Andreas Park PRO

Professor of Finance at UofT

Paper by: Jonathan Brogaard, James Brugler, and Dominik Roesch

Discussion by: Andreas Park

May 14, 2021

8th Annual Conference on Financial Market Regulation, 2021

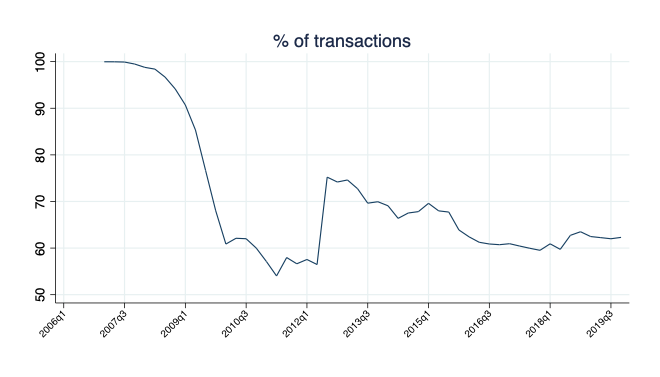

And that's why people are upset:

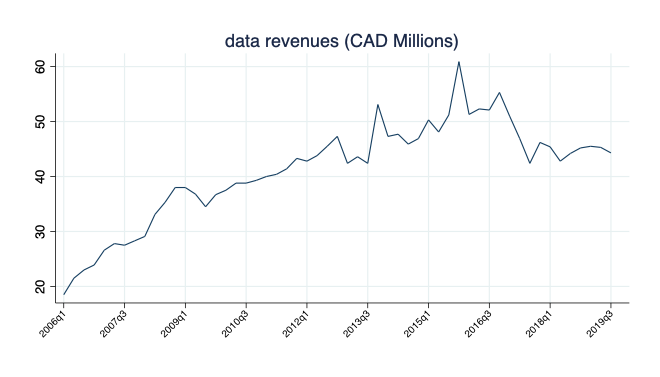

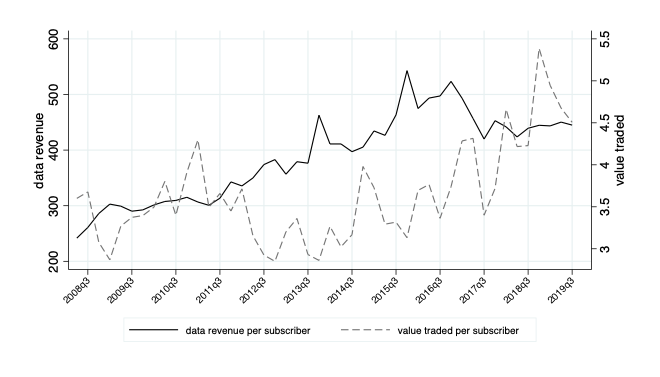

When venue introduces data fees:

Methodology

Measures & Interpretation

Story & explanation

Odds-and-ends

One question: do they even have the free data?

Constraints

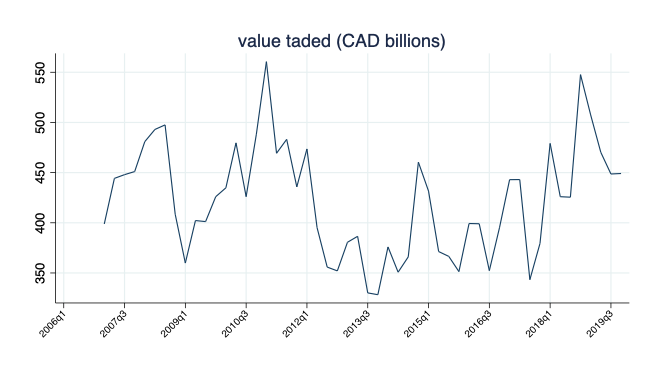

Example: Volume

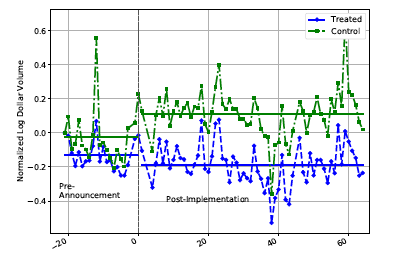

Difference-in-difference vs marketwide structural shift?

E-Spread?

Well-argued paper with clear research question and credible answers ("it's not quite so easy to up the fees")

My suggestion: Focus on visible liquidity & broker routing and trim rest

@financeUTM

andreas.park@rotman.utoronto.ca

slides.com/ap248

sites.google.com/site/parkandreas/

youtube.com/user/andreaspark2812/

By Andreas Park