Andreas Park PRO

Professor of Finance at UofT

Blockchain and Decentralized Finance:

A 2023 Primer

Presenter: Andreas Park

What is a Blockchain?

What is a Cryptocurrency?

Why is this idea powerful?

payments

stocks, bonds, and options

swaps, CDS, MBS, CDOs

insurance contracts

A blockchain is a

What makes DeFi different from TradFi

decentralized finance =

provision of financial service functionality without the necessary involvement of a traditional financial intermediary like a bank or broker-dealer*

digital media =

provision of information service functionality without the necessary involvement of a traditional information intermediary like a publisher, library, or newagency

*my take: applies to only commoditizable services

payments network

Stock Exchange

Clearing House

custodian

custodian

beneficial ownership record

seller

buyer

Broker

Broker

AMM Pricing

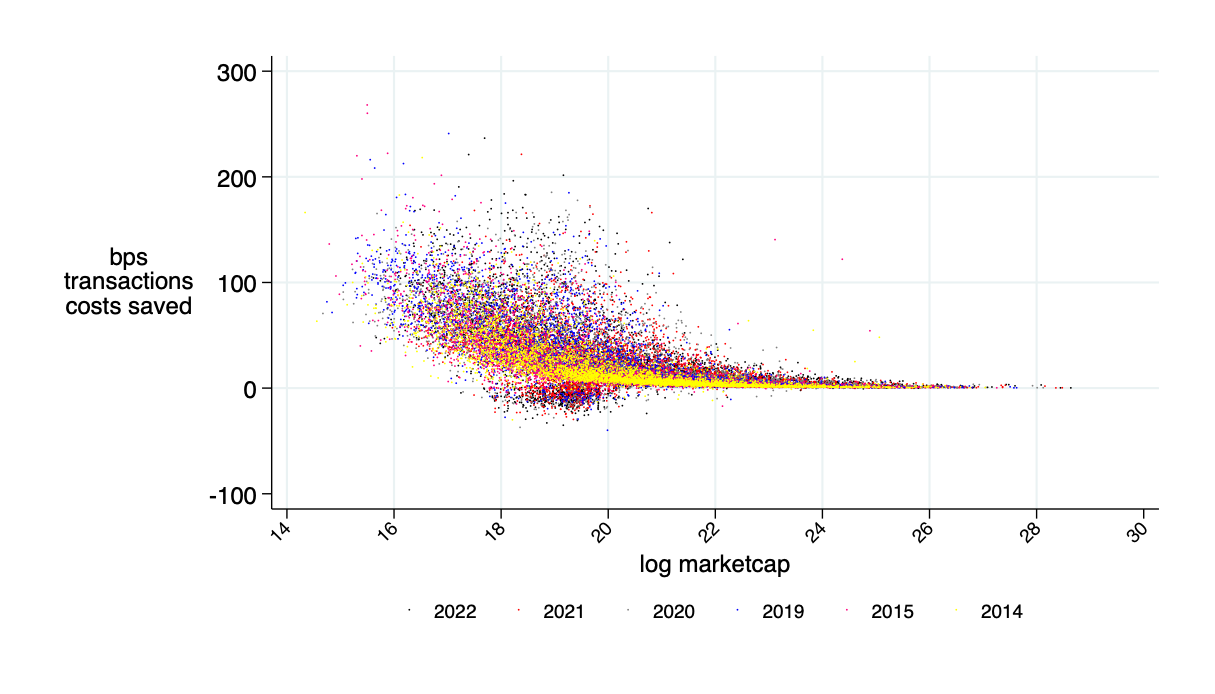

Source of savings:

Possible transaction cost savings when applied to equity trading: \(\approx\) 30%

Source: "Learning from DeFi: Would Automated Market Makers Improve Equity Trading?" working paper, Malinova & Park 2023

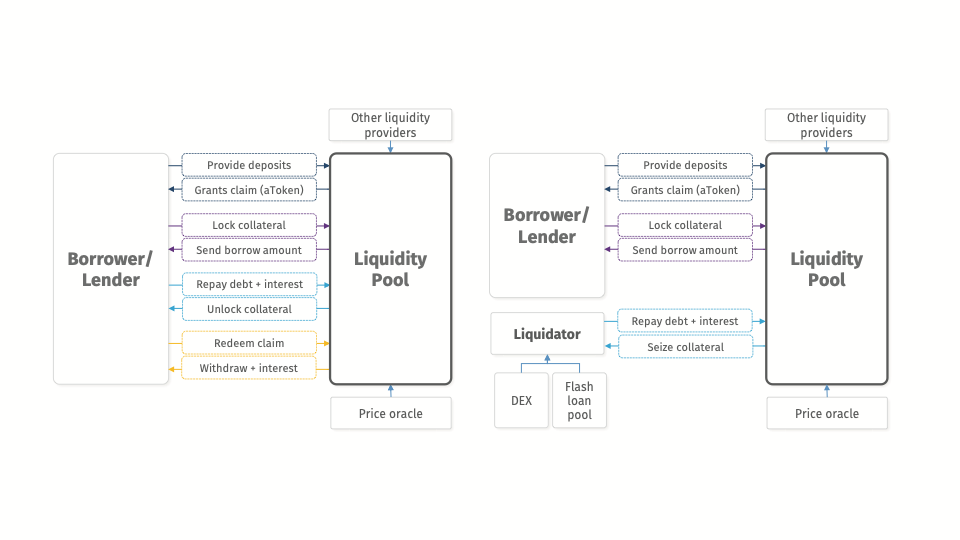

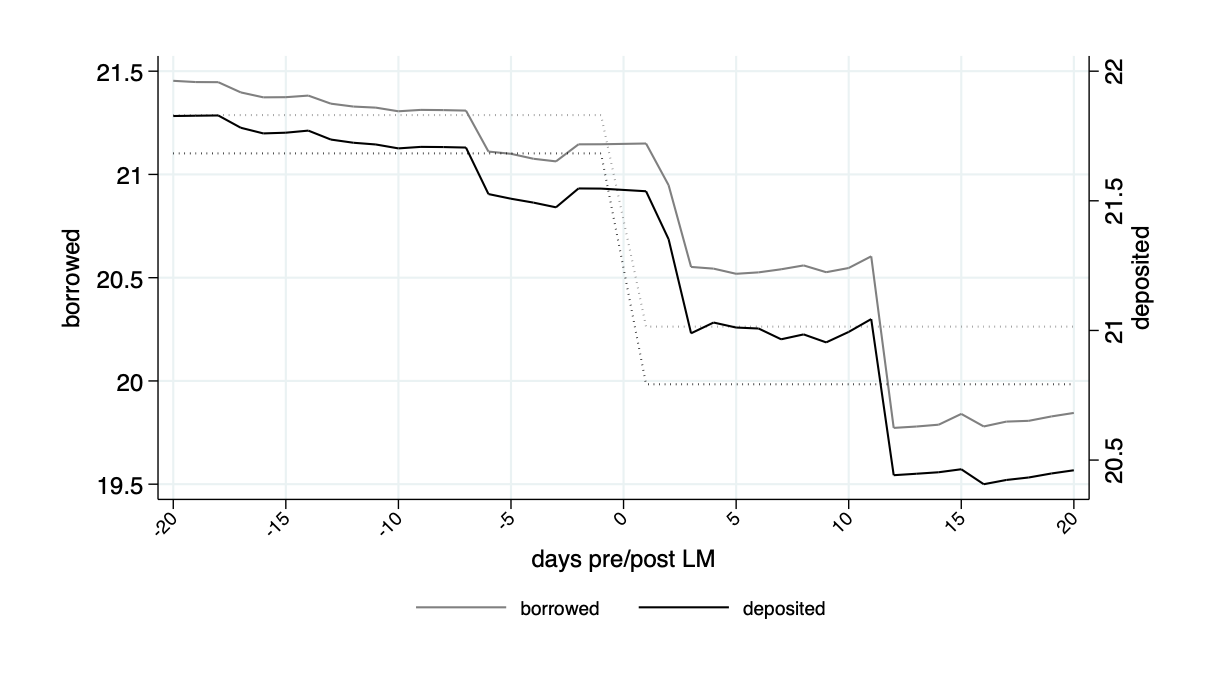

Application: Decentralized Borrowing & Lending

borrow

provide collateral

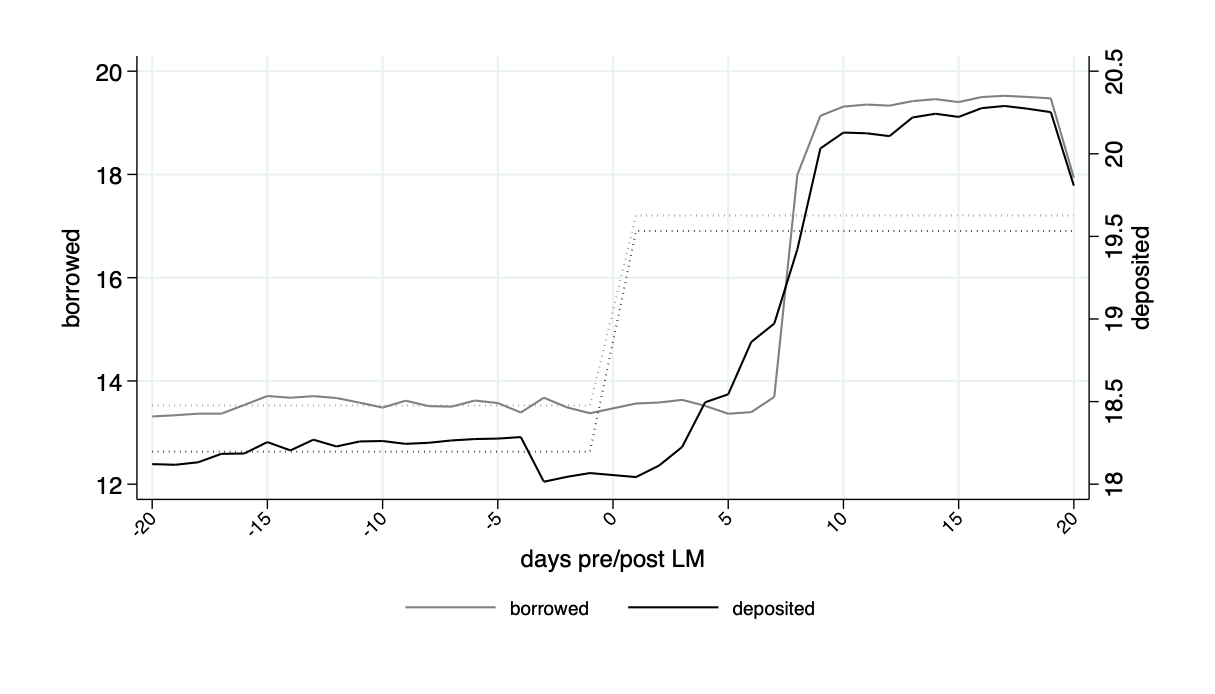

The Flow of Event: Normal Times

The Flow of Event: Collateral Liquidation

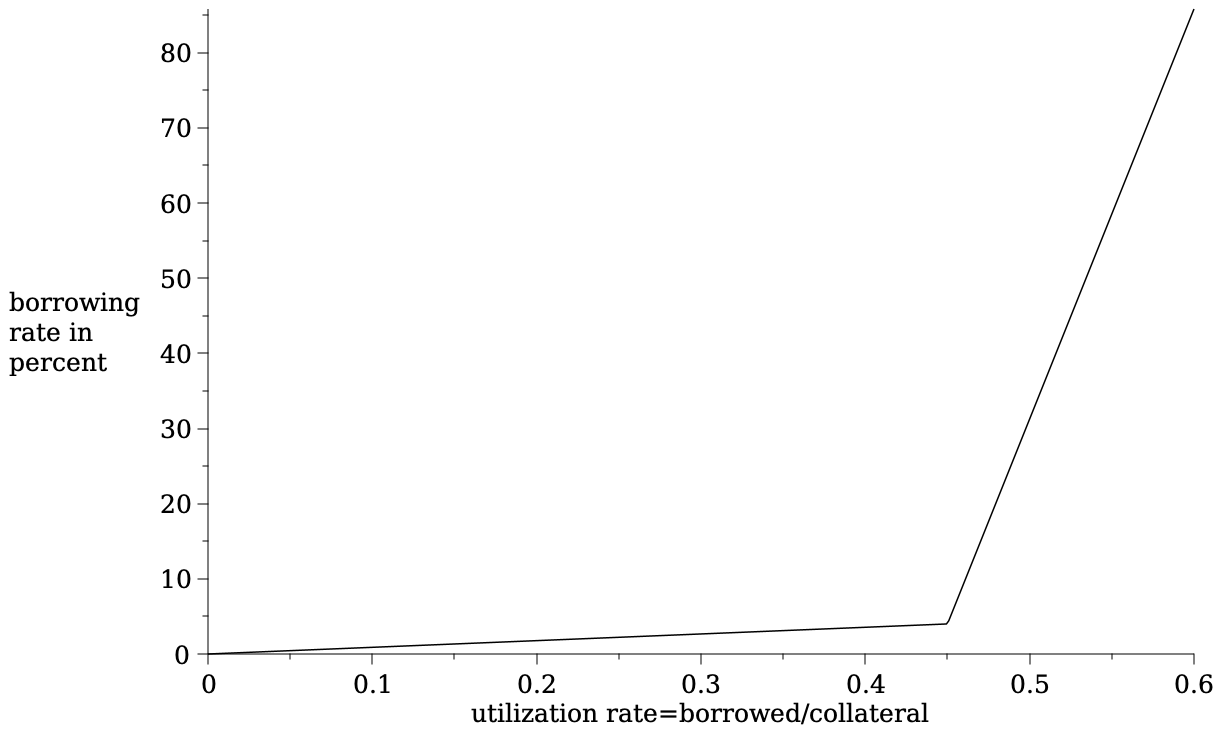

Interest rates: a function of pool usage

threshold usage rate

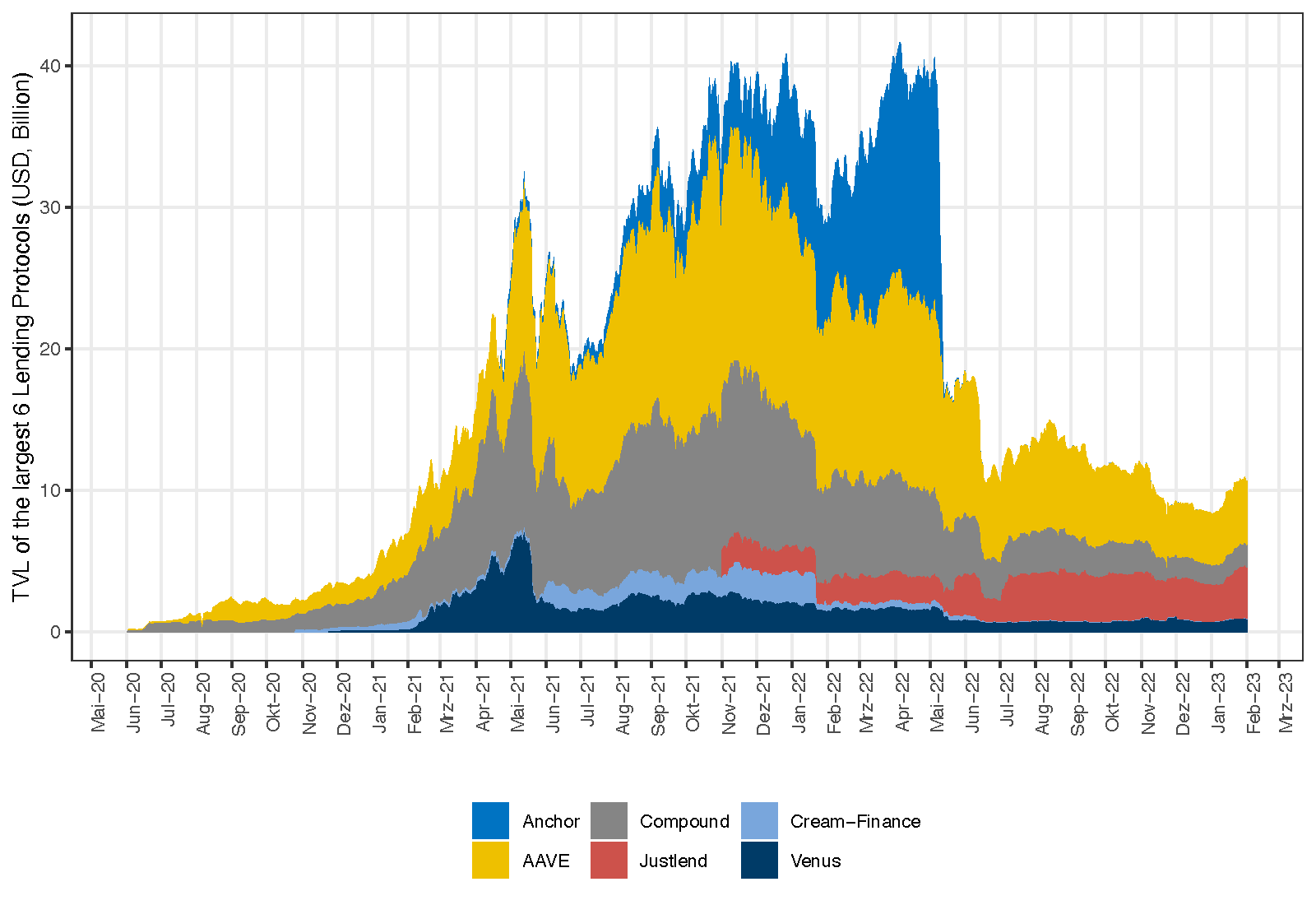

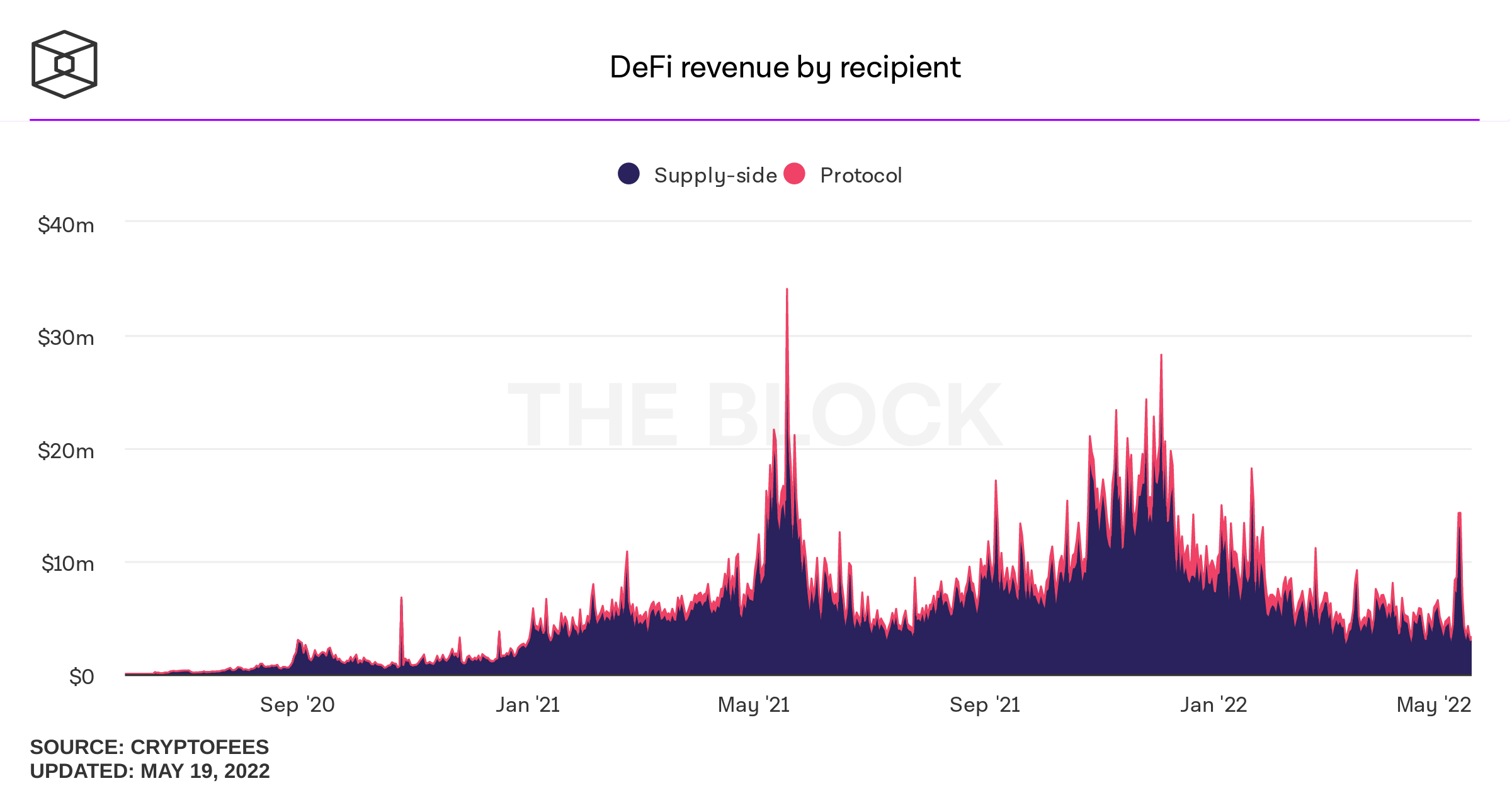

Some Data

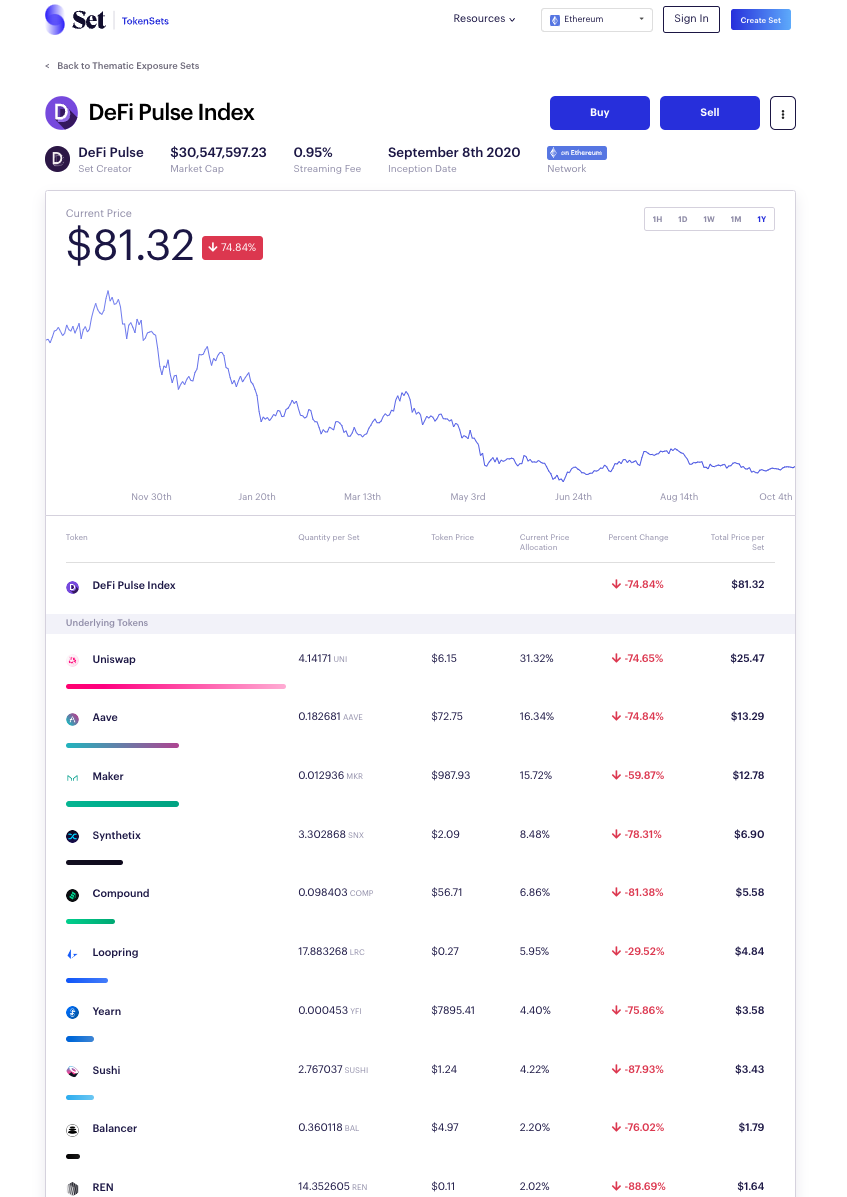

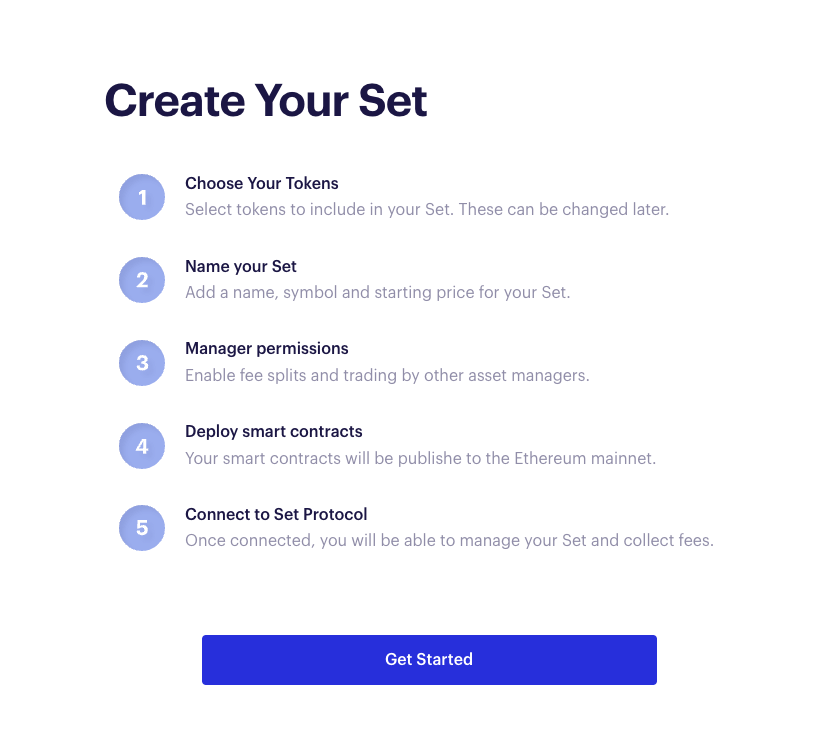

Securities Creation: Tokensets

idea: create new mutual fund like asset

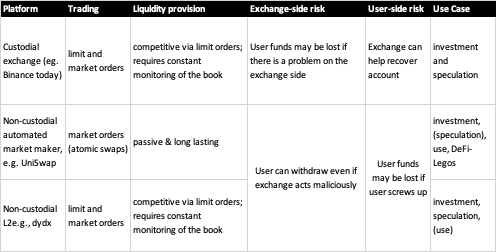

Platforms, Peer-to-Peer, and Decentralization

Philosophy of Peer-to-peer

Traditional Market

two-sided with fixed roles

Decentralized Market?

value management protocol \(\not=\) market

Peer-to-peer \(\Rightarrow\) Platforms

liquidity \(\nearrow\)

volume \(\nearrow\)

protocol fees \(\nearrow\)

token value \(\nearrow\)

Platform economics is tricky:

it works!

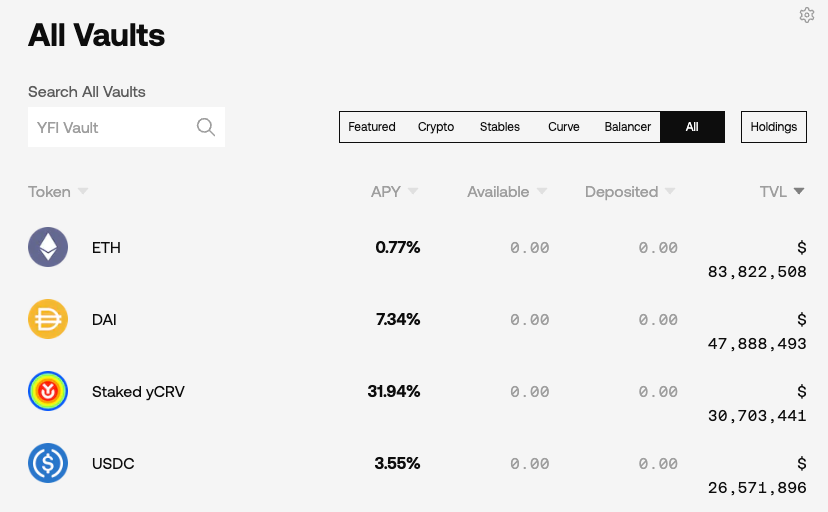

A Consequence of Liquidity Mining: Yield Aggregators

Idea:

UniSwap Lab supports development

a website app accesses the code

token holders control contact features

don't own the code

operation = decentral

control = decentral

anyone can use the baseline code

core code runs on the blockchain

tokens used as rewards

A Taxonomy of Tokens

What's a crypto-token and what's special about it?

Tokens by use

payments:

utility

stablecoins

governance

asset

derivatives

Disclaimer: this list in non-exhaustive, new ideas and concepts come up every day!

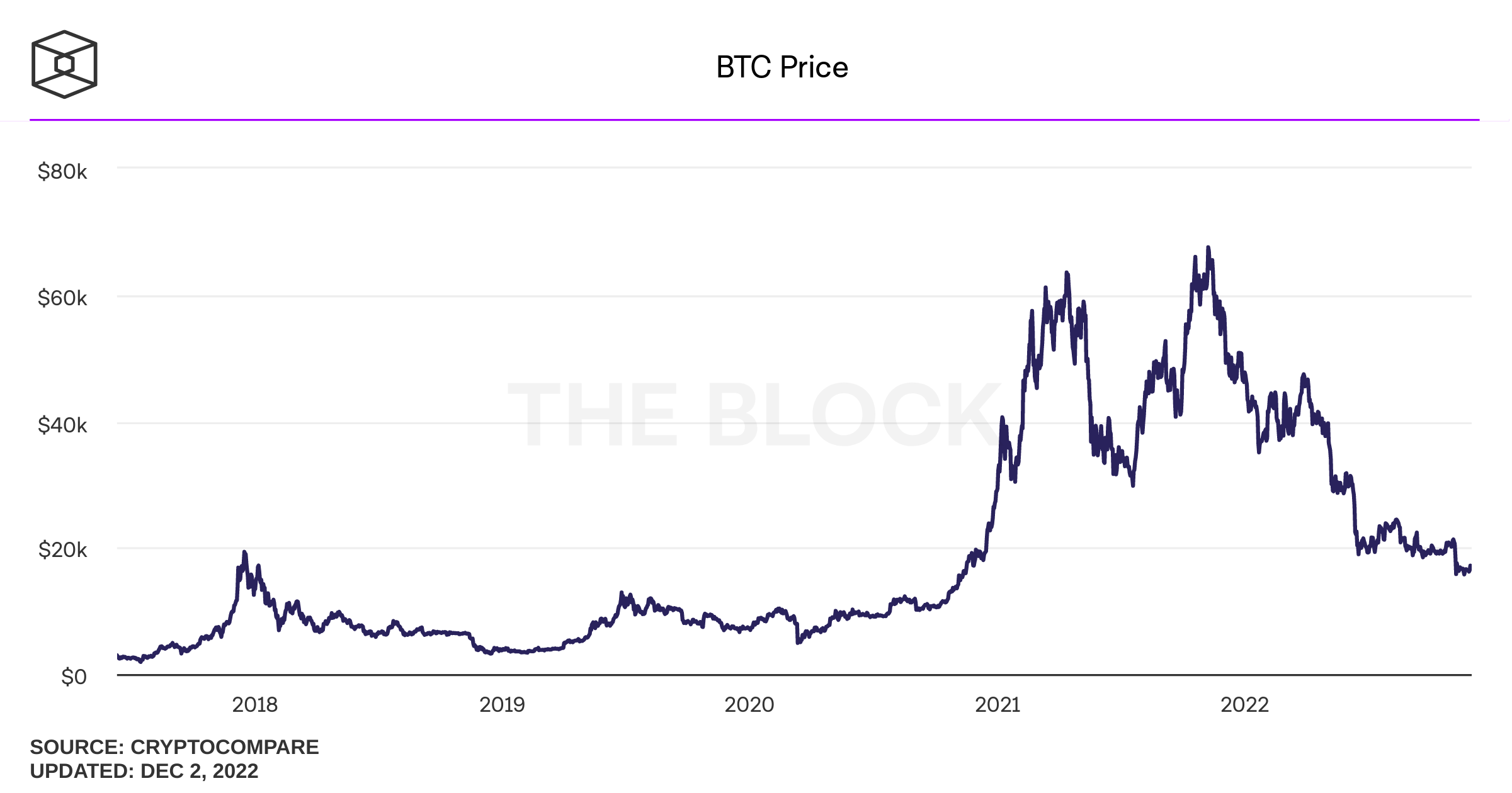

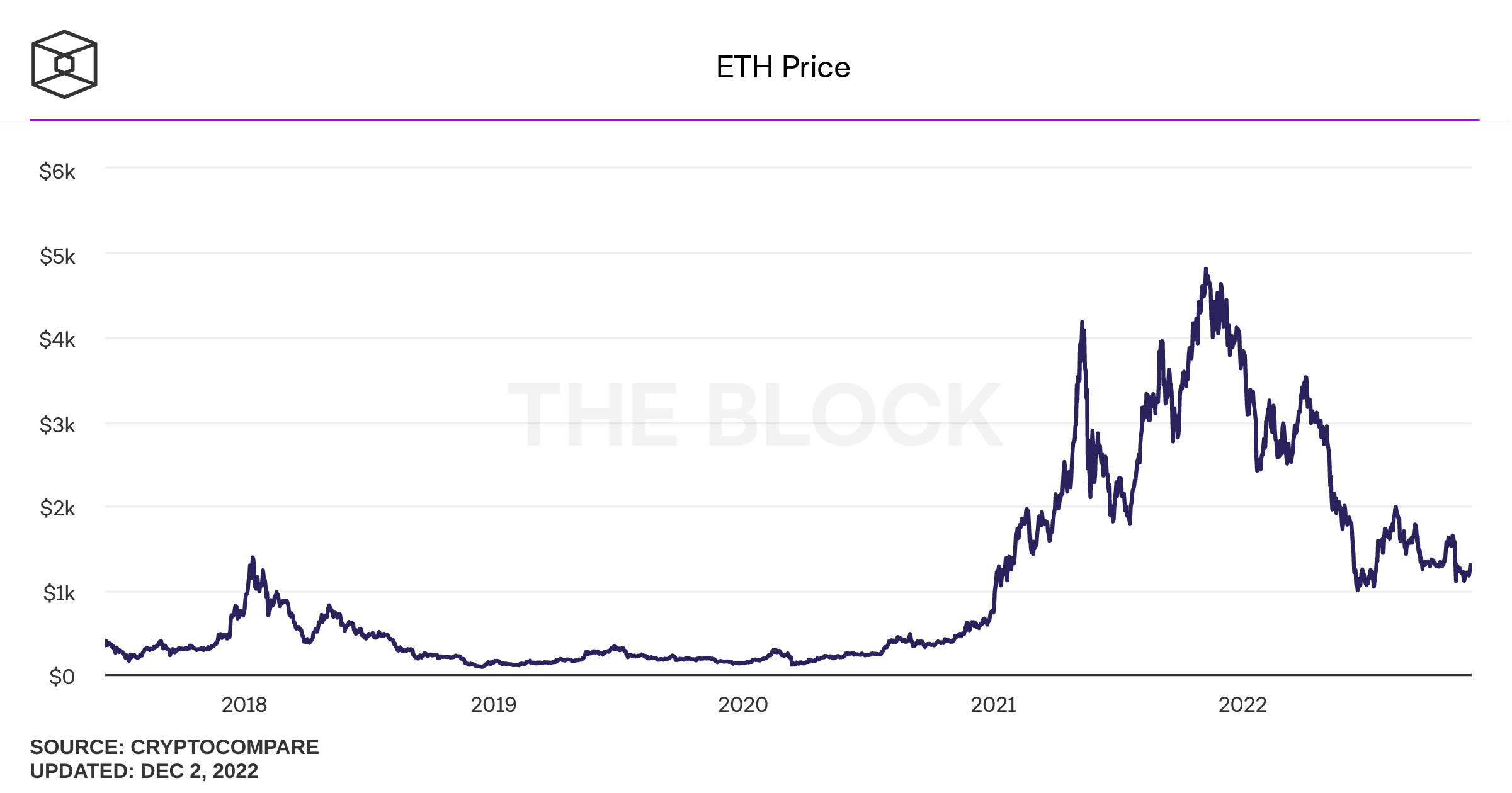

An ugly 9 months

From a slow slide to a thorough crash

-75%

-75%

!

The Terra Implosion

UST Stablecoin

LUNA (cryptocurrency of the TERRA network)

A timeline

May 7: selling pressure on UST from Curve withdrawals

May 12: LUNA and UST at $0.01

June 27: Three Arrows Capital ordered to liquidate

June 12: Celsius Network suspends withdrawals

July 13: Celsius files for Chapter 11

July 6: Voyager Digital files for Chapter 11

July 4: Vault suspends withdrawals

Three Arrows Capital lost >60% of value and faces numerous margin calls that they did not react to

partially "saved" by \(\ldots\) FTX

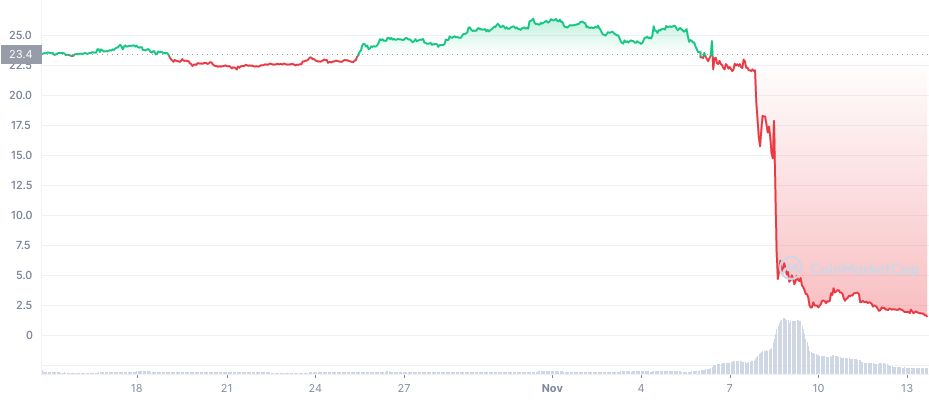

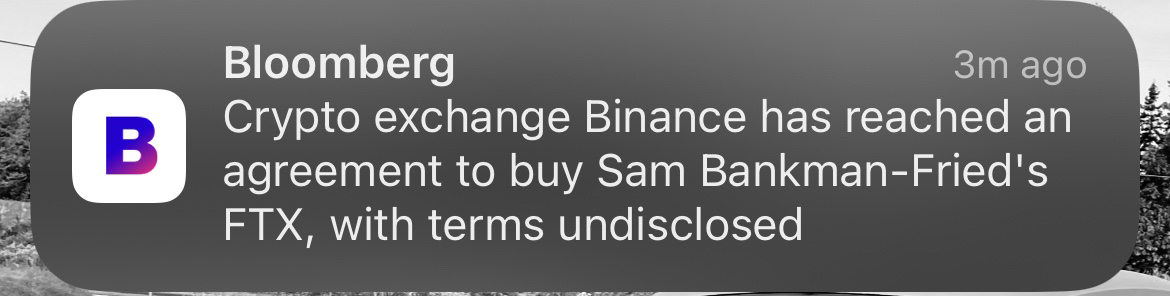

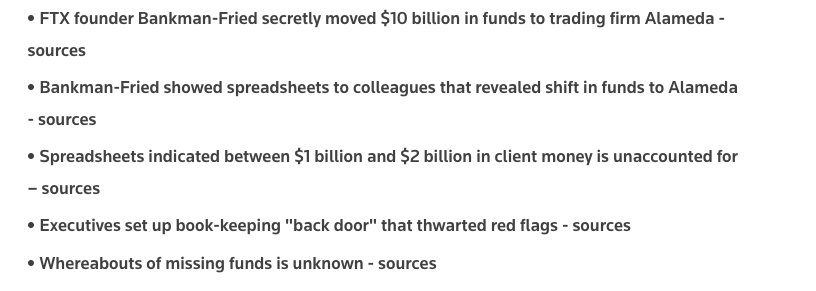

The FTX Implosion

A timeline

Nov 8

Fundamental Problems: Solution sans Regulators?

New trend: data providers check assets

Assets: cash in bank accounts and crypto assets in exchange wallets

Liabilities: customers' crypto and cash deposits

Proof of crypto assets

publish all exchange wallets

proof of control: shift assets from one address to another at a pre-determined time

Proof of crypto liabilities

public customer balances - customer can check

own holding

sum of all

Problem: privacy (adequate solutions exist)

Proof of Assets & Liabilities

A timeline

May 7: selling pressure on UST from Curve withdrawals

May 12: LUNA and UST at $0.01

June 27: Three Arrows Capital ordered to liquidate

June 12: Celsius Network suspends withdrawals

July 13: Celsius files for Chapter 11

July 6: Voyager Digital files for Chapter 11

July 4: Vault suspends withdrawals

Three Arrows Capital lost >60% of value and faces numerous margin calls that they did not react to

partially "saved" by \(\ldots\) FTX

all centralized!

Centralized vs Decentralized?

Why are Blockchains challenging for current regulation?

What is blockchain=crypto? Some basic facts

anyone can use it

a open, general-purpose

digital value management tool

that maintains digital scarcity

ownership & control is direct and not intermediated

it's a protocol, not a thing

it does not belong to anyone

practically impossible to prevent the creation of code

borderless and digital

does not require high tech, a laptop is enough

requires use of tokens

What is blockchain=crypto? Some basic facts

anyone can use it

a open, general-purpose

digital value management tool

that maintains digital scarcity

ownership & control is direct and not intermediated

it's a protocol, not a thing

it does not belong to anyone

practically impossible to prevent the creation of code

borderless and digital

does not require high tech, a laptop is enough

requires use of tokens

The Investment Process

issuers

investors

services

needed & provided

A general purpose value management infrastructure:

intermediaries

separate institutions

The blockchain reality:

new institutions

emerged that do all three

tokens are often not intended to be investments!

... and that brought us ...

Regulators' Focus

MiCA

current look: almost all branches of the US government work to make it "go away"

The Regulator's Dilemma

The Regulator's Dilemma

benign

crypto-assets

non-benign crypto-assets or crypto-assets that look like securities but are unregistered

crypto-assets that look like securities and are registered

crypto-assets that regulators feel comfortable to be traded on a platform under their supervision

The Regulator's Dilemma

The Reality of Markets

benign

crypto-assets

non-benign crypto-assets or crypto-assets that look like securities but are unregistered

crypto-assets that look like securities and are registered

crypto-assets that you feel comfortable to be traded on a platform under your supervision

The Dilemma

Final Thoughts

Some Final Thoughts

@financeUTM

andreas.park@rotman.utoronto.ca

slides.com/ap248

sites.google.com/site/parkandreas/

youtube.com/user/andreaspark2812/

Are Tokens Securities and What Safeguards Should There Be?

Provocative Thoughts

- End of Theory -

Some Developments

seller

buyer

What is a Blockchain?

The Premise of the

Internet & Blockchain

Peer to Peer Communication

Peer to Peer Value

!

?

?

Sidebar: What is digitize-able value?

The challenge: how do you ensure digital scarcity?

By Andreas Park