Andreas Park PRO

Professor of Finance at UofT

Instructors: Andreas Park & Zissis Poulos

Commercial Paper/T-Bill like securities

1 ETH = 150 DAI

collateralization ratio 125%

seller

buyer

supplies 1 ETH collateral today

mints (=borrows) 100 yDAI to be repaid in 1 year

y

receives 92 DAI today

pays 92 DAI today

y

receives 100 yDAI

repays loan with 100 DAI

deposits yDAI and receives 100 DAI

seller

buyer

Scenario 1: ETH \(\ge\)125 DAI

deposits 100 yDAI

withdraws 100 DAI

receives balance of 1 ETH - 100 DAI

What does the seller own (ignore keeper fee)?

seller

buyer

Scenario 2: ETH falls to <125 DAI

keeper

closes undercollateralized position \(\to\) sells 0.8 ETH for 100 DAI

receives 100 DAI early

receives balance

of 0.2 ETH

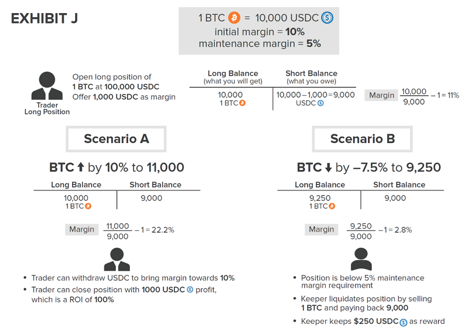

Futures-like securities

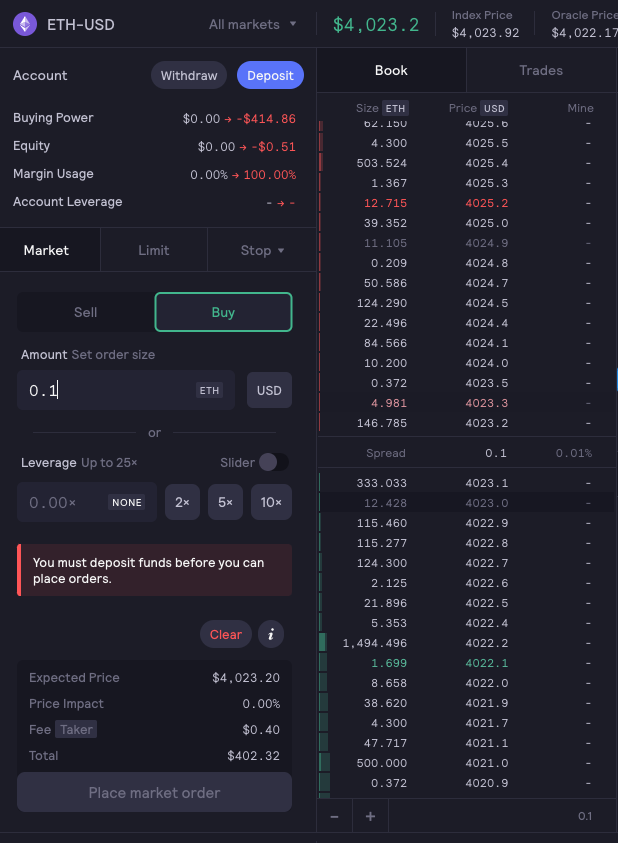

Perpetual futures on Bitcoin on dYdX

Perpetual futures on dYdX

Example

Date: Oct 27, 2021

Example

Scenario: ETH \(\downarrow\) 7.5% to 1,850

1 ETH=

1,850 USDC

1,800 USDC

\(\frac{1,850}{1,800}-1=2.78\%\)

Scenario: ETH \(\uparrow\) 10% to 2,200

1 ETH=

2,200 USDC

1,800 USDC

\(\frac{2,200}{1,800}-1=22\%\)

Options for the trader

What will happen

long balance

(what you will get)

short balance

(what you owe)

margin

1 ETH=

2,000 USDC

2,000-200

=1,800 USDC

\(\frac{2,000}{1,800}-1=11\%\)

Beginning

Smart Contract Derivatives with Synthetix

Note: this screenshot is from June 2021; the equity synths have since been removed

Smart Contract Derivatives with Synthetix: how does it work?

Example for Synthetix

assets

price

quantity

fraction of debt

BTC

ETH

USDC

10,000

1,000

1

2

20

20,000

total debt: 60,000

33% of 60,000=20,000

33%

33%

2 sBTC

20 sETH

20,000 sUSDC

minted

gain/loss

Example for Synthetix: prices for ETH and BTC up

assets

price

quantity

fraction of debt

BTC

ETH

USDC

20,000

5,000

1

2

20

20,000

total debt: 160,000

33%=53,333

2 sBTC

20 sETH

20,000 sUSDC

minted

gain/loss

33%=53,333

33%=53,333

40,000-53,333

=-13,333

100,000-53,333

=46,667

20,000-53,333

=-33,333

you effectively bet that your position outperforms the pool

Example for Synthetix: prices for ETH and BTC down

assets

price

quantity

fraction of debt

BTC

ETH

USDC

5,000

500

1

2

20

20,000

total debt: 40,000

33%=13,333

2 sBTC

20 sETH

20,000 sUSDC

minted

gain/loss

10,000-13,333

=-3,333

20,000-13,333

=7,777

33%=13,333

33%=13,333

10,000-13,333

=-3,333

main product:

BTC perpetual futures contract

initial margin =

amount of collateral needed to be posted

maintenance margin =

amount of price movement after which collateral needs to be replenished

Source: Harvey, Ramachandran, and Santoro (2020)

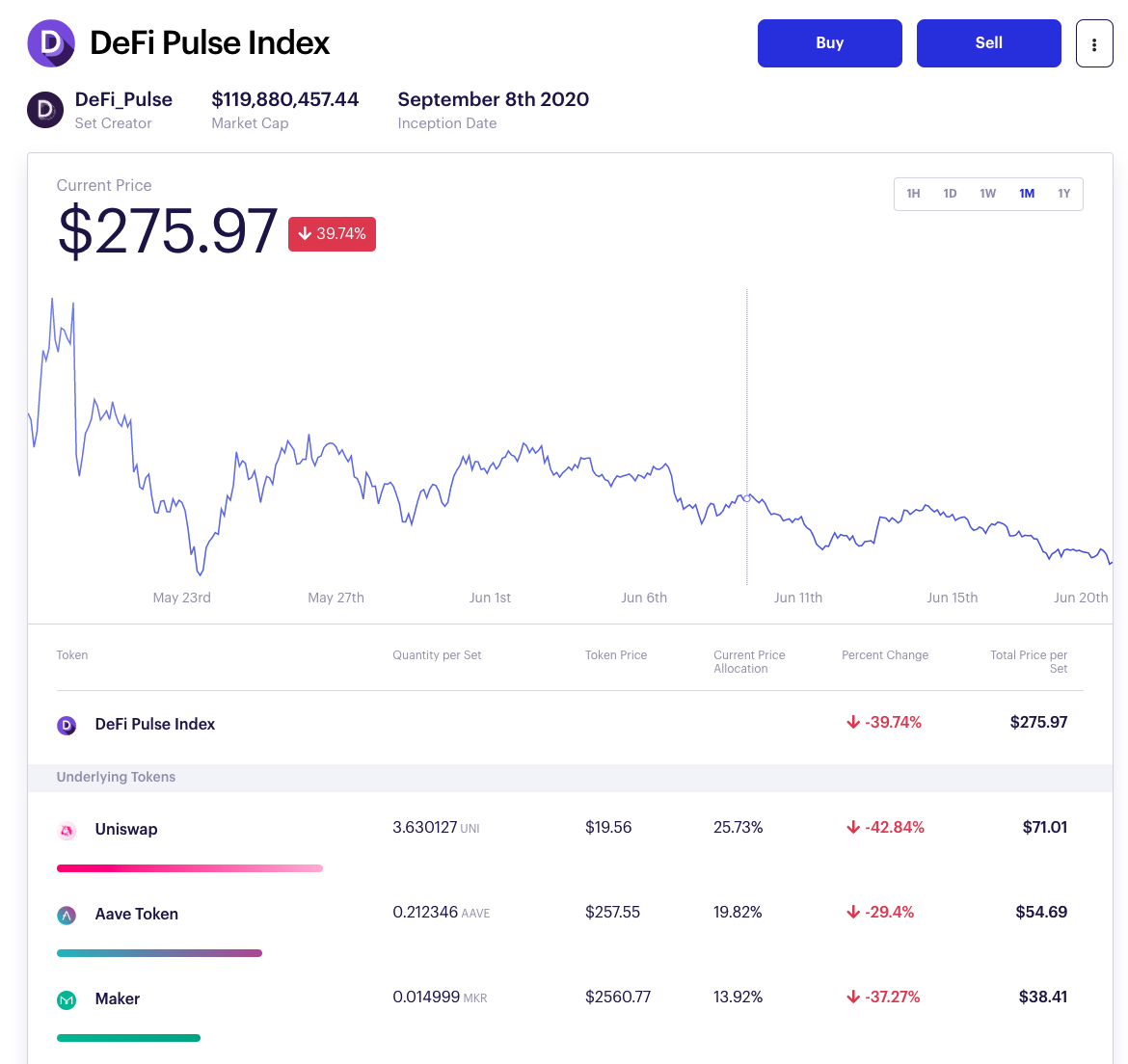

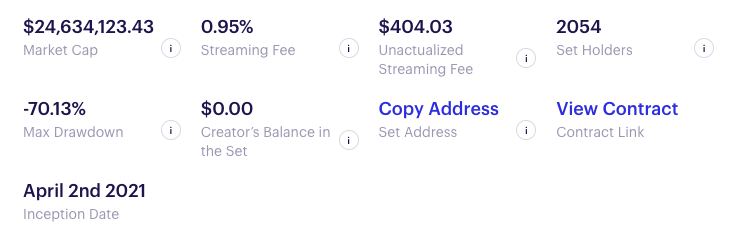

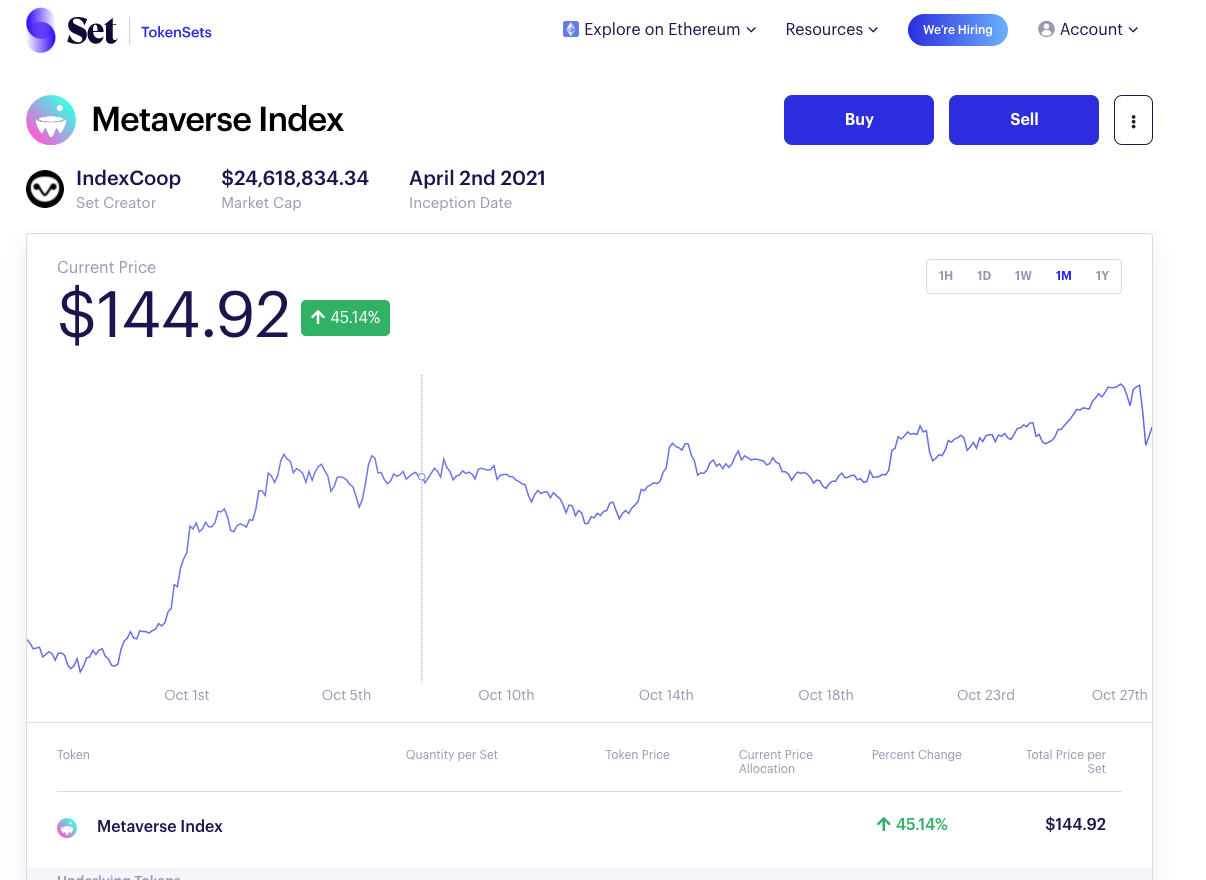

ETF-like securities

Securities Creation: Tokensets

idea: create new mutual fund like asset

Securities Creation: Tokensets

@financeUTM

andreas.park@rotman.utoronto.ca

slides.com/ap248

sites.google.com/site/parkandreas/

youtube.com/user/andreaspark2812/

By Andreas Park

This slide deck provides an overview of DeFi protocols for derivatives (broadly defined). It draws insights from Harvey, Ramachandran, and Santoro (2020) "DeFi and the Future of Finance"