Andreas Park PRO

Professor of Finance at UofT

The Thirteenth Annual Berkowitz Lecture

or, more accurately:

What are the economic questions and how can economic analysis help us understand?

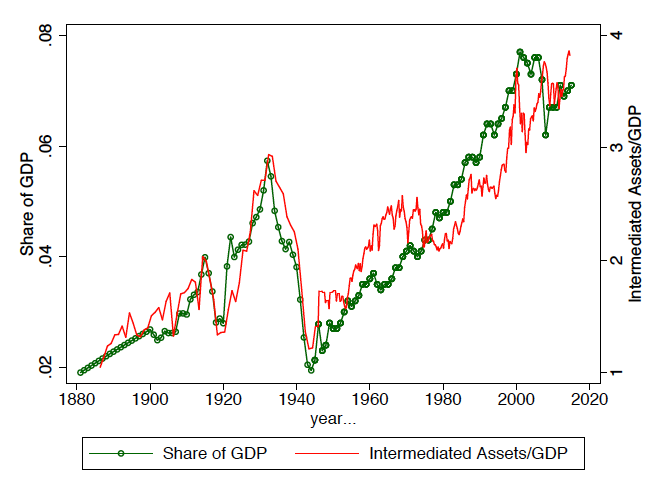

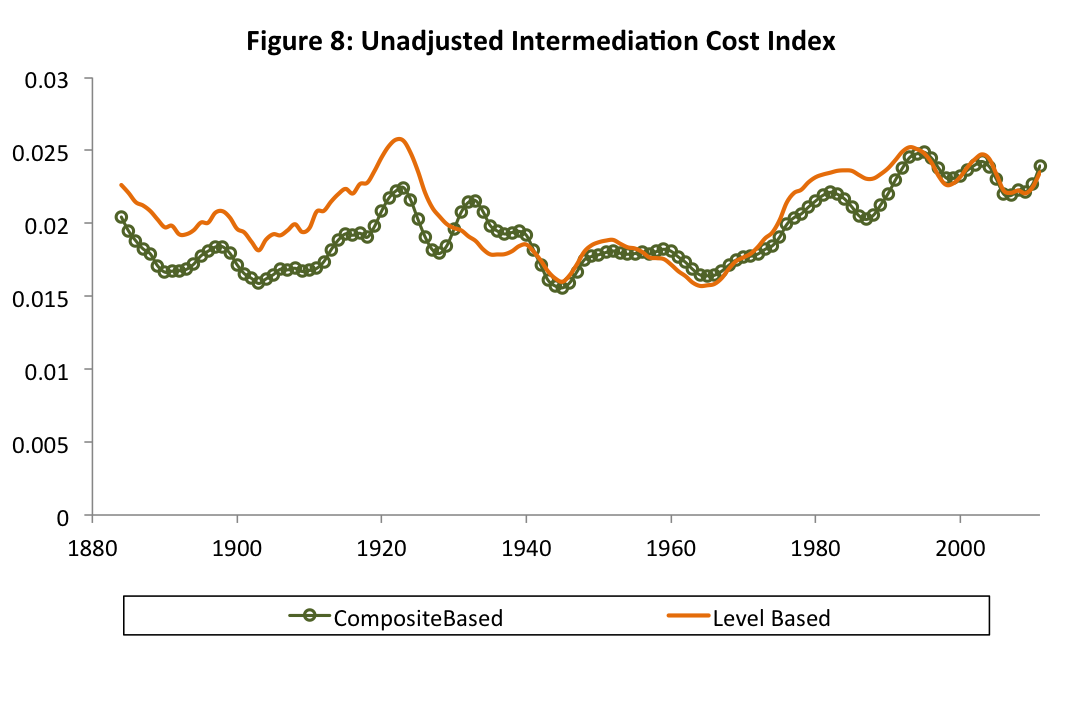

Source: Philippon (AER 2015) "Has the U.S. Finance Industry Become Less Efficient?"

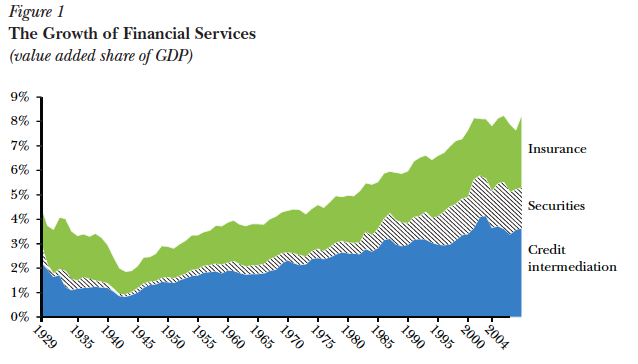

Source: Greenwood & Scharfstein (JEP 2013) "The Growth of Finance"

Source: Philippon (AER 2015) "Has the U.S. Finance Industry Become Less Efficient?"

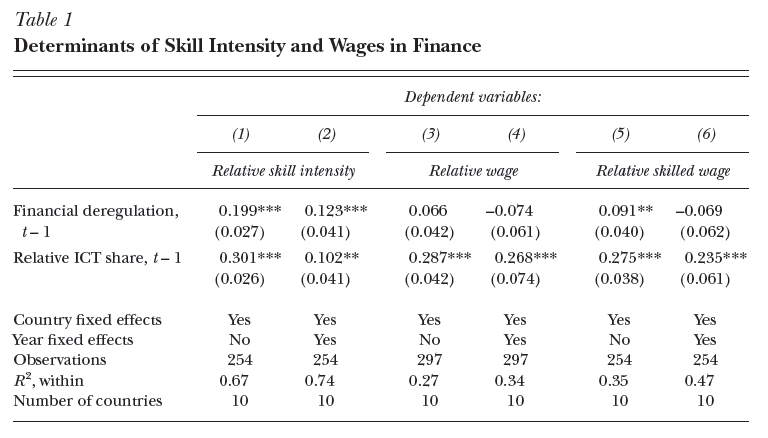

Source: Philippon & Reshef (JEP 2013)

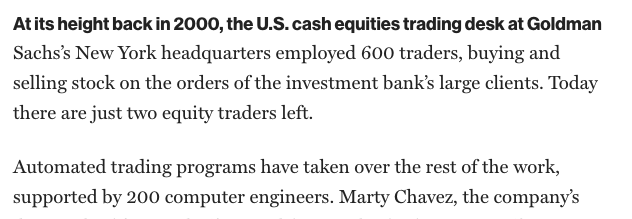

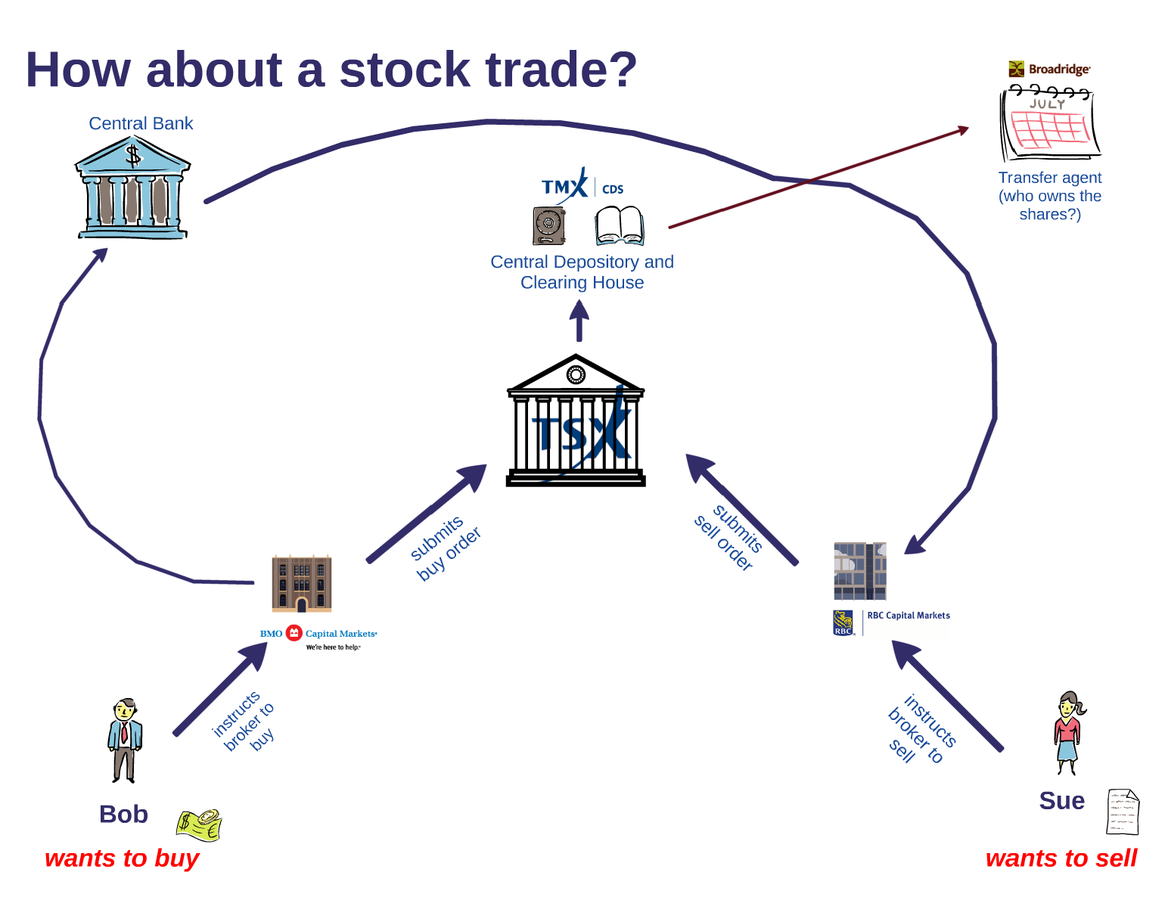

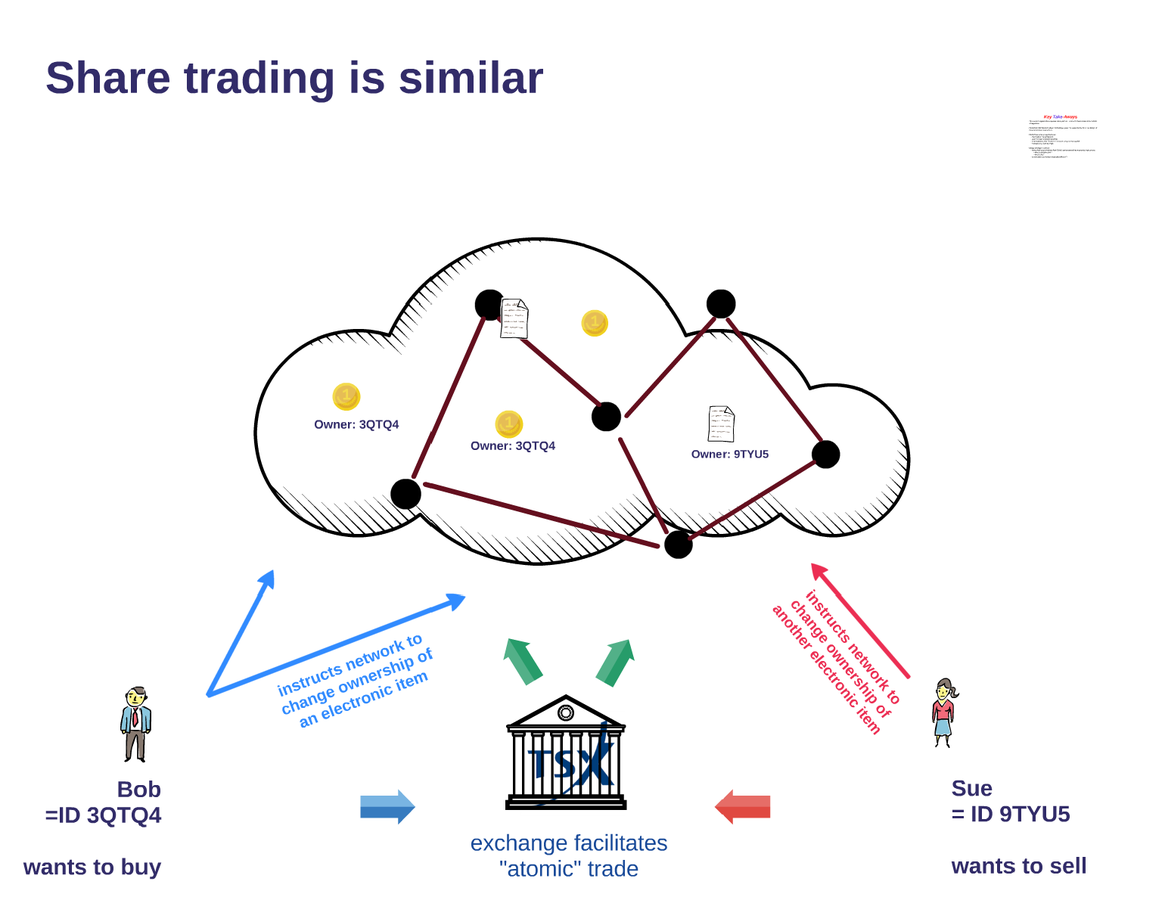

Example: One of the first segments that were disrupted from the outside: equity trading

Source: Bloomberg News, Feb 20, 2015

Note: The biggest disruptors (the HFTs) came from the outside of the traditional system (kinda).

entire career streams disappear

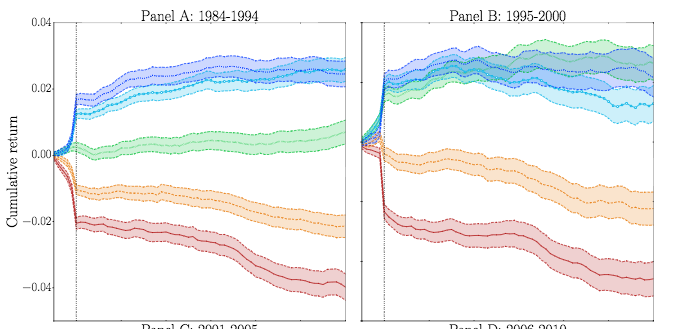

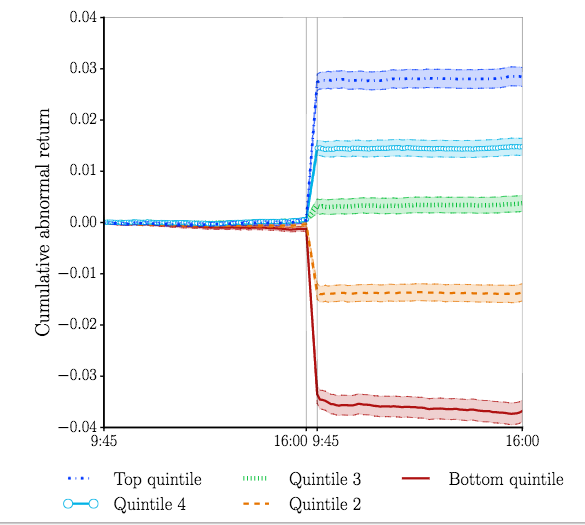

Markets get better

Source: Martineau (future UofT faculty) (WP2017)

Markets get better: the post earnings announcement drift had been a long-standing puzzle in finance

Source: Martineau (future UofT faculty) (WP2017)

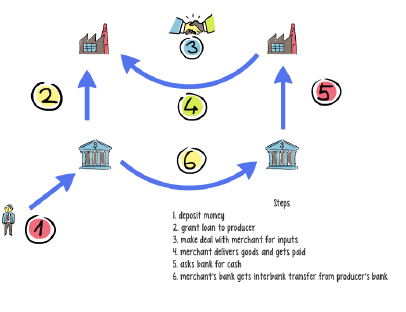

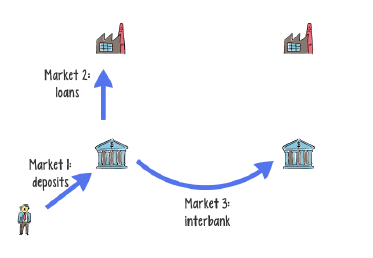

What is it that a bank does?

obtain & store information/data

process information

make decision

allocate capital

monitor and revise

automation

!

!

?

AI?

AI?

ECO?

Source: Philippon (2017)

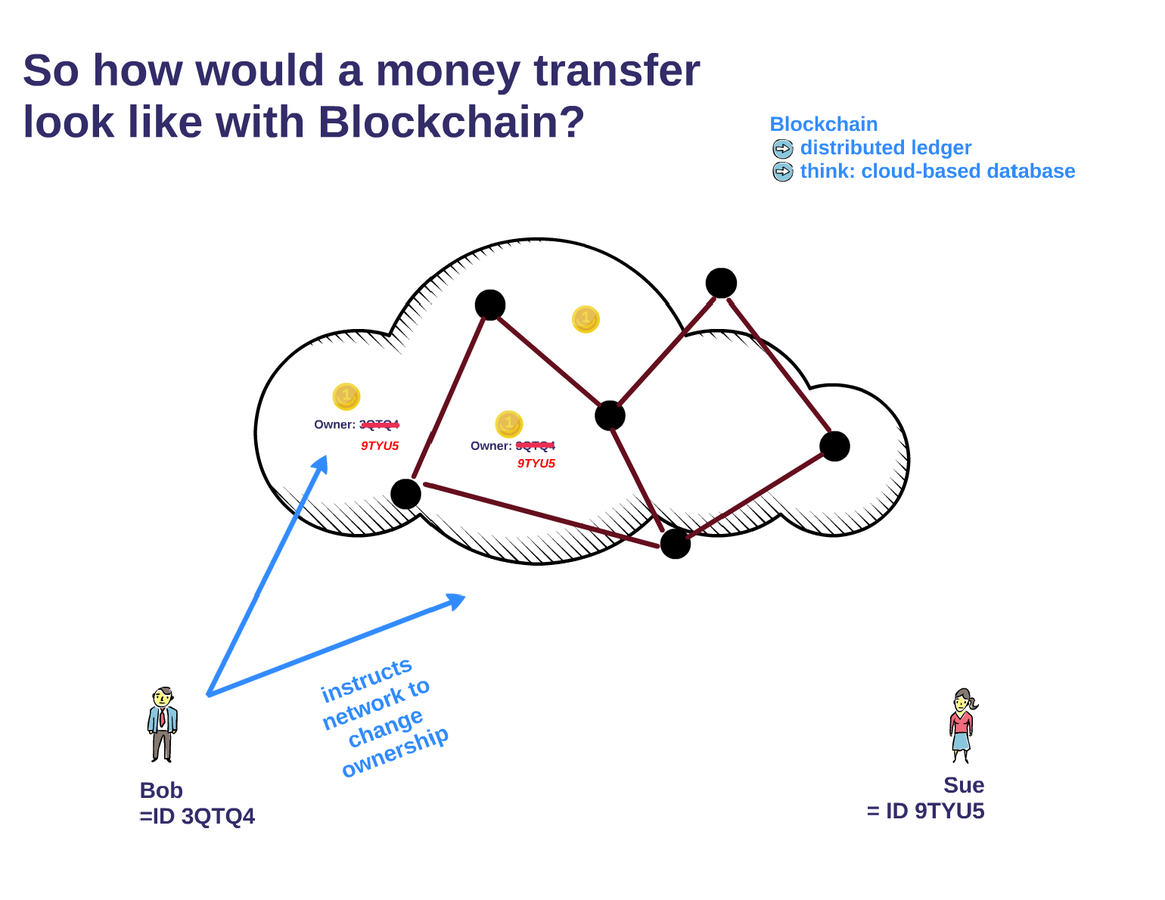

frictionless electronic transfer of information

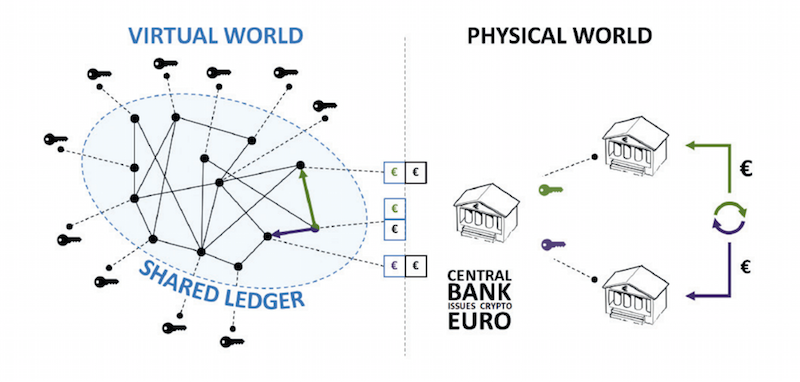

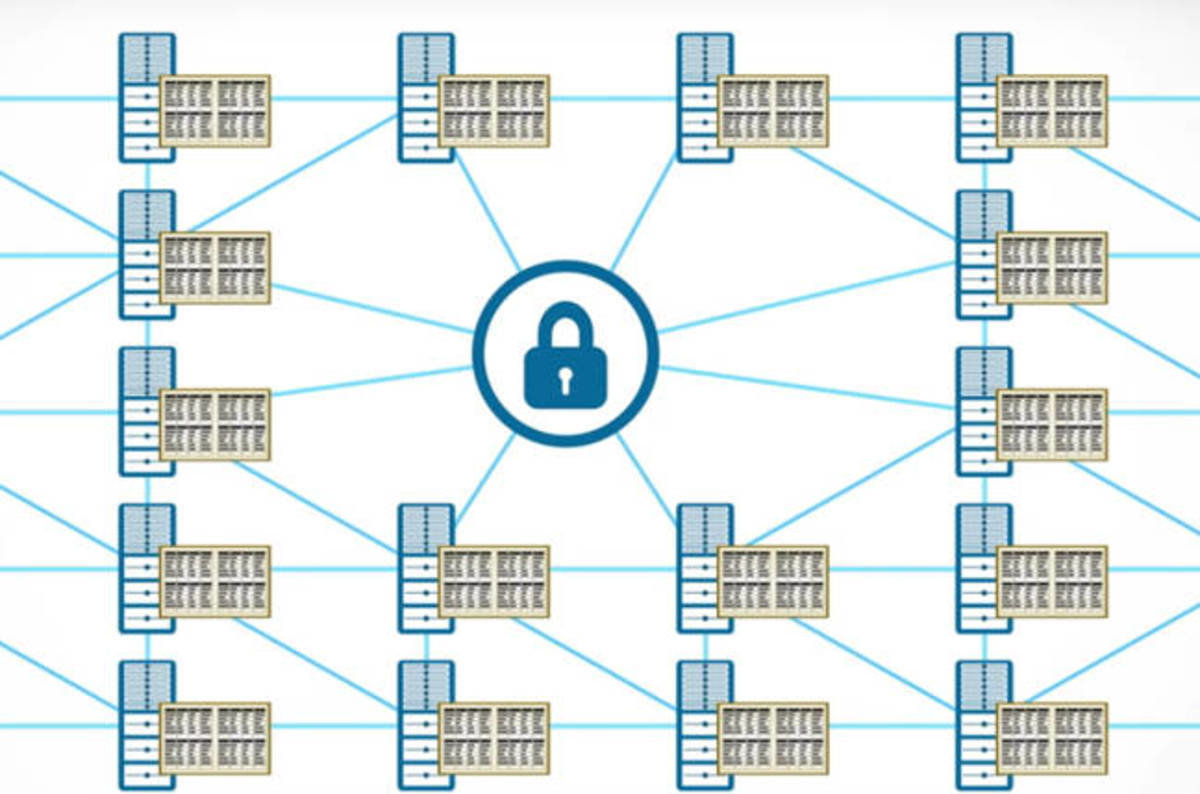

Blockchain:

frictionless electronic transfer of value

Parlour, Rajan, Walden (WP 2017): "Making Money: Commercial Banks, Liquidity Transformation and the Payment System"

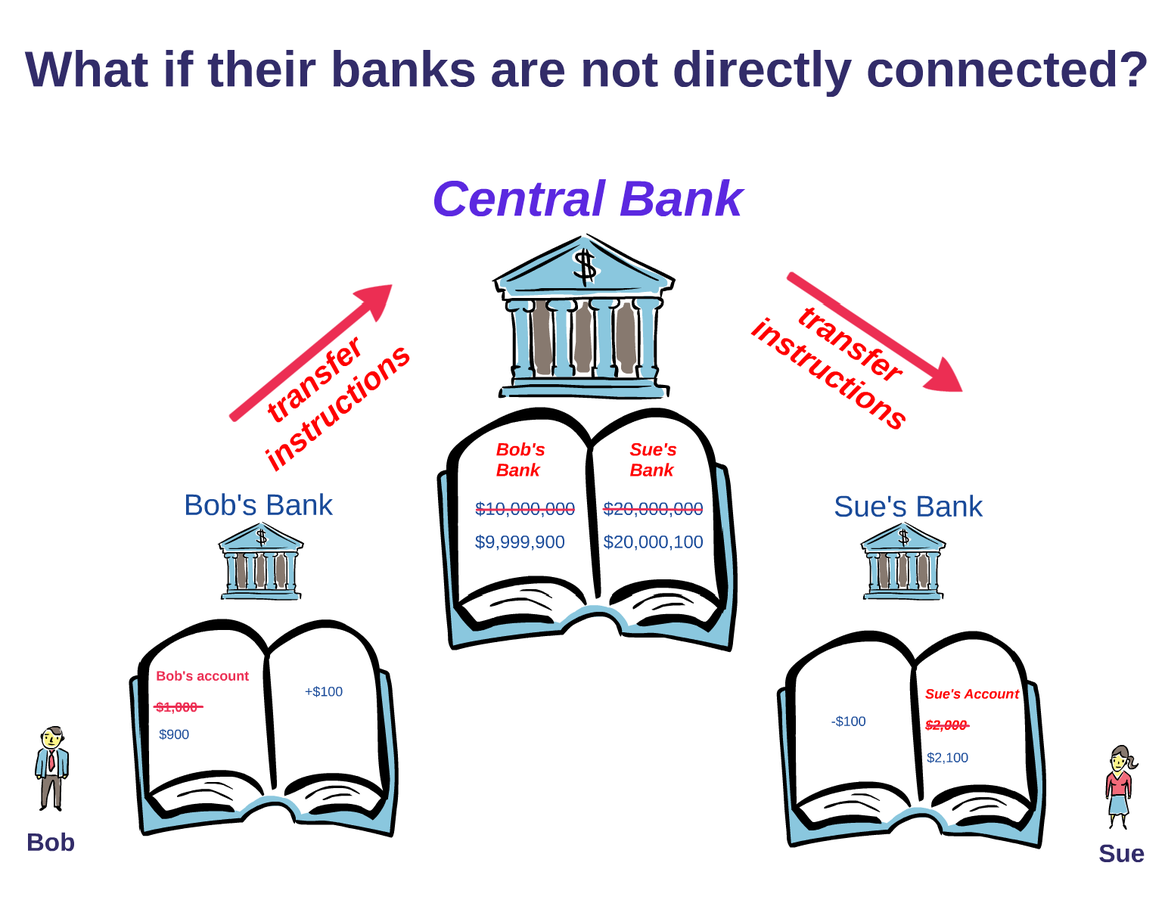

Banks do three things

Macro: impact on payment

Khapko & Zoican (WP 2017): "'Smart' Settlement

(UofT faculty)

Observations:

Khapko & Zoican (WP 2017): "'Smart' Settlement on the Blockchain"

(UofT faculty)

Results

(but Khapko, Malinova, Park, Zoican have registered a proposal)

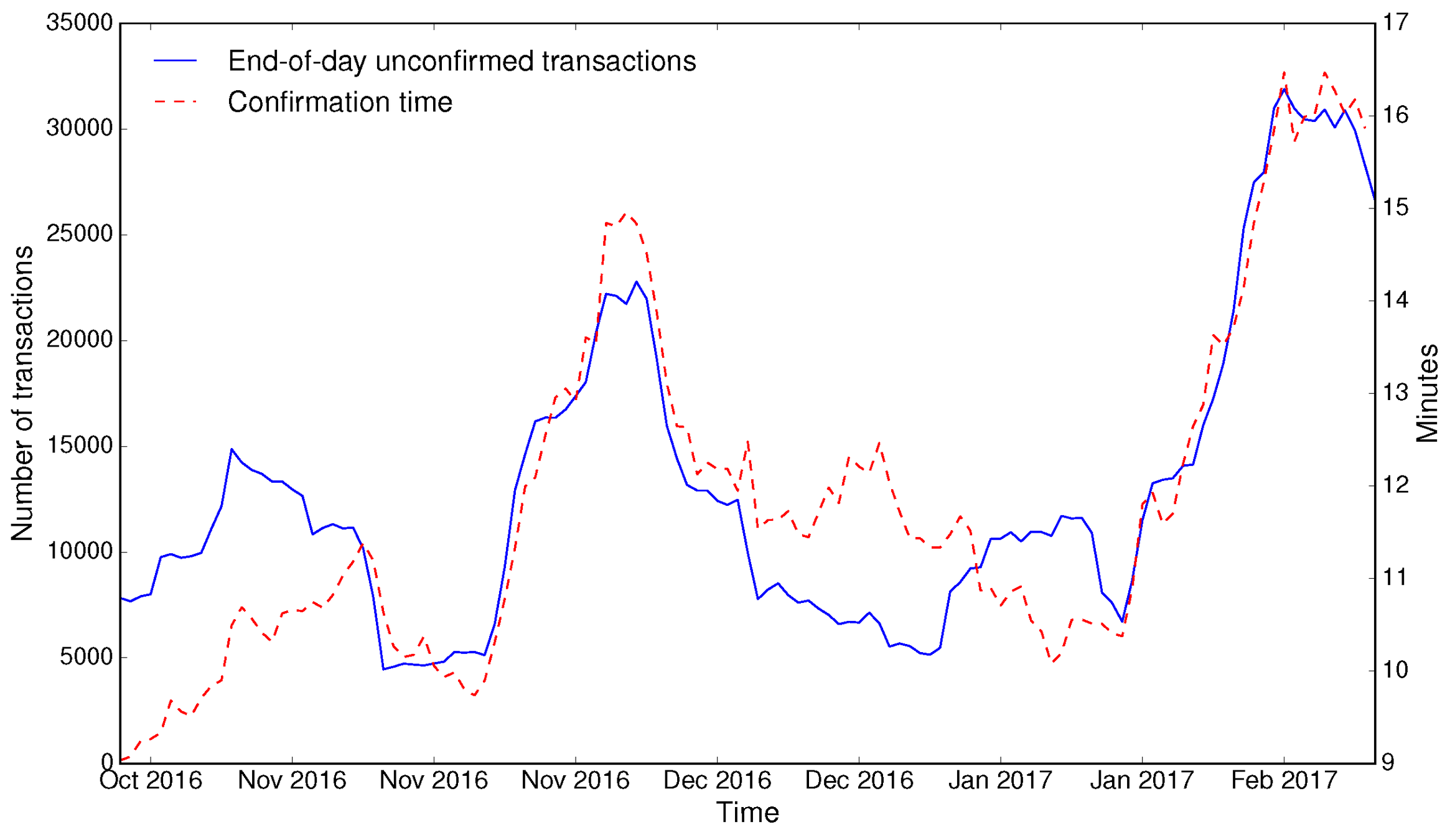

Bitcoin blockchain transaction delays and unconfirmed transactions

keep in min: Bitcoin mining is very competitive

Source: Blockchain.info

(but Khapko, Malinova, Park, and Zoican have "registered a proposal")

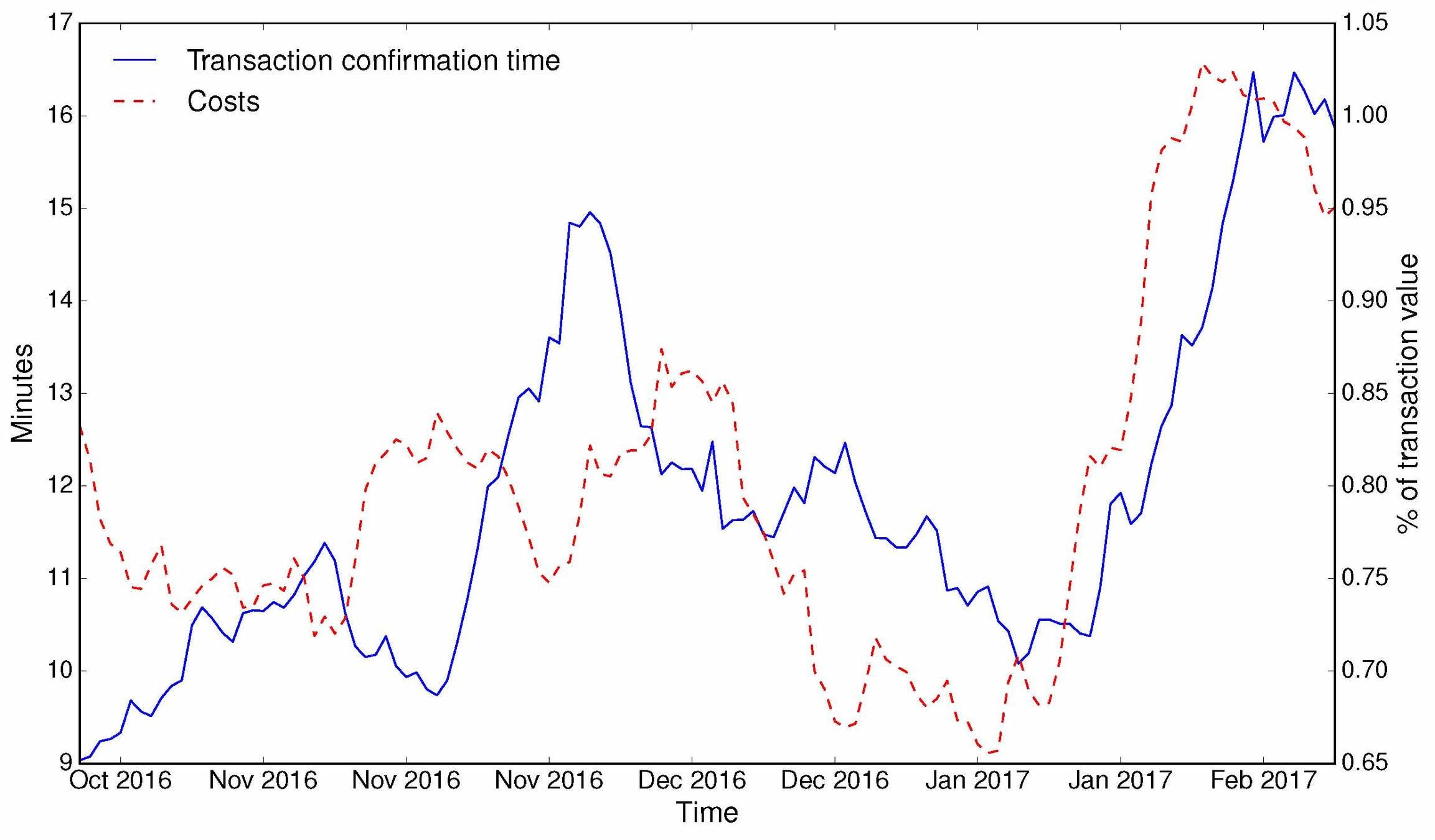

Bitcoin blockchain confirmation delays and incentive payments

keep in min: Bitcoin mining is very competitive

Source: Blockchain.info

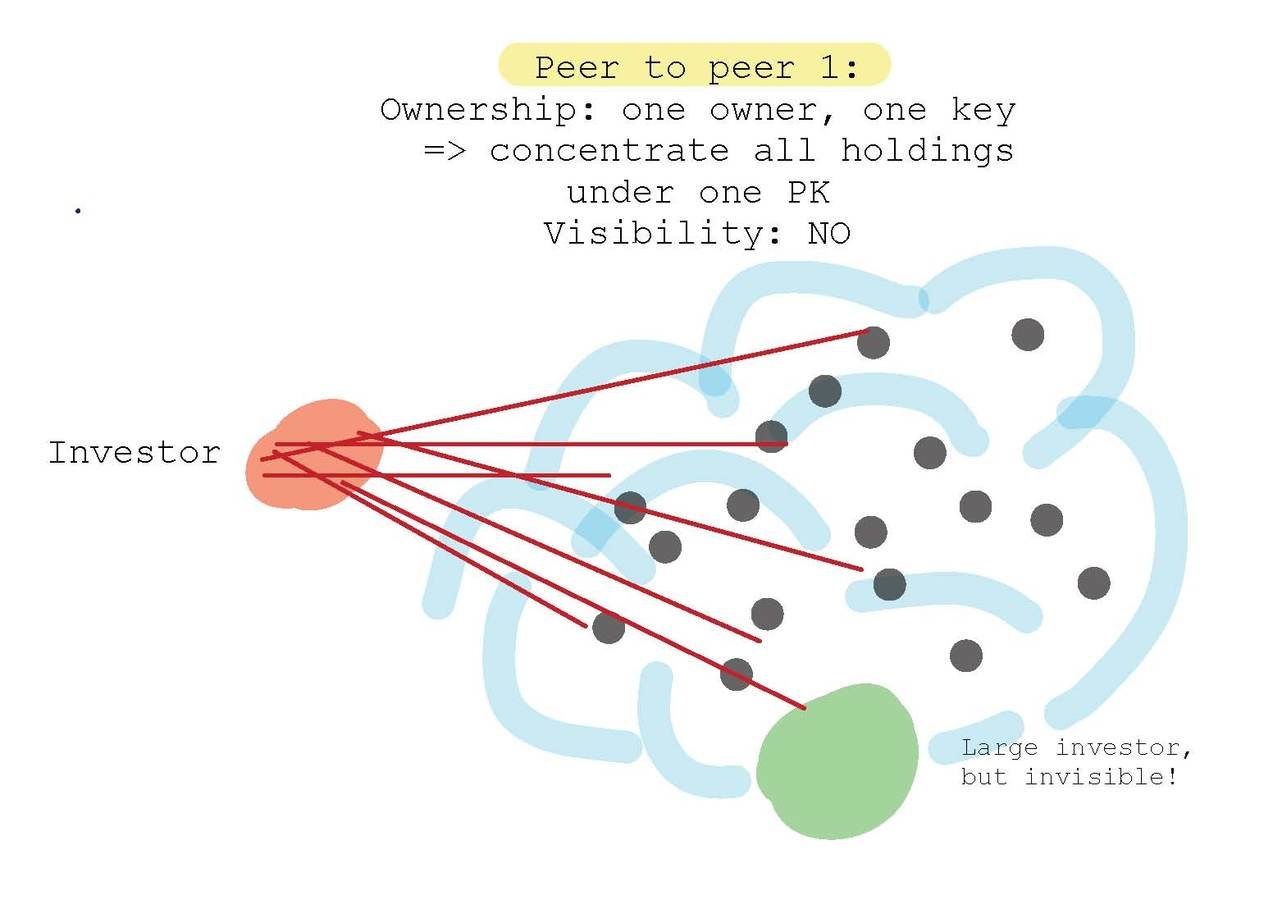

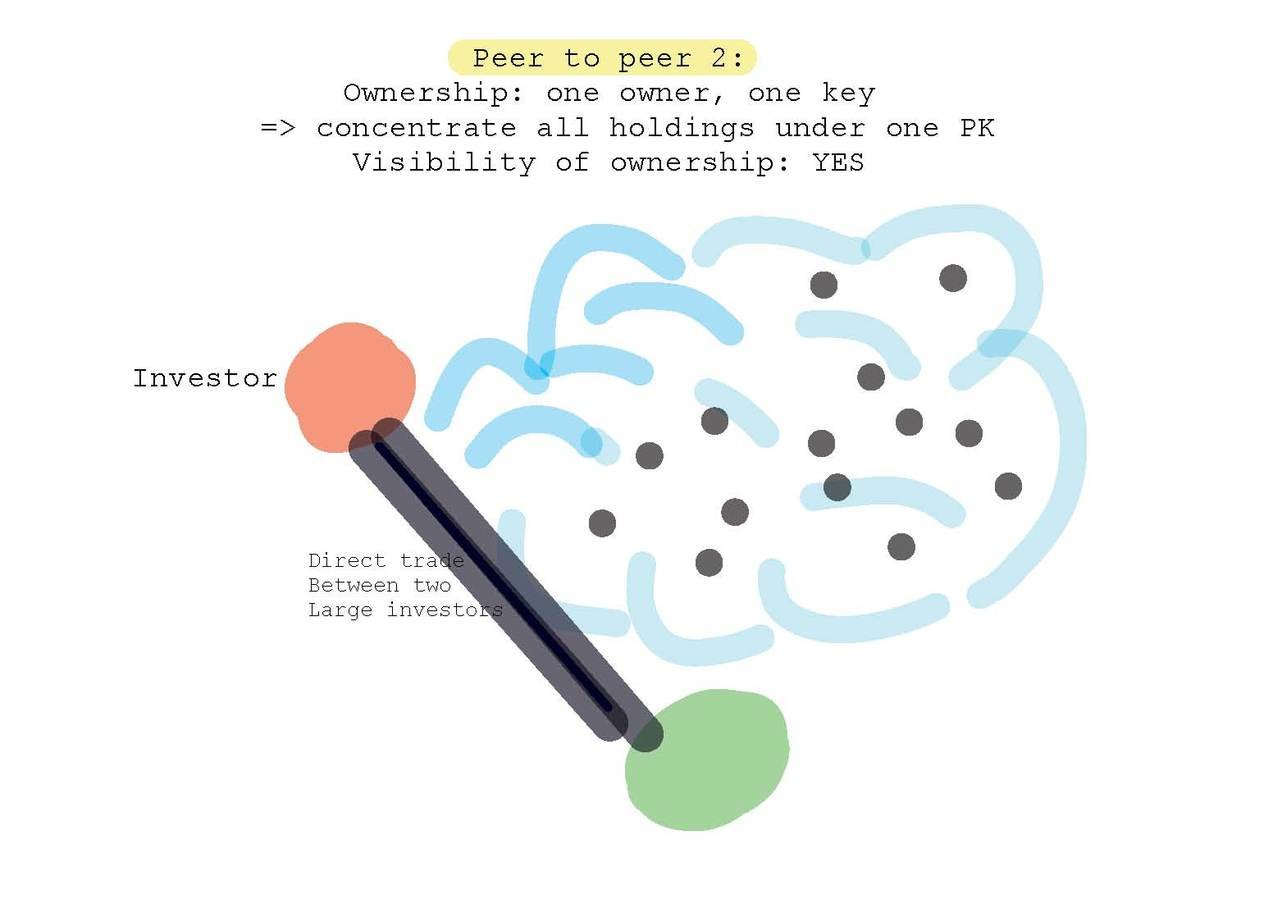

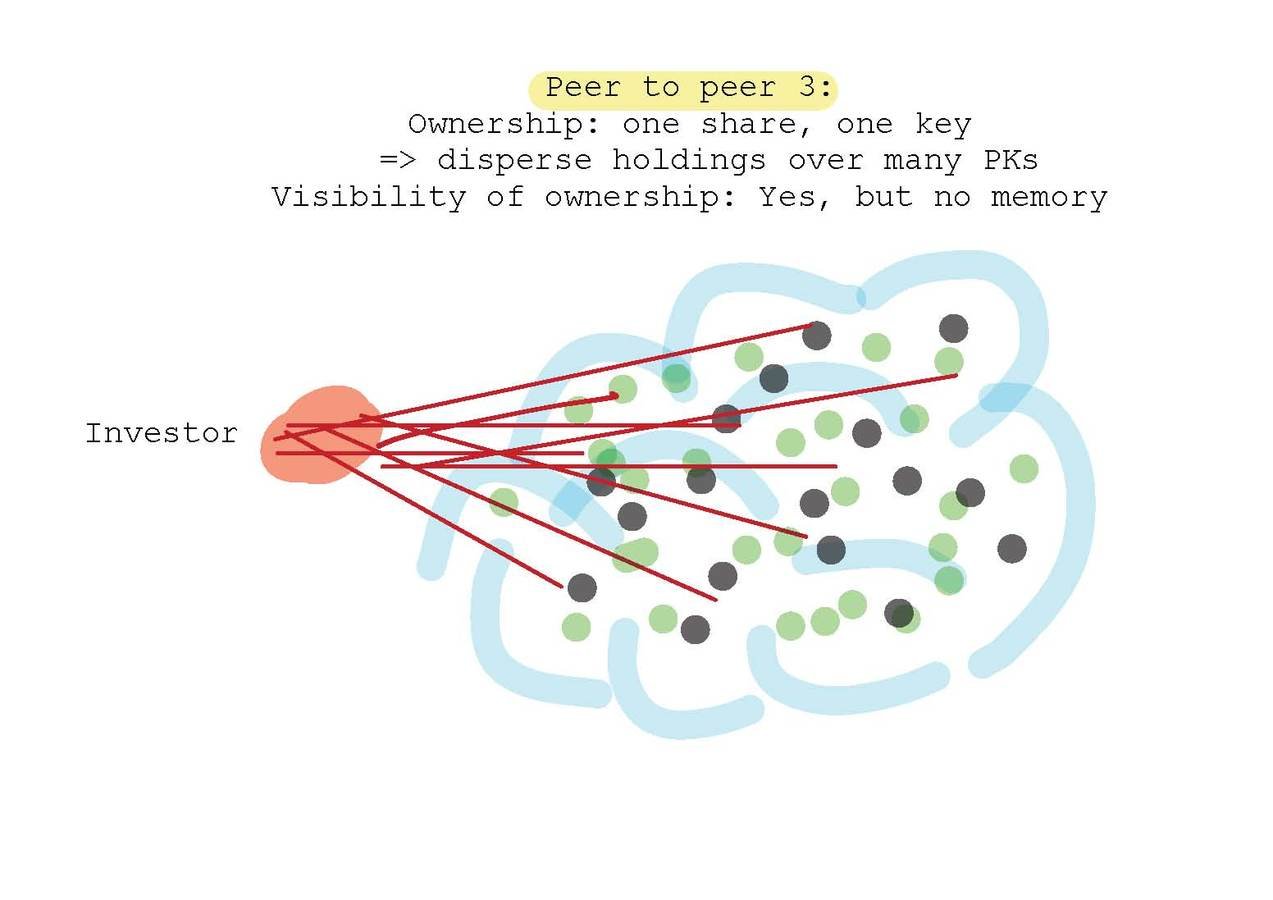

Malinova & Park (WP 2016): "Market Design with Blockchain Technology"

Observations:

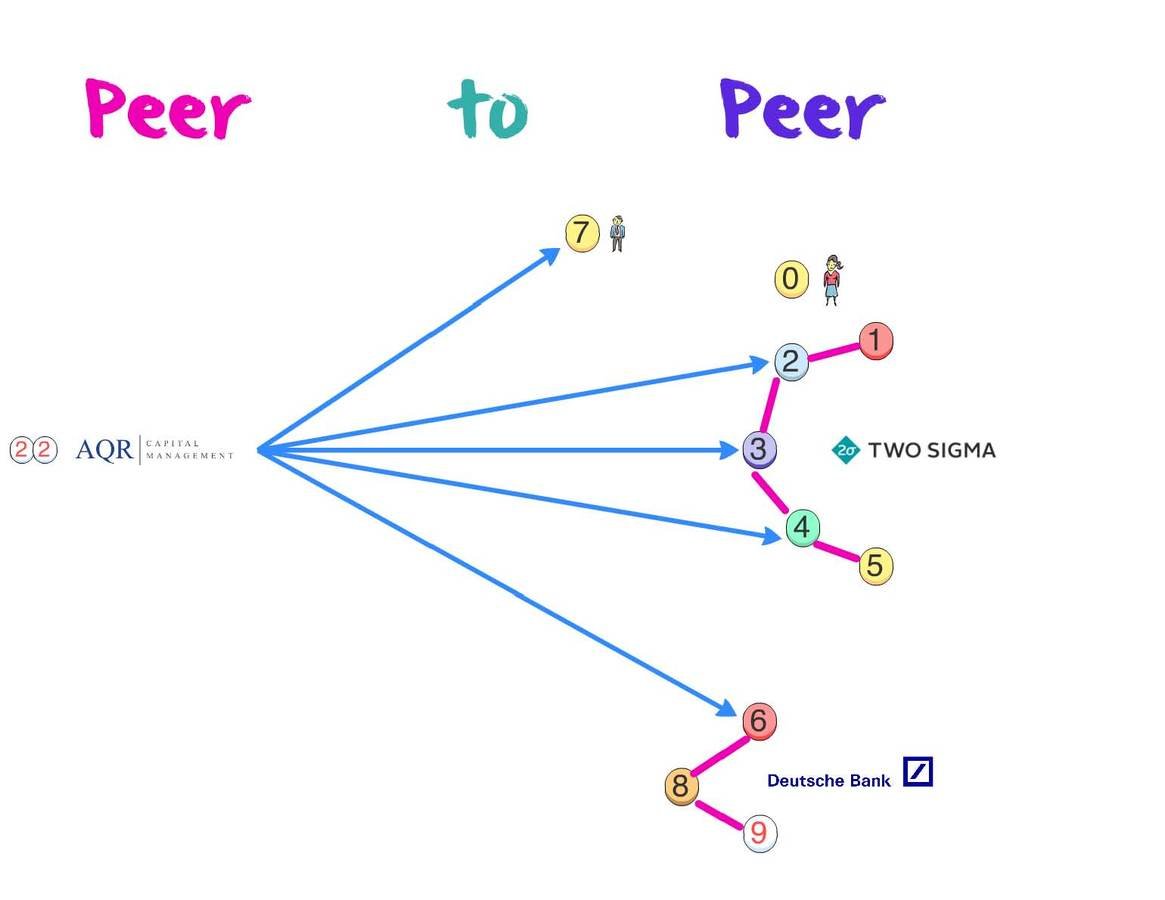

Who benefits and loses under which regime?

small traders

large trader

small traders

large trader

small traders

large trader

filled

unfilled

Setting I:

non-transparent, single IDs

Setting III: large accept

Setting III: large reject

small traders

large trader

Setting II:

transparent

What are the economic questions and how can economic analysis help us understand?

By Andreas Park

a set of slides that I used for UofT's Master in Financial Economics 2017 Berkowitz Lecture