Andreas Park PRO

Professor of Finance at UofT

Andreas Park and Jinhua Wang

SAFE Microstructure Conference 2020

August 18, 2020

more marketplaces

new rules

trading technology advances

new players

"higher market quality"

more liquidity (shares to trade)

lower transaction costs

higher price efficiency

both long-term and at the margin for rule changes (e.g., automated quotes)

Rosu, Solji, Tham (JFQA 2020)

operate autonomously

show/have no feelings

can implement complex strategies across many markets and assets

\(\Rightarrow\) better/faster/stronger "align" prices?

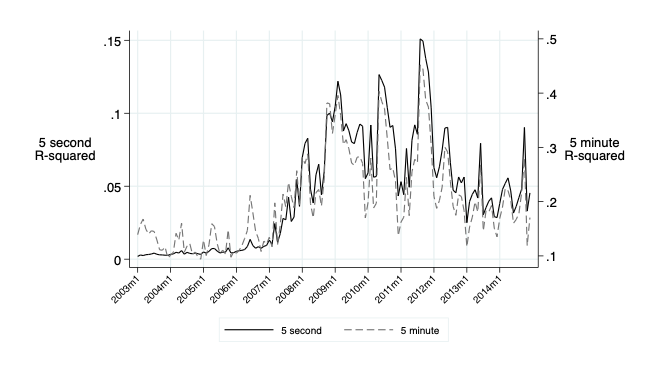

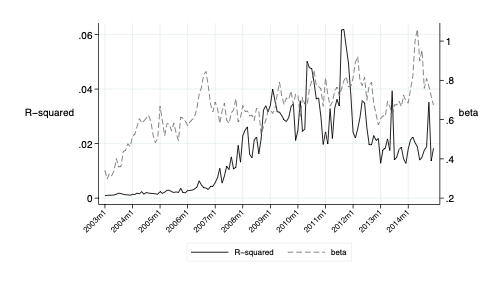

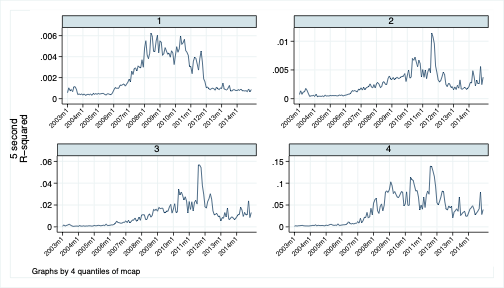

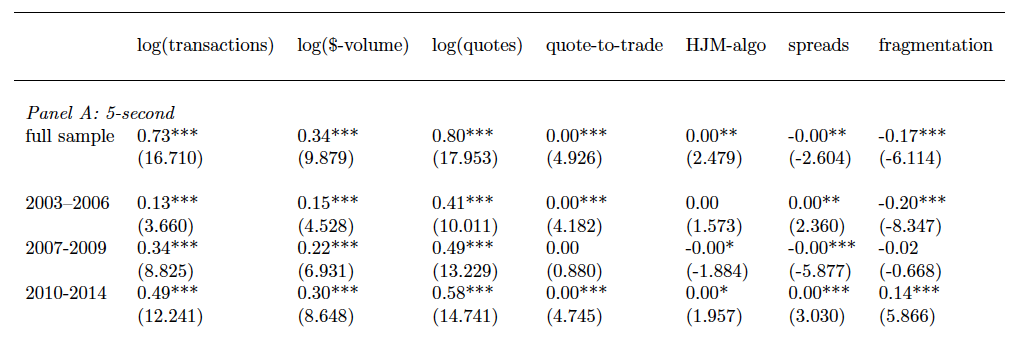

\(R_{it}=\alpha_i+\beta_iR_{mt}+\epsilon_{it} ~~\Rightarrow~~~\mathbb{R}^2\)

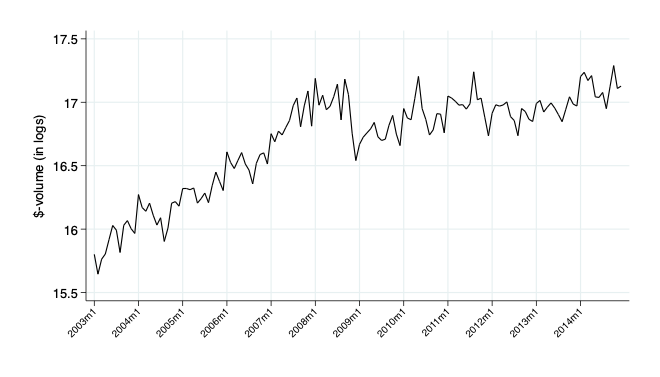

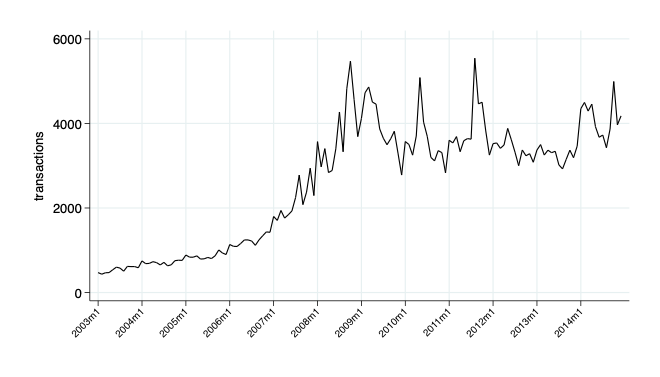

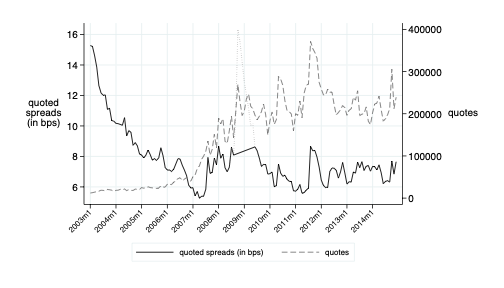

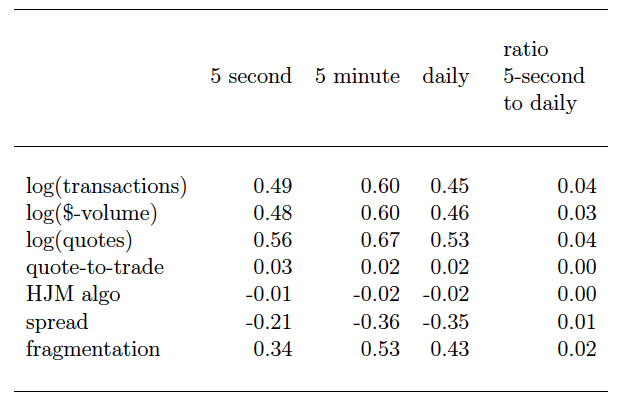

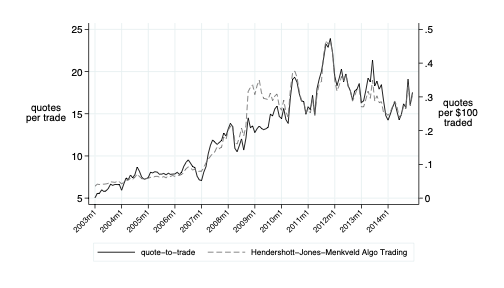

correlation of monthly series: .56

Introduce a "new" (not quite, but not done before) measure to capture impact of bots

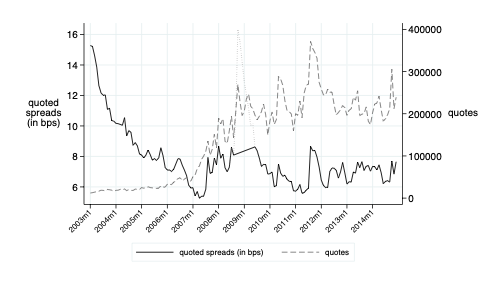

Document the substantial change in the measure across time

Develop a machine learning tool to further underline the causal relationship ("instrumental causal random forests")

Show with traditional means that the shift in the measure was caused by bots

\(R_{it}=\alpha_i+\beta_iR_{mt}+\epsilon_{it} .\)

Still: the increase in R-squared over time is persistent and robust across all kinds of subsamples and splits of the data

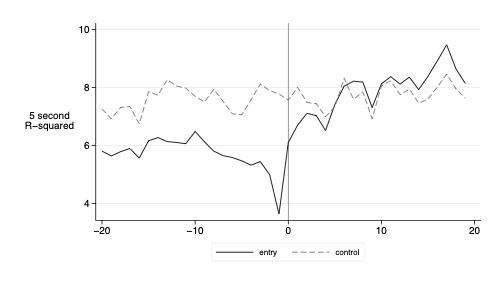

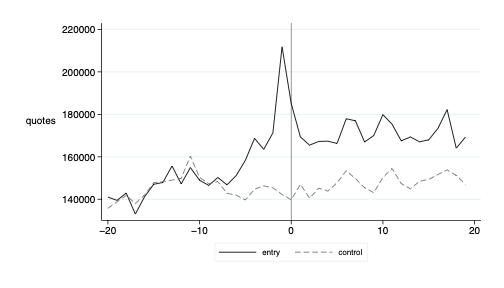

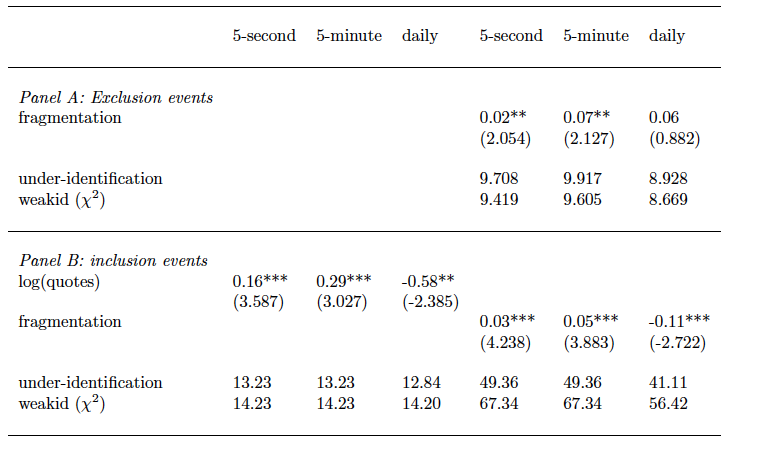

Entry

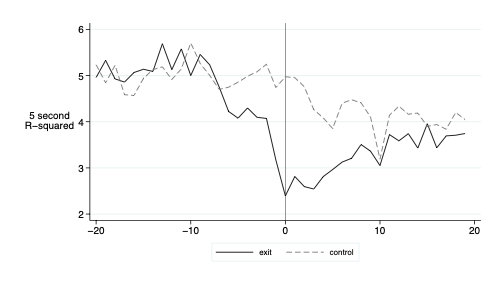

Exit

effect strongest later in sample

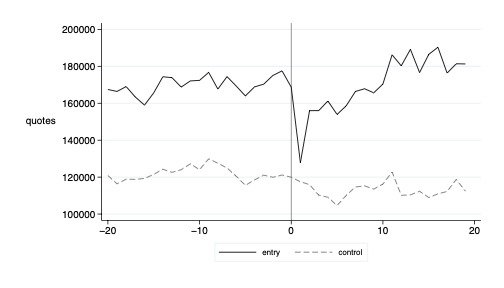

Entry

Exit

effect strongest later in sample

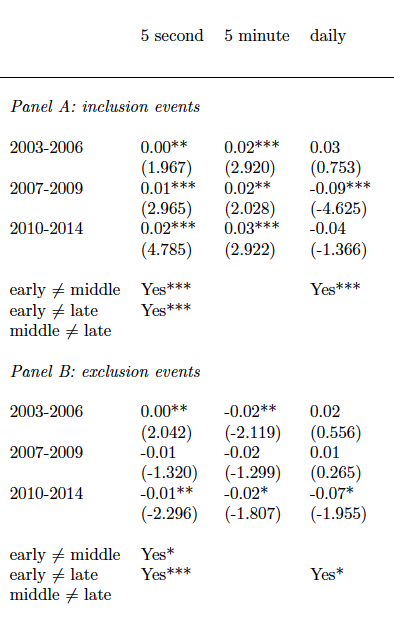

statistically not significant

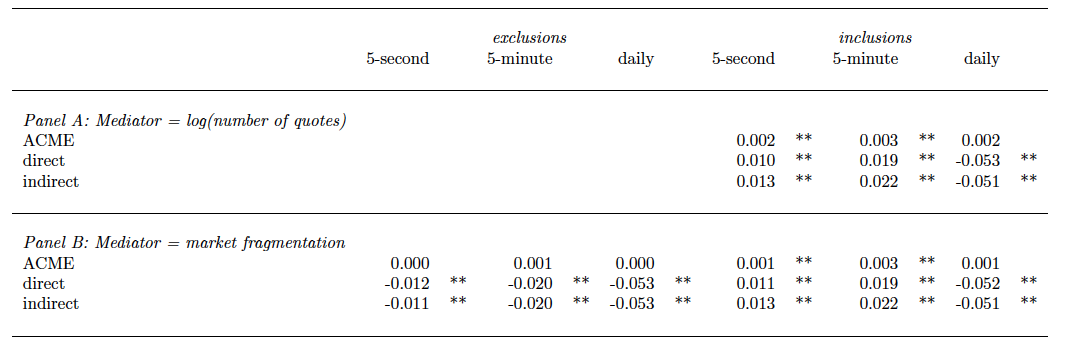

Idea: Mediation analysis allows both a direct and an indirect effect

*ACME=Average Causal Mediation Effect (the mediated effect)

*

*

Linear Model relies on correctness of functional form specification.

Linear causal effect models can only estimate average treatment effect at aggregate level & ignores heterogeneity

Preserves treatment effect heterogeneity

NB: methods and tools developed here are all available on Jinhua's GitHub

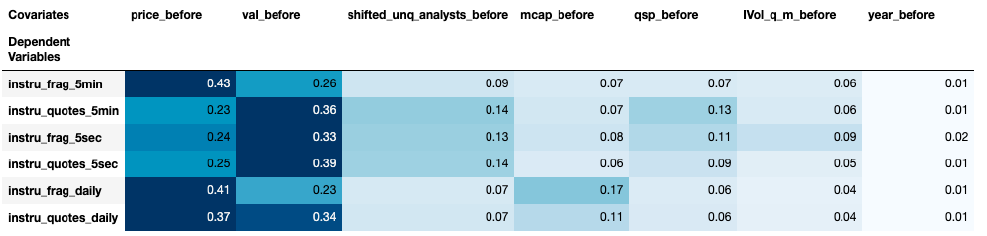

The numbers in the table are the percentage splits on a particular covariate. The higher the percentage, the deeper the gradient in the cell, and the more important the variable is in the causal forest.

Introduce a "new" (not quite, but not done before) measure to capture impact of bots

Document the substantial change in the measure across time

Develop a machine learning tool to further underline the causal relationship ("instrumental causal random forests")

Show with traditional means that the shift in the measure was caused by bots

@financeUTM

andreas.park@rotman.utoronto.ca

slides.com/ap248

sites.google.com/site/parkandreas/

youtube.com/user/andreaspark2812/

identified a shift in "explainability of intra-day market model"

linked this shift to bot trading, with indications of causality from index inclusions

explainability seems a prerequisite for any "real" asset pricing model

still open questions and many avenues for possible future research

Hendershott, Jones, Menkveld (JF 2011)

correlation of monthly series: .56

By Andreas Park