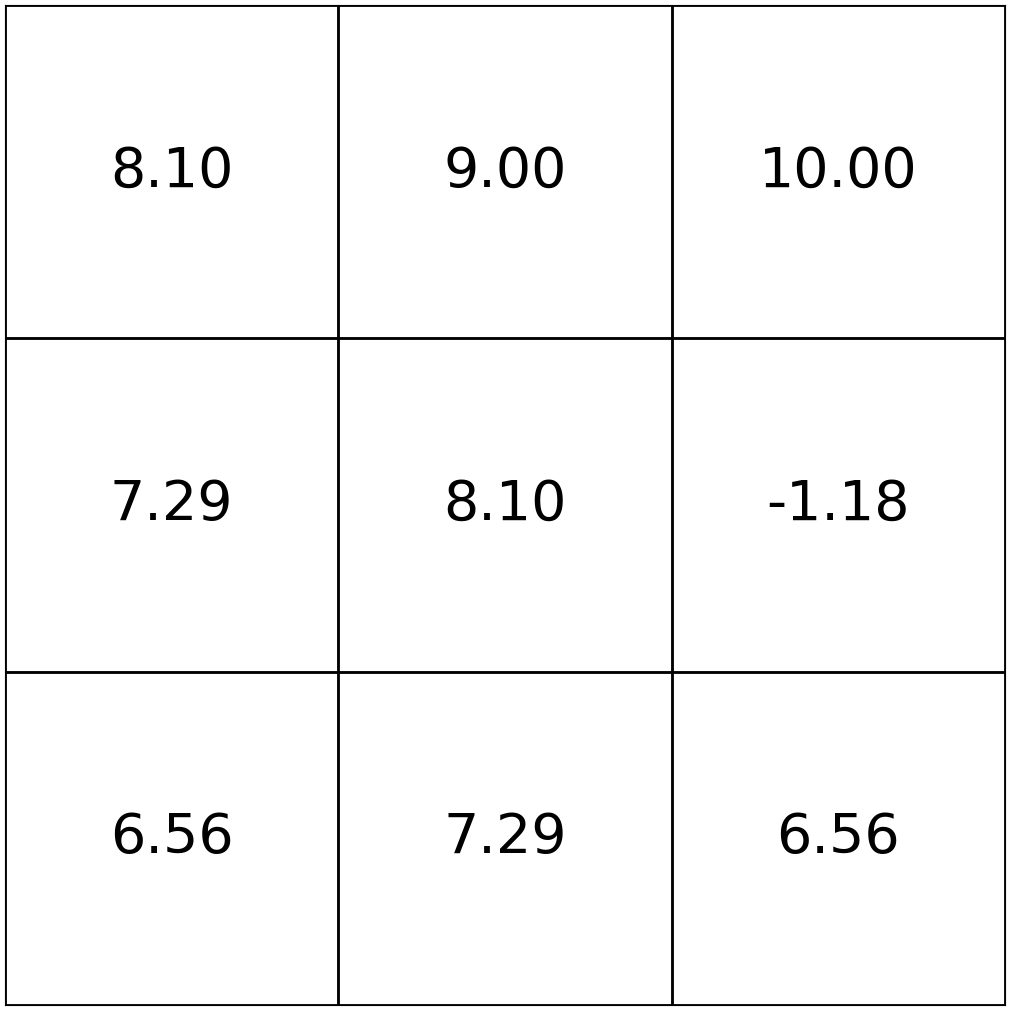

-7.048 = -10 +.9[.2*0+0.8*4.10]

\mathrm{V}^{\uparrow}_{61}(s)

\mathrm{V}^{\uparrow}_{62}(s)

\dots

\mathrm{V}^{\uparrow}_1(s) = \mathrm{R}(s,\uparrow)

\mathrm{V}^{\uparrow}_{6}(6) = \mathrm{R}(6, \uparrow) + \gamma [.2 \mathrm{V}^{\uparrow}_{5}(2) + .8\times \mathrm{V}^{\uparrow}_{5}(3)]

approaches infinity

\mathrm{V}^\pi_{\infty}(s)= \mathrm{R}(s, \pi(s))+ \gamma \sum_{s^{\prime}} \mathrm{T}\left(s, \pi(s), s^{\prime}\right) \mathrm{V}^\pi_{\infty}\left(s^{\prime}\right), \forall s

\(|\mathcal{S}|\) many linear equations, one equation for each state

typically \(\gamma <1\) in MDP definition, motivated to make \(\mathrm{V}^{\pi}_{\infty}(s):=\mathbb{E}\left[\sum_{t=0}^{\infty} \gamma^t \mathrm{R}\left(s_t, \pi\left(s_t\right)\right) \mid s_0=s, \pi\right]\) finite.

Bellman Equations

If the horizon \(h\) goes to infinity

\mathrm{V}_h^\pi(s)=\mathrm{R}\left(s, \pi(s)\right)+\gamma \sum_{s^{\prime}} \mathrm{T}\left(s, \pi(s), s^{\prime}\right) \mathrm{V}_{h-1}^\pi\left(s^{\prime}\right), \forall s

Bellman Recursion

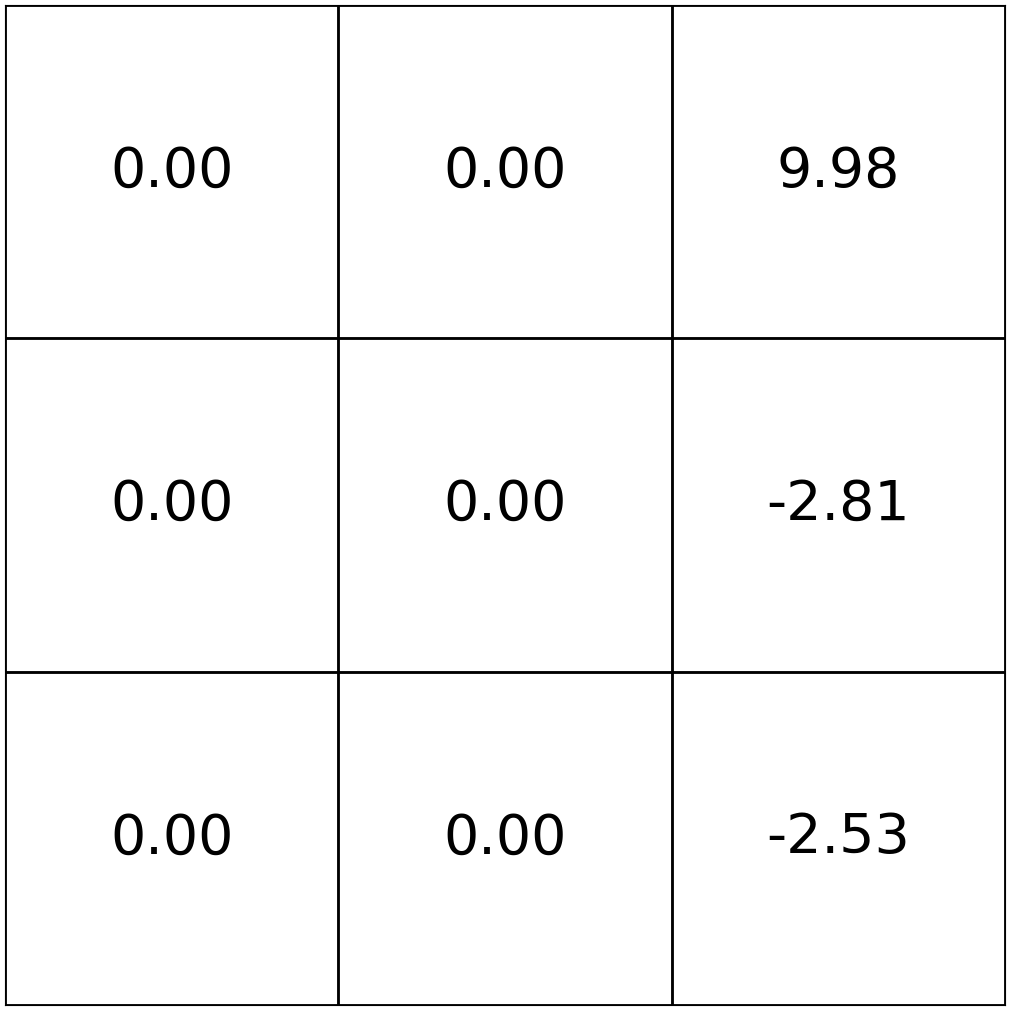

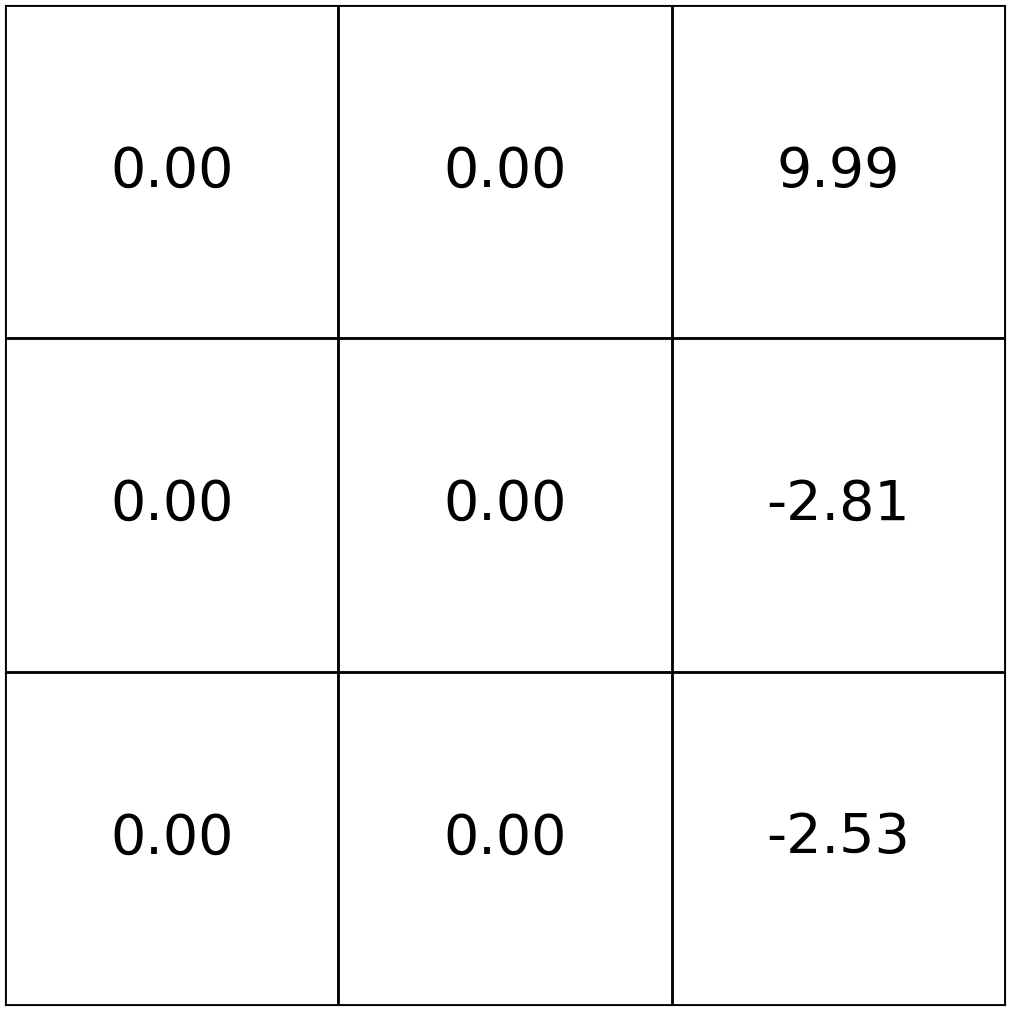

\mathrm{V}^{\uparrow}_{\infty}(s)

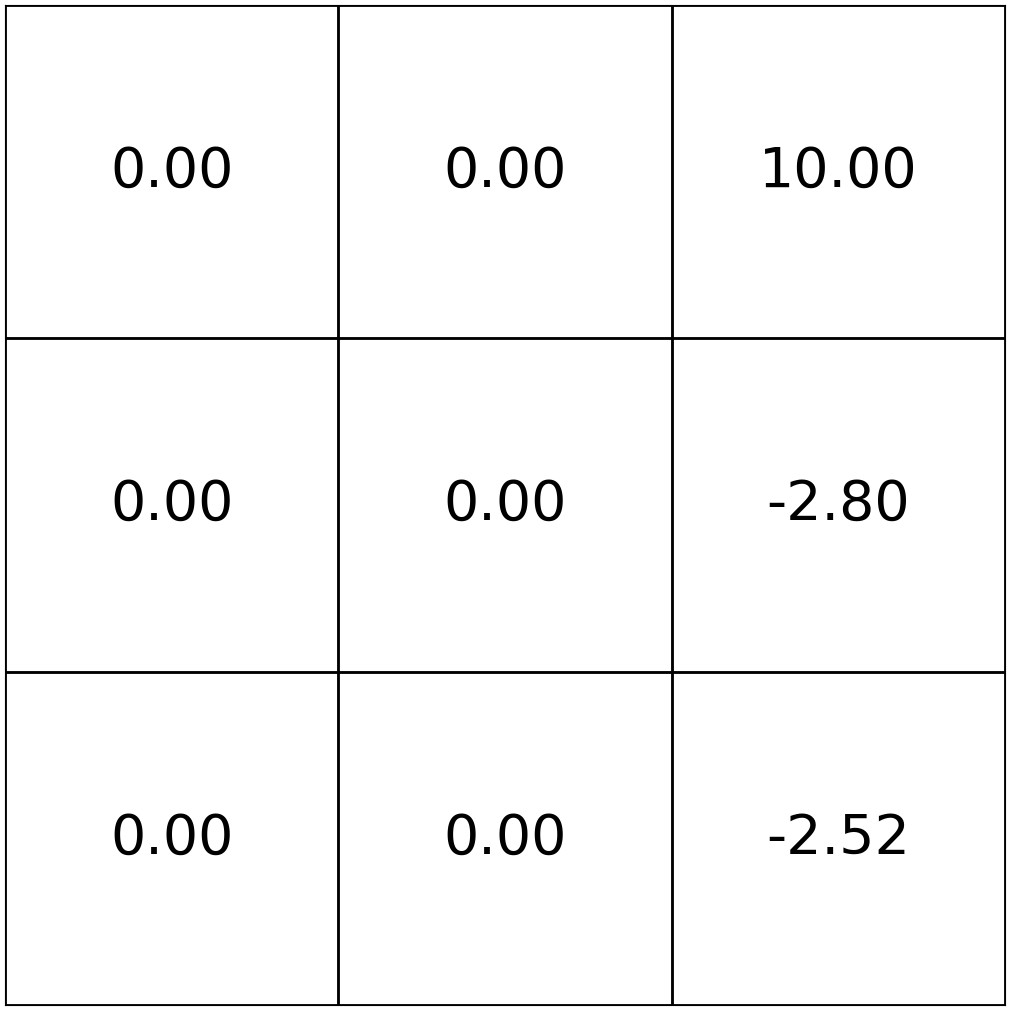

-2.8 = \mathrm{V}^{\uparrow}_{\infty}(6) = \mathrm{R}(6, \uparrow) + \gamma [.2 \mathrm{V}^{\uparrow}_{\infty}(2) + .8\times \mathrm{V}^{\uparrow}_{\infty}(3)]

= -10 + .9 [.2 \times 0 + .8 * 10]

10 = \mathrm{V}^{\uparrow}_{\infty}(3) = \mathrm{R}(3, \uparrow) + \gamma [\mathrm{V}^{\uparrow}_{\infty}(3)] = 1 + .9 \times 10

-2.52 = \mathrm{V}^{\uparrow}_{\infty}(9) = \mathrm{R}(9, \uparrow) + \gamma [\mathrm{V}^{\uparrow}_{\infty}(6)] = 0 + .9 \times (-2.8)

finite-horizon Bellman recursions

infinite-horizon Bellman equations

\mathrm{V}^\pi_{\infty}(s)= \mathrm{R}(s, \pi(s))+ \gamma \sum_{s^{\prime}} \mathrm{T}\left(s, \pi(s), s^{\prime}\right) \mathrm{V}^\pi_{\infty}\left(s^{\prime}\right), \forall s

\mathrm{V}_{h}^\pi(s)= \mathrm{R}(s, \pi(s))+ \gamma \sum_{s^{\prime}} \mathrm{T}\left(s, \pi(s), s^{\prime}\right) \mathrm{V}_{h-1}^\pi\left(s^{\prime}\right), \forall s

Recall: For a given policy \(\pi(s),\) the (state) value functions

\(\mathrm{V}_h^\pi(s):=\mathbb{E}\left[\sum_{t=0}^{h-1} \gamma^t \mathrm{R}\left(s_t, \pi\left(s_t\right)\right) \mid s_0=s, \pi\right], \forall s, h\)

\pi(s)

\mathrm{V}^{\pi}_{h}(s)

MDP

Policy evaluation

Quick summary

1. By summing \(h\) terms:

2. By leveraging structure:

Outline

- Markov Decision Processes Definition, terminologies, and policy

-

Policy Evaluation

-

State Value Functions \(\mathrm{V}^{\pi}\)

-

Bellman recursions and Bellman equations

-

-

Policy Optimization

-

Optimal policies \(\pi^*\)

-

Optimal action value functions: \(\mathrm{Q}^*\)

-

Value iteration

-

- An MDP has a unique optimal value \(\mathrm{V}_h^{*}({s})\).

- Optimal policy \(\pi^*\) might not be unique (think, e.g. symmetric world).

- For finite \(h\), optimal policy \(\pi^*_h\) depends on how many time steps left.

- When \(h \rightarrow \infty\), time no longer matters, i.e., there exists a stationary \(\pi^*\).

- Under optimal policy, recursion holds too

Optimal policy \(\pi^*\)

Definition: for a given MDP and a fixed horizon \(h\) (possibly infinite), \(\pi^*\) is an optimal policy if \(\mathrm{V}_h^{\pi^*}({s}) = \mathrm{V}_h^{*}({s})\geqslant \mathrm{V}_h^\pi({s})\) for all \(s \in \mathcal{S}\) and for all possible policy \(\pi\).

\mathrm{V}_{h}^{{*}}(s)= \mathrm{R}(s, \pi^*(s))+ \gamma \sum_{s^{\prime}} \mathrm{T}\left(s, \pi^*(s), s^{\prime}\right) \mathrm{V}_{h-1}^{{*}}\left(s^{\prime}\right), \forall s, h

- One idea: enumerate over all \(\pi\), do policy evaluation, compare \(V^\pi,\) get \(\mathrm{V}^{*}(s)\)

- tedious, and even with \(\mathrm{V}^{*}(s)\)... not super clear how to act

How to search for an optimal policy \(\pi^*\)?

\mathrm{V}_{h}^{{*}}(s)= \mathrm{R}(s, \pi^*(s))+ \gamma \sum_{s^{\prime}} \mathrm{T}\left(s, \pi^*(s), s^{\prime}\right) \mathrm{V}_{h-1}^{{*}}\left(s^{\prime}\right), \forall s, h

Definition: for a given MDP and a fixed horizon \(h\) (possibly infinite), \(\pi^*\) is an optimal policy if \(\mathrm{V}_h^{\pi^*}({s}) = \mathrm{V}_h^{*}({s})\geqslant \mathrm{V}_h^\pi({s})\) for all \(s \in \mathcal{S}\) and for all possible policy \(\pi\).

\mathrm{V}^{*}_{\infty}(s)

\mathrm{V}^{*}_{62}(s)

\mathrm{V}^{*}_{61}(s)

\dots

Outline

- Markov Decision Processes Definition, terminologies, and policy

-

Policy Evaluation

-

State Value Functions \(\mathrm{V}^{\pi}\)

-

Bellman recursions and Bellman equations

-

-

Policy Optimization

-

Optimal policies \(\pi^*\)

-

Optimal action value functions: \(\mathrm{Q}^*\)

-

Value iteration

-

Optimal state-action value functions \(\mathrm{Q}^*_h(s, a)\)

\(\mathrm{Q}^*_h(s, a)\): the expected sum of discounted rewards for

- starting in state \(s\),

- take action \(a\), for one step

- act optimally there afterwards for the remaining \((h-1)\) steps

\mathrm{Q}^*_h (s, a)=\mathrm{R}(s, a)+\gamma \sum_{s^{\prime}} \mathrm{T}\left(s, a, s^{\prime} \right) \max _{a^{\prime}} \mathrm{Q}^*_{h-1}\left(s^{\prime}, a^{\prime}\right), \forall s, a, h

recursively finding \(\mathrm{Q}^*_h(s, a)\)

\(\mathrm{Q}^*_h(s, a)\): the expected sum of discounted rewards for

- starting in state \(s\),

- take action \(a\), for one step

- act optimally there afterwards for the remaining \((h-1)\) steps

1

2

9

8

7

5

4

3

6

80\%

20\%

Recall:

\(\gamma = 0.9\)

1

1

1

1

-10

-10

-10

-10

States and one special transition:

\(\mathrm{R}(s,a)\)

\mathrm{Q}^*_0(s, a)

\mathrm{Q}^*_1(s, a)

=\mathrm{R}(s, a)

\mathrm{Q}^*_2(s, a)

Let's consider \(\mathrm{Q}^*_2(3, \rightarrow)\)

- receive \(\mathrm{R}(3,\rightarrow)\)

\( = 1 + .9 \max _{a^{\prime}} \mathrm{Q}_{1}^*\left(3, a^{\prime}\right)\)

- next state \(s'\) = 3, act optimally for the remaining one timestep

- receive \(\max _{a^{\prime}} \mathrm{Q}^*_{1}\left(3, a^{\prime}\right)\)

\( = 1.9\)

1.9

Recall:

\(\gamma = 0.9\)

States and one special transition:

- starting in state \(s\),

- take action \(a\), for one step

- act optimally there afterwards for the remaining \((h-1)\) steps

\(\mathrm{Q}^*_2(3, \rightarrow) = \mathrm{R}(3,\rightarrow) + \gamma \max _{a^{\prime}} \mathrm{Q}^*_{1}\left(3, a^{\prime}\right)\)

\mathrm{Q}^*_1(s, a)

=\mathrm{R}(s, a)

80\%

20\%

\(\mathrm{Q}^*_h(s, a)\): the value for

Let's consider \(\mathrm{Q}^*_2(3, \uparrow)\)

- receive \(\mathrm{R}(3,\uparrow)\)

\( = 1 + .9 \max _{a^{\prime}} \mathrm{Q}_{1}^*\left(3, a^{\prime}\right)\)

- next state \(s'\) = 3, act optimally for the remaining one timestep

- receive \(\max _{a^{\prime}} \mathrm{Q}^*_{1}\left(3, a^{\prime}\right)\)

\( = 1.9\)

1.9

1

2

9

8

7

5

4

3

6

80\%

20\%

Recall:

\(\gamma = 0.9\)

States and one special transition:

- starting in state \(s\),

- take action \(a\), for one step

- act optimally there afterwards for the remaining \((h-1)\) steps

\(\mathrm{Q}^*_2(3, \uparrow) = \mathrm{R}(3,\uparrow) + \gamma \max _{a^{\prime}} \mathrm{Q}^*_{1}\left(3, a^{\prime}\right)\)

1.9

=\mathrm{R}(s, a)

\mathrm{Q}^*_1(s, a)

\mathrm{Q}^*_2(s, a)

\(\mathrm{Q}^*_h(s, a)\): the value for

Let's consider \(\mathrm{Q}_2^*(3, \leftarrow)\)

- receive \(\mathrm{R}(3,\leftarrow)\)

\( = 1 + .9 \max _{a^{\prime}} \mathrm{Q}_{1}^*\left(2, a^{\prime}\right)\)

- next state \(s'\) = 2, act optimally for the remaining one timestep

- receive \(\max _{a^{\prime}} \mathrm{Q}_{1}^*\left(2, a^{\prime}\right)\)

\( = 1\)

1

1

2

9

8

7

5

4

3

6

80\%

20\%

Recall:

\(\gamma = 0.9\)

States and one special transition:

- starting in state \(s\),

- take action \(a\), for one step

- act optimally there afterwards for the remaining \((h-1)\) steps

\(\mathrm{Q}_2^*(3, \leftarrow) = \mathrm{R}(3,\leftarrow) + \gamma \max _{a^{\prime}} \mathrm{Q}_{1}^*\left(2, a^{\prime}\right)\)

1.9

1.9

\(\mathrm{Q}^*_h(s, a)\): the value for

\mathrm{Q}^*_2(s, a)

\mathrm{Q}^*_1(s, a)

=\mathrm{R}(s, a)

Let's consider \(\mathrm{Q}^*_2(3, \downarrow)\)

- receive \(\mathrm{R}(3,\downarrow)\)

\( = 1 + .9 \max _{a^{\prime}} \mathrm{Q}_{1}^*\left(6, a^{\prime}\right)\)

- next state \(s'\) = 6, act optimally for the remaining one timestep

- receive \(\max _{a^{\prime}} \mathrm{Q}_{1}^*\left(6, a^{\prime}\right)\)

\( = -8\)

-8

1

2

9

8

7

5

4

3

6

80\%

20\%

Recall:

\(\gamma = 0.9\)

States and one special transition:

- starting in state \(s\),

- take action \(a\), for one step

- act optimally there afterwards for the remaining \((h-1)\) steps

\(\mathrm{Q}_2^*(3, \downarrow) = \mathrm{R}(3,\downarrow) + \gamma \max _{a^{\prime}} \mathrm{Q}_{1}^*\left(2, a^{\prime}\right)\)

1

1.9

1.9

\(\mathrm{Q}^*_h(s, a)\): the value for

\mathrm{Q}^*_2(s, a)

\mathrm{Q}^*_1(s, a)

=\mathrm{R}(s, a)

1

2

9

8

7

5

4

3

6

80\%

20\%

Recall:

\(\gamma = 0.9\)

States and one special transition:

- act optimally for one more timestep, at the next state \(s^{\prime}\)

- 20% chance, \(s'\) = 2, act optimally, receive \(\max _{a^{\prime}} \mathrm{Q}_{1}^*\left(2, a^{\prime}\right)\)

- 80% chance, \(s'\) = 3, act optimally, receive \(\max _{a^{\prime}} \mathrm{Q}_{1}^*\left(3, a^{\prime}\right)\)

-9.28

\(= -10 + .9 [.2 \times 0+ .8 \times 1] = -9.28\)

- receive \(\mathrm{R}(6,\uparrow)\)

- starting in state \(s\),

- take action \(a\), for one step

- act optimally there afterwards for the remaining \((h-1)\) steps

Let's consider \(\mathrm{Q}_2^*(6, \uparrow) \)

-8

1

1.9

1.9

\(=\mathrm{R}(6,\uparrow) + \gamma[.2 \max _{a^{\prime}} \mathrm{Q}_{1}^*\left(2, a^{\prime}\right)+ .8\max _{a^{\prime}} \mathrm{Q}_{1}^*\left(3, a^{\prime}\right)] \)

\(\mathrm{Q}^*_h(s, a)\): the value for

\mathrm{Q}^*_2(s, a)

\mathrm{Q}^*_1(s, a)

=\mathrm{R}(s, a)

1.9

1.9

1

-8

-9.28

\(\mathrm{Q}_2^*(6, \uparrow) =\mathrm{R}(6,\uparrow) + \gamma[.2 \max _{a^{\prime}} \mathrm{Q}_{1}^*\left(2, a^{\prime}\right)+ .8\max _{a^{\prime}} \mathrm{Q}_{1}^*\left(3, a^{\prime}\right)] \)

\mathrm{Q}^*_h (s, a)=\mathrm{R}(s, a)+\gamma \sum_{s^{\prime}} \mathrm{T}\left(s, a, s^{\prime} \right) \max _{a^{\prime}} \mathrm{Q}^*_{h-1}\left(s^{\prime}, a^{\prime}\right), \forall s,a,h

in general

1

2

9

8

7

5

4

3

6

80\%

20\%

Recall:

\(\gamma = 0.9\)

States and one special transition:

- starting in state \(s\),

- take action \(a\), for one step

- act optimally there afterwards for the remaining \((h-1)\) steps

\mathrm{Q}_1^*(s, a)

=\mathrm{R}(s, a)

\mathrm{Q}_2^*(s, a)

\(\mathrm{Q}^*_h(s, a)\): the value for

1.9

1.9

1

-8

-9.28

1

2

9

8

7

5

4

3

6

80\%

20\%

Recall:

\(\gamma = 0.9\)

States and one special transition:

- starting in state \(s\),

- take action \(a\), for one step

- act optimally there afterwards for the remaining \((h-1)\) steps

\mathrm{Q}_1^*(s, a)

=\mathrm{R}(s, a)

\mathrm{Q}_2^*(s, a)

\pi_h^*(s)=\arg \max _a \mathrm{Q}^*_h(s, a), \forall s, h

what's the optimal action in state 3, with horizon 2, given by \(\pi_2^*(3)=?\)

in general

either up or right

\(\mathrm{Q}^*_h(s, a)\): the value for

Outline

- Markov Decision Processes Definition, terminologies, and policy

-

Policy Evaluation

-

State Value Functions \(\mathrm{V}^{\pi}\)

-

Bellman recursions and Bellman equations

-

-

Policy Optimization

-

Optimal policies \(\pi^*\)

-

Optimal action value functions: \(\mathrm{Q}^*\)

-

Value iteration

-

Given the recursion

\mathrm{Q}^*_{\infty}(s, a)=\mathrm{R}(s, a)+\gamma \sum_{s^{\prime}} \mathrm{T}\left(s, a, s^{\prime} \right) \max _{a^{\prime}} \mathrm{Q}^*_{\infty}\left(s^{\prime}, a^{\prime}\right)

- for \(s \in \mathcal{S}, a \in \mathcal{A}\) :

- \(\mathrm{Q}_{\text {old }}(\mathrm{s}, \mathrm{a})=0\)

- while True:

- for \(s \in \mathcal{S}, a \in \mathcal{A}\) :

- \(\mathrm{Q}_{\text {new }}(s, a) \leftarrow \mathrm{R}(s, a)+\gamma \sum_{s^{\prime}} \mathrm{T}\left(s, a, s^{\prime}\right) \max _{a^{\prime}} \mathrm{Q}_{\text {old }}\left(s^{\prime}, a^{\prime}\right)\)

- if \(\max _{s, a}\left|Q_{\text {old }}(s, a)-Q_{\text {new }}(s, a)\right|<\epsilon:\)

- return \(\mathrm{Q}_{\text {new }}\)

- \(\mathrm{Q}_{\text {old }} \leftarrow \mathrm{Q}_{\text {new }}\)

\mathrm{Q}^*_h (s, a)=\mathrm{R}(s, a)+\gamma \sum_{s^{\prime}} \mathrm{T}\left(s, a, s^{\prime} \right) \max _{a^{\prime}} \mathrm{Q}^*_{h-1}\left(s^{\prime}, a^{\prime}\right)

we can have an infinite horizon equation

Value Iteration

if run this block \(h\) times and break, then the returns are exactly \(\mathrm{Q}^*_h\)

\{

\(\mathrm{Q}^*_{\infty}(s, a)\)

\(\mathrm{V}\) values vs. \(\mathrm{Q}\) values

- \(\mathrm{V}\) is defined over state space; \(\mathrm{Q}\) is defined over (state, action) space.

- \(\mathrm{V}_h^*({s})\) can be derived from \(\mathrm{Q}^*_h(s,a):\), and vise versa.

- \(\mathrm{Q}^*\) is easier to read "optimal actions" from.

- We care more about \(\mathrm{V}^{\pi}\) and \(\mathrm{Q}^*\)

\(\mathrm{V}_{h}^*(s)=\max_{a}\left[\mathrm{Q}^*_{h}(s, a)\right]\)

\mathrm{V}^{\uparrow}_{61}(s)

\mathrm{V}^{\uparrow}_{62}(s)

\mathrm{V}^{\uparrow}_{\infty}(s)

\mathrm{V}^{*}_{61}(s)

\mathrm{V}^{*}_{62}(s)

\mathrm{V}^{*}_{\infty}(s)

\(\mathrm{\pi}_{h}^*(s)=\arg\max_{a}\left[\mathrm{Q}^*_{h}(s, a)\right]\)

\mathrm{Q}^{*}_{61}(s,a)

\mathrm{Q}^{*}_{62}(s,a)

\mathrm{Q}^{*}_{\infty}(s,a)

Summary

- Markov decision processes (MDP) is nice mathematical framework for making sequential decisions. It's the foundation to reinforcement learning.

- An MDP is defined by a five-tuple, and the goal is to find an optimal policy that leads to high expected cumulative discounted rewards.

- To evaluate how good a given policy \(\pi, \) we can calculate \(\mathrm{V}^{\pi}(s)\) via

- the summation over rewards definition

- Bellman recursion for finite horizon, equation for infinite horizon

- To find an optimal policy, we can recursively find \(\mathrm{Q}^*(s,a)\) via the value iteration algorithm, and then act greedily w.r.t. the \(\mathrm{Q}^*\) values.

Thanks!

We'd love to hear your thoughts.

6.390 IntroML (Spring25) - Lecture 10 Markov Decision Processes

By Shen Shen