Andreas Park PRO

Professor of Finance at UofT

Katya Malinova and Andreas Park

Agenda

Why did we write this paper?

Seriously?

0. Cynicism aside - big question: Can we improve liquidity for smaller listings?

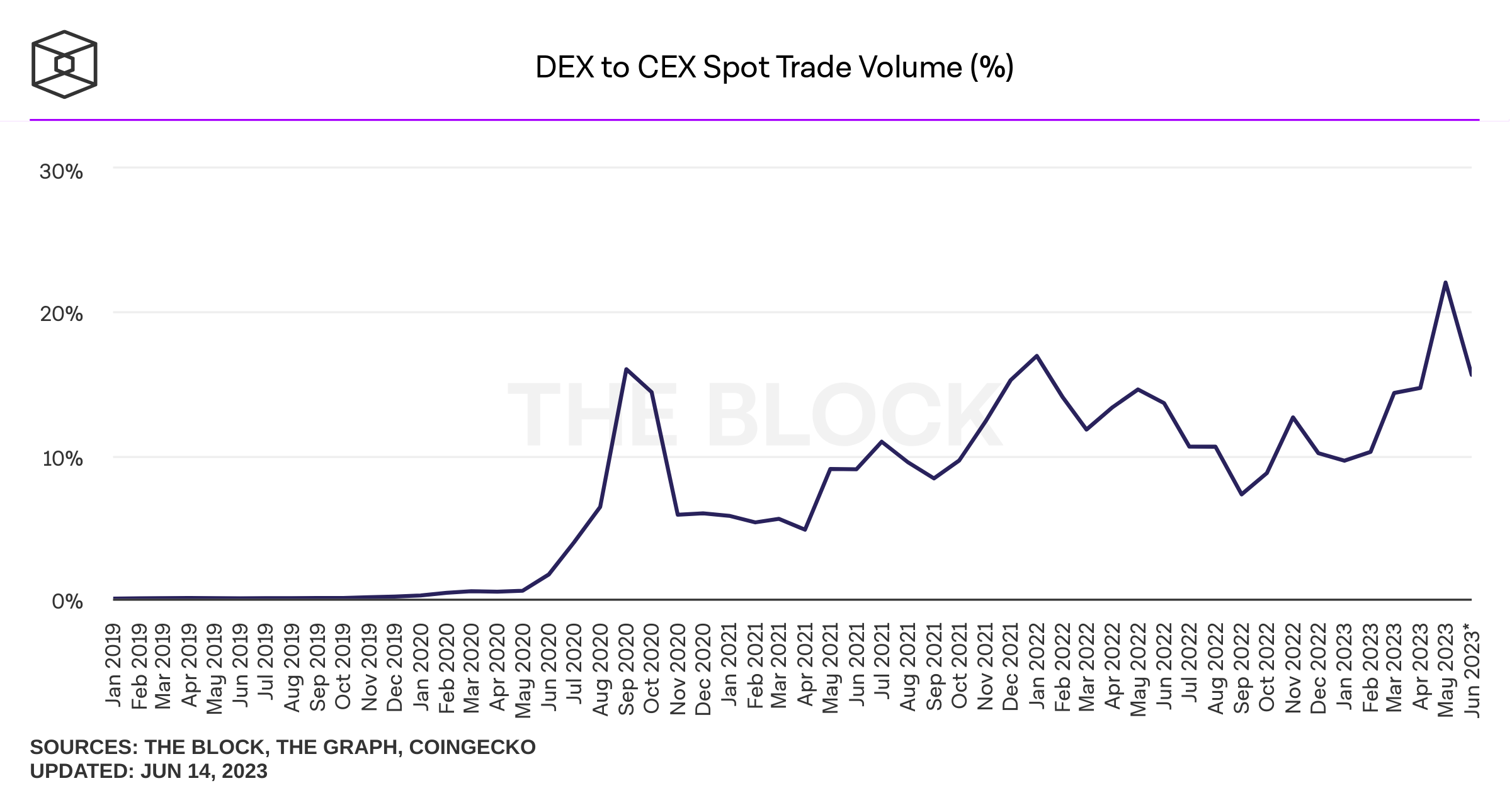

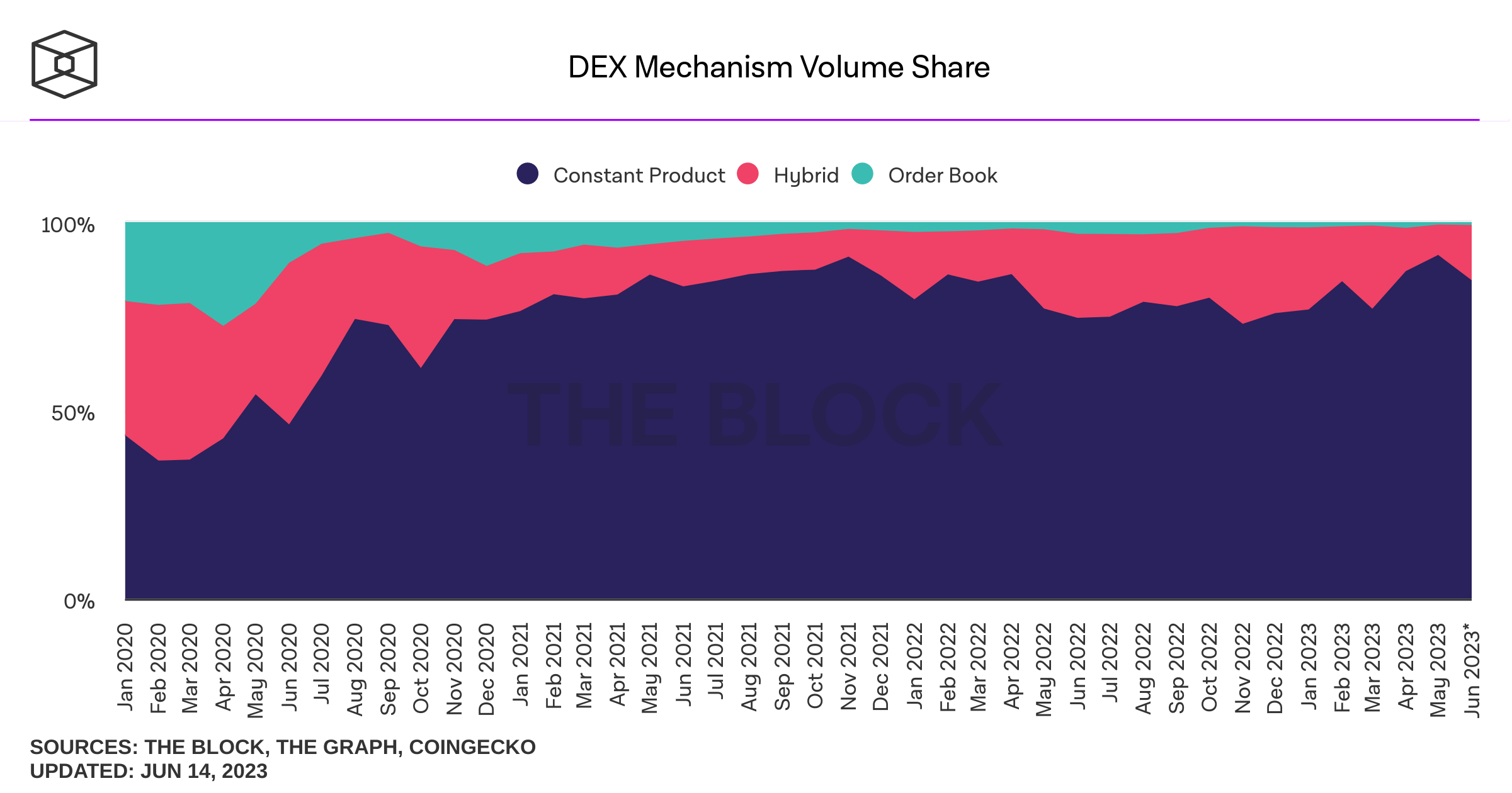

Some Motivation

Basic Idea

payments network

Stock Exchange

Clearing House

custodian

custodian

beneficial ownership record

seller

buyer

Broker

Broker

Broker

Exchange

Internalizer

Wholeseller

Darkpool

Venue

Settlement

AMM Pricing

Constant Liquidity (Product) AMM

Key Components

Liquidity Supply and Demand in an Automated Market Maker

The Pricing Function

Liquidity Deposit \(\Rightarrow\) slope of the price curve

Basics of Liquidity Provision

\[\underbrace{F p_0 V}_{\text{fees earned on balanced flow}}+\int_0^\infty\underbrace{(\Delta c(q^*)-q^*p_t(R)}_{\text{adverse selection loss when the return is \(R\)}} +\underbrace{F \cdot \Delta c(q^*))}_{\text{fees earned from arbitrageurs}}~\phi(R)dR \ge 0.\]

\(q^* \) is what arbitrageurs trade to move the price to reflect \(R\)

Basic idea of liquidity provision: earn more on balanced flow than what you lose on price movement

\[\text{fee income} +\underbrace{\text{what I sold it for}-\text{value of net position}}_{\text{adverse selection loss}} \ge 0 \]

in AMMs:

protocol fee

in tradFi: bid-ask spread

Basics of Liquidity Provision

\[\int_0^\infty\underbrace{(\Delta c(q^*)-q^*p_t(R)}_{\text{adverse selection loss when the return is \(R\)}} +\underbrace{F \cdot \Delta c(q^*))}_{\text{fees earned from arbitrageurs}}~\phi(R)dR +\underbrace{F p_0 V}_{\text{fees earned on balanced flow}}\ge 0\]

\[\frac{1}{\text{initial deposit}}\int_0^\infty(\Delta c(q^*)-q^*p_t(R)+F \cdot \Delta c(q^*))~\phi(R)dR +\frac{F p_0 V}{\text{initial deposit}}\ge 0\]

\[\int_0^\infty\left(\frac{\Delta c(q^*)-q^*p_t(R)}{\text{initial deposit}} +F \cdot \frac{\Delta c(q^*)}{\text{initial deposit}}\right)~\phi(R)dR +\frac{F p_0 V}{\text{initial deposit}}\ge 0\]

closed form functions of \(R\) only

(see Barbon & Ranaldo (2022))

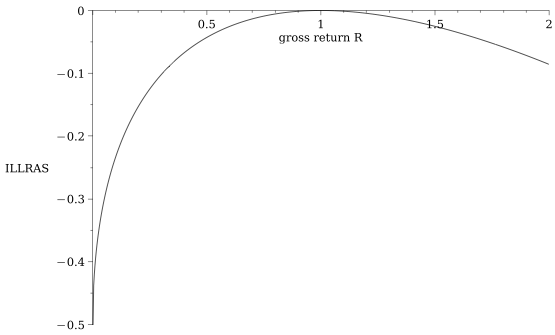

Sidebar: we can quantify how much a PASSIVE LP loses when the price moves by \(R\)

for orientation:

\[\frac{\text{adverse selection loss when the return is \(R\)}}{\text{initial deposit}}=\sqrt{R}-\frac{1}{2}(R+1)\]

see Barbon & Ranaldo (2022)

Basics of Liquidity Provision

Liquidity provision measured as "collective" deposit \(\alpha\) of firm's market cap as function of

\[E[\text{IILRAS}(R)]+F\cdot E[\text{another function of }R]+F\cdot \frac{\text{dollar volume}}{\text{initial deposit}}\ge 0.\]

\[\text{what I sold it for}-\text{value of net position}+\text{fee income} \ge 0 \]

The Decision of the Liquidity Demander

\[F^\pi=\frac{1}{E[|\sqrt{R}-1|/2]+V}\left(-2q\ E[\text{ILLRAS}]+ \sqrt{-2qV\ E[\text{ILLRAS}]}\right).\]

Model Summary

How we think of the Implementation of an AMM for our Empirical Analysis

Approach: daily AMM deposits

Background on Data

some volume may be intermediated

AMMs that's true to the "model"

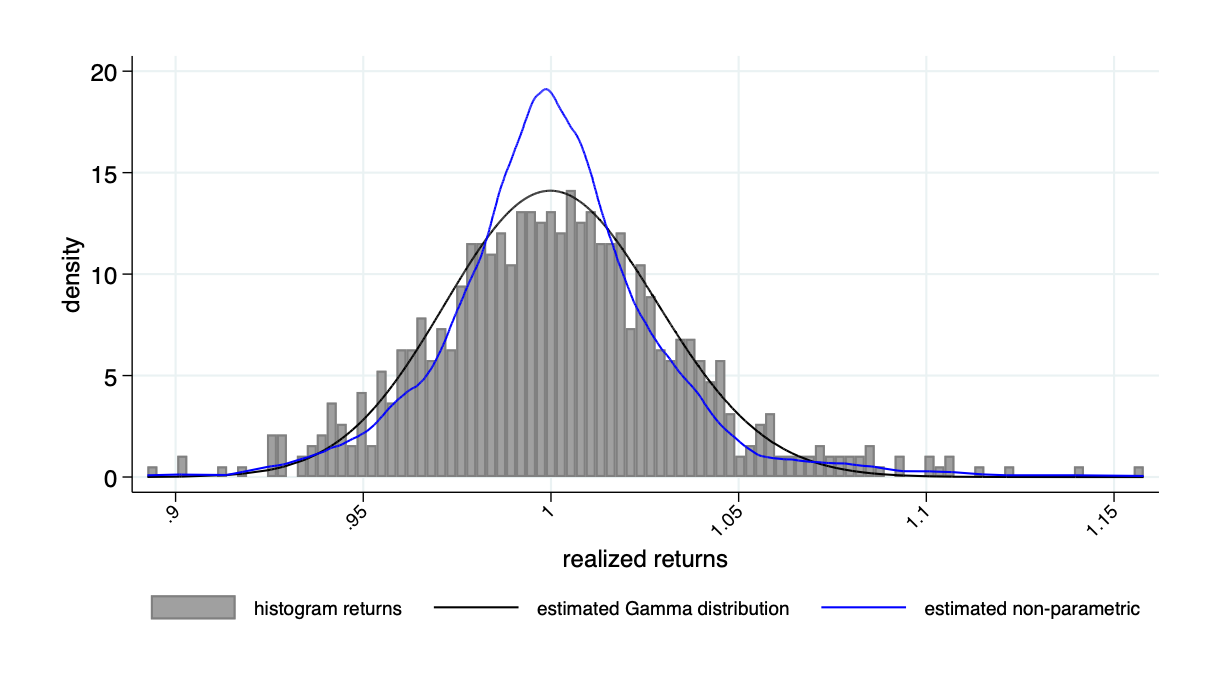

Return distribution example: Microsoft

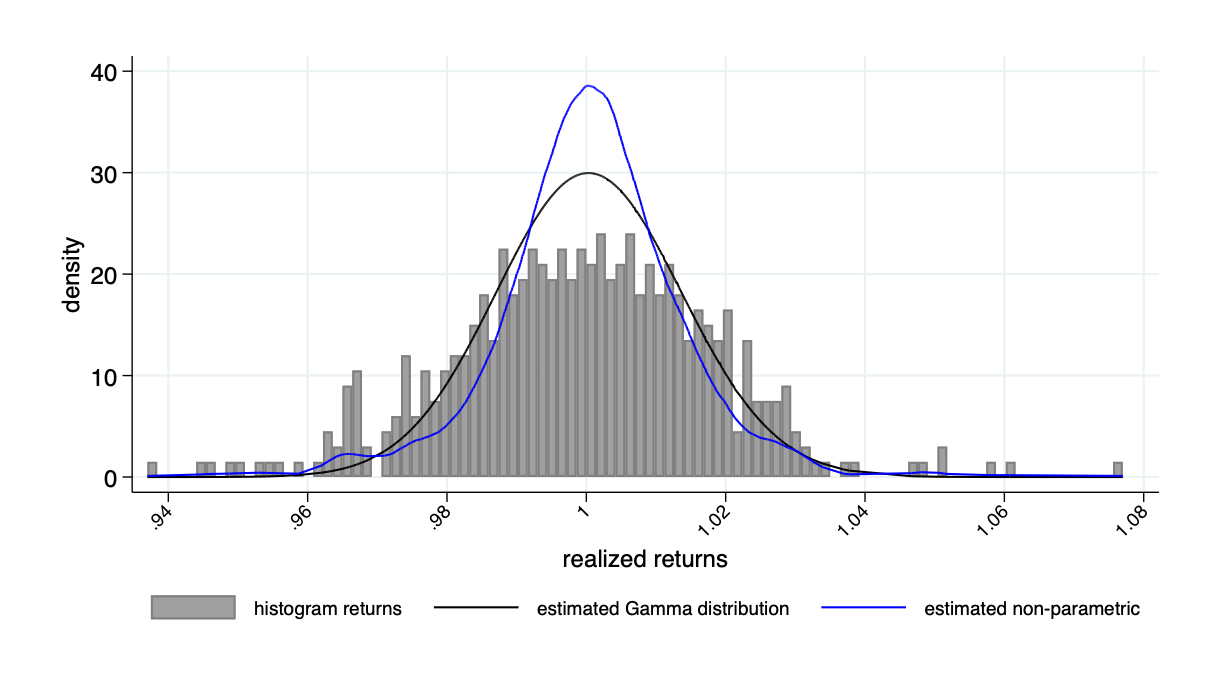

Return distribution example: Tesla

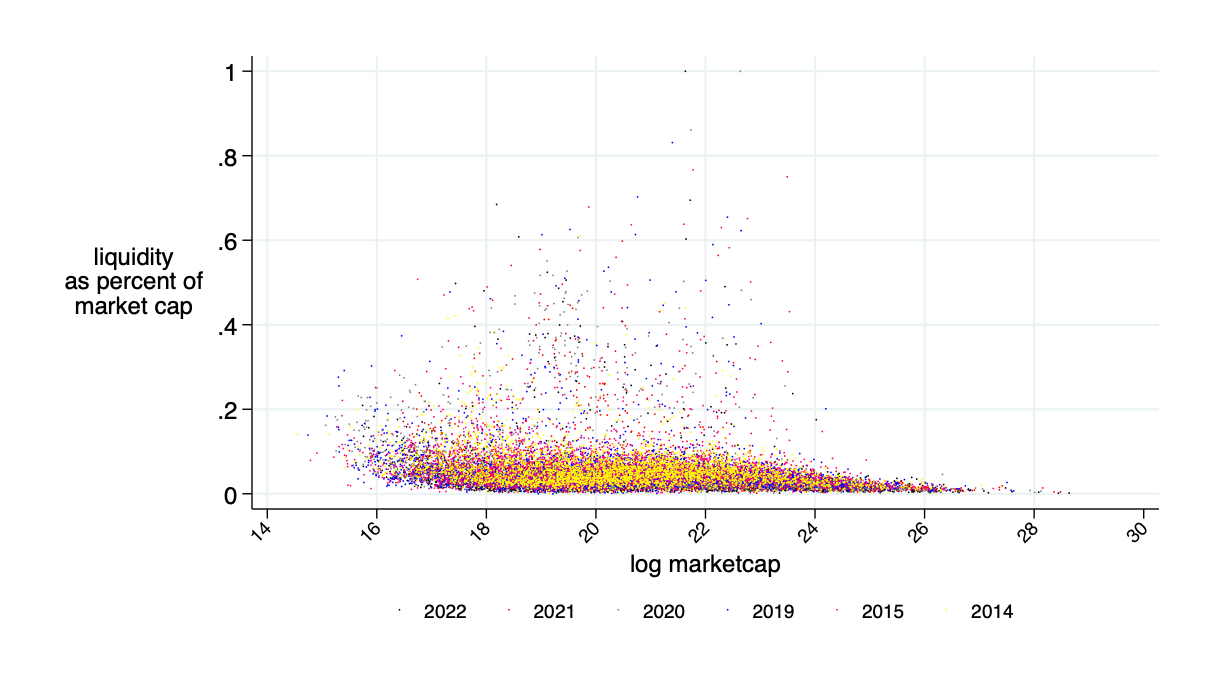

\(\bar{\alpha}\approx 2\%\)

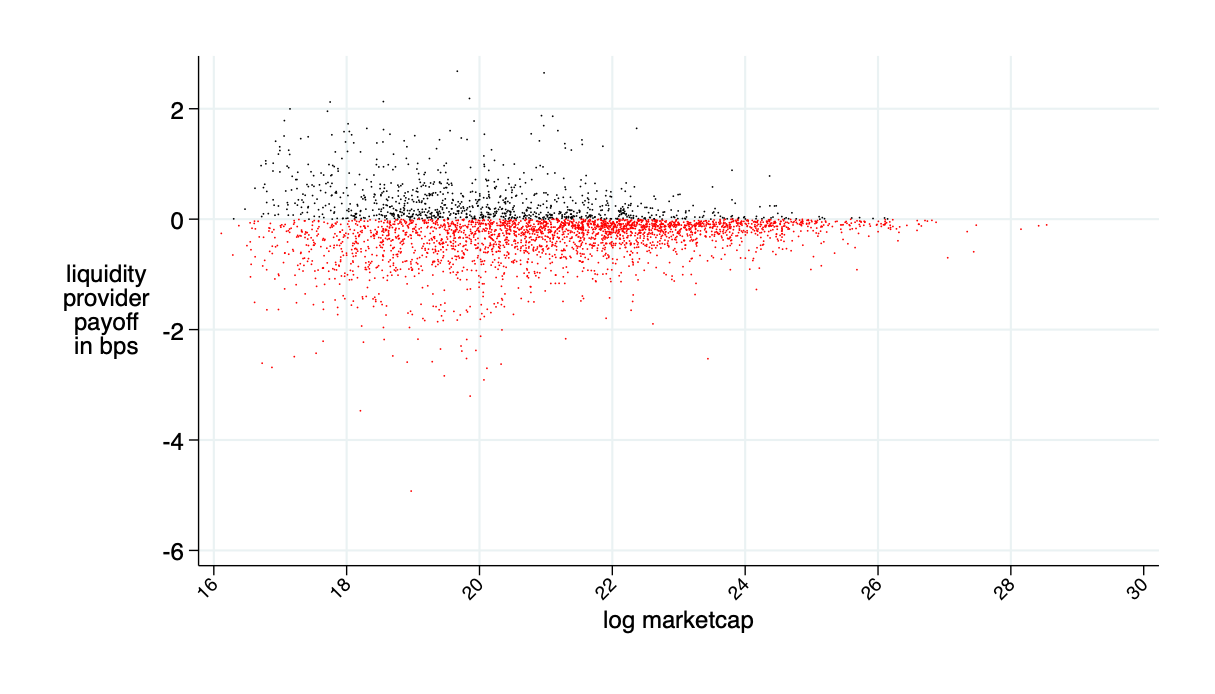

almost break even on average (average loss 0.2bps \(\approx0\))

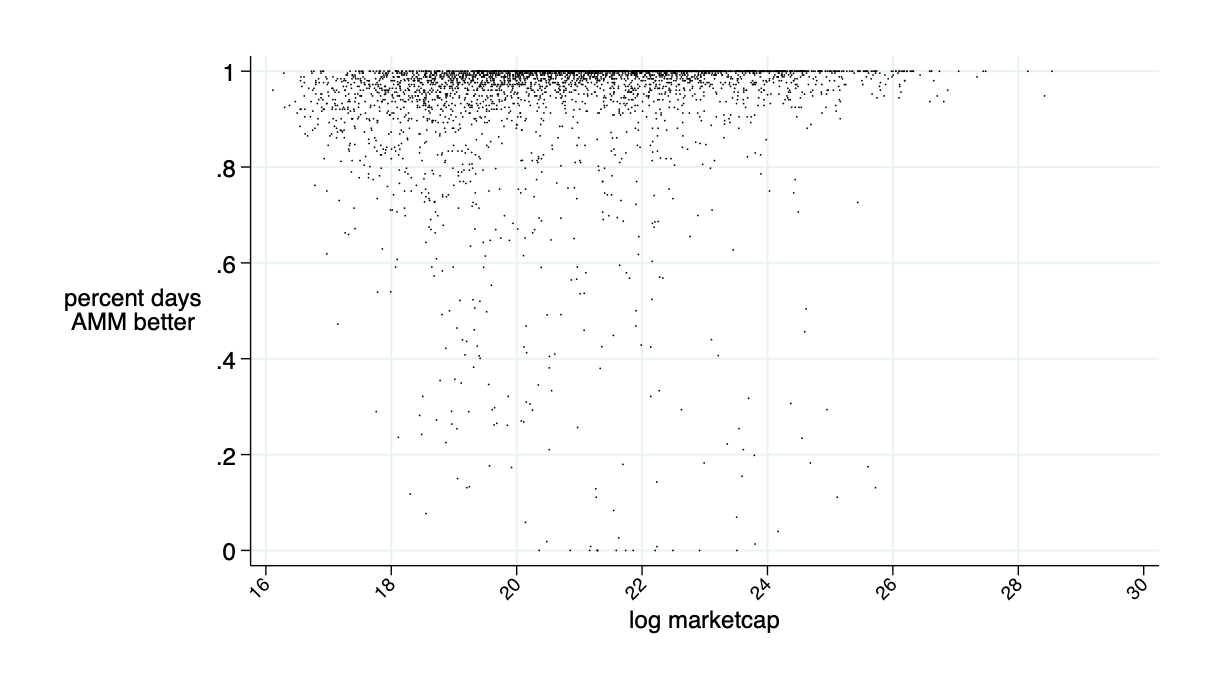

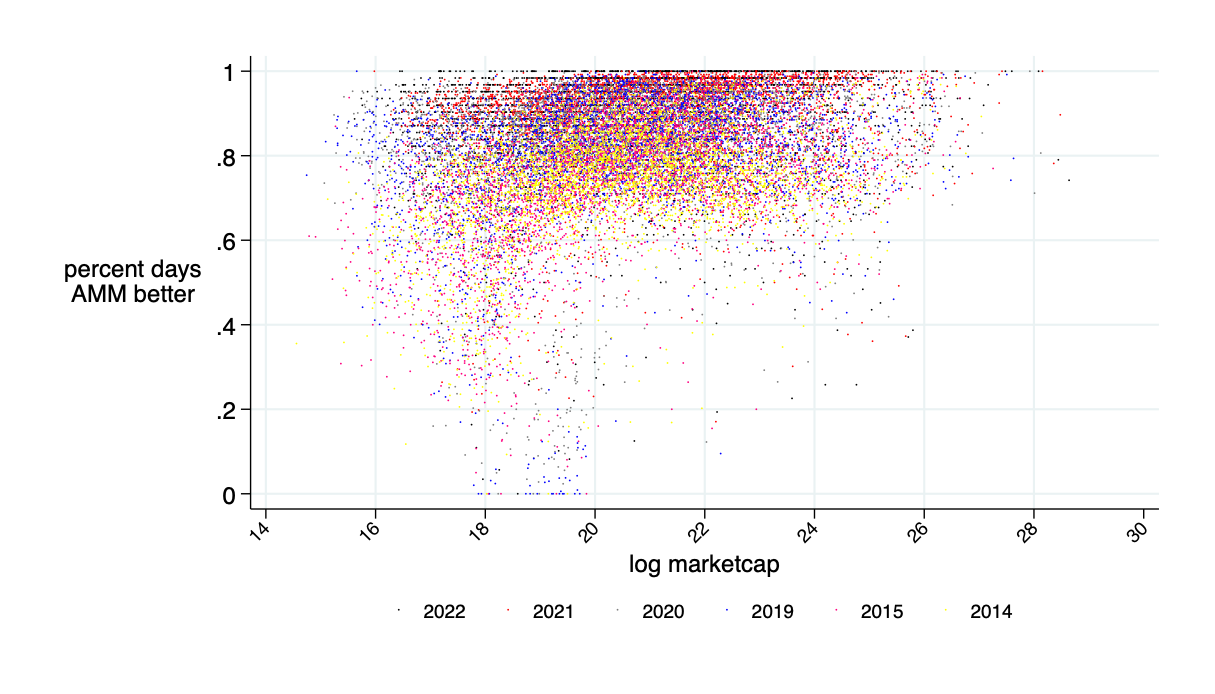

average: 94% of days AMM is better than LOB

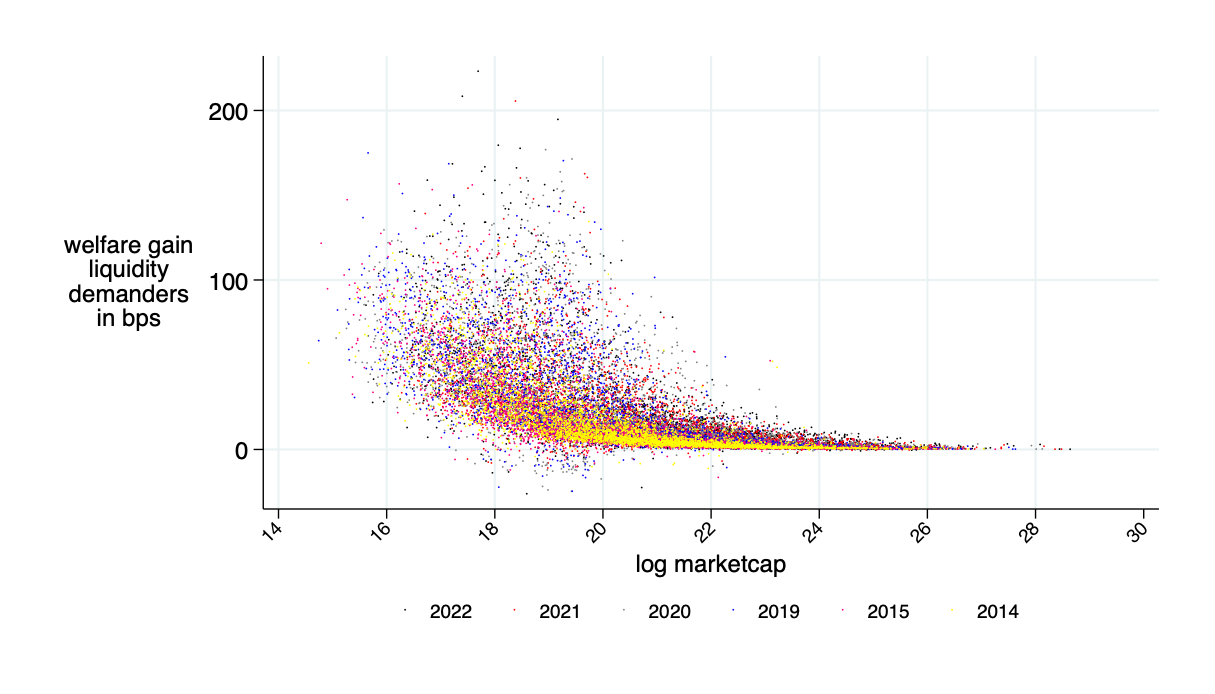

average savings: 16 bps

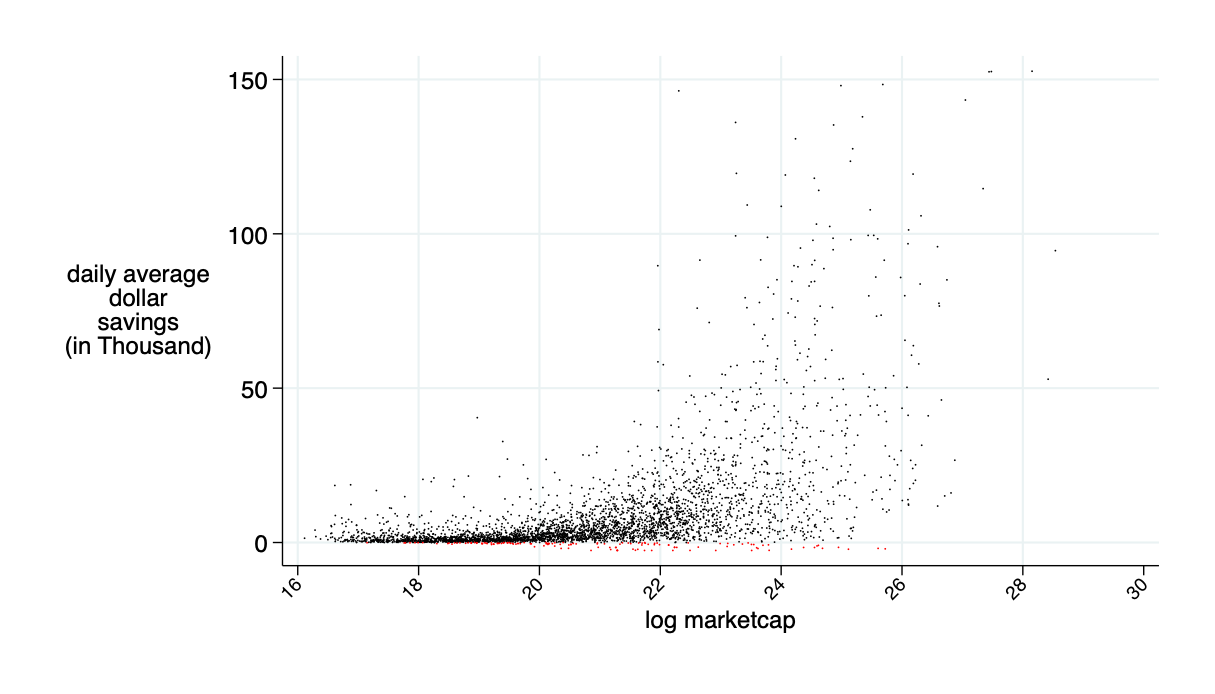

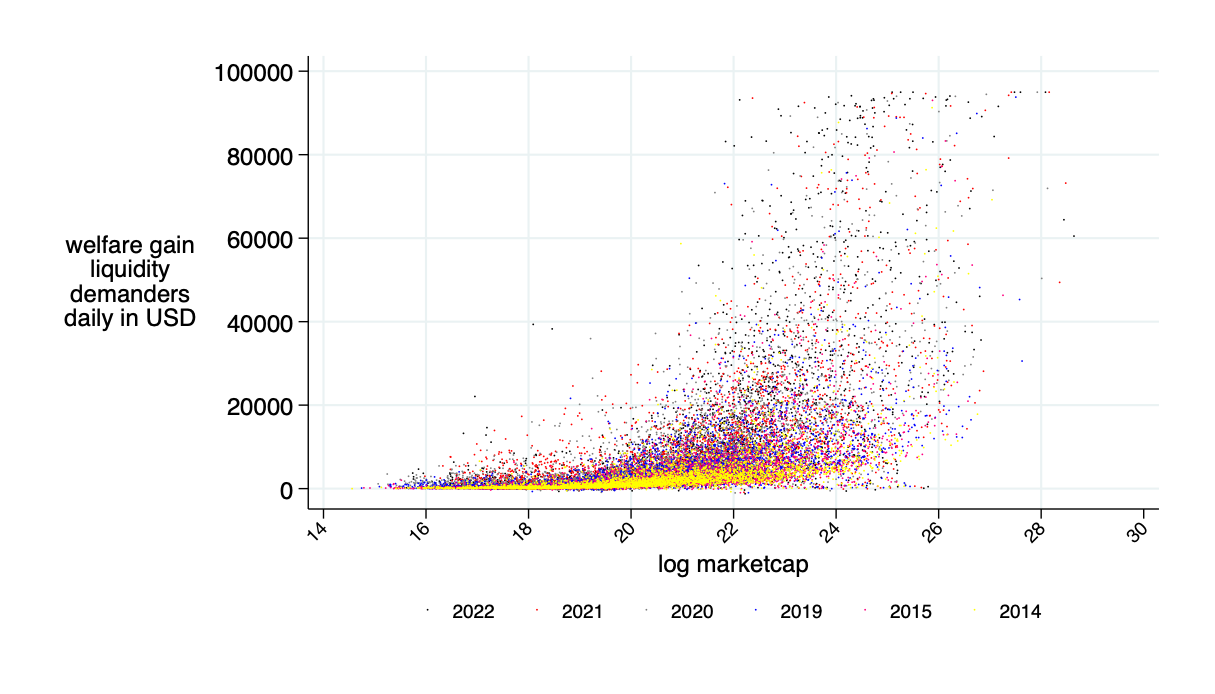

average daily: $9.5K

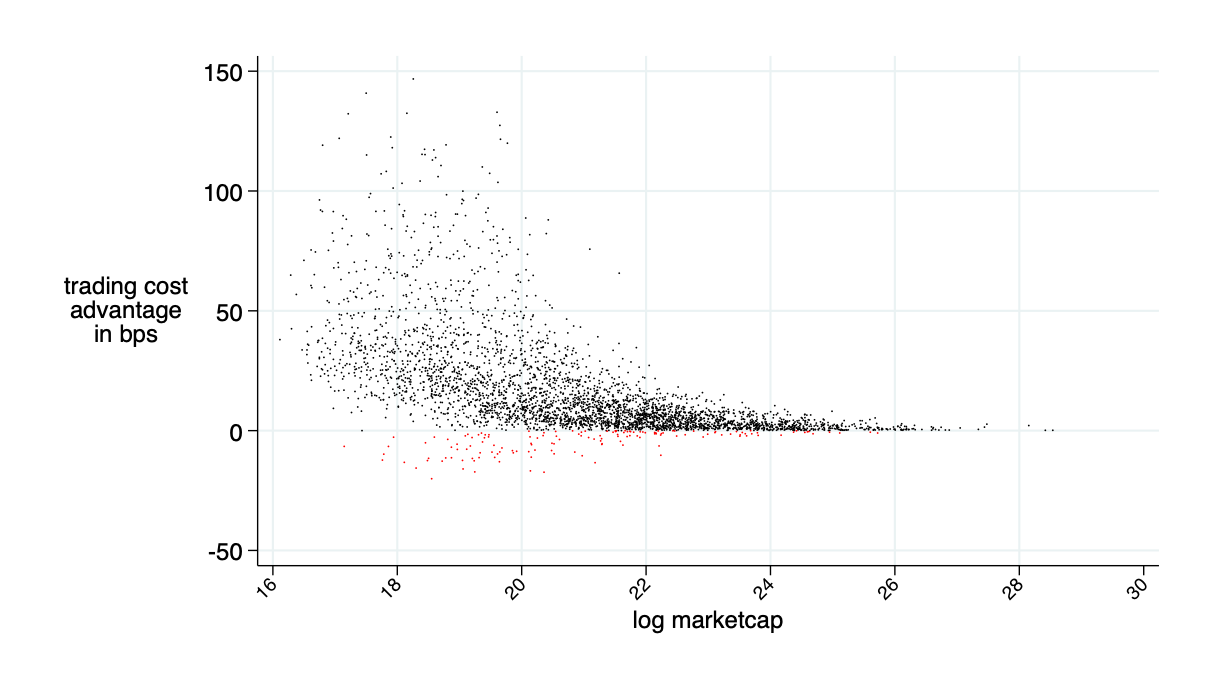

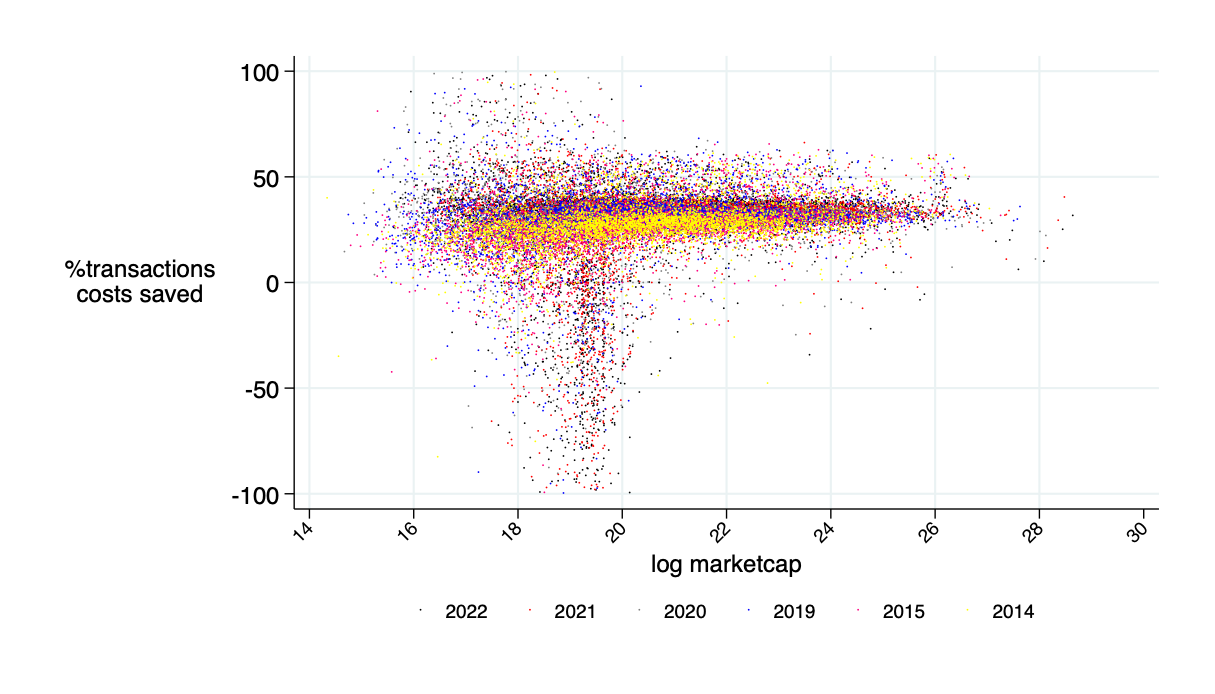

saves around 45% of transaction costs (measured in bid-ask spread)

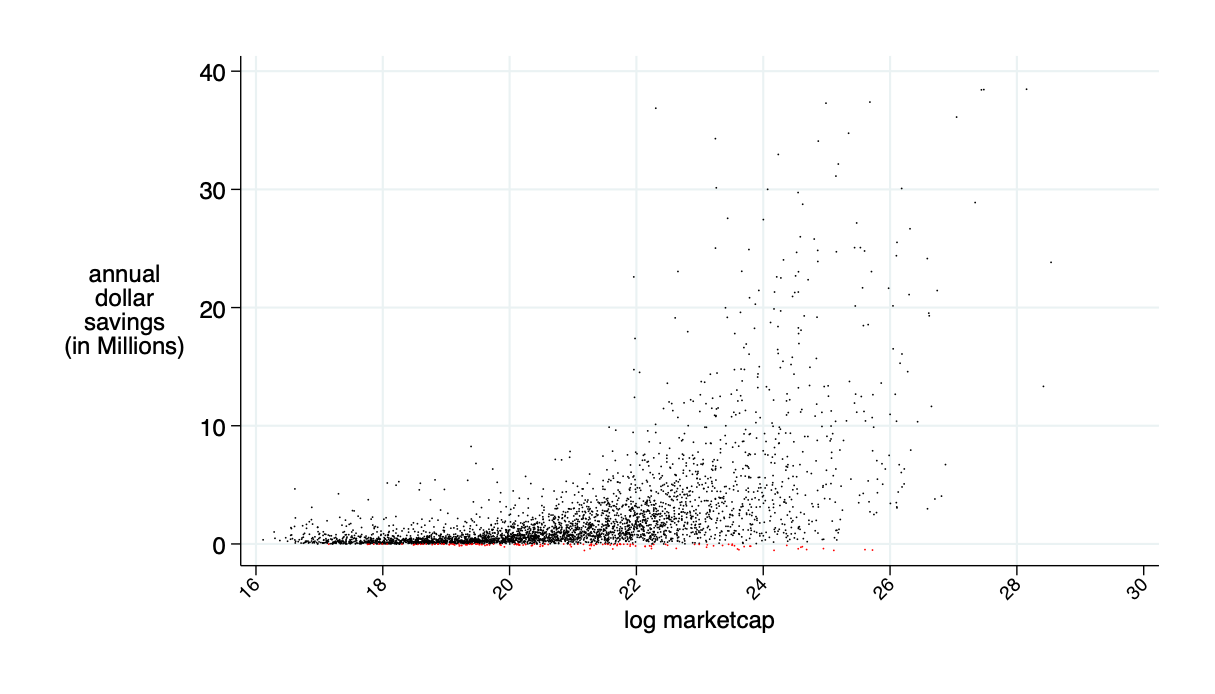

average annual saving: $2.4 million

Optimally Designed AMMs with

"ad hoc" one-day backward look

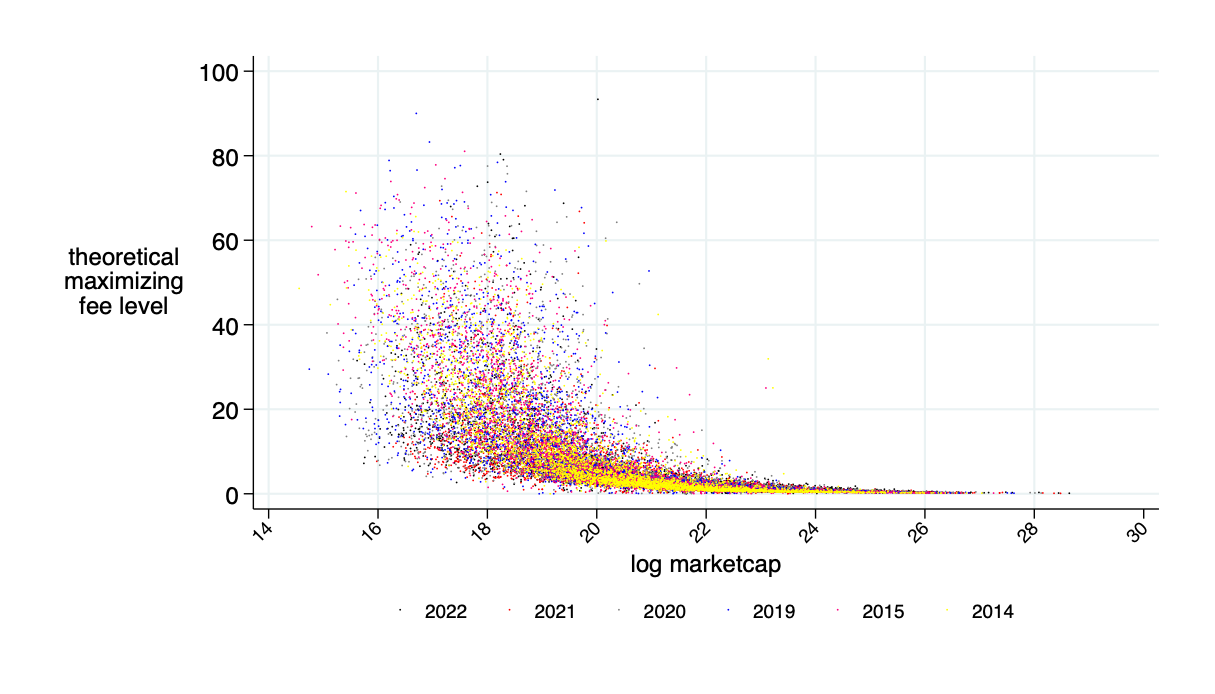

Optimal fee \(F^\pi\)

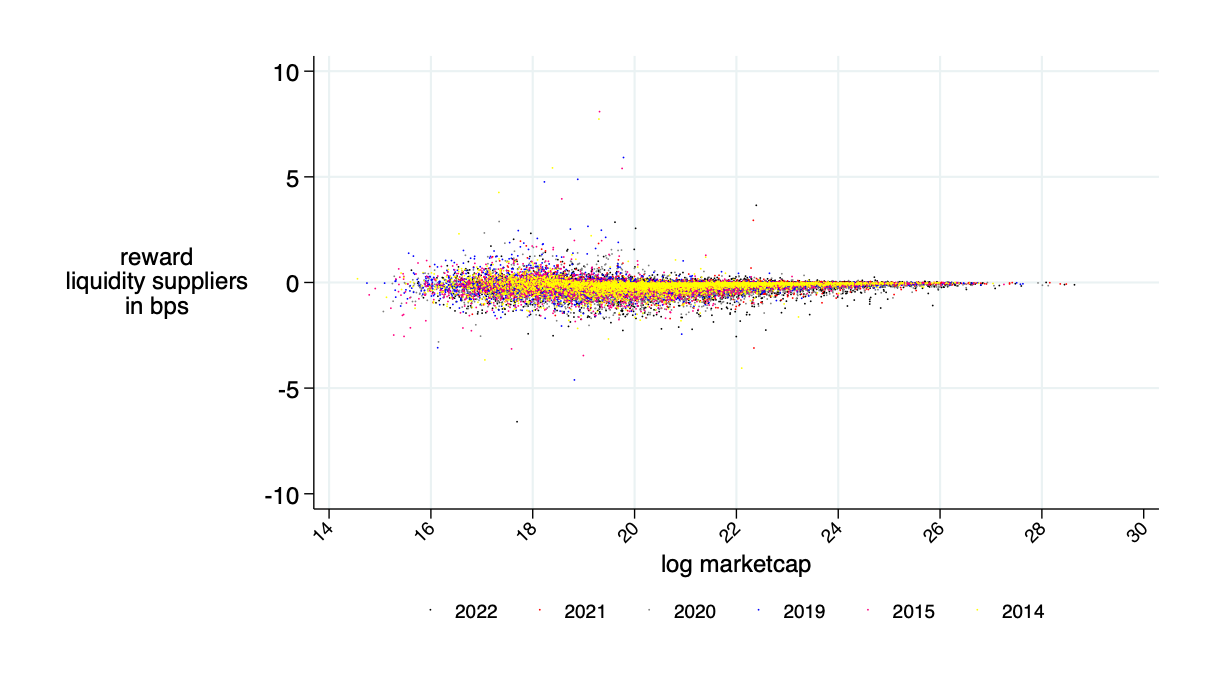

average benefits liquidity provider in bps (average=0)

Insight: Theory is OK - LP's about break even

\(\overline{\alpha}\) for \(F=F^\pi\)

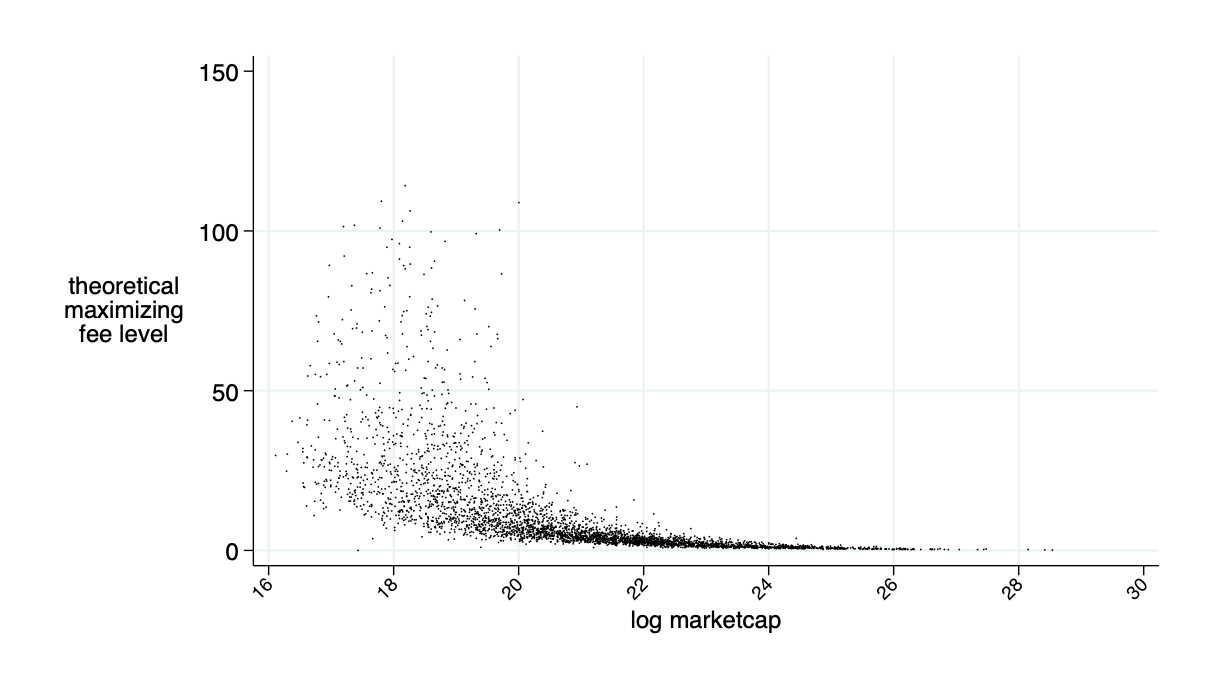

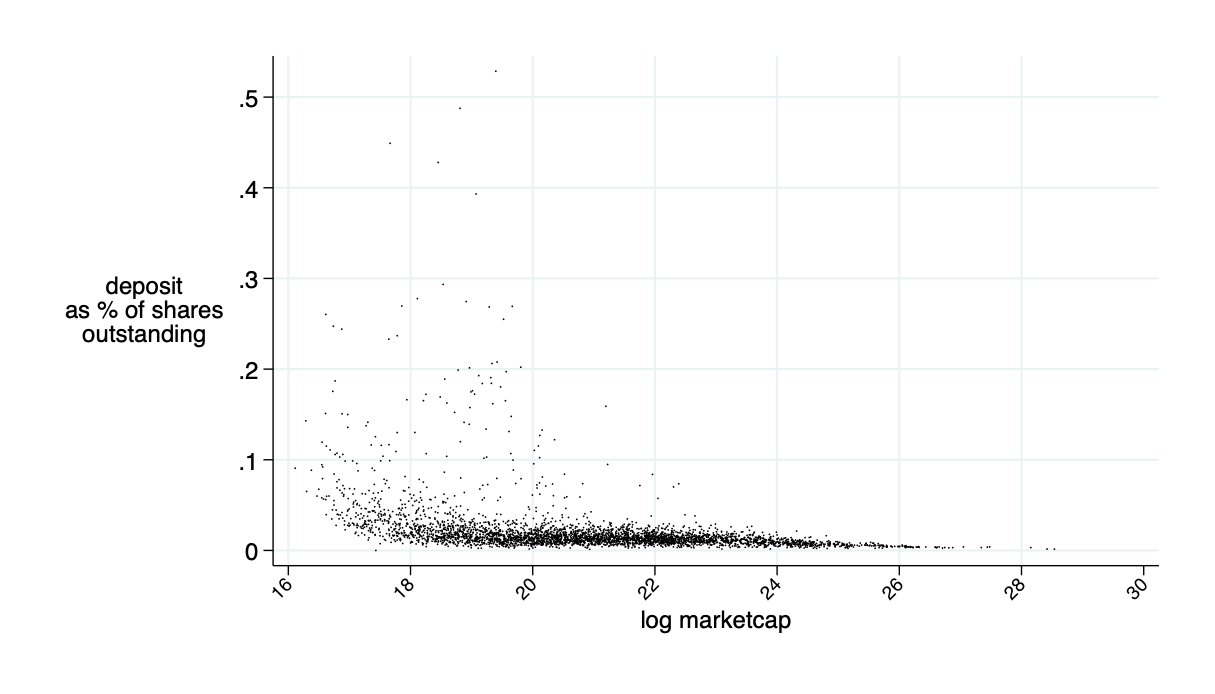

Need about 10% of market cap in liquidity deposits to make this work

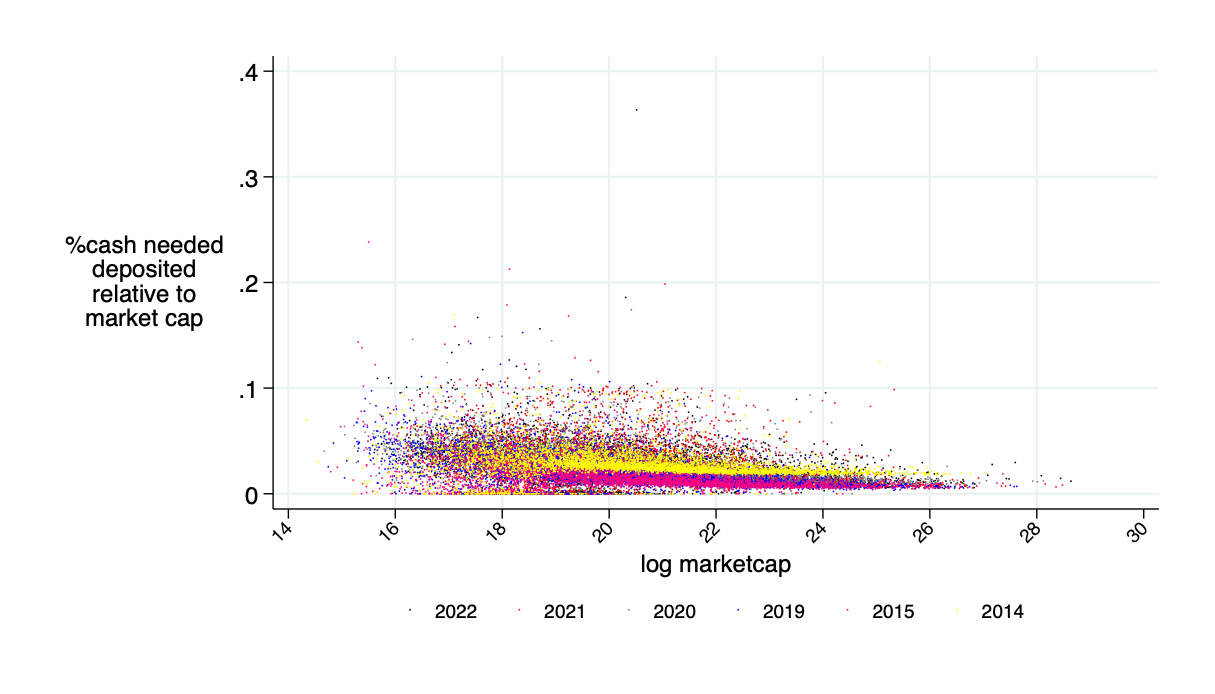

actually needed cash as fraction of "headline" amount

Only need about 5% of the 10% marketcap amount in cash

AMMs are better on about 85% of trading days

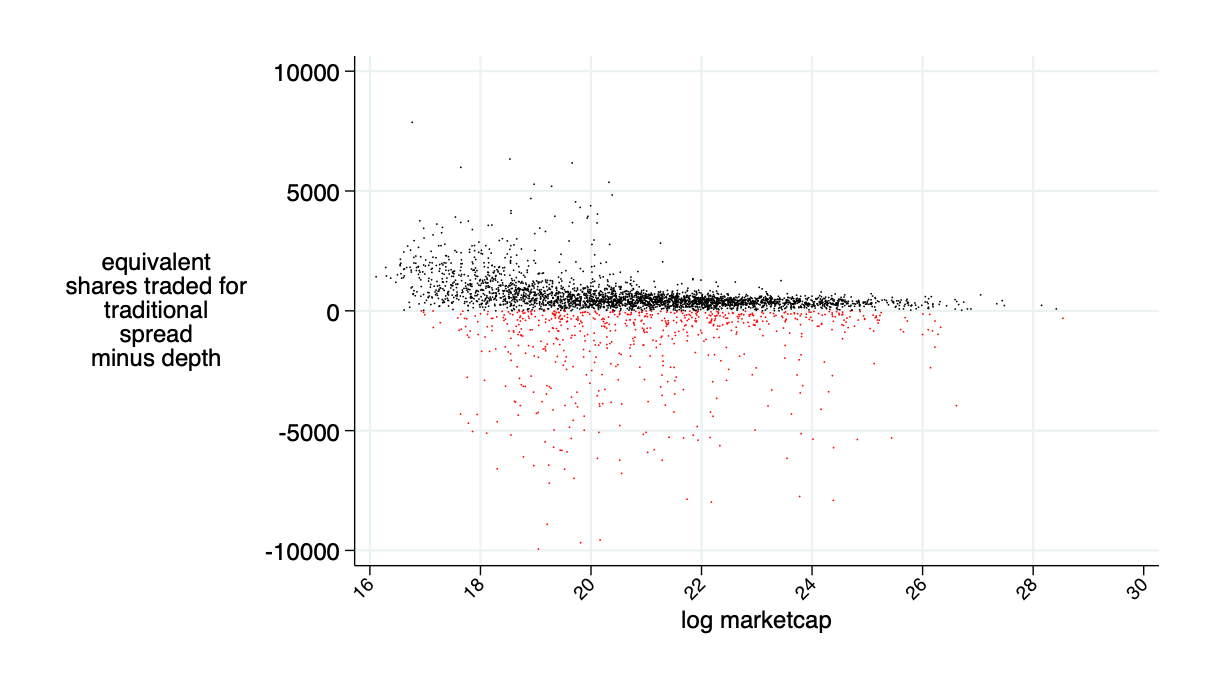

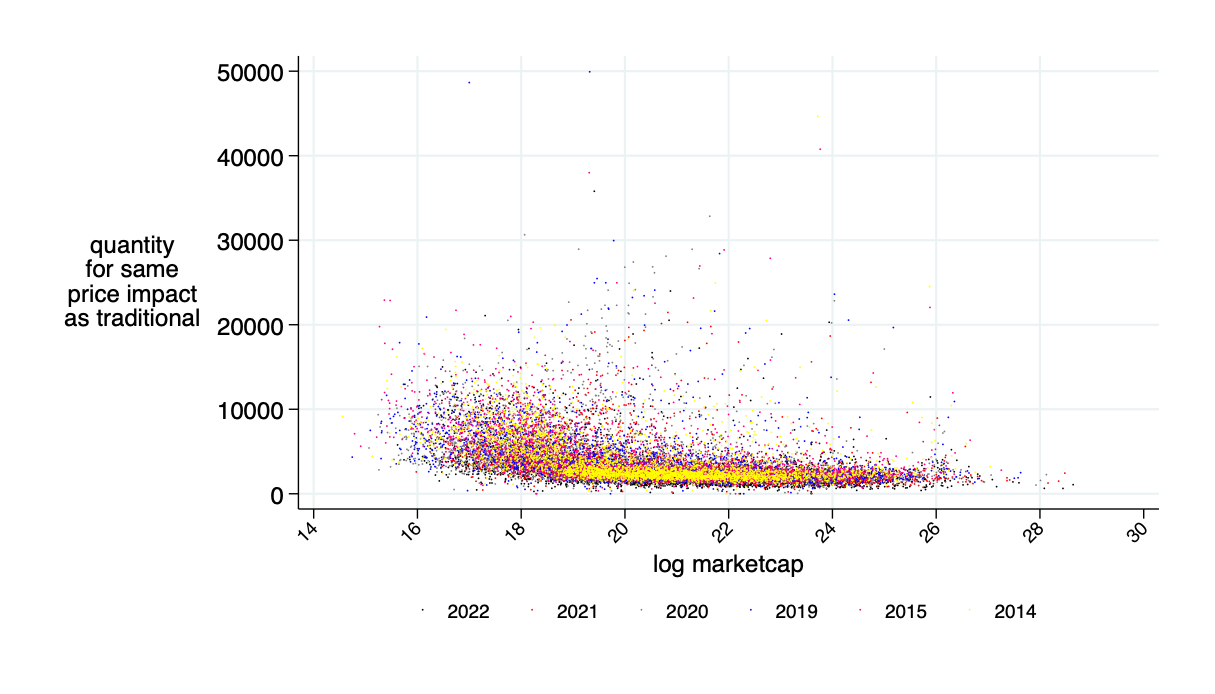

quoted spread minus AMM price impact minus AMM fee (all measured in bps)

relative savings: what fraction of transactions costs would an AMM save? \(\to\) about 30%

theoretical annual savings in transactions costs is about $15B

Sidebar: Capital Requirement

Deposit Requirements

Literature

AMM Literature: a booming field

Lehar and Parlour (2021): for many parametric configurations, investors prefer AMMs over the limit order market.

Aoyagi and Ito (2021): co-existence of a centralized exchange and an automated market maker; informed traders react non-monotonically to changes in the risky asset’s volatility

Capponi and Jia (2021): price volatility \(\to\) welfare of AMM LPs; conditions for a breakdown of liquidity supply in the automated system; more convex pricing \(\to\) lower arbitrage rents & less trading.

Capponi, Jia, and Wang (2022): decision problems of validators, traders, and MEV bots under the Flashbots protocol.

Park (2021): properties and conceptual challenges for AMM pricing functions

Milionis, Moallemi, Roughgarden, and Zhang (2022): dynamic impermanent loss analysis for under constant product pricing.

Hasbrouck, Rivera, and Saleh (2022): higher fee \(\Rightarrow\) higher volume

Empirics:

Lehar and Parlour (2021): price discovery better on AMMs

Barbon and Ranaldo (2022): compare the liquidity CEX and DEX; argue that DEX prices are less efficient.

The Bigger Picture and Last Words

Summary

@financeUTM

andreas.park@rotman.utoronto.ca

slides.com/ap248

sites.google.com/site/parkandreas/

youtube.com/user/andreaspark2812/

By Andreas Park

Oxford-MAN presentation