Andreas Park PRO

Professor of Finance at UofT

Katya Malinova and Andreas Park

How did these guys put it ...?

1. Multiple trading protocols are possible

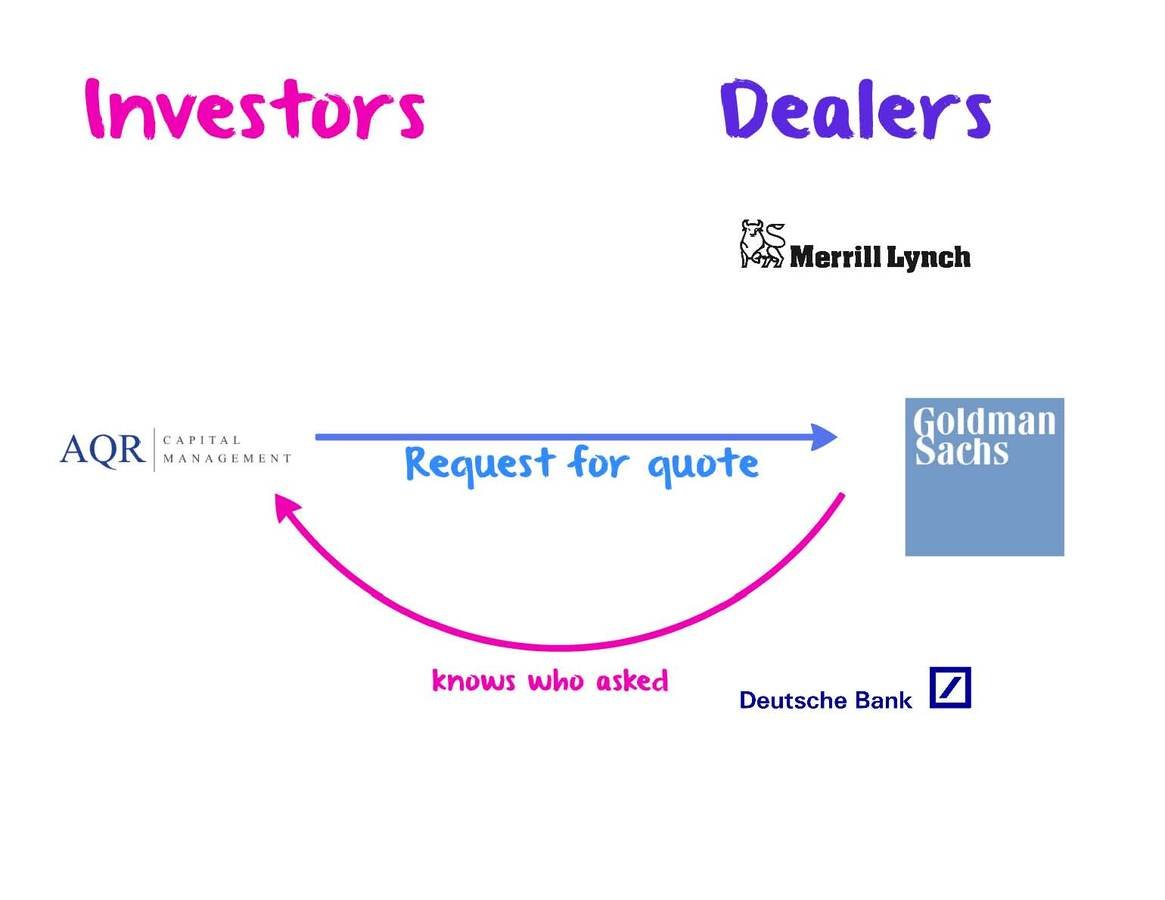

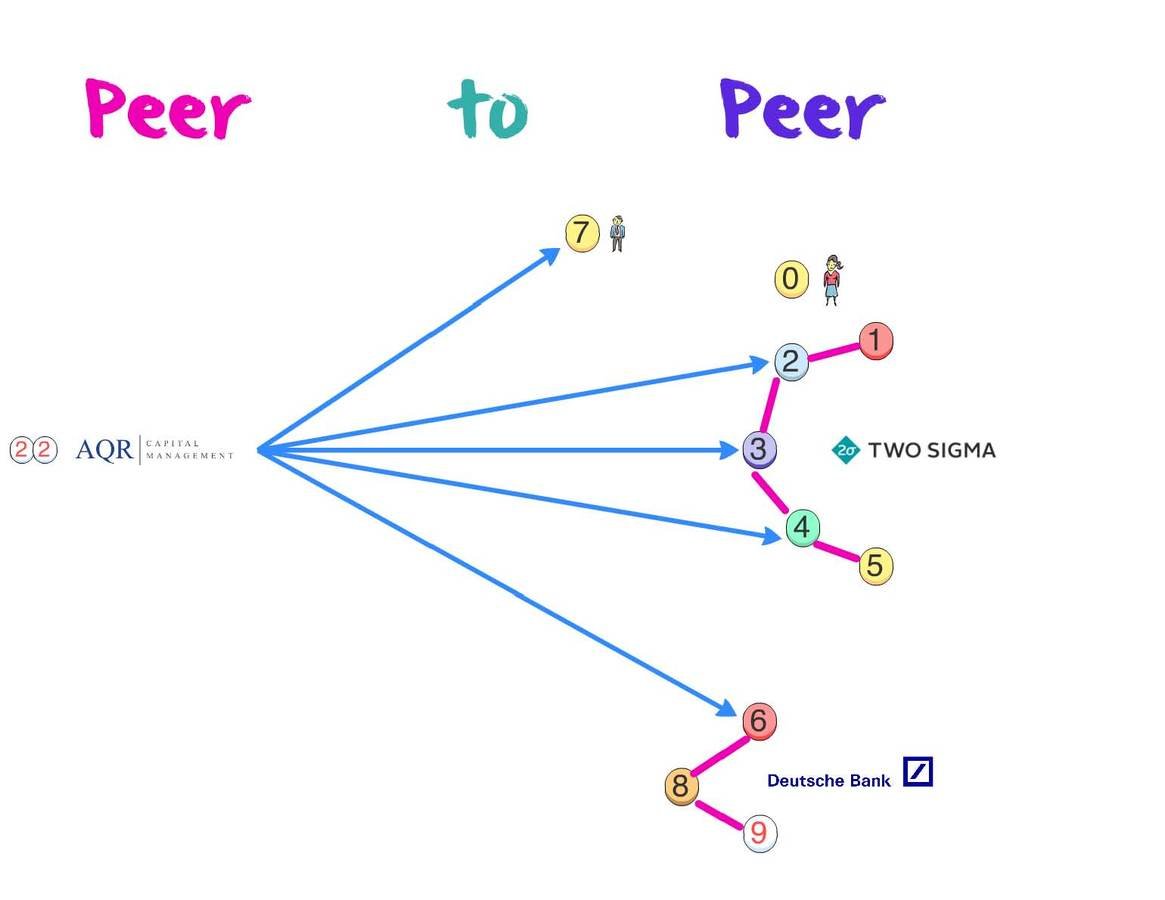

User-facing exchange mask

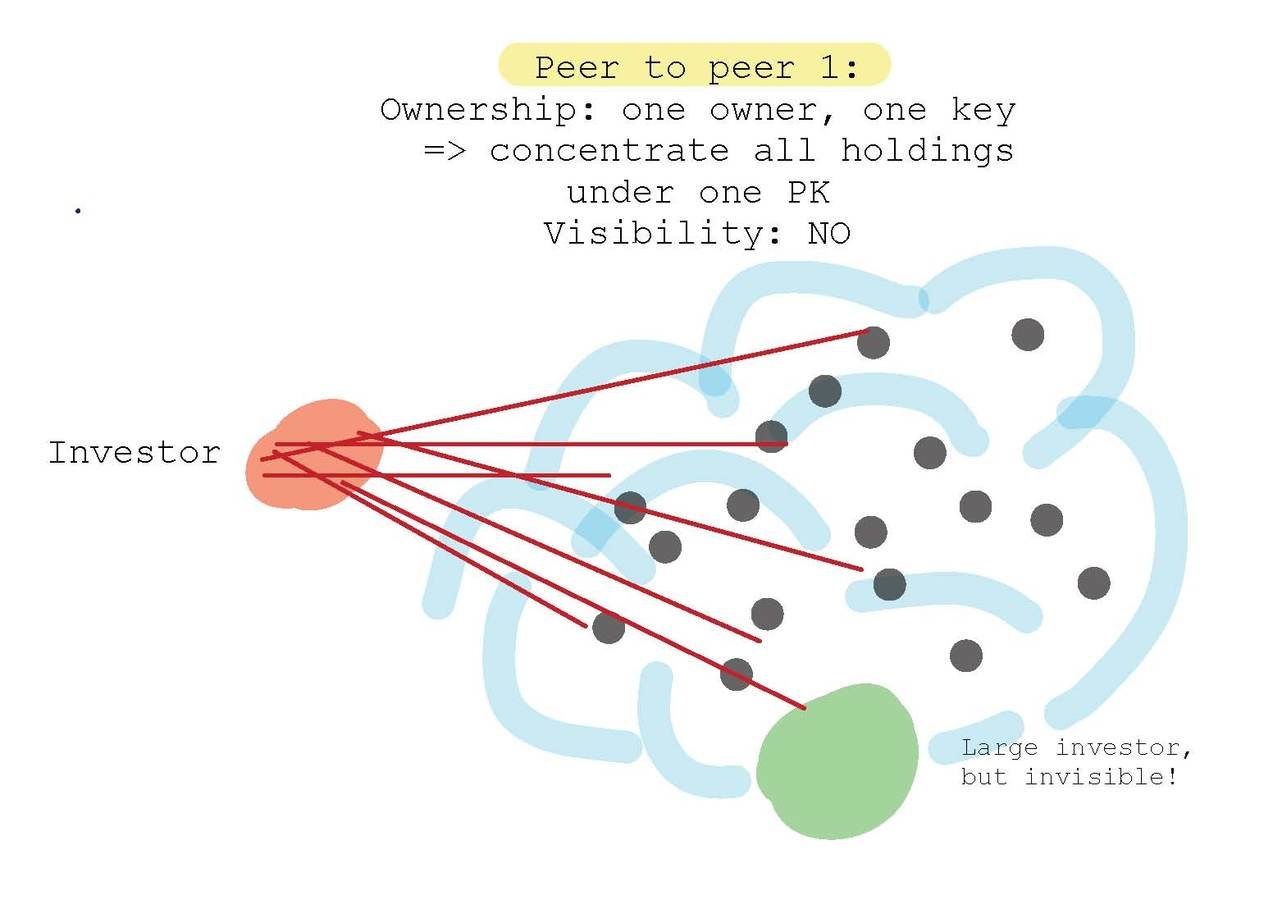

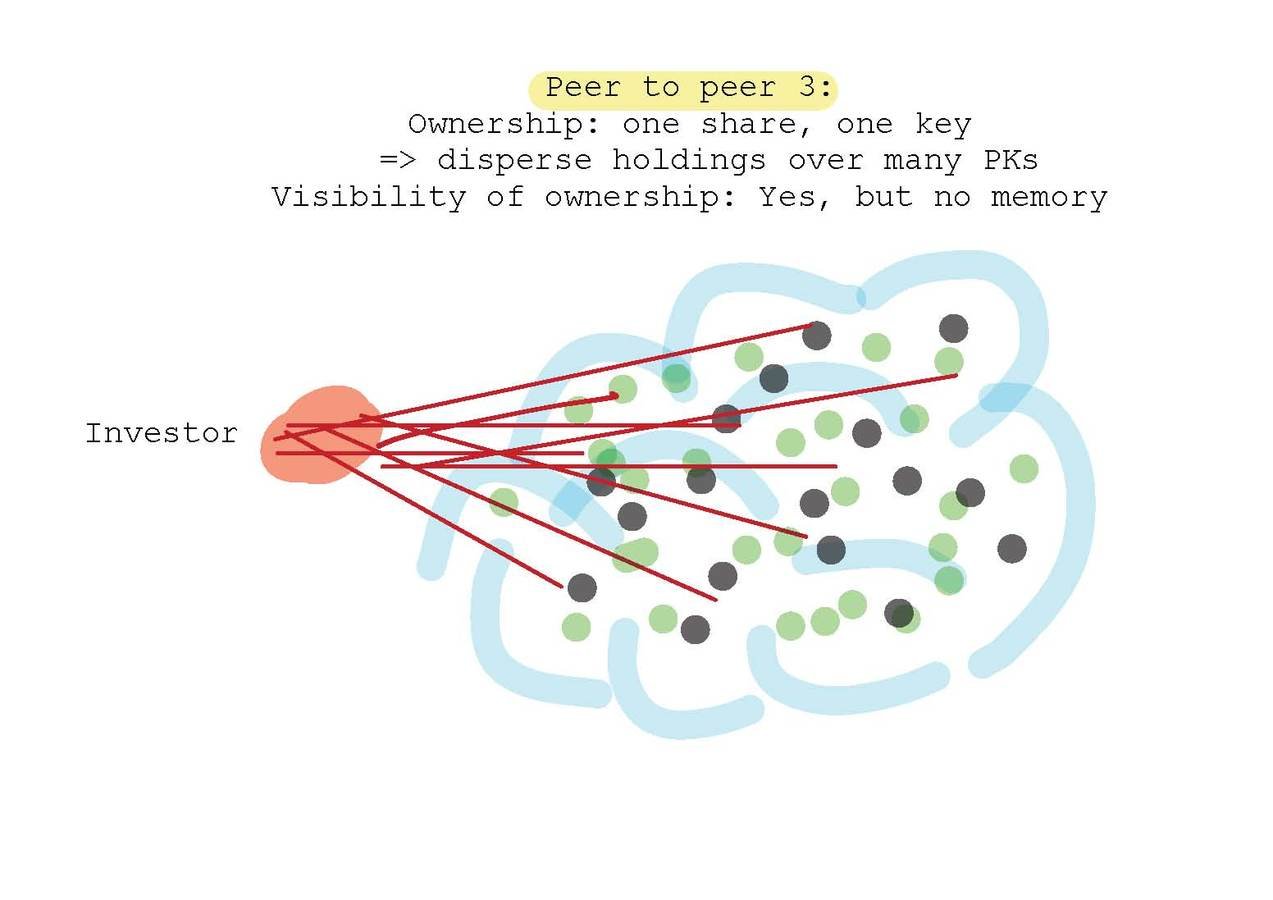

Fully Decentralized, "OTC",

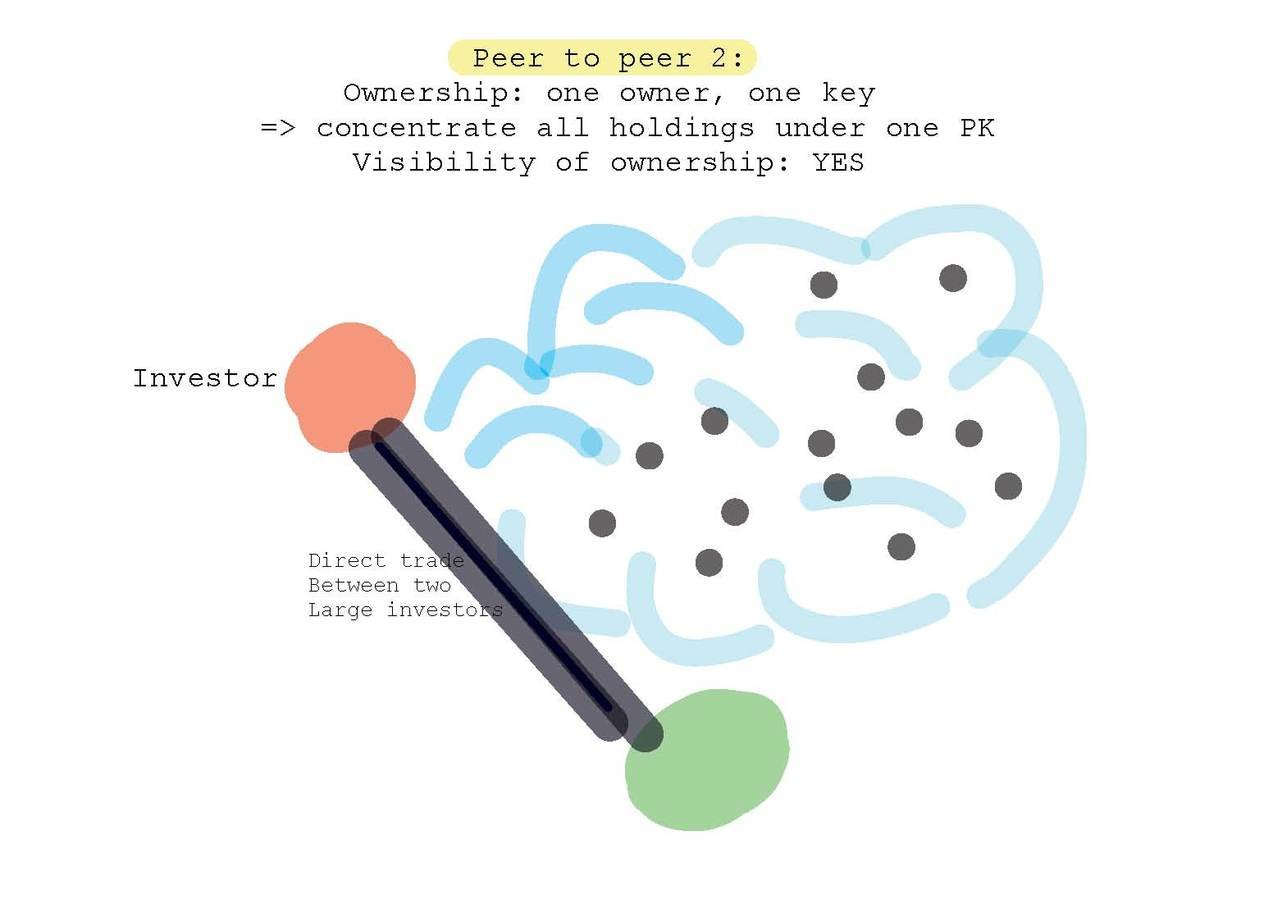

Peer-to-Peer Exchange

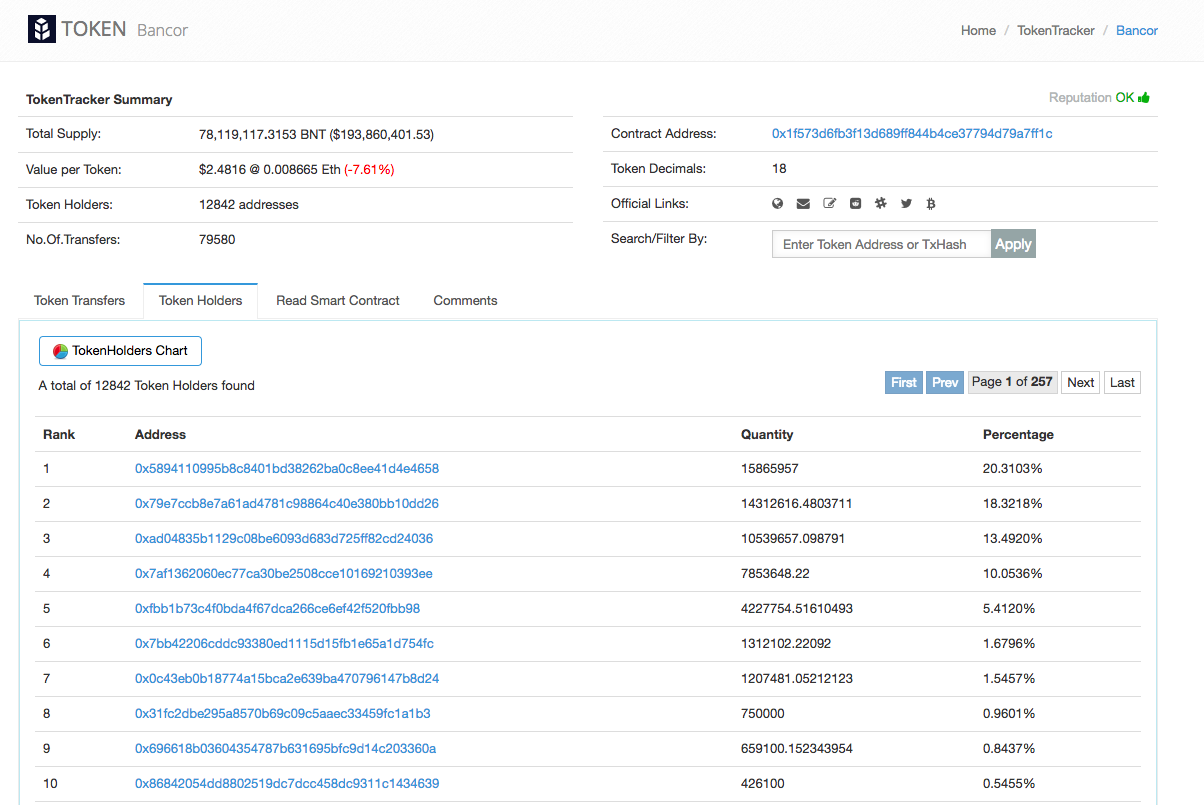

2. High Level of Transparency

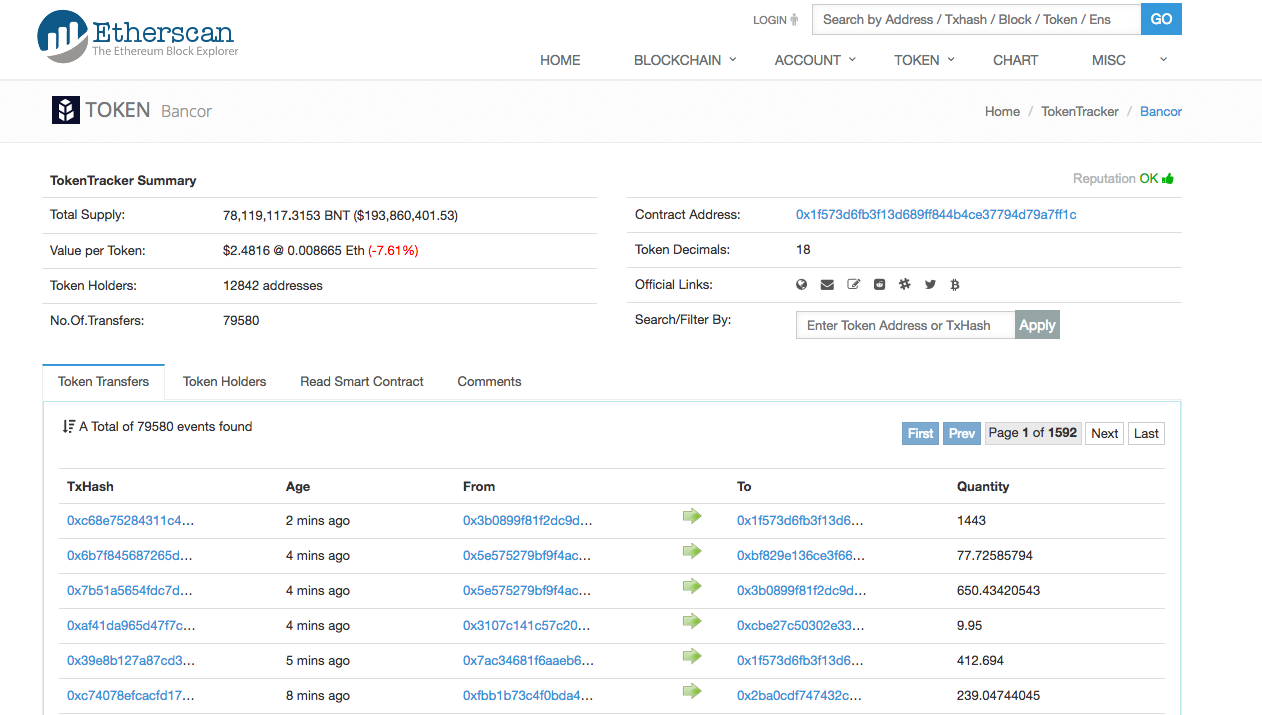

See transactions between "addresses" (="IDs")

3. You can tell who owns what

Who benefits and loses under which regime?

Each period one is hit with size Q=1 liquidity shock.

Other can absorb the shock at zero cost.

Disclaimer:

Disclaimer:

Requires a system design choice:

Large trader LT may:

Trade with small investors.

Trade with the intermediary.

Approach the other large trader LP.

complexity cost

current market price paid to small

costly trading with intermediary

validation cost

escape complexity and validation costs

avoid price impact of trade with risk-averse intermediaries

Closest and native to "public" blockchains:

small traders

large trader

small traders

large trader

small traders

large trader

filled

unfilled

Opaque Single ID

Opaque Multi-ID: LP accepts

Opaque Multi-ID: LP rejects

accept offer

submit large amount to continuum

submit large amount to continuum

front run

Result 1: There exists an equilibrium with no front-running where

provided

Result 2 (numerical): For small discount (=infrequent interaction) factors, the equilibrium with no front-running where LP accept does not exist. Then:

=> over-trading with intermediary

Observations

Finding 3:

The following relations hold for the average equilibrium stage payoffs of large traders.

Finding 4: (Numerical)

There exist parametric configurations such that large traders trade with each other at p > 0 in the multi-ID ownership setting, but their average equilibrium payoff in the opaque single-ID setting is higher.

By Andreas Park

This is a set of slides that my co-author Katya Malinova used for a presentation of my paper with Katya Malinova on our paper "Market Design with Blockchain Technology". This iteration was presented on August 22, 2017. The deck has been designed for a 25 minute presentation.