Andreas Park PRO

Professor of Finance at UofT

Data: coinschedule

for comparison: total size of

Toronto Stock Exchange: $2,200B

Toronto Venture Exchange: $41B

\(x_i\)

\(x_j\)

\(x_k\)

\(c\)

\(MR=x-2q\)

\(p(q)=x-q\)

\(q^m=(x-c)/2\)

\(c\)

\(MR=x-2q\)

\(p(q)=x-q\)

\(q^m=q^e\)

general idea: sell future output

two approaches for token sales

\(c\)

\(MR\)

\(p(q)=x-q\)

\(q^{rs}<q^m\)

\(\alpha_t MR\)

\(c\)

\(MR\)

\(p(q)=x-q\)

\(q^{ps}>q^m\)

\(MR+t\)

\(c\)

\(MR\)

\(p(q)=x-q\)

\(q^t=q^m\)

\(\alpha_tMR+t\)

Presell \(t\) tokens.

If quantity produced \(q>t\), then share \(\alpha_t\) of revenue from incremental \(q-t\) tokens with tokenholders

As with equity, the entrepreneur receives the full NPV.

The entrepreneuer produces optimally at \(q^t=q^m\)

If \(q<t\) \(\Rightarrow\) redeem at rate \(t/q\) and tokenholders receive refund of \(c(t-q)\).

Idea:

entrepreneur can influence expected demand

with effort

without effort

assume \[\textit{NPV}(\theta_h)>0>\textit{NPV}(\theta_l)\]

equity holders

possibly break even

with effort

without effort

cannot break even

entrepreneur

earns \((1-\alpha_e)\ \frac{(\theta_h-c)^3}{12\theta_h} -C_e \)

with effort

without effort

earns \((1-\alpha_e) \frac{(\theta_l-c)^3}{12\theta_l}\)

\(>\) ?

exert effort iff

\[\textit{NPV}_h-C_e\ge \textit{NPV}_h\times\frac{\theta_h}{\theta_l}\left(\frac{\theta_l-c}{\theta_h-c}\right)^3\]

token holders

possibly break even

with effort

without effort

cannot break even

entrepreneur

earns \(\frac{c}{c+t} \frac{2}{3\theta_h}\left(\frac{\theta_h-c}{2}-t \right)^3 -C_e \)

with effort

without effort

earns \(\frac{c}{c+t} \frac{2}{3\theta_l}\left(\frac{\theta_l-c}{2}-t \right)^3\)

\(>\) ?

exert effort iff

\[\textit{NPV}_h-C_e\ge \textit{NPV}_h\times\frac{\theta_h}{\theta_l}\left(\frac{\theta_l-c-2t}{\theta_h-c-2t}\right)^3\]

key math insight

\[\textit{NPV}_h\times\frac{\theta_h}{\theta_l}\left(\frac{\theta_l-c}{\theta_h-c}\right)^3 >\textit{NPV}_h\times\frac{\theta_h}{\theta_l}\left(\frac{\theta_l-c-2t}{\theta_h-c-2t}\right)^3\]

@financeUTM

andreas.park@rotman.utoronto.ca

slides.com/ap248

sites.google.com/site/parkandreas/

youtube.com/user/andreaspark2812/

native to a blockchain for payment

examples: Bitcoin, Bitcoin Cash, Ether, Lumens, Cardano

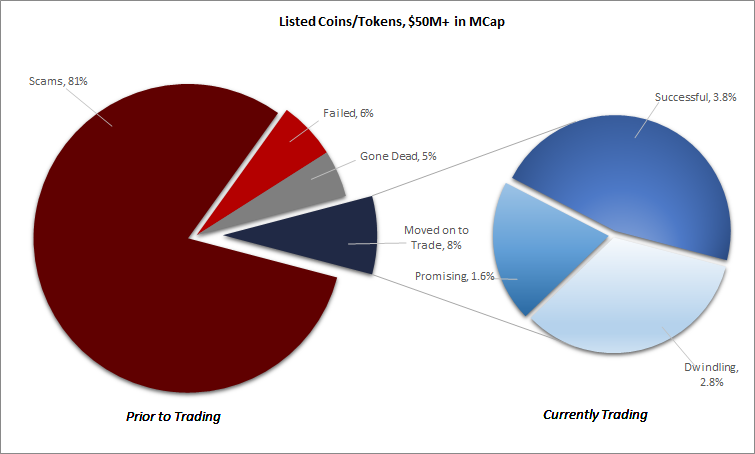

Source: Satis Group LLC

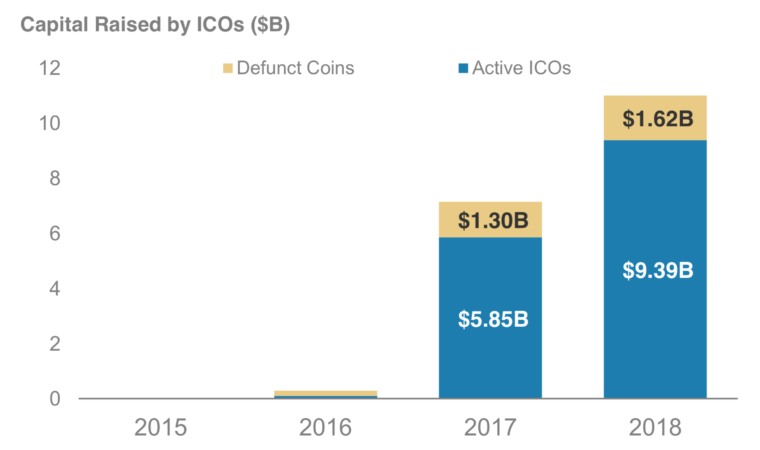

Source: Morgan Stanley (Nov 2018) “Update: Bitcoin, Cryptocurrencies and Blockchain”

By Andreas Park

This deck describes the key insights from a recent paper that Katya Malinova and I wrote on token vs. equity financing. The paper is available here: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3286825 and a summary is available here https://medium.com/@park.andreas/tokenomics-when-tokens-beat-equity-aa4c503bc5bd A narrated version is on YouTube: https://www.youtube.com/watch?v=52giUWmgxN0&feature=youtu.be