Andreas Park PRO

Professor of Finance at UofT

Paper by Alfred Lehar & Christine Parlour

Discussion by Andreas Park

AFA 2022

What is Decentralized Finance?

decentralized finance =

provision of financial services without the necessary involvement of a traditional financial intermediary at extremely low costs

key ingredient =

blockchain technology =

a common infrastructure for decentralized code execution

How do you set the price?

Price mechanism:

Prices

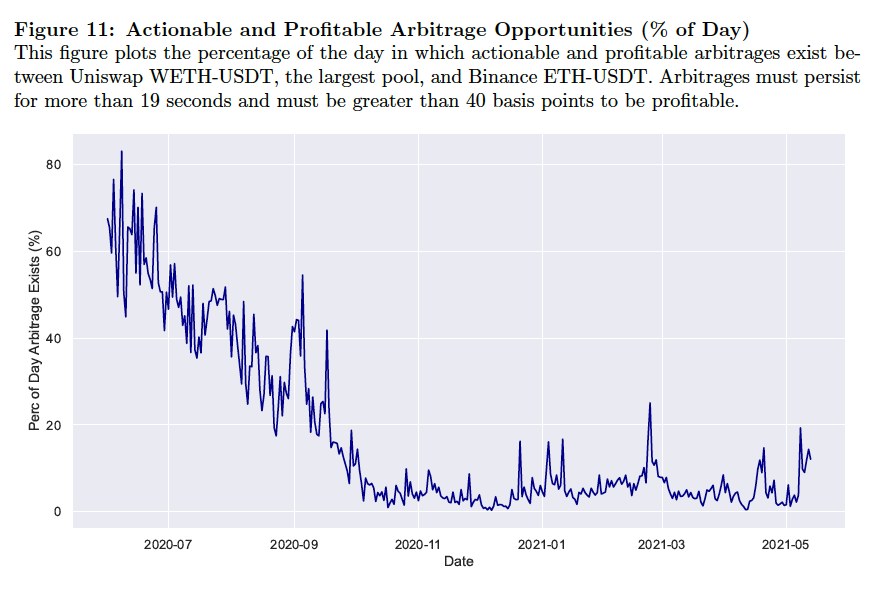

Small observation

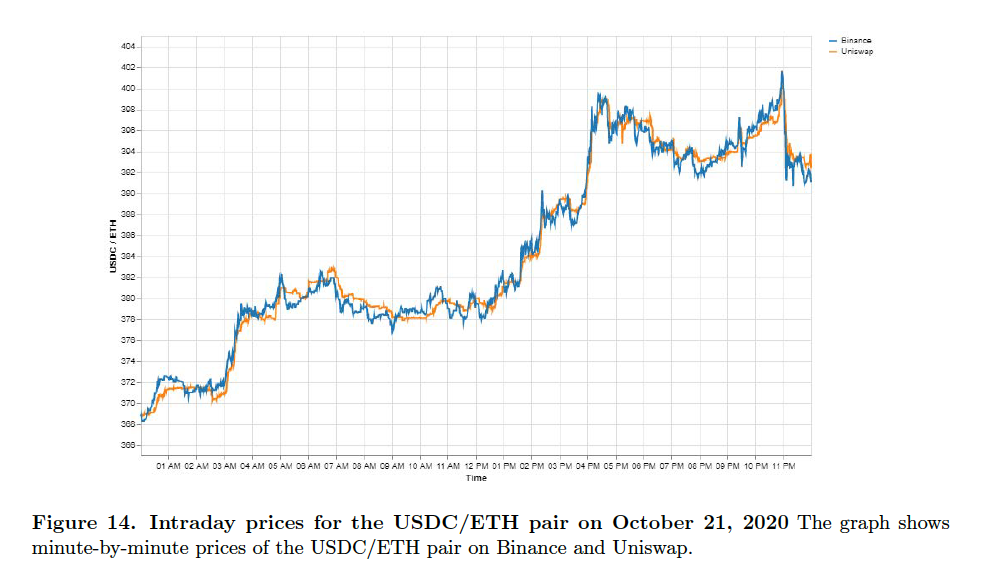

Source: Peter O'Neill "Can Markets be Fully Automated? Evidence From an ‘Automated Market Maker", Nov 2021

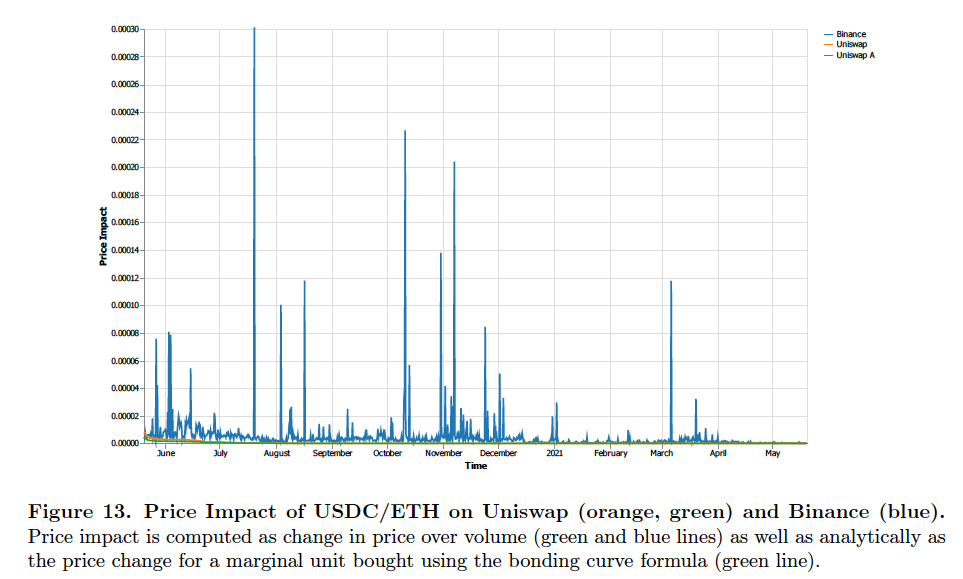

We can see that price impact on Binance almost always exceeds that on Uniswap.

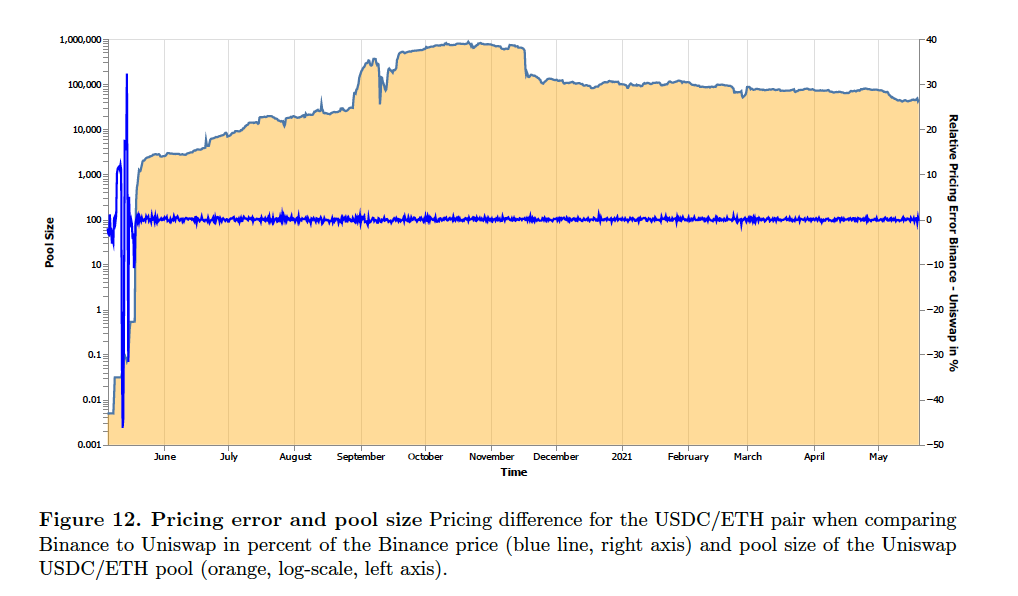

"We find that as Uniswap liquidity provision becomes larger, the Uniswap price undertakes a larger weight in determining the equilibrium cryptocurrency valuation than the Binance price." Trust in DeFi: An Empirical Study of the Decentralized Exchange by Jianlei Han, Shiyang Huang, and Zhuo Zhong

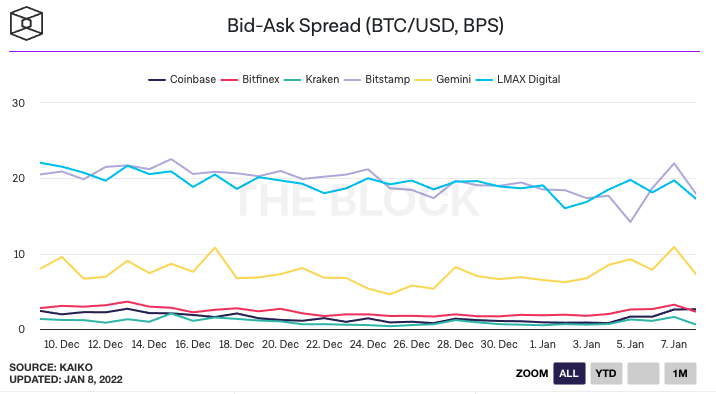

between .5 and 1 bps

Small suggestions: maybe compure implicit spread measure for AMM for comparison

@financeUTM

andreas.park@rotman.utoronto.ca

slides.com/ap248

sites.google.com/site/parkandreas/

youtube.com/user/andreaspark2812/

a

b

c

d

e

f

g

However: although front-running is annoying, it is only a concern if it is intrinsically profitable.

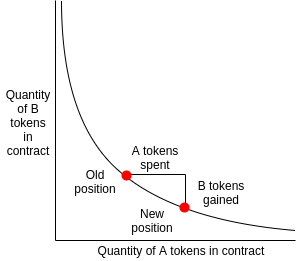

My paper:

\(X\)

\(Y\)

normal trade: sell \(x\) \(\to\) get \(y'\)

\(Y-y'\)

\(X+x\)

front-running:

\(Y-y'-y''\)

\(X+2x\)

\(y'>y''~\Rightarrow\)

front-running is intrinsically profitable

Disclaimer:

\(X\)

\(Y\)

\(Y-y'\)

\(X+x\)

\(Y-y'-y''\)

\(X+2x\)

\(y'=y''~\Rightarrow\)

front-running is not intrinsically profitable

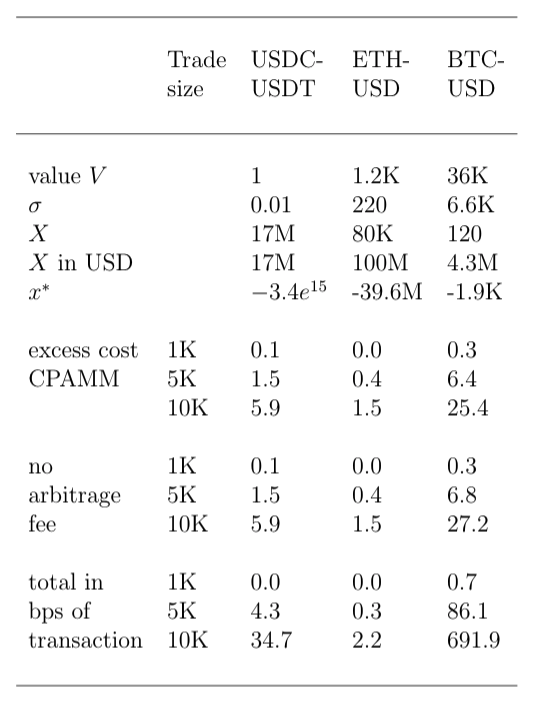

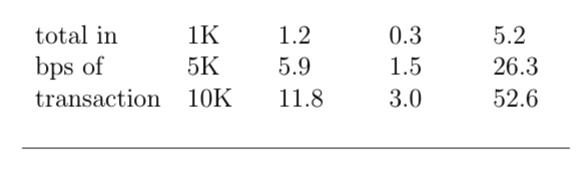

CPAMM

canonical

By Andreas Park