Andreas Park PRO

Professor of Finance at UofT

by Andreas Park

Tokenomics 2021

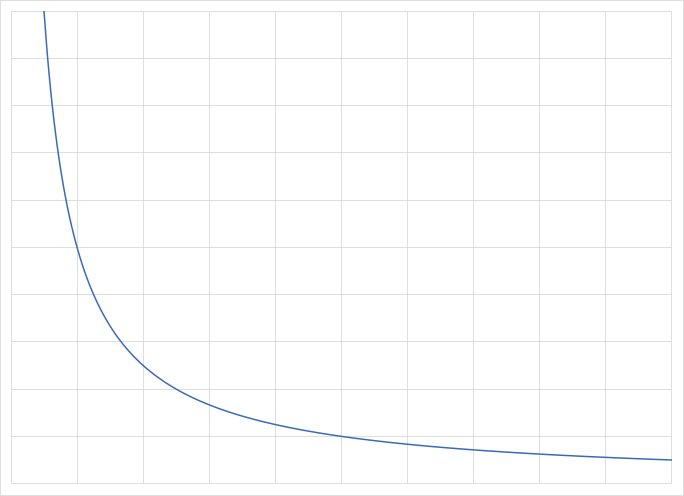

Automated Market Making?

How do you set the price?

Price mechanism:

Prices

Exploits of Liquidity Demanders

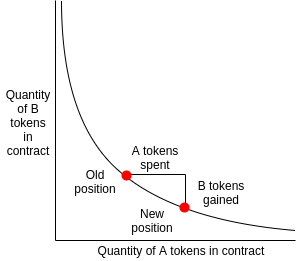

\(X\)

\(Y\)

normal trade: sell \(x\) \(\to\) get \(y'\)

\(Y-y'\)

\(X+x\)

front-running/sandwich trade:

\(Y-y'-y''\)

\(X+2x\)

\(y'>y''~\Rightarrow\)

front-running is intrinsically profitable

Disclaimer:

a

b

c

d

e

f

g

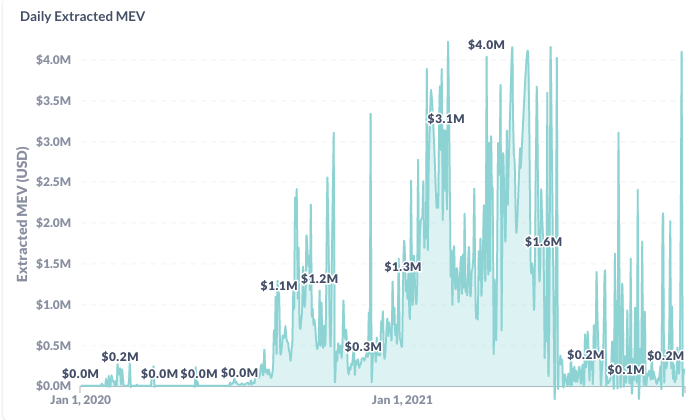

Source: flashbots.net

Risk Compensation for Liquidity Providers

hard coded pricing function

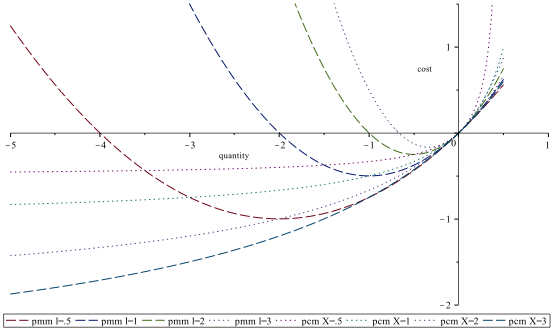

Two pricing approaches in the economics literature

inputs

Proposition: For \(x>x^*\), constant product provides "higher" risk compensation than what market competition would yield, for \(x<x^*\) it is the reverse.

Excessive Trading?

Simple question: does it pay to split an order?

(the papers has some other tests for excessive trading)

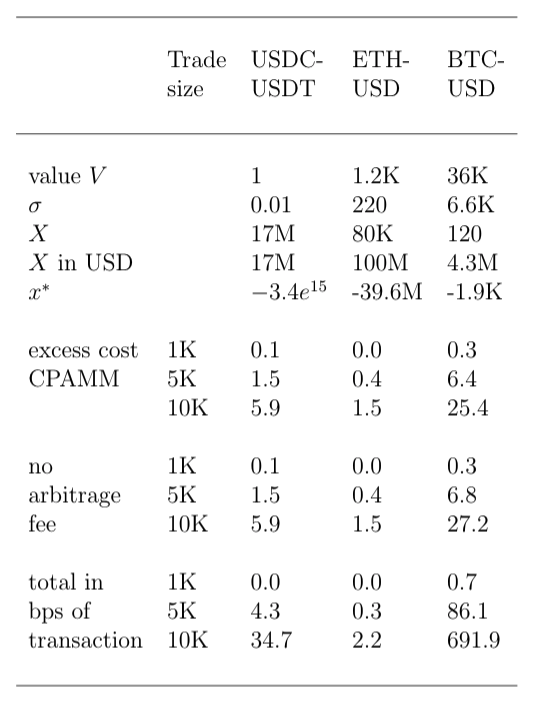

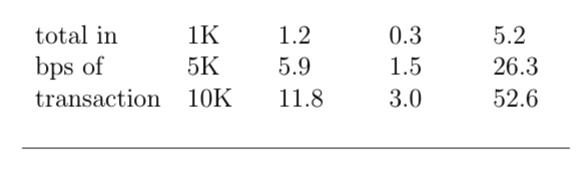

Comparison: market vs CPMM

Comparison of pricing

Constant product pricing

"Standard" economic model-based pricing

uniform

discriminatory

profitable front-running/sandwich trades

fair risk compensation for LPs

profitable order splitting (excessive trades)

Remedies?

no front-running if:

front-running profit < 2\(\times\) submitted fee

Small hiccup: front-runner often is the miner

What does the data say?

@financeUTM

andreas.park@rotman.utoronto.ca

slides.com/ap248

sites.google.com/site/parkandreas/

youtube.com/user/andreaspark2812/

By Andreas Park