Andreas Park PRO

Professor of Finance at UofT

From Ravina, Enricetta. 2018. “Love & Loans: The Effect of Beauty and Personal Characteristics in Credit Markets.” Working Paper

price for loan

effort required to get loan

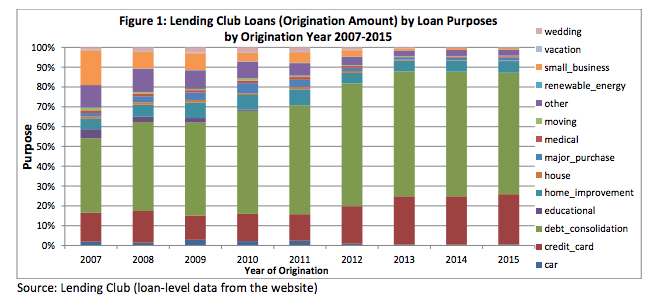

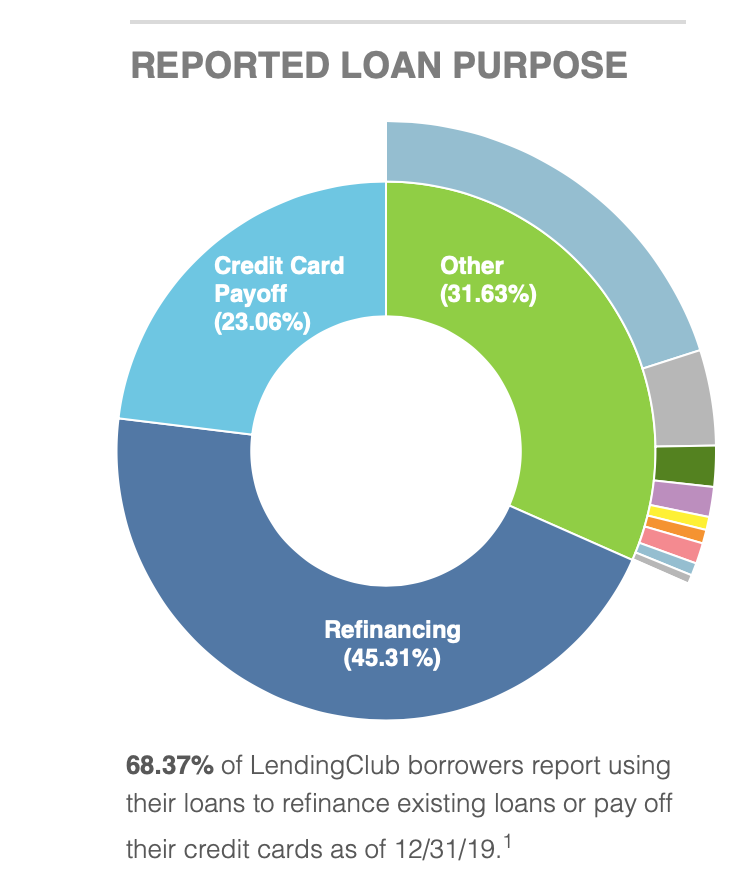

What do people use the online lenders for?

Source: Jagtiani & Lemieux, 2017, Philly Fed Working Paper 17-17

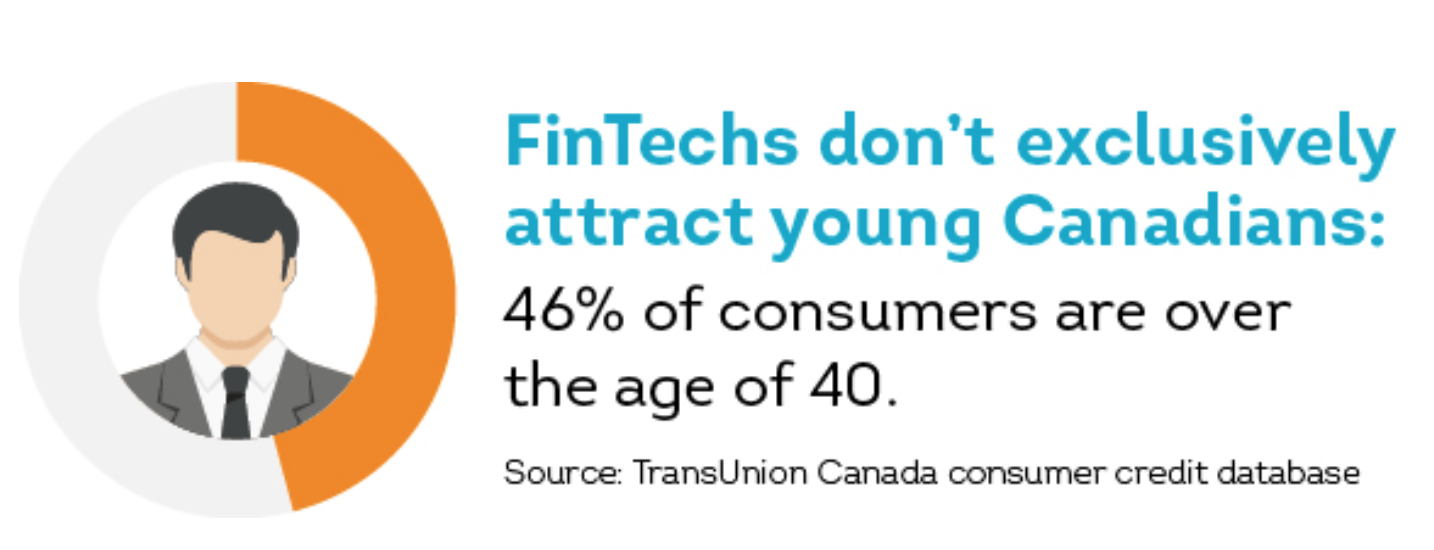

Who uses FinTech lenders? (Canada)

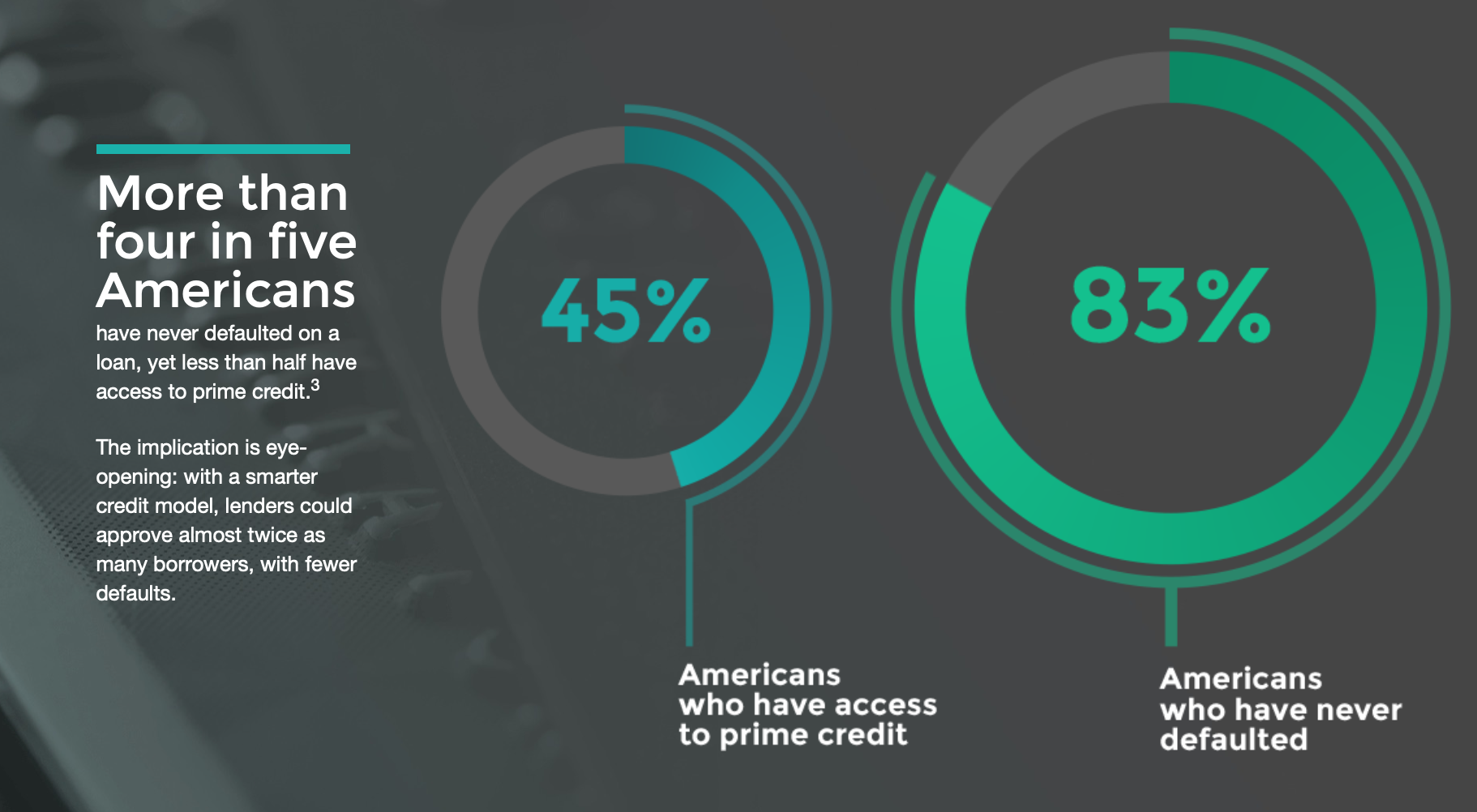

compared to 53% for consumers with personal loans from traditional banks

NB: this data/picture is a few years old. At the time, people under 40 were "millennials"

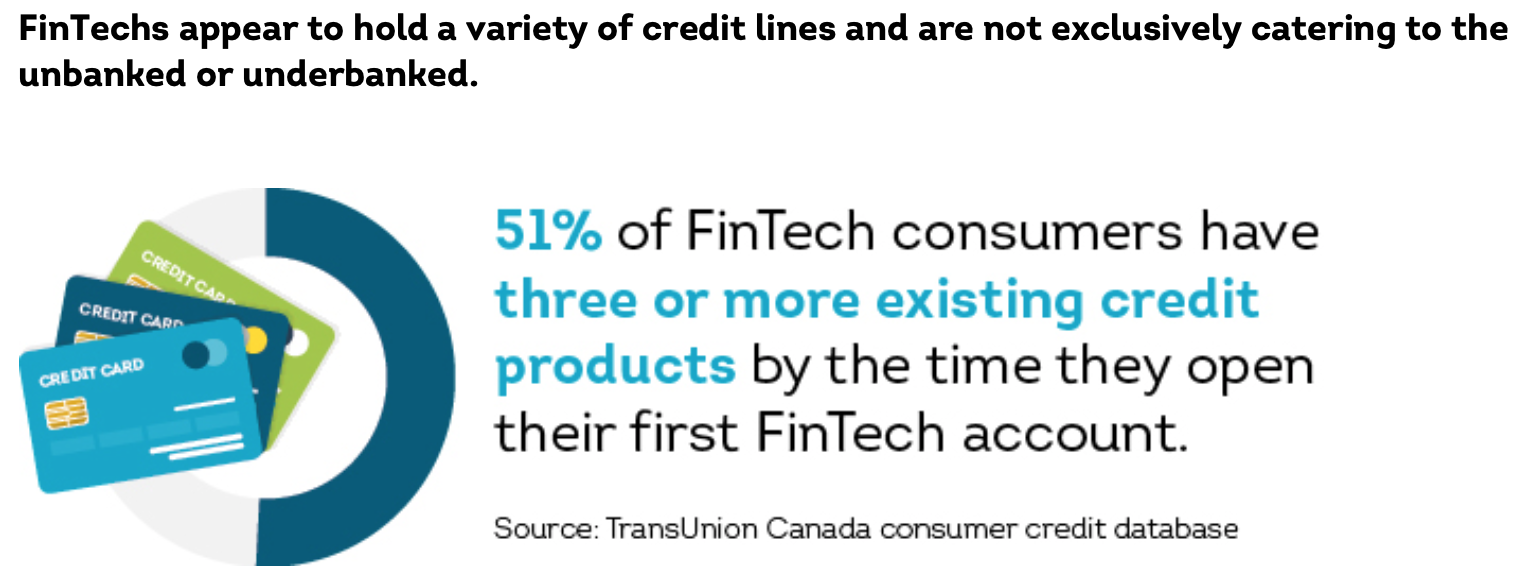

Who uses FinTech lenders? (Canada)

Canadian Bankers Association:

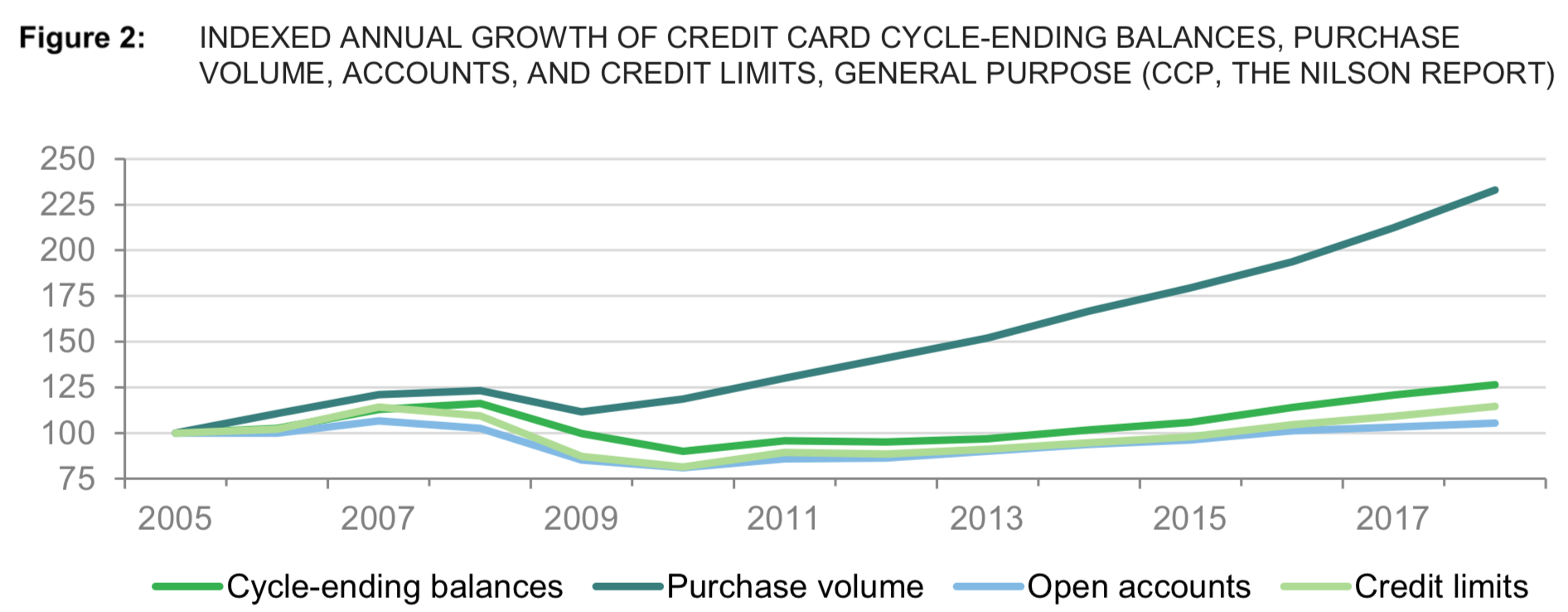

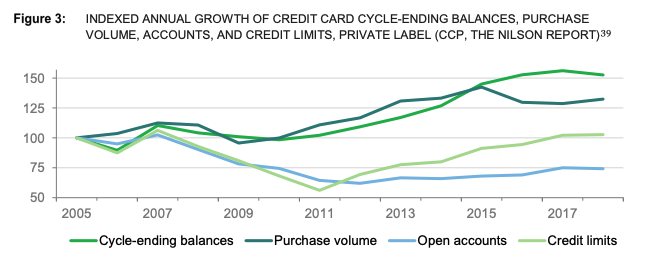

small caveat: high balances for "private label" cards (e.g., store cards)

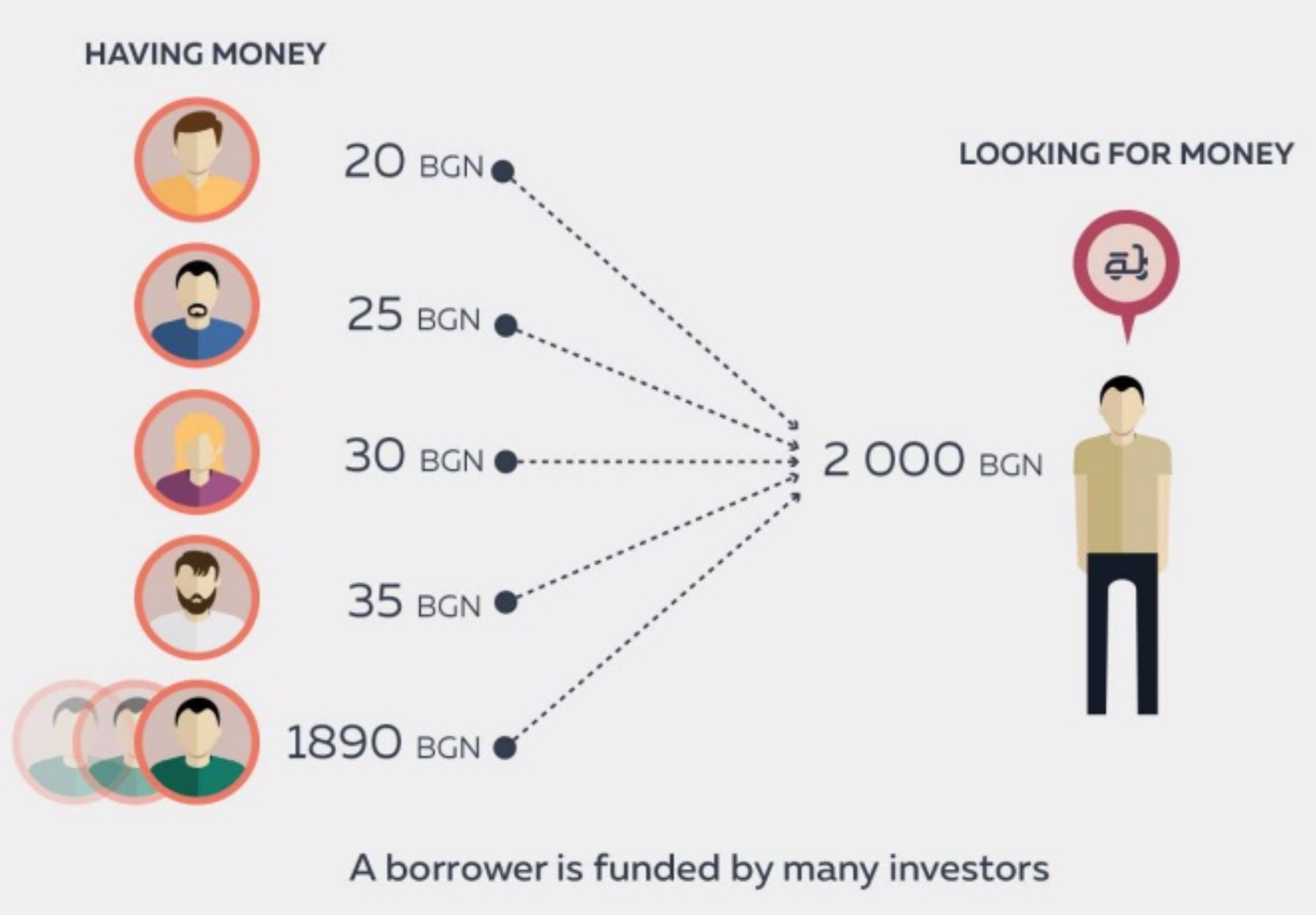

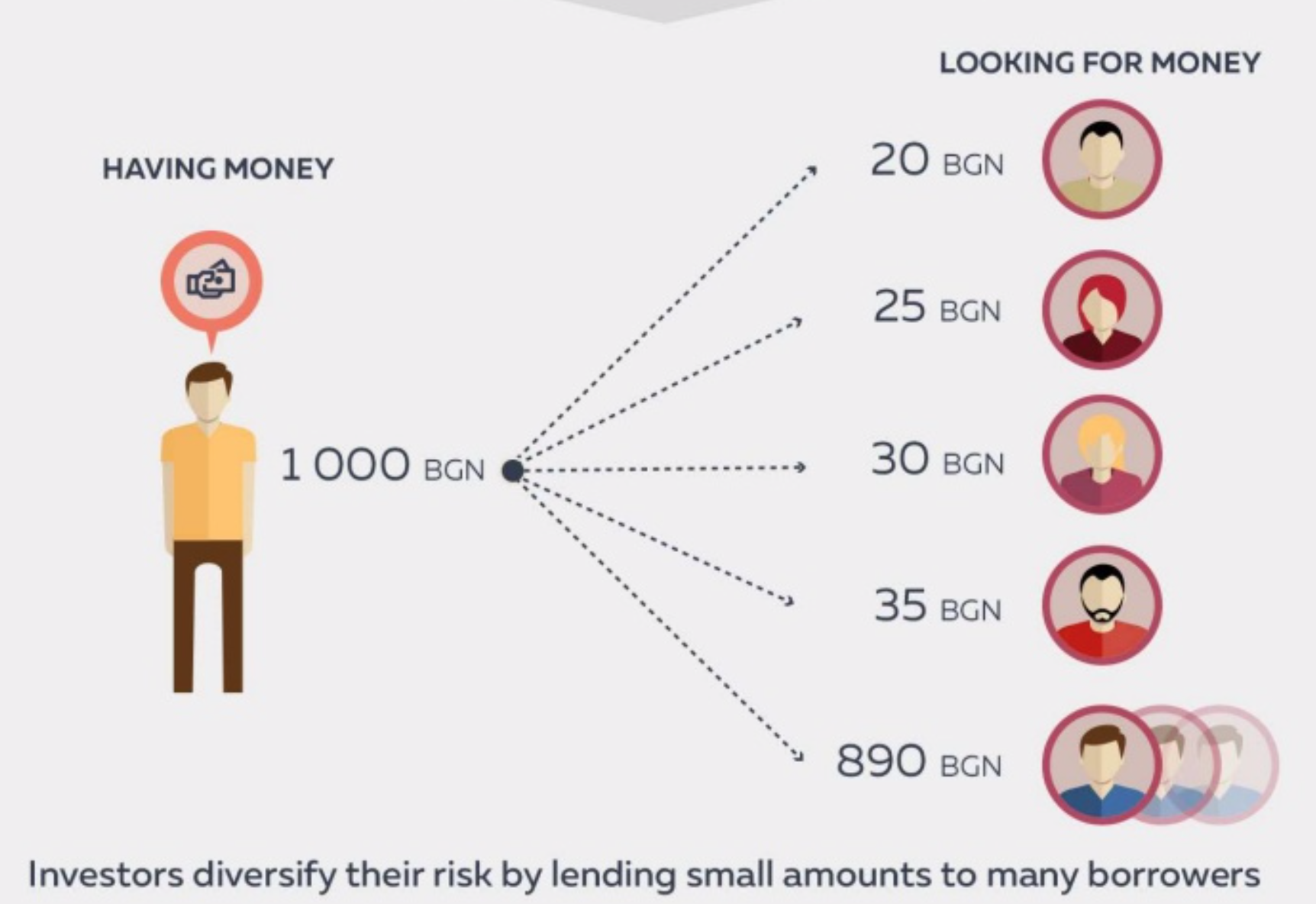

basic portfolio math

All students within a cohort get the same interest rate.

\(\to\) Find the graduates that do well & "cream-skim"!

*

*HELOC=home equity line of credit

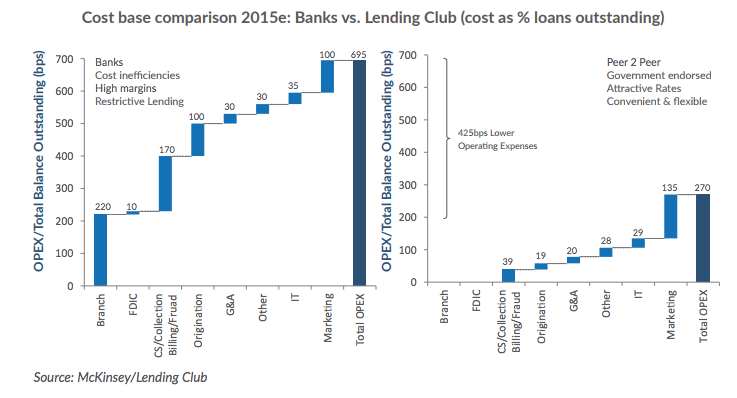

425bps!

G&A=general administrative expenses

OPEX=operational expenditures

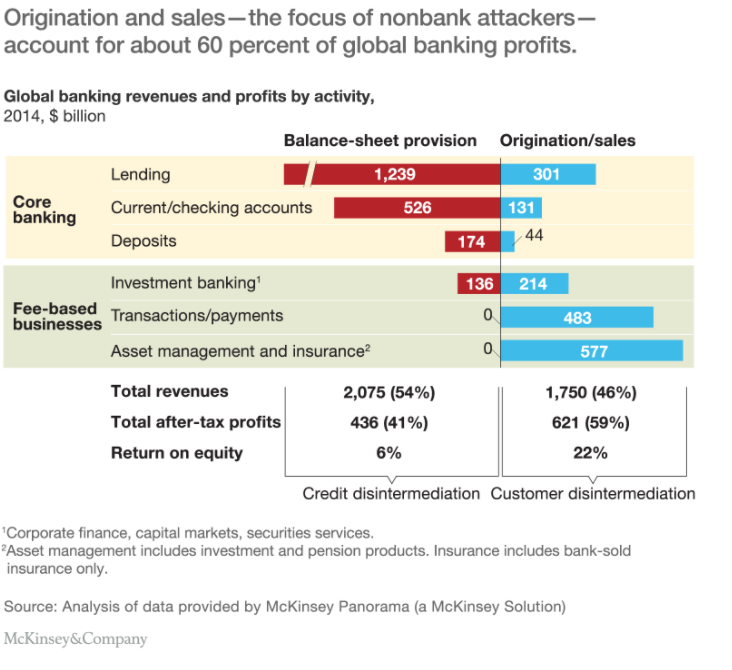

McKinsey: 59% of the banks’ earnings flow from pure fee products as well as the origination, sales, and distribution

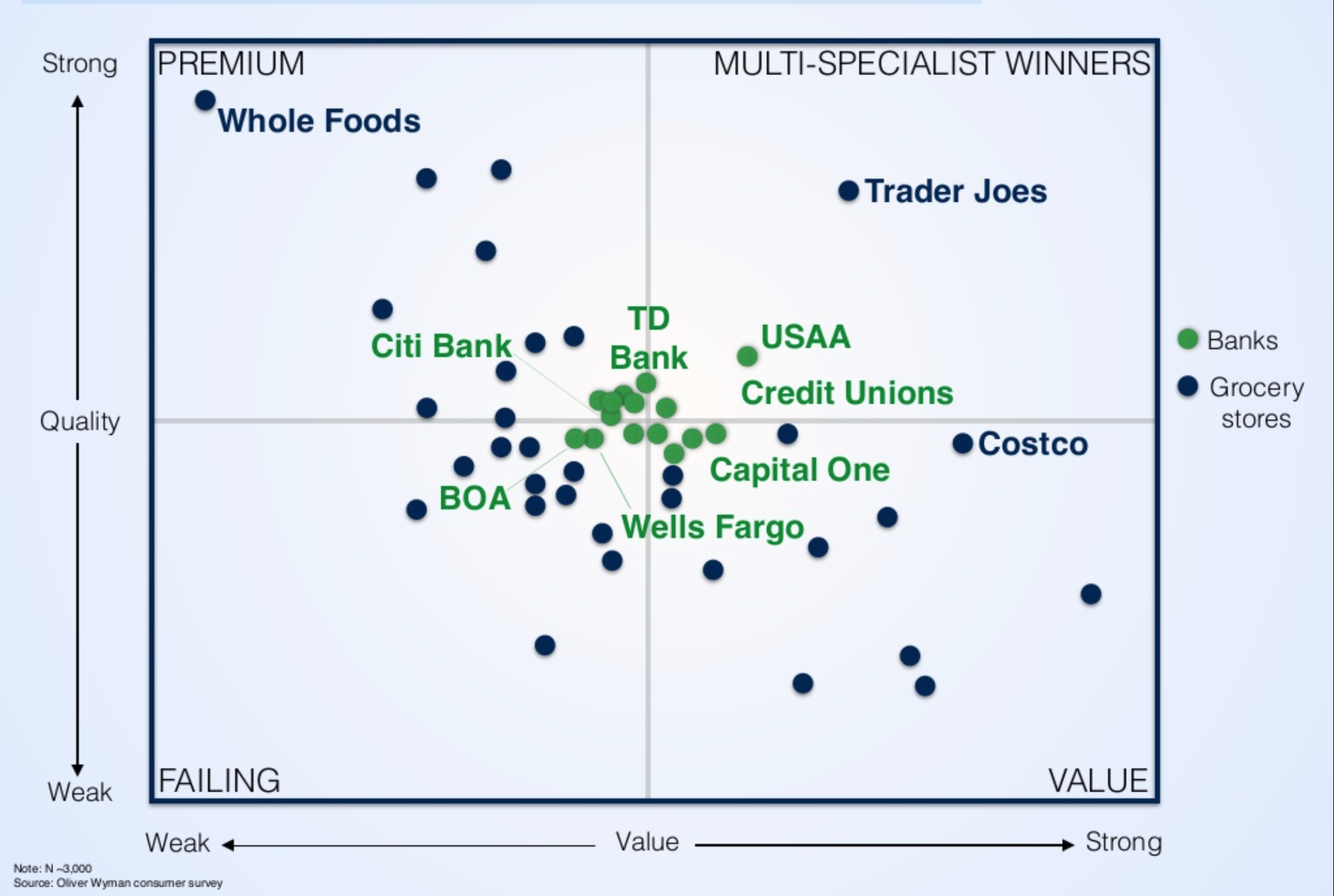

Costs aside, there is very limited differentiation among banks!

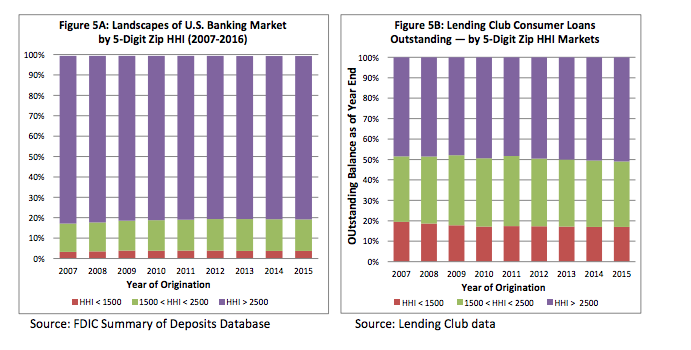

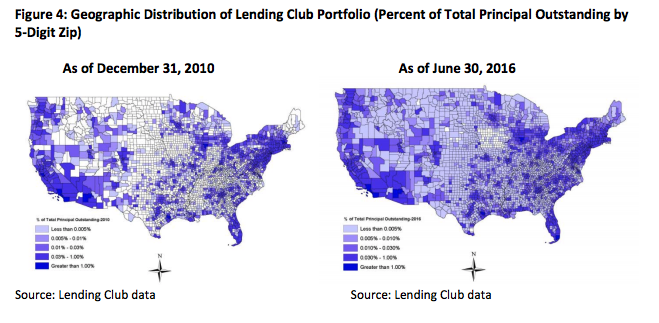

Lending Club filled a niche: went to ZIP codes where competition was low!

Source: Jagtiani & Lemieux, 2017, Philly Fed Working Paper 17-17

Critically: they did scale up!

Source: Jagtiani & Lemieux, 2017, Philly Fed Working Paper 17-17

TransUnion study in Canada:

TransUnion study in Canada:

https://www.transunion.ca/blog/fintechs-in-canada

Word of caution: I haven't been able to find the study (released Feb 25, 2020). Take the TransUnion blog conclusion with a grain of salt.

(Many FinTechs do their own credit scoring!)

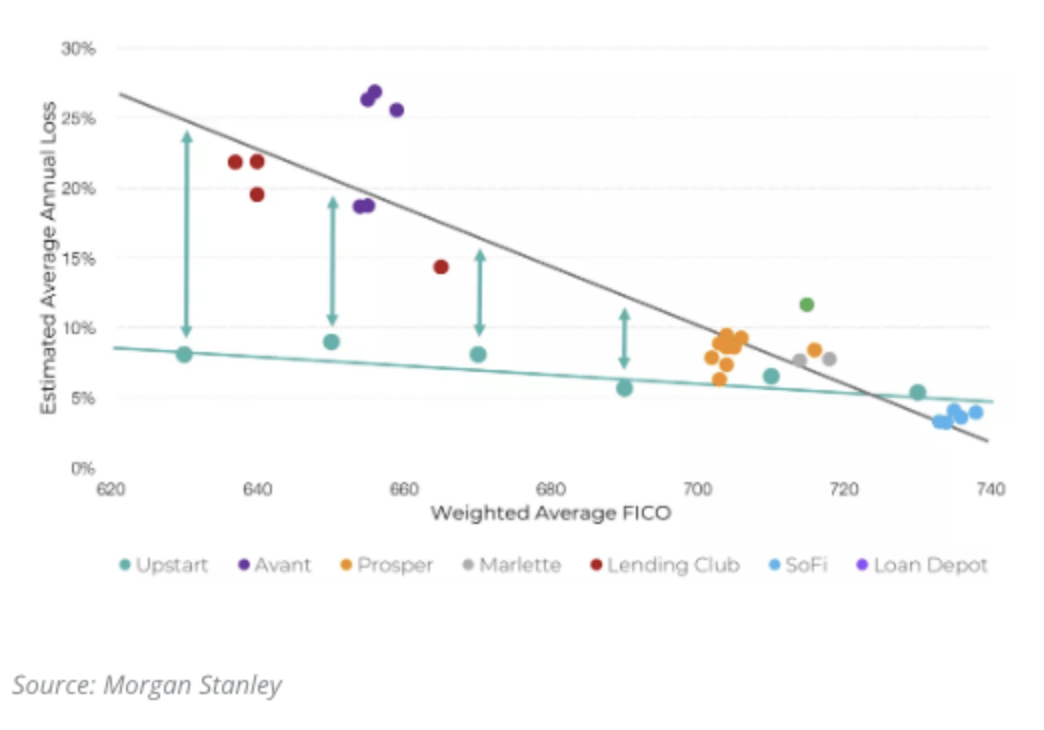

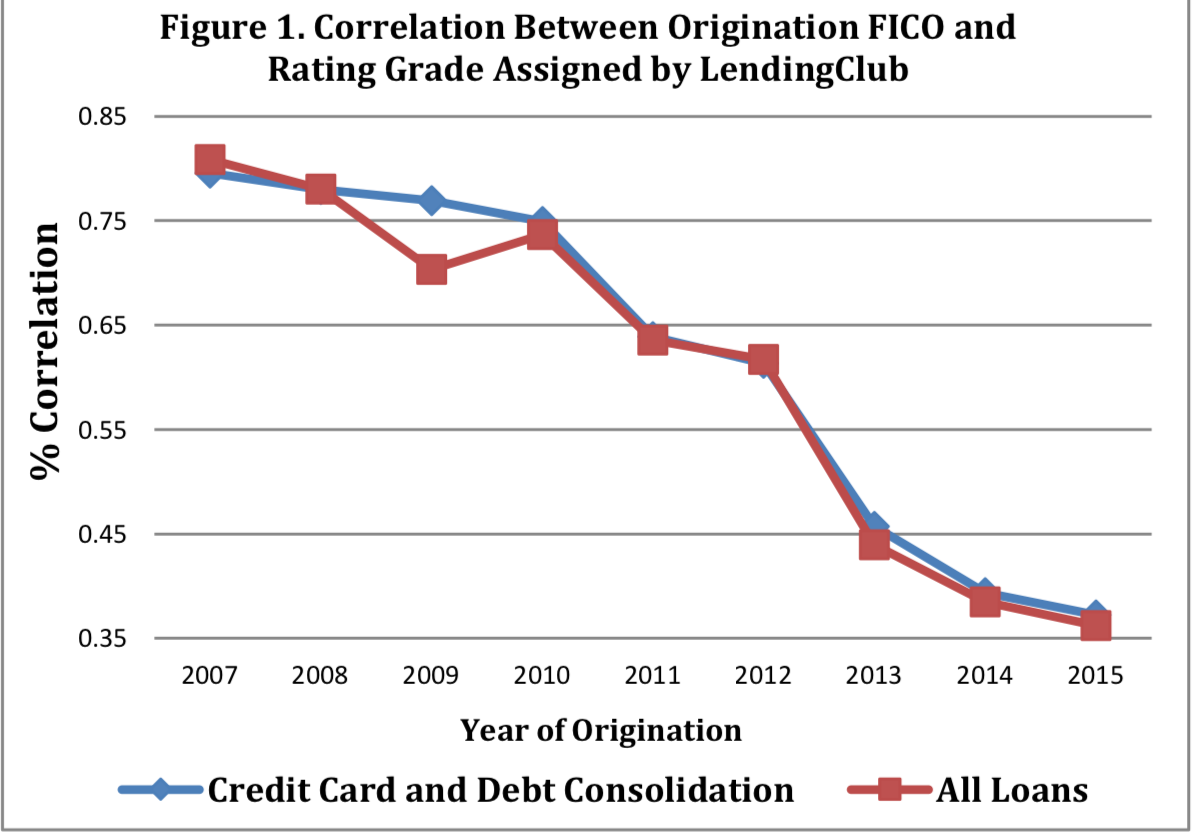

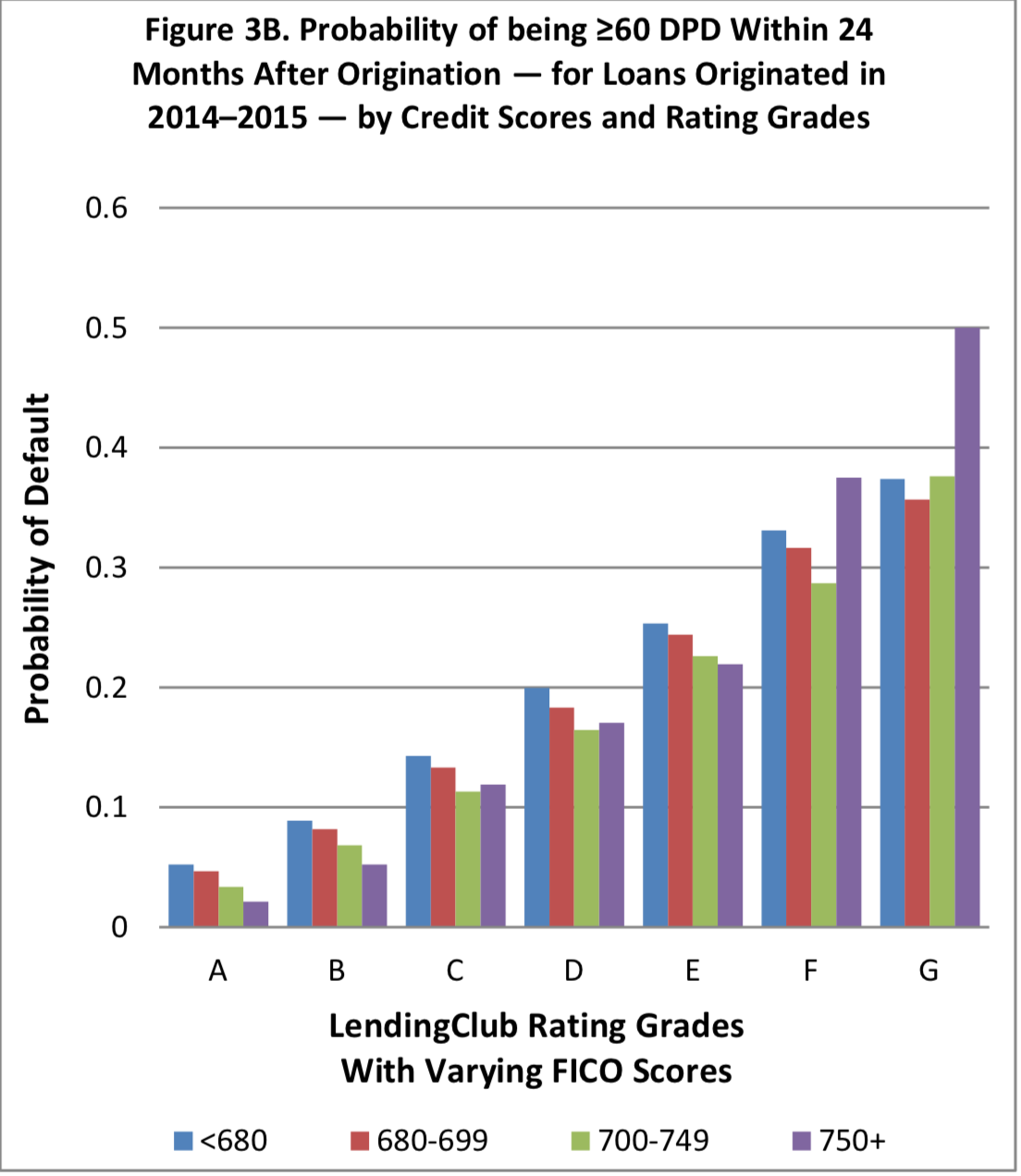

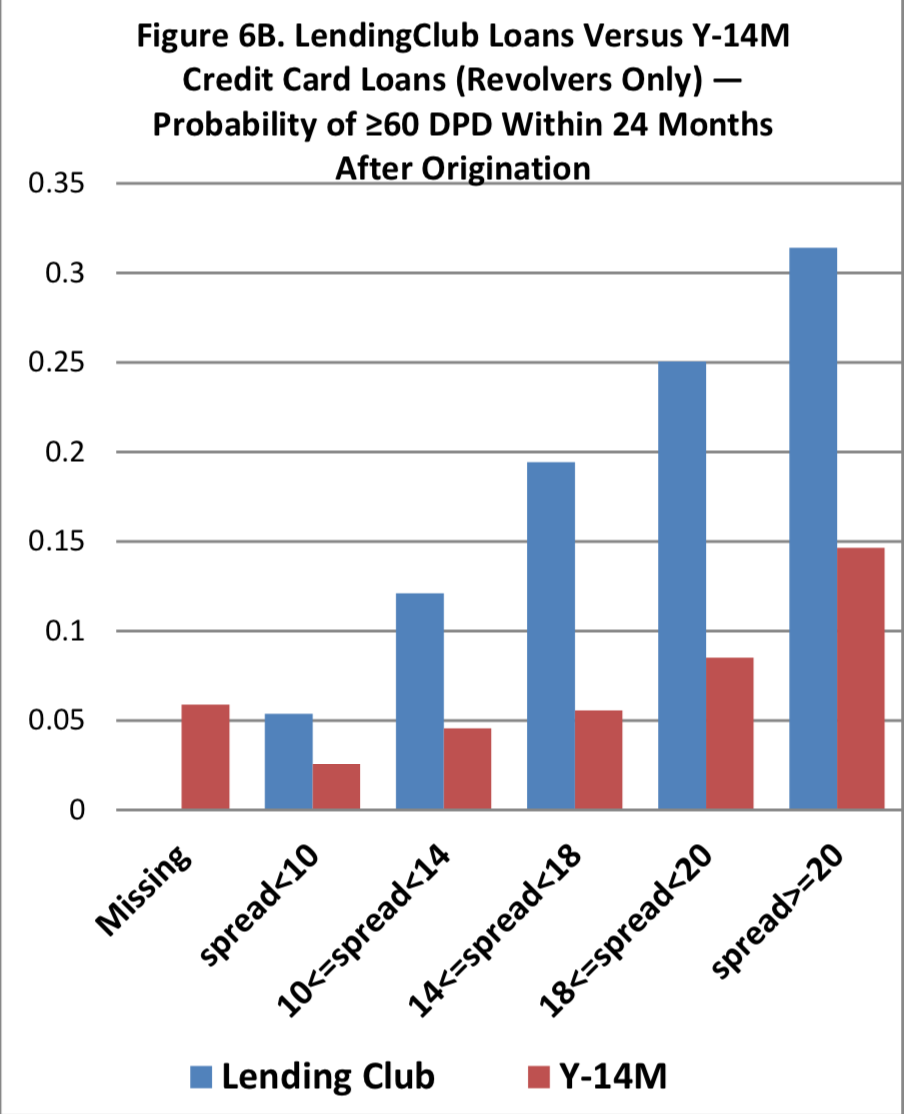

[Lending Club's] model attempts to identify applicants with FICO scores that do not reflect their true credit quality, and thus the risk could have been mispriced based on FICO scores alone.

Source: Jagtiani & Lemieux, 2017, Philly Fed Working Paper 17-17

(Upstart’s Paul Gu)

FinTech lenders: Better data and better techniques

Old days:

"FinTech lenders use technology to obtain new kinds of data that can make lending decisions more efficient and informed."

Goldstein, I., J. Jagtiani, and A. Klein. 2019. “Fintech and the New Financial Landscape.” Bank Policy Institute (BPI): Banking Perspectives, Q1:7, March 2019.

Flavour of the month: text-based analysis

Berg, T., V. Burg, A. Gombovic, and M. Puri. Year? “On the Rise of Fintech — Credit Scoring Using Digital Footprints.” Working Paper:

email contains their real name

make purchases at night time

number of typing mistakes

even the simple, easily accessible digital footprint variables as good as the Equifax Risk Score in predicting loan outcomes.

together with the Equifax Risk Score \(\nearrow\) model’s predictive power

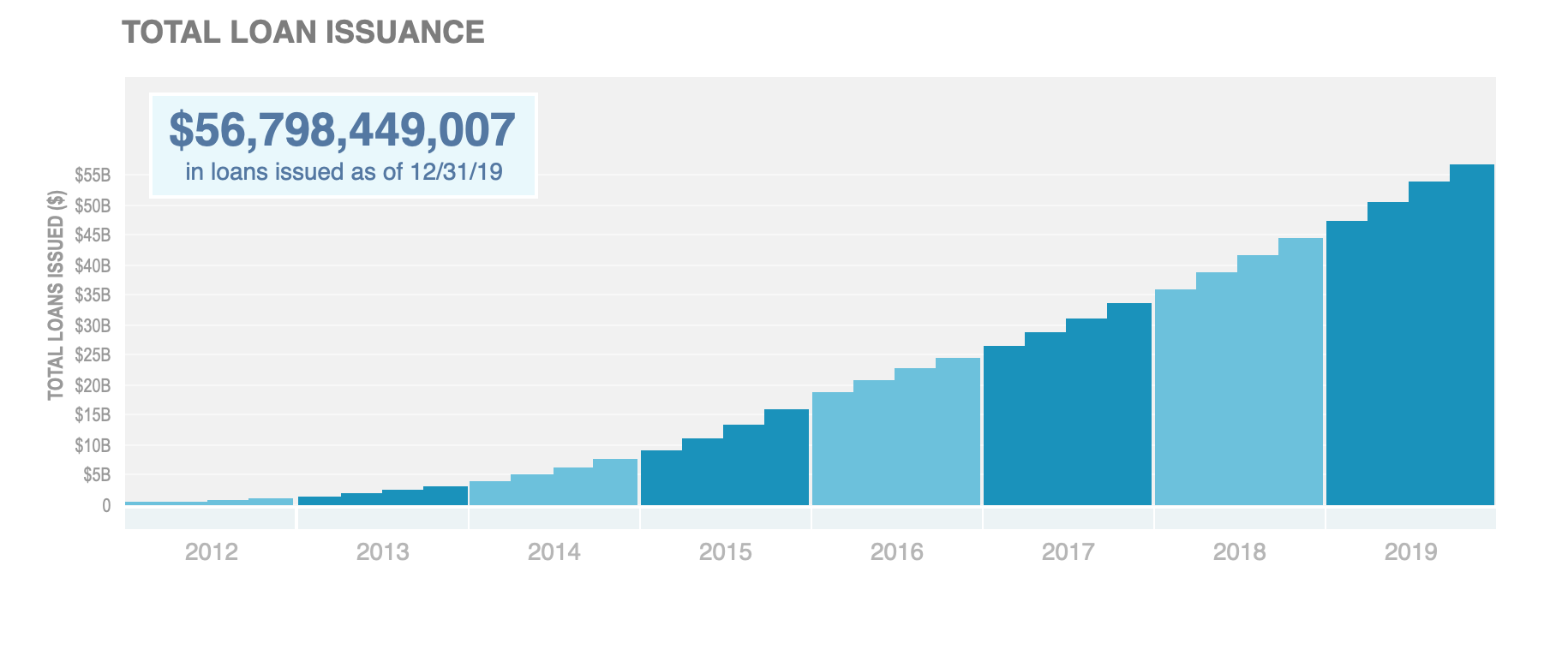

Lending Club: steady growth of loans!

What are key components to their success?

quick note: Lending Club posts a ton of data on its website \(\to\) that's why there is a lot of research on it

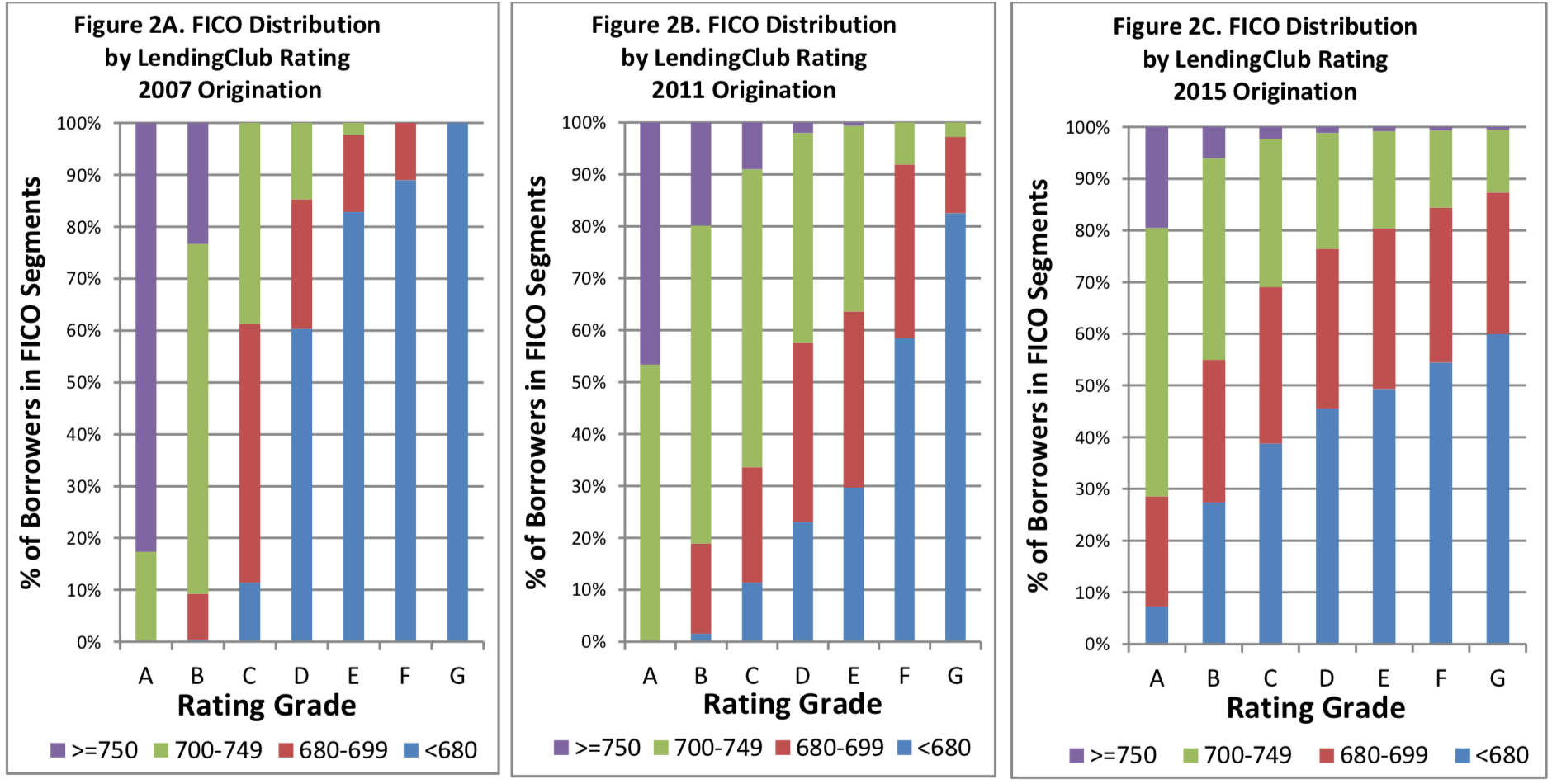

Source: Jagtiani & Lemieux, 2017, Philly Fed Working Paper 17-17

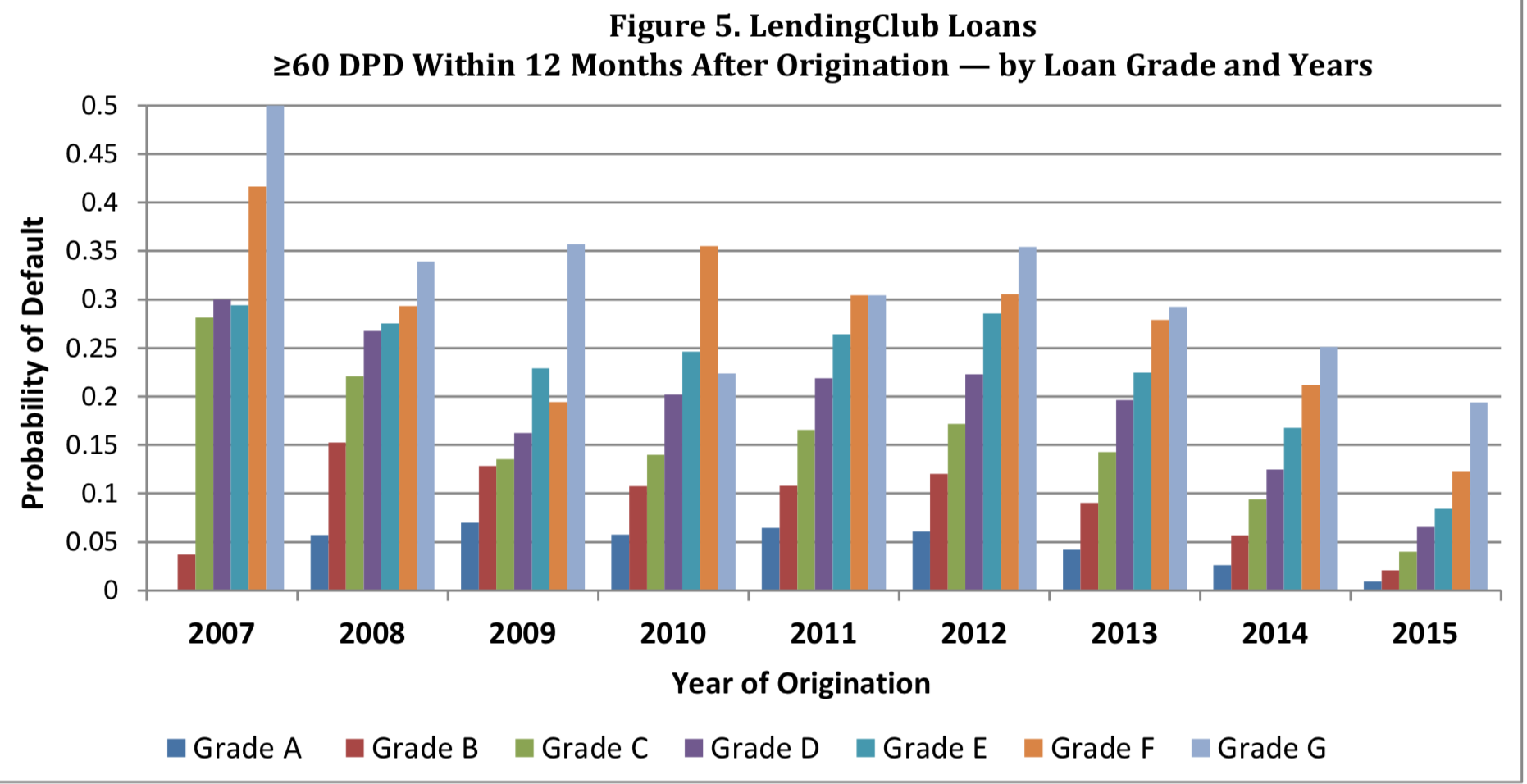

\(\Rightarrow\) They learn!

Source: Jagtiani & Lemieux, 2017, Philly Fed Working Paper 17-17

Source: Jagtiani & Lemieux, 2017, Philly Fed Working Paper 17-17

Source: Jagtiani & Lemieux, 2017, Philly Fed Working Paper 17-17

Source: Jagtiani & Lemieux, 2017, Philly Fed Working Paper 17-17

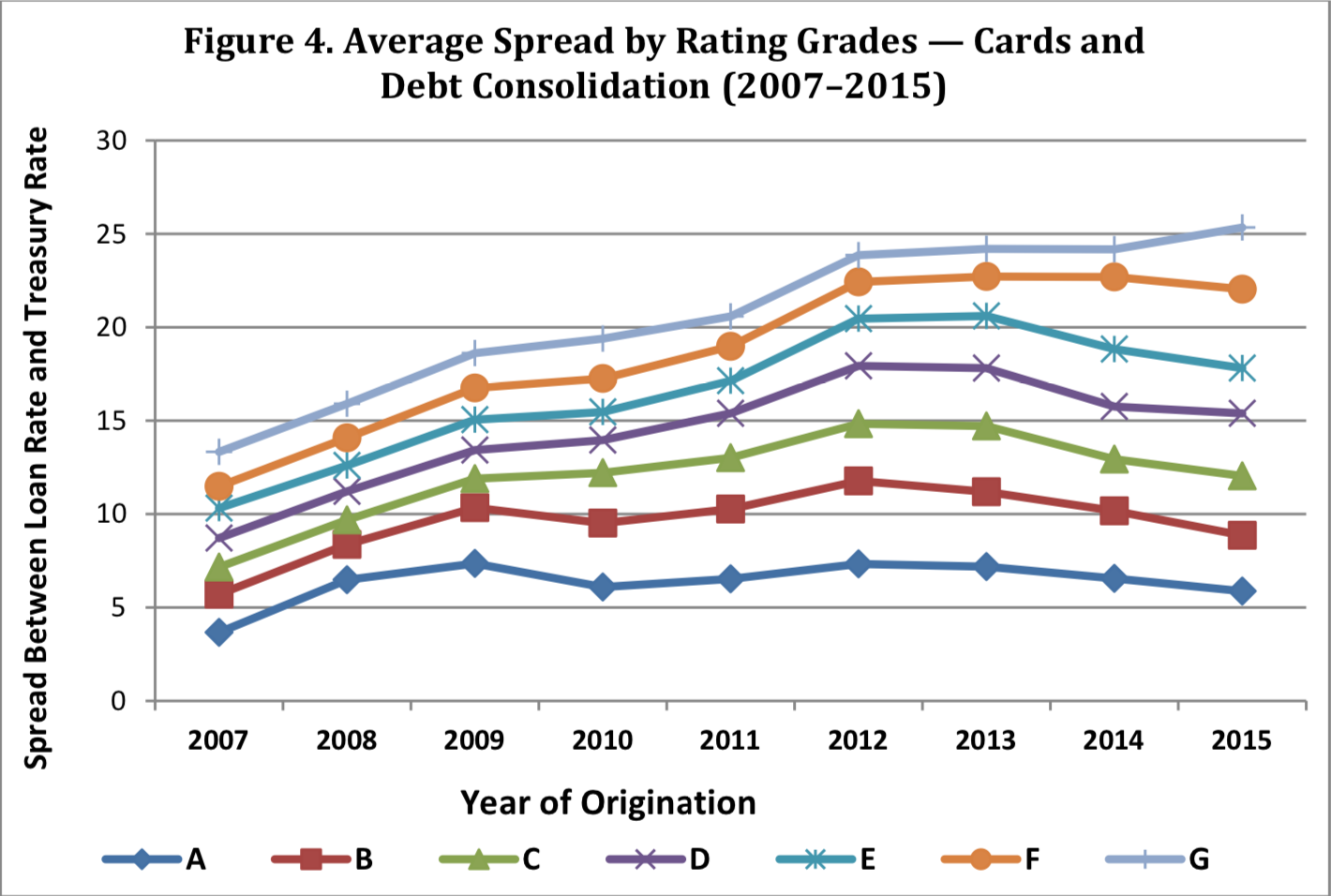

The results show that given the same credit risk (i.e., for borrowers with the same expected delinquency rate), consumers would be able to obtain credit at a lower rate through the Lending Club than through traditional credit card loans offered by banks.

Source: Jagtiani & Lemieux, 2017, Philly Fed Working Paper 17-17

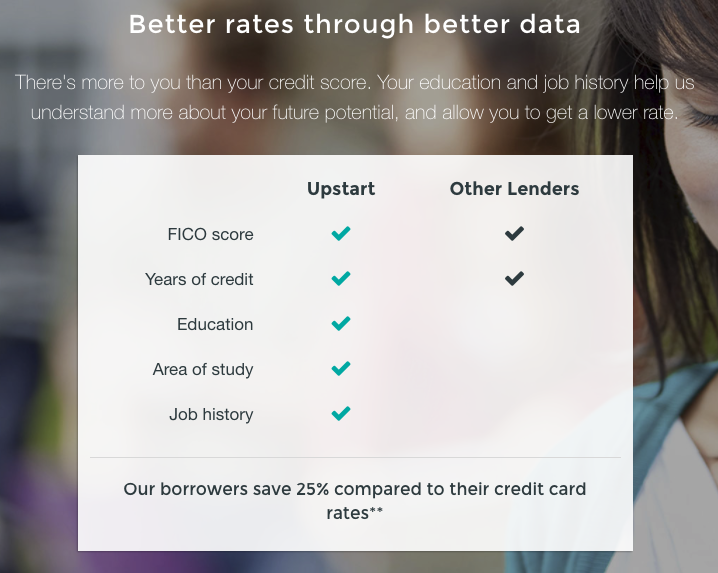

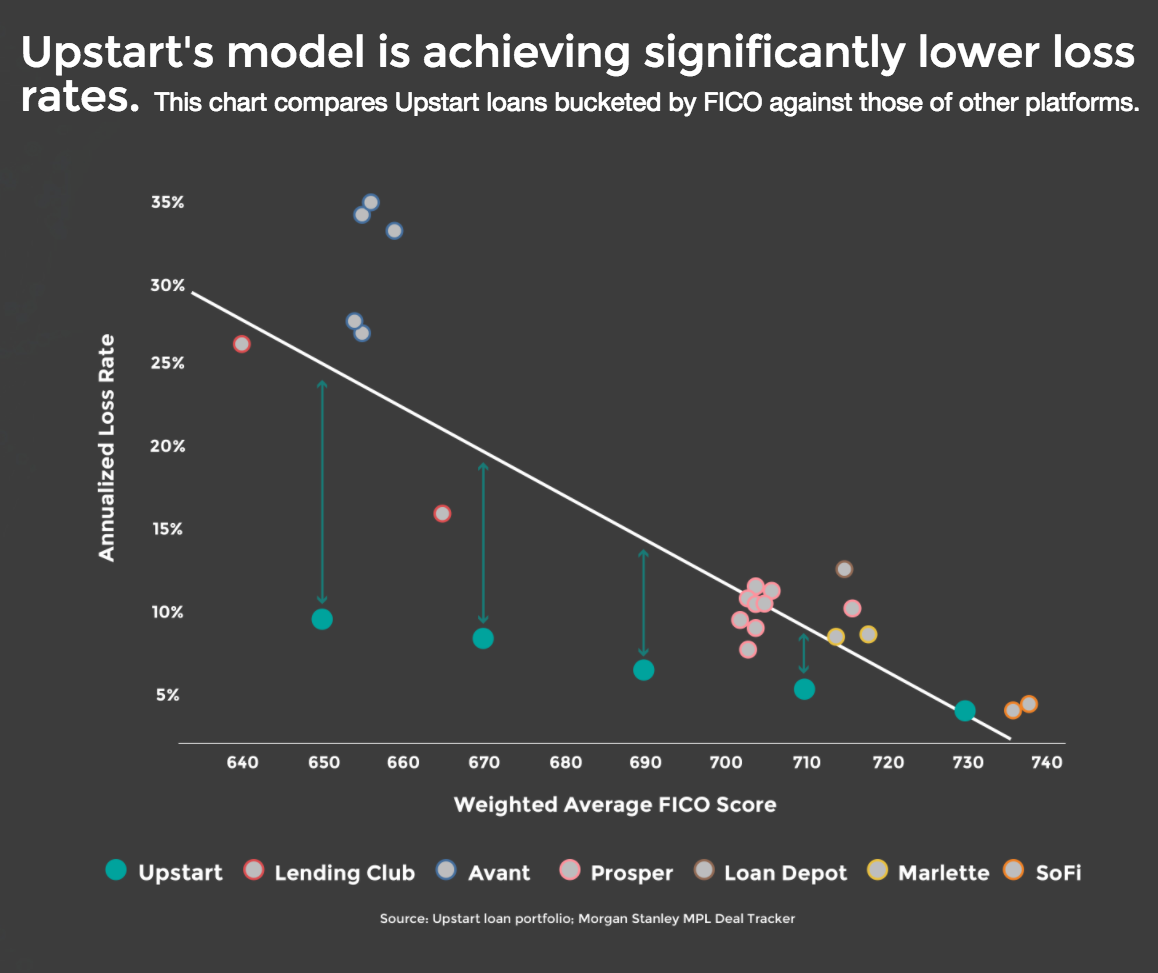

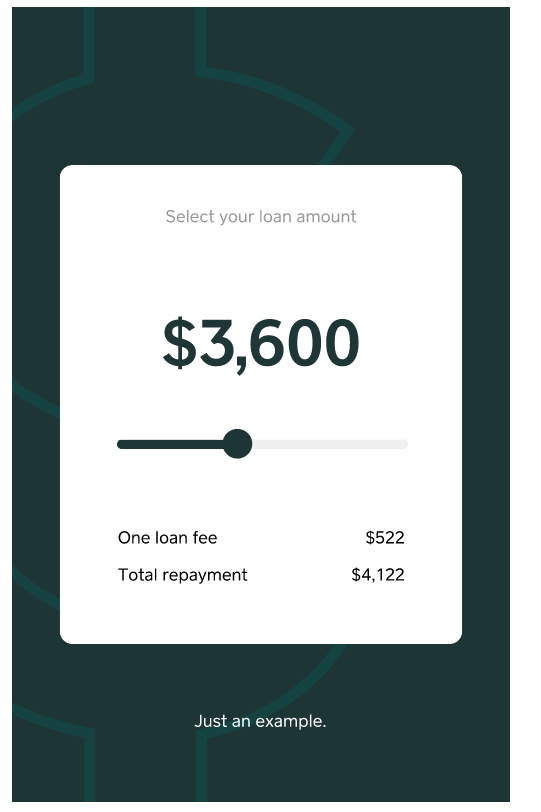

https://www.upstart.com/about#credit-limits-2

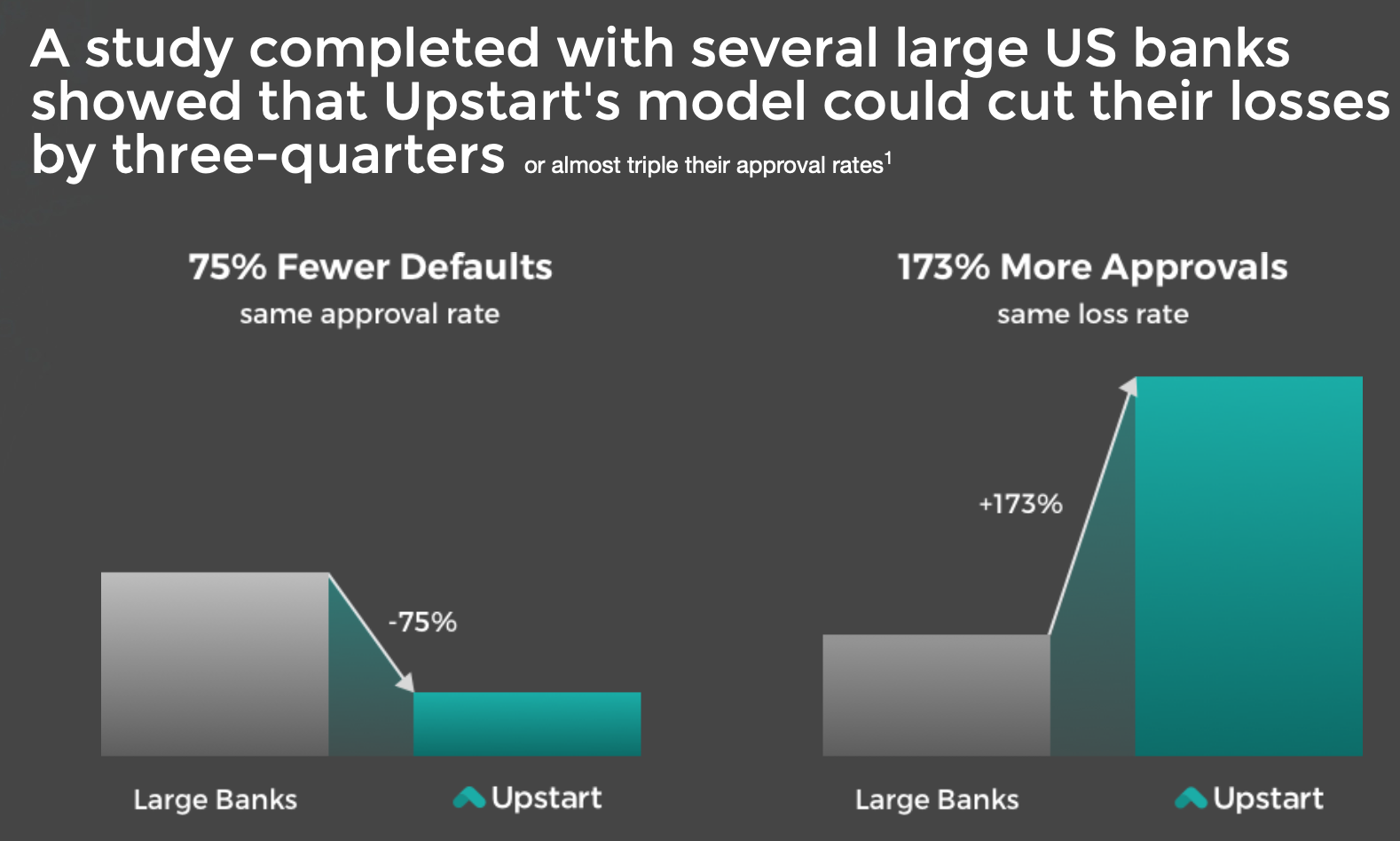

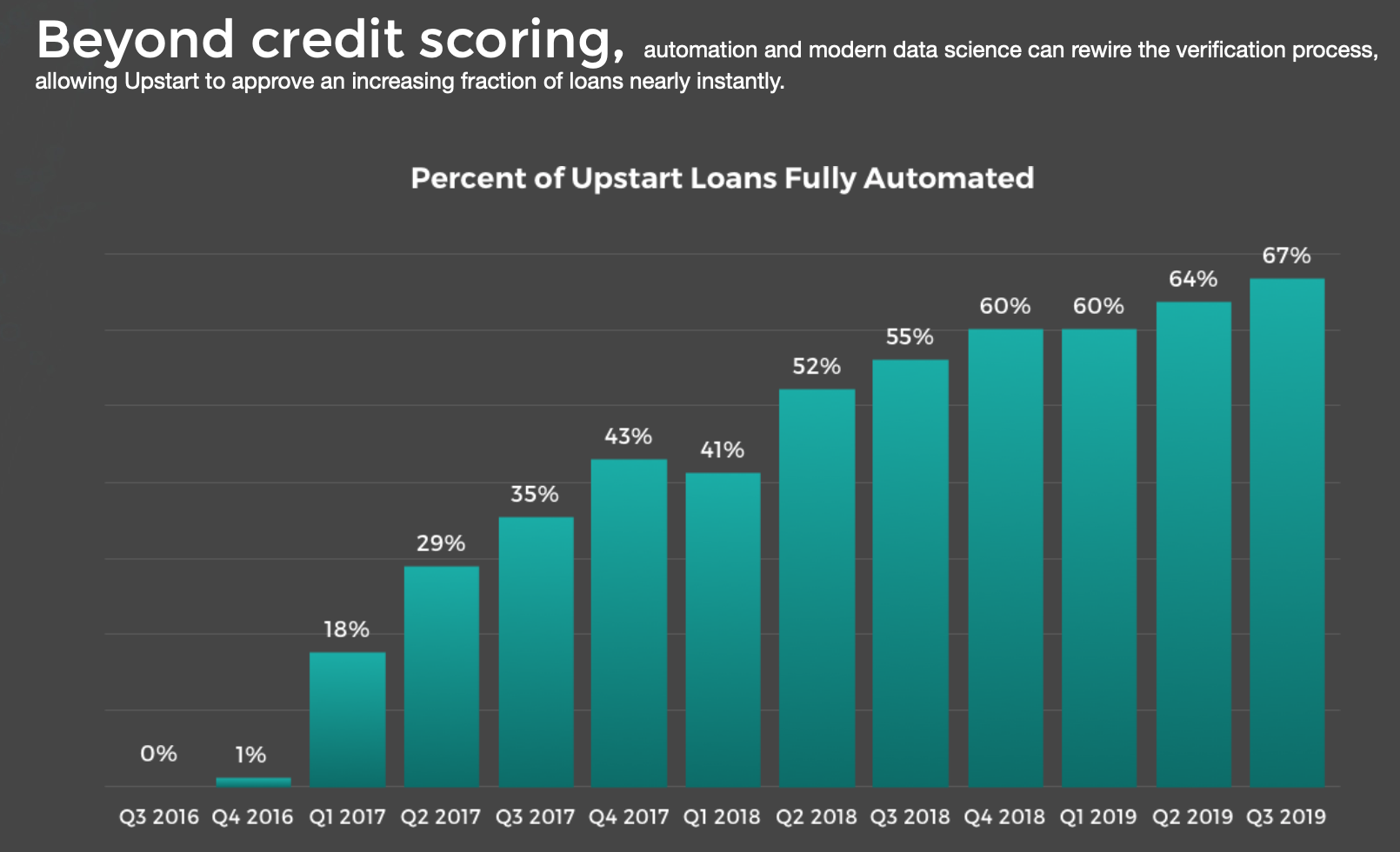

Example: UpStart

Example: Upstart

Source: upstart.com

Upstart

Source: upstart.com

Source: upstart.com

Source: upstart.com

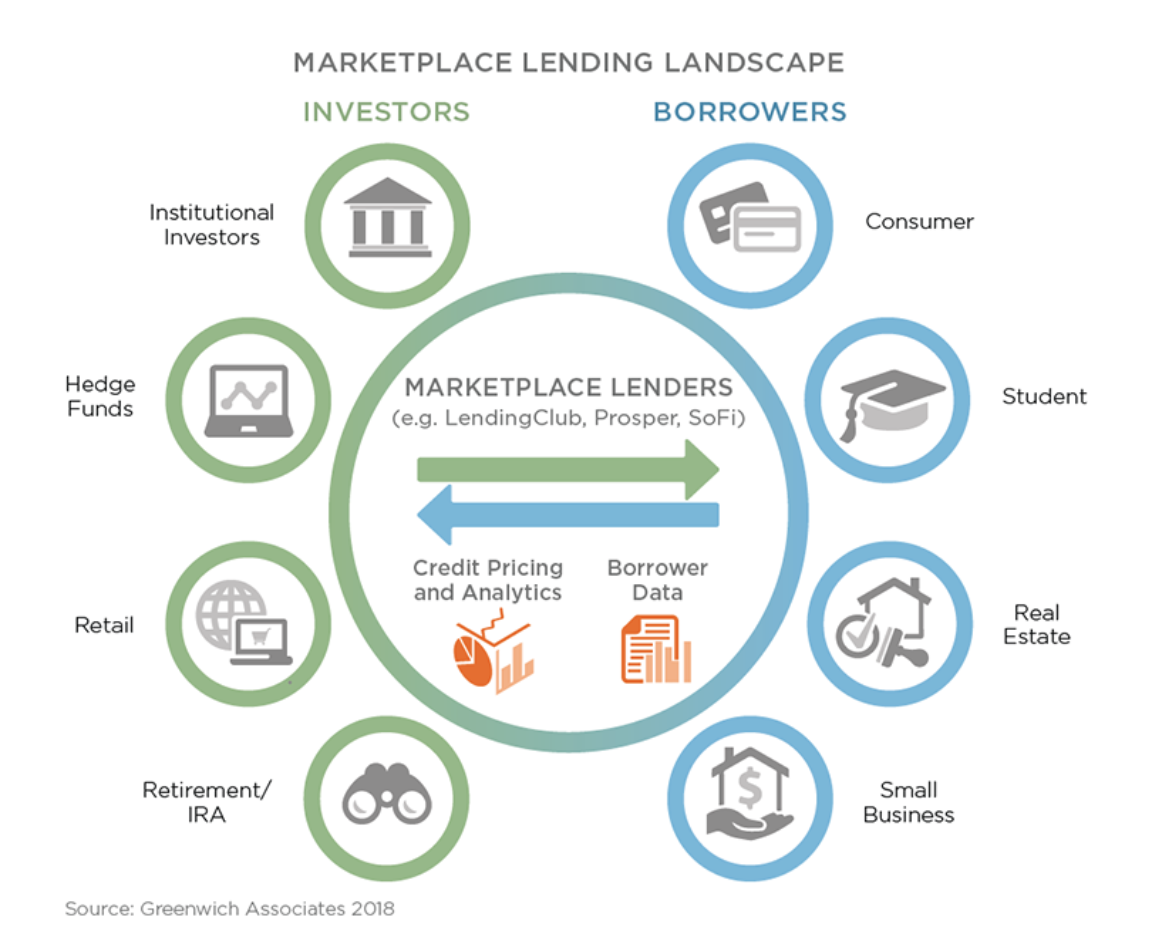

Other Niches? (In consumer lending?)

Other Niches? (In consumer lending?)

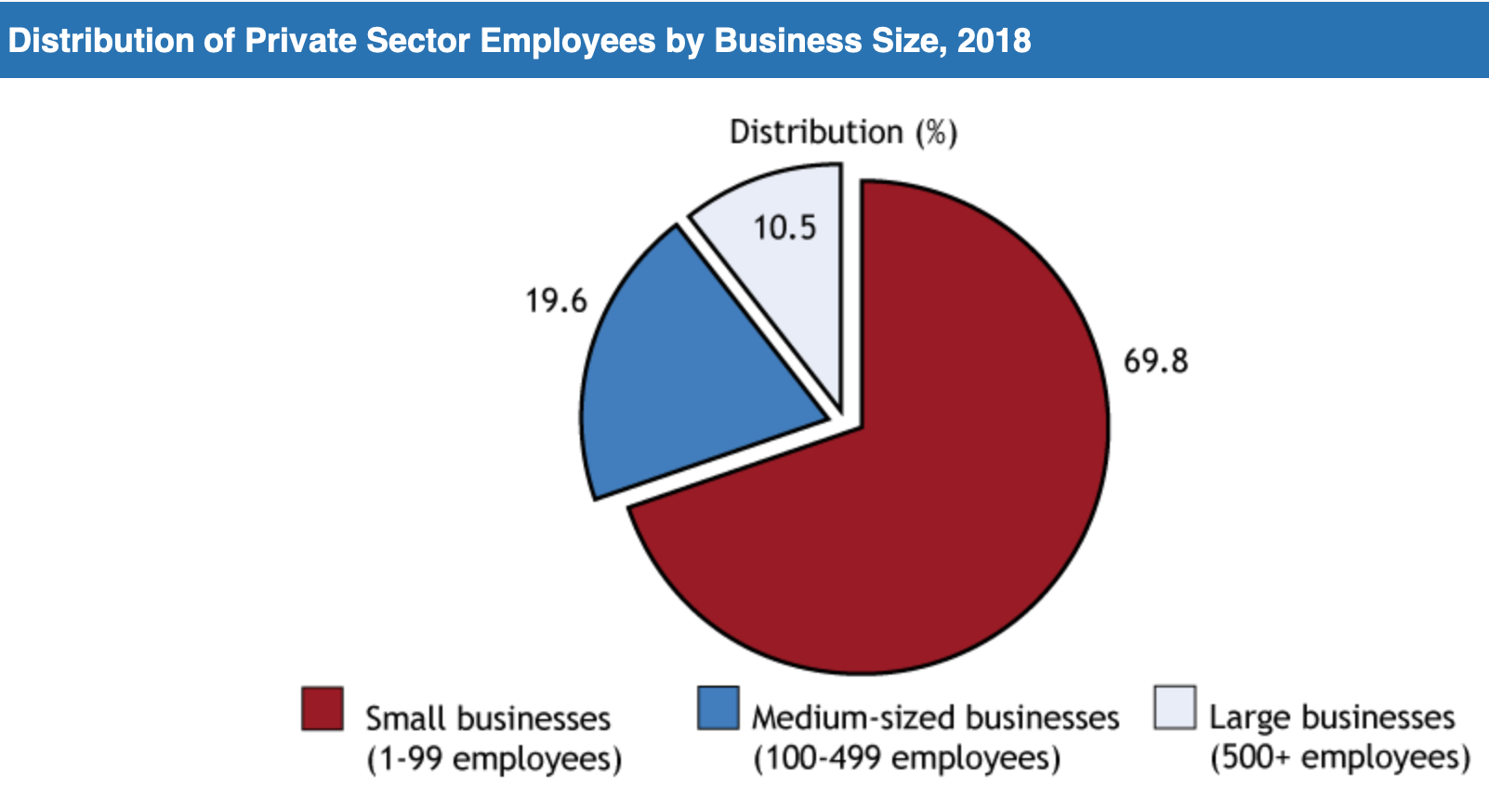

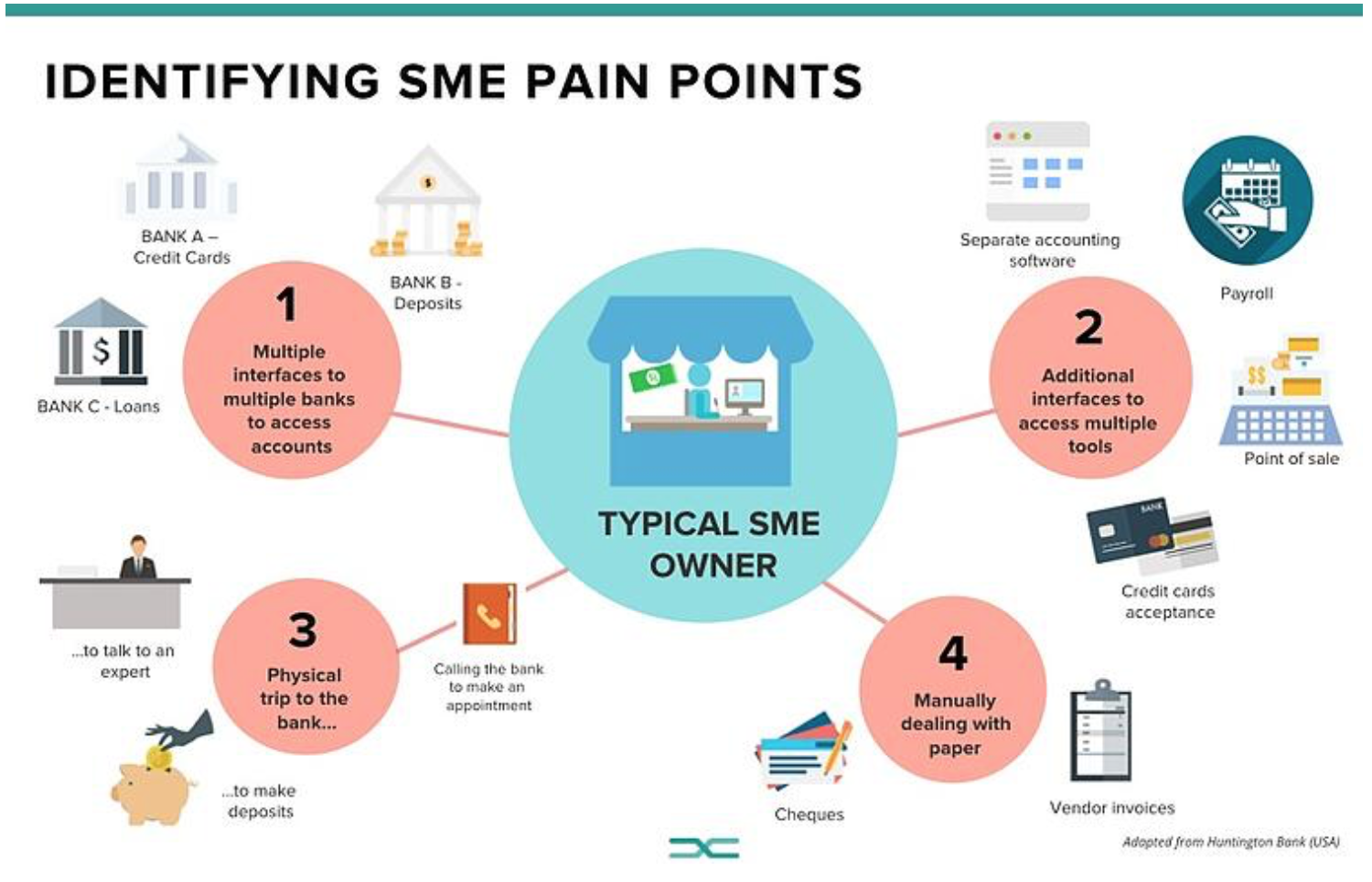

Next big gap: Small and Medium Enterprise Financing

Next big gap: Small and Medium Enterprise Financing

Today, big banks are granting 25.9 percent of the funding requests

This means that they decline 74.1% of applications!

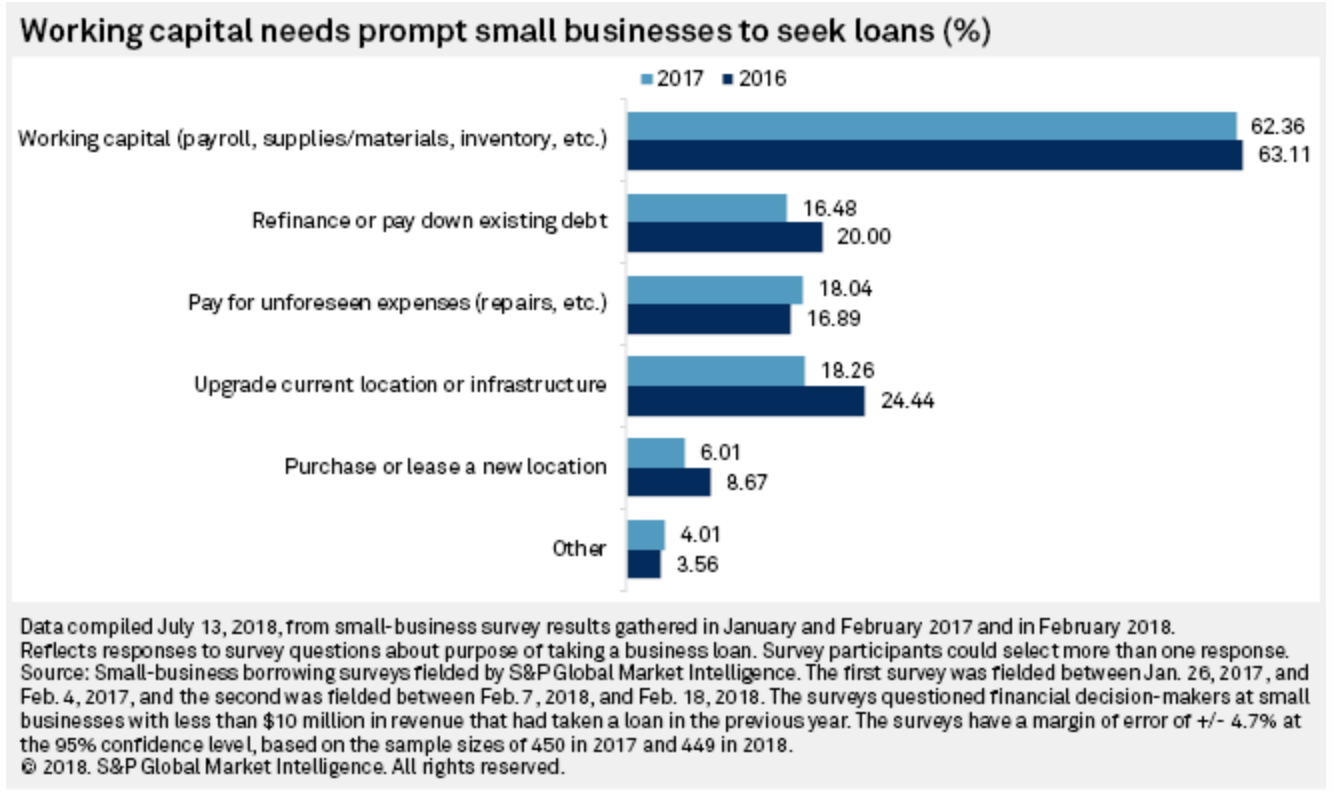

Small Businesses in Canada (2018)

SME: why do they need the money?

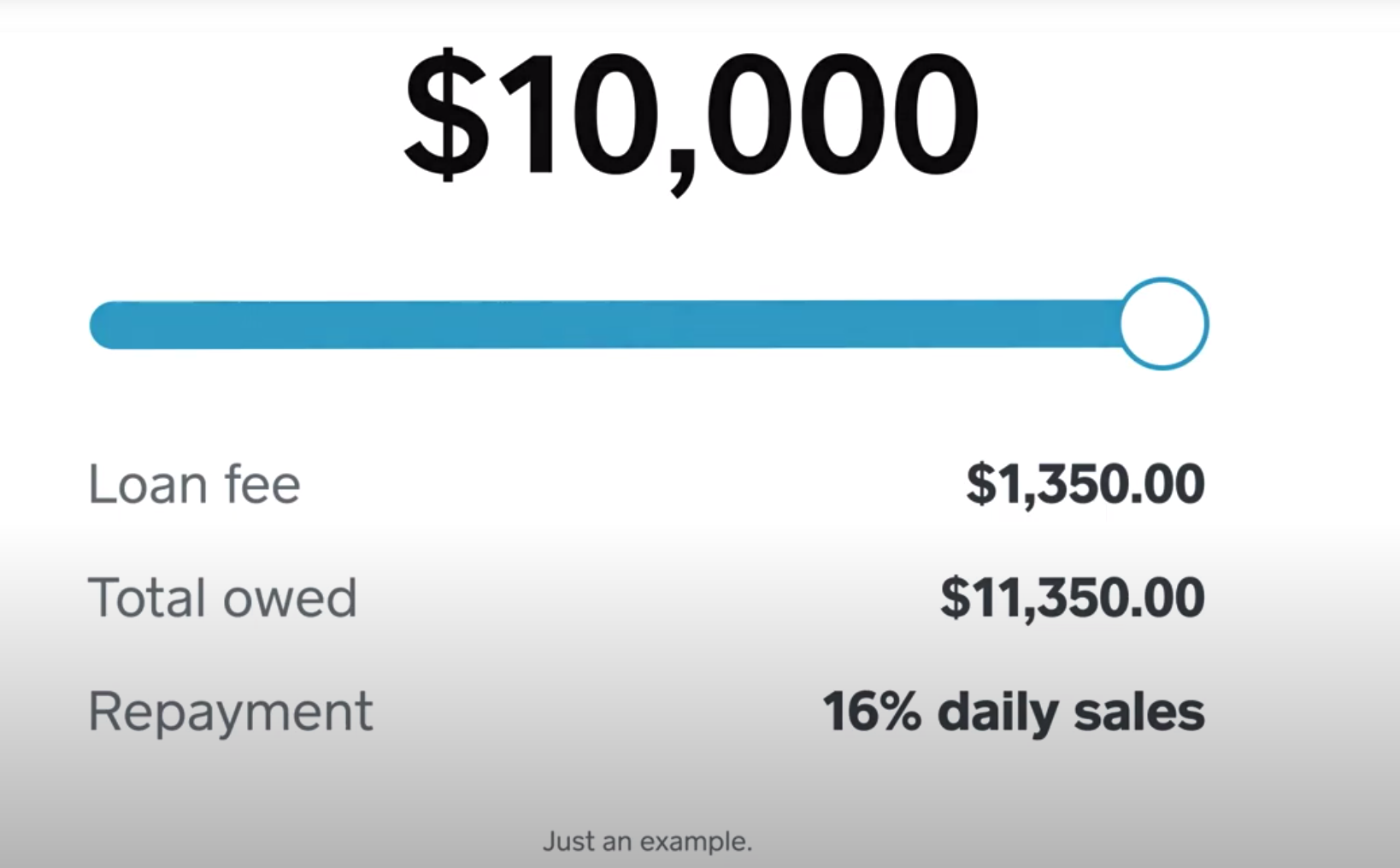

Types of SME loans? (Lending Club)

Market segment challenges?

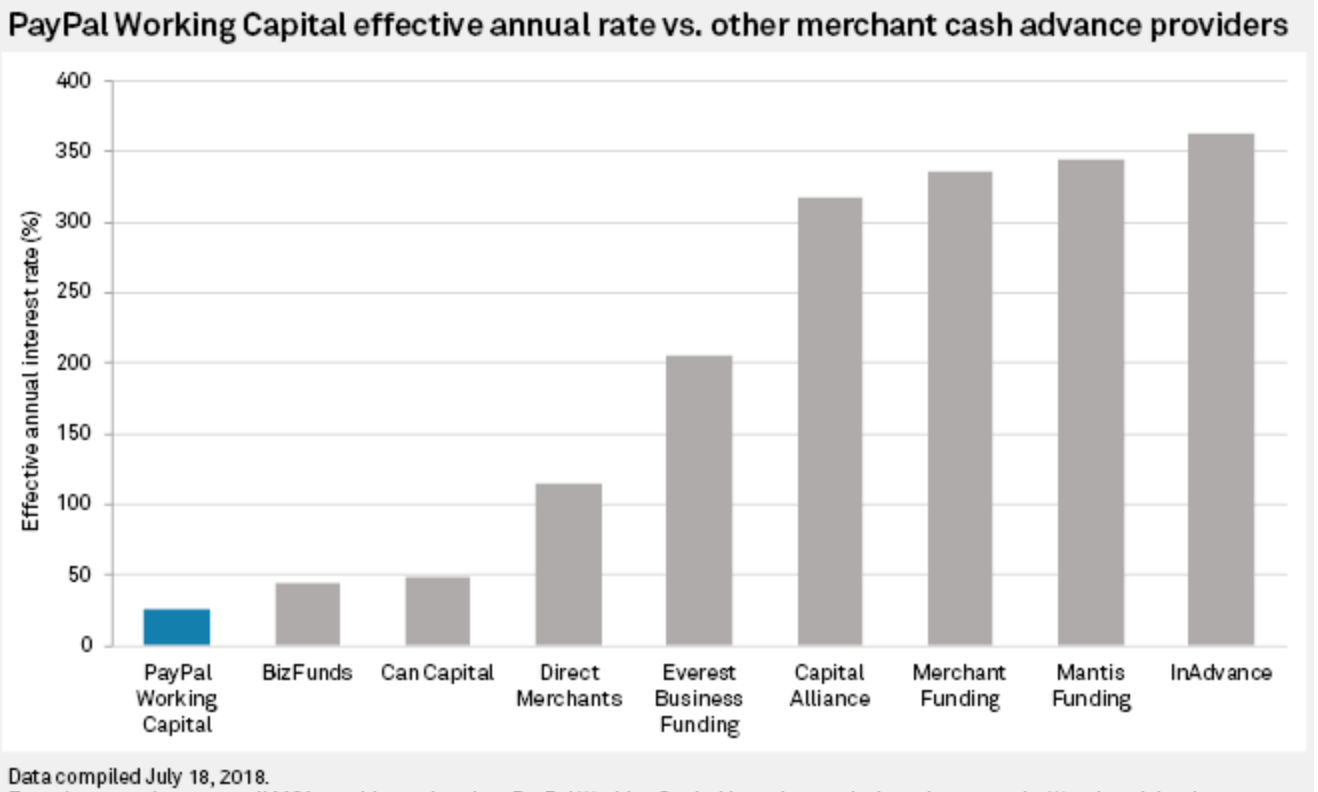

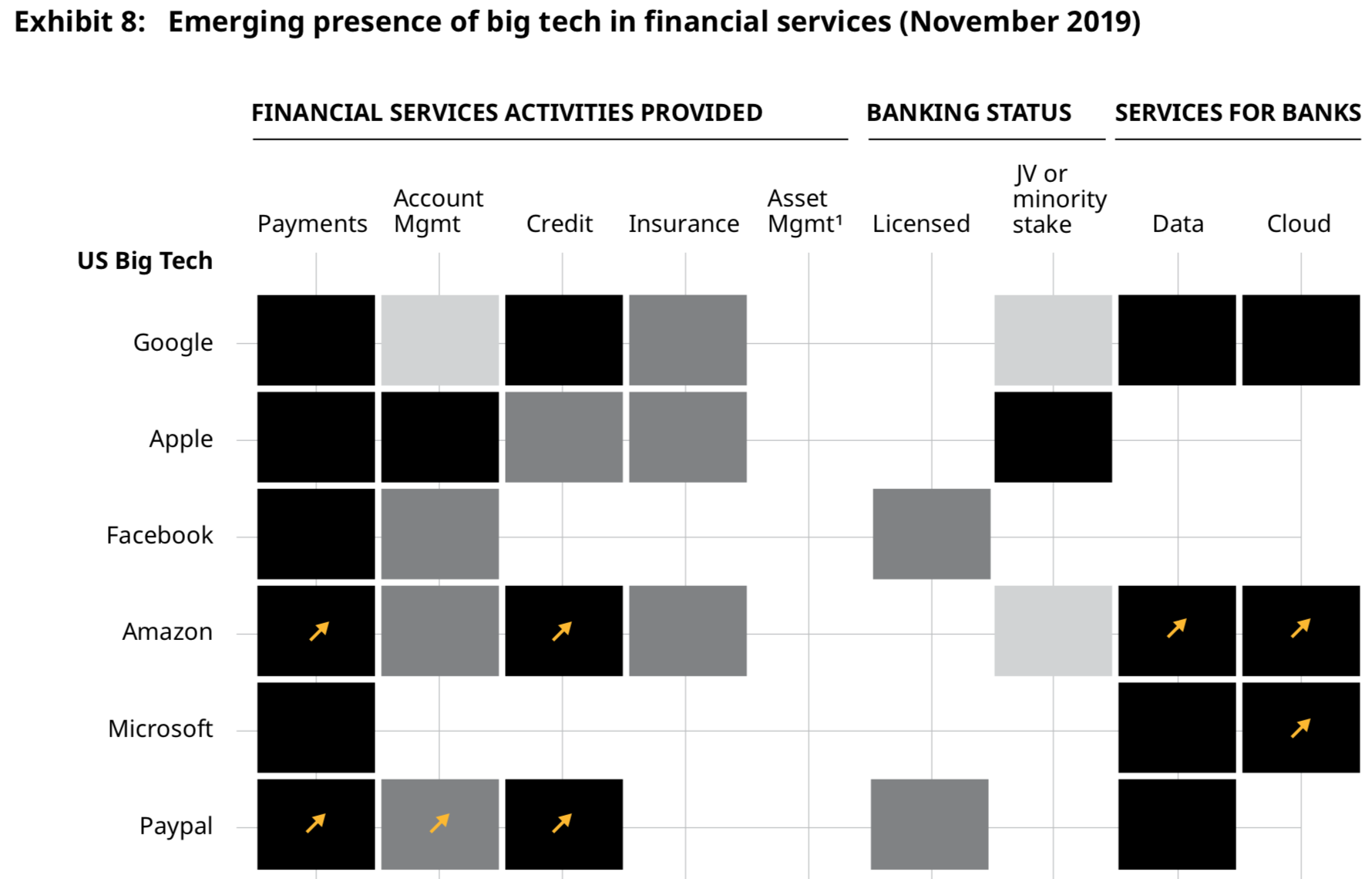

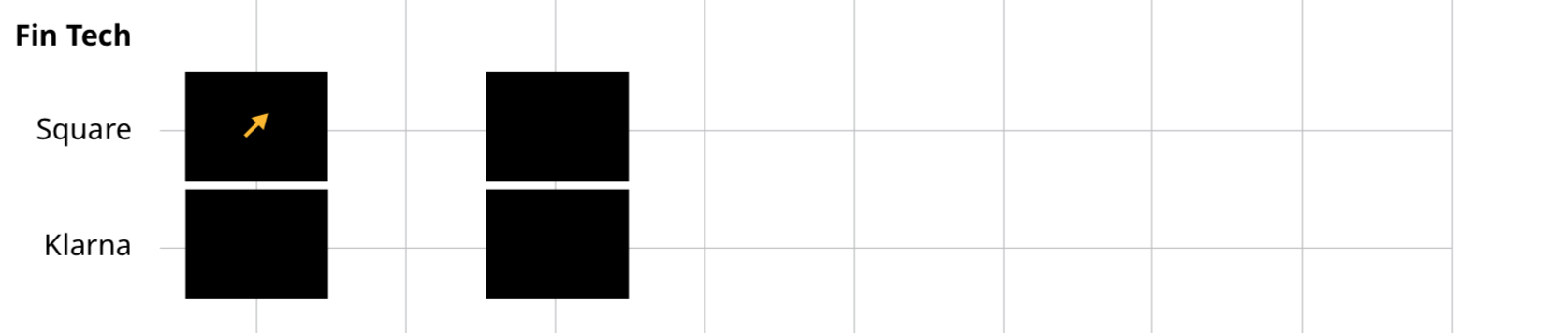

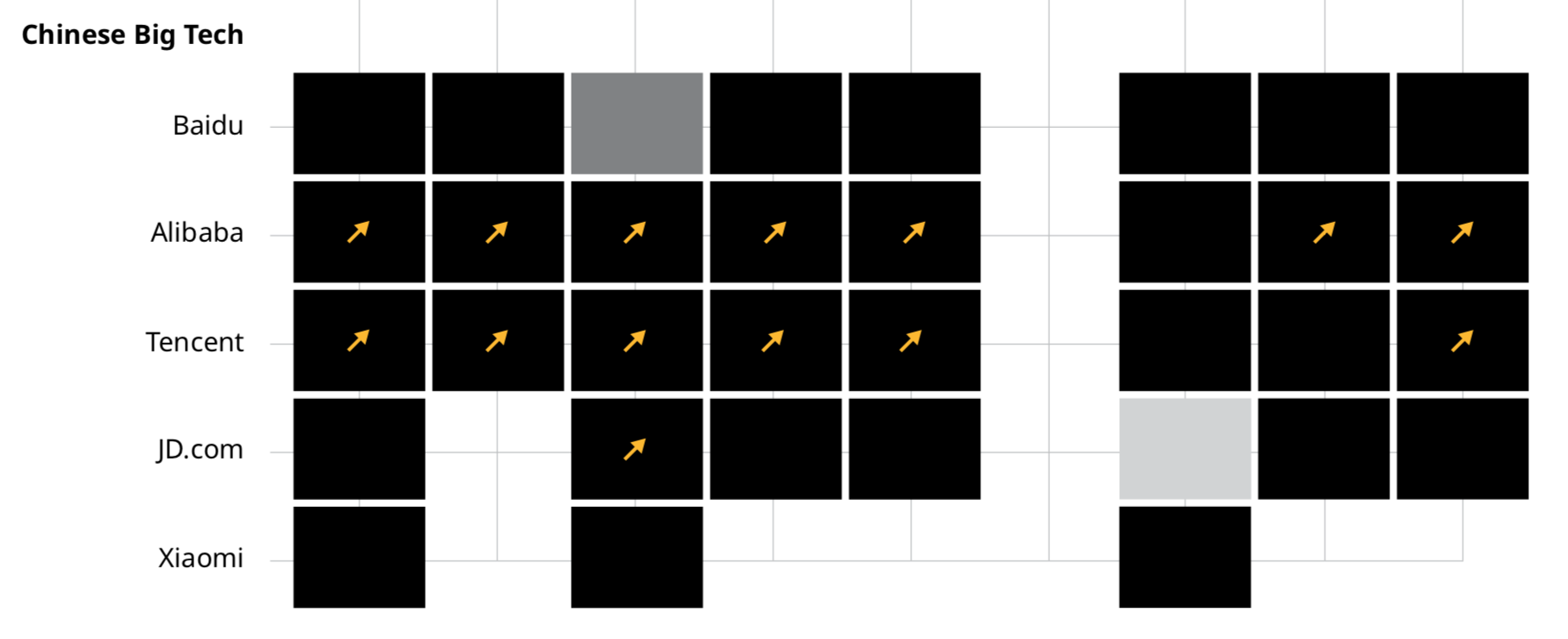

Payments and Lending

Payments and Lending

Alternative (?): look at customers' credit!

The flip side of online lenders?

Speaking of Amazon, data, etc

Alternative sources of funding for SME?

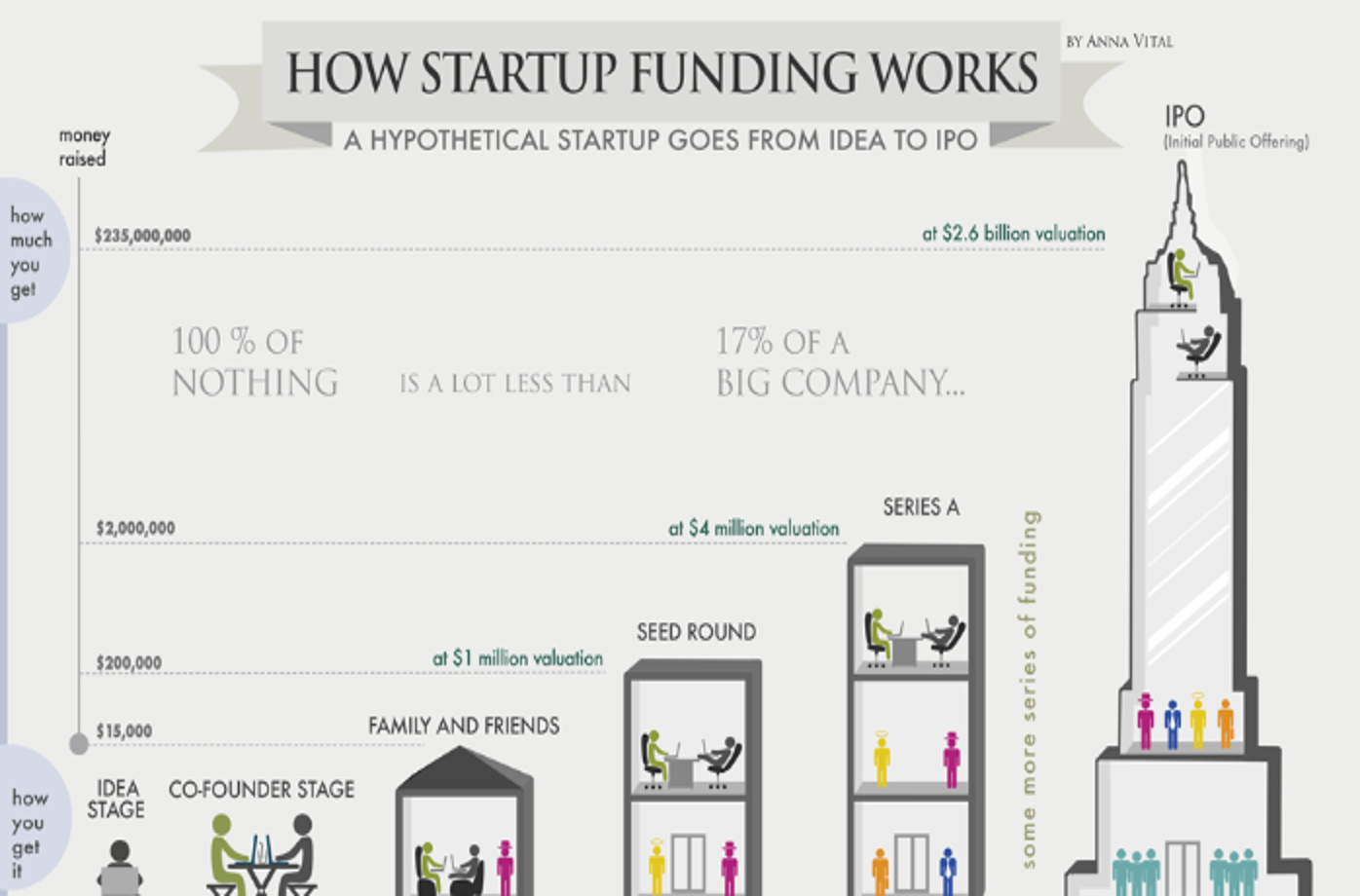

Traditional sources of private equity funding

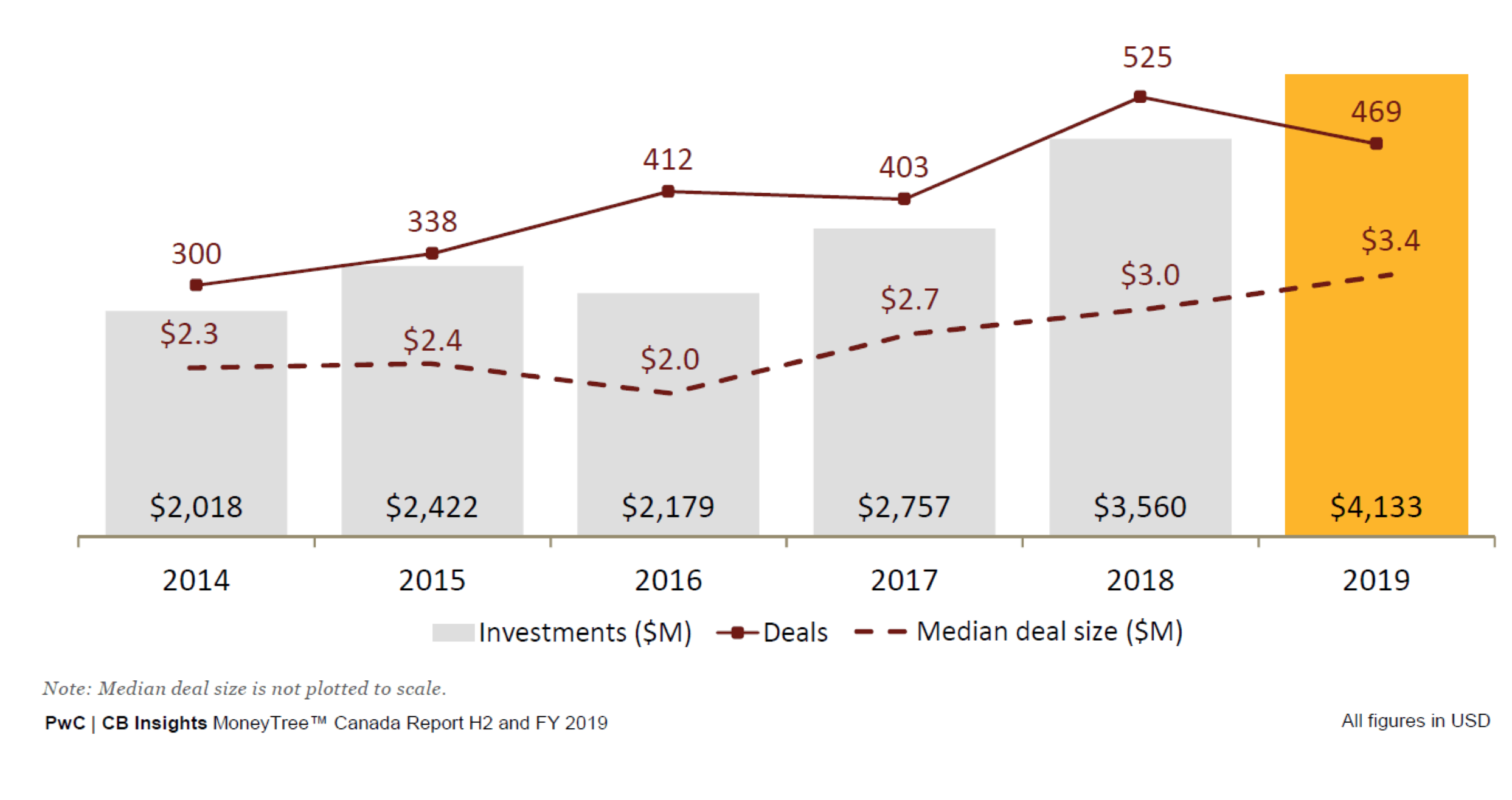

Venture Funding in Canada

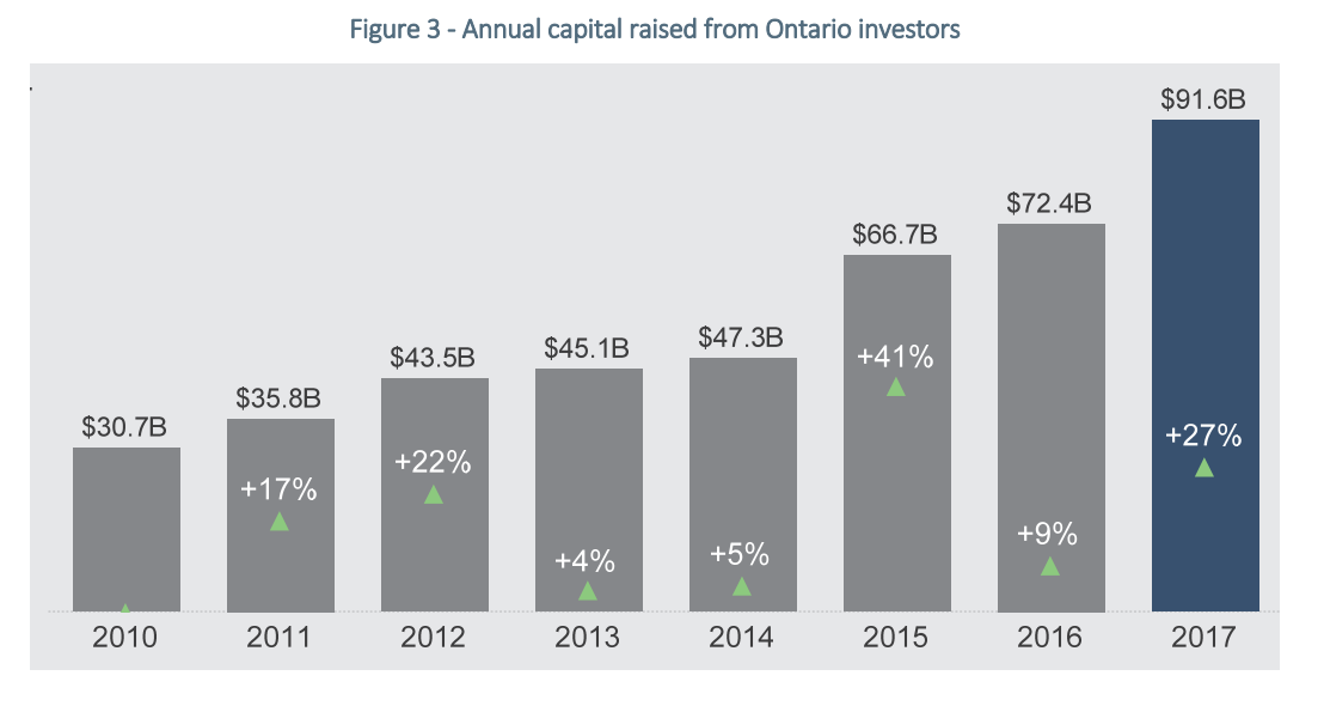

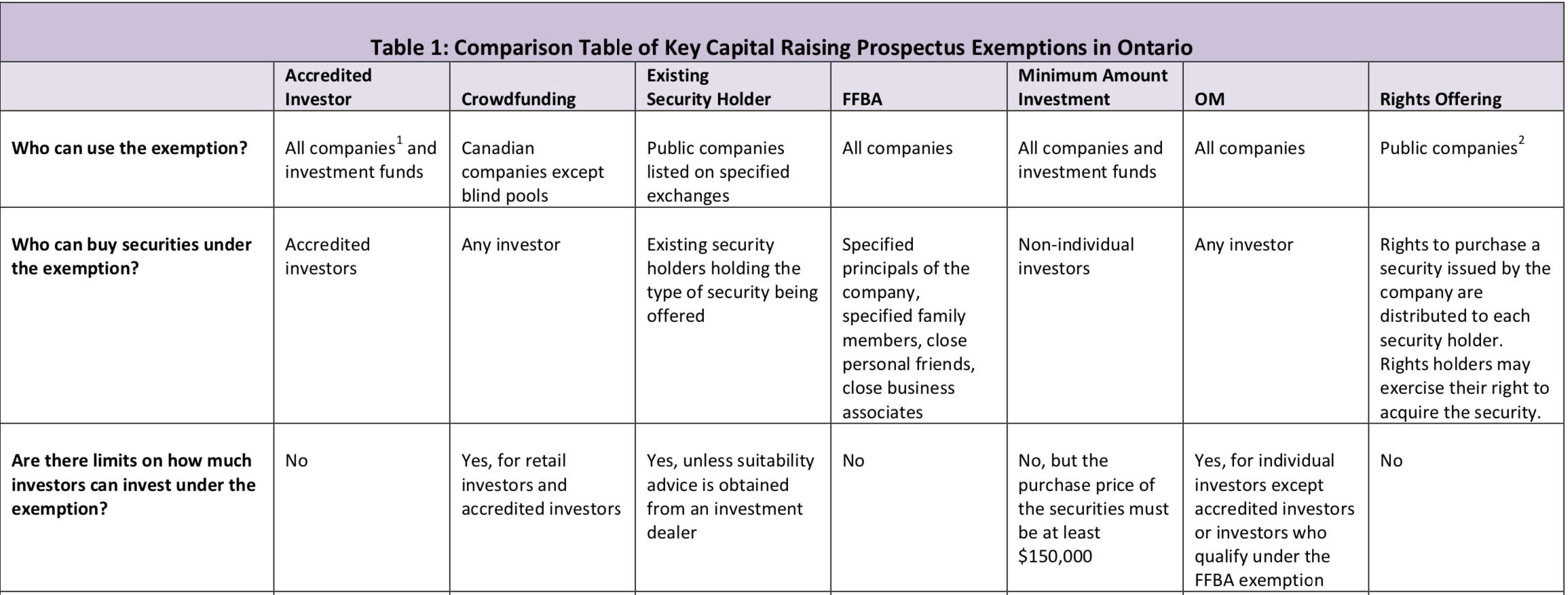

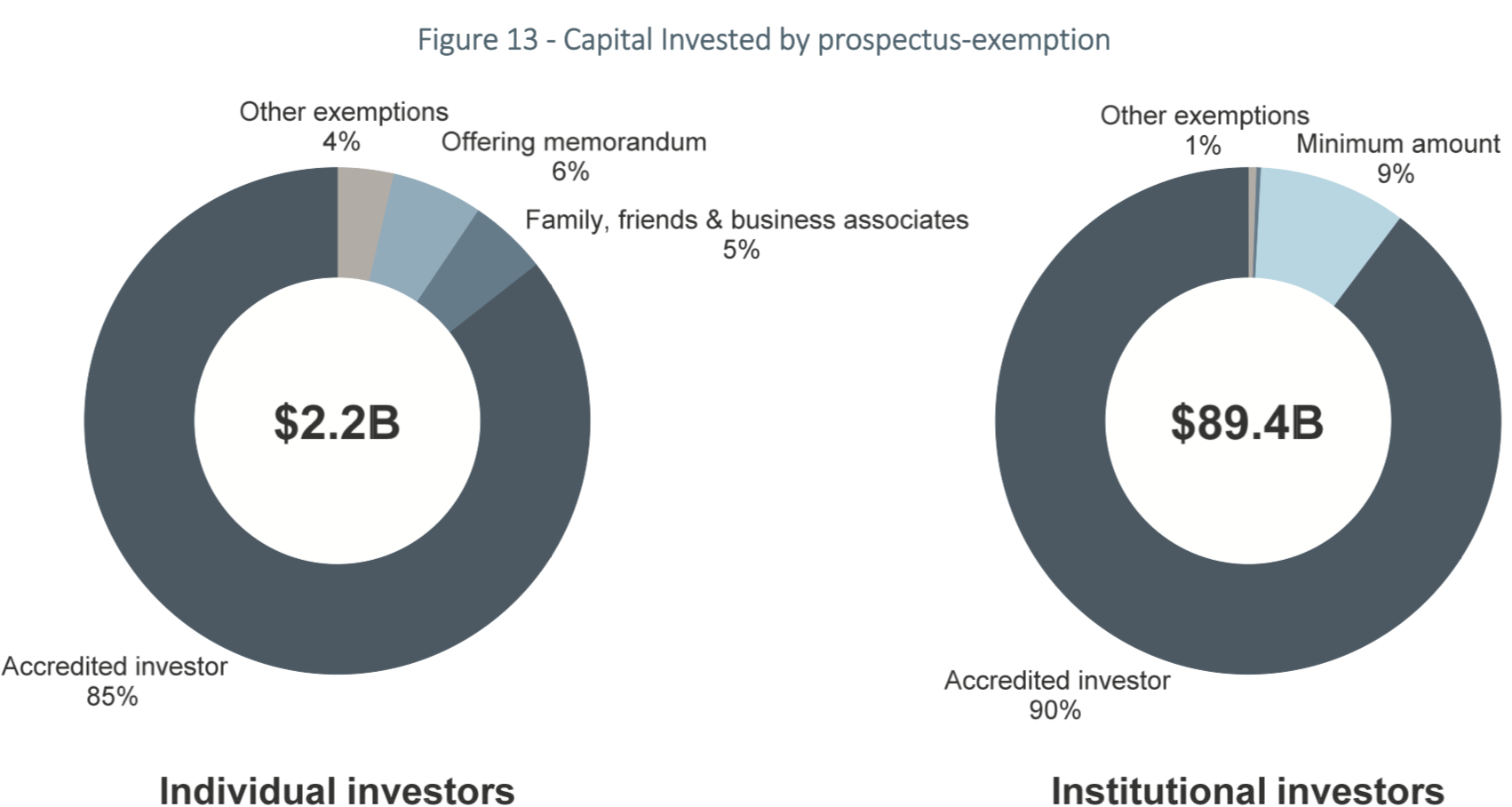

Private markets in Canada (Ontario investors)

Private markets in Canada (Ontario investors)

Private markets in Canada (Ontario investors)

Private markets in Canada (Ontario investors)

Data: coinschedule

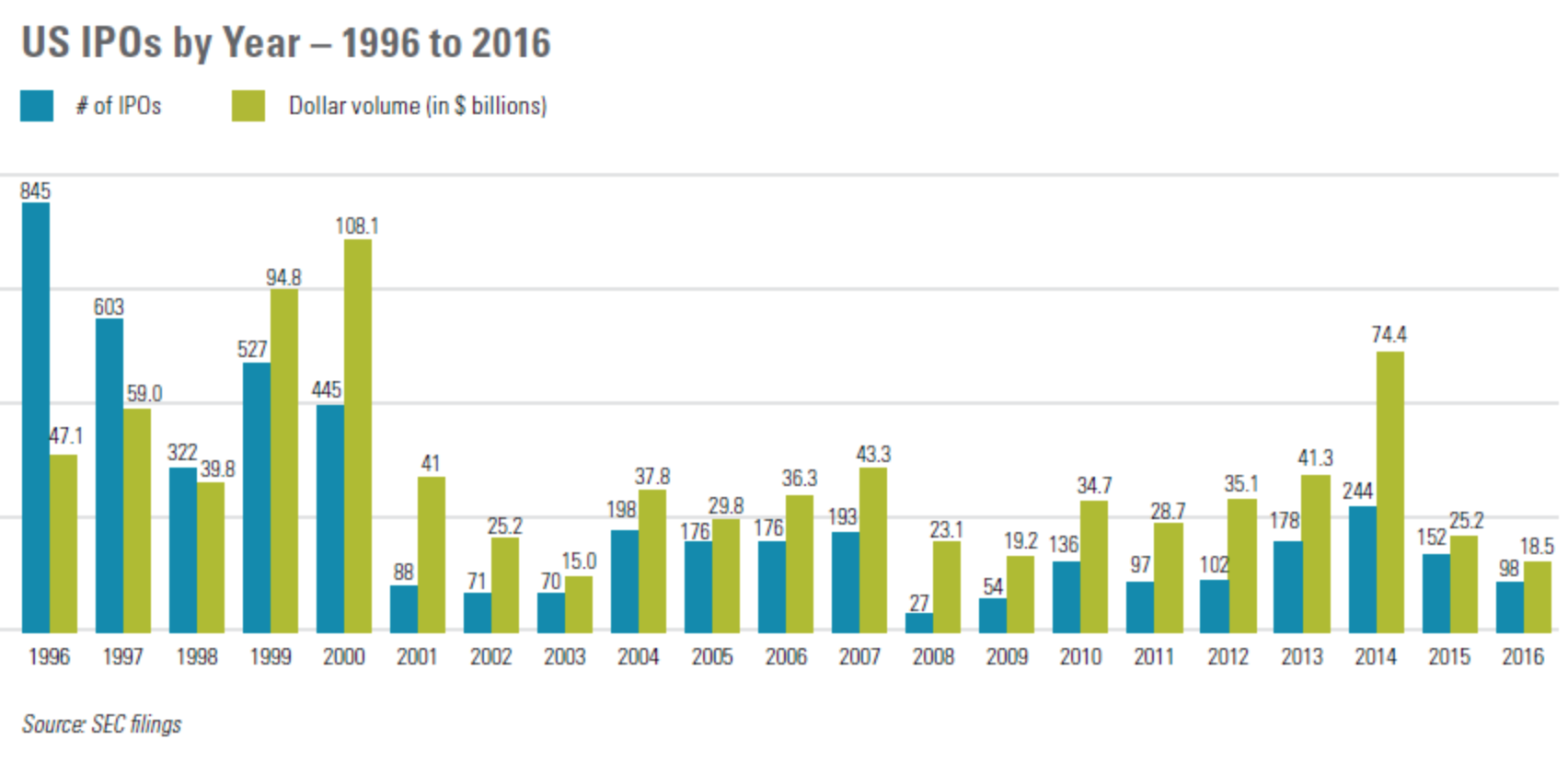

For comparison: publics markets in Canada (IPO)

Data: coinschedule

IPOs: expensive, difficult, and also the # is declining

Data: coinschedule

Why decline in IPOs?

Alternative Sources of Funding?

Crowdfunding

Alternative Sources of Funding?

Crowdfunding: Canada

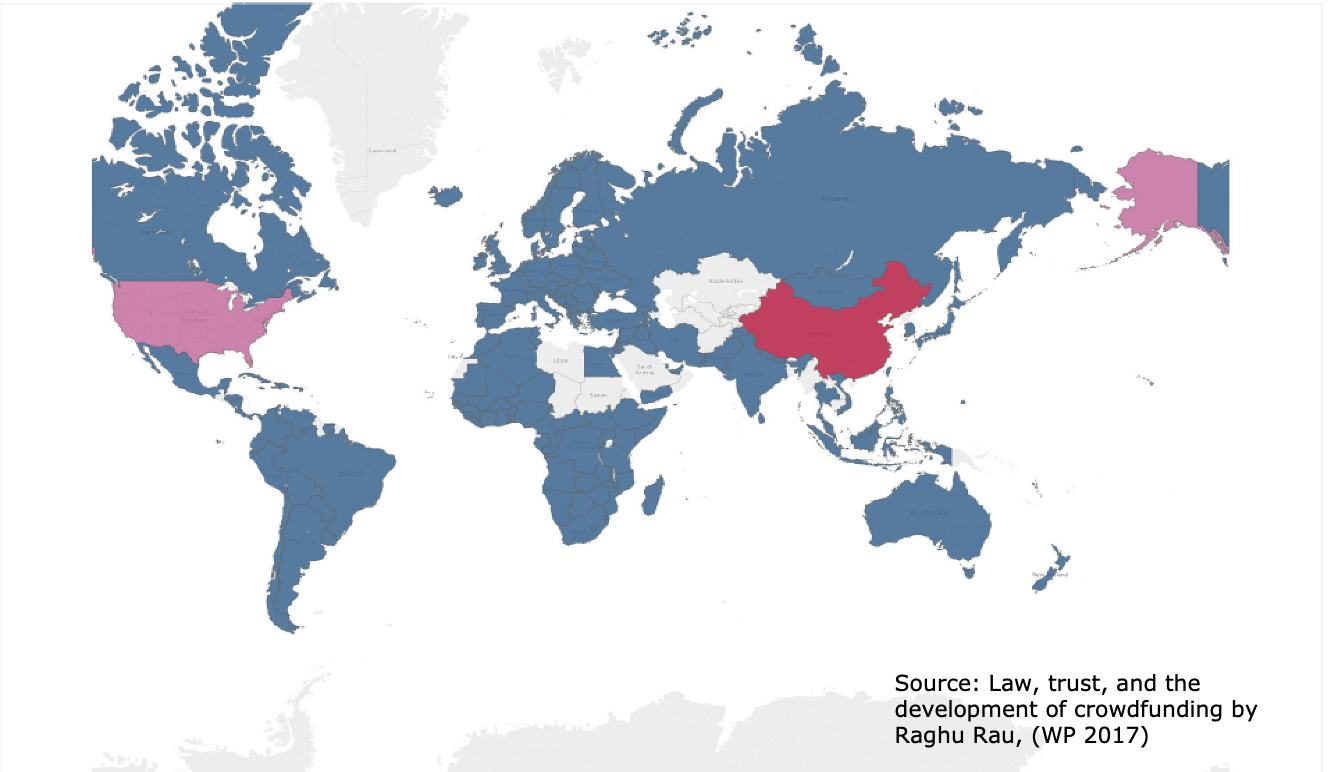

Global Volume of Crowdfunding (2015)

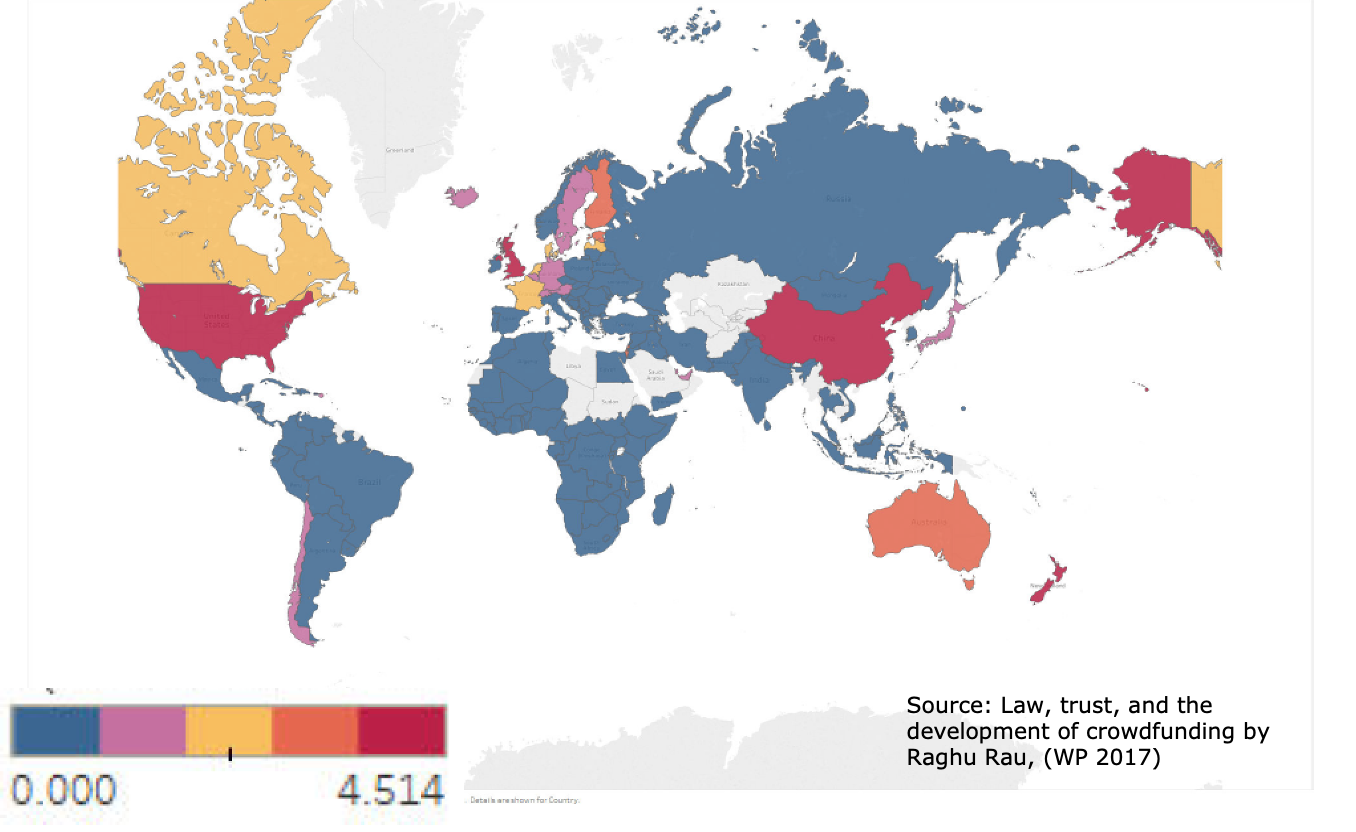

Log Volume Per Capita (Crowdfunding, 2015)

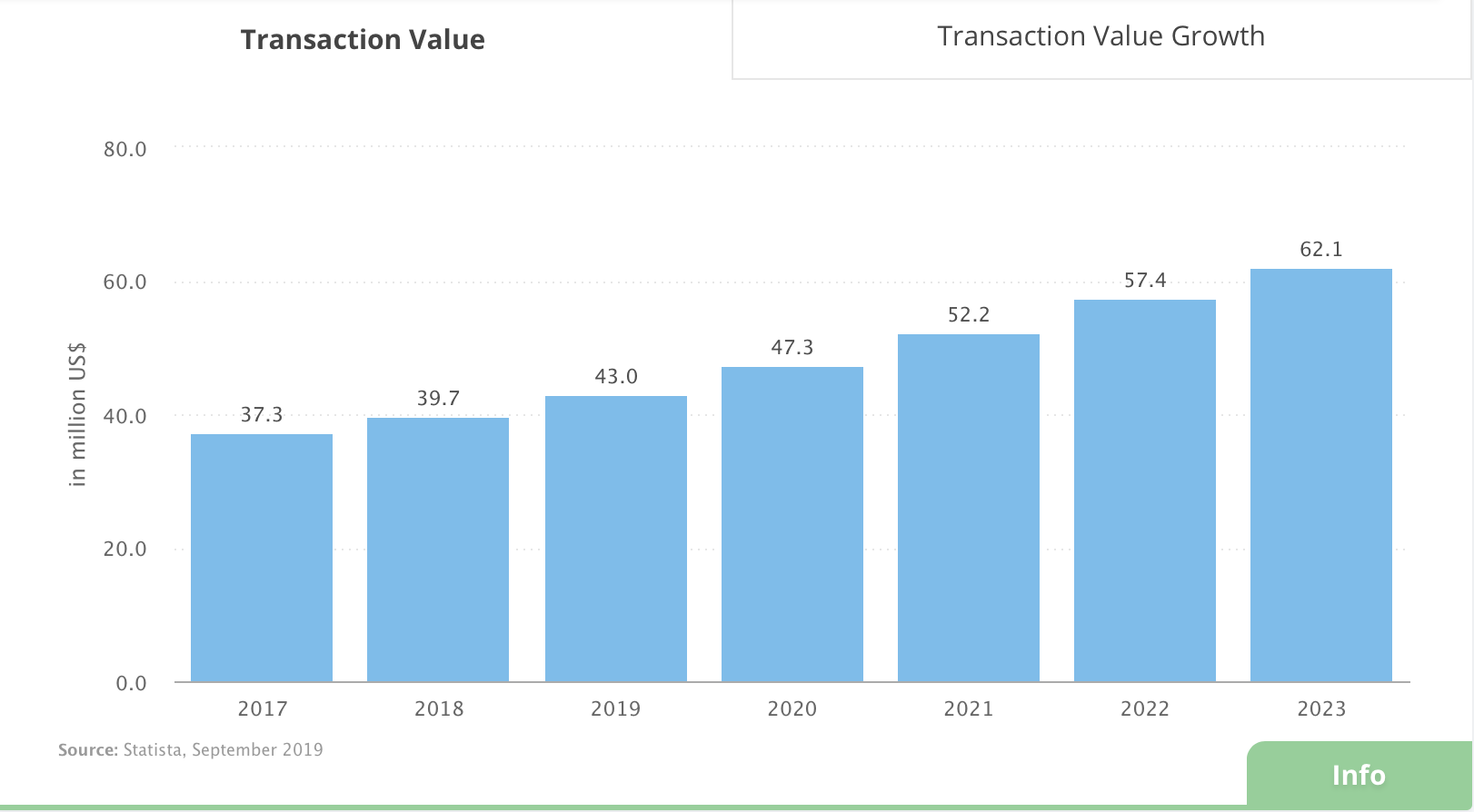

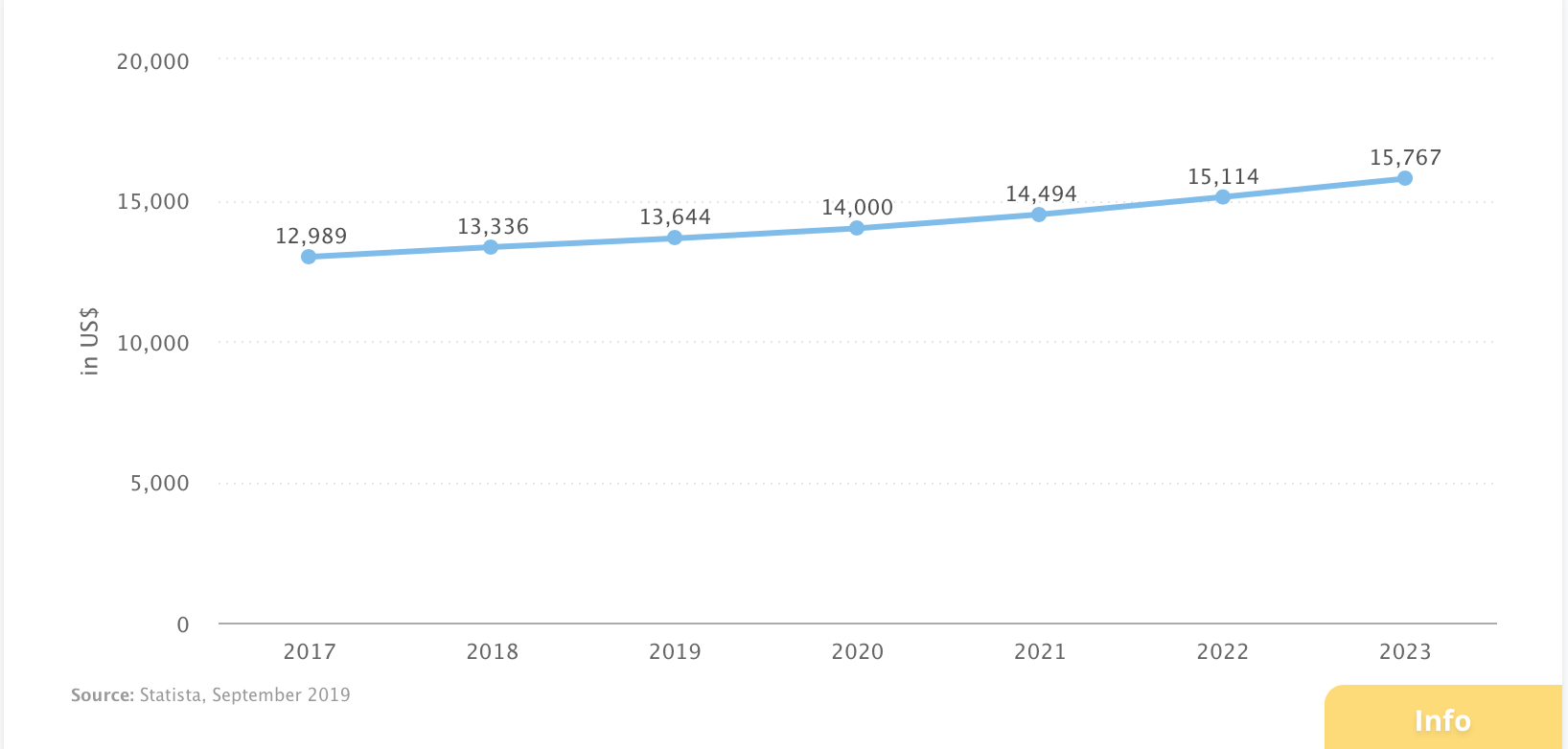

Crowdfunding in Canada (statistic.com projections)

Average deal now is USD13.5-14K

Future of crowdfunding?

Pros and Cons?

Costs of crowdfunding?

Costs to investors?

From Wefunder website:

New frontier: revenue-based lending

14.5% interest - over what horizon?

New frontier: revenue-based lending

Lending and Borrowing

Wealth Management

Payments

Investment Banking Services

Six "Markers of Success" (McKinsey):

Six "Markers of Success" (McKinsey):

By Andreas Park