Andreas Park PRO

Professor of Finance at UofT

Instructor: Andreas Park

Date: November 2, 2019, 10:15-11:45

2019 Rotman – Master in Finance

Financial Innovation

Partnerships

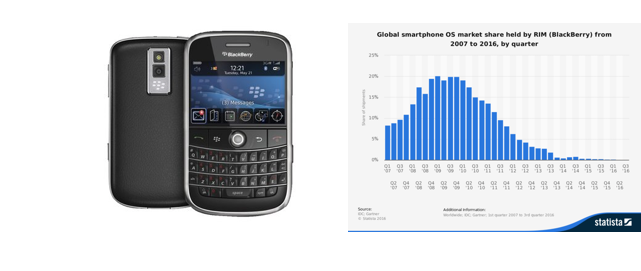

Nokia's market shares for devices:

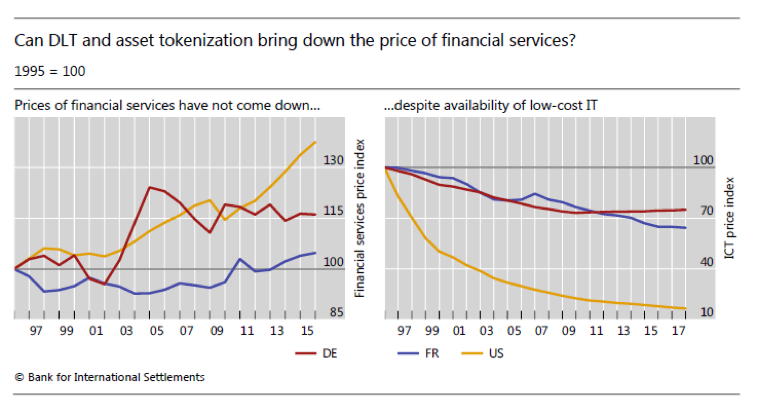

What happened and can it happen to banks?

What did they pay for?

What do people value?

If banks move all data into "the cloud," why do we need banks?

Siloed banks

Cloud computing and cloud storage

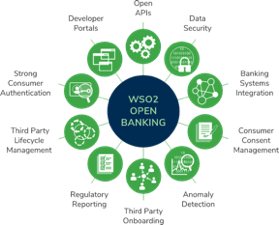

Open banking and open data

The past (and the present?)

The present and near future

3-5 years in the future

5-10 years in the future

Platforms?

Banks?

Tech firms?

Change ledger entry locally

Sue's bank transfers from Sue's account to Bob's bank's account

Bob's bank transfers from its account to Bob's account

Sue's bank transfers from Sue's account to its own account

Bob's bank transfers from its account to Bob's account

Central Bank

Central bank transfers from Sue's bank's account to Bob's bank's account

Sue's bank transfers from Sue's account to its own account

Bob's bank transfers from its account to Bob's account

use the Swift network of correspondent banks

very complex

many parties

lots of frictions and points of failure

very expensive

Cryptography: only Sue can spend her money

Problem: double-spending

How can we trust that

Sue wants to sell ABX

Bob wants to buy ABX

sell order

buy order

Clearing House

Stock Exchange

Broker

Broker

3rd party tech

custodian

custodian

record beneficial ownership

central bank for payment

\(t\)

\(t\)

\(t\)

\(t\)

\(t\)

\(t\)

\(t\)

\(t\)

\(t\)

\(t\)

\(t\)

\(x\)

\(t\)

\(t\)

\(t\)

\(t\)

\(t\)

\(x\)

\(t,t,x\)

\(t,t,x\)

\(t,t,t\)

\(x\)

\(y\)

\(z\)

\(y\)

\(x\)

\(z\)

\(y\)

\(x\)

\(z\)

\(x,y.z\)

\(x,y,z\)

\(x,y,z\)

Equilibrium

Blockchain requirement

= 00000xd4we...

= 00000xd4we...

= 00000xd4we...

consensus is reached if hash starts with right number of leading zeros

Contains transaction from Bob to Alice

Question: Can Bob rewrite history?

Where to add a new block B7?

Contains transaction from Bob to Alice

Bob wants to undo the transaction by rewriting history with B6

Bob's objective

What does it take?

How does Proof of Work prevent this?

Back of the envelope calculation

Double spend attack prevention

Basic idea of competitive equilibrium

aggregate mining cost = aggregate reward

Double spending attack

condition that prevents it

(Chiu & Koeppl RFS 2018)

Who gets to update?

Can a higher body prevent

transactions?

Can the past be altered?

consensus

immutability

censorship resistence

open to anyone

no one can be excluded

past cannot be changed

high visibility of transactions

open-access eco-system

slow governance

privacy only at a cost

joint control and governance

straightforward KYC and AML

tech support

transaction secrecy simpler

rely on corporate development

compliance with law (reversion)

can keep competition out

store of value?

unit of account?

method of exchange?

store of value?

unit of account?

method of exchange?

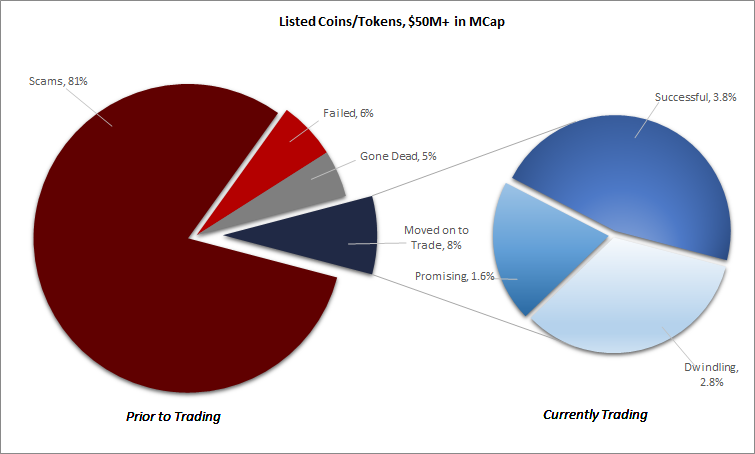

funding figures from Nov 2018; source: blockchain.com

issued by a consortium of firms (e.g., Facebook, Mastercard) and not for profits (Creative Destruction Lab)

each coin will be backed by a basket of SIX fiat currencies

idea is conceptually similar to IMF Special Drawing Rights (pegged to USD, EUR, YEN, GBP, YUAN)

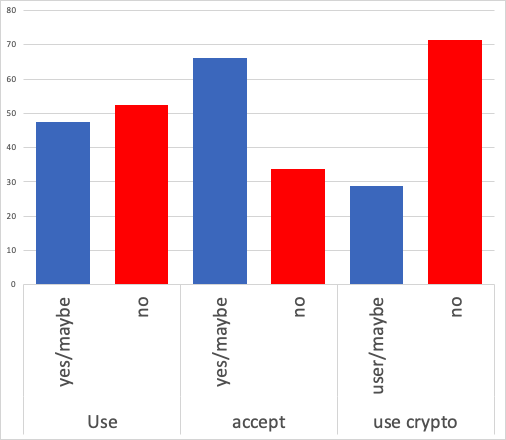

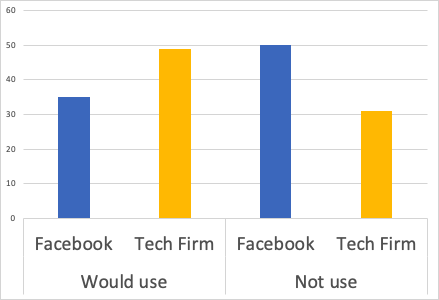

Would you use Libra/Money issue by Tech Firm?

If we ask explicitly for Facebook vs Tech Firm

Scaled to yes/maybe/no. About 20% say: "Need more info"

moving value (remittances)

digital money: real-time settlement, reduced reserves

tokenization of assets

automization of contract payments

securitization

systems and infrastructure reorganization

digital identity

new forms of financial contracts, assets, and forms of financing

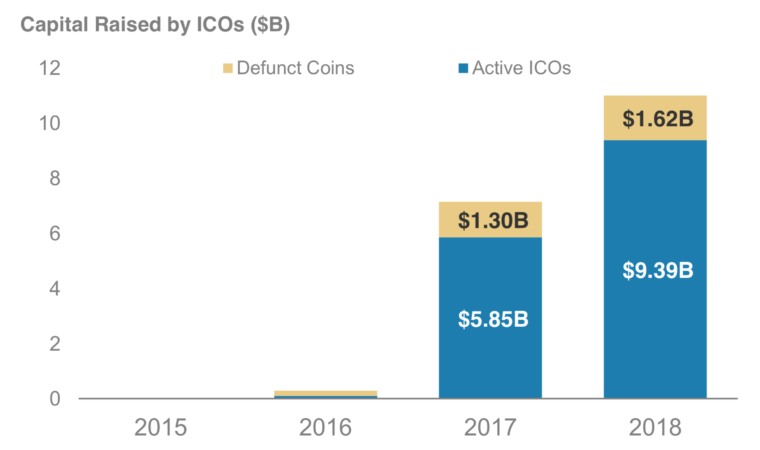

Data: coinschedule

for comparison: total size of

Toronto Stock Exchange: $2,200B

Toronto Venture Exchange: $41B

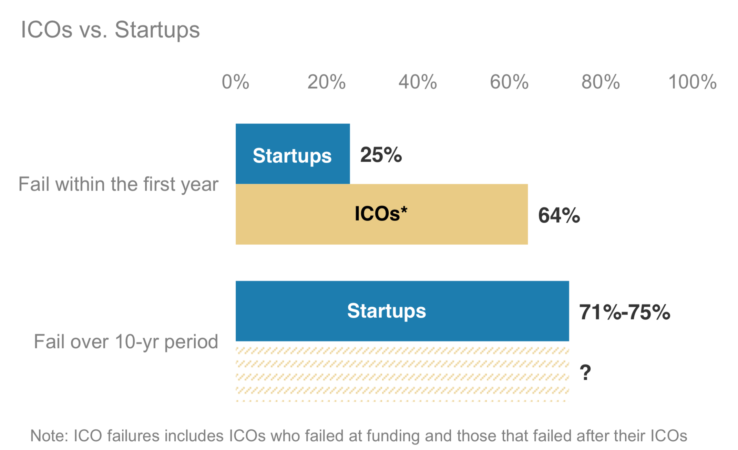

Source: Tokendata

Source: Satis Group LLC

Source: Morgan Stanley (Nov 2018) “Update: Bitcoin, Cryptocurrencies and Blockchain”

Source: Tokendata

Lessons?

can finance projects that otherwise would find no debt or equity funding

enable network effects and new business opportunities

allows entrepreneurs to extract more surplus

can finance projects that otherwise would find no debt or equity funding

Exchange

Internalizer

Wholeseller

Darkpool

Investor

Venue

Broker

Settlement

Investor

Venue

Settlement

On chain

Technology

Legal/Regulation

Economic functions

interoperability

cybersecurity and privacy

functionality

scalability

smart contract features and verification

space constraints

interoperability

scalability

space constraints:

Does the law have to change to accommodate new tech? If so, how? What's dated, what's not?

Legal setup of a platform: what rules can, should, and must a platform establish? What regulations are necessary?

How can token design and the law be married?

What is the economic impact of "tokenizing everything"?

How will it affect investments and investment banking?

Which business opportunities will it enable?

What do tokens and "alternative money" mean for payments?

blockchain is a transformative technology, but won't be used in practice overnight

many conceptual and technological challenges remain, but there are already various areas of application

legal, regulatory, and competitive changes are needed and then the opportunities are endless ...

it will open up the banking world further, foster international competition, and change how we pay and exchange value

My view: business development will happen in private/semi-public space; strong increase in recent activity; no more testing but re-engineering of processes.

@financeUTM

andreas.park@rotman.utoronto.ca

slides.com/ap248

sites.google.com/site/parkandreas/

youtube.com/user/andreaspark2812/

By Andreas Park

This is the slide deck that I used for my presentation in the 2019 MFin FInancial Innovation course on November 2.