Andreas Park PRO

Professor of Finance at UofT

by Andreas Park

Research Presentation

Investor

Broker

Venue

Settlement

Exchange

Wholeseller

Darkpool

Internalizer

Venue

Settlement

Investor

On chain

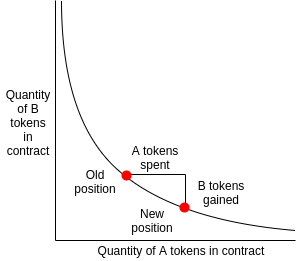

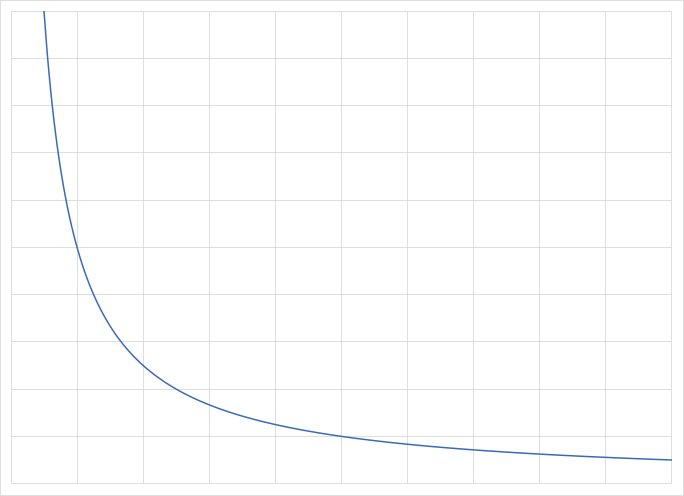

How do you set the price?

Price mechanism:

Prices

invariant \(k=4\times4=16\)

Instantaneous exchange rate:

1 = 1

Contract deposit:

sell 4 DAI for USDC

what price will therefore be quoted?

how many USDC?

a

b

c

d

e

f

g

\(X\)

\(Y\)

normal trade: sell \(x\) \(\to\) get \(y'\)

\(Y-y'\)

\(X+x\)

front-running:

\(Y-y'-y''\)

\(X+2x\)

\(y'>y''~\Rightarrow\)

front-running is intrinsically profitable

Disclaimer:

Market 1

\(Y-y\)

\(X+x\)

\(Y-y'\)

\(X+2x\)

\(X\)

\(Y\)

\(Y-y\)

\(X+x\)

\(Y-y'\)

\(X+2x\)

\(X\)

\(Y\)

Market 2

splitting across time ain't profitable

can't make money from scanning the mem-pool

no intrinsic benefit from market fragmentation

no ping-pong trading

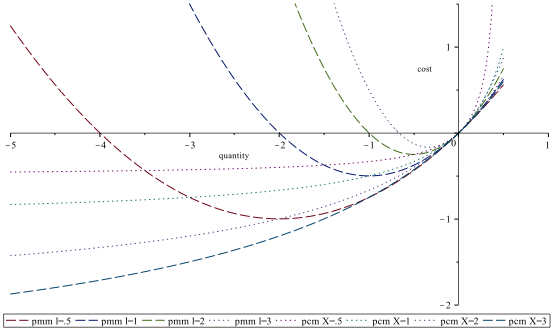

Proposition: For \(x>x^*\), "standard" pricing is "better" for investors than constant product pricing, and for \(x<x^*\) it is the reverse.

splitting across time ain't profitable

can't make money from scanning the mem-pool

no intrinsic benefit from market fragmentation

no ping-pong trading

no front-running if:

front-running profit < 2\(\times\) submitted fee

note, however:

@financeUTM

andreas.park@rotman.utoronto.ca

slides.com/ap248

sites.google.com/site/parkandreas/

youtube.com/user/andreaspark2812/

By Andreas Park