Andreas Park PRO

Professor of Finance at UofT

payments is a profitable line of business

payments data is very valuable

payments \(=\) clunky and full of frictions

payments is the entry level drug to all things FinTech

Giancarlo Bruno, Senior Director, Head of Financial Services Industry, World Economic Forum

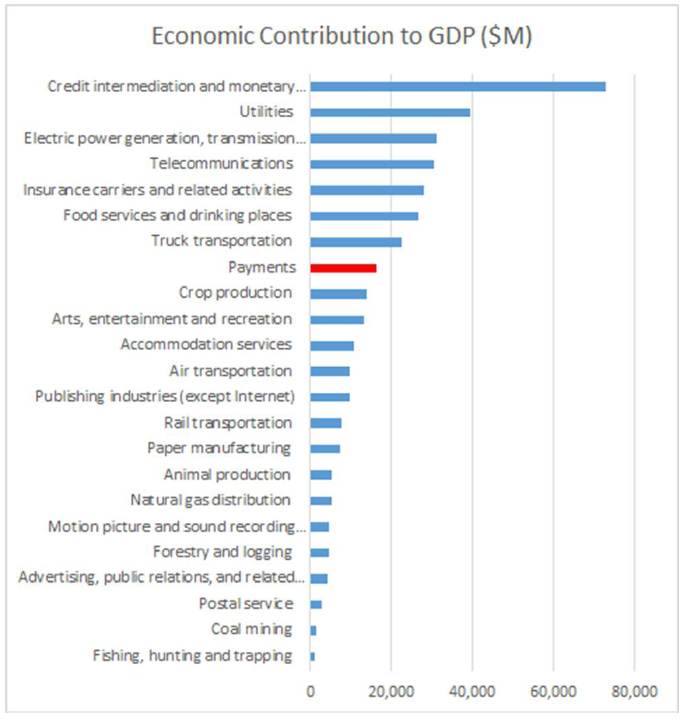

payments matter a lot more to people than we might think

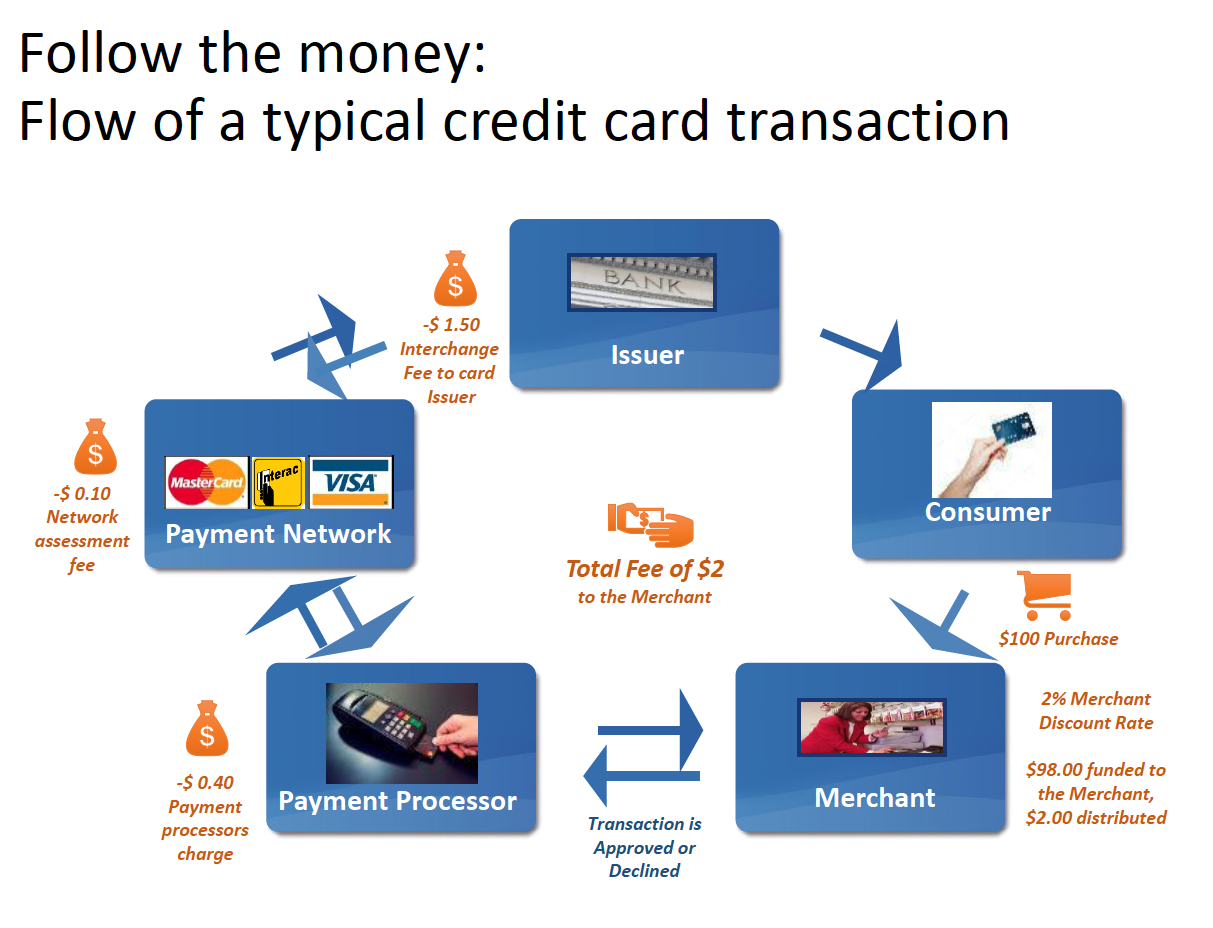

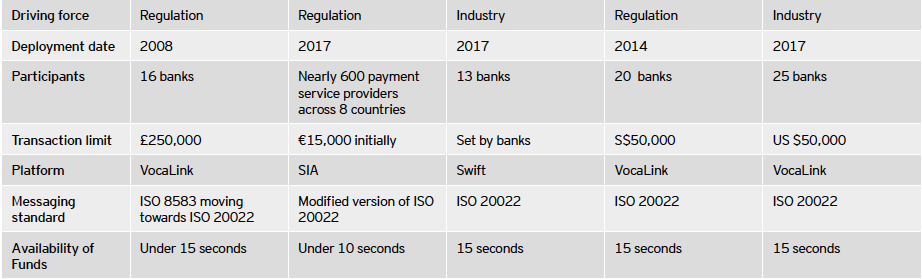

Source: How can payments modernization benefit Canadian businesses? Evaluating the cost of payments processing; EY and Payments Canada, 2018

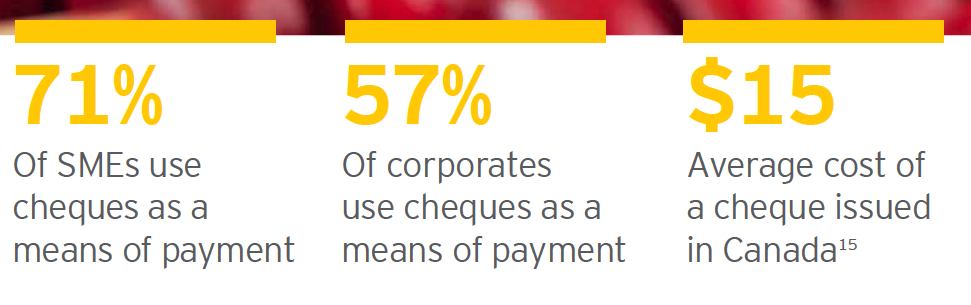

From Wendy Rotenberg: 734 Million Cheques for $4 Trillion

Source: Schmall & Wolkowitz (2016), Center for Financial Services Innovation (2016) "Financially Underserved Market Size Study"

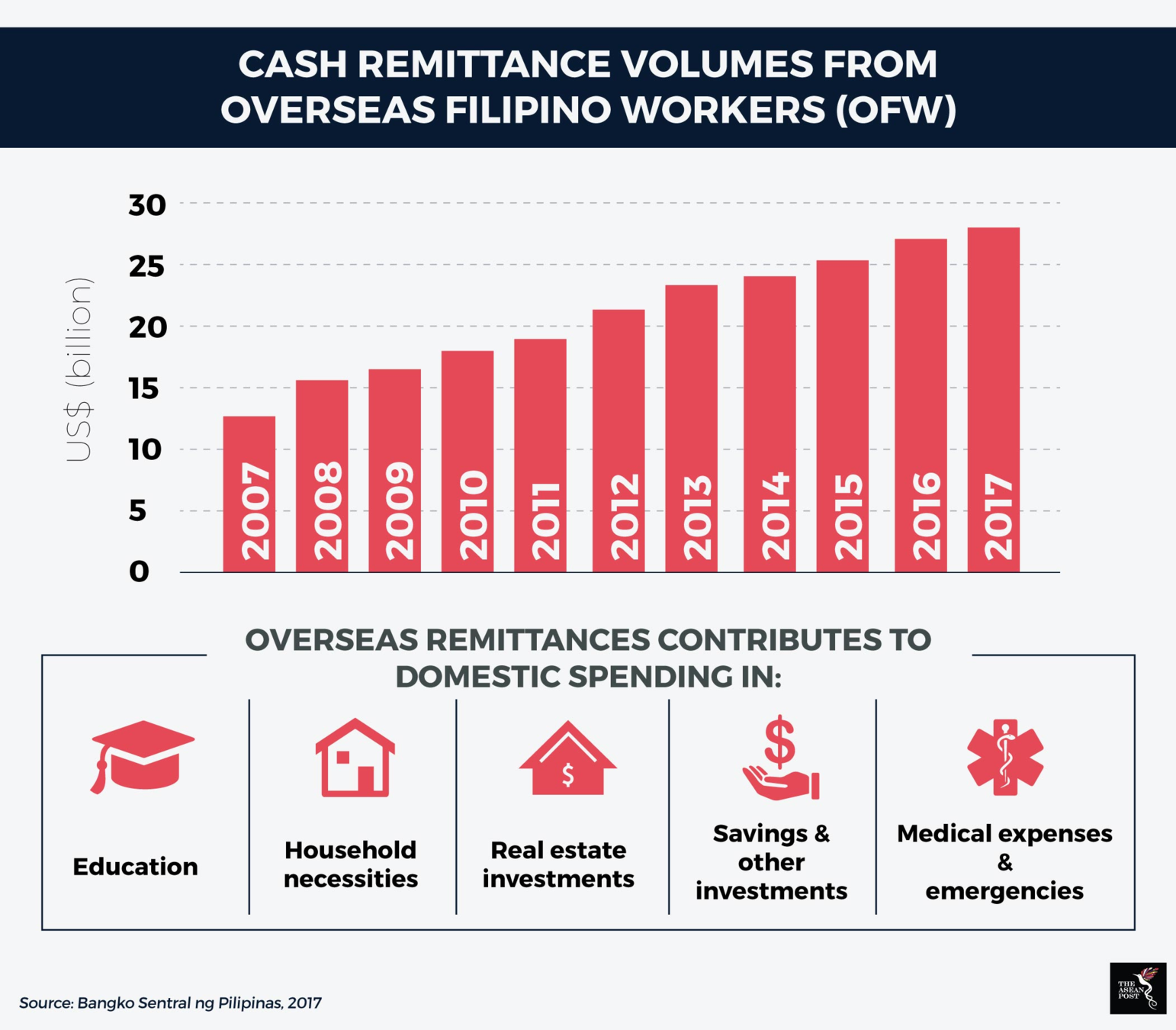

International remittances: $600B (U.S.) p.a.

all in: 10% fees

to be fair: remittances to date don't even work for internationally operating banks

Source: How can payments modernization benefit Canadian businesses? Evaluating the cost of payments processing; EY and Payments Canada, 2018

Source: How can payments modernization benefit Canadian businesses? Evaluating the cost of payments processing; EY and Payments Canada, 2018

https://www.youtube.com/embed/g1IqjY88YuM?enablejsapi=1

Cash-In

agent

Cash-Out

agent

and almost every other 905 tourist mall

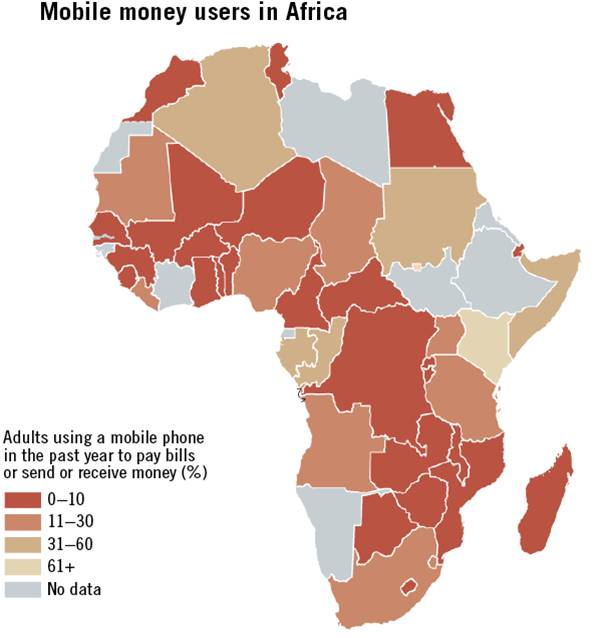

"To empower residents of India with a unique identity and a digital platform to authenticate anytime, anywhere."

UPI puts multiple bank accounts into a single mobile application (of any participating bank), merging several banking features, seamless fund routing & merchant payments under one hood.

Source: Seizing The Opportunity: Building The Toronto Region Into A Global Fintech Leader; TFI/Deloitte/McMillian 2019

Source: Seizing The Opportunity: Building The Toronto Region Into A Global Fintech Leader; TFI/Deloitte/McMillian 2019

loyalty

Payment financing

mobile payment integration

mobile payments + rewards

connect advertising directly with immediate mobile purchasing option

personal payment management app

Payment financing + loyalty

Overall idea: increase visibility of payments across the supply chain and across internal business operations

property management and rent payments

B2B & inter-company real time payments

gig economy instant pay

fast vendor payment

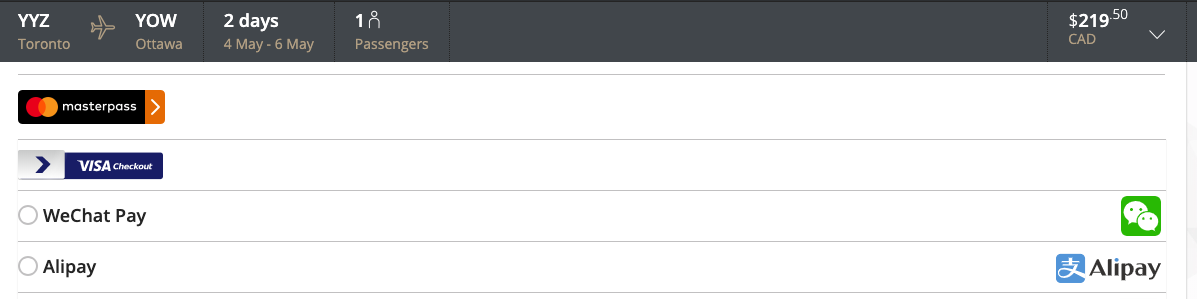

North American merchants connect to Chinese consumers who use WeChat & Alipay

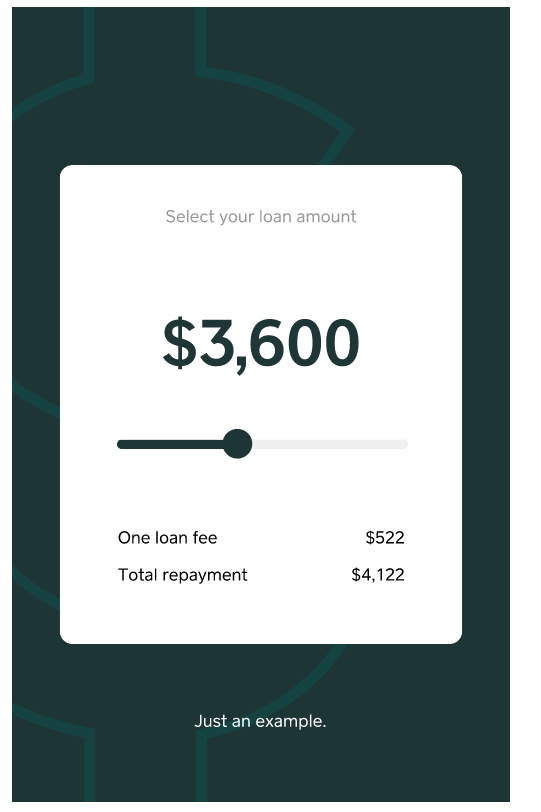

New frontier: revenue-based lending

14.5% interest - over what horizon?

Why we should be skeptical of untethered AI

Partnerships

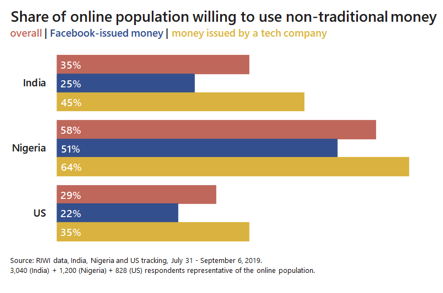

Source: Will Libra Succeed? Results of a Global Randomized Survey Experiment; by Danielle Goldfarb and yours truly

They have ZERO interest in becoming a financial institution/bank

\(\rightarrow\) no expertise

\(\rightarrow\) competitive market

\(\rightarrow\) one of the most regulated business environments

They are trying to deal with frictions that impede their business

They aim to collect data which will vastly improve their business

banking and payments activity require a banking license

need approval of the Finance Minister and the Office of the Superintendent of Financial Institutions (OSFI)

providing any financial service

acting as a financial agent

providing investment counselling or portfolio management services

issuing payment, credit, or charge cards,

operating a payment, credit, or charge card plan in co-operation with others (including other financial institutions)

granting of bank license has extensive list of regulatory criteria (subject to political interpretation)

takes 2 to 5 years to successfully acquire a banking license in Canada

Rogers applied in 2011 and was granted a Schedule I bank license in 2013

most FinTechs and PayTechs do not have the time or money to acquire a banking license

PayTech demonstrated use and purpose of prepaid card to regulator

OSFI rep had never seen one, not had any experience in dealing with the regulatory implications of this product.

OSFI and others do not have Fintechs and PayTechs in scope (not yet threat to the safety and soundness of the financial system).

EXAMPLE #1

regulatory compliance = lawyers

lawyers = second line of defence teams at FI

\(\Rightarrow\) decision makers have very little access to clients and the frontline.

EXAMPLE #2

good at general service and infrastructure

banks have very rigid ways of engaging with their clients, “they push information, they don’t take it”

\(\Rightarrow\) poor at customization and customer service

Banks' Modus Operandi

Premise of FinTech

start with customer needs and then build platforms

How much money is coming into and out of the account each month

Spending habits: what you spend money on and where you spend it

Payment habits: Are you paying bills way ahead of deadline or tardy?

Assess how much a customer spends on products of competitor and undermine competition

Pepper consumer with ads tailored to spending habits

Play on impulses and behavioral biases

Prying on the weak (payday loans)

create a comprehensive overview of balances for customer

keep tabs on expenses and income

show how much one can spend freely until next income

reminders or automated retirement savings when income arrives

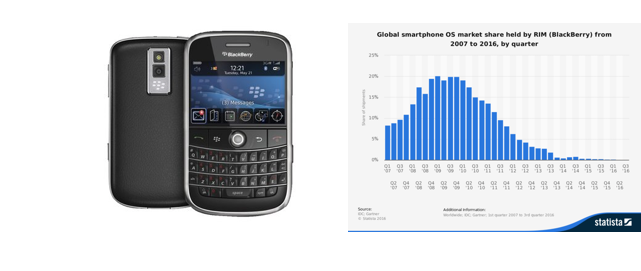

Nokia's market shares for devices:

What happened and can it happen to banks?

What did they pay for?

What do people value?

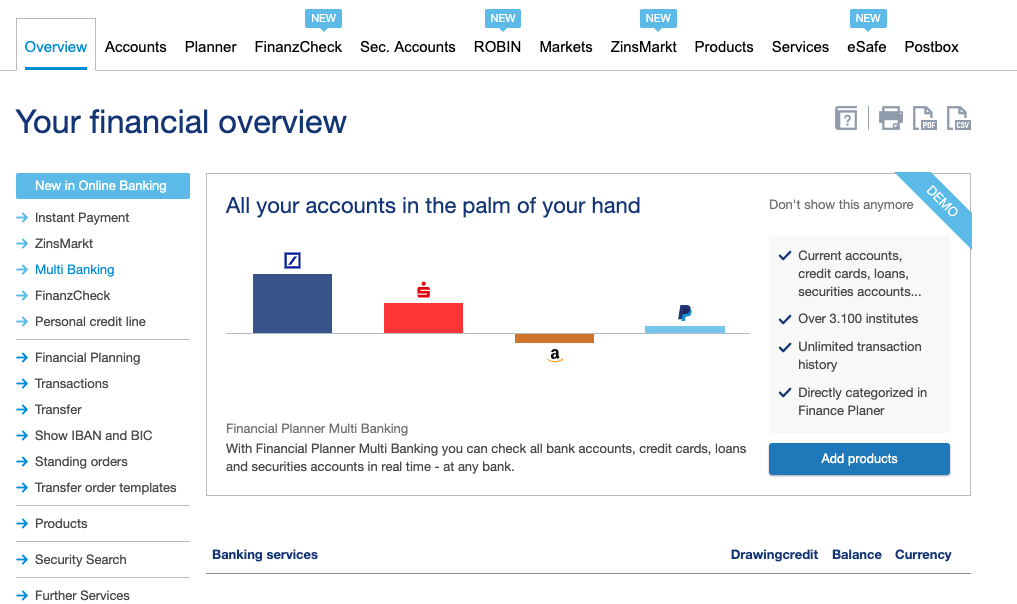

If banks move all data into "the cloud," why do we need banks?

Siloed banks

Cloud computing and cloud storage

Open banking and open data

The past (and the present?)

The present and near future

3-5 years in the future

5-10 years in the future

Platforms?

Banks?

Tech firms?

Sue's bank transfers from Sue's account to its own account

Bob's bank transfers from its account to Bob's account

Central Bank

Central bank transfers from Sue's bank's account to Bob's bank's account

Sue's bank transfers from Sue's account to its own account

Bob's bank transfers from its account to Bob's account

use the Swift network of correspondent banks

very complex

many parties

lots of frictions and points of failure

very expensive

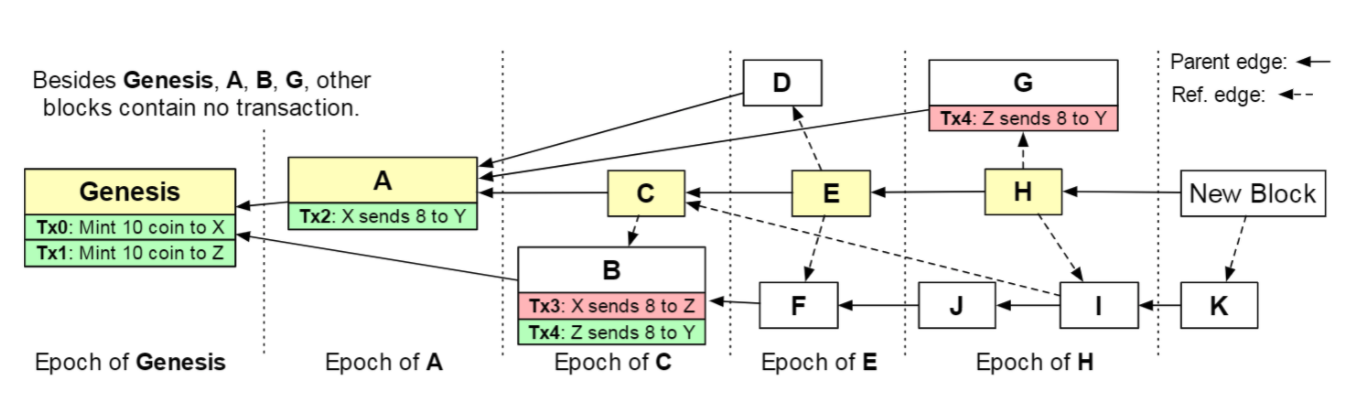

How do we agree on updating of the data?

Idea: mechanism to randomly select a proposer and have incentive to build on the correct past

Text

Source of picture: Cai, Long, Park, & Veneris (2020) (IEEE-BRAINS), original protocol: Li, Li, Zhou, Xu, Long, and Yao (2018)

Who gets to update?

Can a higher body prevent

transactions?

Can the past be altered?

consensus

immutability

censorship resistence

from Forbes

Azure Blockchain Tokens [...] lets enterprises, or anyone really, design, issue and manage a wide range of assets,

Currently, the platform is a permissioned version of the ethereum blockchain that uses Microsoft’s Azure cloud computing.

In the future Azure Blockchain Tokens will interact with the public Ethereum blockchain or even at distributed ledgers created by some of Microsoft’s own competitors.

blockchain \(\not=\) Bitcoin and blockchain \(\not=\) cryptocurrency

cryptocurrency \(\to\) attempt to bootstrap the network

blockchain is more than money - Ethereum is guaranteed execution of code

proof-of-work is horrible, but there are many efforts to get other systems to work

issuance of tokens

escrow contracts

auctions without an auctioneer

decentralized securities exchange

is not just about the money (Libra Coin)

NB:

| TPS | T per 12 hours | |

|---|---|---|

| Bitcoin | 7 | 302,400 |

| Ethereum | 30 | 1,296,000 |

| Athereum | 5000 | 216,000,000 |

| Algorand | 2000 | 86,400,000 |

| Payments Canada retail | 648 | 28,000,000 |

| US retail | 7639 | 330,000,000 |

| Canada number of equity trades | 46 | 2,000,000 |

| Orders on Canadian equity markets | 3588 | 155,000,000 |

| Conflux Network (Ethereum-like) | 3600 | 155,000,000 |

Sue wants to sell ABX

Bob wants to buy ABX

sell order

buy order

Clearing House

Stock Exchange

Broker

Broker

3rd party tech

custodian

custodian

record beneficial ownership

central bank for payment

BUT: more than money, also code execution and added functionality

each Libra coin will be backed by a basket of SIX fiat currencies

idea is conceptually similar to IMF Special Drawing Rights (pegged to USD, EUR, YEN, GBP, YUAN)

developed by a consortium of firms (e.g., Facebook, Uber) and not for profits (Creative Destruction Lab)

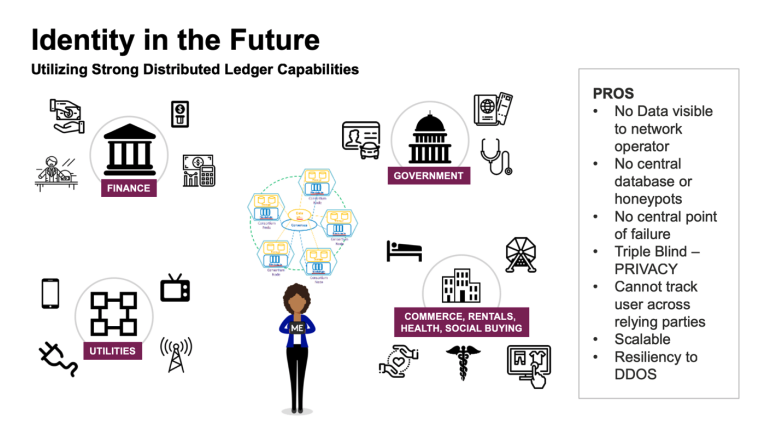

Source: Consumer Digital Identity Leveraging Blockchain, report to DIACC by Securekey

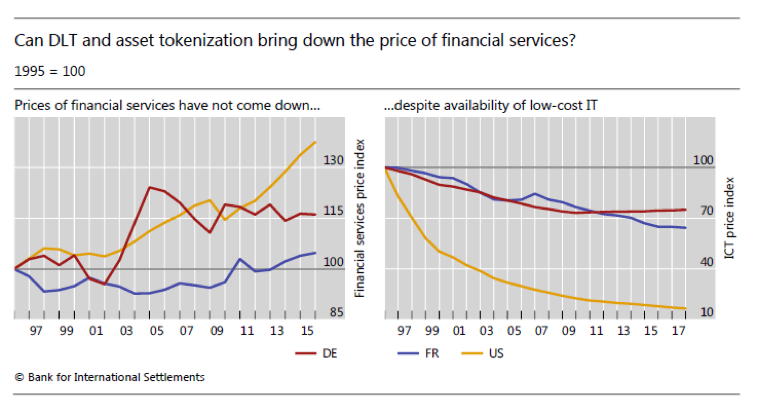

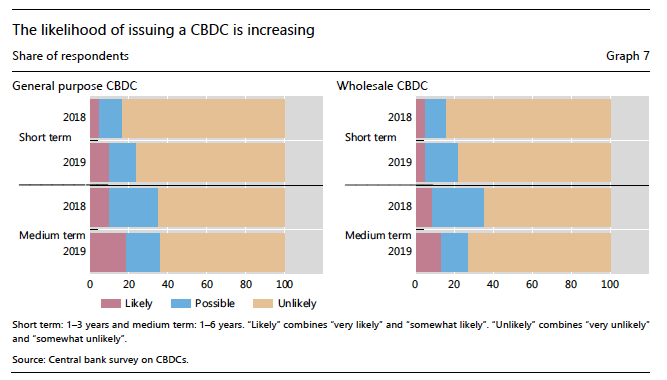

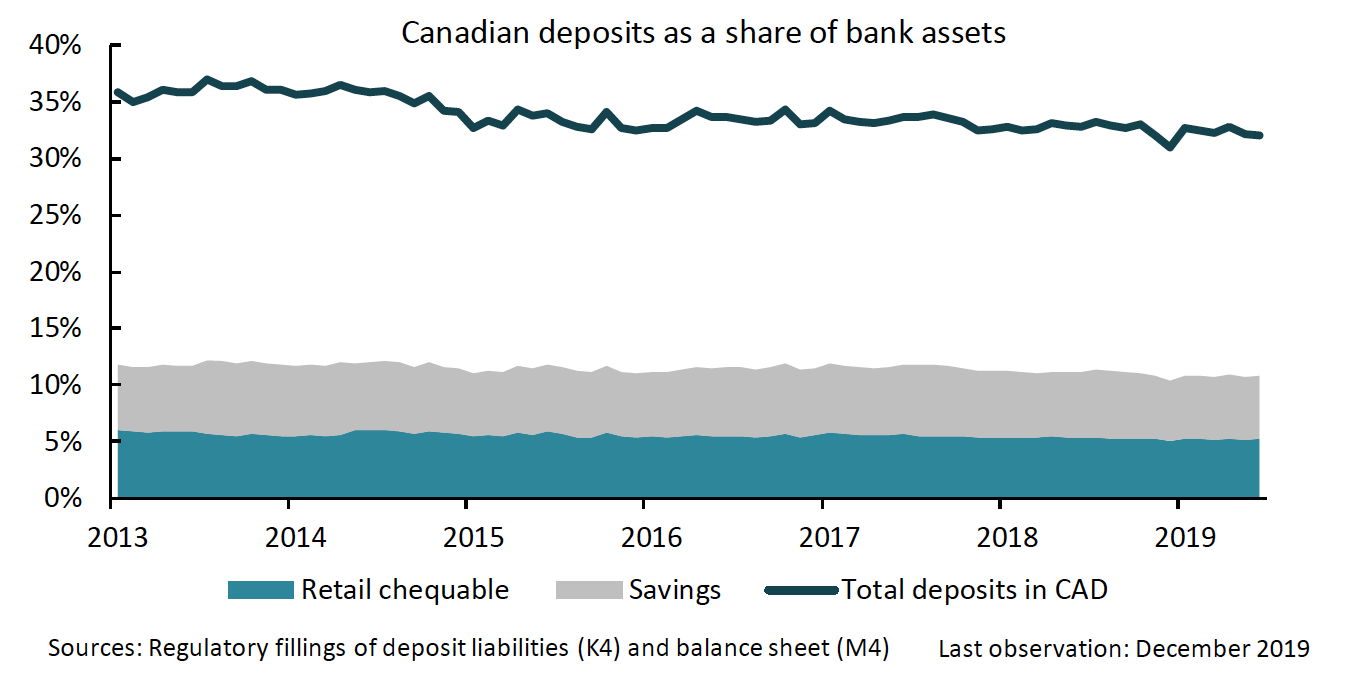

Source: BIS Quarterly Review, March 2020

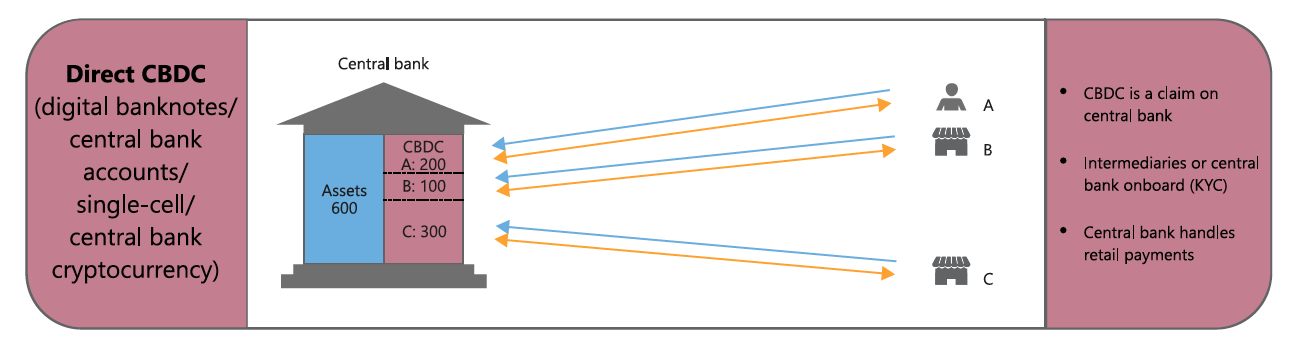

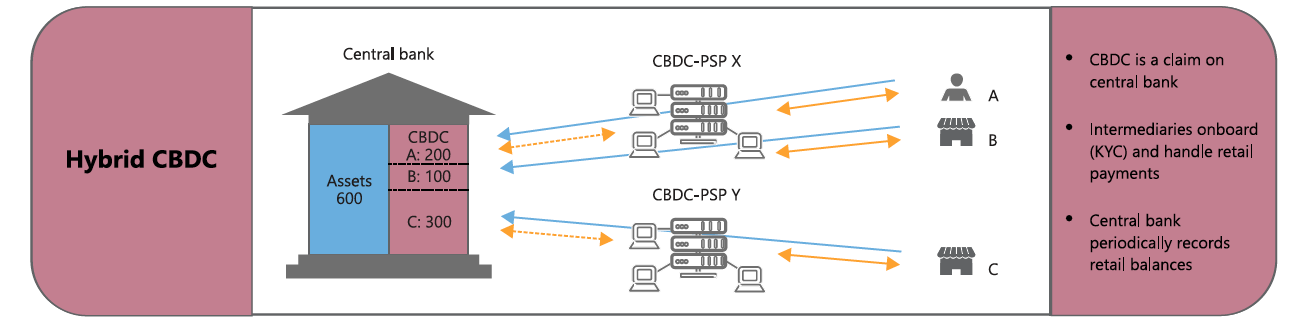

BoC analysis (August 2020):

*Bank of International Settlement: Belgium, Canada, France, Germany, Italy, Japan, the Netherlands, Sweden, Switzerland, the United Kingdom and the United States

merchant sends instructions for transaction

users sends/forwards authentication request and transaction instructions

Payments Canada sends reports to all parties

CPA Secure Network

Payments Canada checks with merchant's bank

Payments Canada instructs BoC to initiate transfer

keeps record of the transaction for 60 days

Source: How can payments modernization benefit Canadian businesses? Evaluating the cost of payments processing; EY and Payments Canada, 2018

Source: How can payments modernization benefit Canadian businesses? Evaluating the cost of payments processing; EY and Payments Canada, 2018

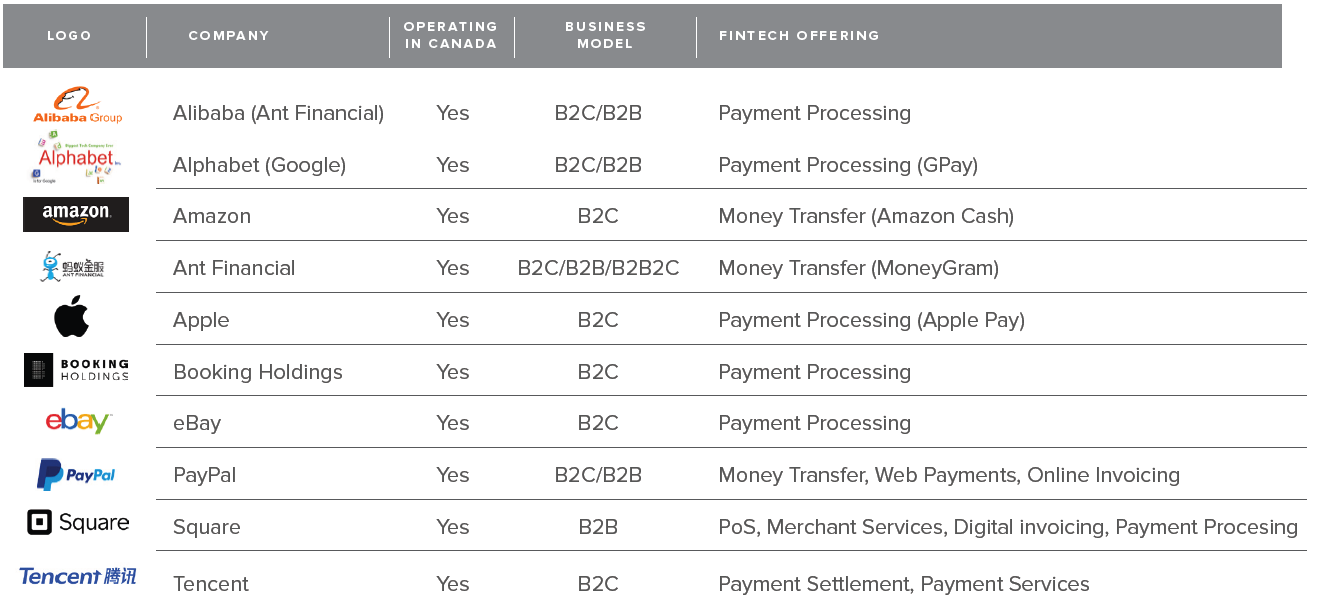

gig economy instant pay

fast vendor payment and B2B & inter-company real time payments

Koho Financial just taught us the risk for owners...

Source: How can payments modernization benefit Canadian businesses? Evaluating the cost of payments processing; EY and Payments Canada, 2018

Source: Accenture Consulting Open Banking in Canada: Opportunity Knocks

@financeUTM

andreas.park@rotman.utoronto.ca

slides.com/ap248

sites.google.com/site/parkandreas/

youtube.com/user/andreaspark2812/

By Andreas Park