.svg)

TILIX

Making energy cheap, clean and cheerful through inventing, deploying and optimising technology and innovation.

Not Confidential

Because nature, people and the future matters.

Optimising

Inventing & Deploying

1st

2nd

3rd

Open Heart, Open Mind & Open Will

1

Position

2

Problem

3

Possibilities

4

Pivot

5

Proposals

6

Planning

7

Plan

Getting to where you're going requires knowing where you are.

David Allen

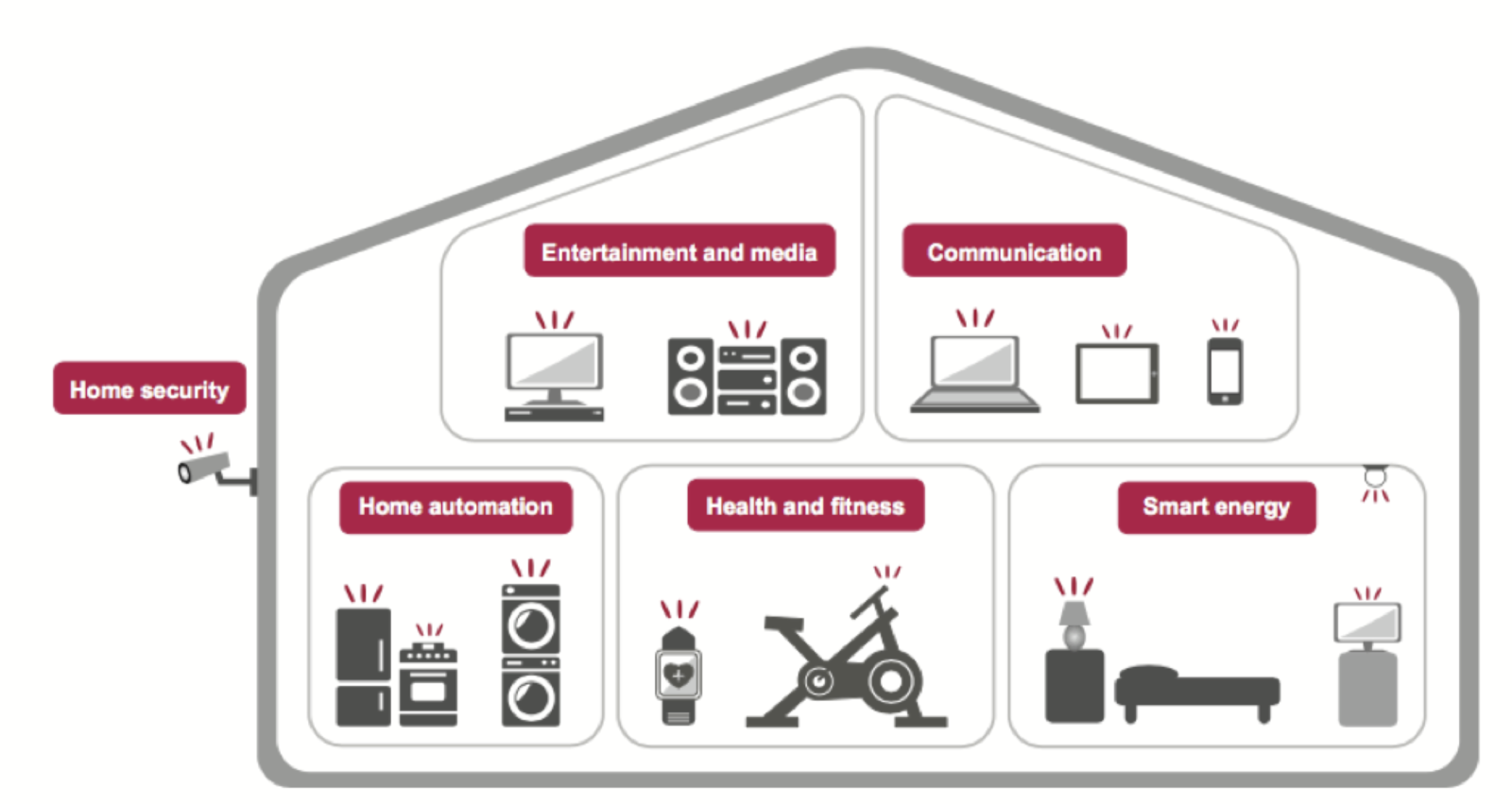

Comms

Music

News

Movies

Banking

Health

Apps

the corporation in no Board meeting or no Supervisory Board meeting has authorized this, but this was a couple of software engineers who put this in, for whatever reasons.

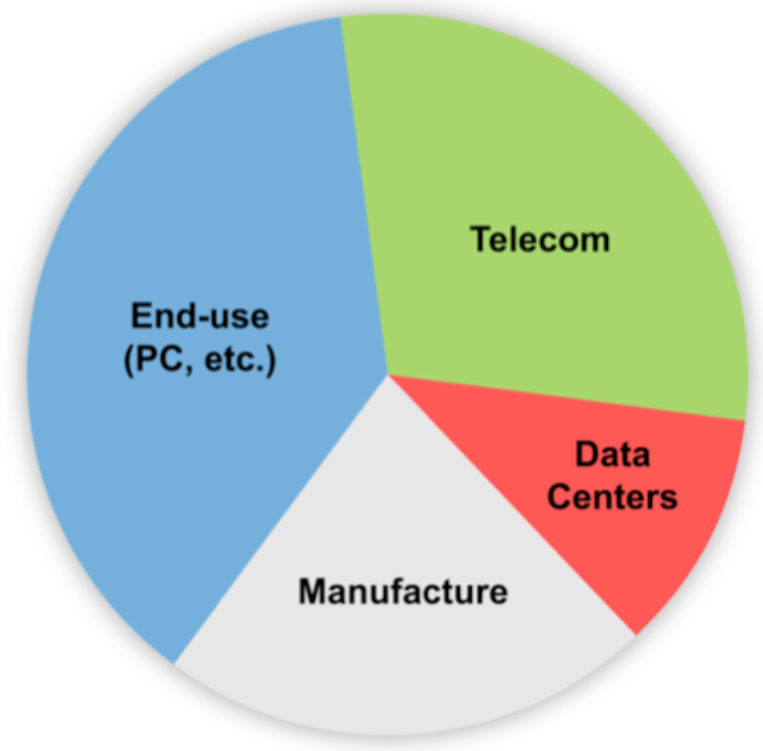

Source: The Cloud Begins With Coal by Mark Mills

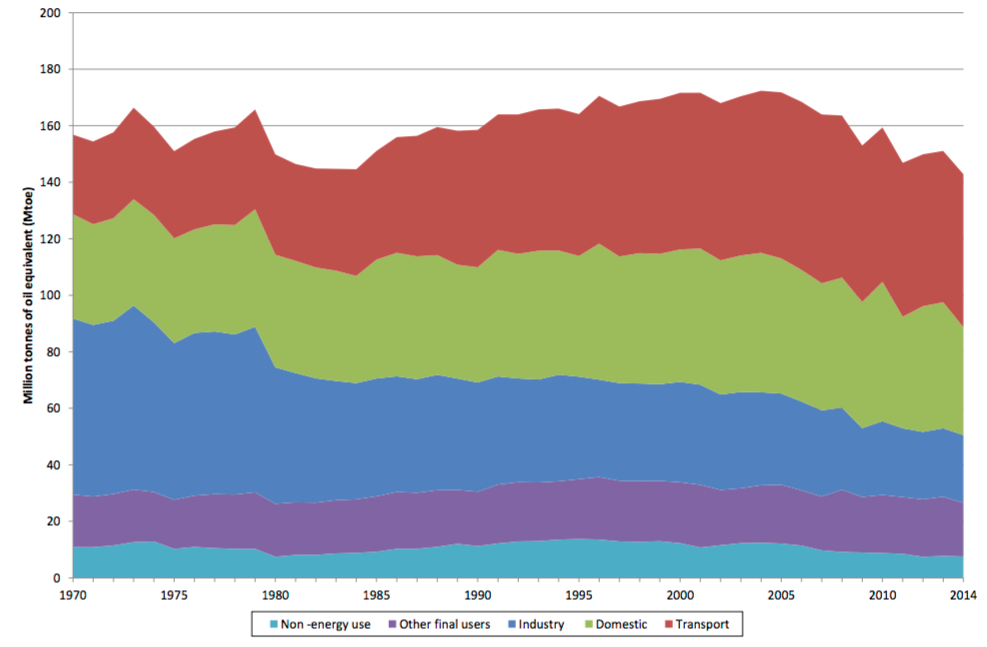

Source: DECC

Share of World Trade - Top Five

14.8% electrical machinery, including computers;

14.4% mineral fuels, including oil, coal, gas, and refined products ;

14.2% nuclear reactors, boilers, and parts ;

8.9% cars, trucks, and buses;

3.5% scientific and precision instruments ;

$113.7 trillion GDP ($15,800 per capita)

GDP - by end use:

GDP - by sector of origin:

3.39 billion workers

While you may ignore economics, it won't ignore you.

IT & Energy orthodoxies are helping to

The pessimist complains about the wind, the optimist expects it to change, the realist adjusts the sails

William Arthur Ward

BIG SIX strategy is to deliver annual growth in the dividend payable to shareholders through the efficient operation of and investment in, a balanced range of economically-regulated and market-based energy-related businesses.

This balance means BIG SIX has a strong and diverse group of energy assets and businesses from which to secure the revenue to support future dividend growth.

To raise new questions, new possibilities, to regard old problems from a new angle requires creative imagination

and marks real advances in science.

Albert Einstein

Primary

Secondary

Tertiary

I am not an optimist. I'm a very serious possibilist. It's a new category where we take emotion apart and we just work analytically with the world.

Professor Hans Rosling

Thinking differently about innovation and technology can be thoughtful & inspiring.

Many industries are converging

to satisfy our hierarchy of needs.

Renewables, smart/digital technology, big data and social media are force multipliers that can overcome the current energy orthodoxy.

Source: Ofgem

The term DSM was coined following the energy crises of the 1970s. Types of management include energy efficiency, demand response & dynamic demand.

Source: Navigant Research

Phasor measurement units, distributed power

flow control, dynamic turn up/down,

automation, artificial intelligence, drones......

OMG!!!

Source: Navigant Research

Lorem ipsum .....

Retreat and reflect, allow the inner knowing to emerge.

Brian Arthur

We’re seeing a continuing sharp, exponential decline in the cost of renewable energy .....

.....in many parts of the world, renewable energy is leapfrogging fossil fuels altogether — the same way mobile phones leap-frogged land-line phones.

Al Gore, Feb 2016

Almost everything around you, was made by people that were no smarter than you.

You can change it, you can influence it, you can build your own things that other people can use.

Steve Jobs

Incumbents have to figure out different ways to use their assets, capabilities and most difficultly their cultures to compete in a very different market that is coming at them at a speed they can scarcely imagine and much faster than their cultures will find it easy to cope with.

The time is right for electric cars.

In fact the time is critical.

Carlos Ghosn, CEO Renault & Nissan

Position & Problems

Possibilities

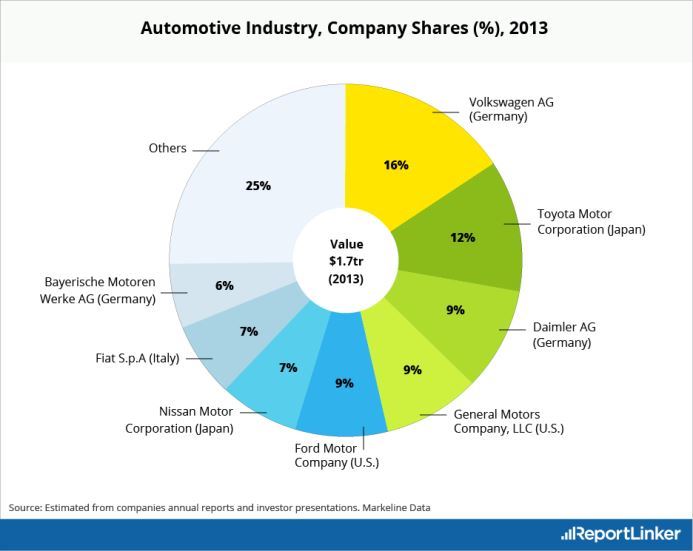

Big Auto

Gas Guzzlers

AFV Challenges

Complexity

EV or FCV?

Uniti

River Simple

Ather Energy

Tesla

Renault/Nissan

Source: Winning The Oil End Game, Amory Lovins

Electric Vehicles - EV

Fuel Cell Vehicles - FCV

Source: www.thinkprogress.org

There are three ways to make a living in this business: be first, be smarter, or cheat.......it sure is a hell of lot easier to just be first.

Margin Call

blog.ev-box.com

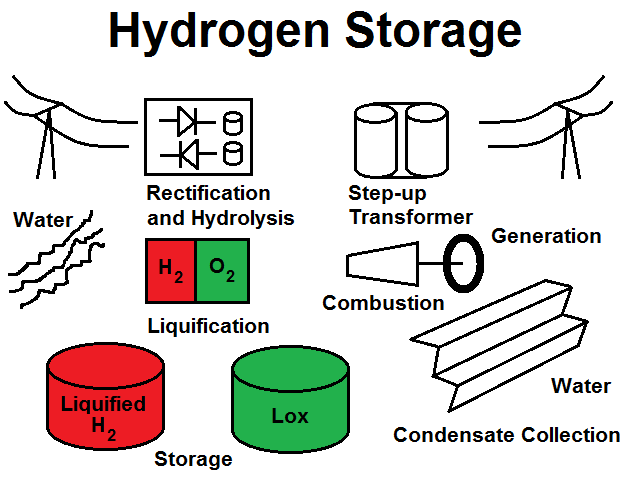

Critical for Demand Side Management (DSM),

optimising renewable generation

and Alternative Fuel Vehicles (AFV).

Transmission

Distribution

Consumer

Position & Problems

Possibilities

Not enough generation

Too much demand

freq < 50Hz

Too much generation

Not enough demand

freq > 50Hz

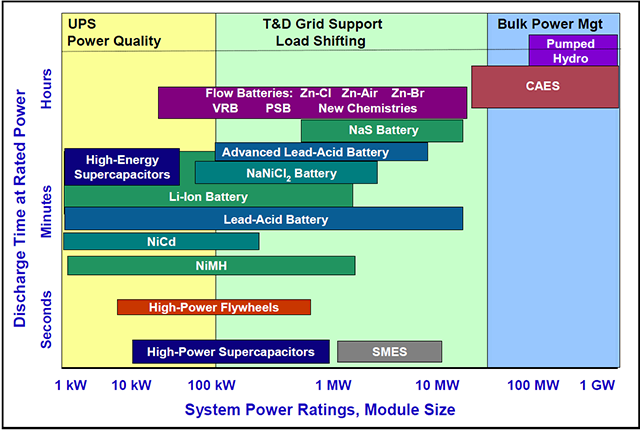

State of art circa 2013. Things are moving on .....

Lithium

Ionic

Lead

acid

Redox

Charge Cycles

Power Density

+

+

-

-

Typically around 60 - 90% efficient

Uses combination of compressors and expansion chambers to store/deliver energy.

Historically very large. Underground caverns and 100-300 MW units

Low cycle efficiency

High self dissipation rates

Above ground units, using air cylinders, more efficient

Established Players

LightSail

FlowBattery

New entrant from Adjacent market

Mattei

Text

2011, 20MW facility in NY from 200 modules for frequency regulation

Compressed air batteries

3kW to 200kW systems

100kWh max

Planning is everything. Plans are nothing. No plan survives contact with the enemy

Field Marshall Helmuth Graf von Molke

Your mind's for having ideas,

not holding them

David Allen

A good plan violently executed now is better

than a perfect plan executed next week.

General George S. Patton

By TILIX

On 26 May 2016, Dr Neil Williams & Dr Duncan Tytler (www.tilix.ukwww.tilix.uk led Bristol Energy Coop's Transition Lab through a discussion of some of the ways that innovation and technology can help make energy cheap, clean and cheerful. As well as a broad overview of the current state of the smart energy market, topics included deep dives into alternative fuel vehicles and energy storage.