Andreas Park PRO

Professor of Finance at UofT

OSC Academy:

A 2023 DeFi Primer

Presenter: Andreas Park

What is a Cryptocurrency?

Conceptually: What is a Blockchain?

payments

stocks, bonds, and options

swaps, CDS, MBS, CDOs

insurance contracts

A blockchain is a

What makes DeFi different from TradFi

decentralized finance =

provision of financial service functionality without the necessary involvement of a traditional financial intermediary like a bank or broker-dealer*

digital media =

provision of information service functionality without the necessary involvement of a traditional information intermediary like a publisher, library, or newagency

*my take: applies to only commoditizable services

payments network

Stock Exchange

Clearing House

custodian

custodian

beneficial ownership record

seller

buyer

Broker

Broker

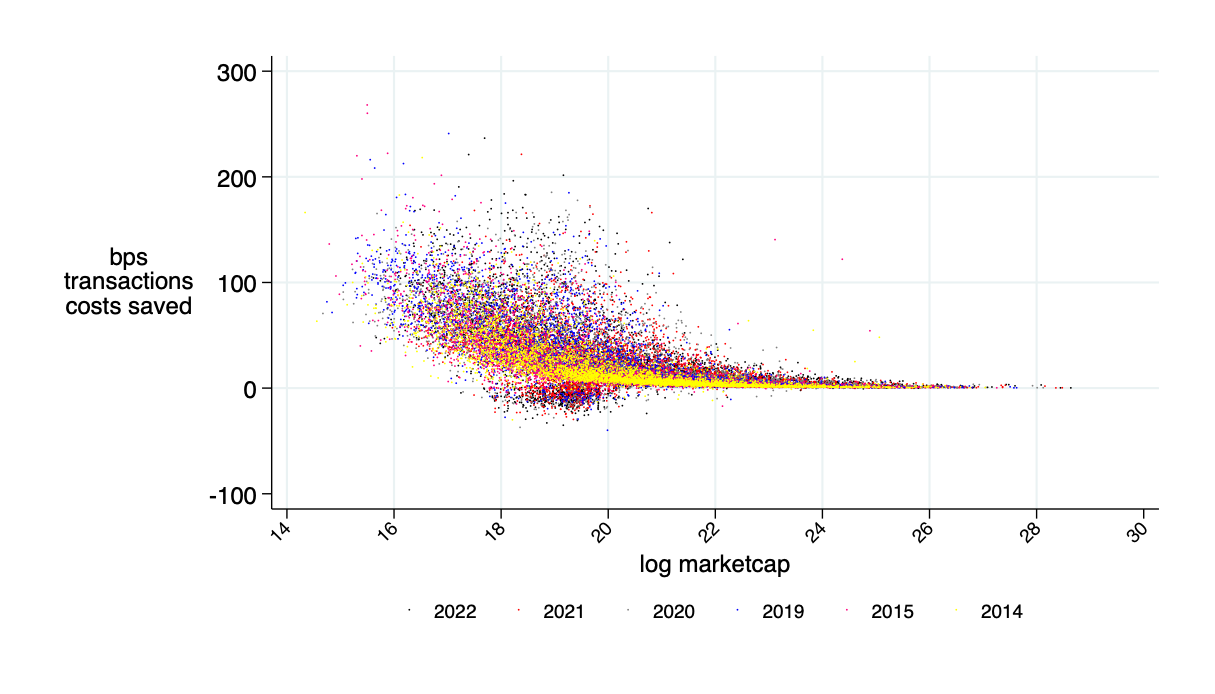

AMM Pricing

Source of savings:

Possible transaction cost savings: \(\approx\) 30%

Source: "Learning from DeFi: Would Automated Market Makers Improve Equity Trading?" working paper, Malinova & Park 2023

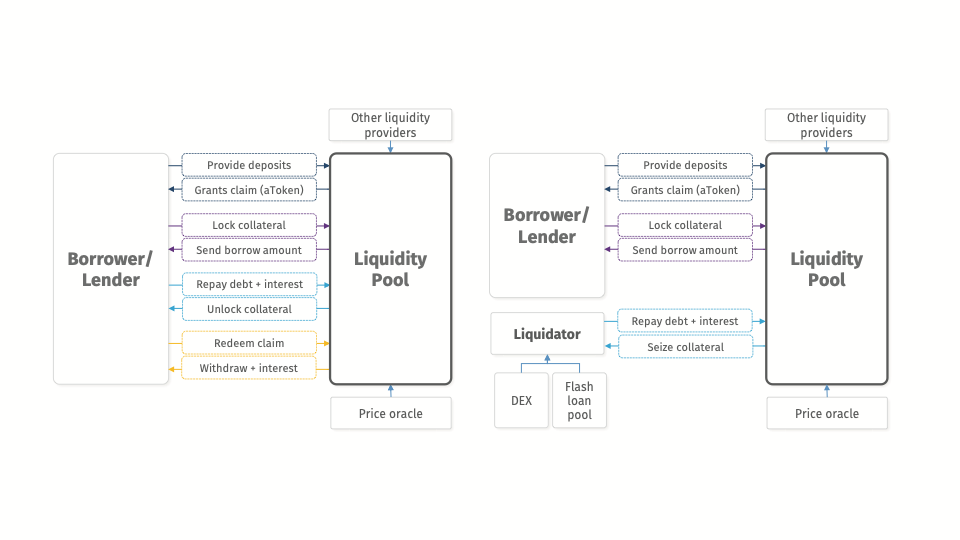

Application: Decentralized Borrowing & Lending

borrow

provide collateral

The Flow of Event: Normal Times

The Flow of Event: Collateral Liquidation

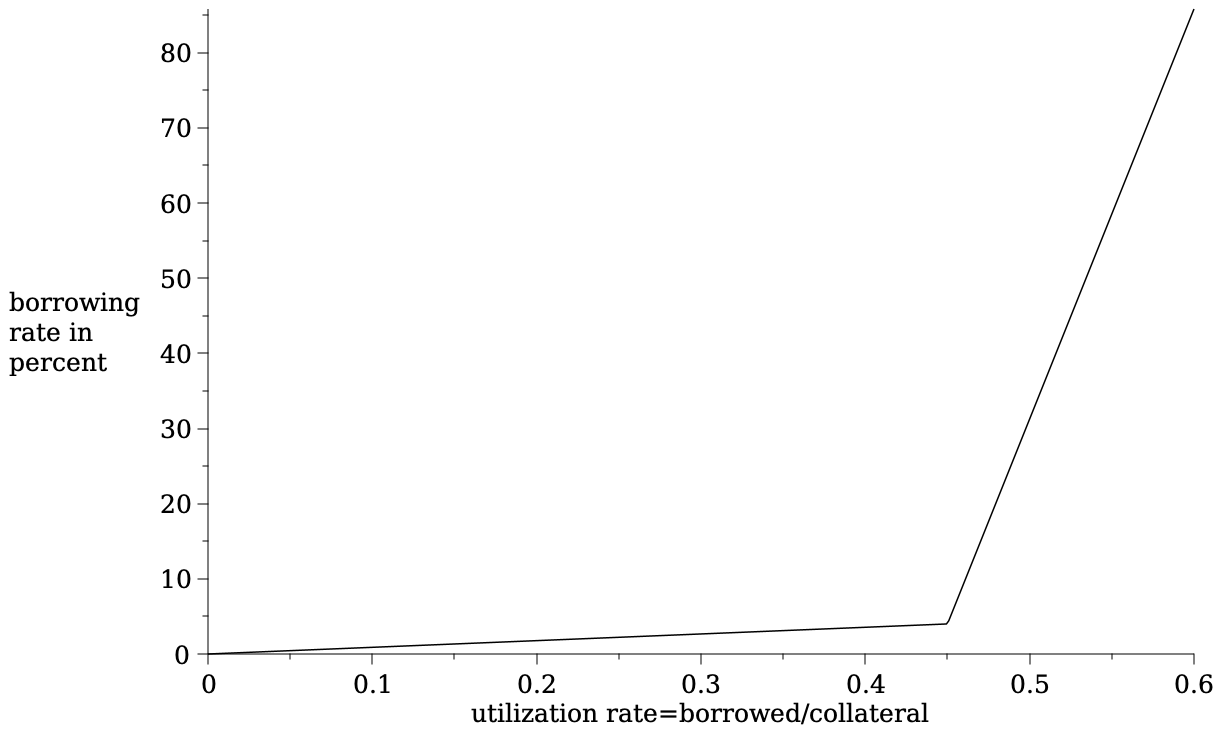

Interest rates: a function of pool usage

threshold usage rate

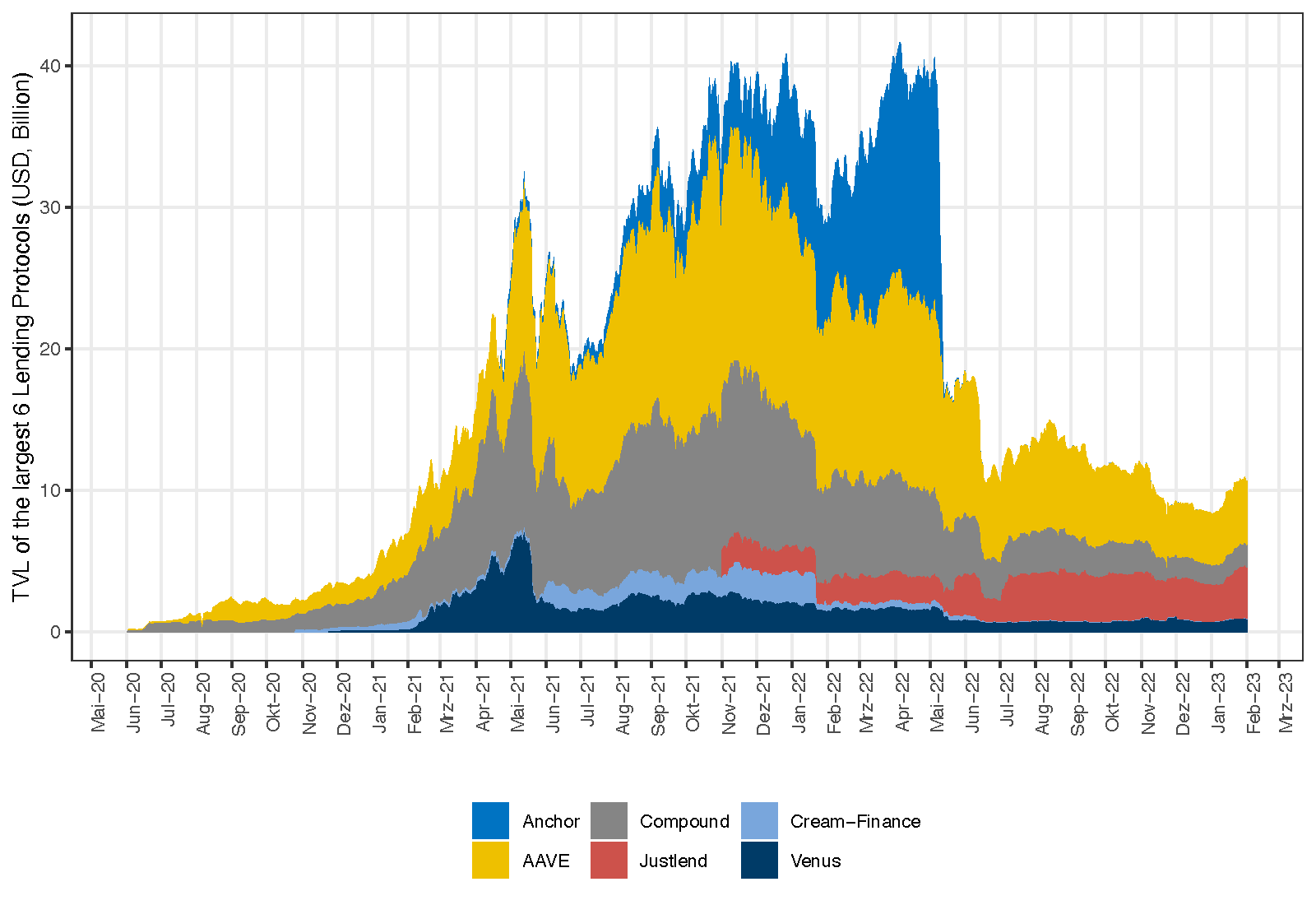

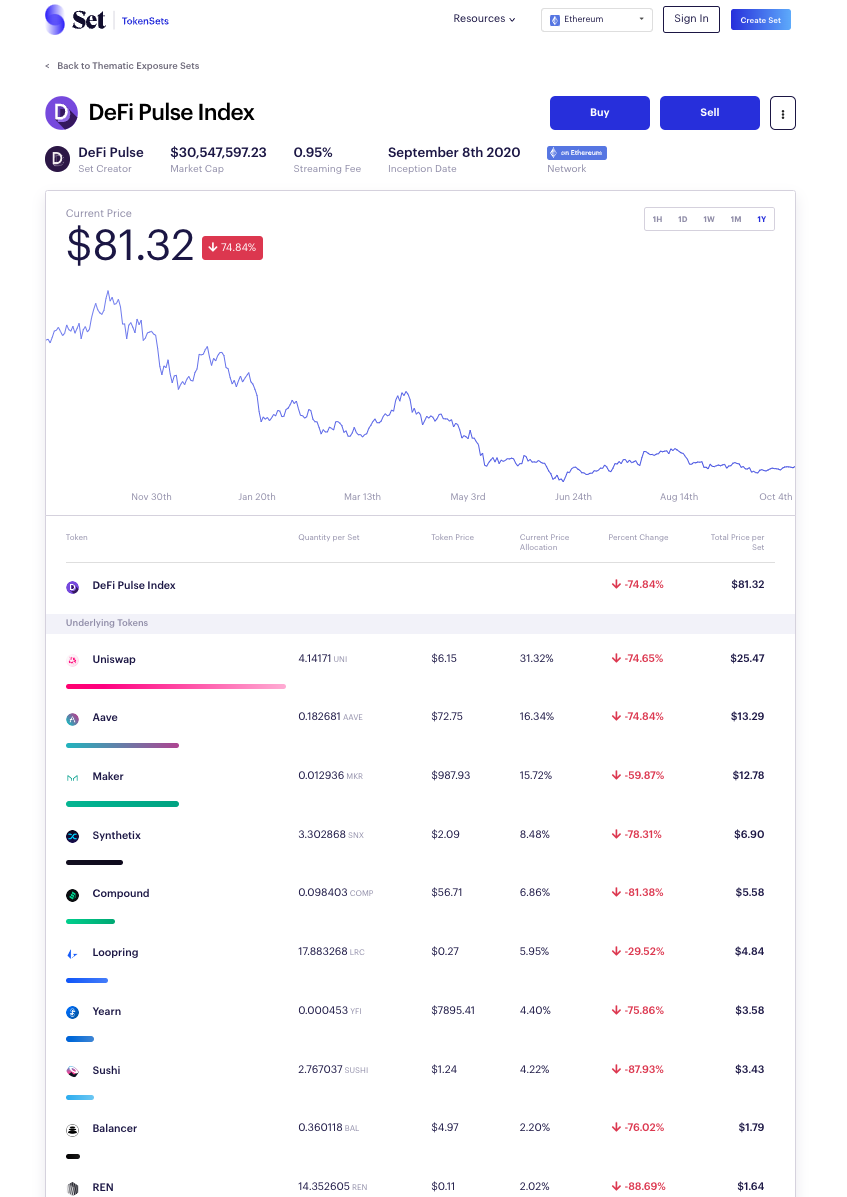

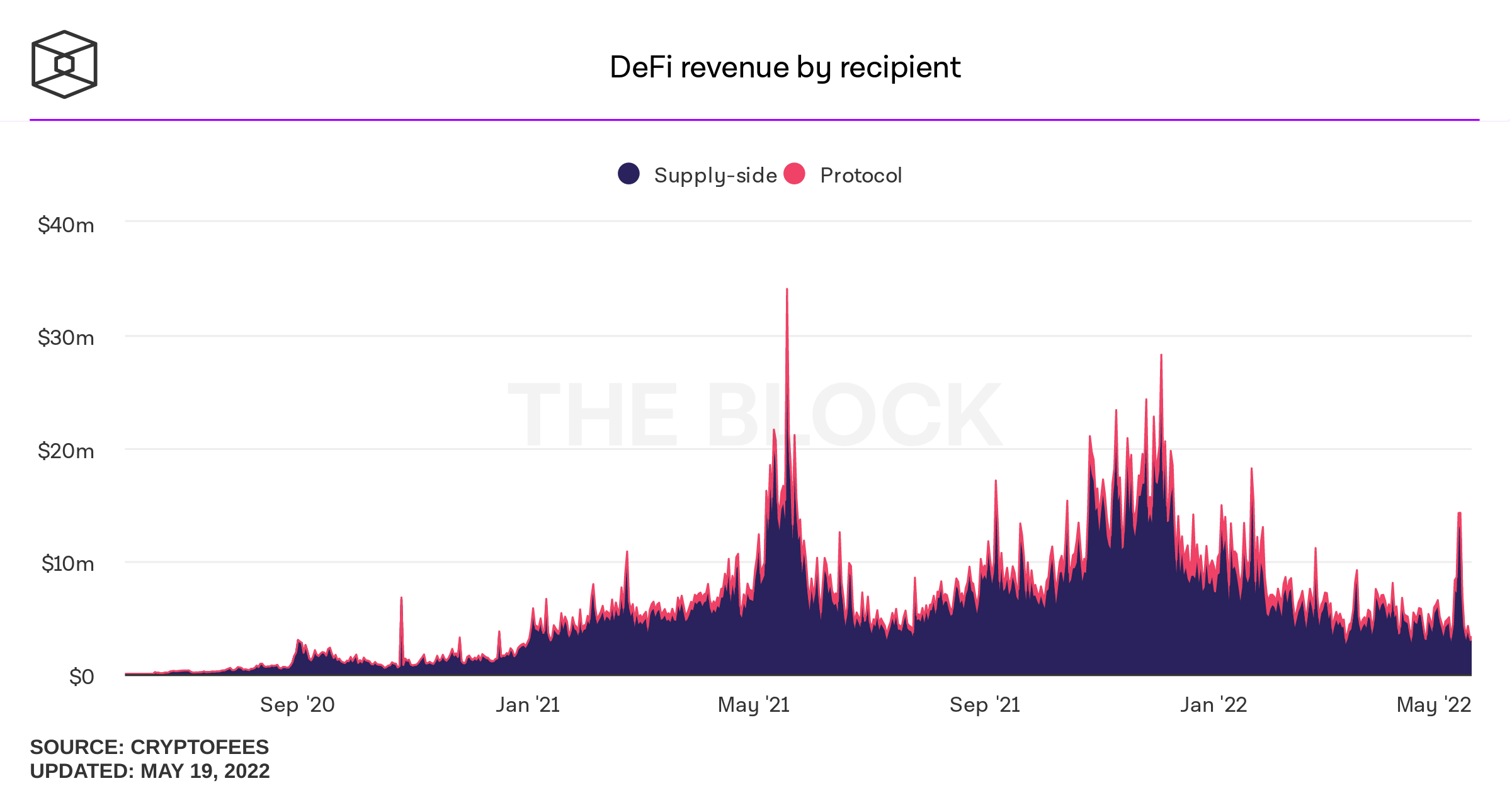

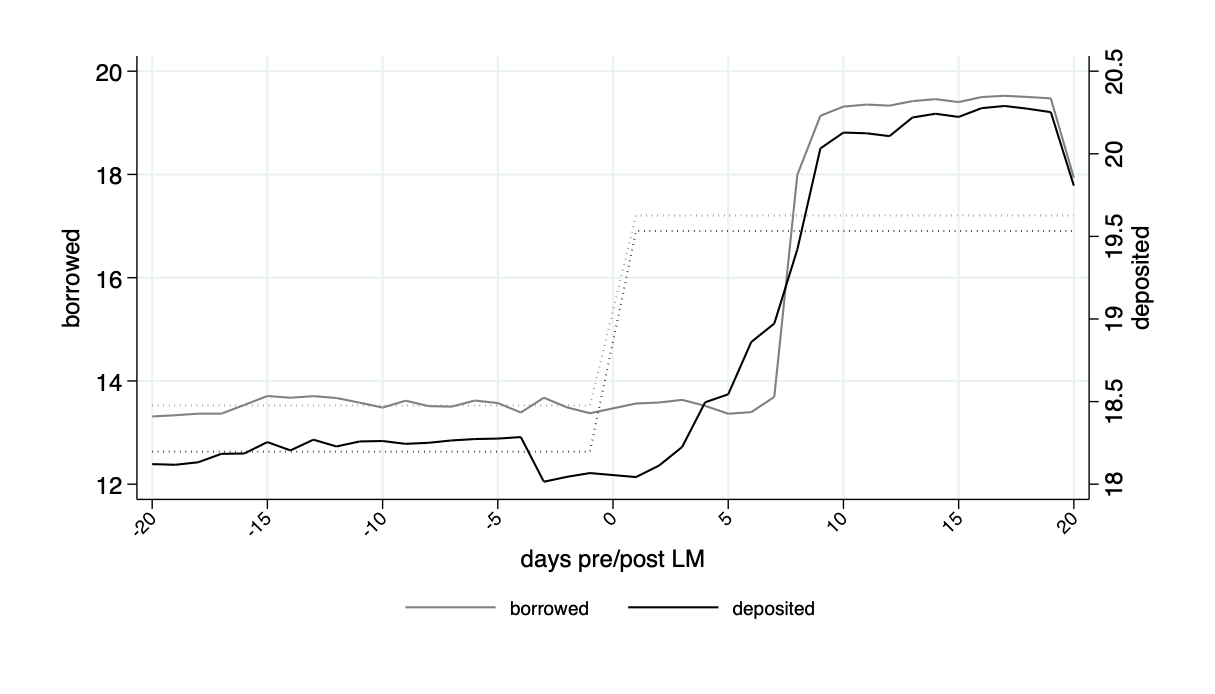

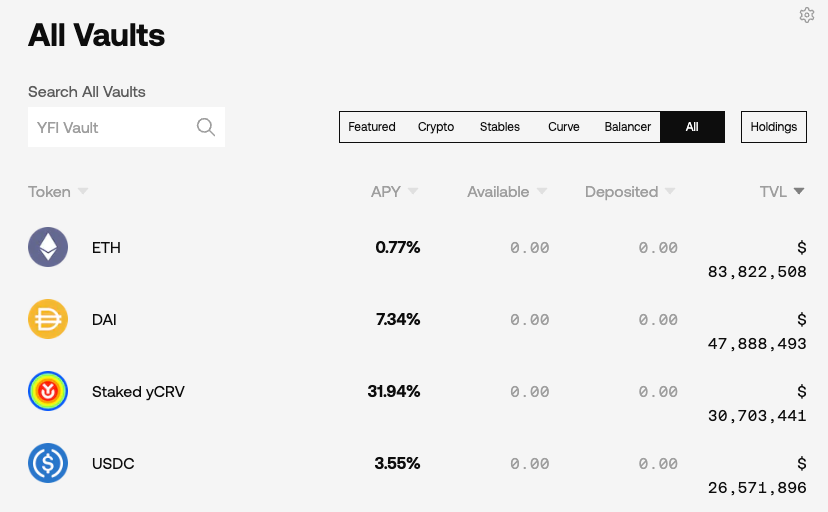

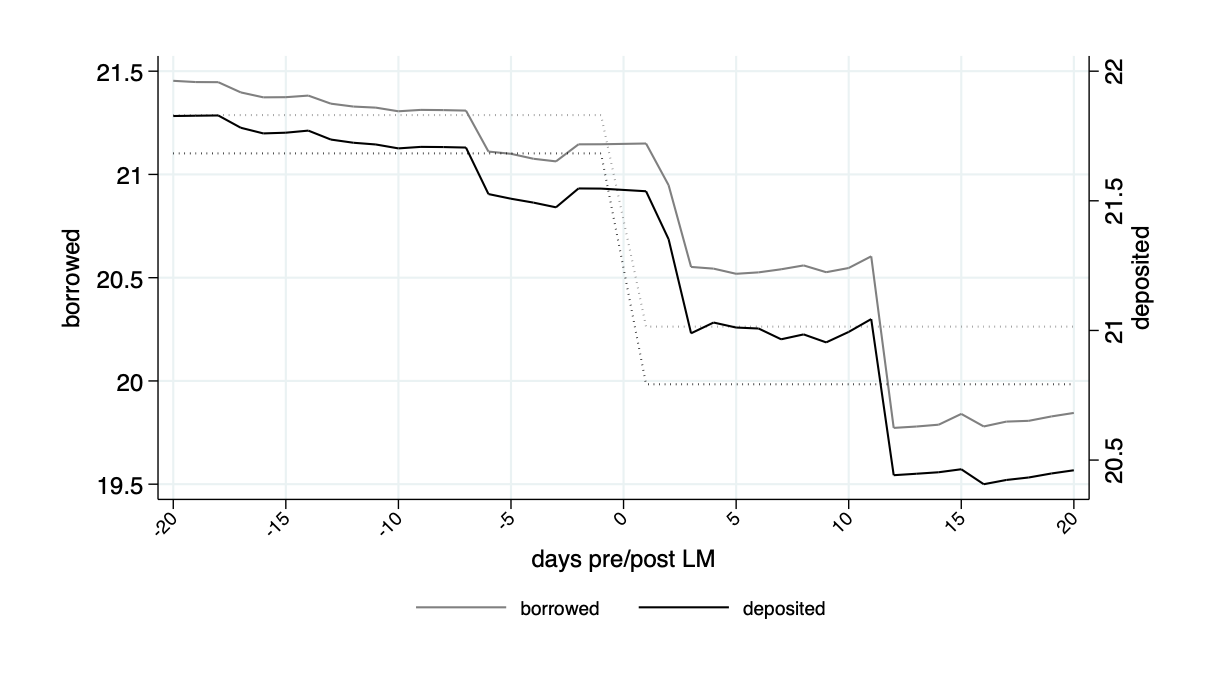

Some Data

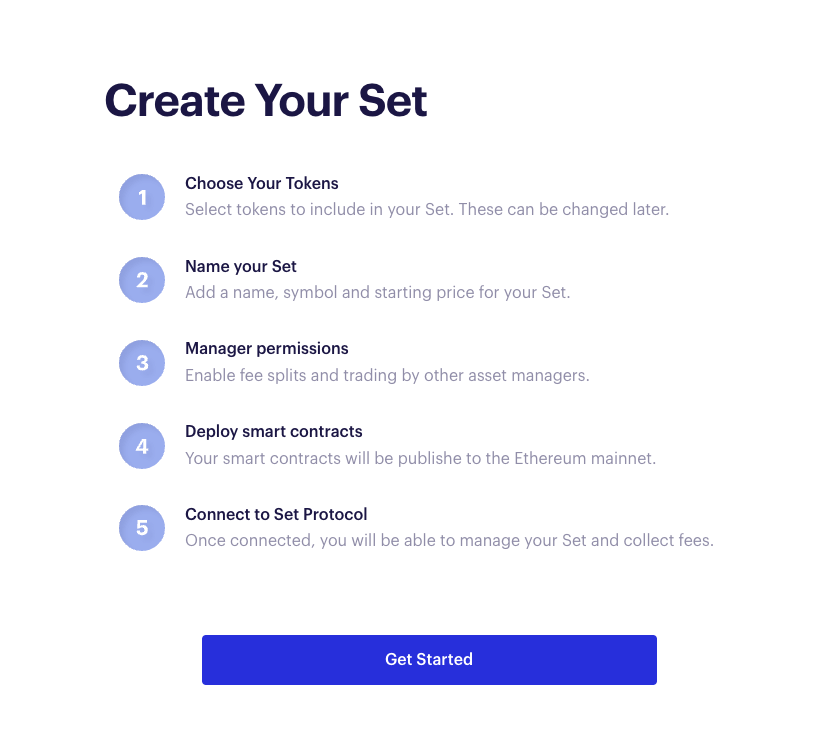

Obvious Smart Contract Application: Automate Investment Strategies

idea: create new mutual fund like asset

"yield aggregator:" push capital where rate of return is highest

Platforms, Peer-to-Peer, and Decentralization

Philosophy of Peer-to-peer

Traditional Market

two-sided with fixed roles

Decentralized Market?

value management protocol \(\not=\) market

Peer-to-peer \(\Rightarrow\) Platforms

liquidity \(\nearrow\)

volume \(\nearrow\)

protocol fees \(\nearrow\)

token value \(\nearrow\)

Platform economics is tricky:

it works!

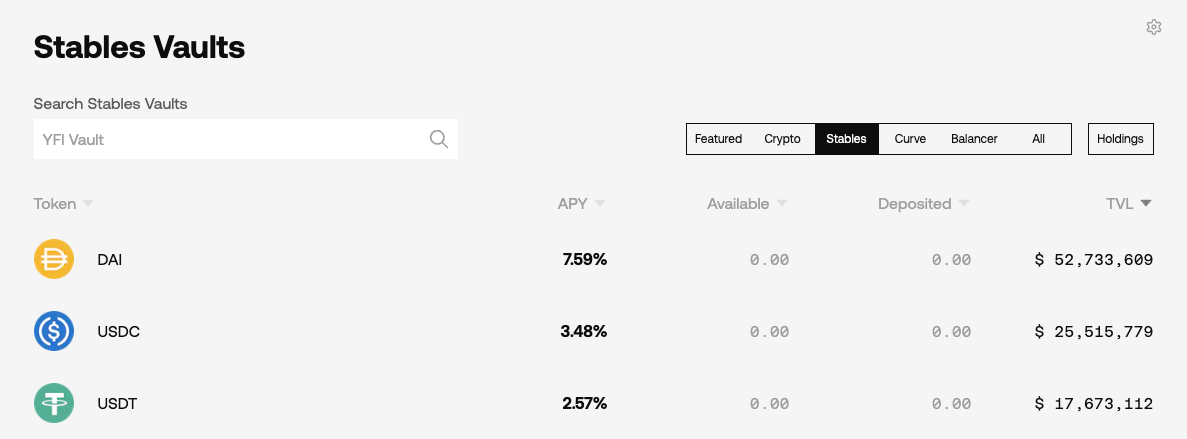

A Consequence of Liquidity Mining: Yield Aggregators

Idea:

A Taxonomy of Tokens

UniSwap Lab supports development

a website app accesses the code

token holders control contact features

don't own the code

operation = decentral

control = decentral

anyone can use the baseline code

core code runs on the blockchain

tokens used as rewards

What's a crypto-token and what's special about it?

Tokens by use

payments:

utility

stablecoins

governance

asset

derivatives

Disclaimer: this list in non-exhaustive, new ideas and concepts come up every day!

Final Thoughts

Some Final Thoughts

@financeUTM

andreas.park@rotman.utoronto.ca

slides.com/ap248

sites.google.com/site/parkandreas/

youtube.com/user/andreaspark2812/

Are Tokens Securities and What Safeguards Should There Be?

Provocative Thoughts

- End of Theory -

Some Developments

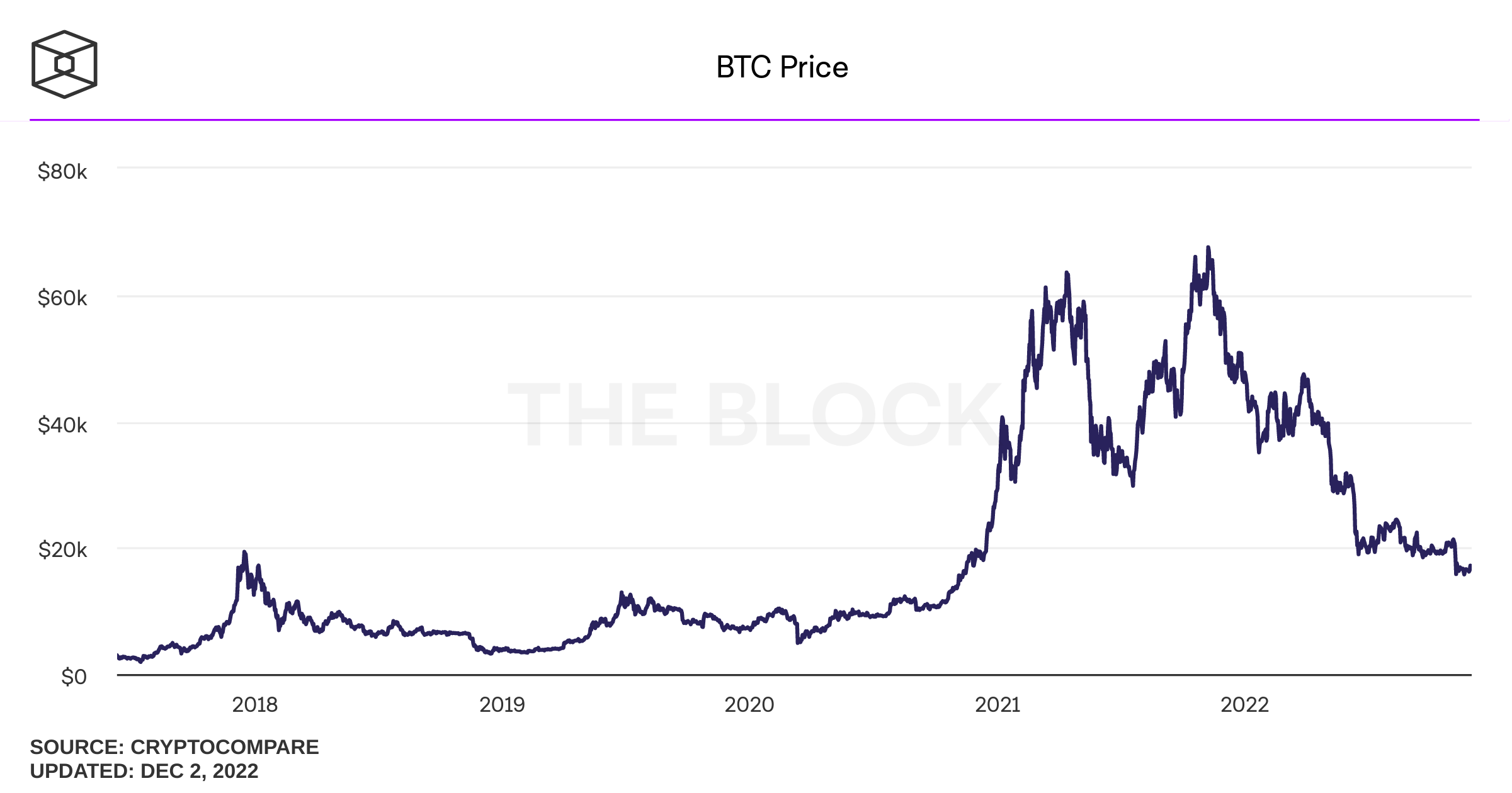

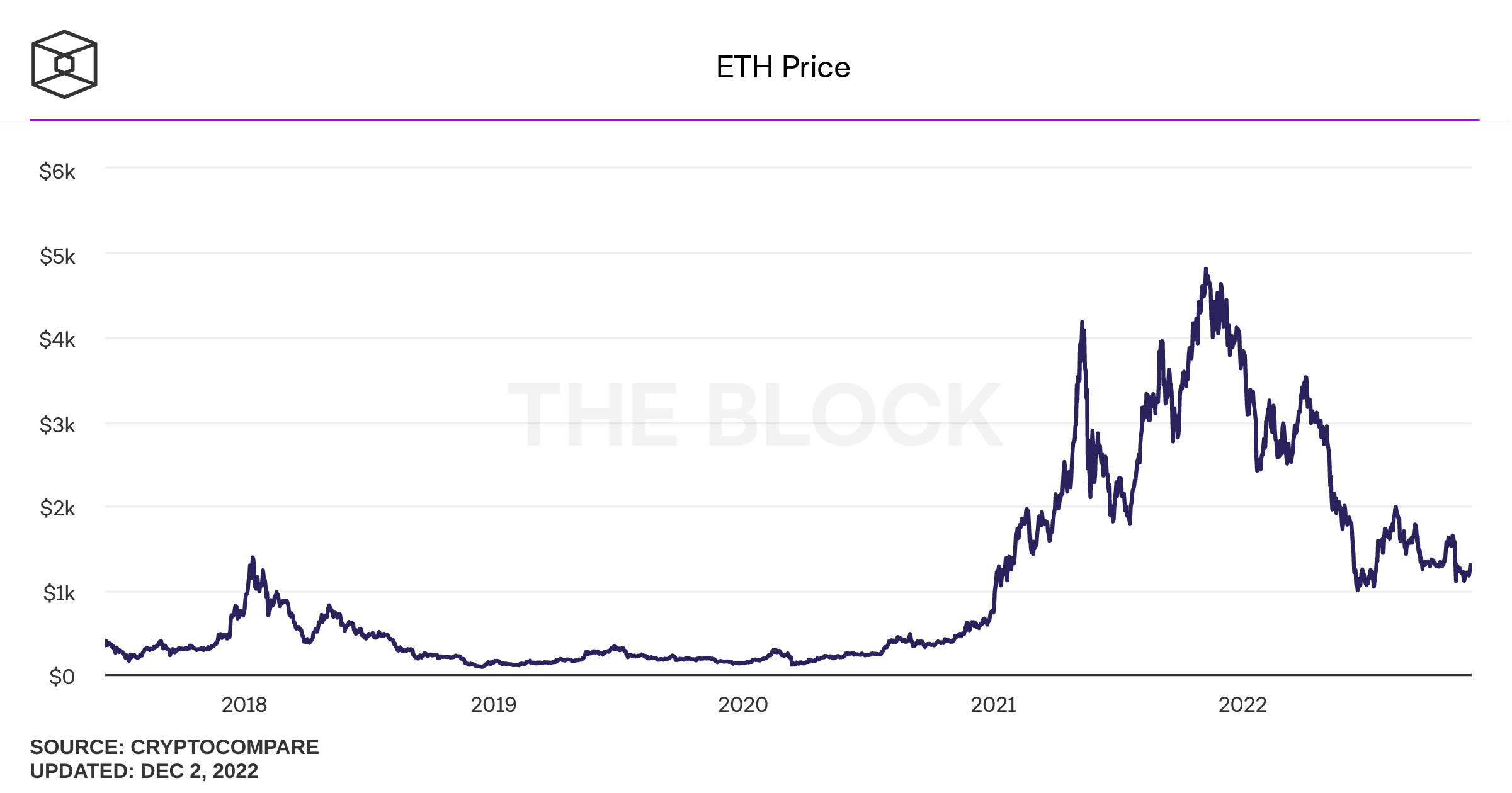

An ugly 9 months

From a slow slide to a thorough crash

-75%

-75%

!

The Terra Implosion

UST Stablecoin

LUNA (cryptocurrency of the TERRA network)

A timeline

May 7: selling pressure on UST from Curve withdrawals

May 12: LUNA and UST at $0.01

June 27: Three Arrows Capital ordered to liquidate

June 12: Celsius Network suspends withdrawals

July 13: Celsius files for Chapter 11

July 6: Voyager Digital files for Chapter 11

July 4: Vault suspends withdrawals

Three Arrows Capital lost >60% of value and faces numerous margin calls that they did not react to

partially "saved" by \(\ldots\) FTX

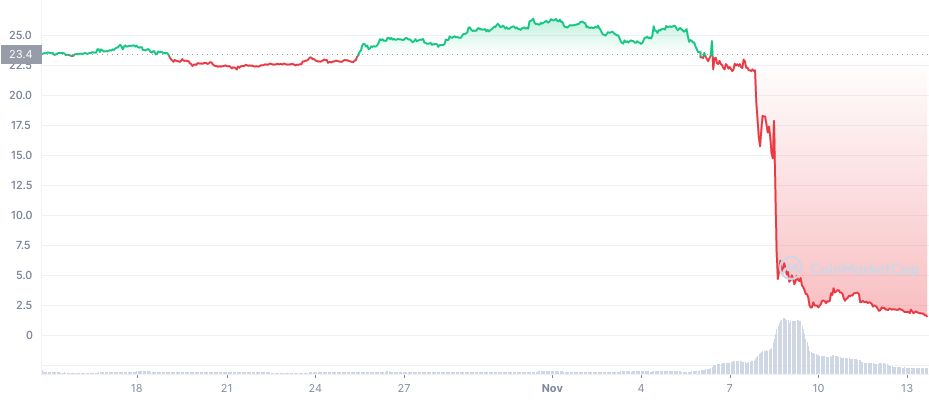

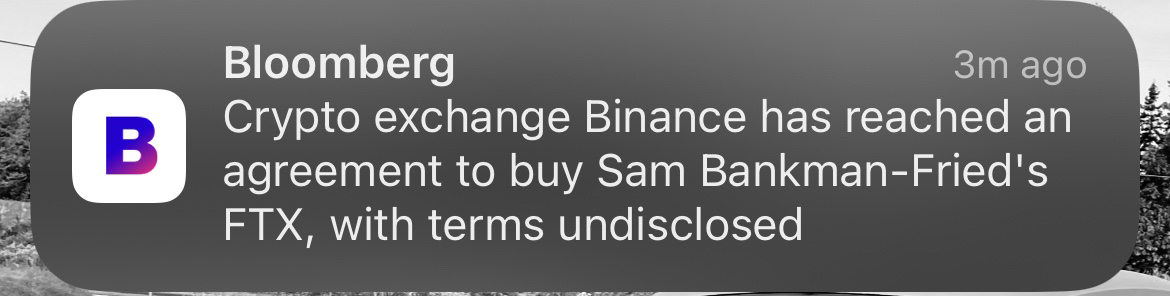

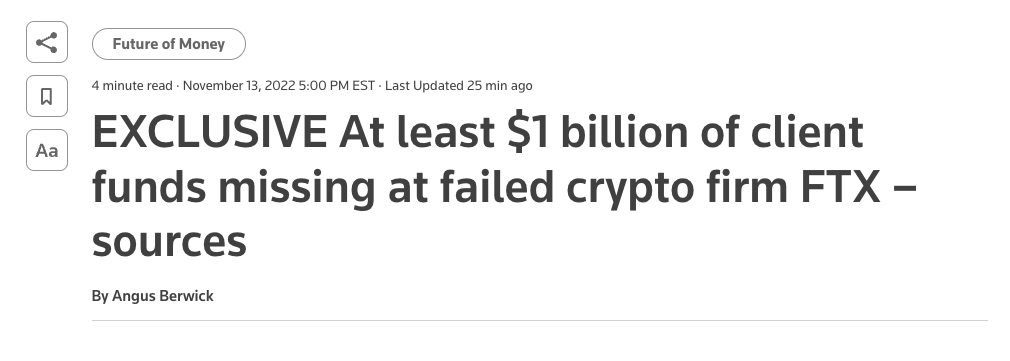

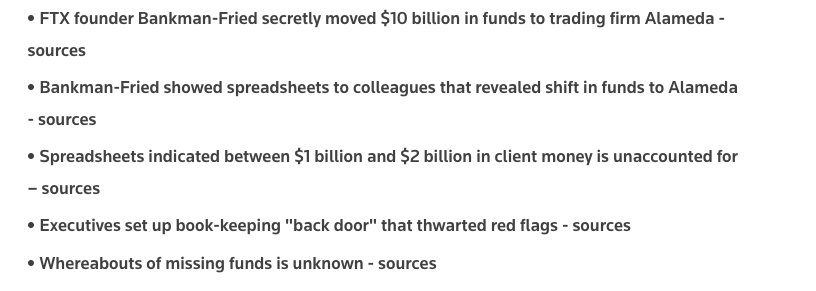

The FTX Implosion

A timeline

Nov 8

Fundamental Problems: Solution sans Regulators?

New trend: data providers check assets

Assets: cash in bank accounts and crypto assets in exchange wallets

Liabilities: customers' crypto and cash deposits

Proof of crypto assets

publish all exchange wallets

proof of control: shift assets from one address to another at a pre-determined time

Proof of crypto liabilities

public customer balances - customer can check

own holding

sum of all

Problem: privacy (adequate solutions exist)

Proof of Assets & Liabilities

A timeline

May 7: selling pressure on UST from Curve withdrawals

May 12: LUNA and UST at $0.01

June 27: Three Arrows Capital ordered to liquidate

June 12: Celsius Network suspends withdrawals

July 13: Celsius files for Chapter 11

July 6: Voyager Digital files for Chapter 11

July 4: Vault suspends withdrawals

Three Arrows Capital lost >60% of value and faces numerous margin calls that they did not react to

partially "saved" by \(\ldots\) FTX

all centralized!

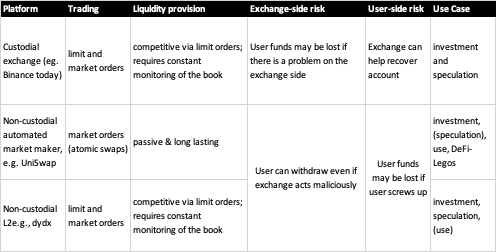

Centralized vs Decentralized?

Path forward

seller

buyer

What is a Blockchain?

The Premise of the

Internet & Blockchain

Peer to Peer Communication

Peer to Peer Value

!

?

?

Sidebar: What is digitize-able value?

The challenge: how do you ensure digital scarcity?

By Andreas Park

A presentation for the OSC in 2023 on DeFi