federica bianco PRO

astro | data science | data for good

State Space Models and MCMC

Fall 2022 - UDel PHYS 667

dr. federica bianco

@fedhere

combinatorial statistics

Bayes' theorem

optimization

gradient descent

stochastic gradient descent

MCMC

space state models for time series analysis

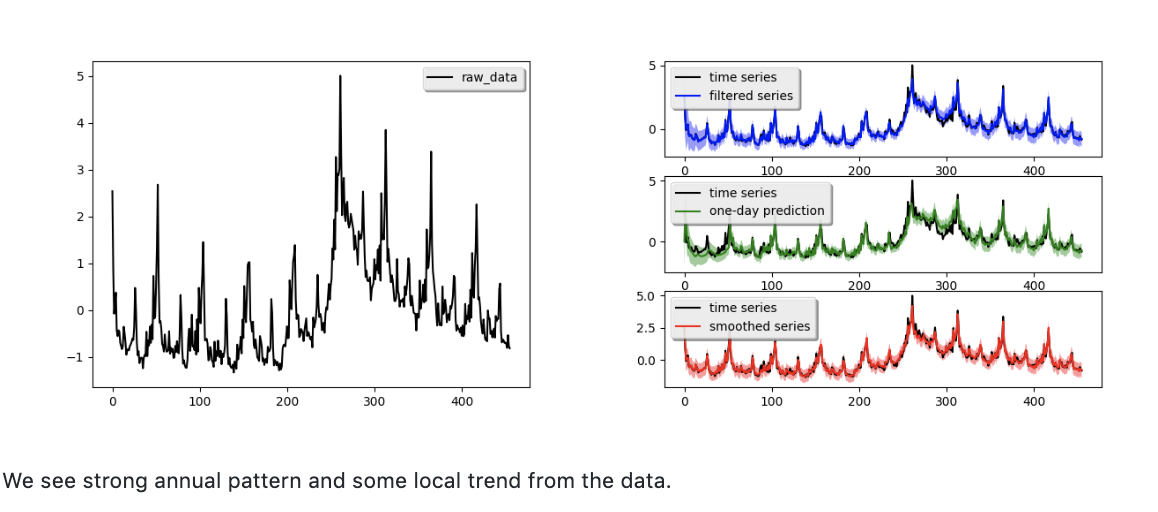

BSTS fitting

includes descriptions of the local linear trend and seasonal state models, as well as spike and slab priors for regressions with large numbers of predictors.

describes a situation where the local level and local linear trend models would be inappropriate. It offers a semilocal linear trend model as an alternative.

describes a model where the response variable is non-Gaussian. The goal in Example 3 is not to predict the future, but to control for serial dependence in an explanatory model that seeks to identify relevant predictor variables.

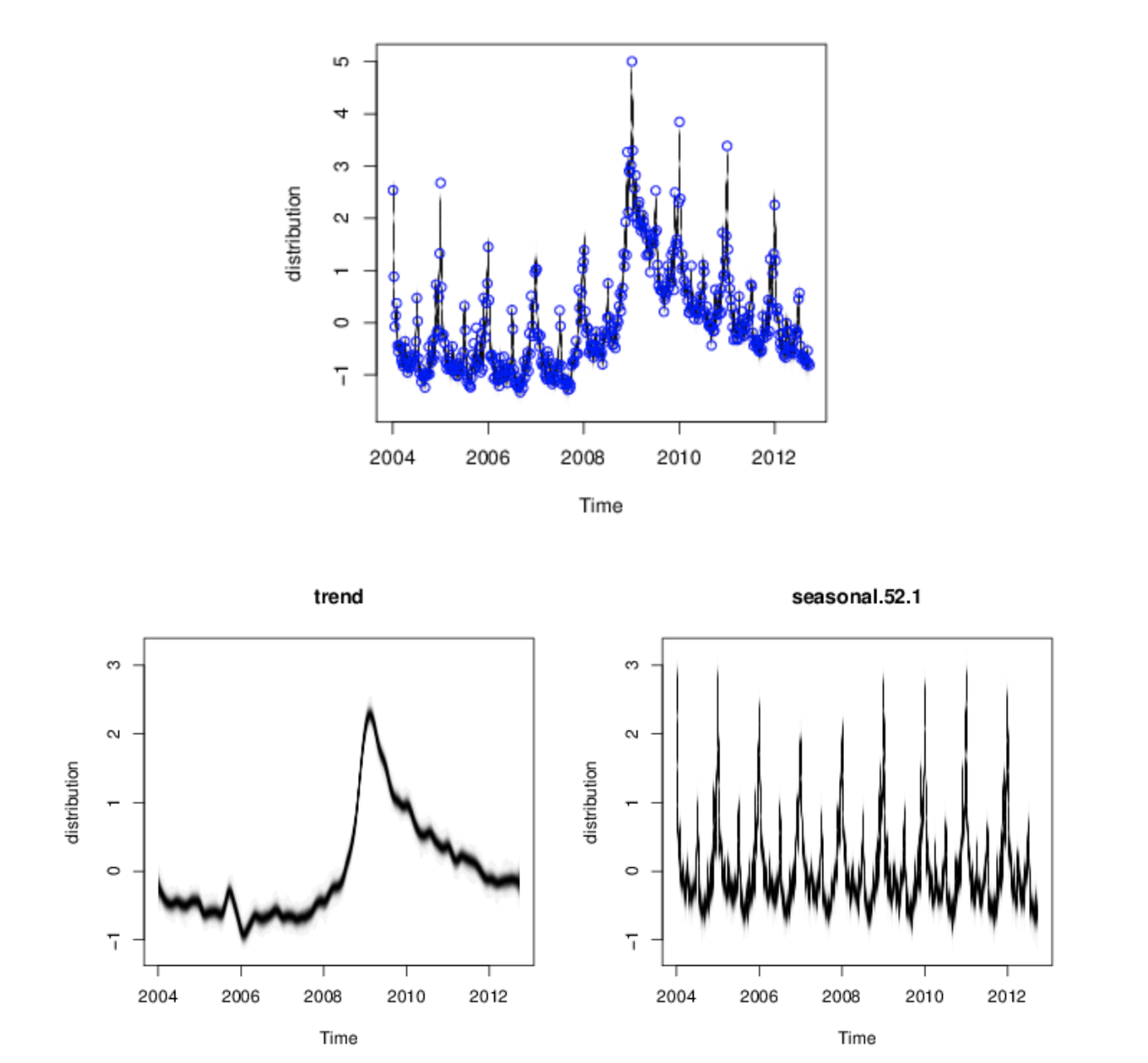

Weekly initial claims for unemployment in the US.

Scott and Varian (2014, 2015)

+

Weekly initial claims for unemployment in the US.

Scott and Varian (2014, 2015)

this slide deck:

Model fit:

Optimization and Likelihood

1

change a, b to minimize χ2

Target Funcion

Linear regression

Target Funcion

Univariate Linear regression

b

a

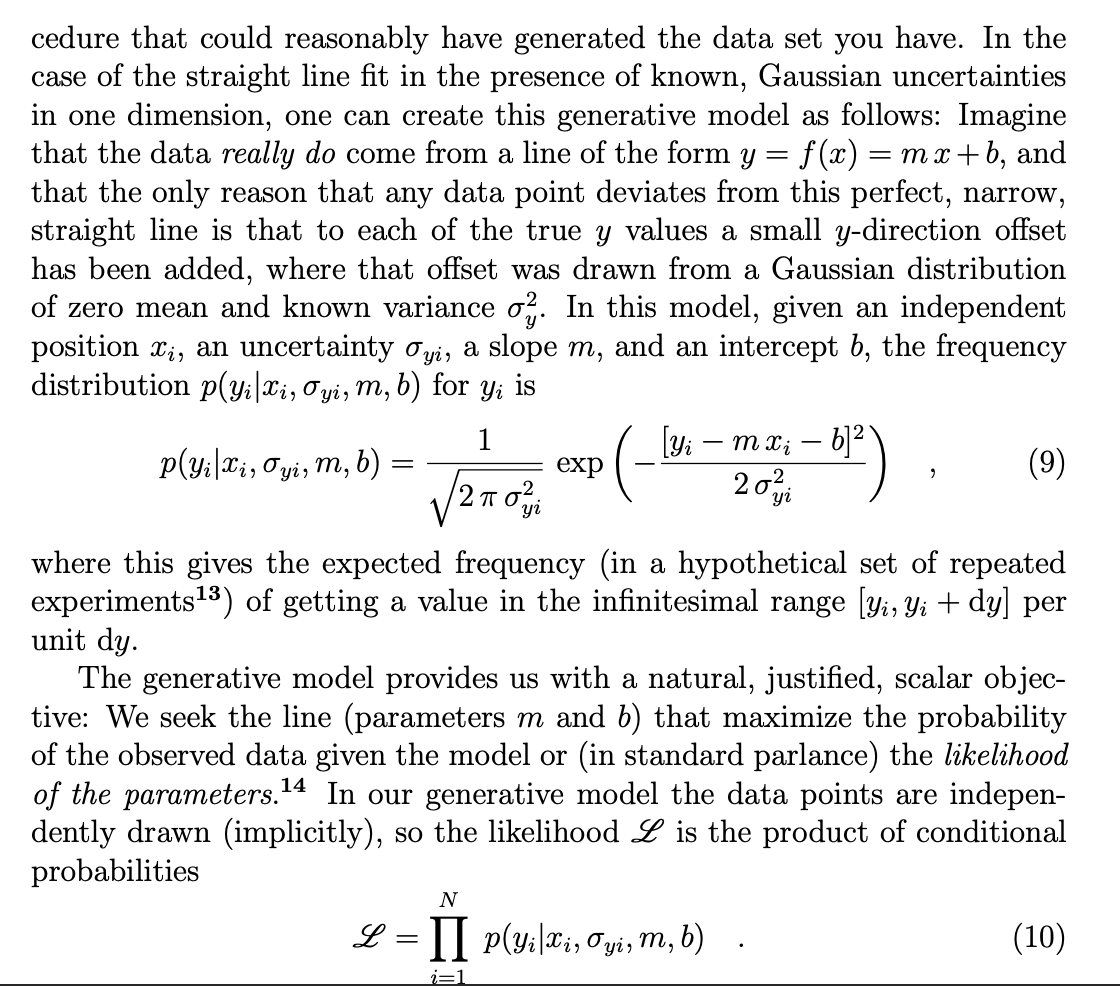

Gaussian

Probability of data given a model, e.g. Gaussian

Maximizing the likelihood we seek the parameters that maximize the probability of the observed data under the chosen model

Likelihood: the probability of the model given the data. Same Gaussian assumptions

unknown variables

unknown variables

Target Funcion

Univariate Linear regression

b

a

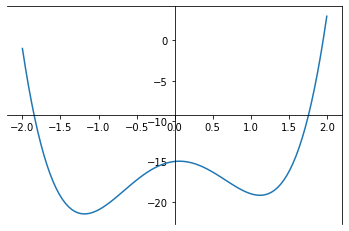

Gradient descent is an iterative algorithm, that starts from a random point on a function and travels down its slope in steps until it reaches the lowest point of that function.

(Toward data science)

Target Funcion

Univariate Linear regression

b

a

Gradient Descent

gradient descent algorithm

"convergence" is reached when the gradient is ~0: with ε tollrance

Target Funcion

Univariate Linear regression

Gradient Descent

Target Funcion

Univariate Linear regression

b

a

Target Funcion

Univariate Linear regression

b

a

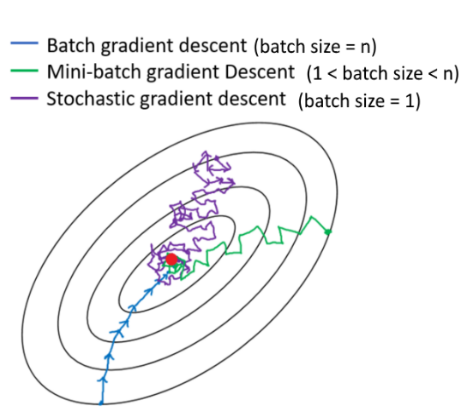

Add stochasticity to avoid getting stuck in a local minimum

stochastic gradient descent algorithm

"convergence" is reached when the gradient is ~0: with ε tollrance

stochastic gradient descent algorithm

"convergence" is reached when the gradient is ~0: with ε tollrance

stochastic gradient descent algorithm

gradient descent algorithm

Target Funcion

Univariate Linear regression

Stochastic Gradient Descent

where i are elements of the full N-dimensional observation set (a subset)

Target Funcion

Univariate Linear regression

b

a

idea 2. start a bunch of parallel optimizations

(we will see it in next class)

Bayes Theorem &

Bayesian statistics

2

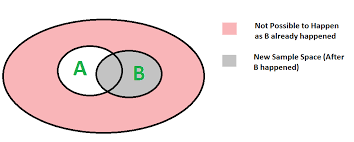

probability of A conditioned on B

probability of A conditioned on B

probability of A conditioned on B

probability of A conditioned on B

A and B are independent

probability of A conditioned on B

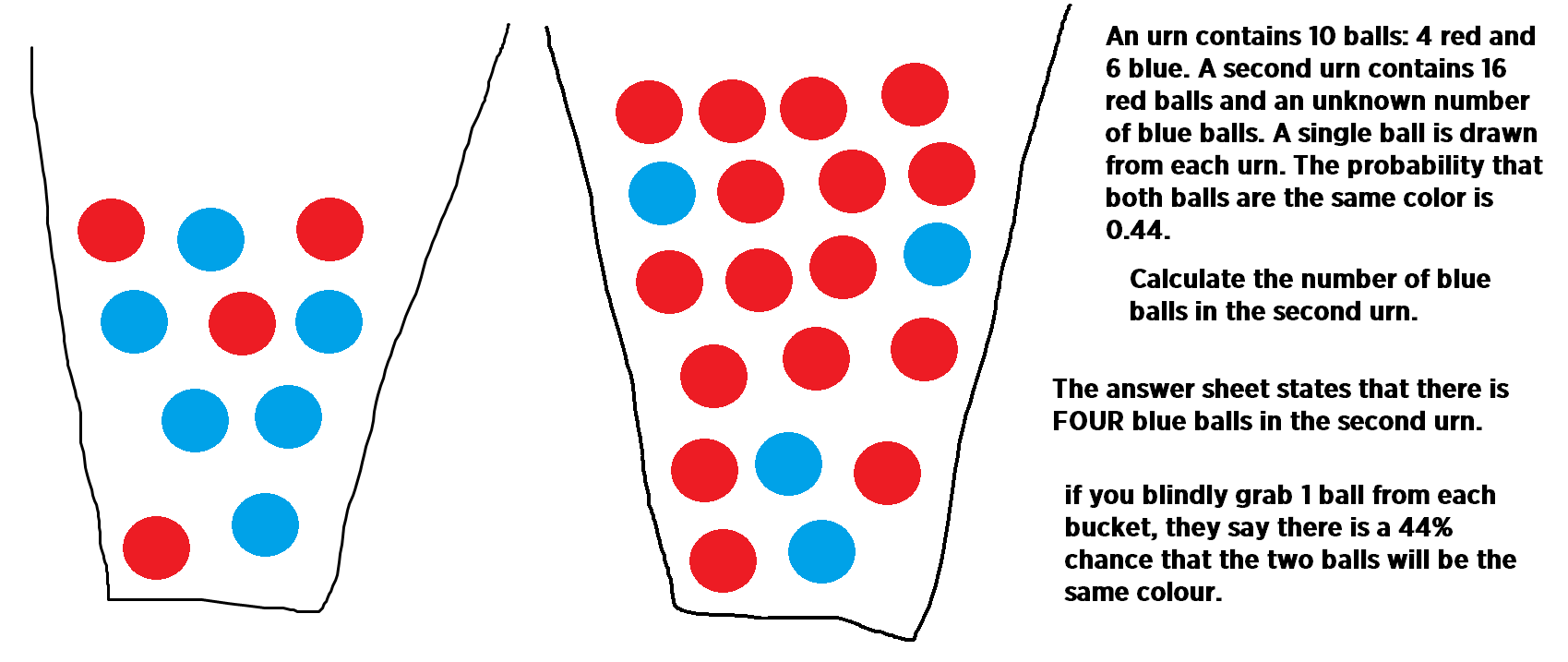

A=red; B=blue

probability of A conditioned on B

A=red; B=blue

probability of A conditioned on B

new sample space after B happened

A

B

posterior

likelihood

prior

evidence

model parameters

data

D

constraints on the model

e.g. flux from a star is never negative

P(f<0) = 0 P(f>=0) = 1

prior:

model parameters

data

D

model parameters

data

D

prior:

constraints on the model

people's weight <1000lb

& people's weight >0lb

P(w) ~ N(105lb, 90lb)

model parameters

data

D

prior:

constraints on the model

people's weight <1000lb

& people's weight >0lb

P(w) ~ N(105lb, 90lb)

the prior should not be 0 anywhere the probability might exist

model parameters

data

D

prior:

"uninformative prior"

model parameters

data

D

prior:

"uninformative prior"

likelihood:

this is our model

model parameters

data

D

evidence

????

model parameters

data

D

evidence

????

model parameters

data

D

it does not matter if I want to use this for model comparison

model parameters

data

D

it does not matter if I want to use this for model comparison

which has the highest posterior probability?

posterior: joint probability distributin of a parameter set (θ, e.g. (m, b)) condition upon some data D and a model hypothesys f

evidence: marginal likelihood of data under the model

prior: “intellectual” knowledge about the model parameters condition on a model hypothesys f. This should come from domain knowledge or knowledge of data that is not the dataset under examination

posterior: joint probability distributin of a parameter set (θ, e.g. (m, b)) condition upon some data D and a model hypothesys f

evidence: marginal likelihood of data under the model

prior: “intellectual” knowledge about the model parameters condition on a model hypothesys f. This should come from domain knowledge or knowledge of data that is not the dataset under examination

in reality all of these quantities are conditioned on the shape of the model: this is a model fitting, not a model selection methodology

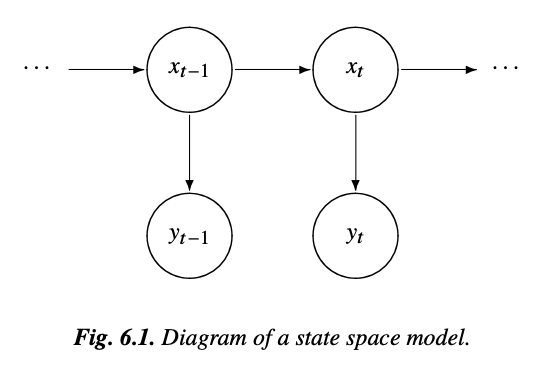

State Space Model

4

motion equations for the position or "state" of a spacecraft

x(t): location

y(t): information that can be observed from a tracking device such as velocity and azimuth

unobserved state

Underlying state x is a time varying Markovian process (the position of the spacecraft)

The observed variable depends at least on the state and on noise.

Other elements (e.g. seasonality) can be included in the model too

we can write a Bayesian structural model like this:

local level

state

seasonal trend

we can write a Bayesian structural model like this:

seasonal variations

unobserved trend

Its a Markovian Process:

stochastic process with 1-step memory

there is a hidden or latent process xt called the state process (the position of the space craft)

a bit more complex

A model that accepts regression on exogenous variables allows feature extraction: which features are important in the prediction?

e.g. CO2 or Irradiance in climate change (HW)

Model Optimization

with MCMC

5

stochastic

"markovian"

sequence

posterior: joint probability distributin of a parameter set (m, b) conditioned upon some data D and a model hypothesys f

Goal: sample the posterior distribution

slope

intercept

slope

Goal: sample the posterior distribution

choose a starting point in the parameter space: current = θ0 = (m0,b0)

WHILE convergence criterion is met:

calculate the current posterior pcurr = P(D|θ0,f)

//proposal

choose a new set of parameters new = θnew = (mnew,bnew)

calculate the proposed posterior pnew = P(D|θnew,f)

IF pnew/pcurr < 1:

current = new

ELSE:

//probabilistic step: accept with probability pnew/pcurr

draw a random number r ૯U[0,1]

IF r > pnew/pcurr >:

current = new

ELSE:

pass // do nothing

stochasticity allows us to explore the whole surface but spend more time in interesting spots

Goal: sample the posterior distribution

choose a starting point in the parameter space: current = θ0 = (m0,b0)

WHILE convergence criterion is met:

calculate the current posterior pcurr = P(D|θ0,f)

//proposal

choose a new set of parameters new = θnew = (mnew,bnew)

calculate the proposed posterior pnew = P(D|θnew,f)

IF pnew/pcurr > 1:

current = new

ELSE:

Questions:

1. how do I choose the next point?

Any Markovian ergodic process

choose a starting point in the parameter space: current = θ0 = (m0,b0)

WHILE convergence criterion is met:

calculate the current posterior pcurr = P(D|θ0,f)

//proposal

choose a new set of parameters new = θnew = (mnew,bnew)

calculate the proposed posterior pnew = P(D|θnew,f)

IF pnew/pcurr > 1:

current = new

ELSE:

//probabilistic step: accept with probability pnew/pcurr

draw a random number r ૯U[0,1]

IF r > pnew/pcurr >:

current = new

ELSE:

pass // do nothing

choose a starting point in the parameter space: current = θ0 = (m0,b0)

WHILE convergence criterion is met:

calculate the current posterior pcurr = P(D|θ0,f)

//proposal

choose a new set of parameters new = θnew = (mnew,bnew)

calculate the proposed posterior pnew = P(D|θnew,f)

IF pnew/pcurr > 1:

current = new

ELSE:

//probabilistic step: accept with probability pnew/pcurr

draw a random number r ૯U[0,1]

IF r > pnew/pcurr >:

current = new

ELSE:

pass // do nothing

A process is Markovian if the next state of the system is determined stochastically as a perturbation of the current state of the system, and only the current state of the system, i.e. the system has no memory of earlier states (a memory-less process).

(given enough time) the entire parameter space would be sampled.

At equilibrium, each elementary process should be equilibrated by its reverse process.

reversible Markov process

Detailed Balance is a sufficient condition for ergodicity

Metropolis Rosenbluth Rosenbluth Teller 1953 - Hastings 1970

If the chains are a Markovian Ergodic process

the algorithm is guaranteed to explore the entire likelihood surface given infinite time

This is in contrast to gradient descent, which can get stuck in local minima or in local saddle points.

how to choose the next point

how you make this decision names the algorithm

simulated annealing (good for multimodal)

parallel tempering (good for multimodal)

differential evolution (good for covariant spaces)

Gibbs sampling (move in along one variable at a time)

choose a starting point in the parameter space: current = θ0 = (m0,b0)

WHILE convergence criterion is met:

calculate the current posterior pcurr = P(D|θ0,f)

//proposal

choose a new set of parameters new = θnew = (mnew,bnew)

calculate the proposed posterior pnew = P(D|θnew,f)

IF pnew/pcurr > 1:

current = new

ELSE:

//probabilistic step: accept with probability pnew/pcurr

draw a random number r ૯U[0,1]

IF r > pnew/pcurr >:

current = new

ELSE:

pass // do nothing

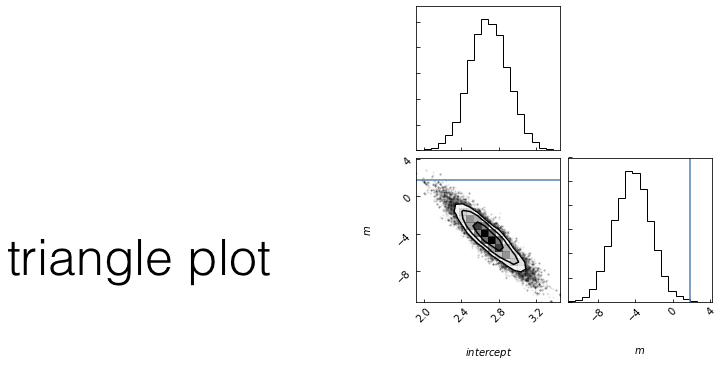

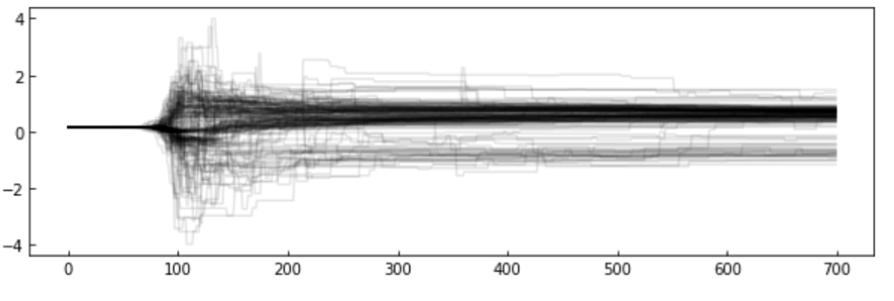

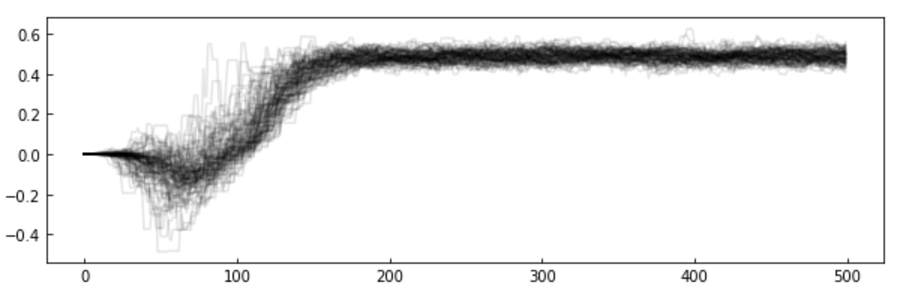

The chains: the algorithm creates a "chain" (a random walk) that "explores" the likelihood surface.

More efficient is to run many parallel chains - each exploring the surface, an "ensemble"

The path of the chains can be shown along each feature

choose a starting point in the parameter space: current = θ0 = (m0,b0)

WHILE convergence criterion is met:

calculate the current posterior pcurr = P(D|θ0,f)

//proposal

choose a new set of parameters new = θnew = (mnew,bnew)

calculate the proposed posterior pnew = P(D|θnew,f)

IF pnew/pcurr > 1:

current = new

ELSE:

//probabilistic step: accept with probability pnew/pcurr

draw a random number r ૯U[0,1]

IF r > pnew/pcurr >:

current = new

ELSE:

pass // do nothing

step

feature value

Examples of how to choose the next point

affine invariant : EMCEE package

choose a starting point in the parameter space: current = θ0 = (m0,b0)

WHILE convergence criterion is met:

calculate the current posterior pcurr = P(D|θ0,f)

//proposal

choose a new set of parameters new = θnew = (mnew,bnew)

calculate the proposed posterior pnew = P(D|θnew,f)

IF pnew/pcurr > 1:

current = new

ELSE:

//probabilistic step: accept with probability pnew/pcurr

draw a random number r ૯U[0,1]

IF r > pnew/pcurr >:

current = new

ELSE:

pass // do nothing

step

feature value

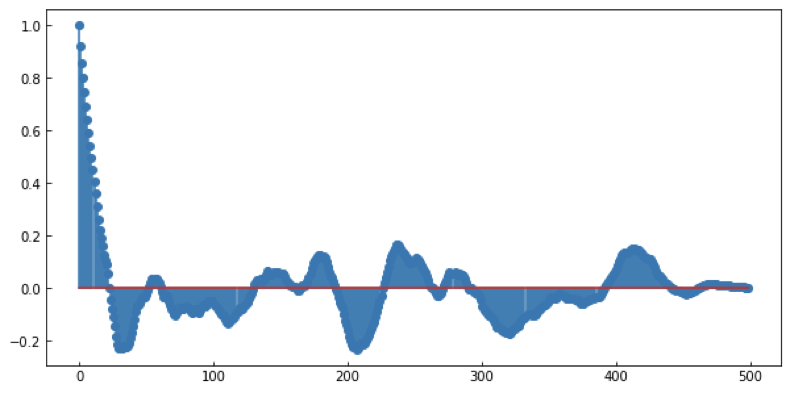

MCMC convergence

MCMC convergence

MCMC convergence

MCMC convergence

MCMC convergence

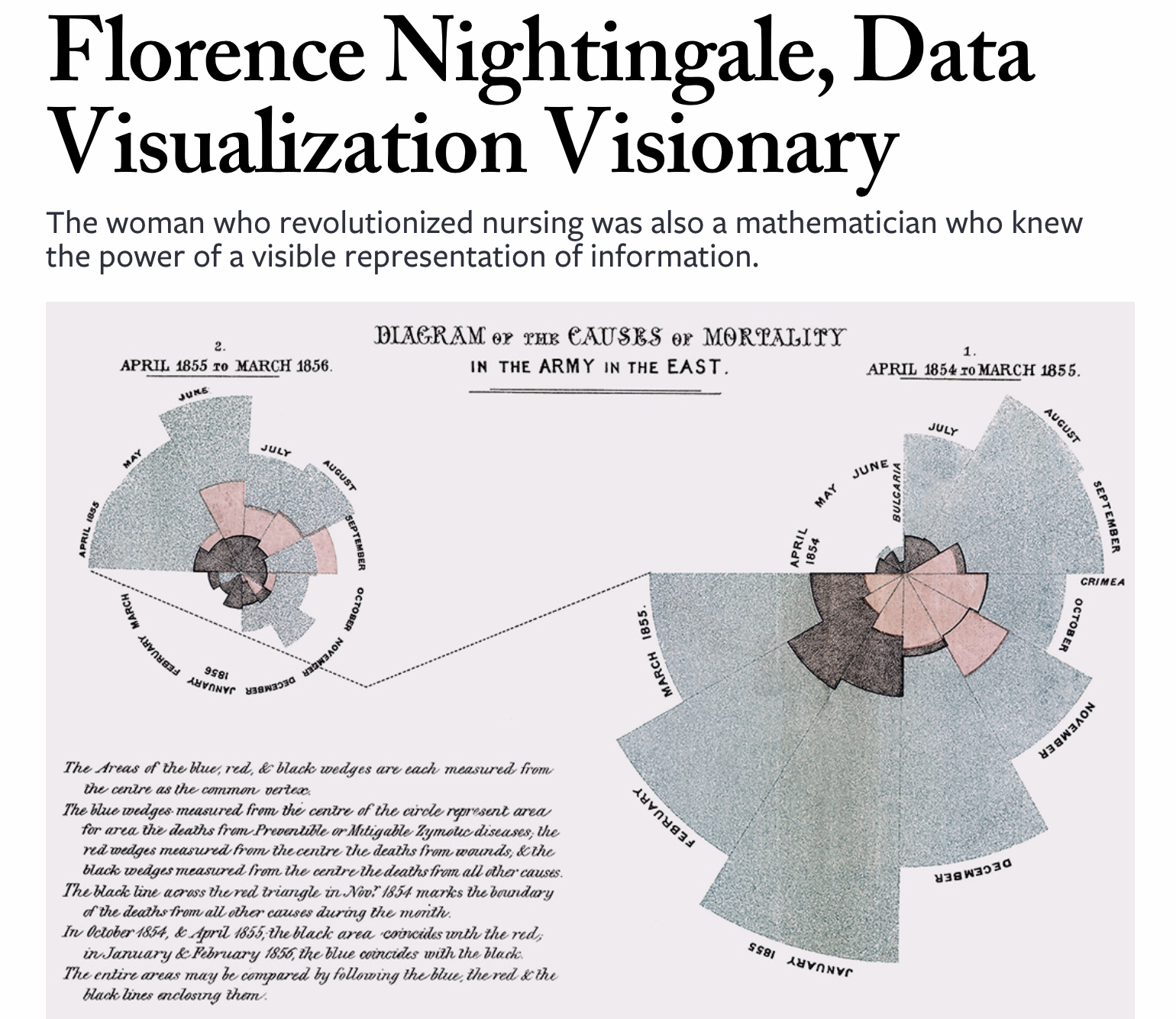

OF THE WEEK

when to do circles?

cyclic visualizations

(annual behavior)

when you do not want to impress importance on the hierarchical time order

Elements of Statistical Learning Chapter 7

https://towardsdatascience.com/implementing-facebook-prophet-efficiently-c241305405a3

By federica bianco

Bayes theorem and MCMC