Katya Malinova PRO

I am an Associate Professor, Mackenzie Investments Chair in Evidence-Based Investment Management at the DeGroote School of Business, McMaster University, Canada.

Ruizhe Jia & Agostino Capponi

DeGroote School of Business

McMaster University

NFA 2021 (virtual)

DeFi: provision of financial services without the necessary involvement of a traditional financial intermediary

blockchain

Idea:

How?

Basic idea: (great!)

Question:

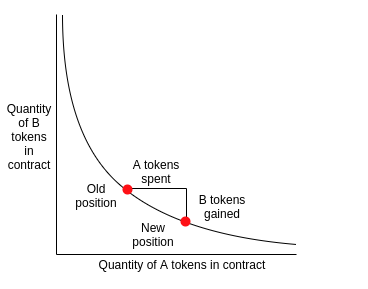

pricing mechanism:

Does/can this pricing function work?

10

10

15

6.67

Very interesting paper: cleanly & clearly drills down to the economics of swap exchanges

@katyamalinova

malinovk@mcmaster.ca

slides.com/kmalinova

https://sites.google.com/site/katyamalinova/

By Katya Malinova

NFA 2021 Discussion: The Adoption of Blockchain-based Decentralized Exchanges