Andreas Park PRO

Professor of Finance at UofT

Authors:

Date:

Andreas Veneris, Andreas Park, Fan Long, Poonam Puri

February 10, 2021

\(-38\%\)

The Internet of Things

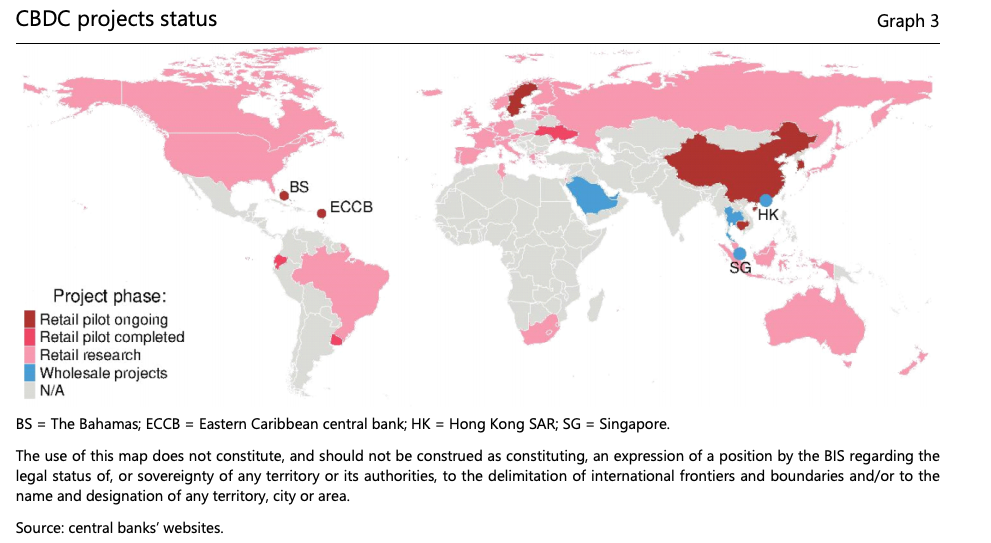

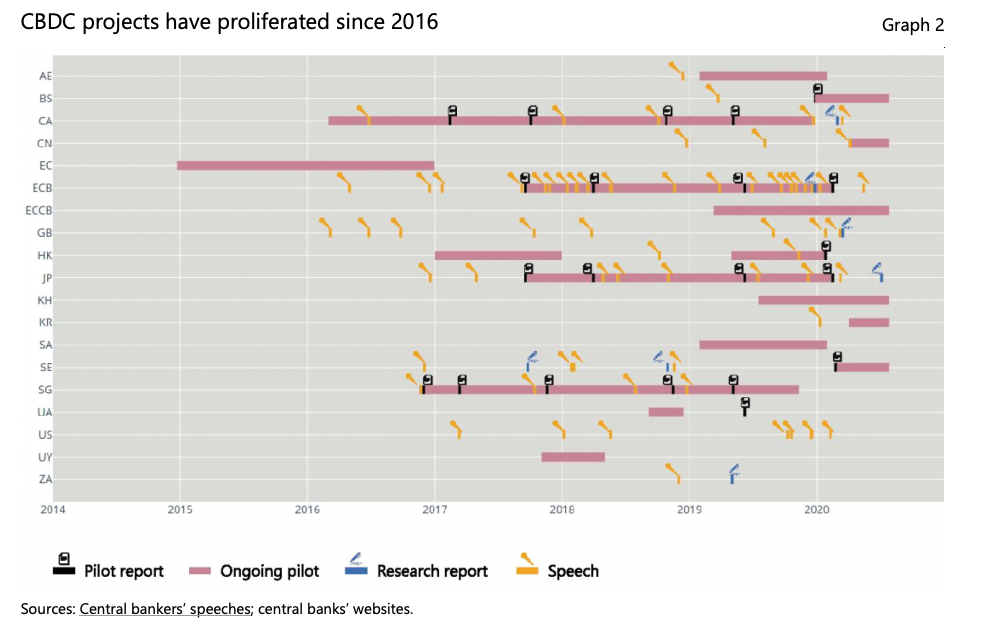

Source: BIS Working Papers No 880 "Rise of the central bank digital currencies: drivers, approaches and technologies" by Raphael Auer, Giulio Cornelli and Jon Frost

user obtains wallet

registers wallet address via e-KYC

NB processes transactions among whitelisted wallets quasi-anonymously

issues transaction instructions

checks

( )

( )

initiates wallet transfer

record keeping and AML/CFT processing

each offline card is linked to a KYC-ed user/e-wallet

NB transfers CBDL with serial numbers to the card

user pays offline

user pays offline

user pays offline

user pays offline

user initiates transfer from card to e-wallet

user initiates transfer from e-wallet to card

LVTS/

Lynx

consumers can initiate EFTs from chequing account at commercial bank to CBDL wallet at NB

existing payments system facilitates transfers to CBDL system

NB has reserve account at BoC to link with commercial banks

NB handles all

CBDL payments

overnight house- keeping

*

service example: internal payment-reward system

service example: small business bookkeeping

NB transitions into a validator node

a

b

c

d

e

f

g

blockchain network with validators and nodes

Central Bank-issued Digital Loonie as a common infrastructure

provide a public good that enables Canadians to participate in the digital economy without being subjected to third-party commercial interests

e-KYC using existing resources

two-stage process

Stage 1: do-it-alone to kickstart

Stage 2: enable private sector innovation

By Andreas Park

Final Report for the Bank of Canada's 2020-21 Model X Challenge by Andreas Veneris, Andreas Park, Fan Long, and Poonam Puri. Video presentation available here: https://www.youtube.com/playlist?list=PLTmzBTSqnXduG8kmgSYUx0eblM50BQcFw