Andreas Park PRO

Professor of Finance at UofT

Instructors: Andreas Park

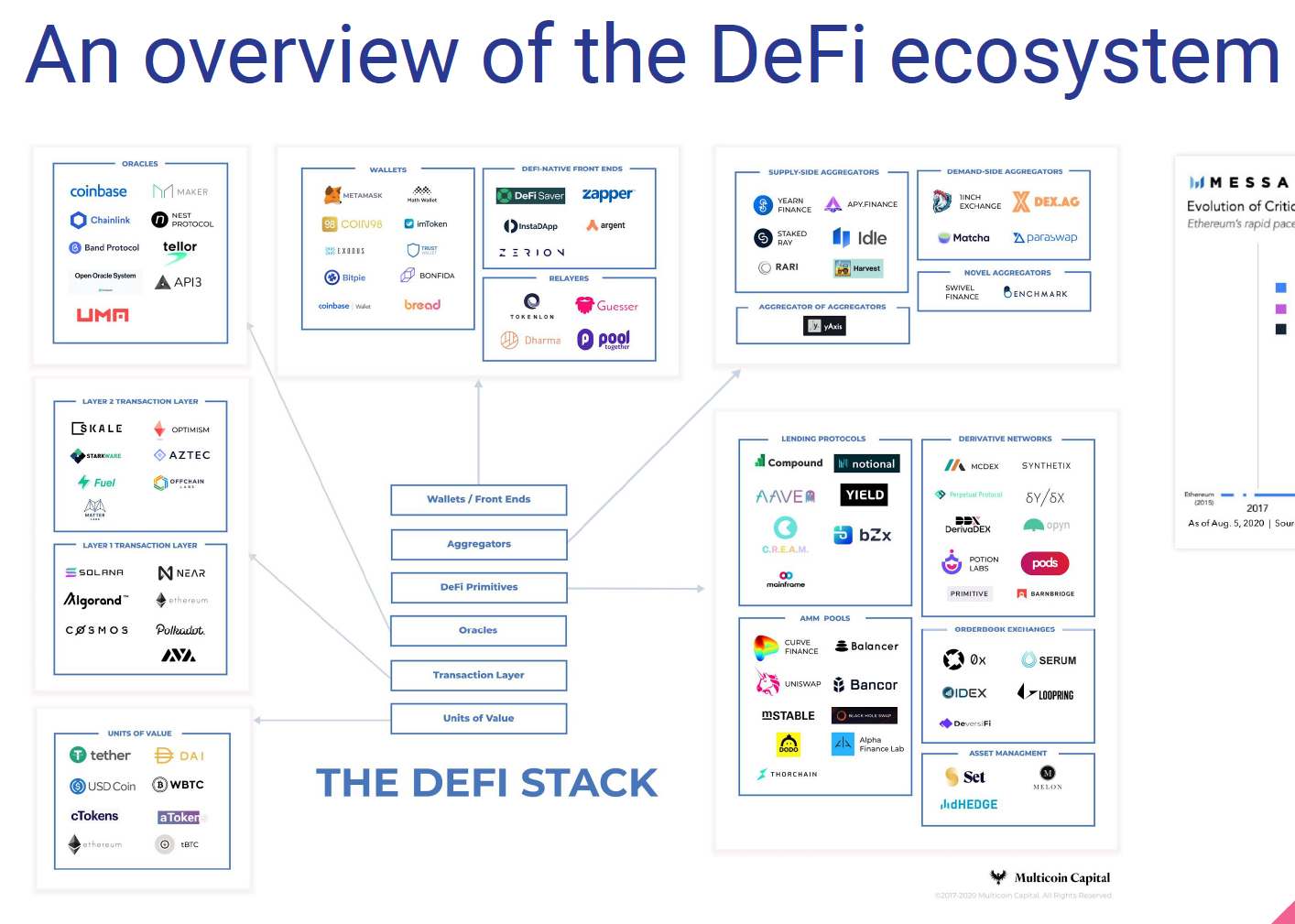

A glimpse of overall infrastructure

Sue wants to sell ABX

Bob wants to buy ABX

sell order

buy order

Clearing House

Stock Exchange

Broker

Broker

3rd party tech

custodian

custodian

record beneficial ownership

central bank for payment

Retail

Institutional

Pro-Traders

high volume securities

low volume securities

50%

50-60%

0%

30-40%

40-50%

10-20%

Exchange

Internalizer

Wholeseller

Darkpool

Investor

Venue

Broker

Settlement

Exchanges

Wholesellers

Dark pools

Broker Internalizations

Exchanges

Wholesellers

Dark pools

Broker Internalizations

(

(

Retail

Institutional

Pro-Traders

Rule: must send to exchange with best price

Exchange

Wholeseller

market order

limit order

In Europe: no best price obligation

Exchange

Dark pools

Type 2: "borrow" broker-dealer system

Type 1: licenced broker-dealer

risk control

You commonly don't access the market directly.

Brokers take many decisions but they are bound by regulations.

Critical: markets are formally linked by best-price rules.

Retail

Institutional

Pro-Traders

high volume securities

low volume securities

50%

50-60%

0%

30-40%

40-50%

10-20%

Investor

Venue

Settlement

On chain

Retail, Institutions, and Pro-Traders are indistiguishable

not clear whether and which institutions are active

Exchanges

Dark pools

Smart On-chain contracts

Exchanges

Smart Contract

Order Driven

Market Maker

Exchanges

Smart On-chain contracts

(307 CEX, rest DEX)

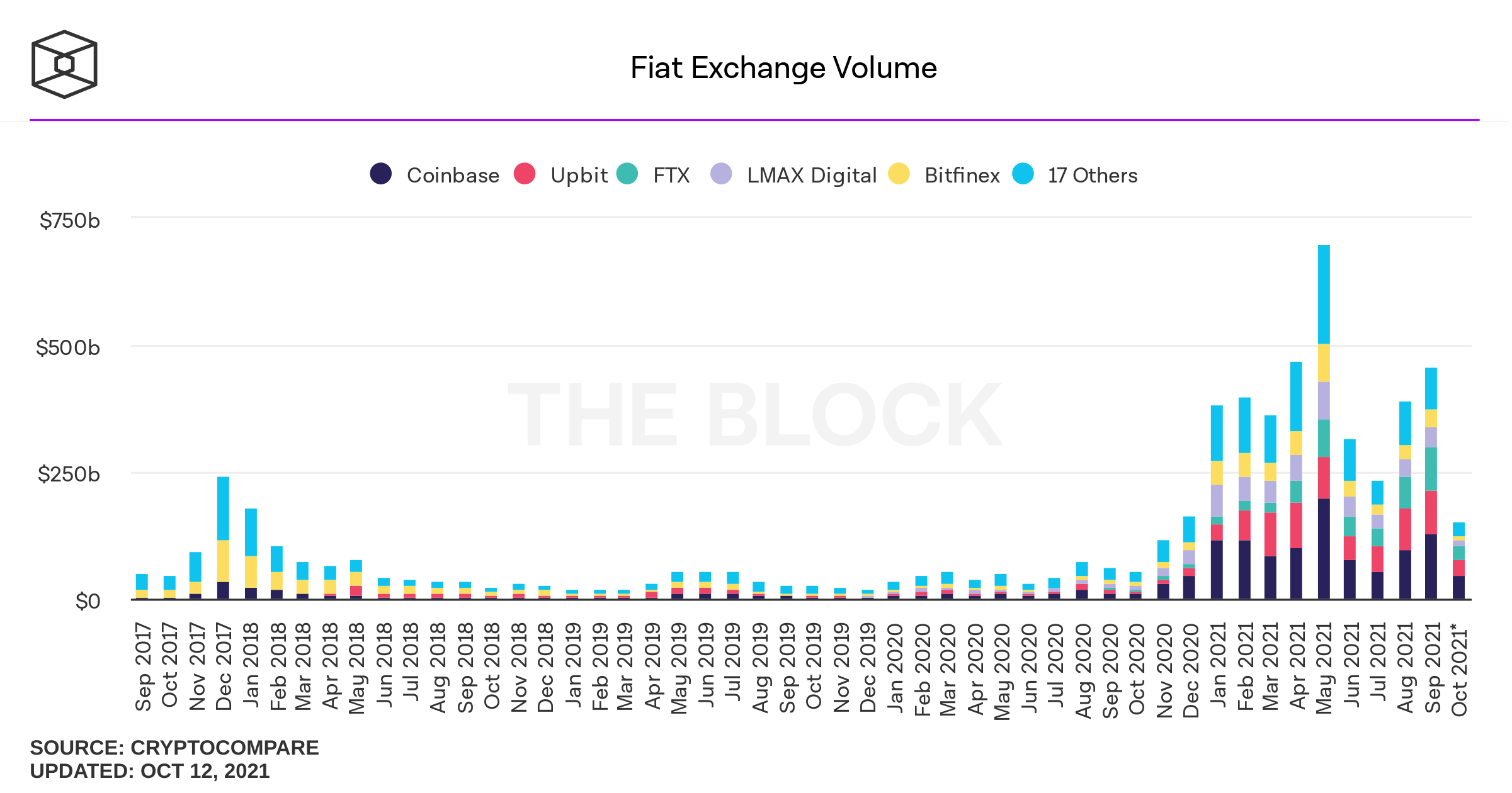

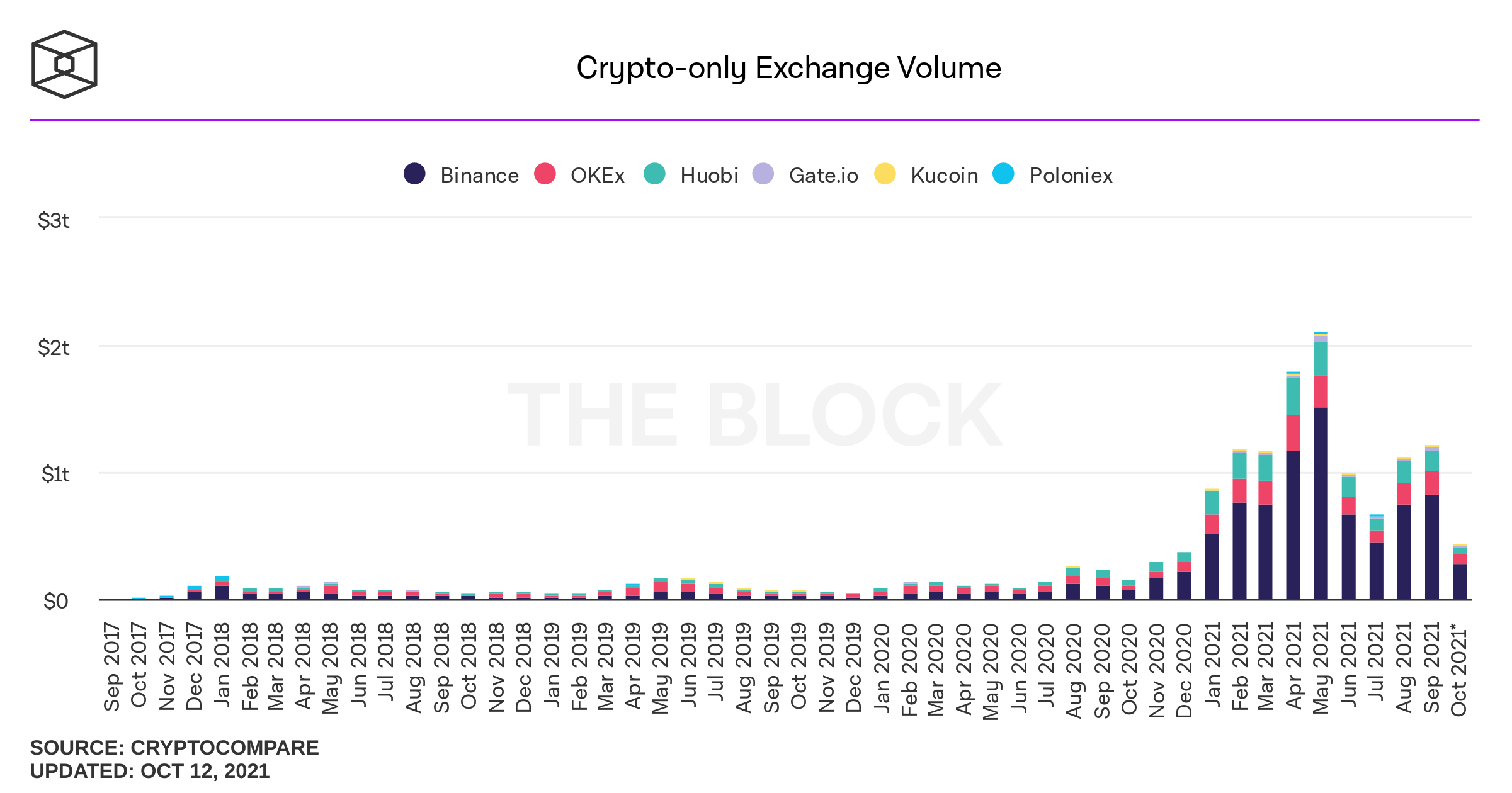

Settle on the blockchain for digital "assets"

Wire transfer for fiat

BTC/USD

ask: 7,600

bid: 7,550

BTC/USD

ask: 7,500

bid: 7,450

buy low

sell high

BTC/USD

ask: 7,600

bid: 7,550

BTC/USD

ask: 7,500

bid: 7,450

buy BTC

sell BTC

move BTC to Kraken

Wire: free*; 1-5 days

Credit card: 3.5%

trading fee: 10-25 bps

flat fee in BTC \(\approx\) $4-8

\(\approx\) 10-60 minutes

trading fee: 0-26 bps

35 USD + 0.125%

($5 if >$50,000)

1-3 business days;

possible other fees/delays

Some exchanges allow short selling

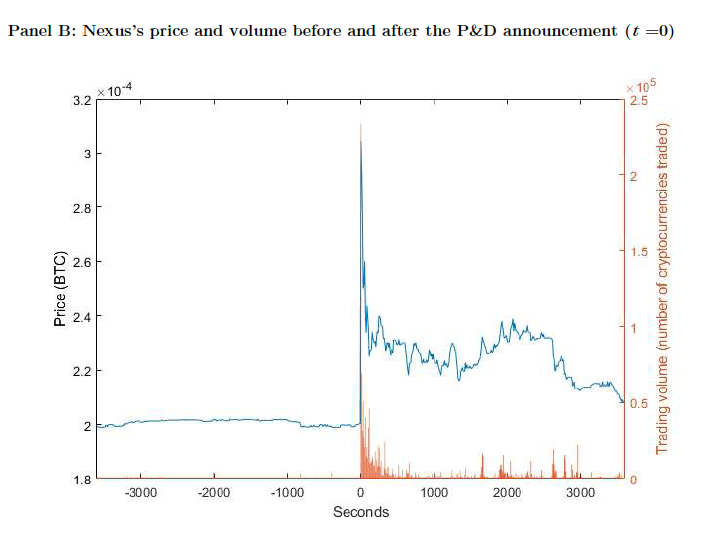

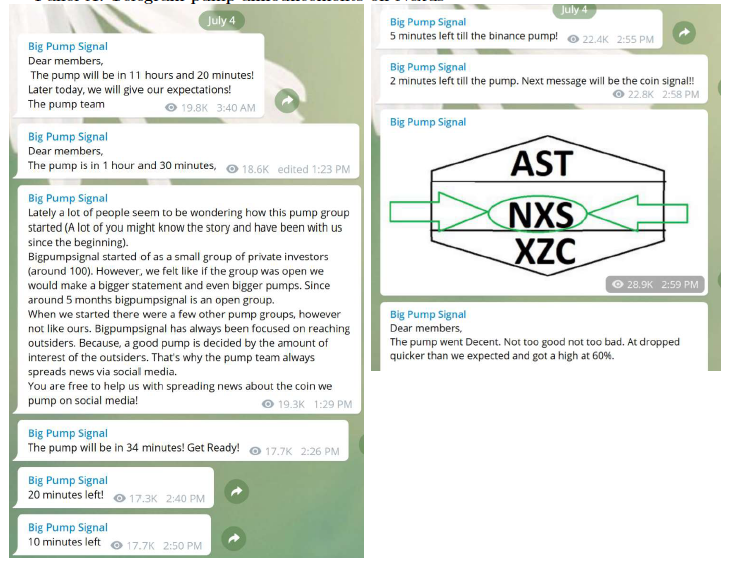

Crypto Wash Trading, Lin William Cong, Xi Li, Ke Tang, Yang Yang

What is pump and dump?

arranged via Telegram Channels

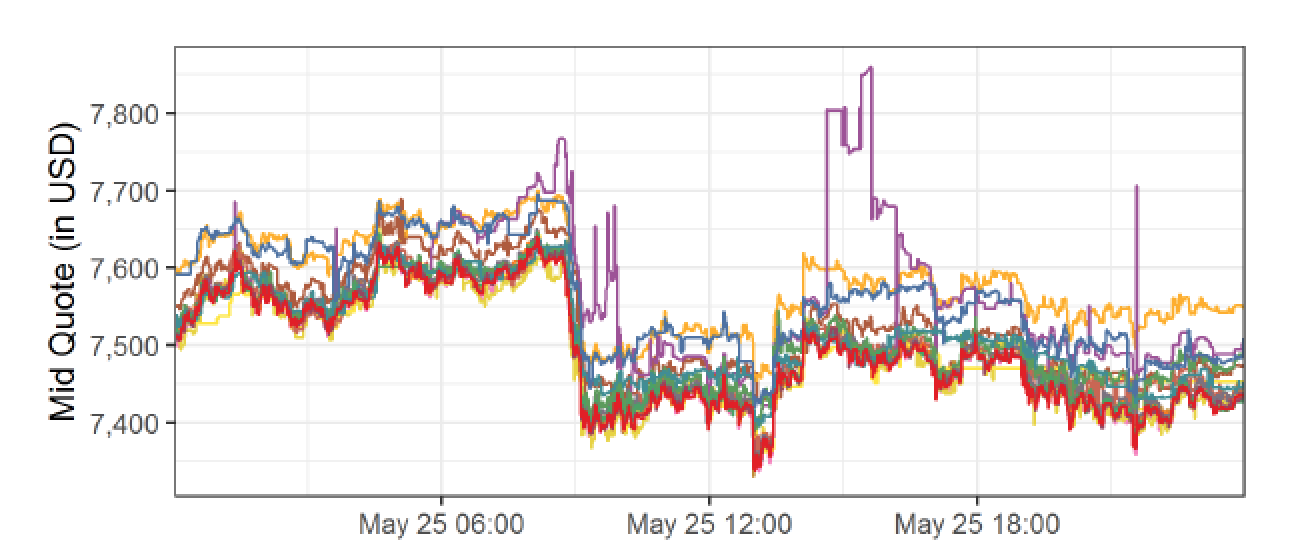

IS BITCOIN REALLY UN-TETHERED? JOHN M. GRIFFIN and AMIN SHAMS

Journal of Finance 2020

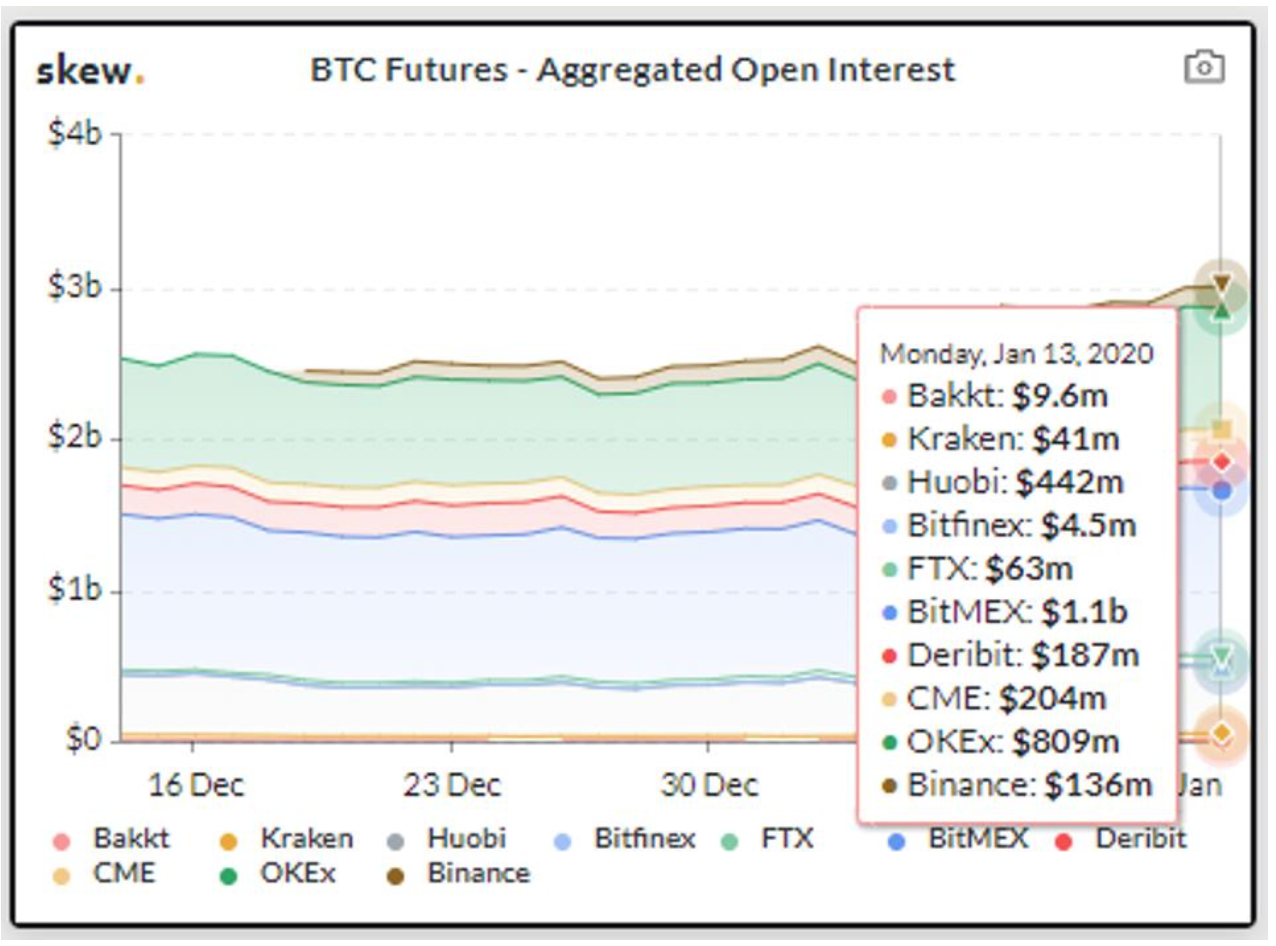

Regulated Exchanges

Derivatives trade mostly offshore! Unregulated(?!)

Historically: “Tether Platform currencies are 100% backed by actual fiat currency

assets in our reserve account.”

Today: "The Tether Platform is fully reserved when the sum of all tethers in circulation is less than or equal to the value of our reserves."

IS BITCOIN REALLY UN-TETHERED?

JOHN M. GRIFFIN and AMIN SHAMS

Journal of Finance 2020

IS BITCOIN REALLY UN-TETHERED?

JOHN M. GRIFFIN and AMIN SHAMS

Journal of Finance 2020

Text

IS BITCOIN REALLY UN-TETHERED?

JOHN M. GRIFFIN and AMIN SHAMS

Journal of Finance 2020

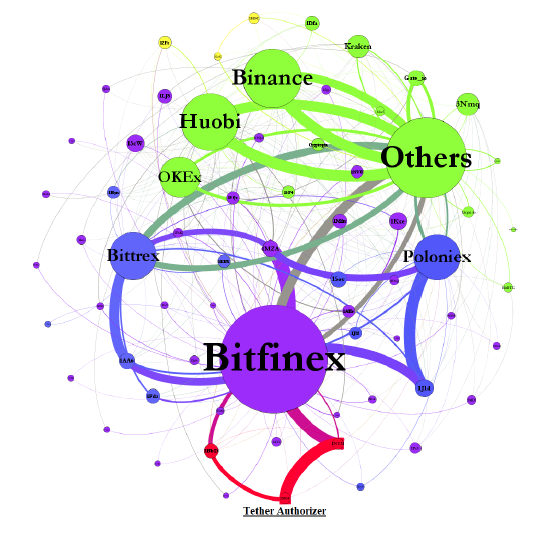

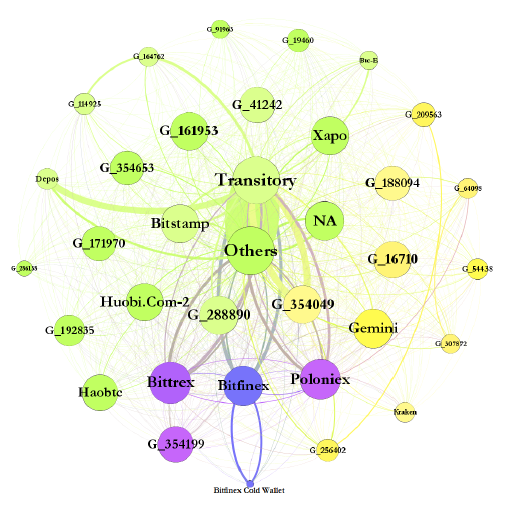

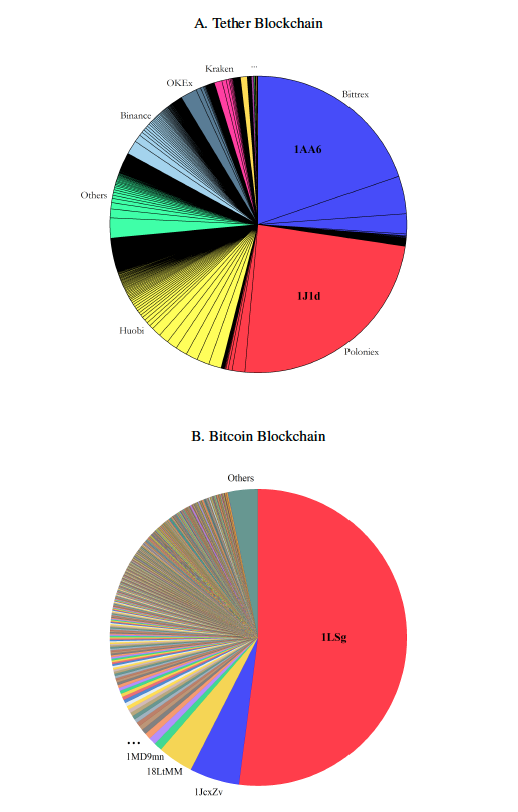

Figure 1. Aggregate Flow of Tether between Major Addresses

Figure 3. Aggregate Flow of Bitcoin between Major Addresses.

Top Accounts Associated with the Flow of Tether from and Bitcoin to Bitfinex

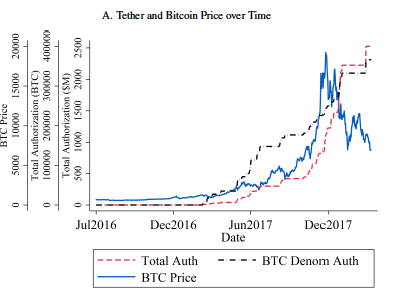

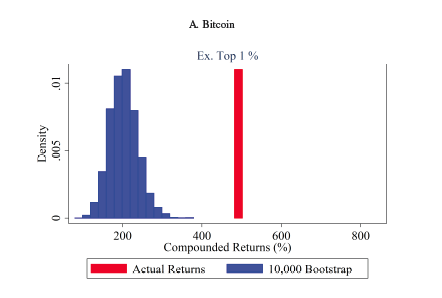

the 1% of hours with the strongest lagged Tether flow are associated with 58.8% of the Bitcoin buy-and-hold return over the period.

the "normal-times" returns

August 2016

By yours truly, Dec 2017: "What really concerns me about the current craziness is the role of the cryptocurrency exchange platforms, such as Coinbase, Quadriga, or Bitfinex, which most people use to buy Bitcoins. These are like banks that hold deposits. For cryptocurrencies to succeed it is critical that these interfaces with the real world are financially robust. Are they? Do they have all the Bitcoins they sell? Can they always satisfy depositors’ demands?"

https://www.forbes.com/sites/jasonbrett/2019/12/19/congress-considers-federal-crypto-regulators-in-new-cryptocurrency-act-of-2020/#7ddcdfd65fcd

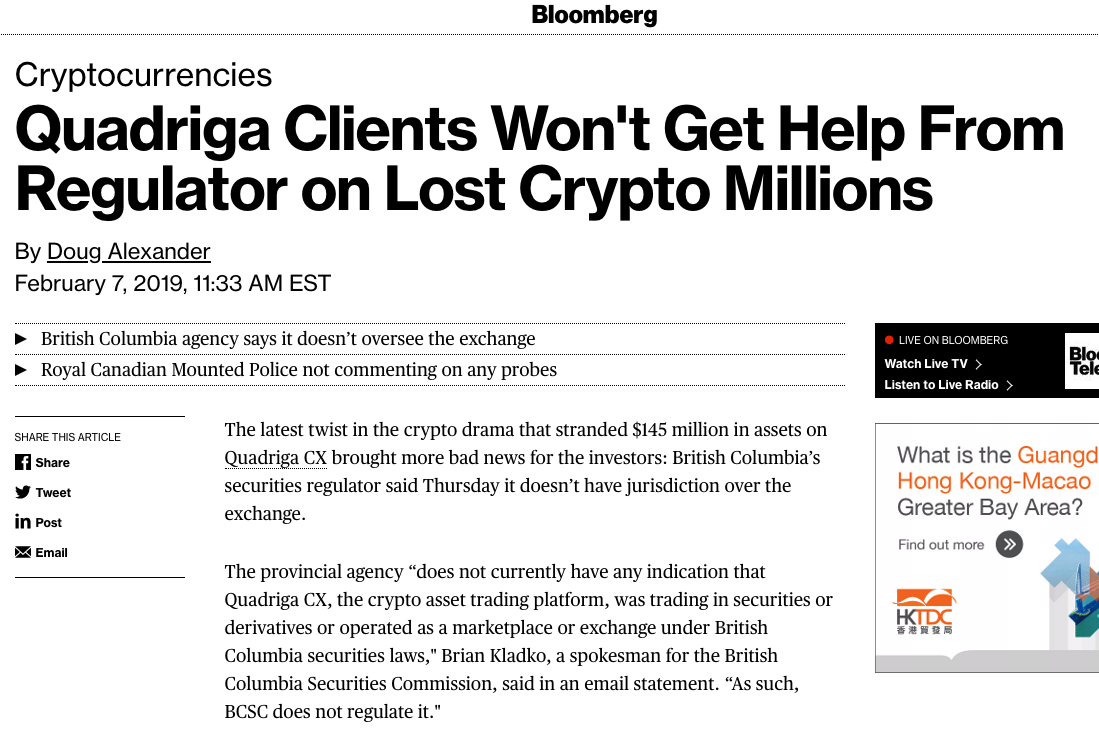

https://www.osc.ca/en/news-events/news/osc-working-ensure-crypto-asset-trading-platforms-comply-securities-law

SEC denies Bitcoin ETF

Actually ...

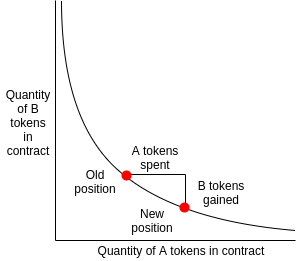

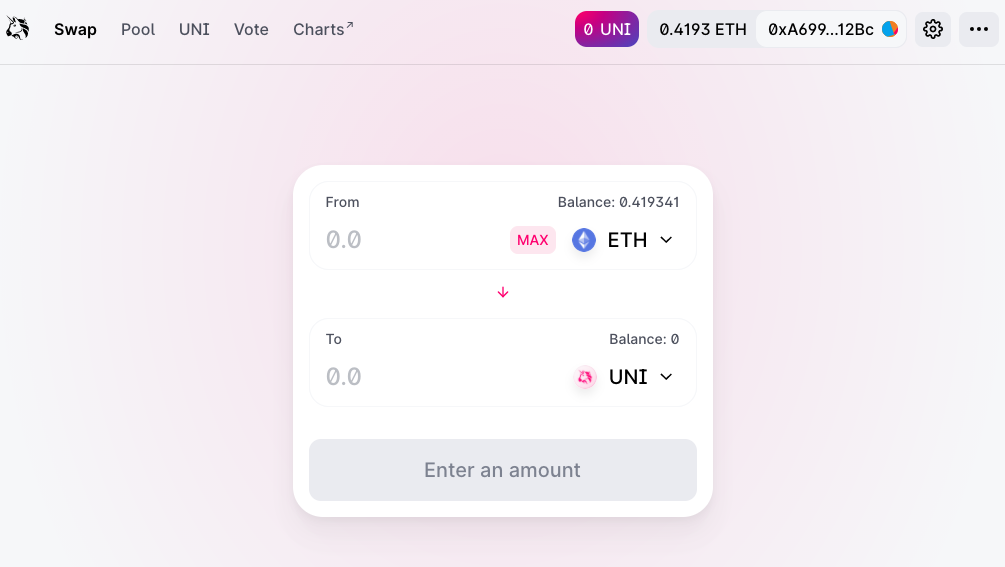

How do you set the price?

Price mechanism:

Prices

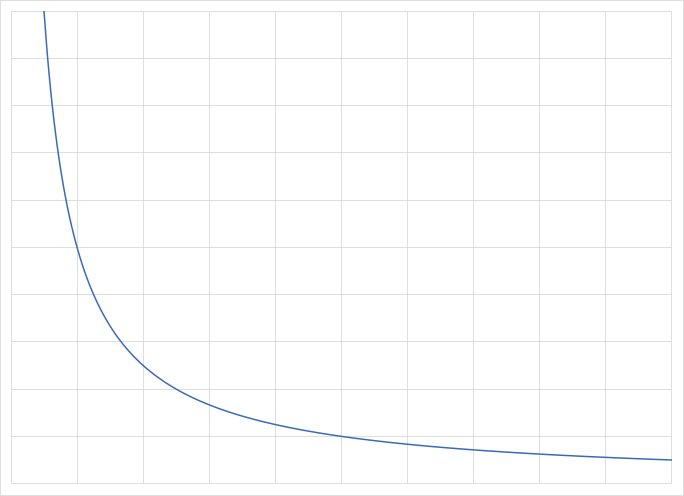

invariant \(k=4\times4=16\)

Instantaneous exchange rate:

1 = 1

Contract deposit:

sell 4 DAI for USDC

what price will therefore be quoted?

how many USDC?

Problem: large "slippage" (or price impact)

establish and sell a new token

front-running

transactions enter mem-pool

\(\to\) all visible there

arbitrageur make instant-swap trade at higher gas price

\(\to\) trade instead of original trade

\(\to\) reverse to gain slippage from earlier trader

1

2

4

3

5

6

1

2

5

3

6

7

4

front-running is annoying for the front-run - but will it happen?

\(\Rightarrow\) profitable!

take three pairs (ignore that BTC is not directly on Ethereum)

BTC-DAI

ETH-BTC

ETH-DAI

\(\to\) simply connect with MetaMask (or similar wallet)

\(X\)

\(Y\)

normal trade: sell \(x\) \(\to\) get \(y'\)

\(Y-y'\)

\(X+x\)

front-running:

\(Y-y'-y''\)

\(X+2x\)

\(y'>y''~\Rightarrow\)

front-running is intrinsically profitable

Disclaimer:

From Vitalik Buterin's post on the topic:

https://ethresear.ch/t/improving-front-running-resistance-of-x-y-k-market-makers/1281

a

b

c

d

e

f

g

Exchange

Internalizer

Wholeseller

Darkpool

Investor

Venue

Broker

Settlement

Investor

Venue

Settlement

On chain

By Andreas Park