Katya Malinova PRO

I am an Associate Professor, Mackenzie Investments Chair in Evidence-Based Investment Management at the DeGroote School of Business, McMaster University, Canada.

Roberto Riccó, Barbara Rindi, Duane J. Seppi

DeGroote School of Business

McMaster University

EFA 2023 Annual Meeting

Amsterdam

Sophie: V = 20.0325

has the asset

Katya: V = 20.0375

price = 20.04

price = 20.03

Gains from trade \(\checkmark\)

but: the grid is too wide

Trade @p=20.03,

fee of 0.005 on Katya, rebate 0.005 to Sophie

Trade @p=20.04

fee of 0.005 on Sophie, rebate 0.005 cent to Katya

As if trade @20.035

Sophie: V = 20.0325

has the asset

Roberto: V = 25.0375

500 price levels between 20.04 and 25.03 to trade at

No need to rebate anybody for a trade to occur

Trade occurs even for large trading fees

\(\to\) exchange rent extraction!

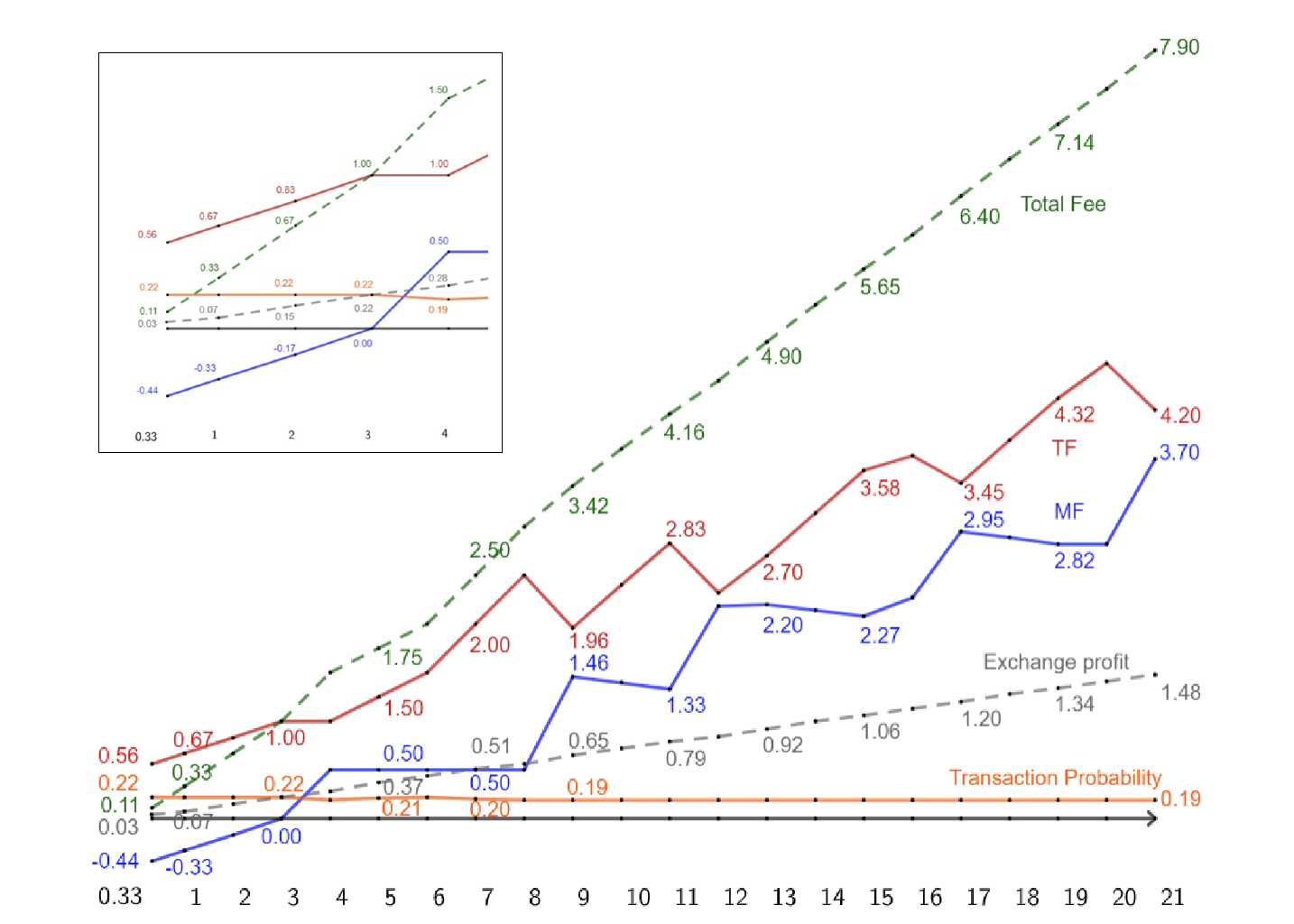

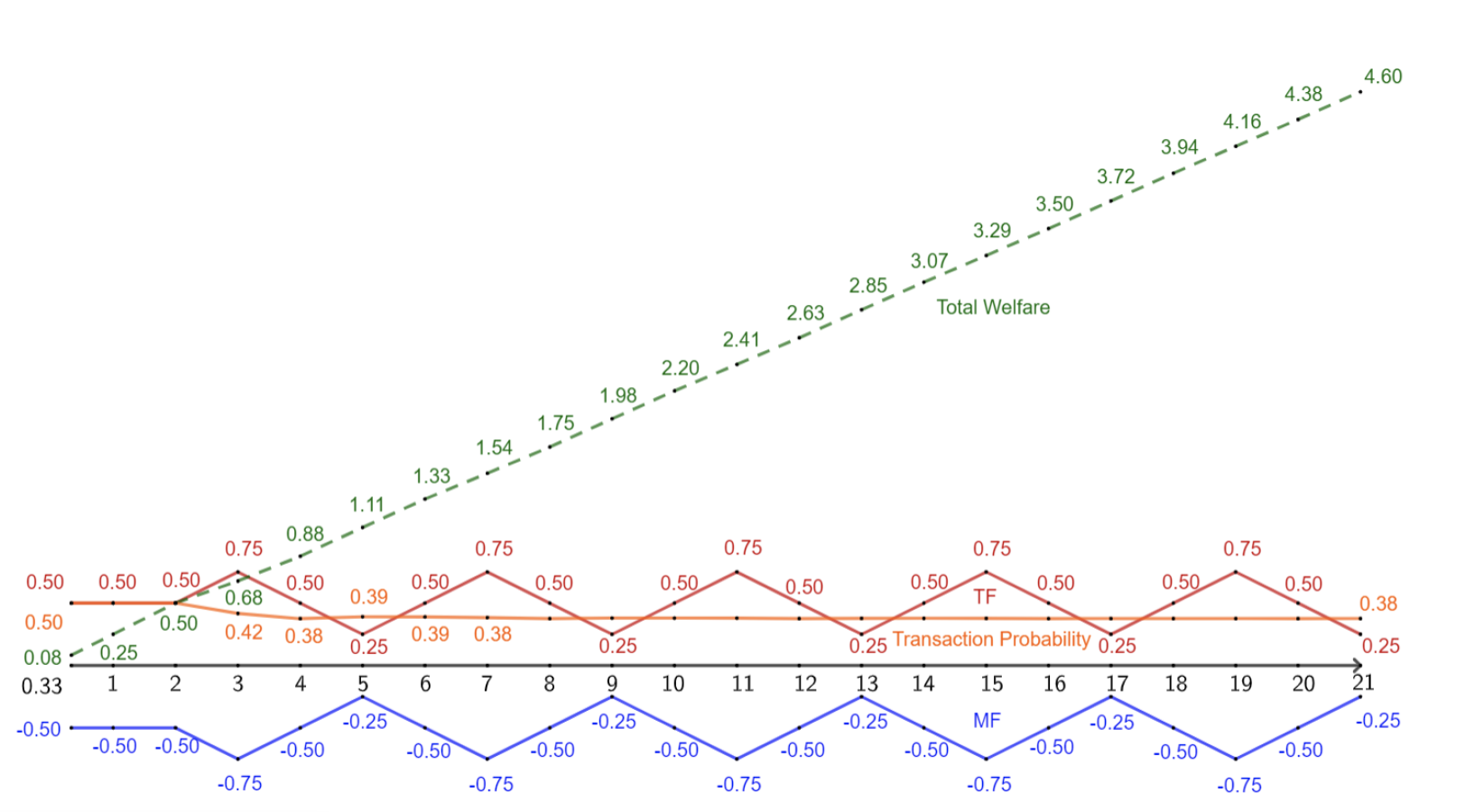

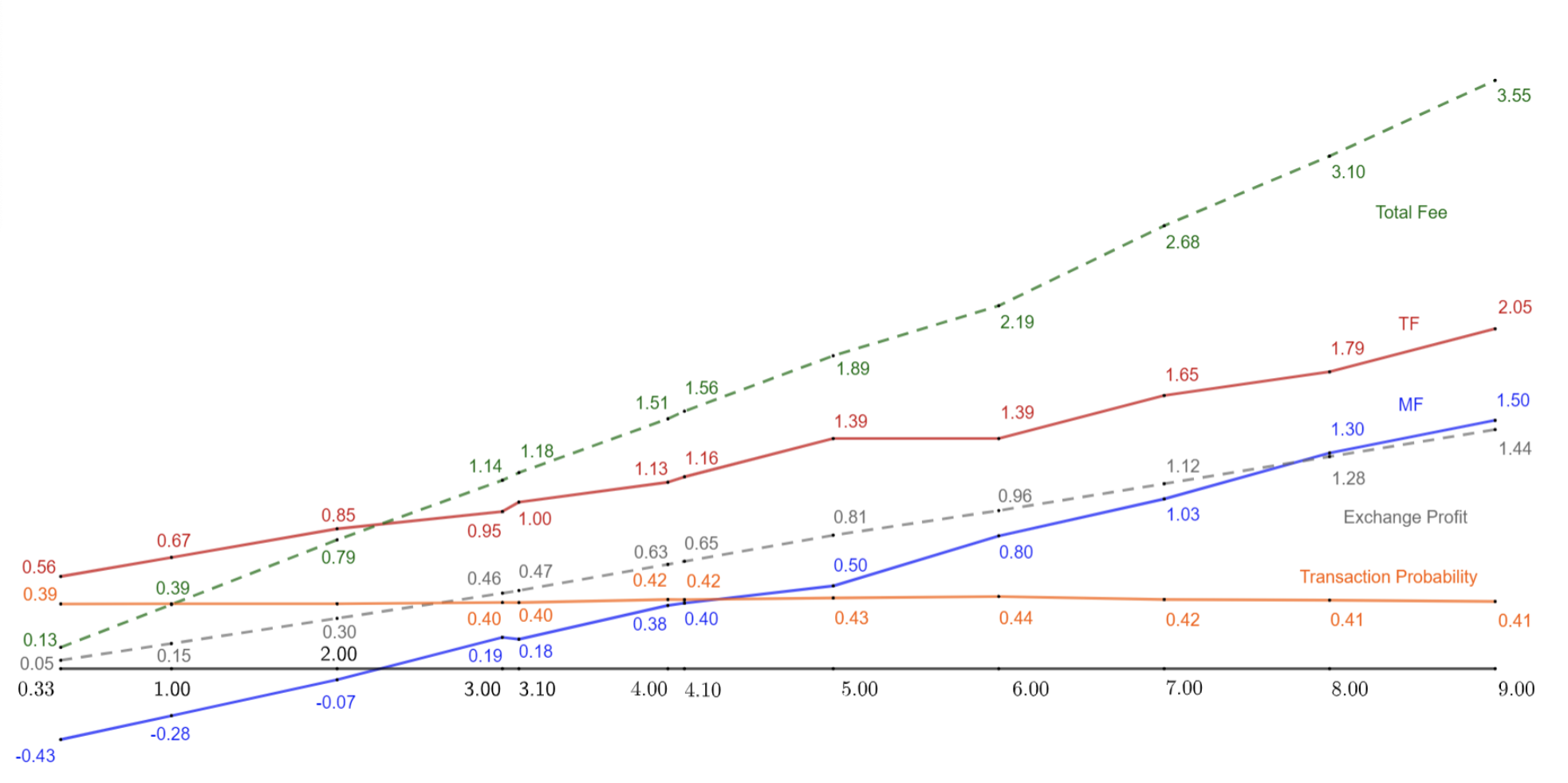

Maker + taker = total exchange fee

Taker fee

Maker fee

Exchange profit

Range of investor valuations

Rebates only for small ranges of valuations = low gains from trade

transaction probability

Fees oscillate with changes in valuation ranges:

Welfare

Taker fee

Maker fee

Set the total exchange fee to 0

Questions:

Side comment 1: model solved for limit buys (?), do the values of the optimal fees depend on this?

Side comment 2: authors interpret valuations range = "trading demand"

To me: large demand = lots of orders/frequent arrival

Question/suggestion:

Traditional approach

An alternate view

An alternate view

@katyamalinova

malinovk@mcmaster.ca

slides.com/kmalinova

https://sites.google.com/site/katyamalinova/

By Katya Malinova

EFA 2023 Discussion