Jason Dobry

Husband. Father. Software Engineer. Open Source hacker. Always learning.

By Jason Dobry

Autopilot

Tracking and Vertex Fitting of charged particles in Particle Detectors

Tracking of objects in computer vision

Economics, in particular macroeconomics, time series, and econometrics

Inertial guidance system

Orbit Determination

Radar tracker

Dynamic positioning &

Navigation systems

Seismology

Simultaneous localization and mapping

Speech enhancement, Weather forecasting, 3D modeling

By Jason Dobry

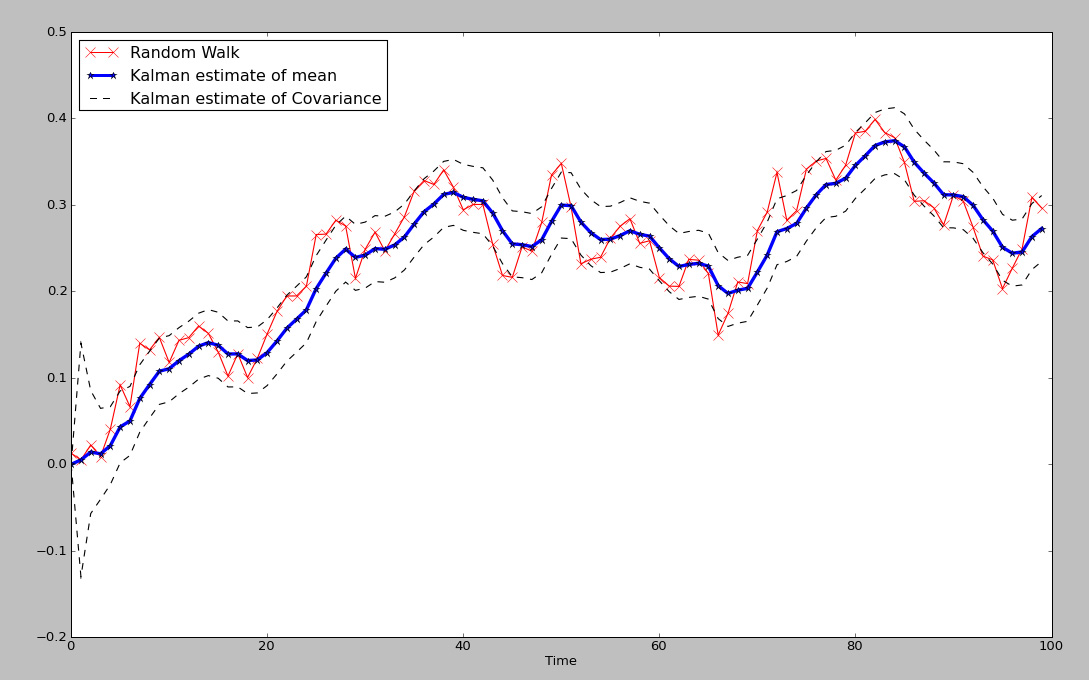

Portfolio Optimization with Kalman Filters