illicit financial flowS and micro data

who is the largest investor in germany?

who is the largest investor in brazil?

who is the largest investor in south africa?

why?

Spoiler: Tax avoidance

professionals

corporate entities

state

PARt 1: The corporations

corporate ownership is complex

Garcia-Bernardo, J., Fichtner, J., Takes, F. W., & Heemskerk, E. M. (2017). Uncovering offshore financial centers: Conduits and sinks in the global corporate ownership network. Scientific Reports, 7(1), 1-10.

Work with Valeria Secchini (PhD candidate at COPTAX, Charles University)

modeling corporate structures with higher-order dependencies

Work with Valeria Secchini (PhD candidate at COPTAX, Charles University)

modeling corporate structures with higher-order dependencies

Xu, Jian, Thanuka L. Wickramarathne, and Nitesh V. Chawla. "Representing higher-order dependencies in networks." Science advances 2.5 (2016): e1600028.

Kullback-Leibler divergence

Problem: overfitting

(high number of false positives)

On realistic synthetic data:

Precision: 10%

Sensitivity: 80%

Our solution: Train/Validation approach

Find in the training, keep if it holds in validation

Jensen–Shannon divergence

Depends on frequency of each higher-order dependency, and the variability in train/test

On realistic synthetic data:

Precision: 70%

Sensitivity: 50%

<

-

Open questions:

How to derive the thresholds (δ) theoretically?

How to handle heterogeneity? Higher-order dependencies may be "owner dependent" (the first node in the chain)

How to handle time series? (e.g. detect changes in structures, measure effect of policy)

(lots on results: community, ranking, simulation)

Results:

Applied to multinational corporations

70 patterns, 75% containing a tax haven

p.

p.

p.

PARt 2: the professionals

- Corporate structures are created by tax professionals:

- Set up the entity

- Provide directors

- Manage the accounts

- In the Netherlands: Trust Industry (trustkantoren)

- 94% of the services are provided to foreign companies

- 250,592 entities in 100 addresses

- Providing trust services requires a license

- But it is expensive + compliance

8150 companies

9.3/window

facilitators are key

How many illegal trust service providers are in the netherlands?

detect them based on their network

Garcia-Bernardo, Javier, Joost Witteman, and Marilou Vlaanderen. "Uncovering the size of the illegal corporate service provider industry in the Netherlands: a network approach." EPJ Data Science 11.1 (2022): 23.

Strategy:

- Build network features

- Find similar directors to those from a licensed trust

- Manually annotate a sample

- Robustness test

Open questions:

Better way to find illegal directors? (maybe GNNs)

Motifs mining: What are some motifs linked to providing trust services

(lots on applications: e.g., suspicious transactions)

Results:

Illegal trust service providers:

- 31-51% of total number of trust service providers

- 19-27% of all companies managed

PARt 3: The state

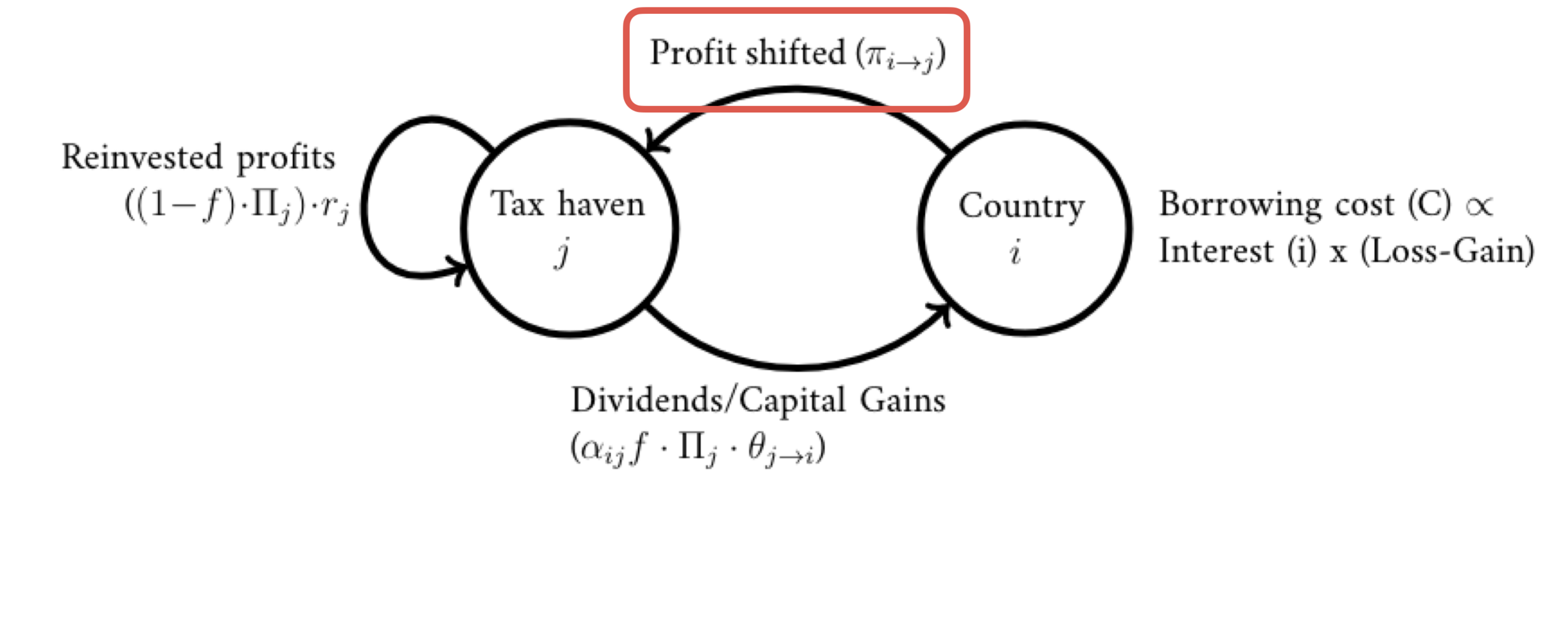

what type of country lose the most from tax avoidance?

Garcia-Bernardo, Javier, and Petr Janský. "Profit shifting of multinational corporations worldwide." arXiv preprint arXiv:2201.08444 (2022).

Cost = (Profits shifted out - Profits shifted in) * Tax rate / GDP

Garcia-Bernardo, J., Haberly, D., Janský, P., Palanský, M., & Secchini, V. (2022). The indirect costs of corporate tax avoidance exacerbate cross-country inequality (No. 2022/33). WIDER Working Paper.

Garcia-Bernardo, J., Haberly, D., Janský, P., Palanský, M., & Secchini, V. (2022). The indirect costs of corporate tax avoidance exacerbate cross-country inequality (No. 2022/33). WIDER Working Paper.

Garcia-Bernardo, J., Haberly, D., Janský, P., Palanský, M., & Secchini, V. (2022). The indirect costs of corporate tax avoidance exacerbate cross-country inequality (No. 2022/33). WIDER Working Paper.

Garcia-Bernardo, J., Haberly, D., Janský, P., Palanský, M., & Secchini, V. (2022). The indirect costs of corporate tax avoidance exacerbate cross-country inequality (No. 2022/33). WIDER Working Paper.

Garcia-Bernardo, J., Haberly, D., Janský, P., Palanský, M., & Secchini, V. (2022). The indirect costs of corporate tax avoidance exacerbate cross-country inequality (No. 2022/33). WIDER Working Paper.

developing countries lose more

Open questions:

How to implement policy interventions in the model?

How to calibrate the model to find time trends?

summary

- Wealth inequality is rising

- Tax avoidance is key

- Complex corporate structures are used for it

- Network science tools help us:

- Understand how they organize (higher order dependencies)

- Estimate which countries gain/lose

- Detect facilitators

Image: R-package signet

Covid spread on family & school networks

with RIVM, ministry of health, Christine Hedde-von Westernhagen

Experiments on information spread in networks

with: Zohar Neu, Mathew Hardy, Tom Griffiths, Aleksandra AloriĆ,

P.M. Krafft, Andrea Santoro, Allison Morgan

Detecting organized groups in social networks Polarization in signed networks with: Sofia Chelmi, Elena Candellone, Erik-Jan van Kesteren, Shazia Babul

summary

- Wealth inequality is rising

- Tax avoidance is key

- Complex corporate structures are used for it

- Network science tools help us:

- Understand how they organize (higher order dependencies)

- Estimate which countries gain/lose

- Detect facilitators

Javier García-Bernardo

javier@duck.com

NetSci

By Javier GB

NetSci

Presentation for the dutch network science society