Andreas Park PRO

Professor of Finance at UofT

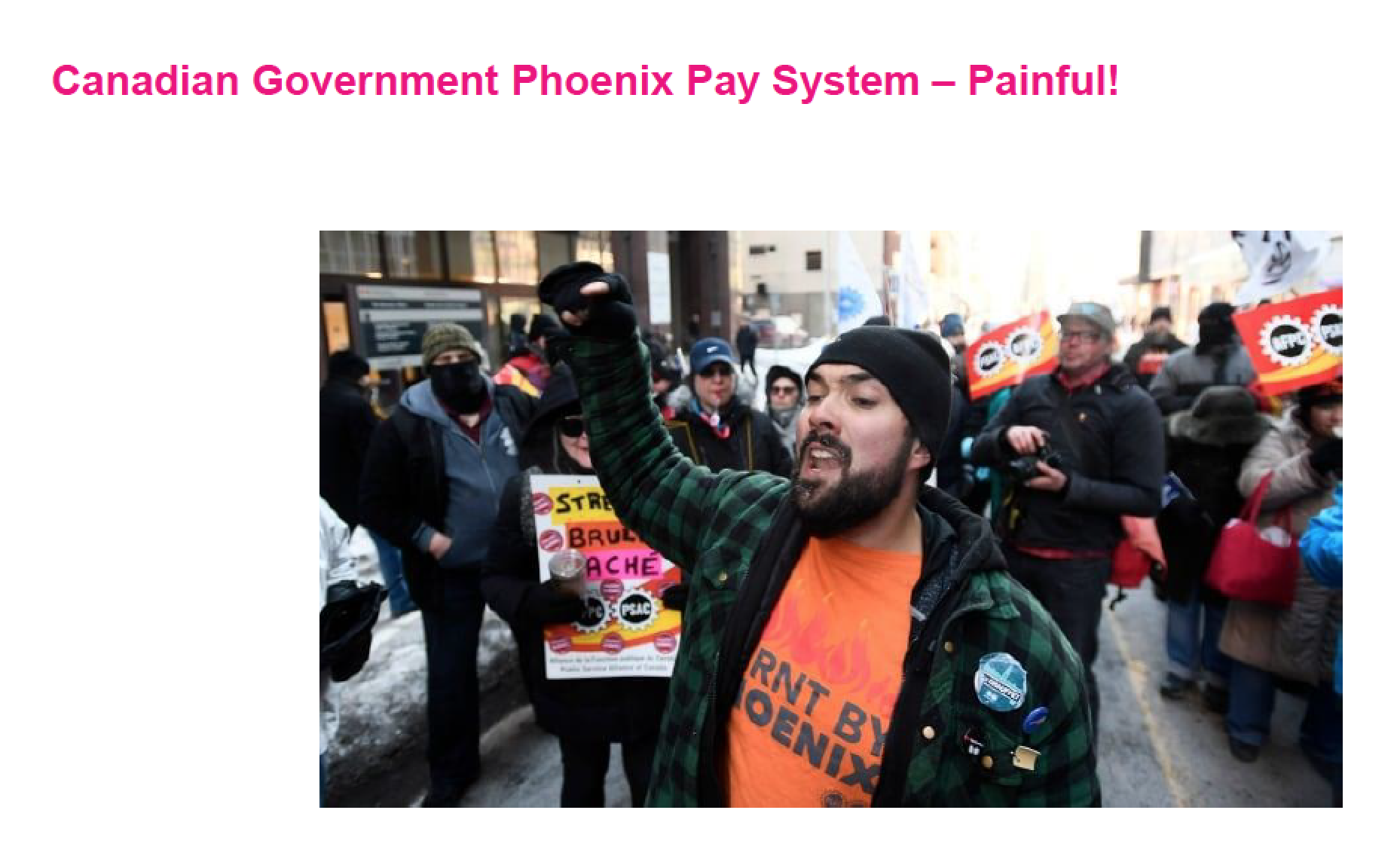

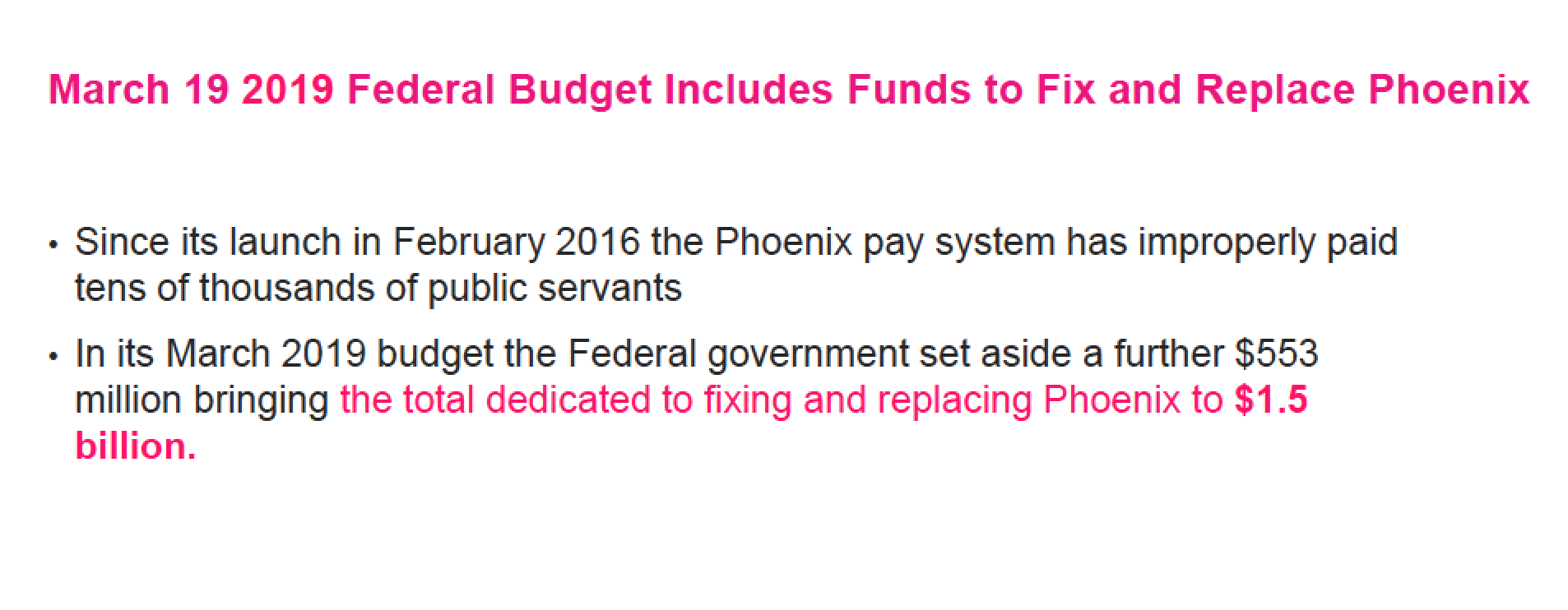

https://www.cbc.ca/news/canada/ottawa/phoenix-ottawa-timeline-1.3691812

Check out the video "Just Walk Out"

https://www.payments.ca/sites/default/files/canadianpaymentmethodsandtrendsreport_2019.pdf

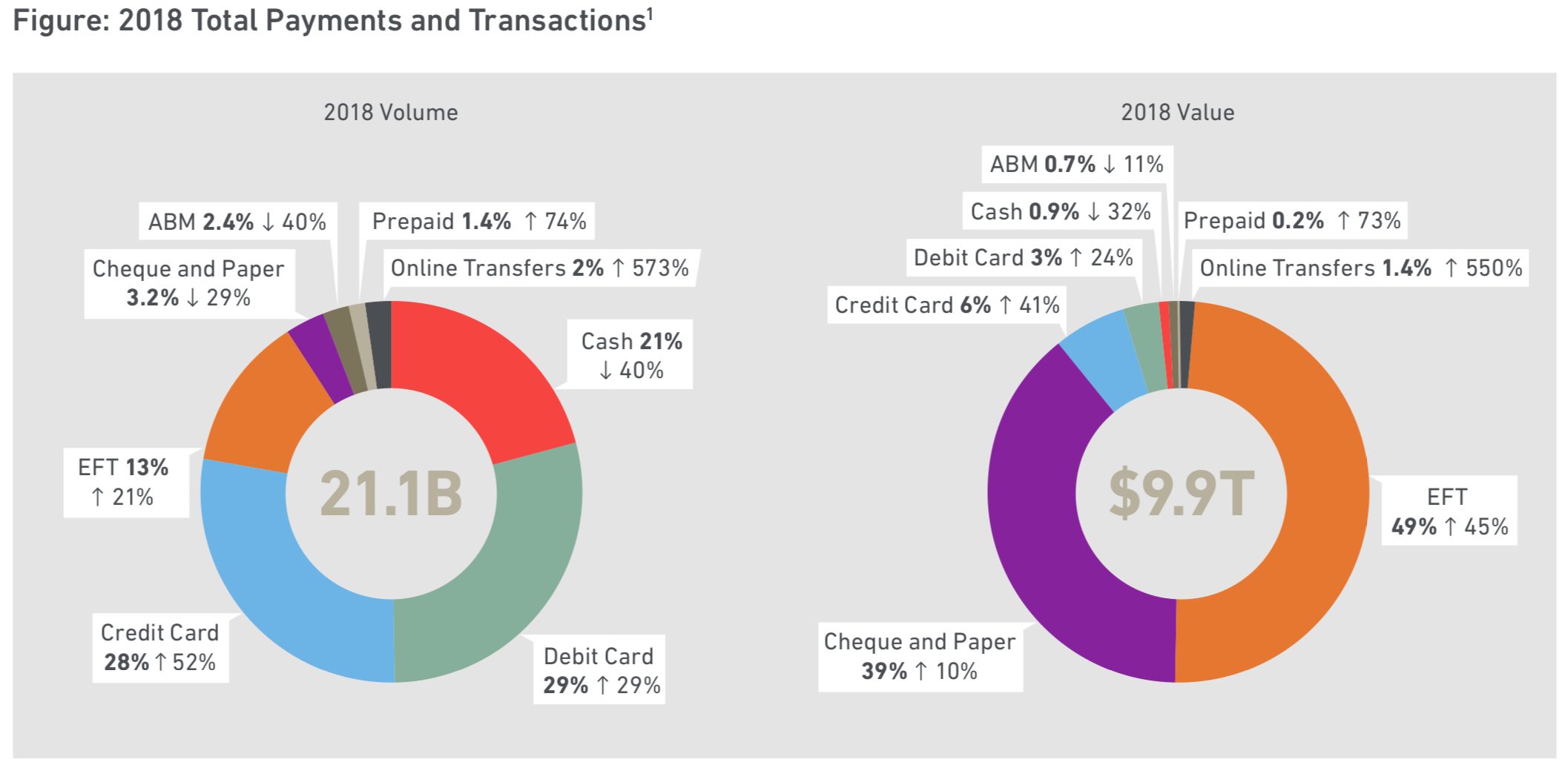

1 The arrows represent the growth and decline of the key payment methods between 2013 and 2018.

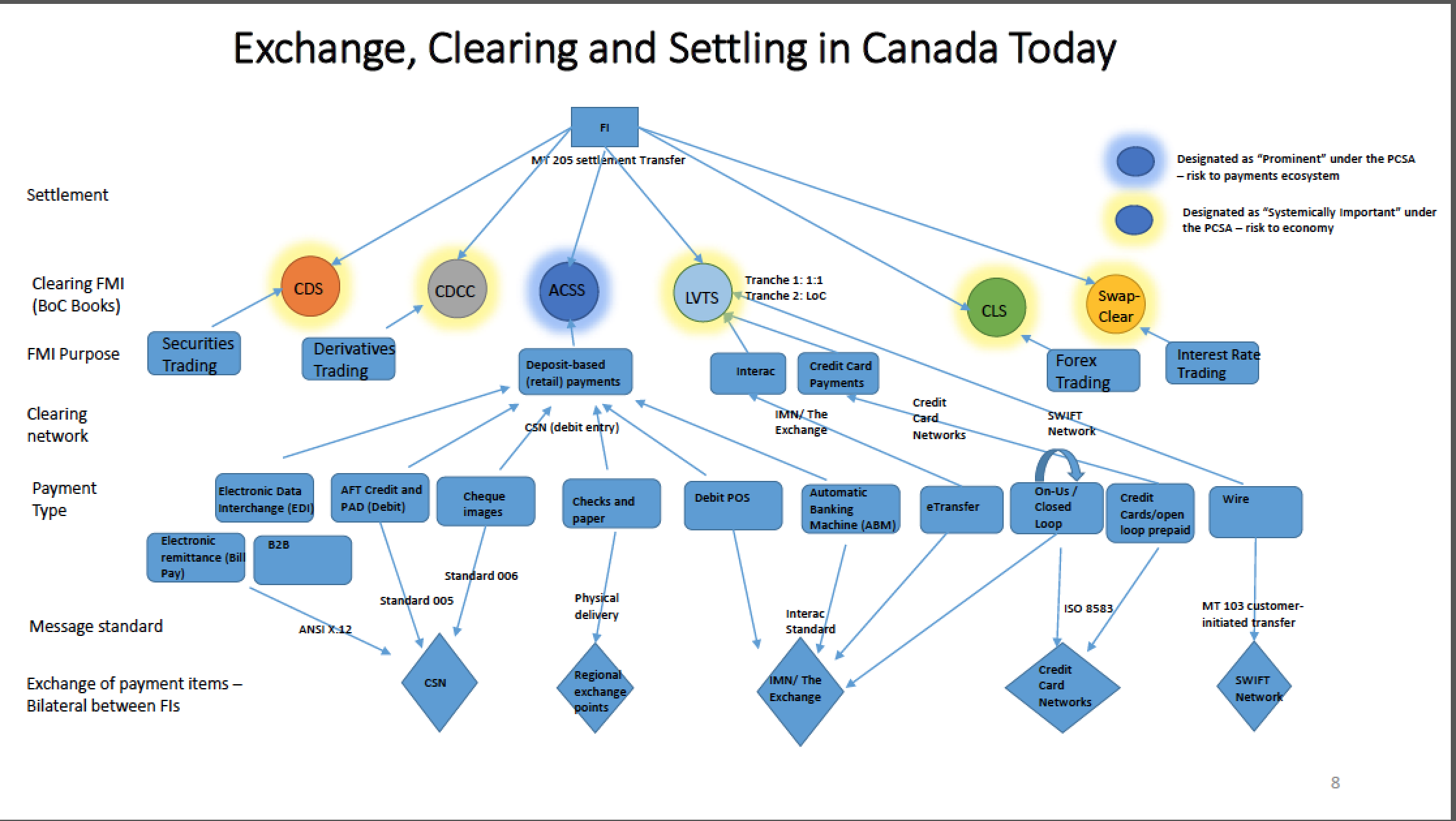

Payments Canada is responsible for the clearing and settlement infrastructure, processes and rules essential to those transactions.

[...] delegated by the Canadian Government. [...] provide Canada’s national payments systems.

Large Value System lets financial institutions and their customers send large payments securely. Retail System is where the vast majority of day-to-day Canadian commerce is cleared by our financial institutions.

The value of payments cleared by Payments Canada’s systems in 2019 was approximately $55 trillion or $218 billion every business day.

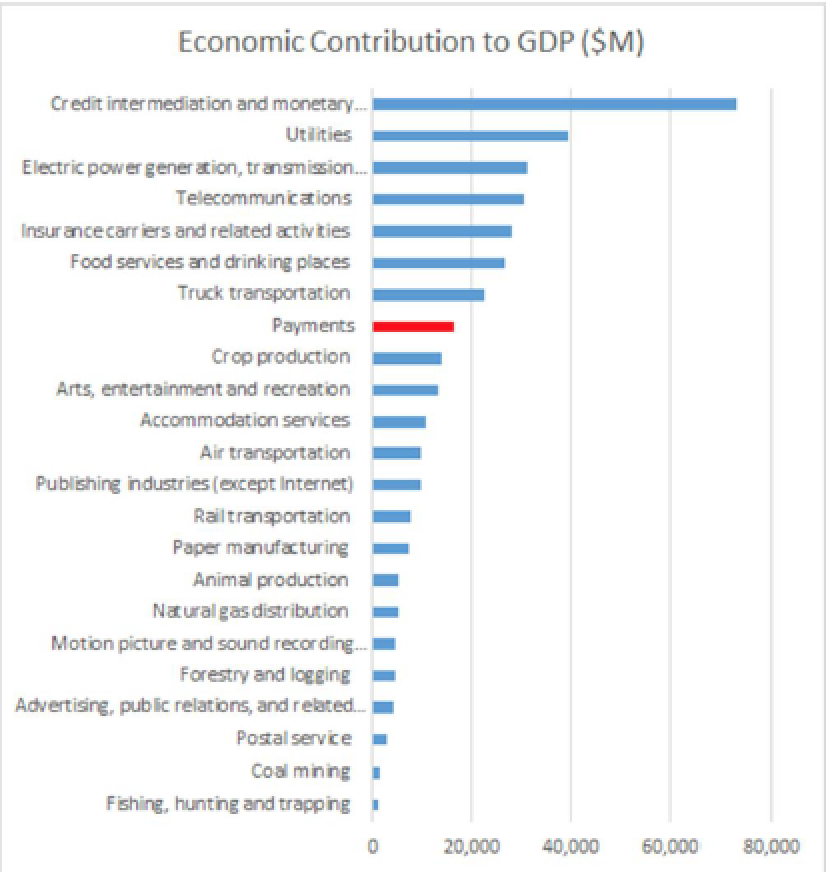

Payments industry revenues just over $16 billion in 2016.

Larger than agriculture!

CDS

ACSS

LVTS

Cheques

Debit at POS

e-transfer

Credit Card/

open loop

ATMs

Wire

Interac

Credit

Card

deposit based retail

Interac standard

credit card network

SWIFT

CSN

Settlement

Clearing process

Underlying network

Type of payment

Financial market infrastructure purpose

Securities Trading

Before we had the money, there were still transactions ....

How were these conducted?

https://www.pbs.org/wgbh/nova/article/history-money/

https://www.npr.org/sections/money/2011/02/15/131934618/the-island-of-stone-money

Rai stones on the island of Yap

But:

Beaver Pelts

HBC made-beavers

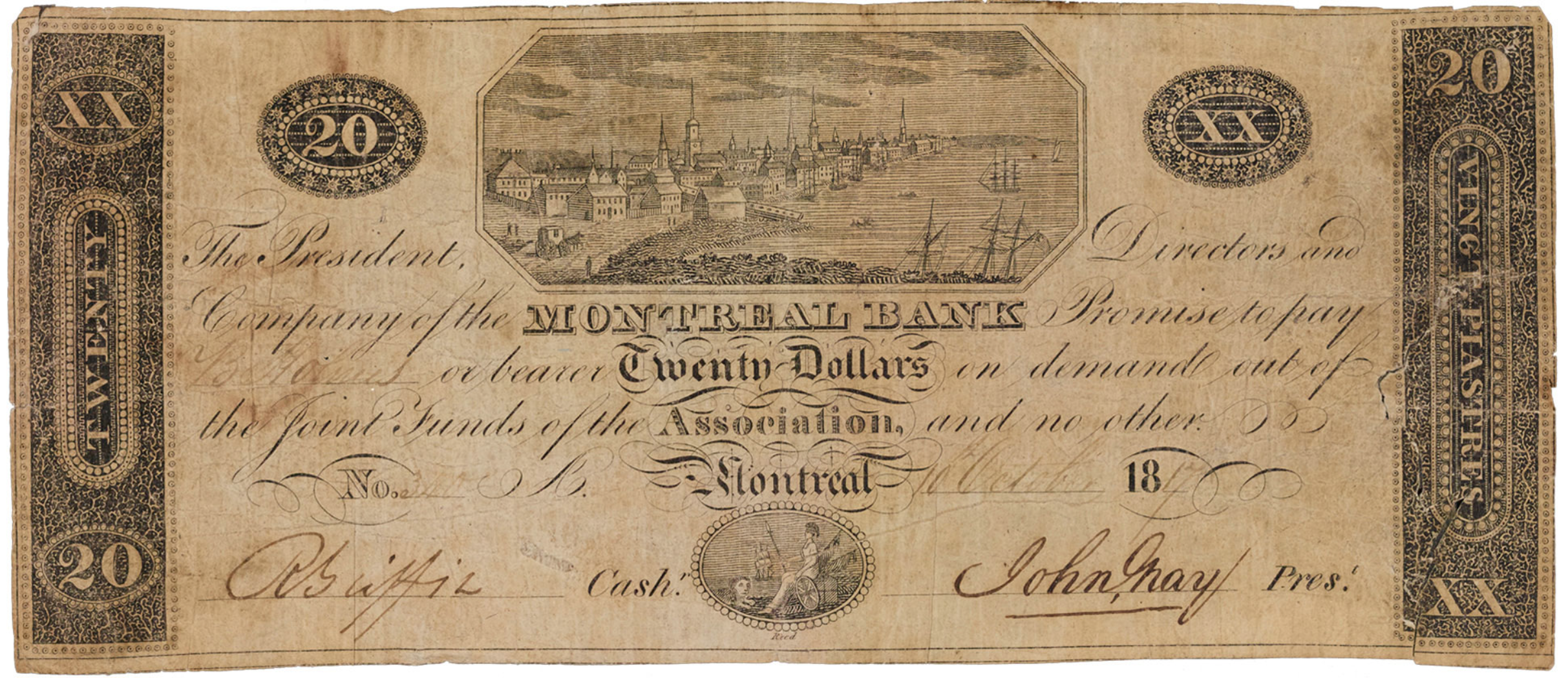

1817: the Montreal Bank’s promise to pay the bearer, on demand, the face value of the note in gold and silver coins

Time-consuming to move/process cheques

No immediate use of funds

Costly to process paper cheques

Cheques, Drafts ... "payment from an account"

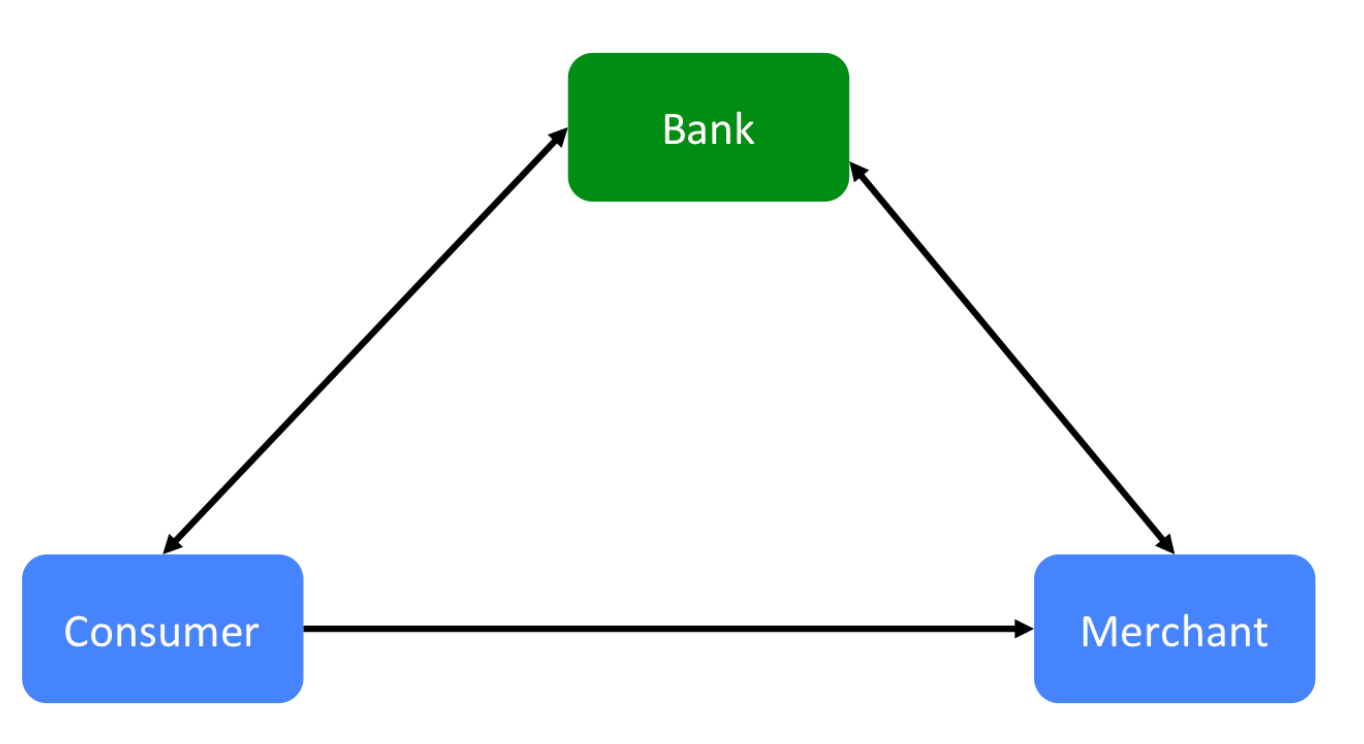

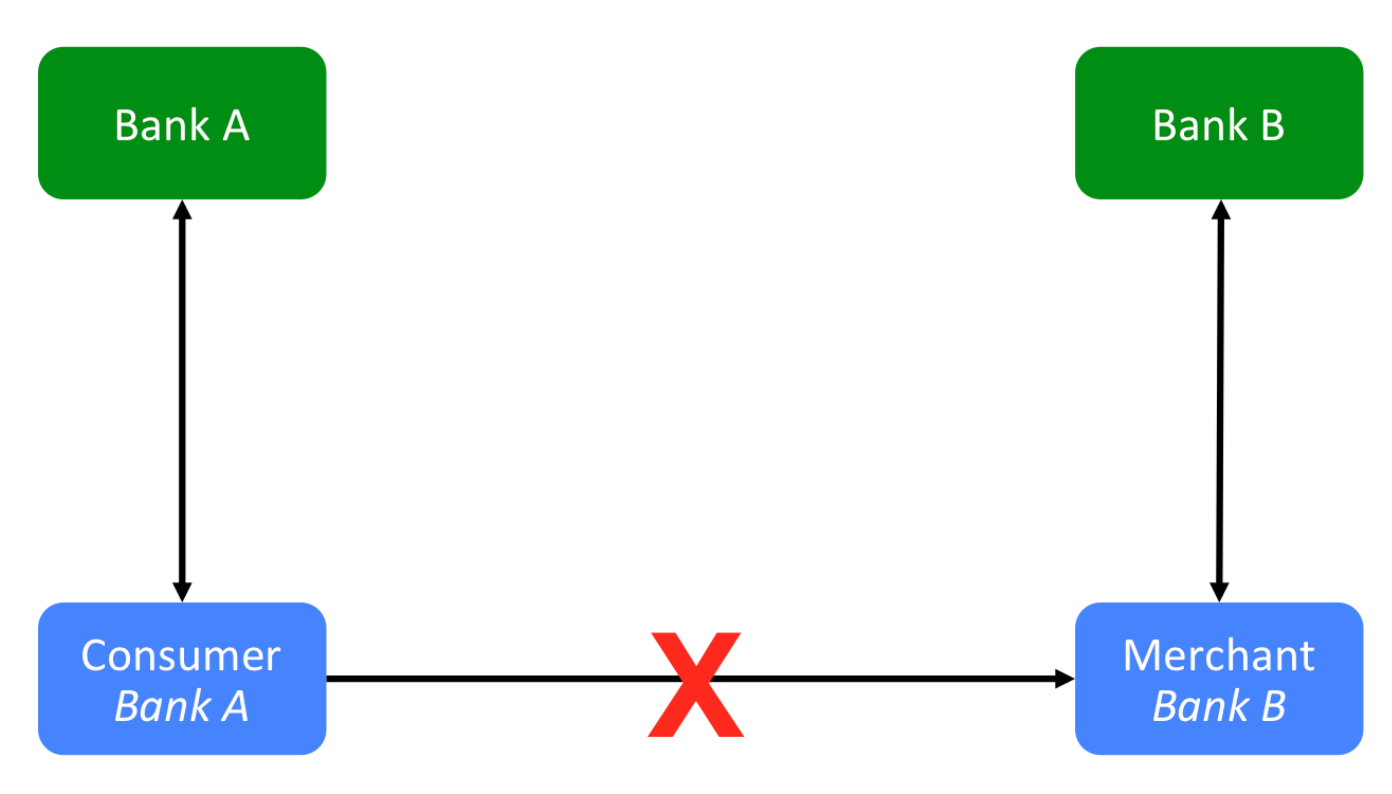

Imagine you run a bank

Wouldn’t it be great if your customers could go to local shops and “charge” their purchases to an account that you hold for them?

Make money offering credit to the customers and make some more money charging the merchants for providing this service.

https://gendal.me/tag/payments/

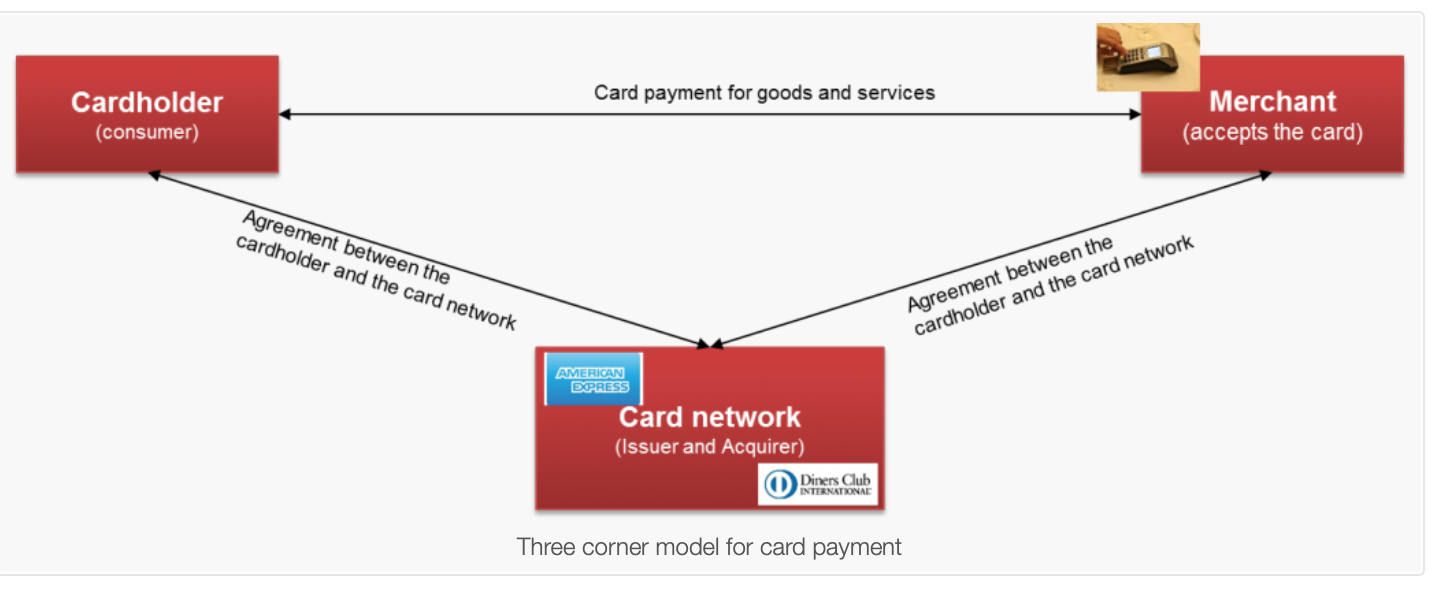

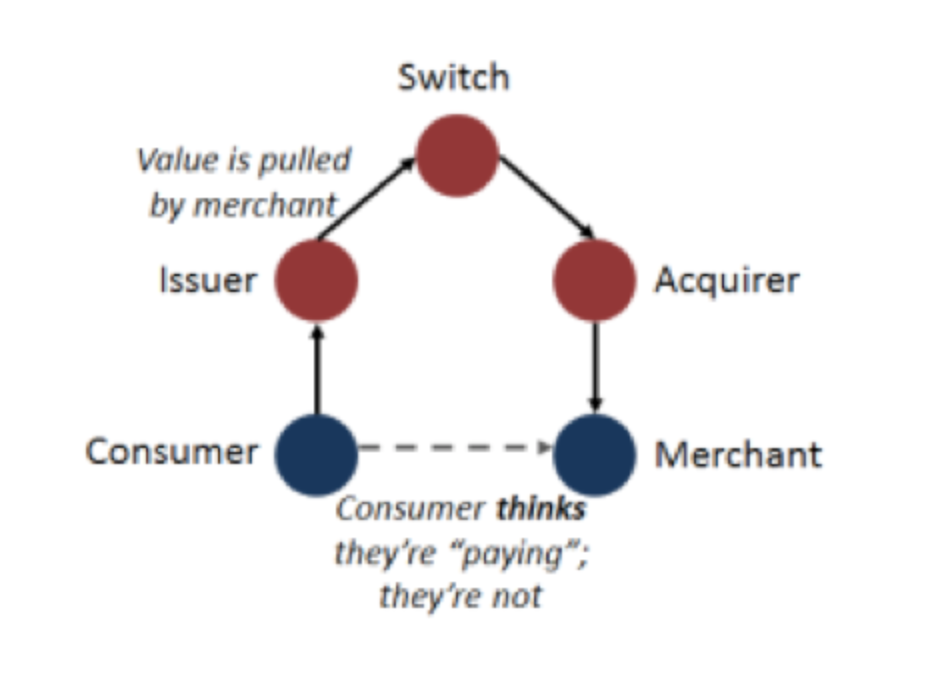

Cards "business"

= TWO businesses

Business #1: offering credit to customers & processing their payments

CARD ISSUING

Business #2: enabling merchants to accept card payments & to get reimbursed

MERCHANT ACQUIRING*

*The card payment = a receivable that the processor acquires from the merchant

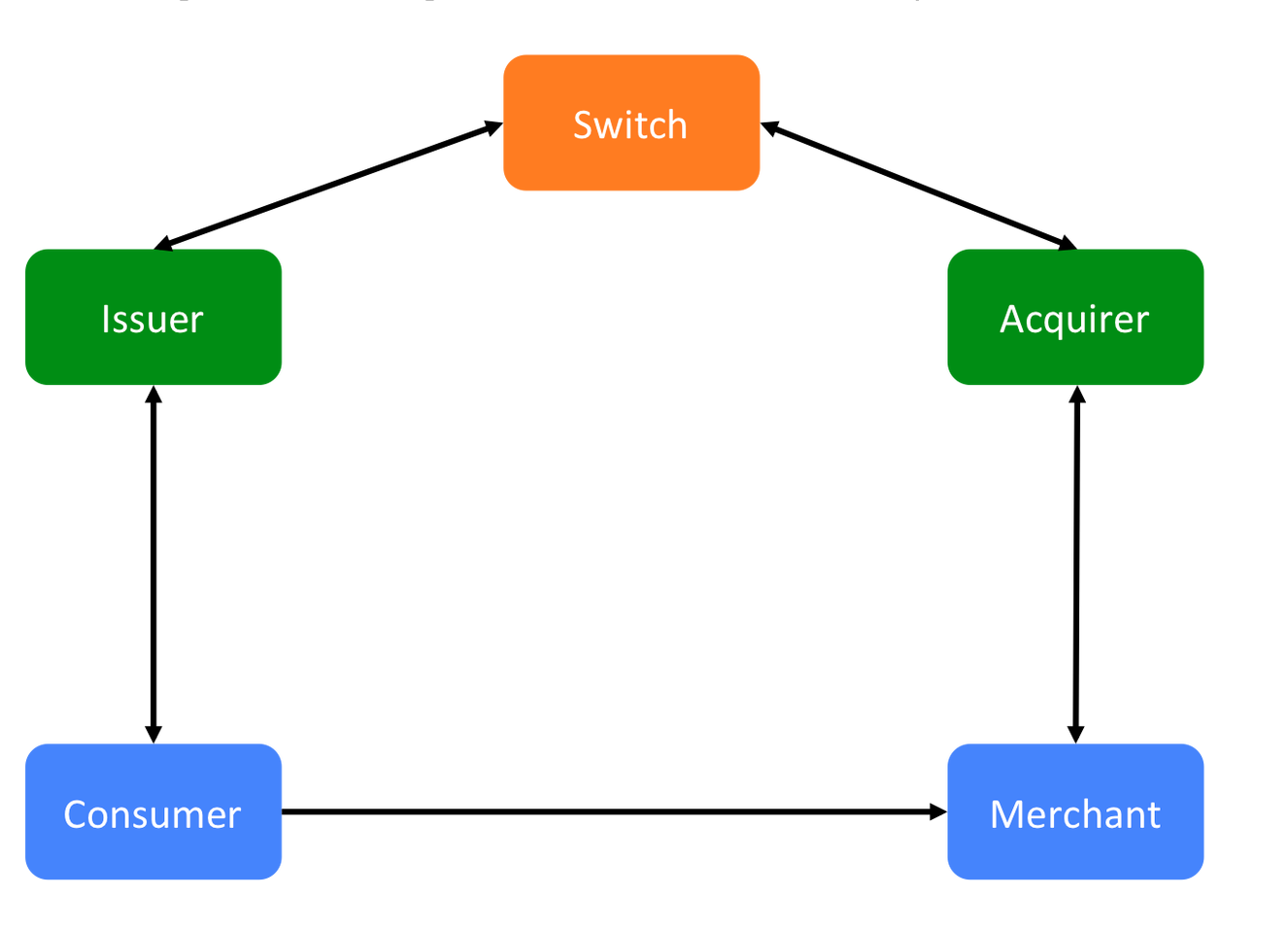

Or: Payment Processor

Switch = set of rules + brand recognition for the merchants and customers that are members of this arrangement

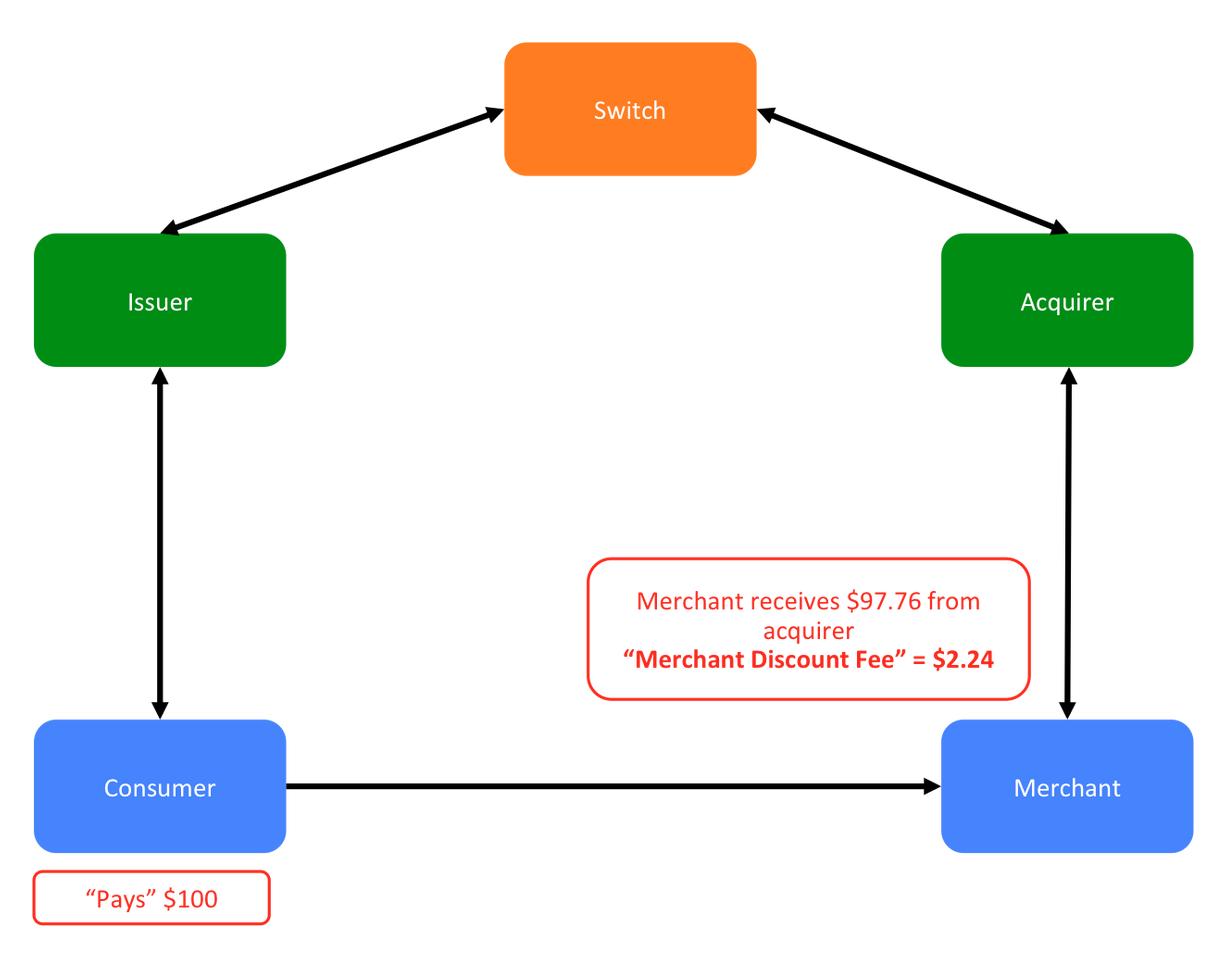

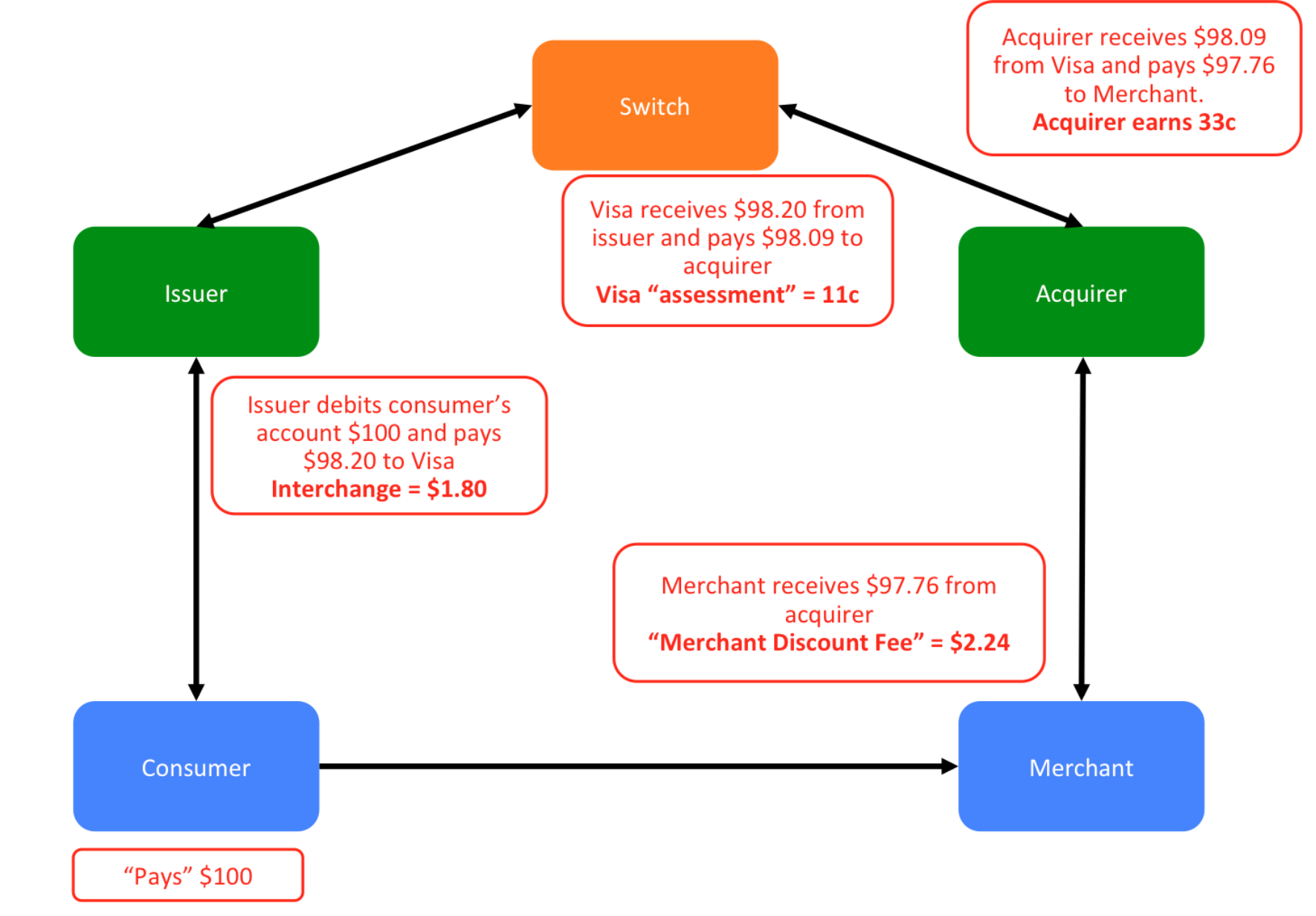

https://www.visa.ca/en_CA/support/small-business/interchange.html

https://www.cardfellow.com/blog/credit-card-processing-fees/

https://www.costcopaymentprocessing.ca/index.html

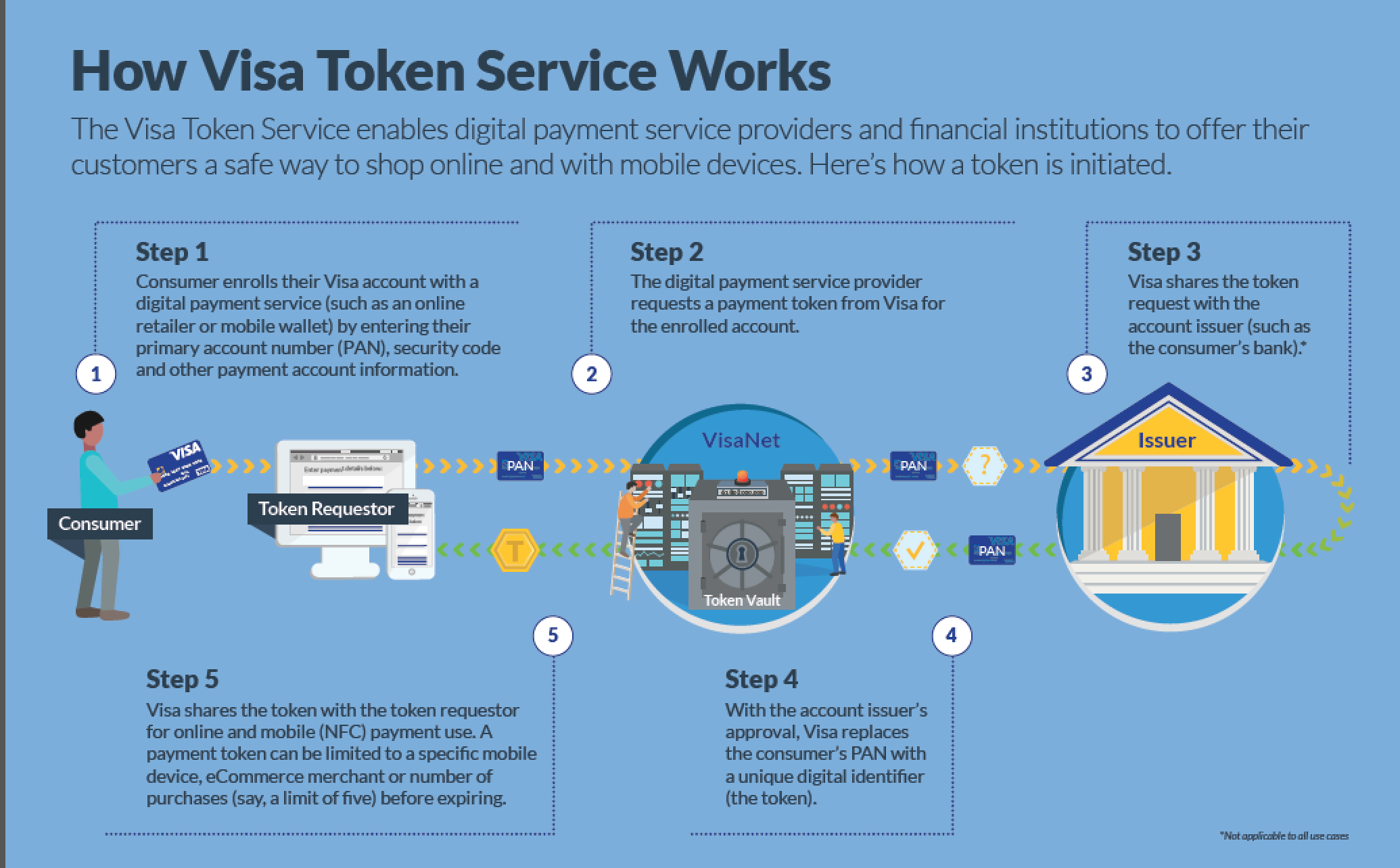

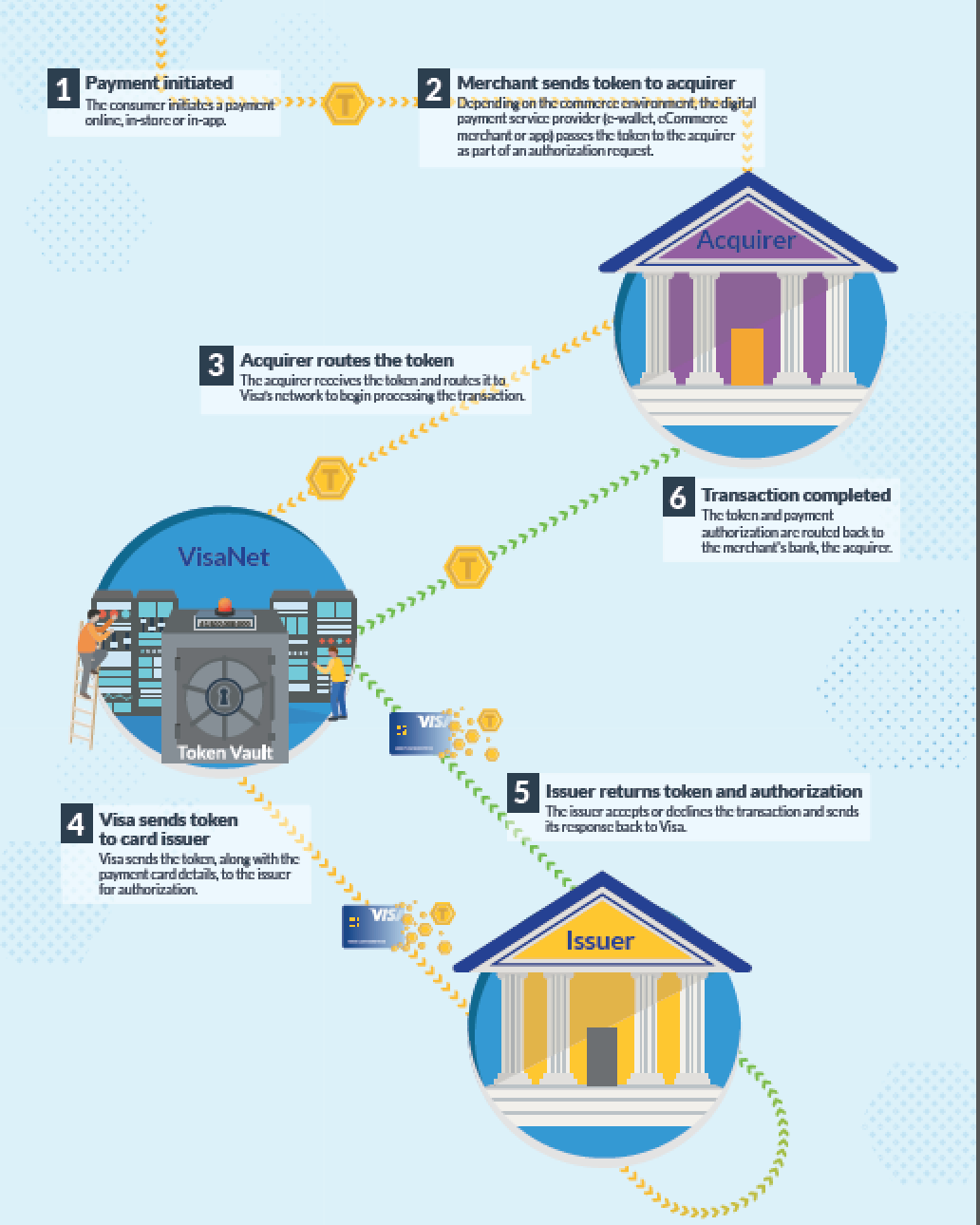

When you allow a merchant to store your credit card details on file, you must trust all these actors "not to mess up" ...

https://www.bhartipay.com/payment-tokenization-benefits

80% of cocaine in the US

$14 billion in drug profits

Source: bbc.com

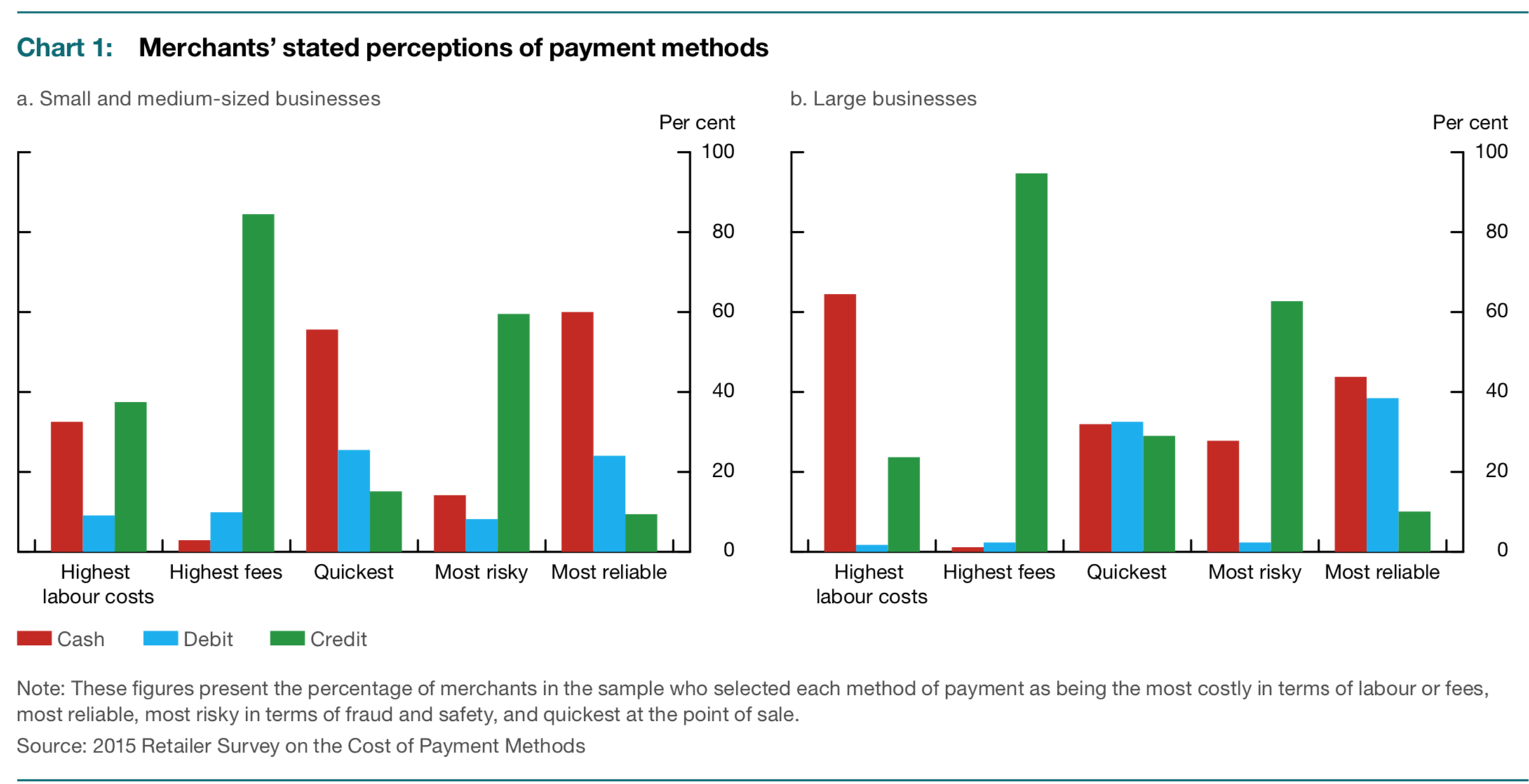

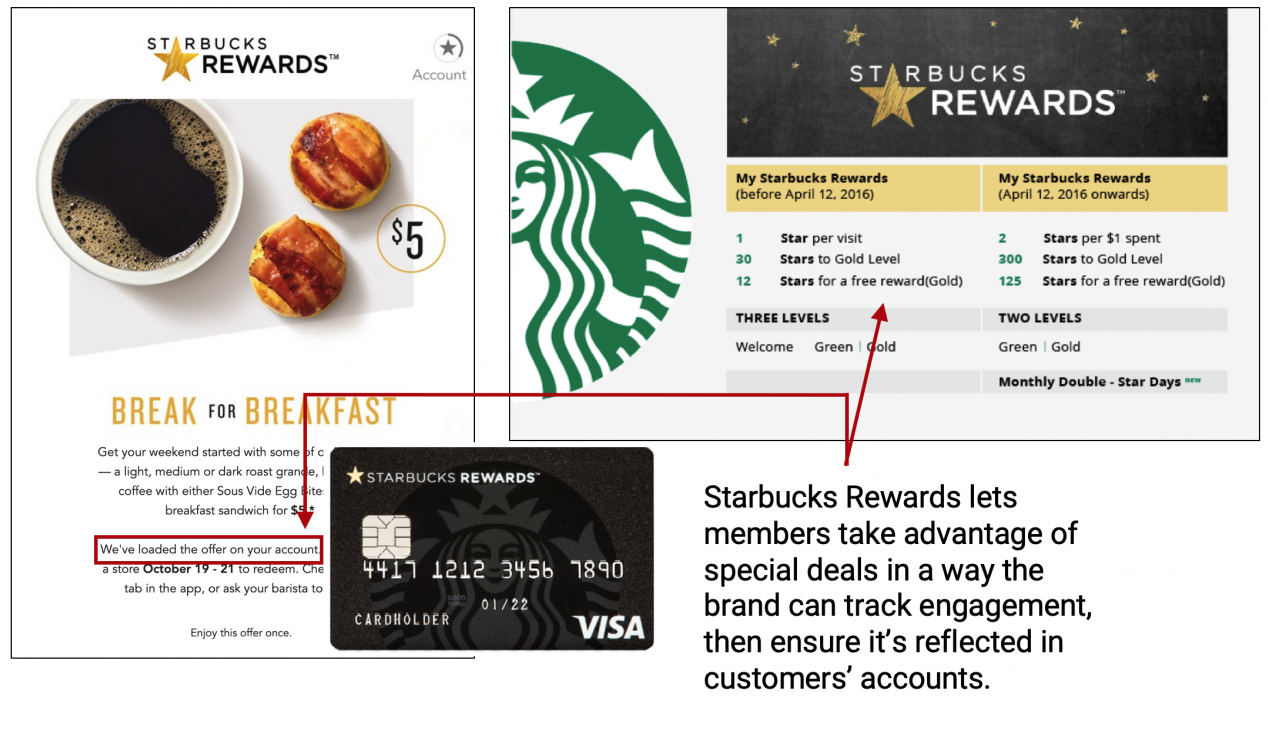

Loyalty rewards

is (mostly) not about rewarding loyalty.

It's DATA!

A

B

\(-\)

0

+

A

B

0

+

\(-\)

Option 1: borrow from BoC

lending rate:

deposit rate:

target rate

target rate\(+\)25bps

target rate\(-\)25bps

A

B

0

+

\(-\)

Option 2: borrow from another bank

target rate

By Andreas Park

This is the first set of slides on payments