Andreas Park PRO

Professor of Finance at UofT

Instructor: Andreas Park

Rotman – Master in Financial Risk Management

Financial Innovation

Retail

Institutional

Pro-Traders

Exchanges

Wholesellers

Dark pools

Broker Internalizations

Exchanges

Wholesellers

Dark pools

Broker Internalizations

(

(

Retail

Institutional

Pro-Traders

Rule: must send to exchange with best price

Exchange

Wholeseller

market order

limit order

In Europe: no best price obligation

Exchange

Dark pools

Type 2: "borrow" broker-dealer system

Type 1: licenced broker-dealer

risk control

You commonly don't access the market directly.

Brokers take many decisions but they are bound by regulations.

Critical: markets are formally linked by best-price rules.

A glimpse of overall infrastructure

Sue wants to sell ABX

Bob wants to buy ABX

sell order

buy order

Clearing House

Stock Exchange

Broker

Broker

3rd party tech

custodian

custodian

record beneficial ownership

central bank for payment

Retail, Institutions, and Pro-Traders are indistiguishable

not clear whether and which institutions are active

Exchanges

Dark pools

Smart On-chain contracts

Exchanges

Smart Contract

Order Driven

Market Maker

Exchanges

Smart On-chain contracts

Settle on the blockchain for digital "assets"

Wire transfer for fiat

BTC/USD

ask: 7,600

bid: 7,550

BTC/USD

ask: 7,500

bid: 7,450

buy low

sell high

BTC/USD

ask: 7,600

bid: 7,550

BTC/USD

ask: 7,500

bid: 7,450

buy BTC

sell BTC

move BTC to Kraken

Wire: free*; 1-5 days

Credit card: 3.5%

trading fee: 10-25 bps

flat fee in BTC \(\approx\) $4-8

\(\approx\) 10-60 minutes

trading fee: 0-26 bps

35 USD + 0.125%

($5 if >$50,000)

1-3 business days;

possible other fees/delays

Some exchanges allow short selling

Regulated Exchanges

Derivatives trade mostly offshore! Unregulated(?!)

August 2016

https://www.forbes.com/sites/jasonbrett/2019/12/19/congress-considers-federal-crypto-regulators-in-new-cryptocurrency-act-of-2020/#7ddcdfd65fcd

Idea:

Source: Letter to Janet Yellen, Chair of the Financial Stability Oversight Council (FSOC) https://www.warren.senate.gov/imo/media/doc/FSOC%20Crypto%20Letter%2007.26.2021.pdf

“[…] the need for a coordinated and cohesive regulatory strategy to mitigate the growing risks that cryptocurrencies pose to the financial system”

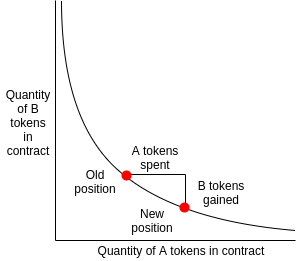

How do you set the price?

Price mechanism:

Prices

invariant \(k=4\times4=16\)

Instantaneous exchange rate:

1 = 1

Contract deposit:

sell 4 DAI for USDC

what price will therefore be quoted?

how many USDC?

Problem: large "slippage" (or price impact)

establish and sell a new token

a

b

c

d

e

f

g

However: although front-running is annoying, it is only a concern if it is intrinsically profitable.

My paper:

\(X\)

\(Y\)

normal trade: sell \(x\) \(\to\) get \(y'\)

\(Y-y'\)

\(X+x\)

front-running:

\(Y-y'-y''\)

\(X+2x\)

\(y'>y''~\Rightarrow\)

front-running is intrinsically profitable

Disclaimer:

\(X\)

\(Y\)

\(Y-y'\)

\(X+x\)

\(Y-y'-y''\)

\(X+2x\)

\(y'=y''~\Rightarrow\)

front-running is not intrinsically profitable

CPAMM

canonical

Price mechanism:

Prices

front-running

transactions enter mem-pool

\(\to\) all visible there

arbitrageur make instant-swap trade at higher gas price

\(\to\) trade instead of original trade

\(to\) reverse to gain slippage from earlier trader

take three pairs (ignore that BTC is not directly on Ethereum)

BTC-DAI

ETH-BTC

ETH-DAI

\(\to\) simply connect with MetaMask (or similar wallet)

Exchange

Internalizer

Wholeseller

Darkpool

Investor

Venue

Broker

Settlement

Investor

Venue

Settlement

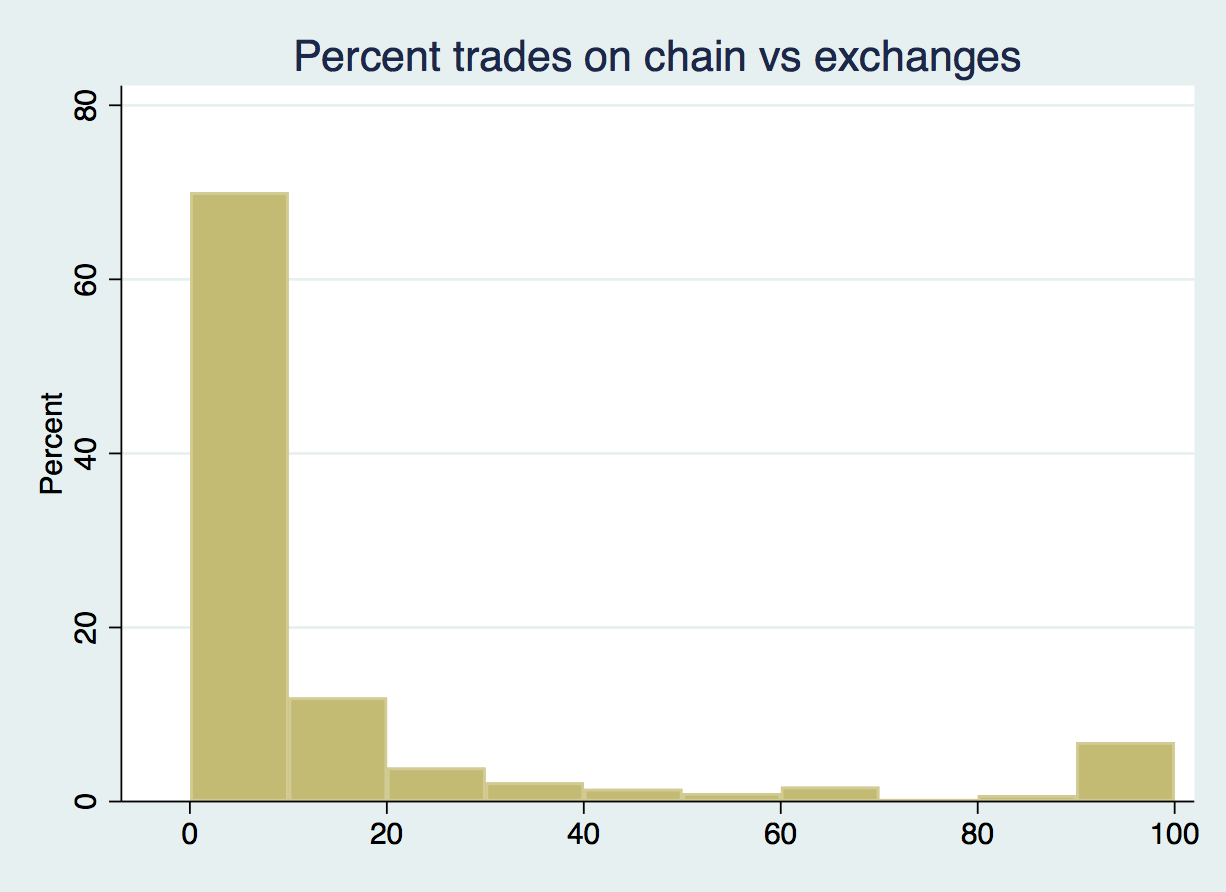

On chain

most tokens stay at exchanges and don't get settled on the blockchain

some usage tokens are "in use"

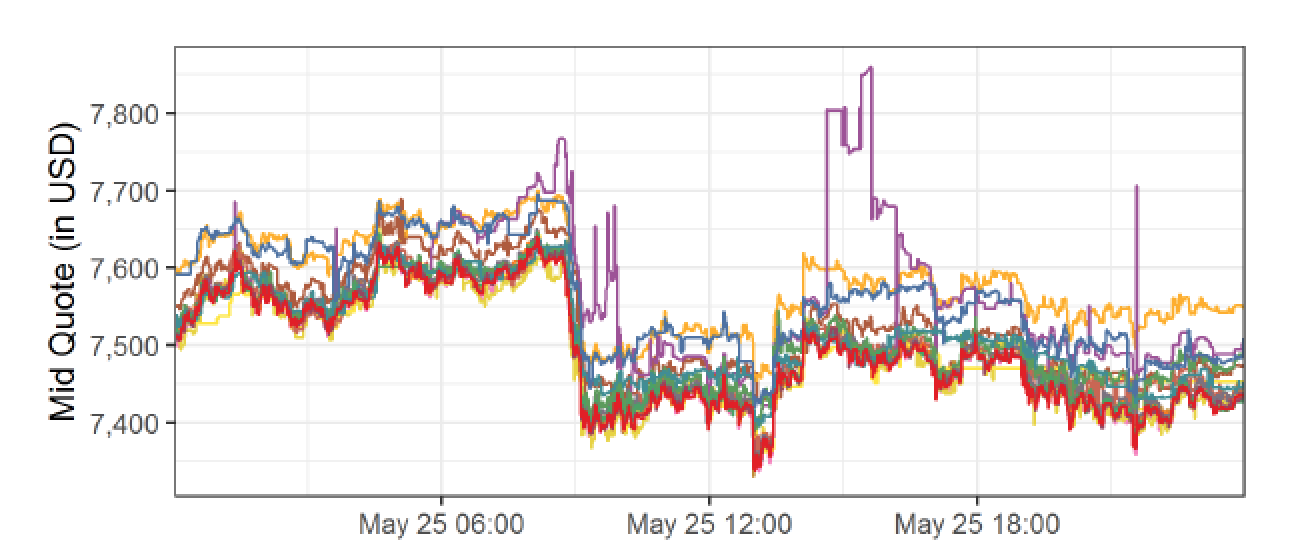

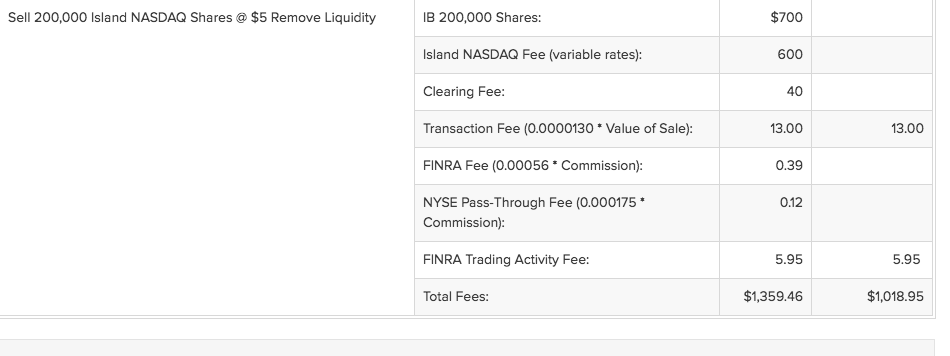

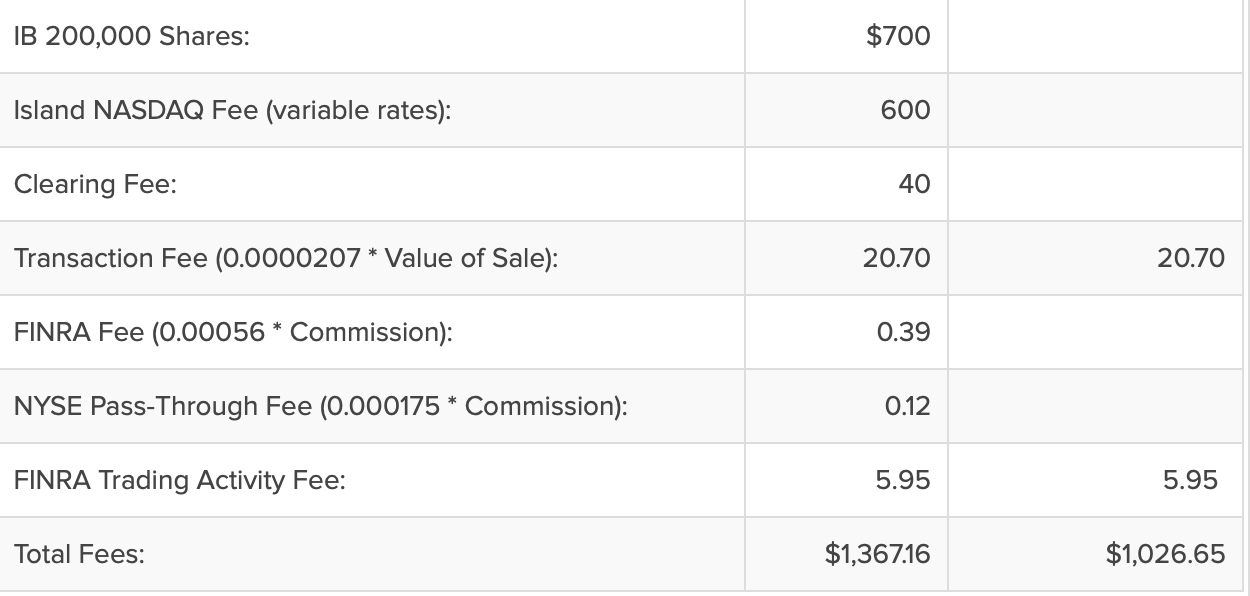

Source: Interactive Brokers

$1,000,000 market order

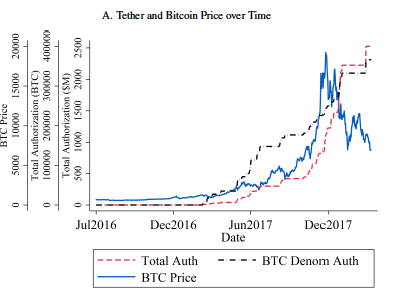

Historically: “Tether Platform currencies are 100% backed by actual fiat currency

assets in our reserve account.”

Text

Today: "The Tether Platform is fully reserved when the sum of all tethers in circulation is less than or equal to the value of our reserves."

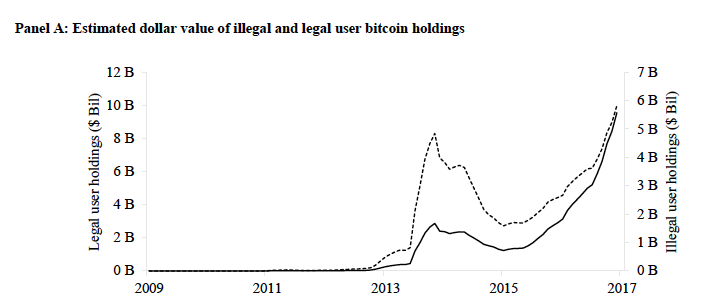

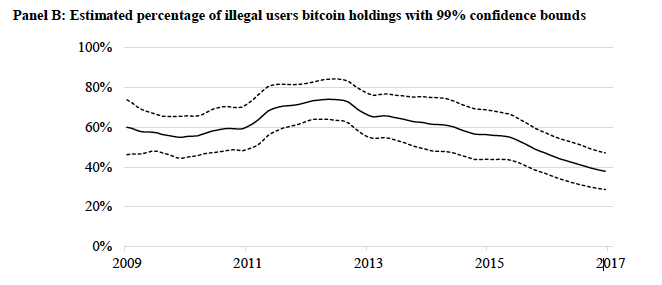

IS BITCOIN REALLY UN-TETHERED?

JOHN M. GRIFFIN and AMIN SHAMS

Journal of Finance 2020

Text

IS BITCOIN REALLY UN-TETHERED?

JOHN M. GRIFFIN and AMIN SHAMS

Journal of Finance 2020

Text

IS BITCOIN REALLY UN-TETHERED?

JOHN M. GRIFFIN and AMIN SHAMS

Journal of Finance 2020

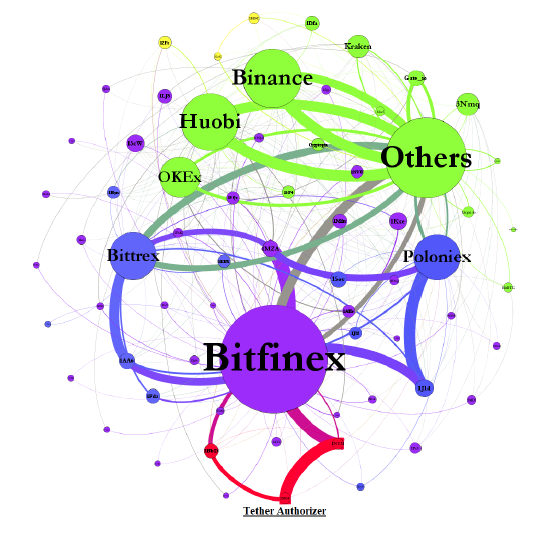

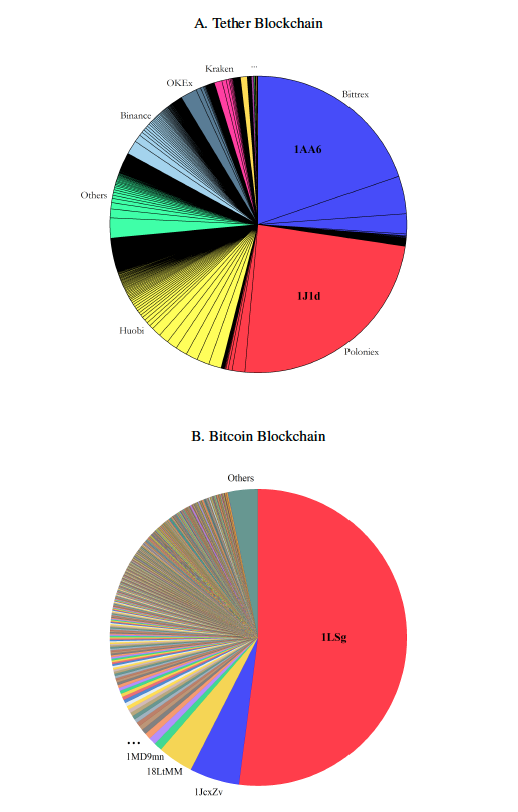

Figure 1. Aggregate Flow of Tether between Major Addresses

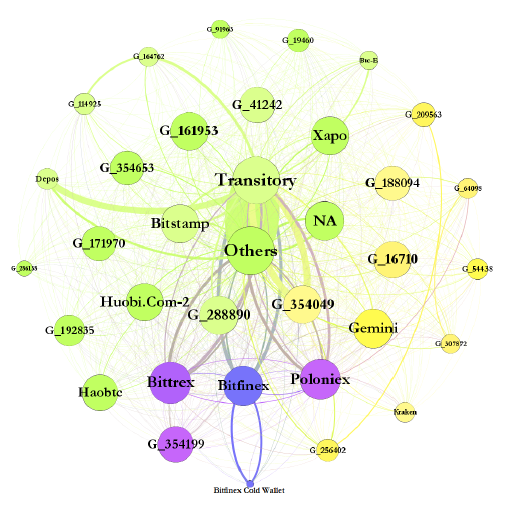

Figure 3. Aggregate Flow of Bitcoin between Major Addresses.

Top Accounts Associated with the Flow of Tether from and Bitcoin to Bitfinex

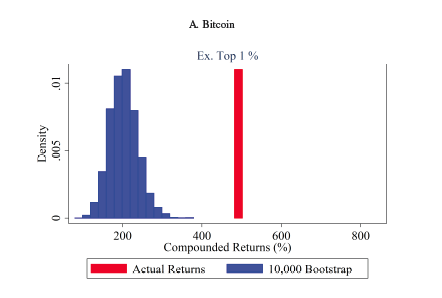

the 1% of hours with the strongest lagged Tether flow are associated with 58.8% of the Bitcoin buy-and-hold return over the period.

the "normal-times" returns

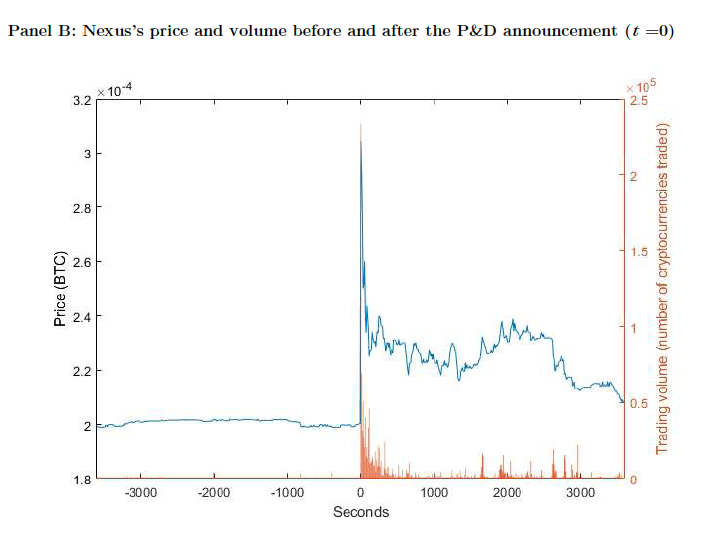

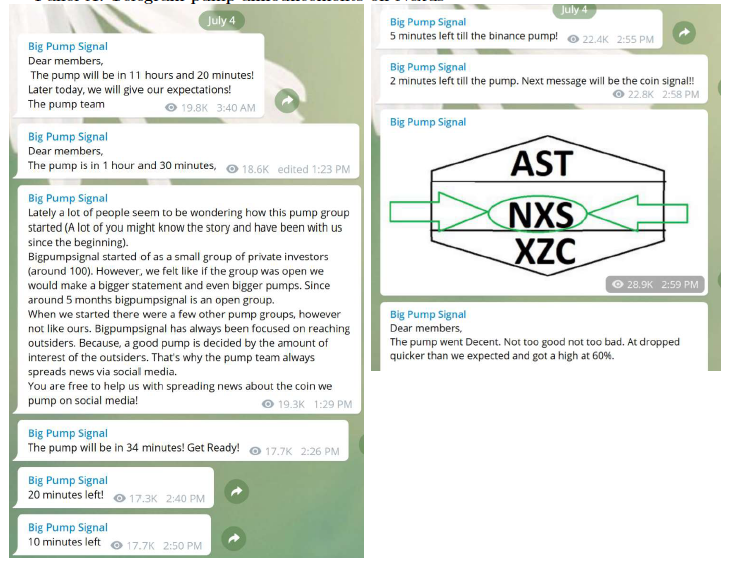

What is pump and dump?

arranged via Telegram Channels

Katya Malinova and Andreas Park

1. Multiple trading protocols are possible

User-facing exchange mask

Fully Decentralized, "OTC",

Peer-to-Peer Exchange

2. High Level of Transparency

See transactions between "addresses" (="IDs")

3. You can tell who owns what

Key: wallets/addresses = IDs but NOT = traders

Who benefits and loses under which regime?

Each period one is hit with size Q=1 liquidity shock.

Other can absorb the shock at zero cost.

Disclaimer:

Idea:

Requires a system design choice:

Repeated setting:

Front-running is punished by “grim trigger” & trade forever with small and intermediary.

Single shot:

LP always extracts all surplus (or would front-run).

Closest and native to "public" blockchains:

small traders

large trader

small traders

large trader

small traders

large trader

filled

unfilled

Opaque Single ID

Opaque Multi-ID: LP accepts

Opaque Multi-ID: LP rejects

accept offer

"target" small investors only

"target" IDs of both: large and small

front run

Result 1: There exists an equilibrium with no front-running where

provided

Result 2 (numerical): For small discount (=infrequent interaction) factors, the equilibrium with no front-running where LP accept does not exist. Then:

=> "over-trading" with intermediary

Observations

Finding 3:

For the average equilibrium stage payoffs of large traders.

Finding 4: (Numerical)

There exist parametric configurations such that large traders trade with each other at p > 0 in the multi-ID ownership setting, but their average equilibrium payoff in the opaque single-ID setting is higher.

By Andreas Park