Andreas Park PRO

Professor of Finance at UofT

Instructors: Andreas Park & Zissis Poulos

Rotman – MBA

5-minute version:

What is a blockchain?

blockchain=

an infrastructure for digital resource transfers

5-minute version:

What is a cryptocurrency?

cryptocurrency =

internal payment mechanism to pay for operation of a blockchain

5-minute version:

What is Decentralized Finance?

decentralized finance =

provision of financial services without the necessary involvement of a traditional financial intermediary based on blockchain technology

in practice: new financial infrastructure that will be a common resource

payments

stocks, bonds, and options

swaps, CDS, MBS, CDOs

insurance contracts

\(\vdots\)

Source: Harvey, Ramachandran, and Santoro (2020)

\(\Rightarrow\) Can we decentralize finance?

Partnerships

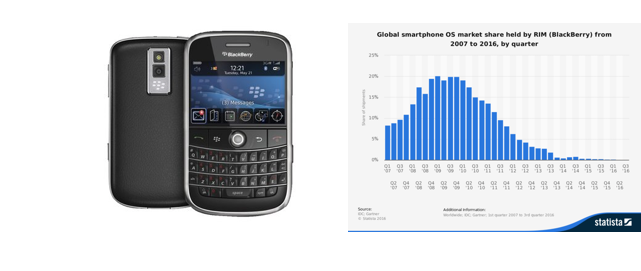

Nokia's market shares for devices:

What happened and can it happen to banks?

What did they pay for?

What do people value?

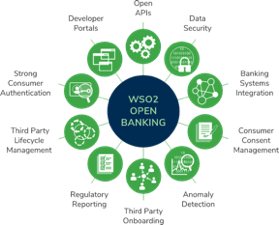

If banks move all data into "the cloud," why do we need banks?

Siloed banks

Cloud computing and cloud storage

Open banking and open data

The past (and the present?)

The present and near future

3-5 years in the future

5-10 years in the future

Platforms?

Banks?

Tech firms?

Silos vs Common Infrastructures

Change ledger entry locally

Sue's bank transfers from Sue's account to Bob's bank's account

Bob's bank transfers from its account to Bob's account

Sue's bank transfers from Sue's account to its own account

Bob's bank transfers from its account to Bob's account

Central Bank

Central bank transfers from Sue's bank's account to Bob's bank's account

Sue's bank transfers from Sue's account to its own account

Bob's bank transfers from its account to Bob's account

use the Swift network of correspondent banks

very complex

many parties

lots of frictions and points of failure

very expensive

How does it all work and why?

A deep dive into the "How?"

Cryptography: only Sue can spend her money

Problem: double-spending

How can we trust that

Contains transaction from Sue to Bob

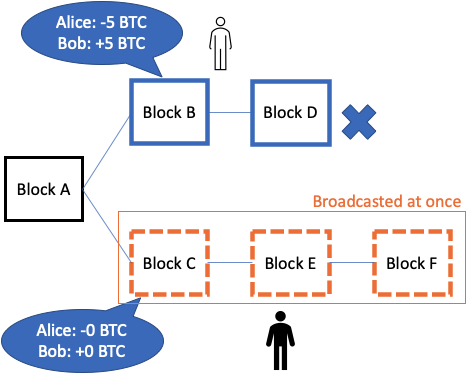

Question: Can Sue rewrite history?

Where to add a new block B7?

Contains transaction from Sue to Bob

Sue wants to undo the transaction by rewriting history with B6

Sue's objective

What does it take?

How does Proof of Work prevent this?

Back of the envelope calculation

Double spend attack prevention

Basic idea of competitive equilibrium

aggregate mining cost = aggregate reward

Double spending attack

condition that prevents it

(Chiu & Koeppl RFS 2018)

How do you agree though that something happened, or, what is consensus?

\(t\)

\(t\)

\(t\)

\(t\)

\(t\)

\(t\)

\(t\)

\(t\)

\(t\)

\(t\)

\(t\)

\(x\)

\(t\)

\(t\)

\(t\)

\(t\)

\(t\)

\(x\)

\(t,t,x\)

\(t,t,x\)

\(t,t,t\)

\(x\)

\(y\)

\(z\)

\(y\)

\(x\)

\(z\)

\(y\)

\(x\)

\(z\)

\(x,y.z\)

\(x,y,z\)

\(x,y,z\)

Equilibrium

Blockchain requirement

= 00000xd4we...

= 00000xd4we...

= 00000xd4we...

consensus is reached if hash starts with right number of leading zeros

Challenges

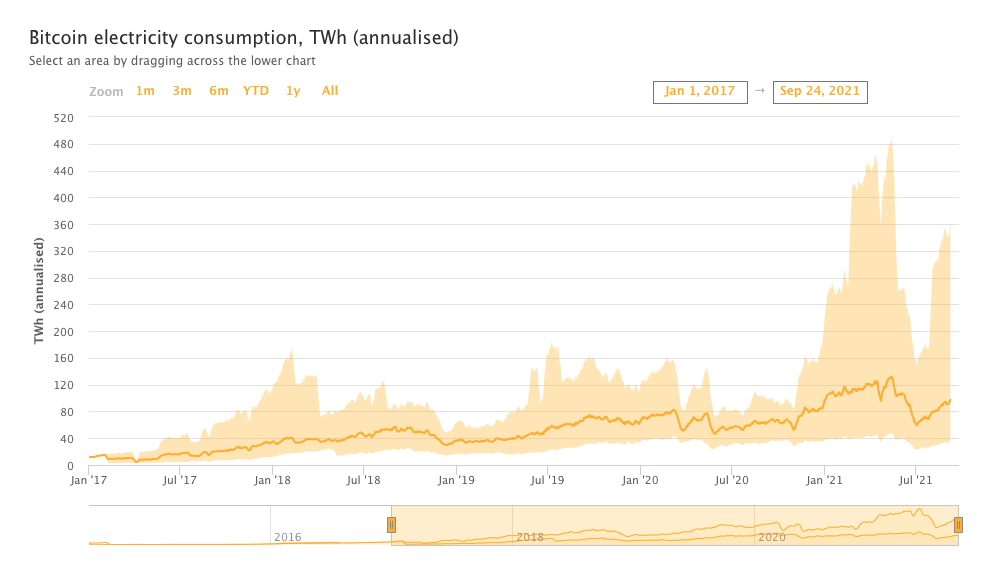

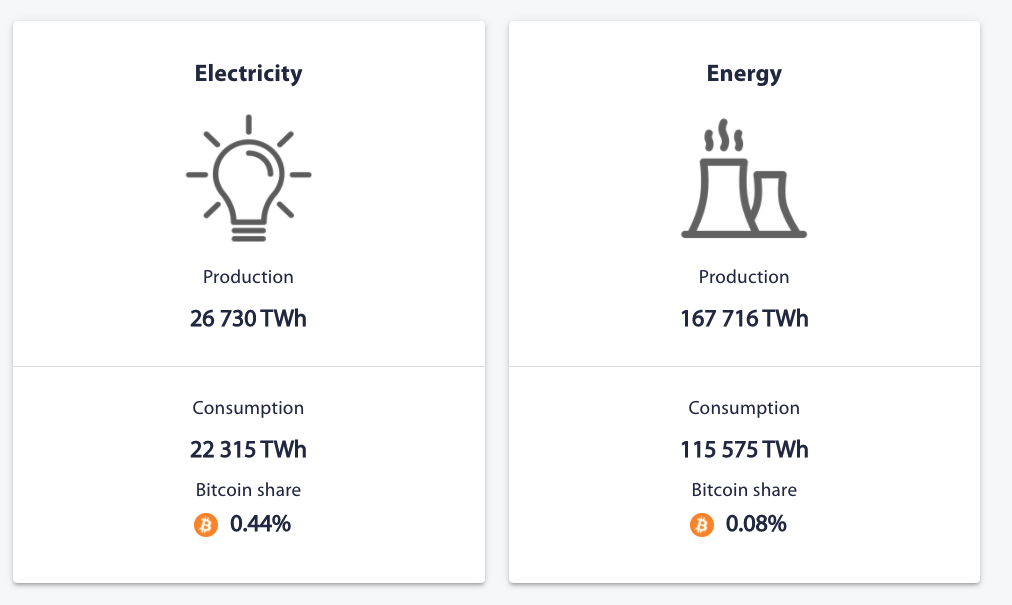

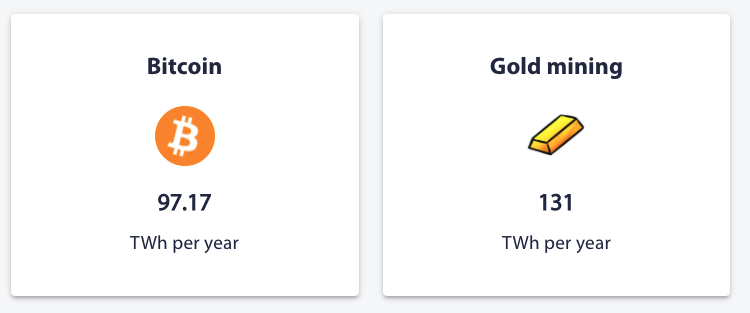

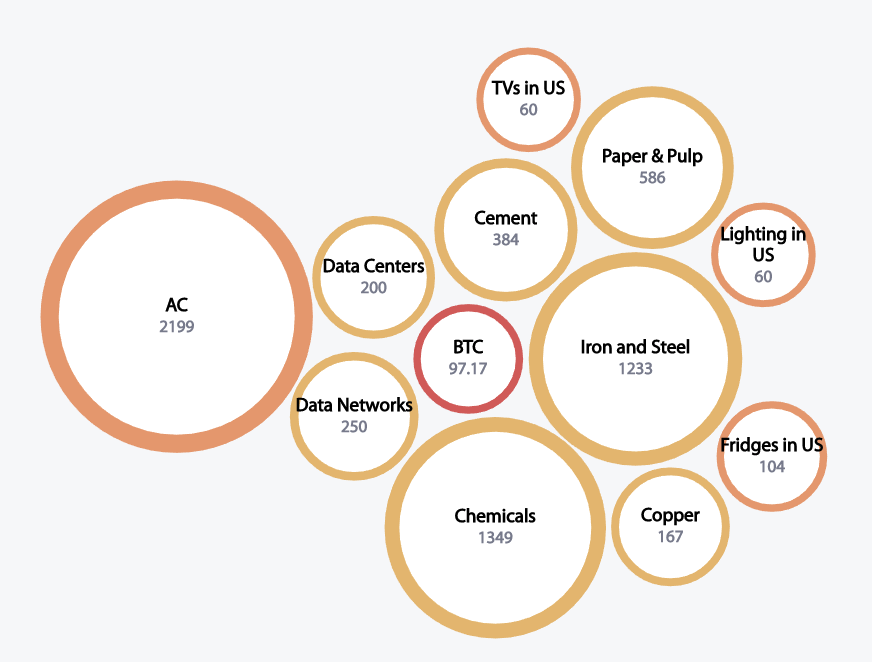

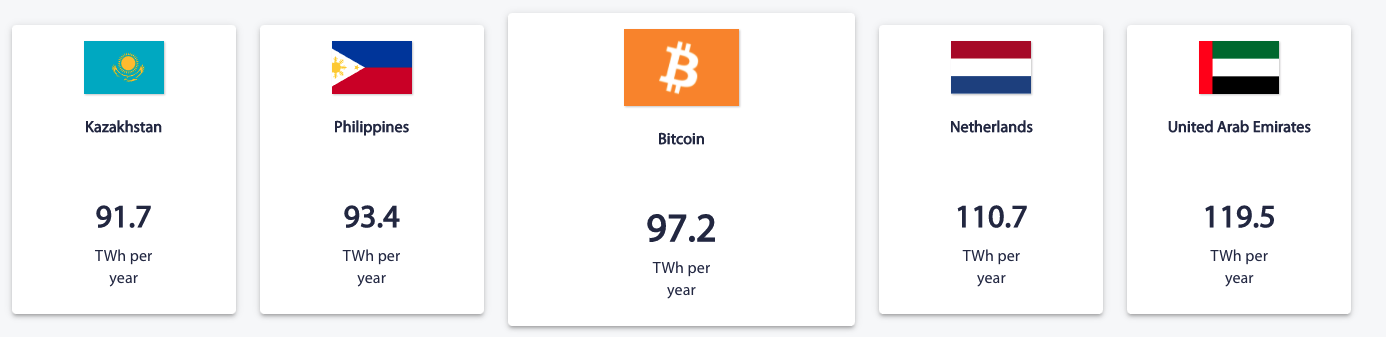

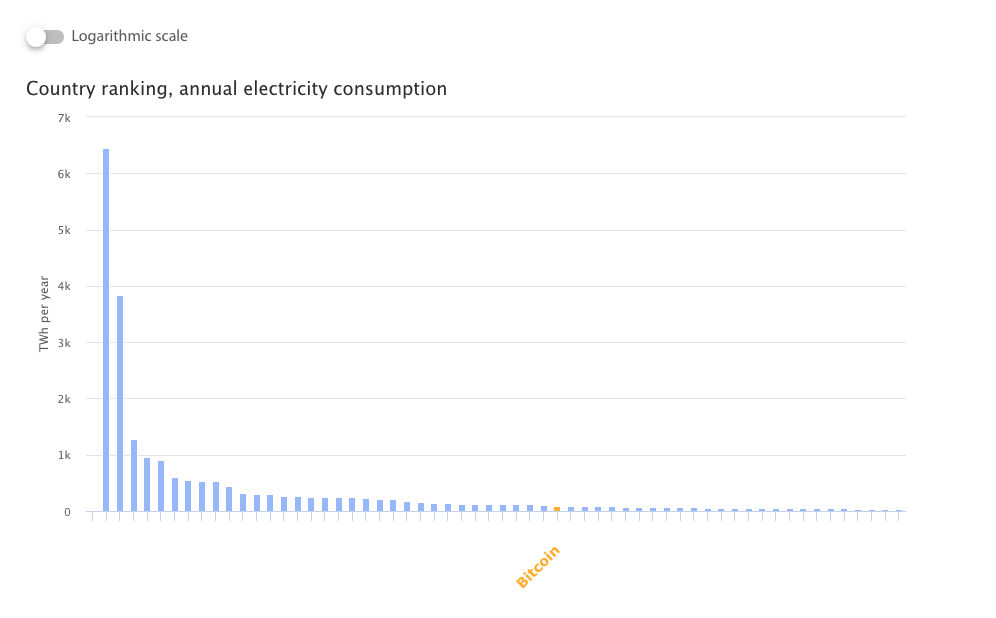

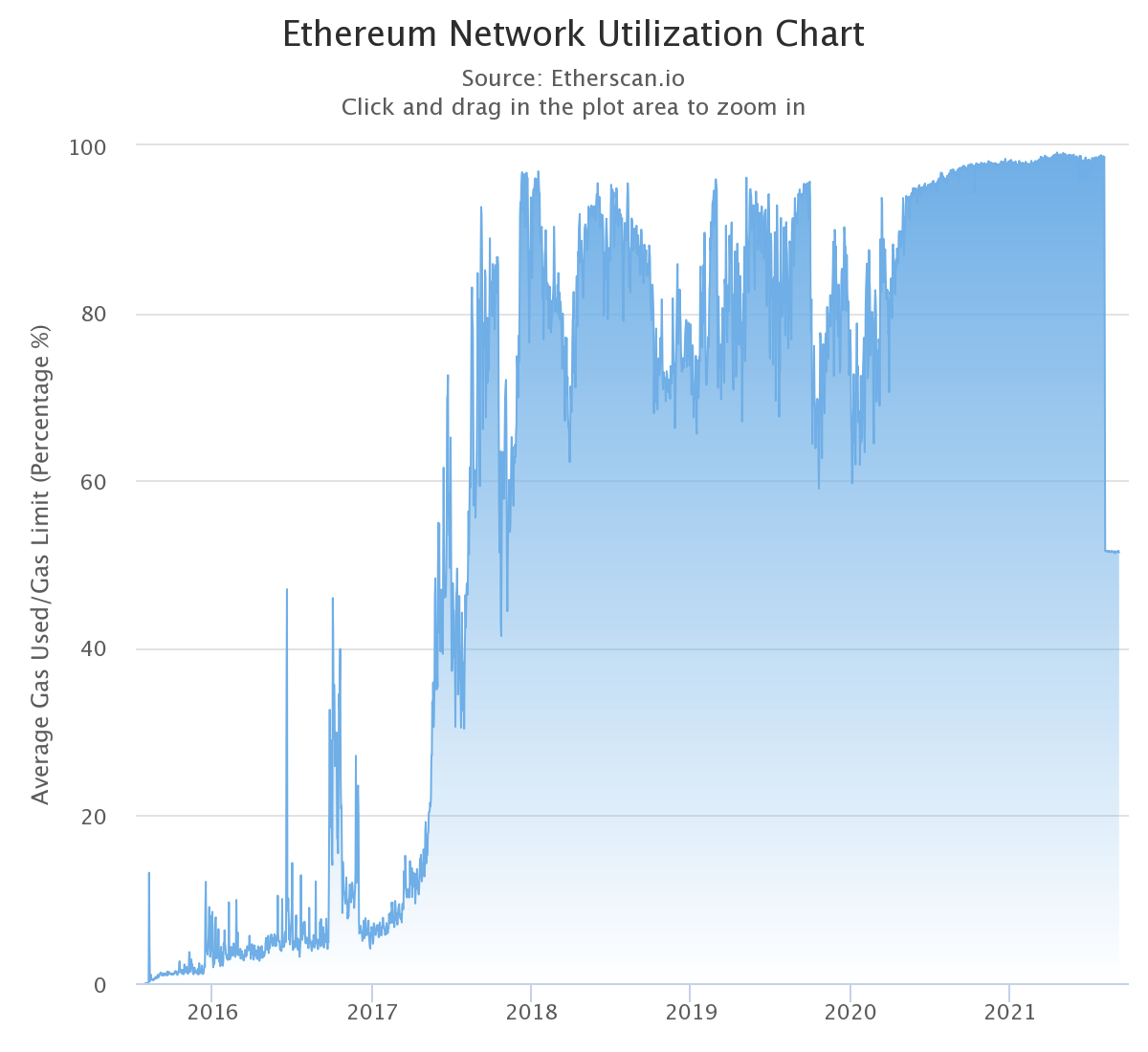

Source: Cambridge Bitcoin Energy Consumption Index https://cbeci.org/

Root Problem

Solutions

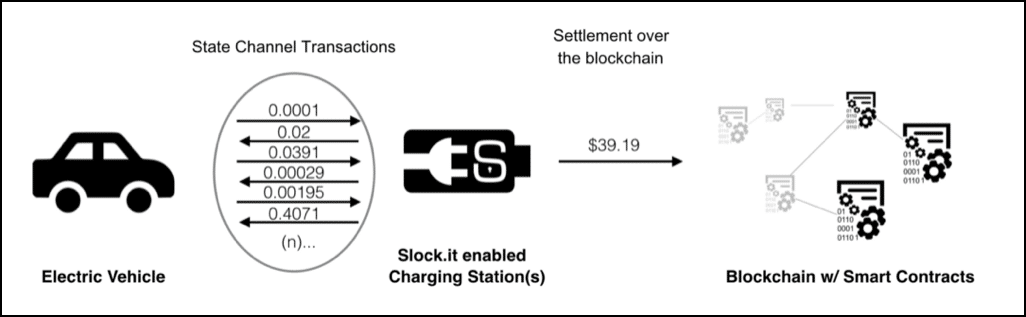

https://blog.stephantual.com/what-are-state-channels-32a81f7accab

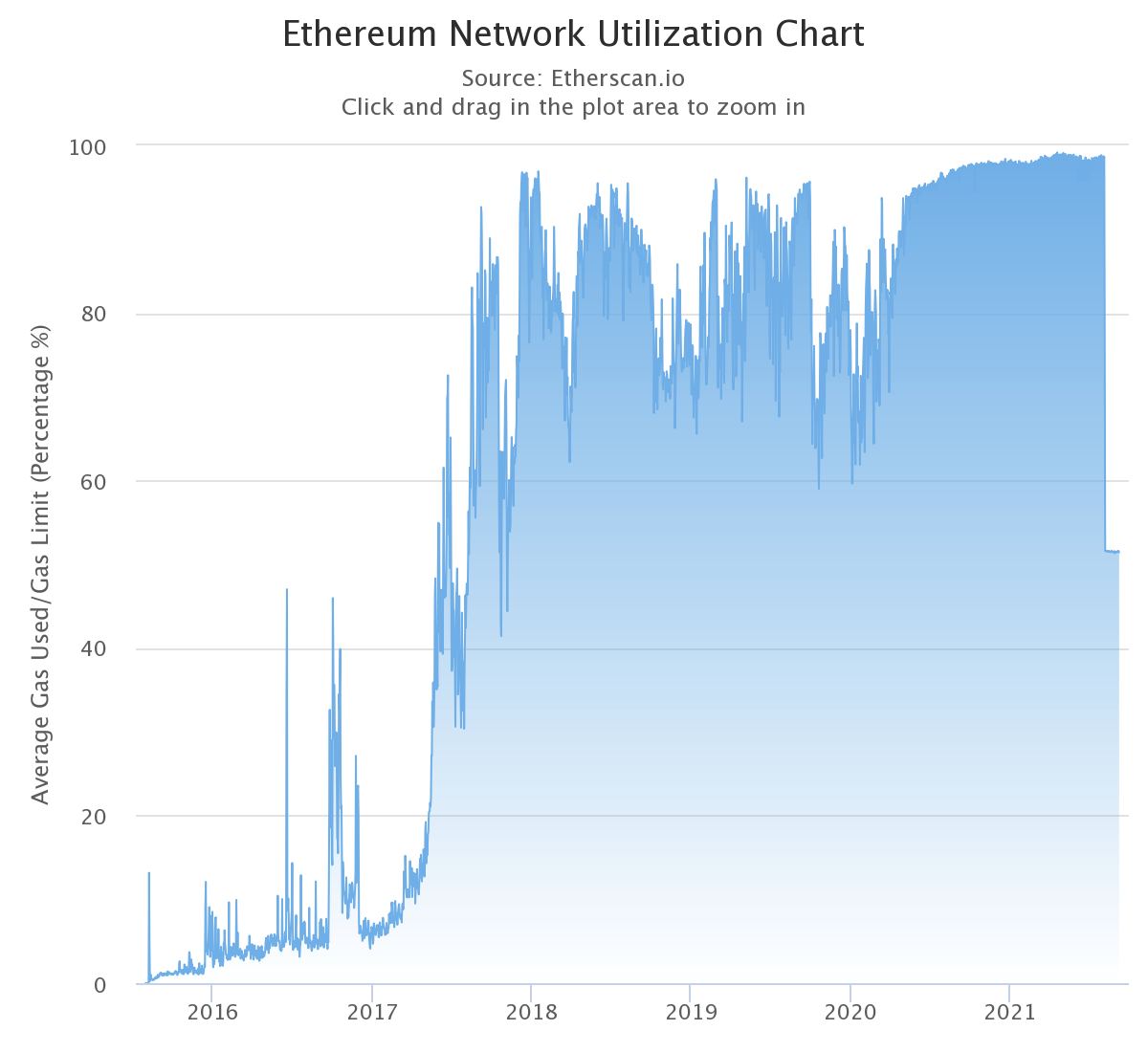

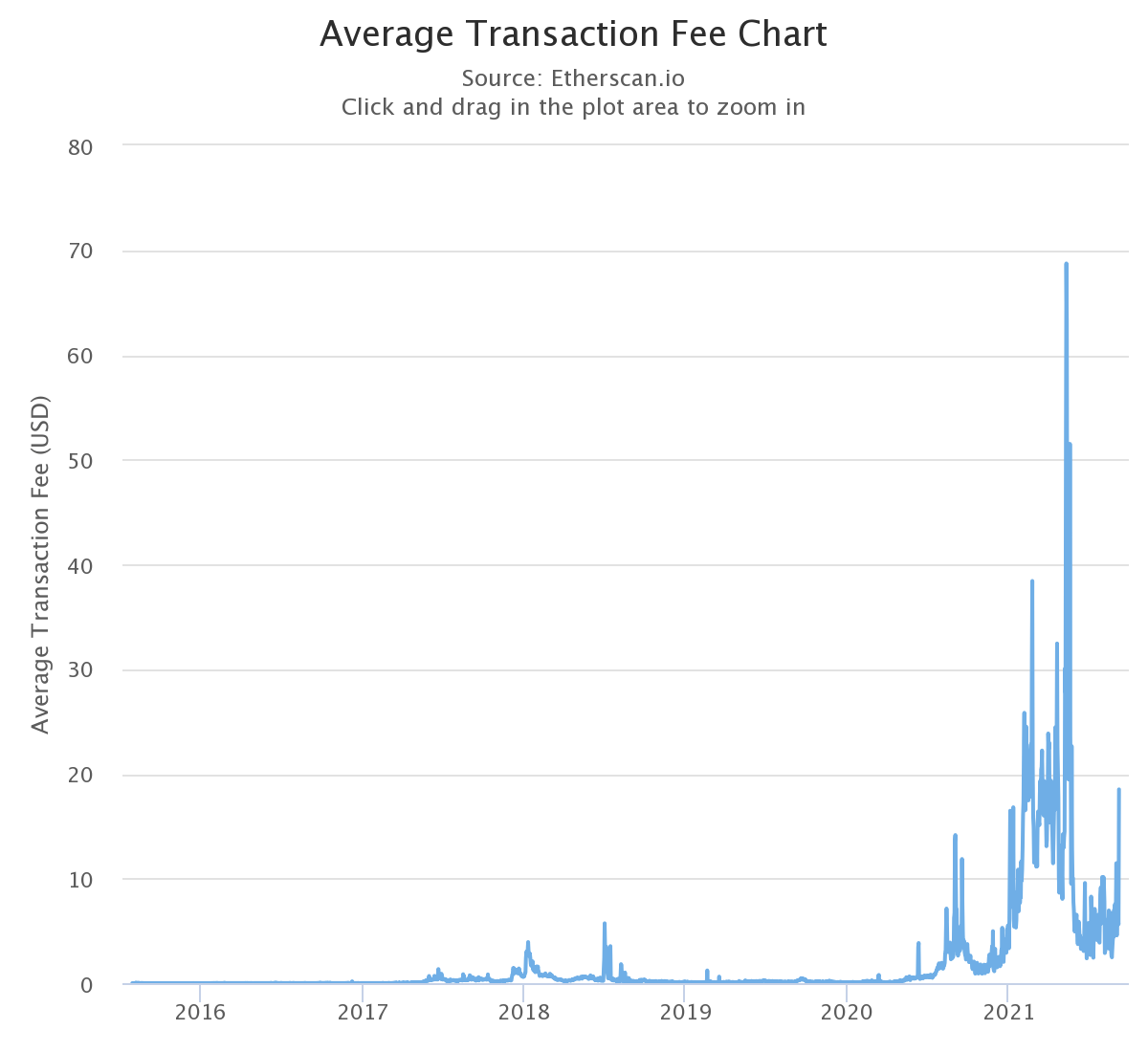

Transaction Processing

Disclaimer: token design strongly influenced by yours truly

going back to Budish (2018)

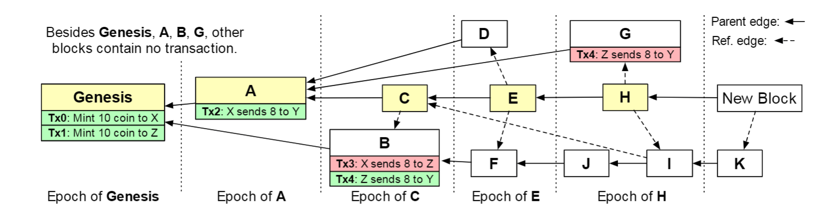

Serial Chain

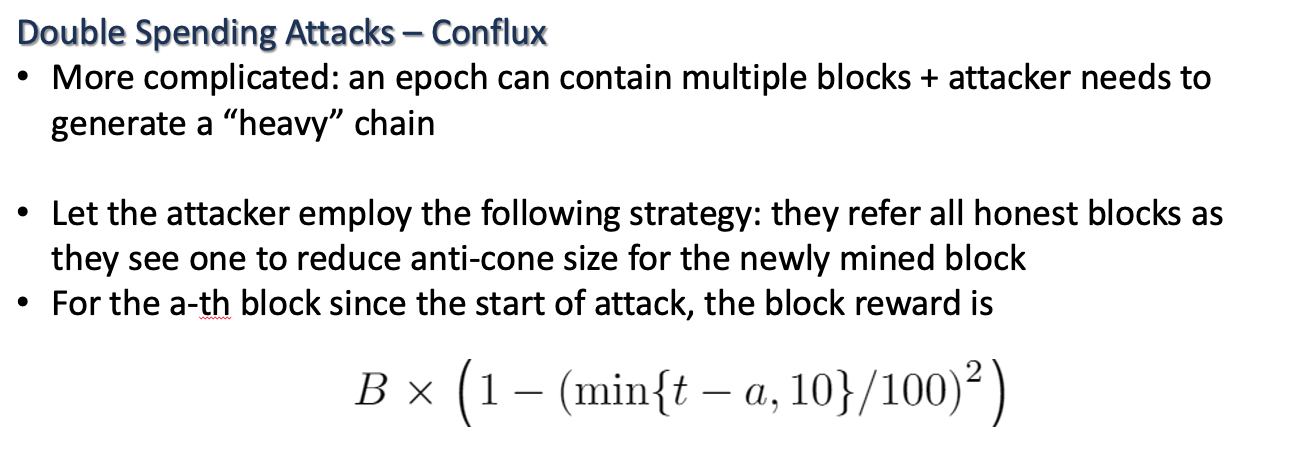

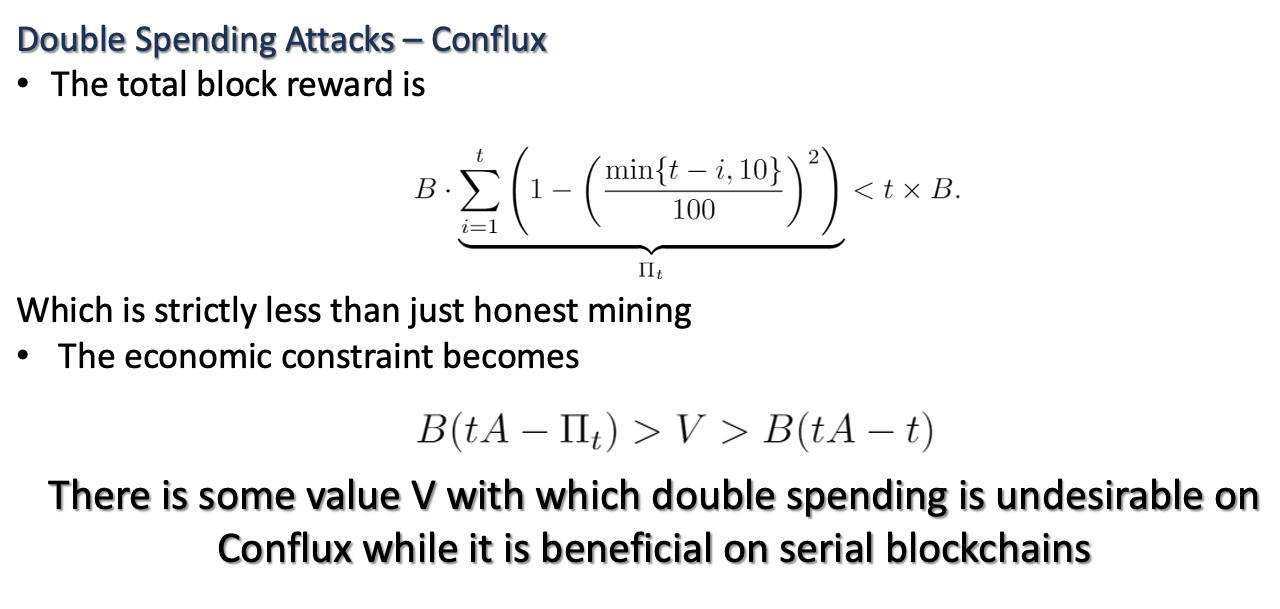

Conflux Chain

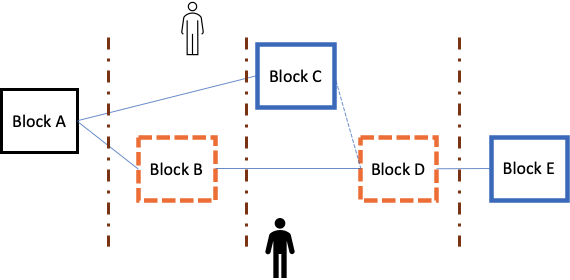

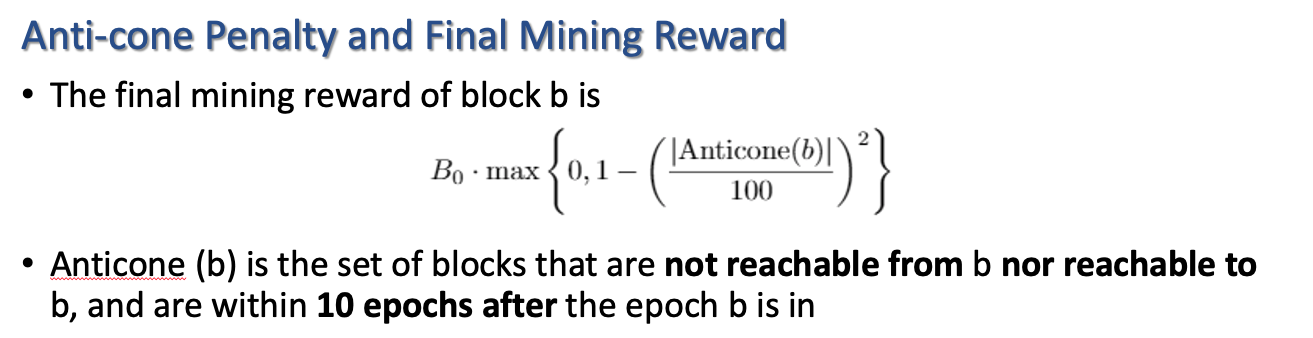

In Conflux, withholding a block leads to greater anti-cone size

Intuition: Anticone = blocks created without properly referencing others blocks in its vicinity

Where to add a new block B7?

My personal problem: I have not yet seen a convincing theoretical model of PoS

economic result: Fahad Saleh (2021) Review of Financial Studies, "Blockchain Without Waste: Proof-of-Stake" shows that PoS is an equilibrium

current state:

| transactions per second | T per 12 hours (business day) | |

|---|---|---|

| Bitcoin | 7 | 302,400 |

| Ethereum | 30 | 1,296,000 |

| Algorand | 2000 | 86,400,000 |

| Conflux | 4000 | 172,800,000 |

| Athereum | 5000 | 216,000,000 |

| Payments Canada ACSS | 648 | 28,000,000 |

| US retail | 7639 | 330,000,000 |

| Canada number of equity trades | 46 | 2,000,000 |

| Orders on Canadian equity markets | 3588 | 155,000,000 |

Tweaks: lighting network (BTC) or side chains, SegWit, blocksize possible, but there are limits

microtransactions, IoT, and other smart contract use cases place very high demands

What can it for finance, what are problems and obstacles?

Sue wants to sell ABX

Bob wants to buy ABX

sell order

buy order

Clearing House

Stock Exchange

Broker

Broker

3rd party tech

custodian

custodian

record beneficial ownership

central bank for payment

Evolution

vs

"Let me just say how impressed I am with Ethereum...If Bitcoin is email ––a one-trick pony, so to speak, but obviously revolutionary–– Ethereum goes far beyond that; it's more like the Internet...The whole idea of DeFi really is, number one, it’s obviously revolutionary, and I think at the end of the day could lead to a massive disintermediation of the financial system and the traditional players."

Heath P. Tarbert, CFTC Chairman, October 2020

moving value (remittances)

digital money: real-time settlement, reduced reserves

tokenization of assets

automization of contract payments

securitization

systems and infrastructure reorganization

digital identity

new forms of financial contracts, assets, and forms of financing

Private Sector Solutions

Who gets to update?

Can a higher body prevent

transactions?

Can the past be altered?

consensus

immutability

censorship resistence

open to anyone

no one can be excluded

past cannot be changed

high visibility of transactions

open-access eco-system

slow governance

privacy only at a cost

joint control and governance

straightforward KYC and AML

tech support

transaction secrecy simpler

rely on corporate development

compliance with law (reversion)

can keep competition out

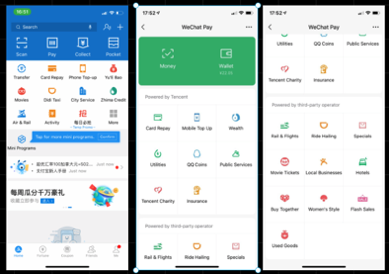

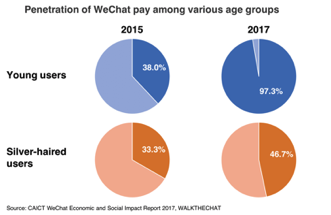

Enter BigTech

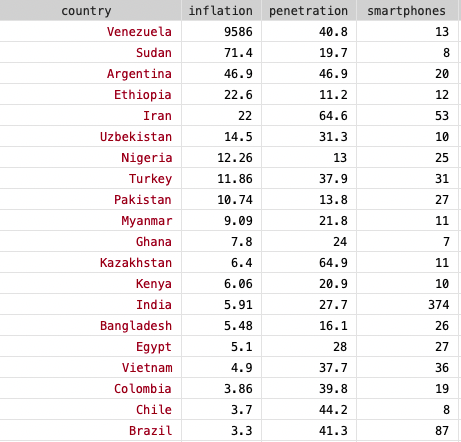

cellphone data from 2018 (NewZoo), inflation from 2020 (World Population Review)

Evolution

DIEM = "new financial infrastructure"

They have ZERO interest in becoming a financial institution/bank

\(\rightarrow\) no expertise

\(\rightarrow\) competitive market

\(\rightarrow\) one of the most regulated business environments

They are trying to deal with frictions that impede their business

They aim to collect data which will vastly improve their business

Lay the groundwork for the next step of the digital evolution: the "Metaverse"

5-minute version:

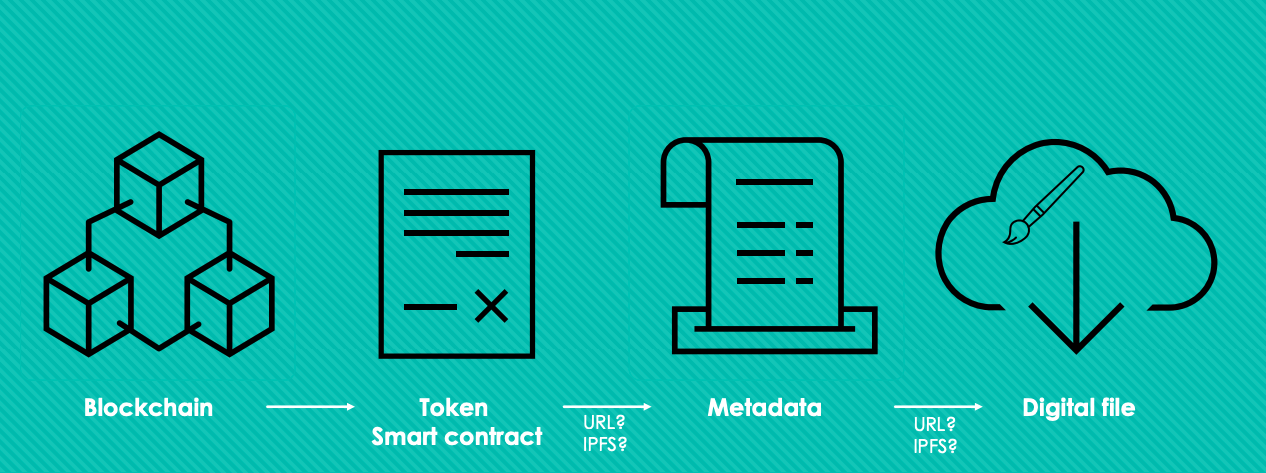

Finance, Metaverse, and Non-Fungible Tokens

metaverse =

marriage of the digital and physical world

sale price: $69,000,000

What is an NFT?

Why bother with an NFT?

Metaverse application

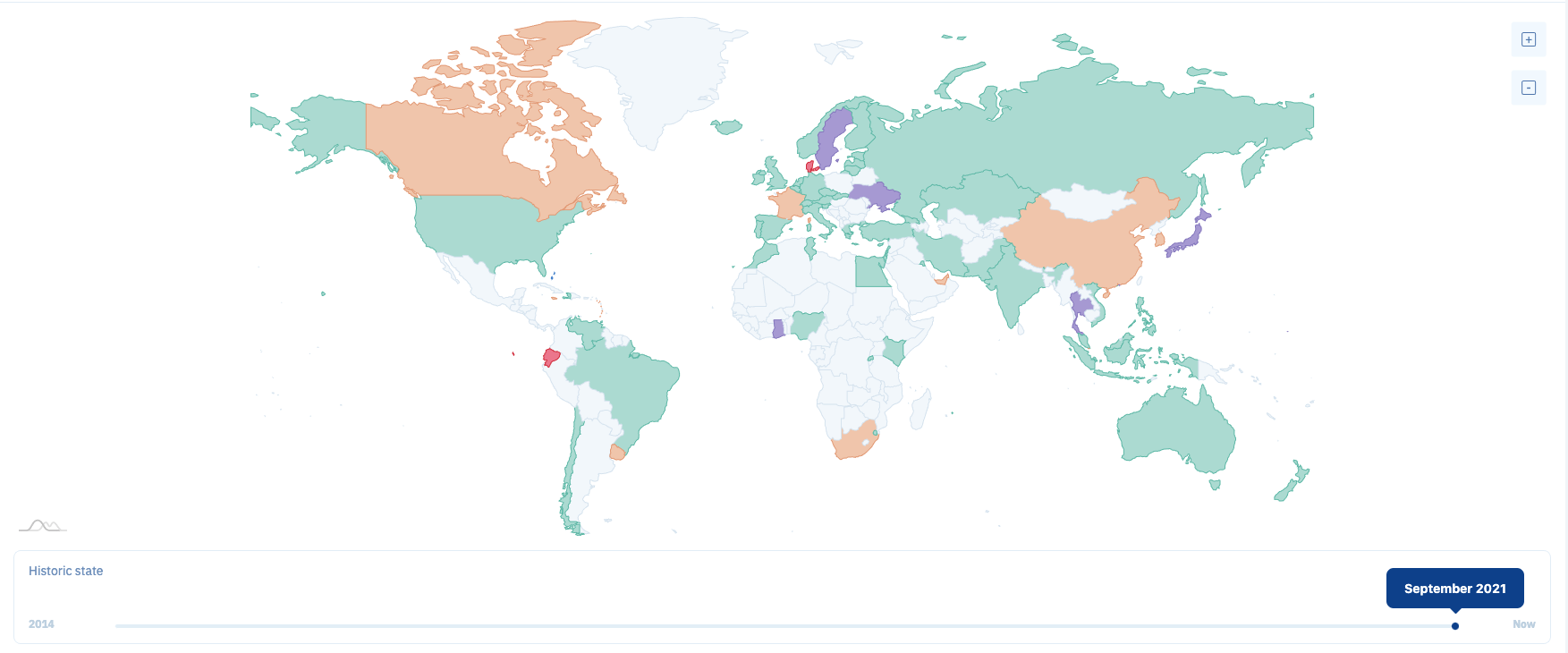

Related Development: Central Bank-Issued Digital Currencies

Evolution

CBDCs

Source: CBDCTracker.org

Risks and open problems

Investor

Broker

Venue

Settlement

Exchange

Wholeseller

Darkpool

Internalizer

Venue

Settlement

Investor

On chain

Technology

Legal/Regulation

Economic functions

interoperability

cybersecurity and privacy

functionality

scalability

smart contract features and verification

space constraints

interoperability

scalability

space constraints:

Does the law have to change to accommodate new tech? If so, how? What's dated, what's not?

Legal setup of a platform: what rules can, should, and must a platform establish? What regulations are necessary?

How can token design and the law be married?

What is the economic impact of "tokenizing everything"?

How will it affect investments and investment banking?

Which business opportunities will it enable?

What do tokens and "alternative money" mean for payments?

Who gets to update?

Can a higher body prevent

transactions?

Can the past be altered?

consensus

immutability

censorship resistence

open to anyone

no one can be excluded

past cannot be changed

high visibility of transactions

open-access eco-system

slow governance

privacy only at a cost

joint control and governance

straightforward KYC and AML

tech support

transaction secrecy simpler

rely on corporate development

compliance with law (reversion)

can keep competition out

Crypto vs Money

store of value?

unit of account?

method of exchange?

store of value?

unit of account?

method of exchange?

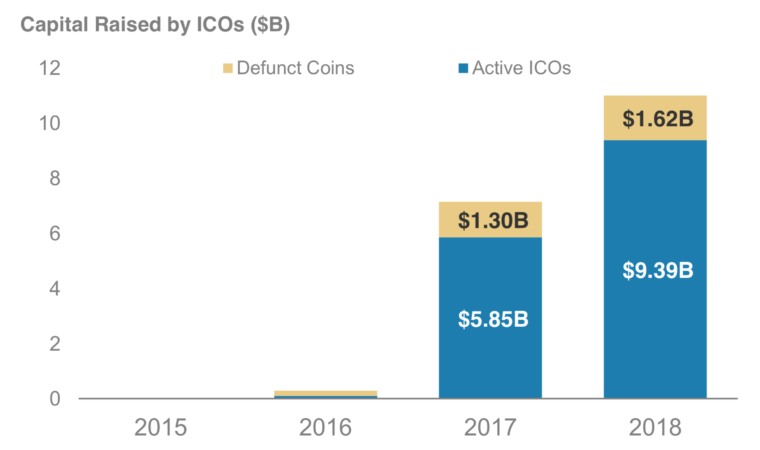

funding figures from Nov 2018; source: blockchain.com

issued by a consortium of firms (e.g., Facebook, Mastercard) and not for profits (Creative Destruction Lab)

each coin will be backed by a basket of SIX fiat currencies

idea is conceptually similar to IMF Special Drawing Rights (pegged to USD, EUR, YEN, GBP, YUAN)

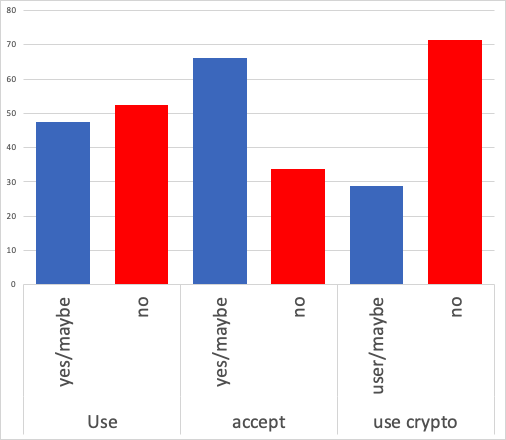

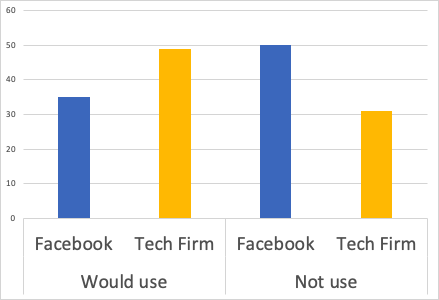

Would you use Libra/Money issue by Tech Firm?

If we ask explicitly for Facebook vs Tech Firm

Scaled to yes/maybe/no. About 20% say: "Need more info"

Data: coinschedule

for comparison: total size of

Toronto Stock Exchange: $2,200B

Toronto Venture Exchange: $41B

Source: Tokendata

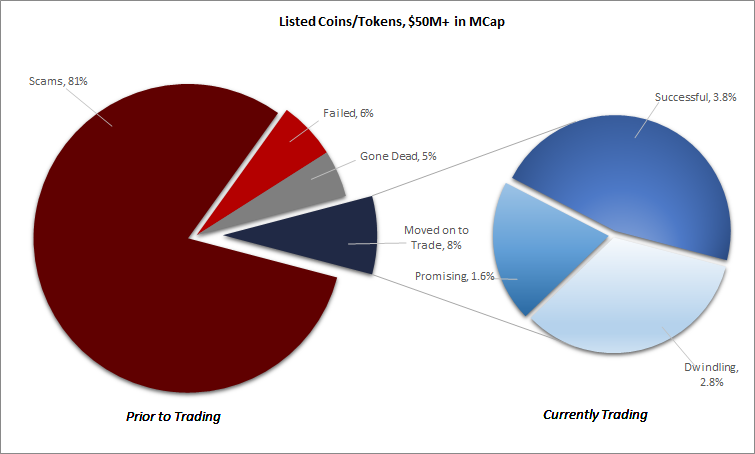

Source: Satis Group LLC

Source: Morgan Stanley (Nov 2018) “Update: Bitcoin, Cryptocurrencies and Blockchain”

Source: Tokendata

Lessons?

can finance projects that otherwise would find no debt or equity funding

enable network effects and new business opportunities

allows entrepreneurs to extract more surplus

can finance projects that otherwise would find no debt or equity funding

FinTech

DeFi

innovation vs. salesmanship

main focus

blockchain is a transformative technology, but won't be used in practice overnight

many conceptual and technological challenges remain, but there are already various areas of application

legal, regulatory, and competitive changes are needed and then the opportunities are endless ...

it will open up the banking world further, foster international competition, and change how we pay and exchange value

My view: business development will happen in private/semi-public space; strong increase in recent activity; no more testing but re-engineering of processes.

@financeUTM

andreas.park@rotman.utoronto.ca

slides.com/ap248

sites.google.com/site/parkandreas/

youtube.com/user/andreaspark2812/

By Andreas Park

This is the slide deck that I use for a quick introduction to the Decentralized Finance class.