Andreas Park PRO

Professor of Finance at UofT

Andreas Park

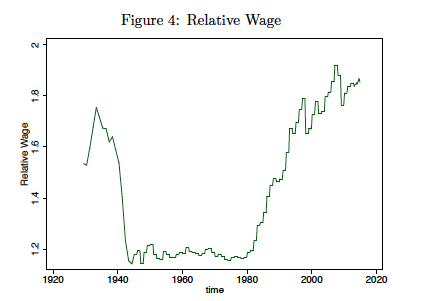

relative wage=avg wage in finance/avg rest of economy

Source: Philippon (AER 2015) "Has the U.S. Finance Industry Become Less Efficient?"

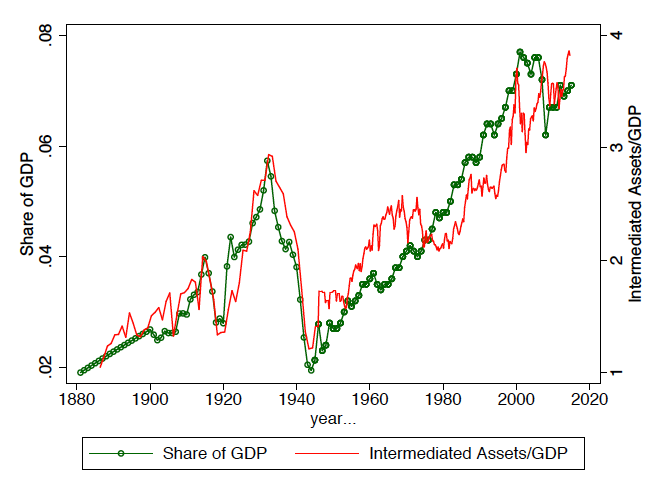

Source: Philippon (AER 2015) "Has the U.S. Finance Industry Become Less Efficient?"

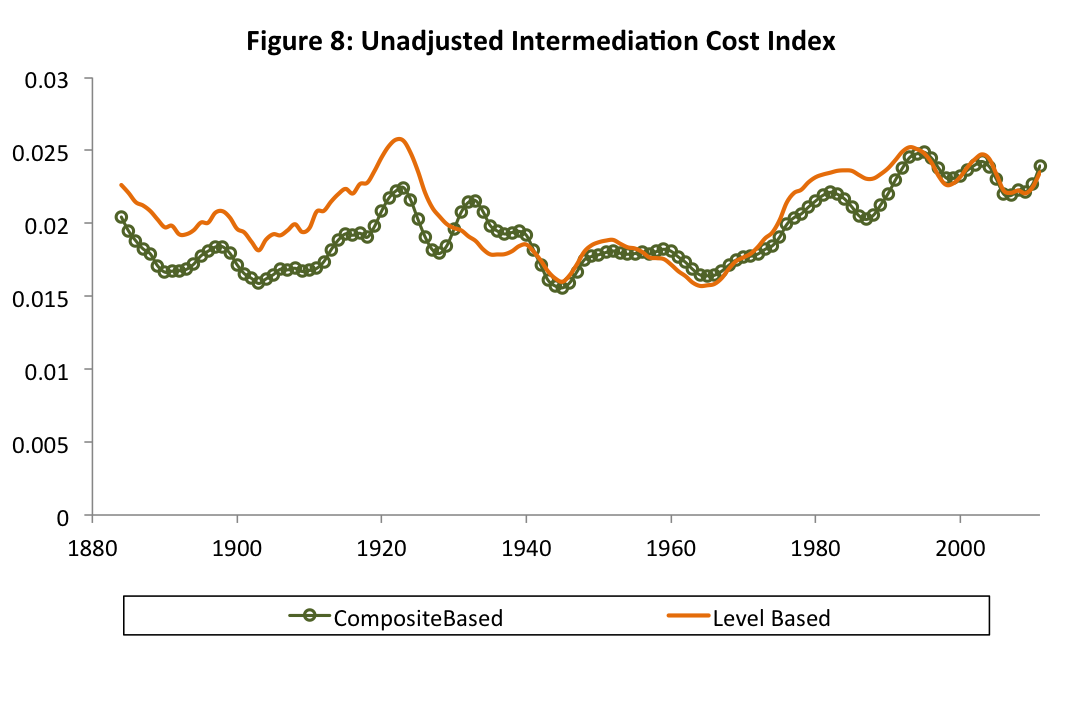

Source: Philippon (AER 2015) "Has the U.S. Finance Industry Become Less Efficient?"

Key features

Approach: Propositions that are

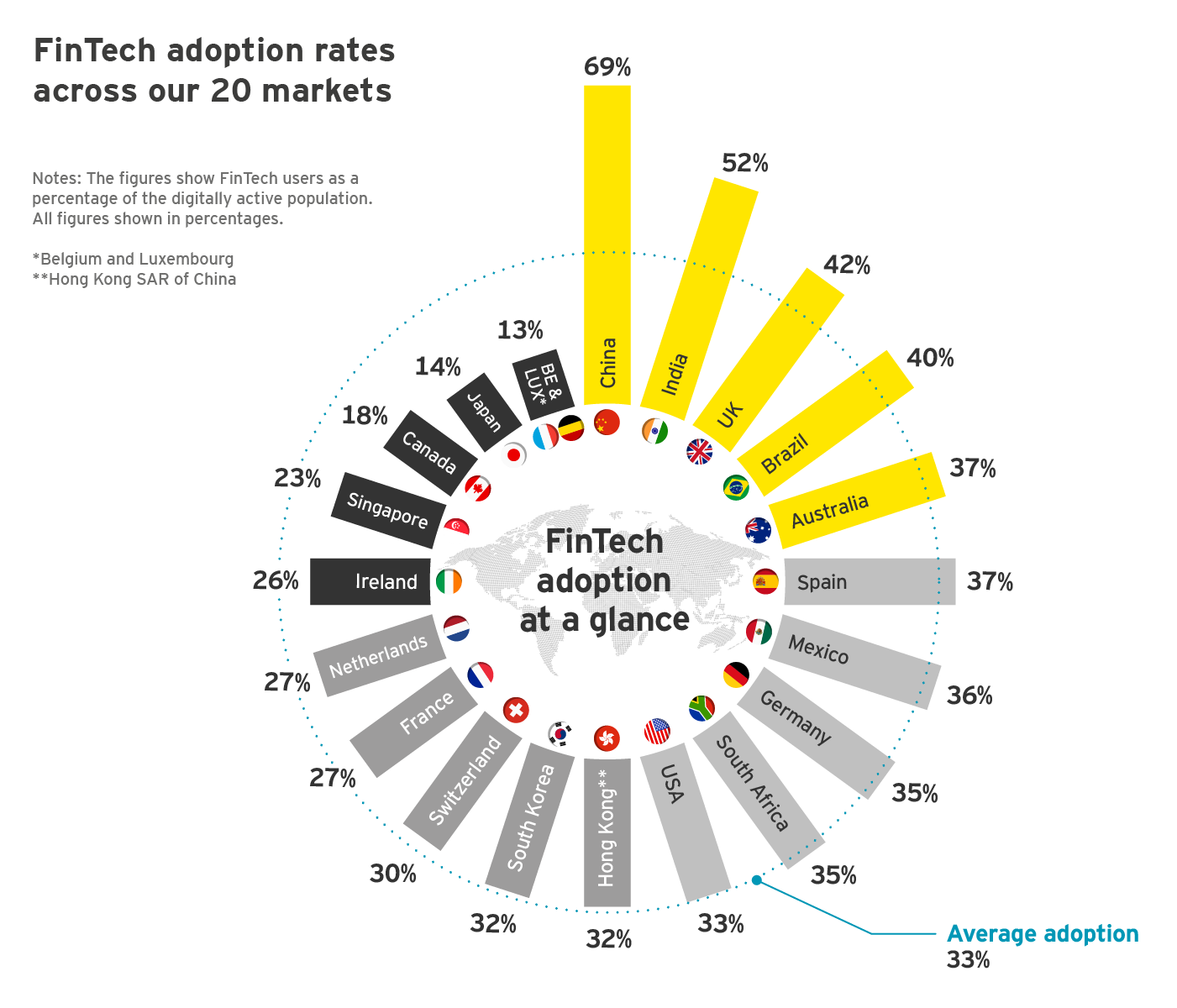

based on EY 2017 FinTech report

Impact on incumbents: struggle to deliver the seamless and personalized user.

Consequence: ripple effect

based on EY 2017 FinTech report

Problem for incumbents

Source: EY FinTech Adoption Index 2017

18%

4. Big Tech Firms

3. Those that work to replace or change the financial system as we know it.

Lending and Borrowing

Wealth Management

Payments

Investment Banking Services

Lending and Borrowing

price for loan

effort required to get loan

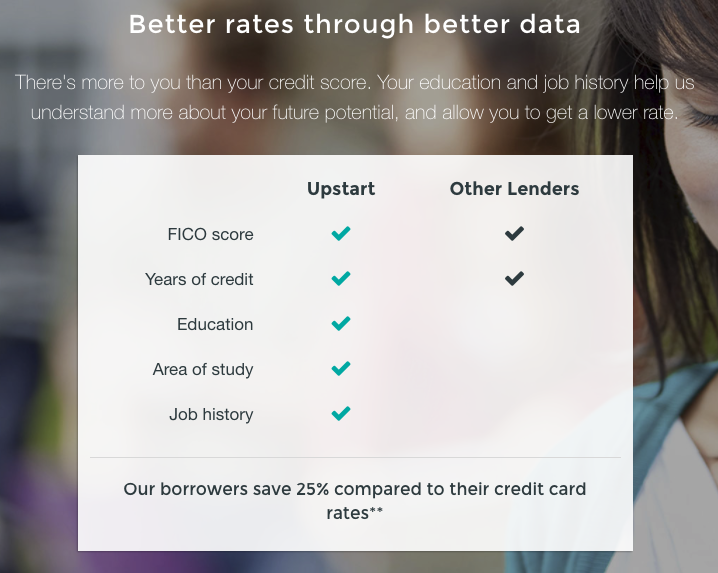

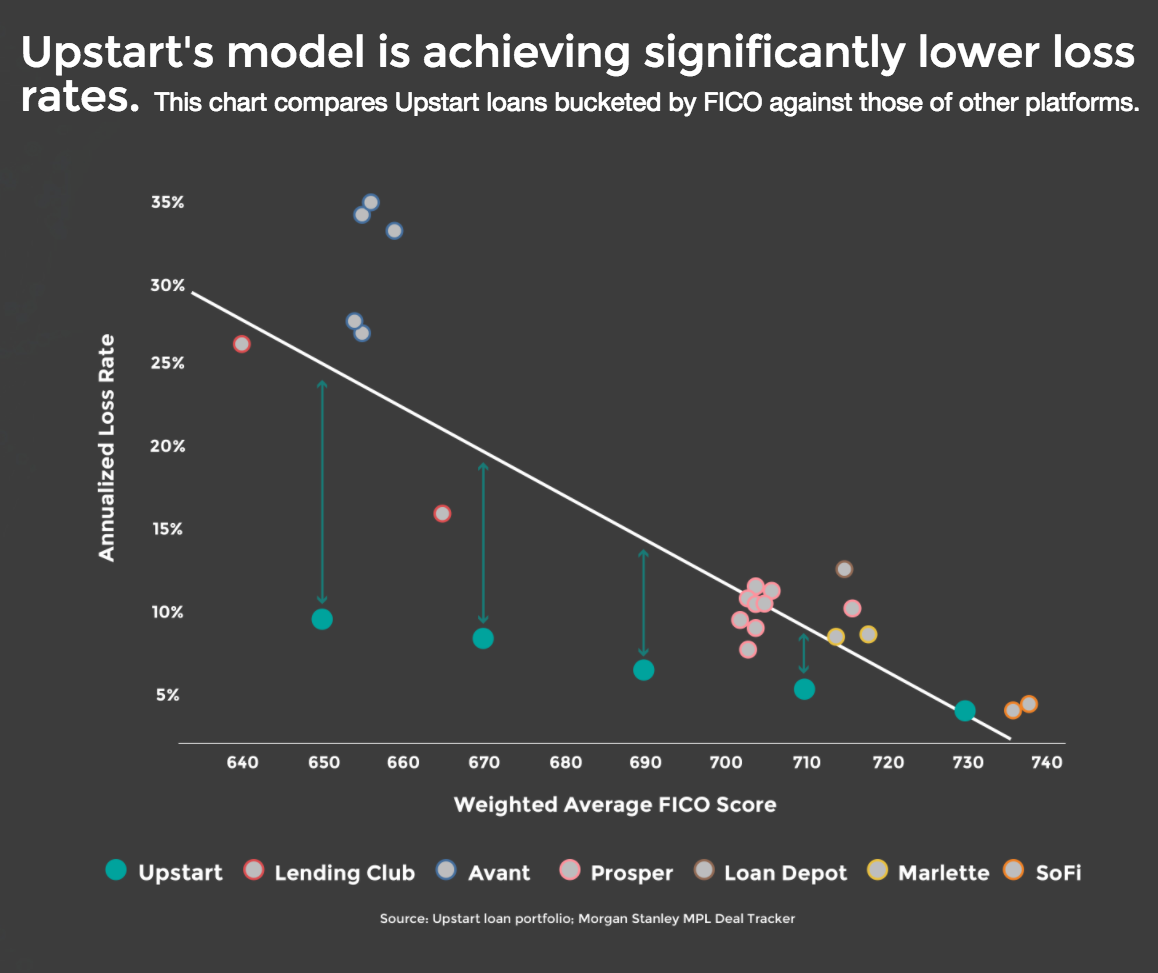

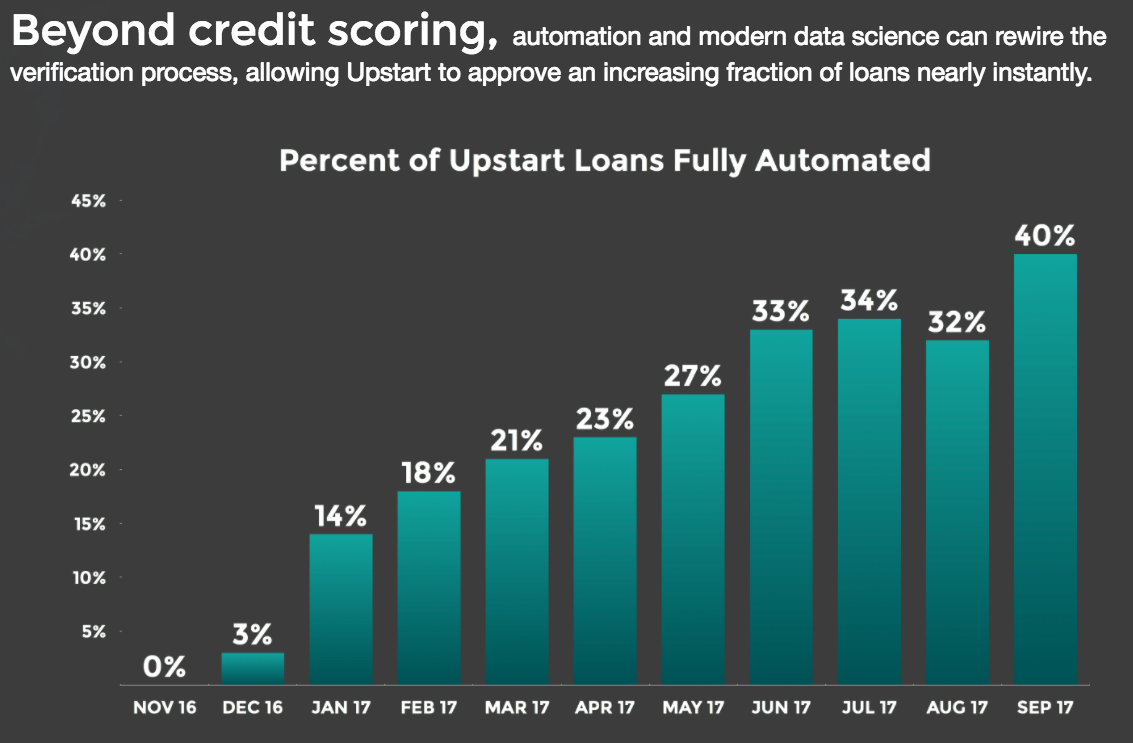

Example: Upstart

Source: upstart.com

Tools? Machine Learning

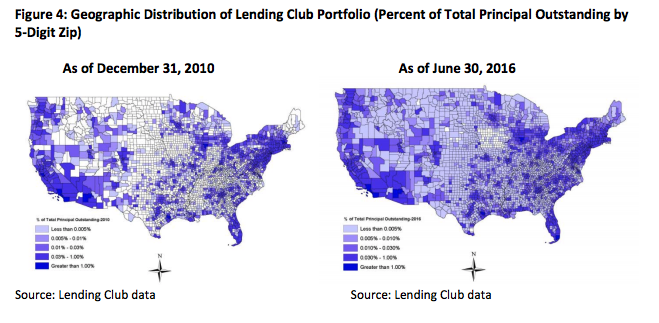

Source: Jagtiani & Lemieux, 2017, Philly Fed Working Paper 17-17

Future: Scalability

Source: Jagtiani & Lemieux, 2017, Philly Fed Working Paper 17-17

Payments

5% to cab firm and 10-day delay

International remittances: $600B (U.S.) p.a.

all in: 10% fees

Payments

500M users in India

free international transfers at Interbank rates

used by >60% of total population in Denmark

RegTech

Compliance

Security

Crowdfunding

Payments

Lending and Borrowing

Digital Wealth

Personal Finance

Platforms,

Accounting

Data and Analytics

InsurTech

Blockchain, DLT

Cryptocurrencies

Andreas Park

By Andreas Park

I used this deck for a presentation for the UofT Economics Department's RBC Chair Angelo Melino's event on FinTech 2017