Andreas Park PRO

Professor of Finance at UofT

Andreas Park

Presentation for Lakehead University's

Third Age Learning Initiative

What is a blockchain?

What is a cryptocurrency?

What is Decentralized Finance?

decentralized finance =

provision of financial services without the necessary involvement of a traditional financial intermediary

in practice: new financial infrastructure that will be a common resource

payments

stocks, bonds, and options

swaps, CDS, MBS, CDOs

insurance contracts

\(\vdots\)

Source: Harvey, Ramachandran, and Santoro (2020)

Risks and open problems

What lies ahead?

Fall 2021 description

previous description: "New financial infrastructure"

NB: underlying language "Move" is explicitly designed for financial contracts

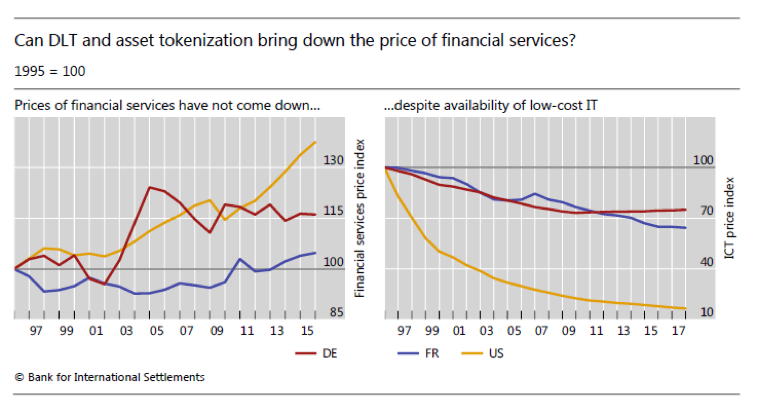

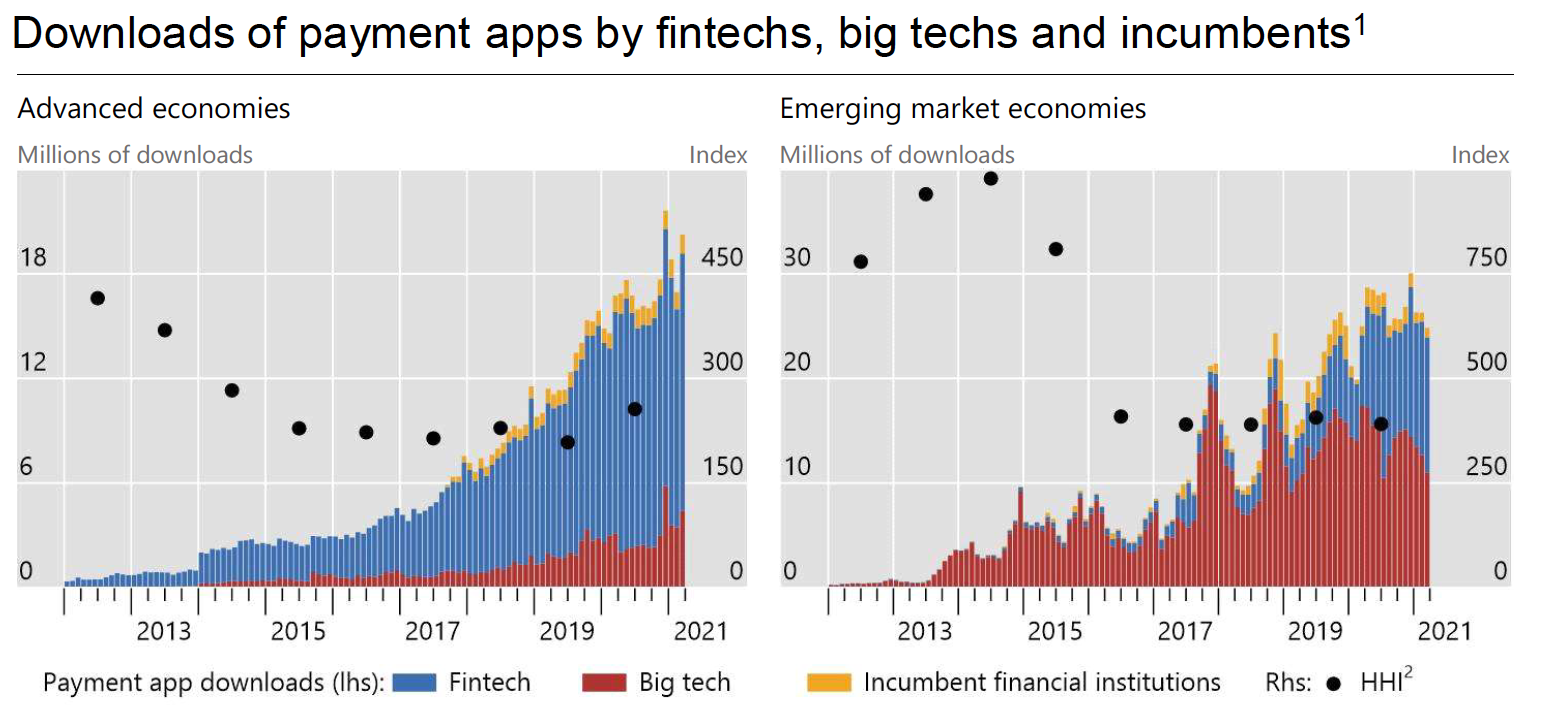

Source: Croxson, Frost, Gambacorta and Valletti (2021)

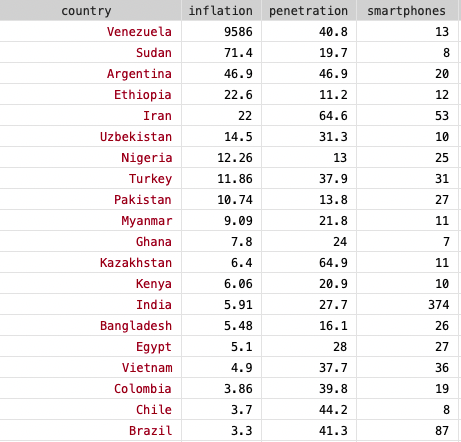

cellphone data from 2018 (NewZoo), inflation from 2020 (World Population Review)

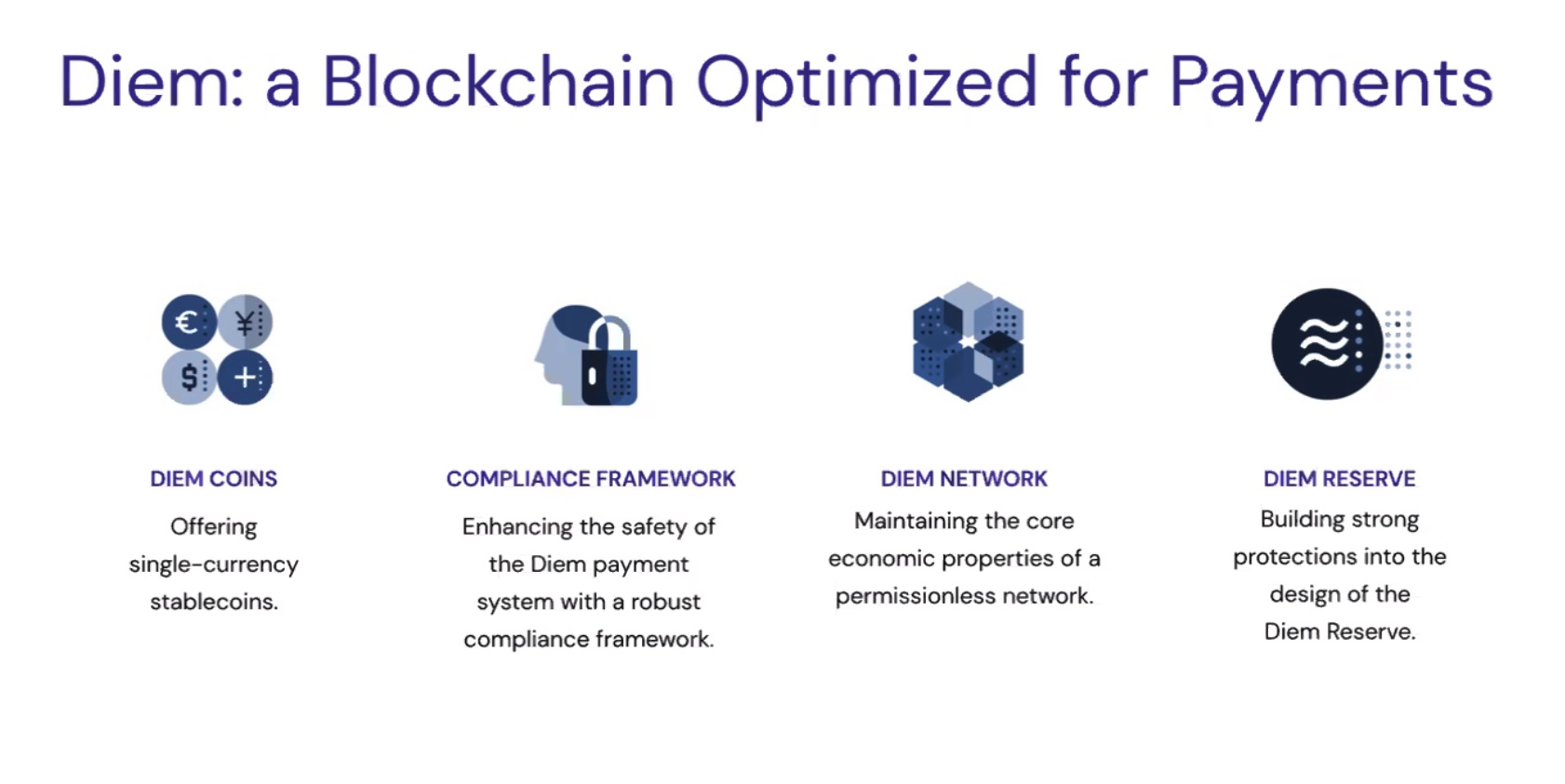

DIEM = "new financial infrastructure"

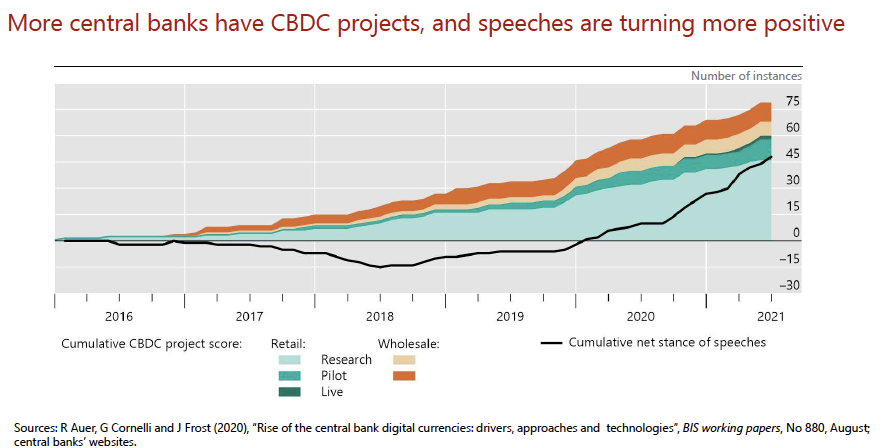

Source: BIS Working Papers No 880 "Rise of the central bank digital currencies: drivers, approaches and technologies" by Raphael Auer, Giulio Cornelli and Jon Frost

CBDCs are on their way

The Bank of Canada's Contingency Plan (Feb 2020):

Consider Issuing CBDC if:

Will they?

Veneris, Park, Long, Puri (2021): BoC is in a legal position to issue a CDBC and there are several legal paths to do so

Can they?

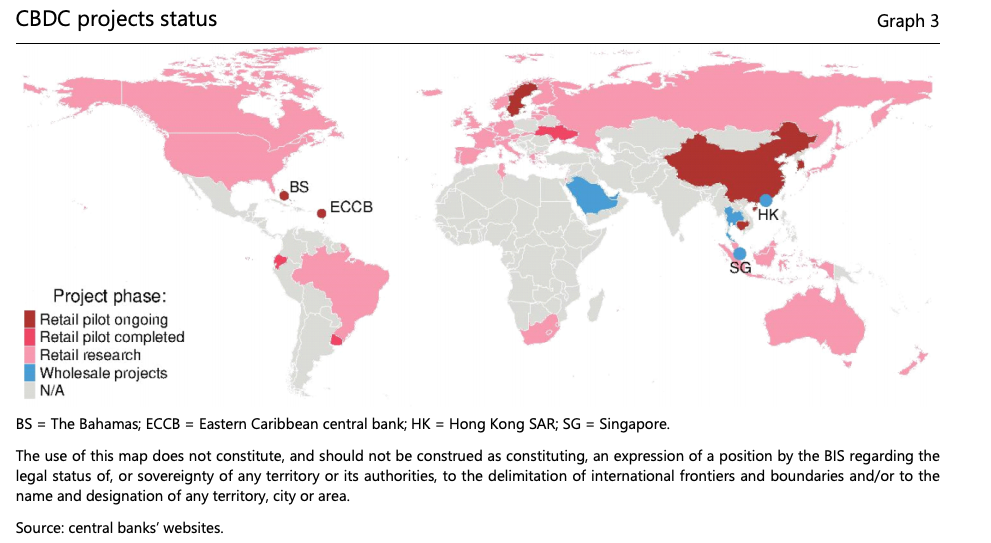

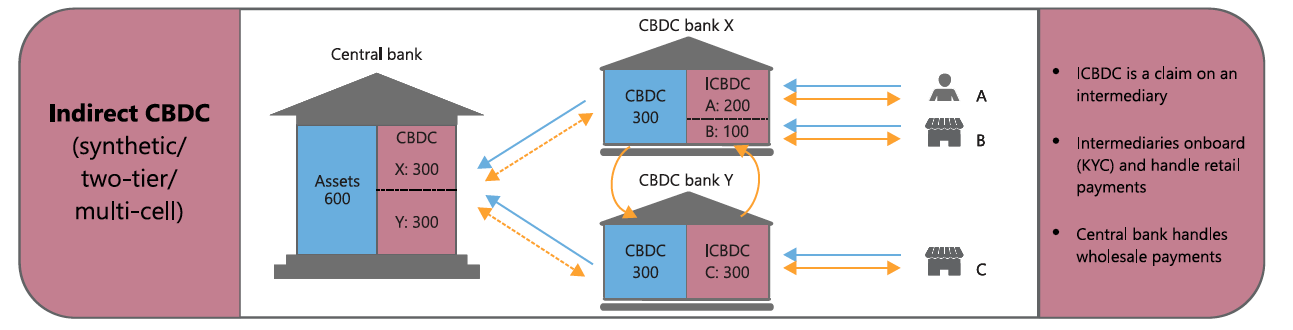

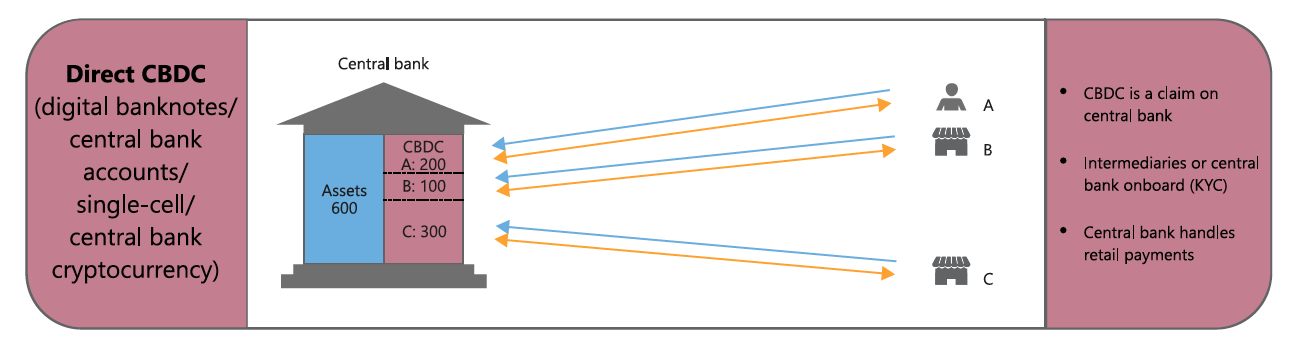

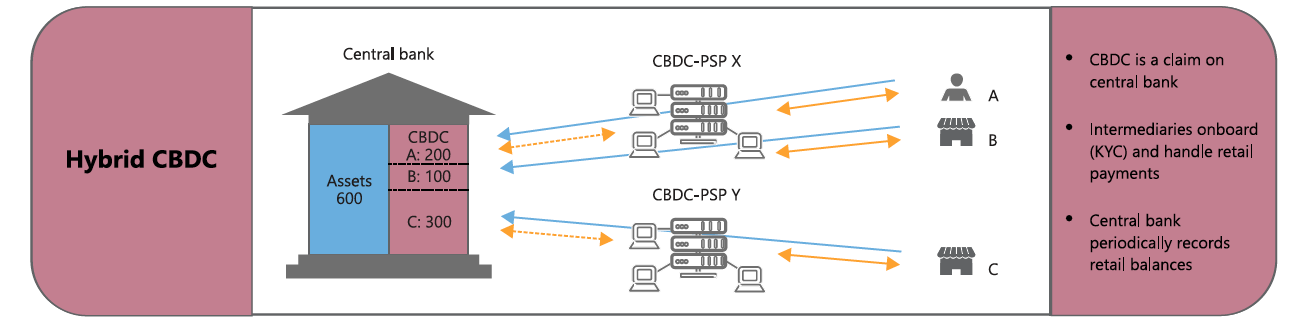

Possible CBDC architectures

Source: BIS Quarterly Review, March 2020

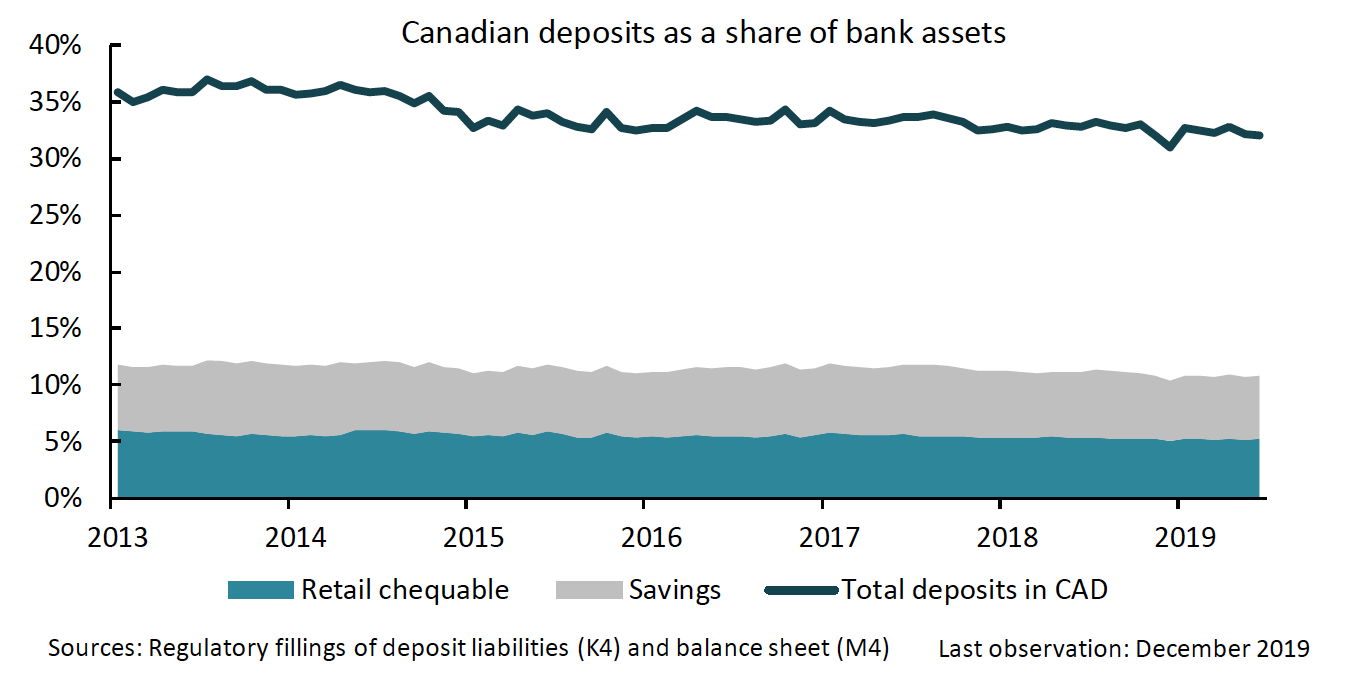

Disintermediation through CBDCs: the common view

BoC analysis (August 2020):

Disintermediation through CBDCs: the evidence

Disintermediation through CBDCs: the evidence (part II)

BoC paper May 2020 (Chiu, Davoodalhosseini, Jiang and Zhu): "[...] a CBDC that competes with bank deposits as a means of payment can compel banks to raise the deposit rate and expand bank intermediation and output. The model [... for US] suggests that a CBDC [...] can raise bank lending by 3.55% and output by 0.50%. "

Federal Reserve Board research by Anderson, Du, and Schlusche (2021): when large U.S. banks lost access to roughly $1 trillion of below-market-rate funding because of the 2016 reform of money-market mutual funds, these banks did not cut back on lending.

Duffie and Krishnamurthy (2016): "By lowering frictions in the payment system, a CBDC should improve the efficiency of money markets and lead to increased lending."

My reading of the evidence:

Final Thoughts

Evolution

CBDCs

Source: Letter to Janet Yellen, Chair of the Financial Stability Oversight Council (FSOC) https://www.warren.senate.gov/imo/media/doc/FSOC%20Crypto%20Letter%2007.26.2021.pdf

“[…] the need for a coordinated and cohesive regulatory strategy to mitigate the growing risks that cryptocurrencies pose to the financial system”

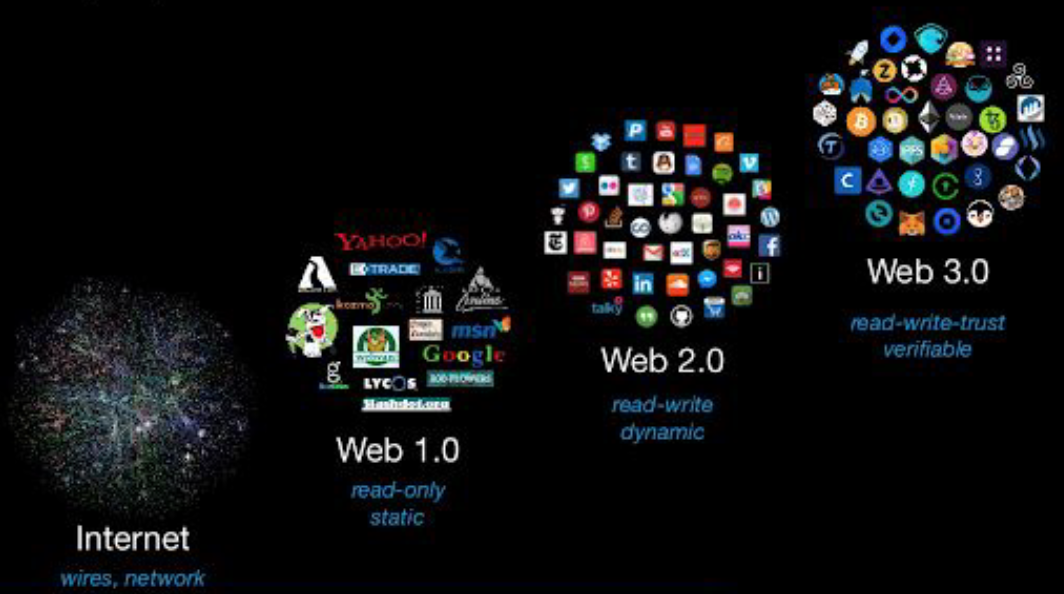

Blockchain = Web 3.0

metaverse =

marriage of the digital and physical world

Web 4.0: The Metaverse and Non-Fungible Tokens

Qualitative description of risks

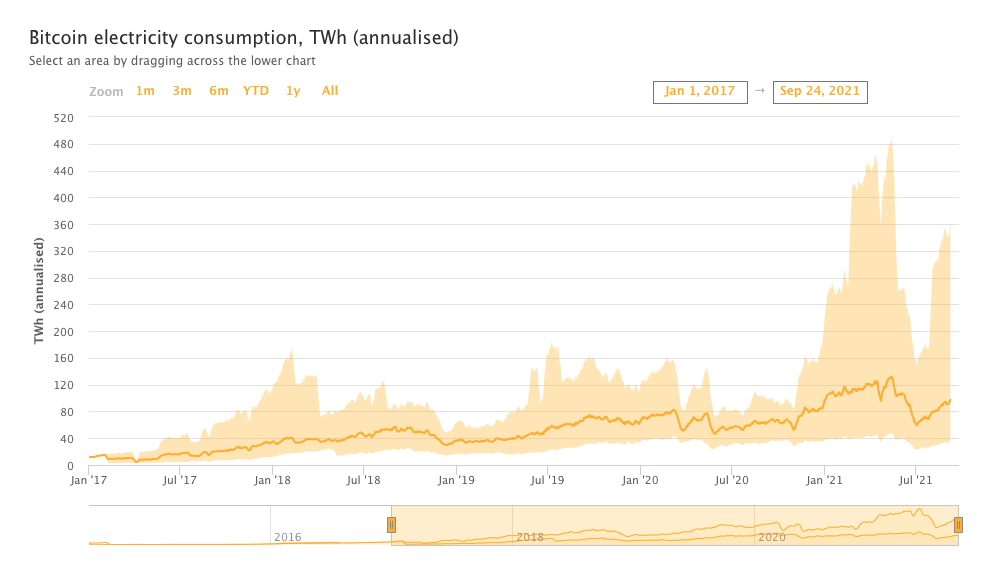

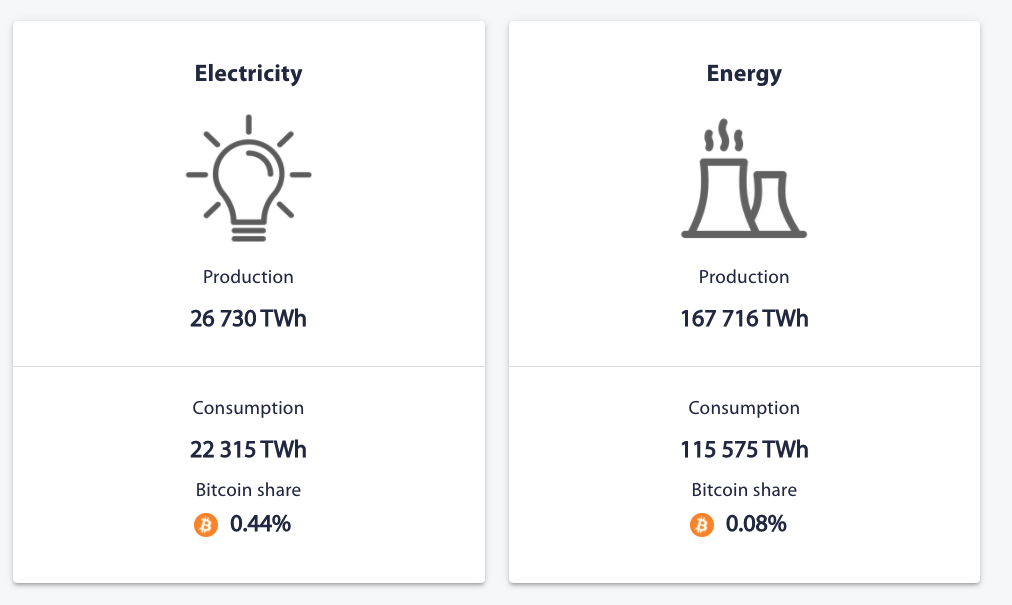

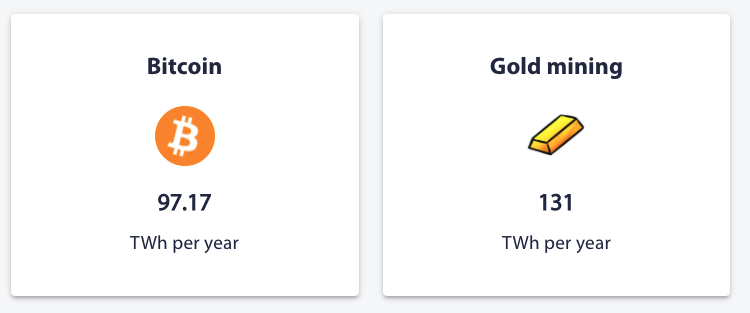

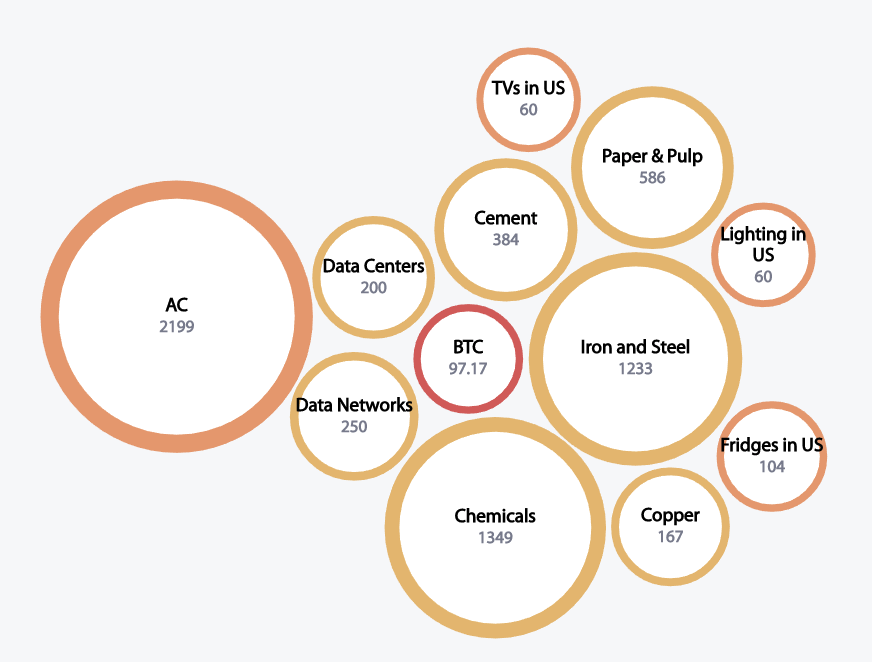

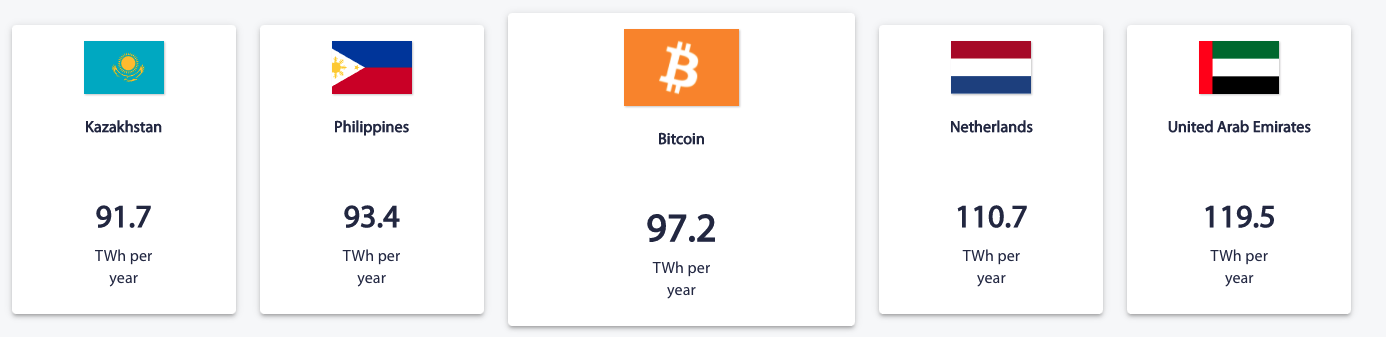

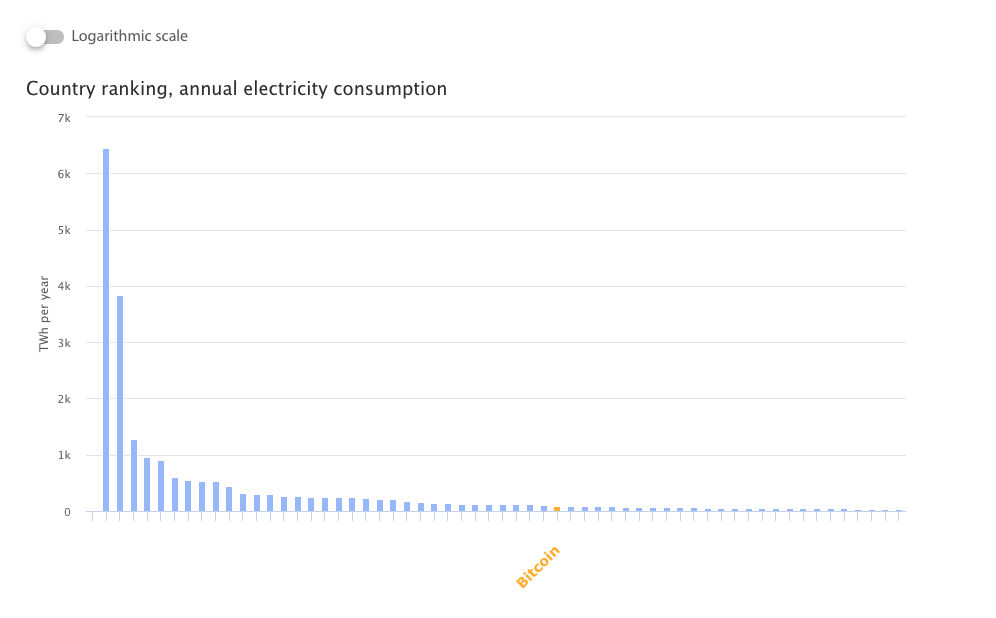

Source: Cambridge Bitcoin Energy Consumption Index https://cbeci.org/

@financeUTM

andreas.park@rotman.utoronto.ca

slides.com/ap248

sites.google.com/site/parkandreas/

youtube.com/user/andreaspark2812/

By Andreas Park

This is the slide deck that I used in a presentation for UofT Alumni on June 10, 2021.