Andreas Park PRO

Professor of Finance at UofT

by Andreas Park

Based on:

Central Bank Digital Loonie: Canadian Cash for a New Global Economy

(Model X Competition Final Report)

by Veneris, Park, Long and Puri, 2021

Workshop on Future of Money, Paris , June 2022

Our Approach and Thinking

Phase 1:

Phase 2:

Other Key CBDL Proposal Features

user obtains wallet

registers wallet address via e-KYC

transactions processing among whitelisted wallets quasi-anonymously

LVTS/

Lynx

consumers can initiate EFTs from chequing account at commercial bank to CBDL wallet at NB

existing payments system facilitates transfers to CBDL system

NB has reserve account at BoC to link with commercial banks

NB handles all

CBDL payments

issues transaction instructions

checks

( )

( )

initiates wallet transfer

record keeping and AML/CFT processing

overnight house- keeping

*

service example: internal payment-reward system

service example: small business bookkeeping

NB transitions into a validator node

a

b

c

d

e

f

g

blockchain network with validators and nodes

build a new infrastructure based on solid foundation:

avoid building by committee and just do it:

Law allows the BoC to do it, but an open, broad discussion is critical.

@financeUTM

andreas.park@rotman.utoronto.ca

slides.com/ap248

sites.google.com/site/parkandreas/

youtube.com/user/andreaspark2812/

Contingency applies when:

Other Considerations:

Changes to Canada Deposit Insurance Corporation Act

do CBDL wallet require deposit insurance?

Our insight says "no" but our design is flexible

Consumer Protection Initiatives

Privacy Considerations

Tax Considerations

Service provider's wallet licensing

Central Bank Digital Loonie (CBDL) would be programmable money with high privacy protection that powers a new financial infrastructure

Phase 2 Extend Phase 1 to a

Digital "fiat" is already here: Diem, DCEP, Stablecoins, Digital USD & EUR

Phase 1 BoC goes alone to establish CBDLs as new digital payment means

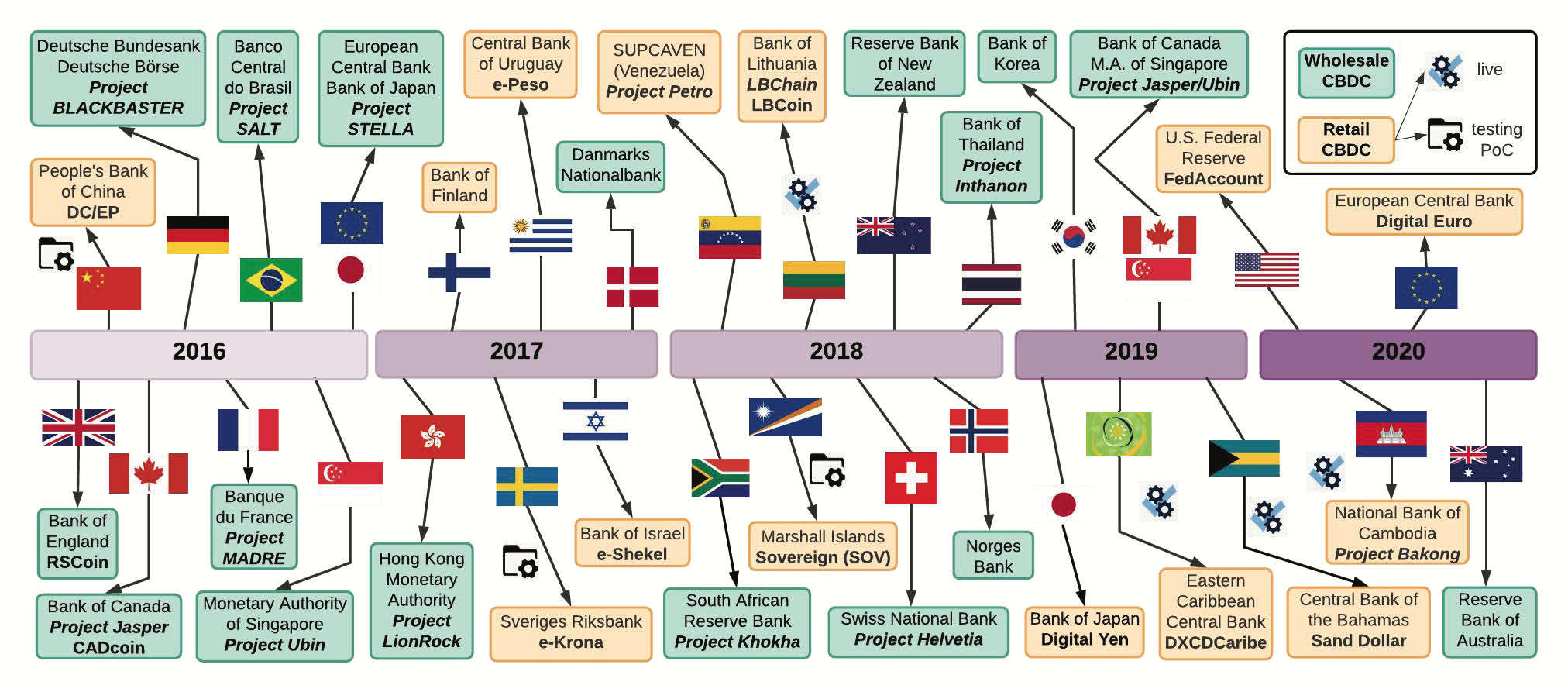

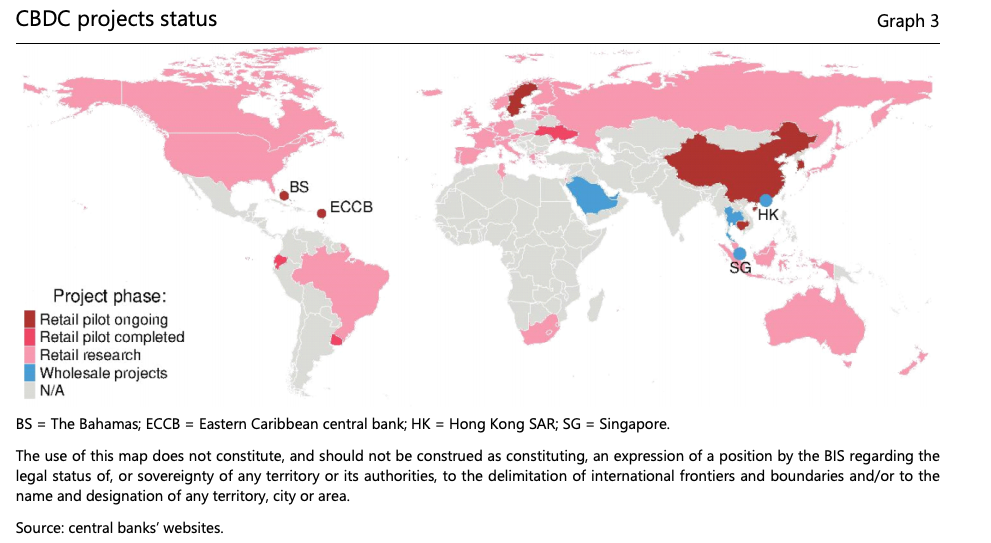

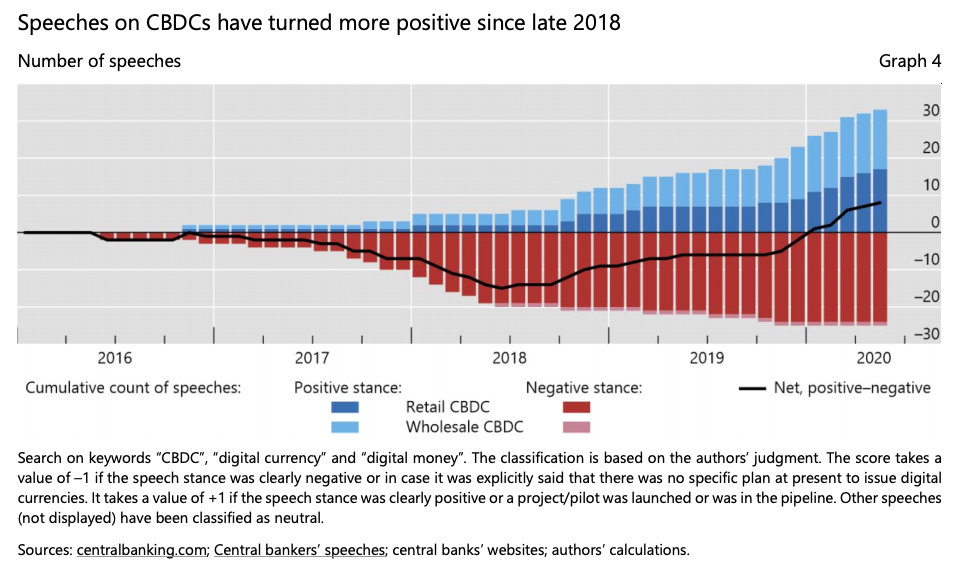

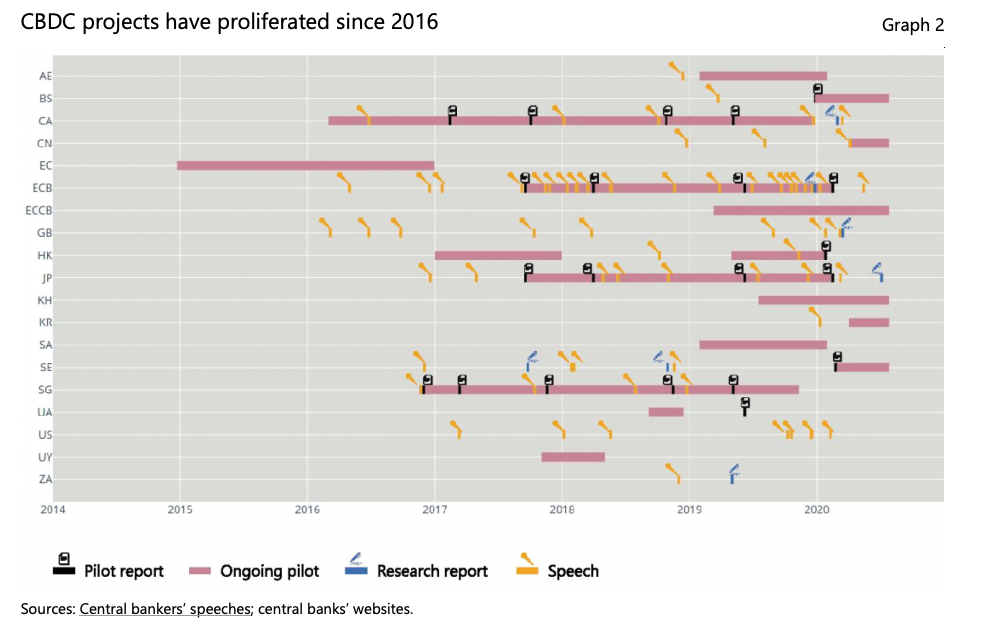

Source: BIS Working Papers No 880 "Rise of the central bank digital currencies: drivers, approaches and technologies" by Raphael Auer, Giulio Cornelli and Jon Frost

each offline card is linked to a KYC-ed user/e-wallet

NB transfers CBDL with serial numbers to the card

user pays offline

user pays offline

user pays offline

user pays offline

user initiates transfer from card to e-wallet

user initiates transfer from e-wallet to card

Separate legal entity

Entirely digital (no physical locations)

Other Considerations:

Changes to Canada Deposit Insurance Corporation Act

do CBDL wallet require deposit insurance?

Our insight says "no" but our design is flexible

Consumer Protection Initiatives

Privacy Considerations

Tax Considerations

Service provider's wallet licensing

Contingency applies when:

Changes to Canada Deposit Insurance Corporation Act

do CBDL wallet require deposit insurance?

Our insight answers "no" but our design remains flexible

Consumer Protection Initiatives

Privacy Considerations

Tax Considerations

Service provider's wallet licensing

\(-38\%\)

The Internet of Things

Contingency applies when:

Our recommendation:

\(\Rightarrow\)

\(\Leftarrow\) Centralized system/Boss-Node gives strong control

\(\Leftarrow\) Likely a Phase 2 solution but could be provided by merchants directly

\(\Leftarrow\) new utility, using existing KYC processes

\(\Leftarrow\) NB provides a seamless link

strategically bad idea

tech not design choice

Source: BIS Working Papers No 880 "Rise of the central bank digital currencies: drivers, approaches and technologies" by Raphael Auer, Giulio Cornelli and Jon Frost

Will they come?

Go it alone for Phase 1

By Andreas Park

Presentation for a Canada and the Digitalization of Money , August 2021